Spectator Sports Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

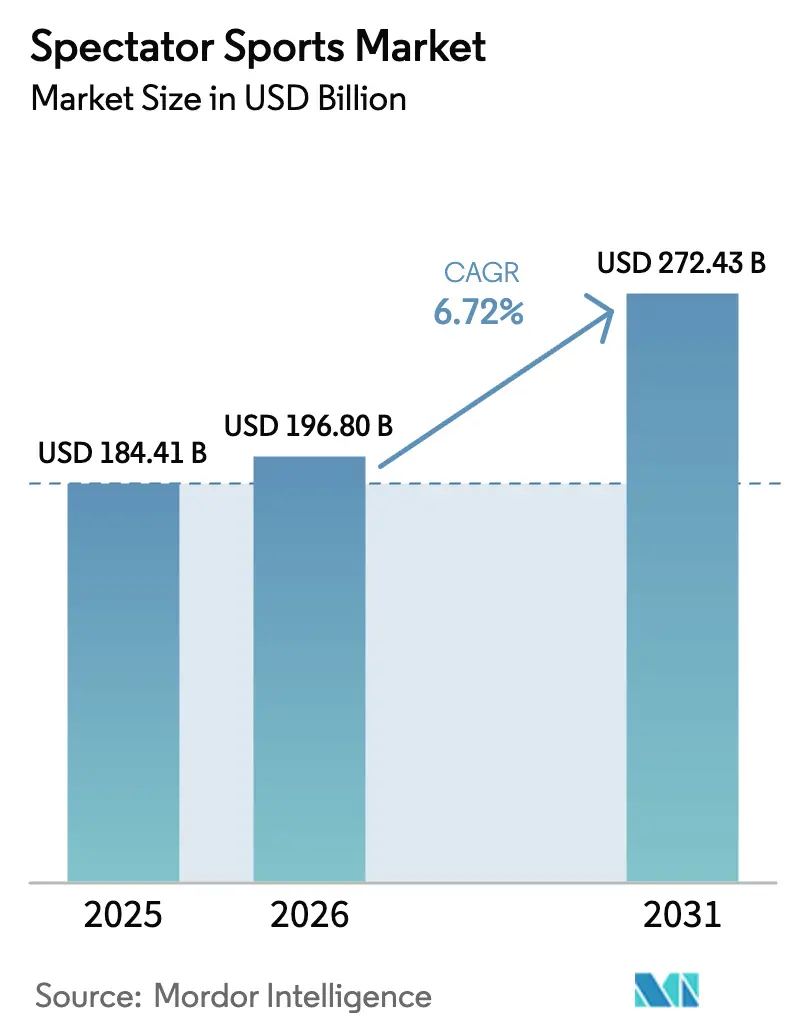

| Market Size (2026) | USD 196.8 Billion |

| Market Size (2031) | USD 272.43 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

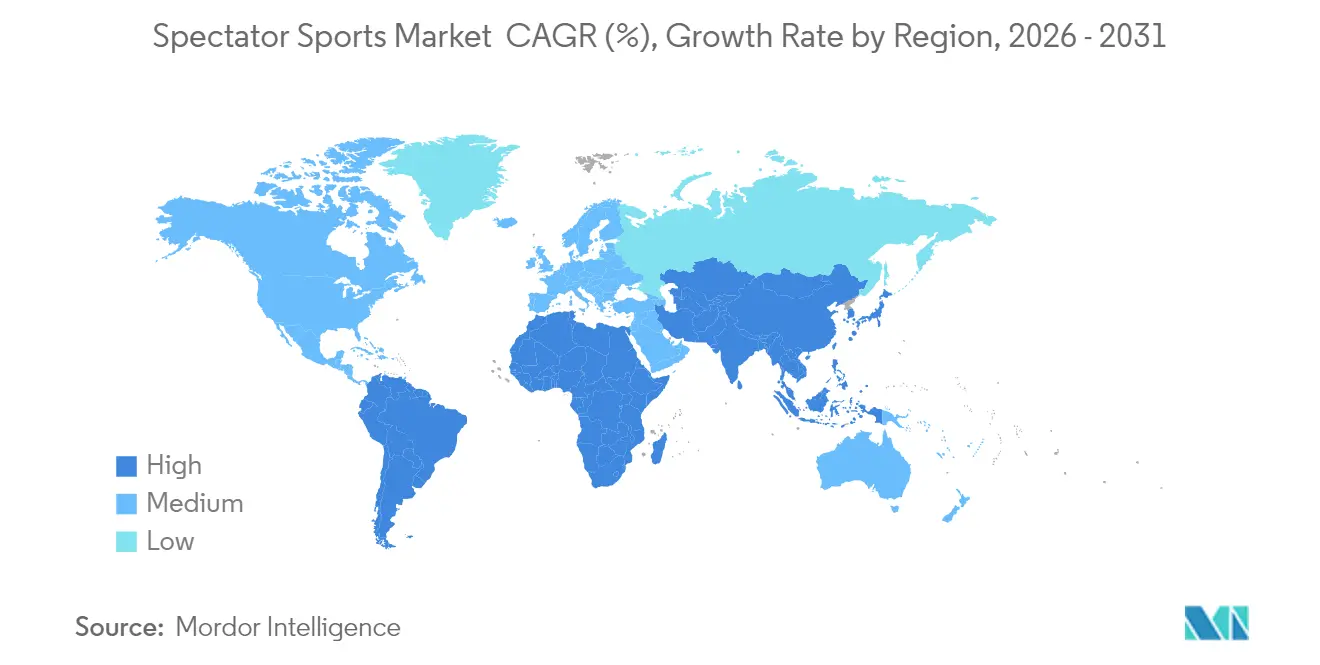

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spectator Sports Market Analysis by Mordor Intelligence

The spectator sports market size was valued at USD 184.41 billion in 2025 and estimated to grow from USD 196.8 billion in 2026 to reach USD 272.43 billion by 2031, at a CAGR of 6.72% during the forecast period (2026-2031). Expansion reflects the league-wide pivot toward direct-to-consumer streaming, the legalization of sports wagering in major economies, and the commercial rise of Asia-Pacific franchises. Live-rights bidding intensified as platforms fight subscriber churn, while legalized gambling lengthened average viewing minutes and lifted in-game advertising yields. Condensed formats such as Twenty20 cricket and indoor golf sustain younger viewers across mobile screens, and omnichannel merchandising paired with blockchain-based loyalty programs helps clubs counter rising labor costs. These cross-currents show that agility in content packaging and fan monetization keeps the spectator sports market resilient even as ticket-price inflation tests household budgets.

Key Report Takeaways

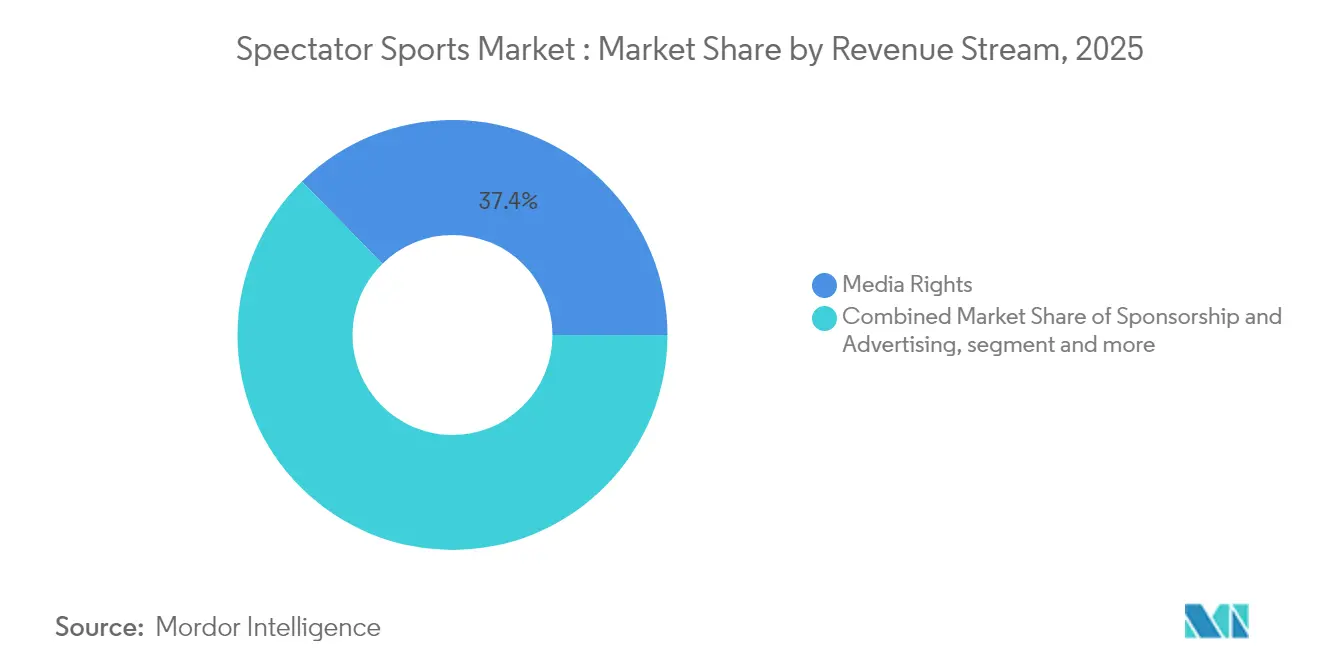

- By revenue stream, media rights captured 37.35% of the spectator sports market share in 2025, while sponsorship and advertising are projected to grow at a 6.68% CAGR through 2031.

- By sport type, football/soccer led with a 38.40% revenue share of the spectator sports market in 2025, cricket is forecast to expand at an 7.96% CAGR to 2031, driven by the Indian Premier League’s valuation surge.

- By geography, North America held 42.55% of the spectator sports market share in 2025, whereas Asia-Pacific is set to record a 7.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Spectator Sports Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising media rights valuations from streaming competition | +1.8% | Global, with concentration in North America, Europe, APAC | Medium term (2-4 years) |

| Legalization of sports betting boosting engagement | +1.2% | North America, expanding to Europe and select APAC markets | Short term (≤ 2 years) |

| Commercialization of emerging APAC leagues | +1.0% | APAC core, spill-over to MEA and Europe | Long term (≥ 4 years) |

| Blockchain-based fan tokens as revenue streams | +0.7% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| Climate-adaptive stadium designs mitigating weather risk | +0.5% | Global, with priority in climate-vulnerable regions | Long term (≥ 4 years) |

| AI-personalized viewing experiences increasing ARPU | +0.9% | Global, led by technologically advanced markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising media-rights valuations from streaming competition

Global sports-rights fees surpassed USD 60 billion in 2024, underscoring platforms’ willingness to pay premiums for live content that anchors subscriber retention [1]SportBusiness, “Global Sports Rights Values Top USD 60 Billion,” sportbusiness.com . Netflix moved into live National Football League inventory, while Amazon secured additional National Basketball Association packages, illustrating how tech giants treat sports as must-have engagement engines. YouTube TV’s NFL Sunday Ticket deal, valued at about USD 2 billion per season, signaled the end of single-platform exclusivity and raised bid floors for other marquee properties. Rights owners now stagger packages to extract multiple income streams, though viewers navigate an increasingly fragmented landscape.

Legalization of sports betting boosts engagement

The Supreme Court’s 2018 ruling accelerated wagering adoption; by early 2025, 38 U.S. states and the District of Columbia had legalized sports betting, generating handles that materially lift game-day viewership. Internal league analyses indicate that bettors exhibit higher engagement by watching games for longer durations compared to non-bettors. Additionally, gaming integrations, such as live odds tickers, are driving higher advertising premiums. The American Gaming Association estimates the NBA and MLB together could add USD 1.7 billion in annual revenue from regulated betting ecosystems [2]American Gaming Association, “Leagues’ Revenue Rises with Betting,” americangaming.org . Early data also reveal downside risk: losing wagers on a home team can dampen long-term engagement, prompting clubs to embed responsible-gaming prompts in apps.

Commercialization of emerging Asia-Pacific leagues

In 2024, the valuation of the Indian Premier League (IPL) recorded a 6.50% growth, reaching USD 16.4 billion (approximately Rs 1,34,858 crore). Live streams on JioCinema drew 620 million unique viewers in 2024, proving that data-affordable markets can eclipse linear-TV reach. Saudi Arabia's Vision 2030 strategy has directed significant financial resources toward domestic events, including securing long-term Formula 1 hosting rights. This highlights the strategic use of government funding to expedite the development and establishment of competitive leagues. Sponsors follow audience momentum, making Asia-Pacific the lead target for new franchise development through 2030.

Climate-adaptive stadium designs mitigating weather risk

Clubs adopt retractable roofs, water-harvesting systems, and renewable-energy microgrids to address weather volatility. Forest Green Rovers achieved net-zero operations using onsite solar arrays and closed-loop catering, cutting operating costs. Allianz Arena’s rainwater-capture program provides all of the pitch-irrigation needs, lowering utility bills and securing eco-label sponsorships. Crowd-density sensors feed real-time evacuation algorithms, improving insurer risk ratings. Digital ticketing and cash-free concessions reduce queuing times, pushing per-capita spend higher without expanding the footprint.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating player salary inflation compressing margins | -1.4% | Global, most pronounced in North America and Europe | Short term (≤ 2 years) |

| Macroeconomic pressure on discretionary event spend | -0.9% | Global, with varying intensity by economic conditions | Medium term (2-4 years) |

| Cyber-security threats to live-streaming stability | -0.6% | Global, particularly affecting digital-first markets | Short term (≤ 2 years) |

| Regulatory curbs on gambling advertisements | -0.5% | Europe, Australia, expanding to other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating player salary inflation is compressing margins

The National Basketball Association's salary cap for the 2024-25 season rose to USD 140.6 million, reflecting the league's sustained revenue growth and financial expansion [3]Sportico, “Salary-Cap Projection,” sportico.com . Collective-bargaining agreements mandate that approximately 50% of basketball-related income is allocated to players, which imposes financial pressures on team ownership due to escalating fixed costs. In parallel, the Premier League experienced a 10% year-over-year increase in wage bills in 2024, driven by higher revenues from Champions League broadcasting rights. To address the challenges of shrinking operating margins, clubs are strategically channeling resources into youth academy development to cultivate homegrown talent and reduce reliance on expensive transfers. Furthermore, they are focusing on expanding premium hospitality offerings to diversify income streams and improve overall profitability.

Cybersecurity threats to live-stream stability

As over-the-top distribution replaces linear feeds, piracy and denial-of-service attacks proliferate. Major League Baseball and the Premier League collaborated with Internet-service providers to block illegal streams within 15 minutes of detection, reducing unauthorized viewership. Broadcasters now embed forensic watermarks and zero-trust edge nodes to harden streaming stacks, but smaller rights holders struggle to absorb soaring security spend. Consumer backlash after high-profile outages pushes regulators to draft minimum-uptime standards for live events.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Revenue Stream: Media-rights dominance amid digital transformation

In 2025, media-rights revenues contributed 37.35% to the overall spectator sports market income, solidifying their position as a critical revenue driver. This growth is attributed to the increasing shift of cord-cutters toward platform bundles that prioritize live sports as high-value content. Sponsorship and advertising are projected to achieve a compound annual growth rate (CAGR) of 6.68% through 2031, supported by advancements in granular fan-data targeting and the integration of augmented-reality features within applications. In contrast, ticketing revenue growth is expected to lag behind inflation, as consumers increasingly favor premium, one-time experiences over frequent attendance. These trends highlight the evolving consumer preferences and the strategic focus on maximizing revenue streams within the spectator sports market.Merchandising is witnessing renewed momentum, driven by the adoption of rapid-print fulfillment centers that enable the on-demand production of customized jerseys within stadium premises.

This approach minimizes inventory risks and enhances operational efficiency by reducing stock obsolescence. Ancillary digital revenue streams, such as fan tokens and AI-powered content personalization subscriptions, are emerging as significant contributors to the market's growth. These innovations reflect the increasing monetization of data and the integration of technology to enhance fan engagement. Collectively, these developments underscore the expanding role of digital transformation in shaping the future trajectory of the spectator sports market.

By Sport Type: Cricket’s rapid ascent reshapes hierarchies

In 2025, football/soccer maintained its leadership position in the spectator sports market, capturing 38.40% of the market share due to its extensive global broadcast network. The sport's robust club ecosystems and deeply ingrained cultural significance further solidified its dominance. Cricket, however, is emerging as a high-growth segment, with an anticipated CAGR of 7.96%, driven by the Indian Premier League's (IPL) valuation of USD 16 billion. The expansion of the Twenty20 format, which aligns with the increasing demand for short-form, engaging content, is a key growth driver. These factors collectively position cricket as a dynamic force within the evolving spectator sports market.Baseball, facing stagnant national ratings, has implemented rule modifications such as pitch clocks to address concerns over game pacing.

These adjustments aim to enhance the viewing experience and sustain audience interest in a competitive market. Motorsports, on the other hand, are leveraging innovative strategies like city-center night races to attract younger demographics. Additionally, sponsorships from Gulf sovereign entities are enabling motorsports to expand their geographic reach and diversify their audience base. Together, these efforts are reshaping the spectator sports market by addressing shifting consumer preferences and regional growth opportunities.

Geography Analysis

North America, accounting for 42.55% spectator sports market share in 2025, benefits from entrenched franchise structures, high media-rights baselines, and mature stadium ecosystems. Streaming competition intensified when YouTube TV secured NFL Sunday Ticket, prompting incumbents to bundle multi-sport packages and parity-price mobile-only passes. Climate-neutral retrofits, including solar canopies and waste-heat recovery systems, attract municipal co-funding and ESG-minded sponsors, adding resilience to the spectator sports market.

Asia-Pacific registers the fastest 7.39% CAGR through 2031, led by India’s target to scale its sports sector to USD 100 billion by 2027. The IPL streamed in eight languages and generated peak concurrency records on JioCinema, validating segmented-audience strategies. Japan pioneers mixed-reality signage and elder-friendly amenities, while South Korea’s esports heritage feeds cross-promotion into traditional leagues. Australia’s proposed ad ban presses broadcasters to diversify partner portfolios, but domestic women’s football successes drive grassroots participation. Southeast Asian federations leverage modular venues and public-private partnerships to host multisport events with lower capital risk, broadening spectator sports market penetration.

Europe delivers consistent revenue through legacy football, rugby, and cycling, though regulatory shifts on gambling ads create short-term sponsorship gaps. Cross-border over-the-top subscriptions hedge domestic saturation; Bundesliga’s new match windows add Asia-Pacific prime-time slots, widening audience reach. Africa remains an expansion frontier: Nigeria’s youth population, mobile-first payments, and diaspora networks create a test bed for low-bandwidth live-stream models that bypass traditional infrastructure.

Mordor Intelligence provides coverage of the spectator sports market across other key regional markets, including Asia, Europe, and North America, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to India and United Kingdom incorporating local coverage and market participation, as required.

Competitive Landscape

The spectator sports market exhibits a fragmented structure, with the top five players collectively generating a substantial portion of the revenue, resulting in a significant concentration score. Traditional media conglomerates integrated vertically: TKO Group completed a USD 3.25 billion acquisition of IMG, On Location, and Professional Bull Riders, adding event operations and hospitality to its WWE and UFC content stable [4]Business Wire, “TKO Group Completes IMG Acquisition,” businesswire.com . Technology-first entrants such as Amazon fuse streaming, e-commerce, and cloud analytics, creating moats that cross-sell Prime benefits. Clubs roll out on-demand jersey printing and predictive pricing to maximize game-day yield while dampening inventory write-offs.

Intellectual-property stewardship drives differentiation: Nike extended exclusive uniform deals with both the NBA (to 2037) and NFL (to 2038), locking in apparel visibility across physical and digital worlds. Data-rights negotiations intensify as leagues weigh selling anonymized player-tracking feeds to third-party analytics firms. Cybersecurity readiness becomes a competitive edge; operators with zero-trust streaming stacks record 35% faster post-outage recovery times, boosting fan loyalty metrics. Sovereign wealth and private-equity funds aim at youth-sports academies, health-tech tie-ins, and multi-use arenas, betting that diversified asset clusters insulate returns against single-league volatility within the spectator sports market.

Spectator Sports Industry Leaders

The Walt Disney Company (ESPN)

Comcast Corp (NBC Sports & Sky Sports)

Liberty Media Corp (Formula 1)

DAZN Group Ltd

Madison Square Garden Sports Corp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: TKO Group closed its USD 3.25 billion acquisition of IMG, On Location, and Professional Bull Riders, expanding annual events beyond 200 and extending reach to 285 million households.

- January 2025: ESPN, Fox, and Warner Bros. Discovery created a joint venture to introduce a streaming sports bundle aimed at cord-cutting audiences.

- December 2024: Nike renewed its partnership with the NFL through 2038, recommitting to uniform supply for all 32 teams.

- October 2024: Nike signed a 12-year extension with the NBA, WNBA, and NBA G League, securing uniform exclusivity through 2037.

Global Spectator Sports Market Report Scope

A spectator sport is a sport that is characterized by the presence of spectators or watchers. Spectator sports may be professional sports or amateur sports. Spectator sports refers to sporting events that attract viewers watching through different modes of online channels and offline (stadiums). These sporting events charge fees to the viewers of the events for watching the events through entry tickets or subscriptions to digital channels.

The spectator sports market is segmented by sports (badminton, baseball, basketball, cricket, cycling, hockey, and other sports), by revenue source (tickets, media rights, sponsorships, and merchandising), and by region (North America, Europe, Asia Pacific, South America, Middle East & Africa, and Rest of World).

The report offers market size and forecasts in value (USD) for all the above segments.

| Ticket Sales |

| Media Rights |

| Sponsorship & Advertising |

| Merchandising & Licensing |

| Other Ancillary Revenues |

| Football / Soccer |

| Basketball |

| Baseball |

| Cricket |

| Motorsports |

| Tennis |

| Golf |

| Other Sports |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Revenue Stream | Ticket Sales | |

| Media Rights | ||

| Sponsorship & Advertising | ||

| Merchandising & Licensing | ||

| Other Ancillary Revenues | ||

| By Sport Type | Football / Soccer | |

| Basketball | ||

| Baseball | ||

| Cricket | ||

| Motorsports | ||

| Tennis | ||

| Golf | ||

| Other Sports | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the spectator sports market?

The spectator sports market is valued at USD 196.8 billion in 2026 and is projected to reach USD 272.43 billion by 2031.

Which revenue stream contributes the most to industry earnings?

Media rights dominate with 37.35% of revenue in 2025, reflecting sustained demand for exclusive live content.

Why is cricket the fastest-growing sport type?

Cricket benefits from the Indian Premier League’s digital-first model, which supports an 7.96% CAGR forecast through 2031.

Which region shows the highest growth potential?

Asia Pacific is expected to grow at 7.39% CAGR to 2031, thanks to India’s rapid industry expansion and rising digital viewership.

How do blockchain fan tokens generate new revenue?

Token issuances provide upfront cash and grant fans voting rights on team matters; FC Barcelona sold USD 1.3 million worth in two hours.

What recent mergers are reshaping the landscape?

TKO Group’s USD 3.25 billion acquisition of IMG, On Location, and Professional Bull Riders broadened its live-event portfolio in 2025.

Page last updated on: