Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

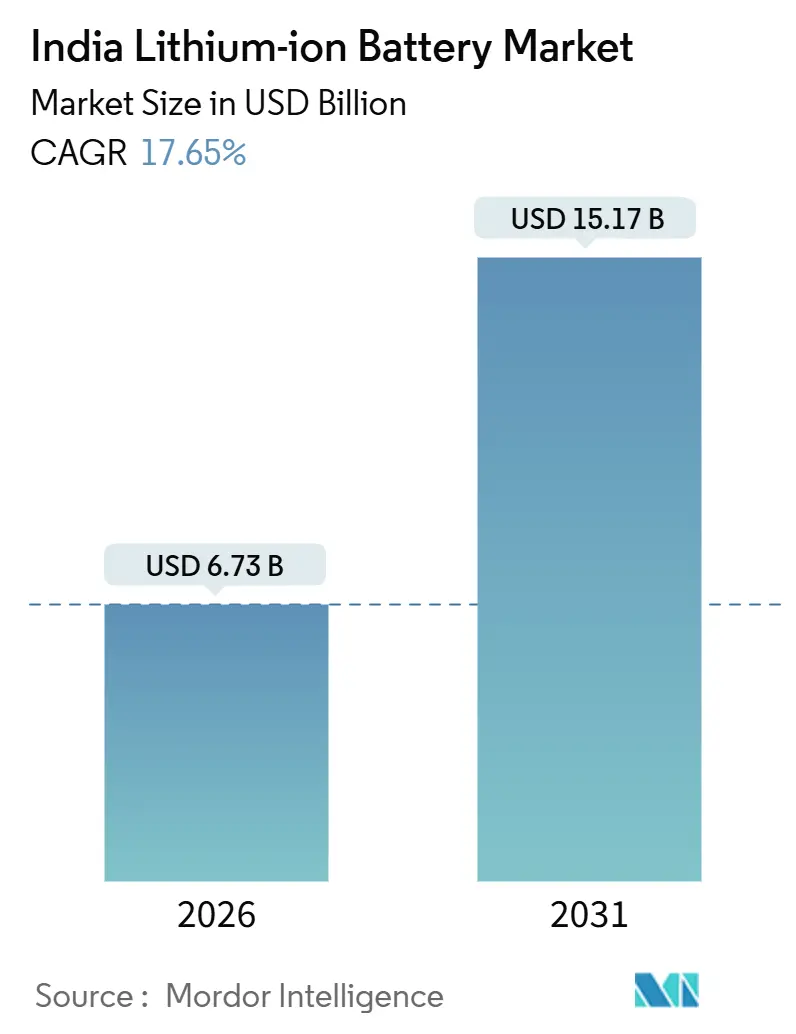

| Market Size (2026) | USD 6.73 Billion |

| Market Size (2031) | USD 15.17 Billion |

| Growth Rate (2026 - 2031) | 17.65% CAGR |

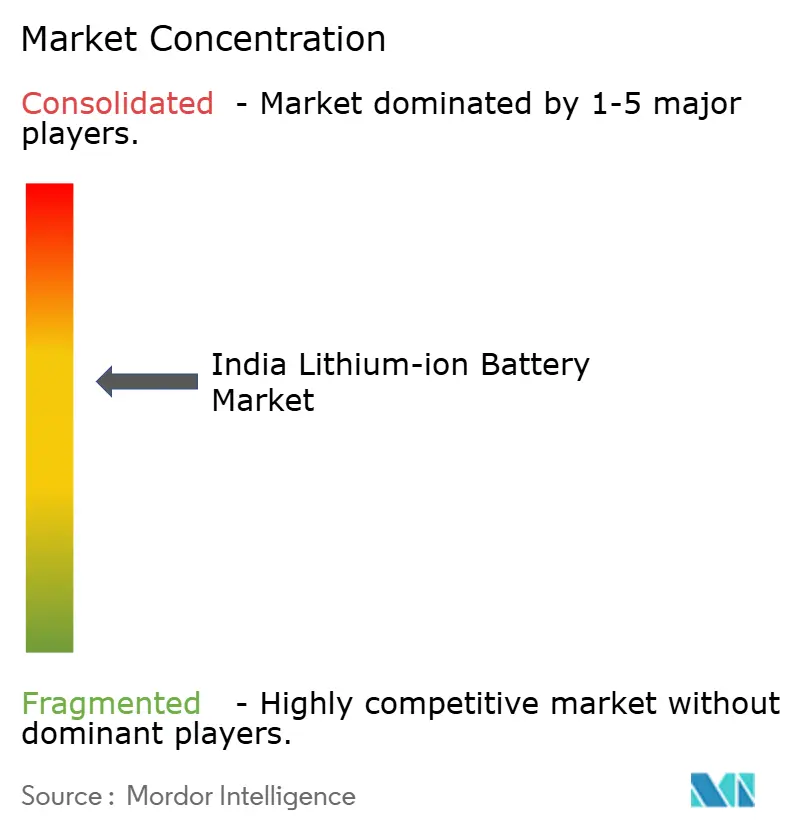

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Lithium-ion Battery Market Analysis by Mordor Intelligence

The India Lithium-ion Battery Market size is estimated at USD 6.73 billion in 2026, and is expected to reach USD 15.17 billion by 2031, at a CAGR of 17.65% during the forecast period (2026-2031).

This steep growth trajectory is rooted in strong policy incentives, accelerating localization of cell production, and a dramatic shift in mobility and energy-storage economics. FAME-II subsidies trimmed upfront prices of electric two-wheelers and buses by up to 30%, pushing electric models to 48% of new two-wheeler sales in India’s largest cities.[1]Press Information Bureau, “FAME-II Achievements,” pib.gov.in At the supply side, the Production-Linked Incentive (PLI) scheme committed INR 18,100 crore (USD 2.17 billion) to 11 cell makers, cutting the landed-cost gap with imported cells to less than 5%.[2]Ministry of Heavy Industries, “Advanced Chemistry Cell PLI Awards,” heavyindustries.gov.in Parallel grid-scale energy-storage auctions from SECI and NTPC are anchoring long-term demand, while corporate renewable power-purchase agreements bundled with storage have pushed levelized storage costs below INR 5 per kWh in 2025. Intensifying domestic competition, backed by aggressive capital expenditure, is expected to unlock cost reductions that favorably reshape the India lithium-ion battery market through the decade.

Key Report Takeaways

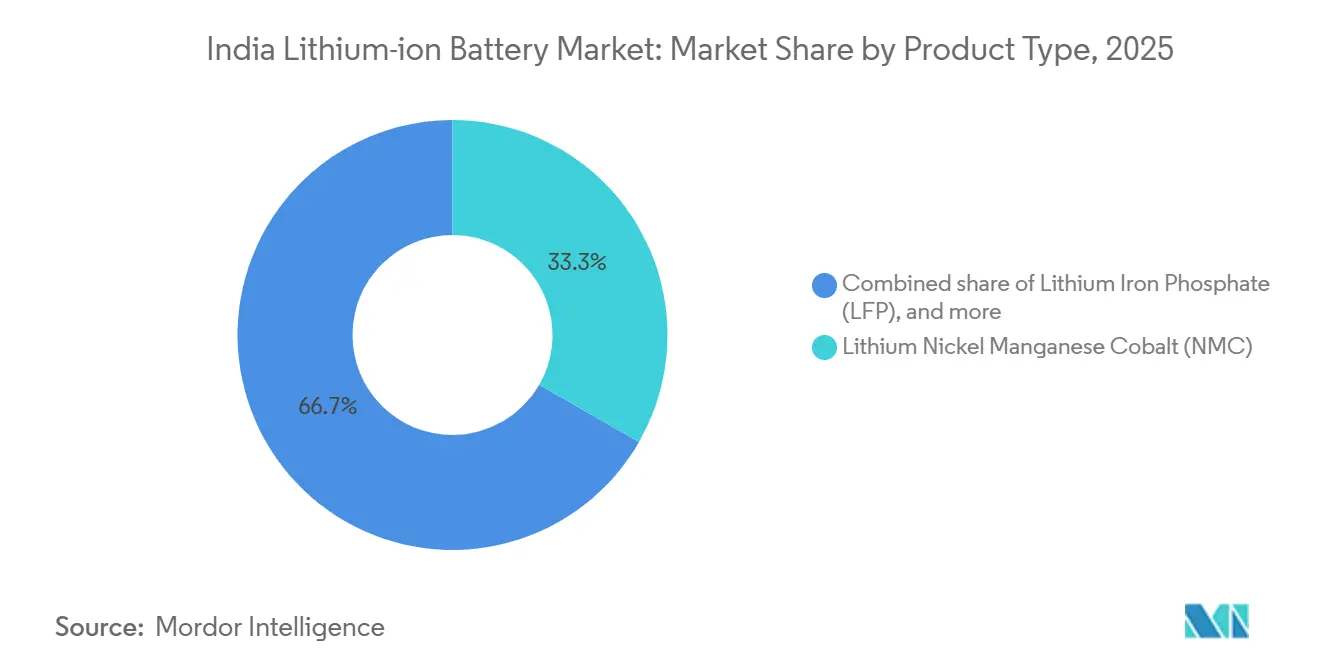

- By chemistry, Lithium Nickel Manganese Cobalt (NMC) retained 33.3% revenue share in 2025, while Lithium Iron Phosphate (LFP) is projected to expand at a 27.1% CAGR to 2031.

- By form factor, cylindrical cells held 55.8% of India's lithium-ion battery market share in 2025; pouch cells exhibit the fastest projected CAGR at 24.3% through 2031.

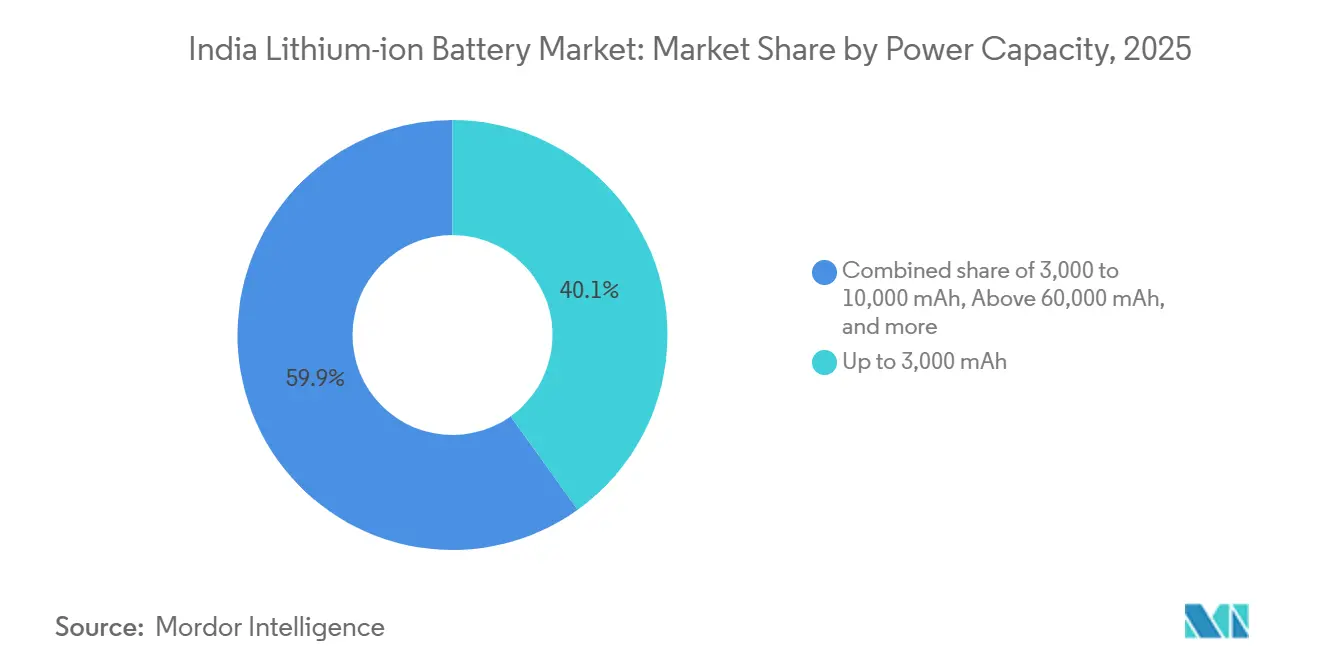

- By power capacity, the up-to-3,000 mAh bracket led with 40.1% contribution to the India lithium-ion battery market size in 2025; the above-60,000 mAh segment is forecast to surge at a 28.5% CAGR between 2026 and 2031.

- By end-use industry, consumer electronics commanded 35.5% of demand in 2025; automotive applications are advancing at a 25.9% CAGR and are on track to become the largest segment by 2029.

- Ola Electric, Exide Industries, Amara Raja, LG Energy Solution, and Reliance New Energy collectively accounted for roughly 48% of domestic cell capacity commitments in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Lithium-ion Battery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining lithium-ion battery cost curve acceleration | +3.2% | National, with early gains in Maharashtra, Tamil Nadu, Gujarat | Medium term (2-4 years) |

| Government FAME-II subsidies and PLI schemes | +4.8% | National, concentrated in urban centers and PLI-designated manufacturing zones | Short term (≤ 2 years) |

| Electric two-wheeler boom in urban mobility | +3.9% | Urban India, led by Tier-1 and Tier-2 cities | Short term (≤ 2 years) |

| Grid-scale energy-storage tenders by SECI & NTPC | +2.1% | National, with project clusters in Rajasthan, Gujarat, Karnataka | Medium term (2-4 years) |

| Localization of cell manufacturing under Atmanirbhar Bharat | +2.6% | Manufacturing hubs in Tamil Nadu, Gujarat, Maharashtra, Karnataka | Long term (≥ 4 years) |

| Corporate renewable + storage PPAs in C&I segment | +1.5% | Industrial corridors in Gujarat, Maharashtra, Andhra Pradesh | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Declining Lithium-ion Battery Cost Curve Acceleration

Battery-pack prices in India fell to USD 115 per kWh in 2025 from USD 132 per kWh a year earlier as raw-material prices cooled and domestic scale improved. By early 2026, locally produced NMC cells cost USD 95 per kWh, almost matching imported Chinese equivalents once freight and GST are added. This rapid deflation is tipping total-cost-of-ownership equations in favor of electric two- and three-wheelers, where price sensitivity is high. LFP, representing 22% of 2025 demand, offers an 18-22% bill-of-materials discount over NMC, though its energy density is roughly 15-20% lower. Cost parity is also enabling 4-hour stationary systems to undercut diesel gensets on levelized cost in commercial buildings, a milestone crossed in 2025.

Government FAME-II Subsidies and PLI Schemes

The government disbursed INR 7,500 crore (USD 900 million) in FAME-II incentives by March 2025, underwriting 1.2 million electric two-wheelers and 18,000 e-buses and slicing sticker prices by 25-30%. Extension through March 2027 locks in demand visibility, helping OEMs align with phased manufacturing mandates. Complementing demand pull, the ACC-PLI program earmarked INR 18,100 crore (USD 2.17 billion) to catalyze 50 GWh of domestic capacity by 2030. Reliance New Energy’s 10 GWh Jamnagar plant and Ola Electric’s 20 GWh Tamil Nadu gigafactory headline the beneficiaries, each capturing more than INR 2,900 crore (USD 350 million) in incentives. The 20% value-addition subsidy during the first five years compresses the landed-cost gap with imports to below 5%, galvanizing localization decisions by major OEMs.

Electric Two-Wheeler Boom in Urban Mobility

Electric two-wheelers seized 48% of all two-wheeler sales across India’s top 10 cities in 2025, up from 38% in 2024. Ola Electric, Ather Energy, and TVS Motor sold a combined 1.8 million e-scooters, each packing 2.5–4 kWh NMC batteries that deliver 100–150 km real-world range. While high-nickel cathodes fuel urban models, limited public charging in Tier-2 and Tier-3 cities still restrains inter-city adoption, underscoring infrastructure gaps highlighted by the Ministry of Power. Elevated demand for cylindrical 21700 cells mirrors the segment’s preference for thermally benign pack architectures that can be rapidly assembled at scale.

Grid-Scale Energy-Storage Tenders by SECI & NTPC

SECI awarded 4 GWh of BESS contracts in 2025 at an average tariff of INR 4.8 per kWh (USD 0.058) for two-hour LFP systems in Rajasthan and Gujarat. In January 2026, NTPC floated the nation’s first 10-year performance-linked tender covering 2 GWh, signaling a pivot from capex to lifecycle-cost metrics. Reliability clauses favor LFP cells rated for 6,000+ cycles, nudging domestic manufacturers toward iron-phosphate cathode lines. With a 12 GWh pipeline through 2027, utility bids are triggering second-life opportunities as retired EV packs are repurposed, although regulatory clarity for reuse remains nascent under the Ministry of Power.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical-mineral import dependence | -2.8% | National, affecting all manufacturing clusters | Long term (≥ 4 years) |

| Under-developed battery-recycling ecosystem | -1.4% | National, with acute gaps in collection logistics | Medium term (2-4 years) |

| High GST differential on cells vs. packs | -1.2% | National, impacting domestic cell manufacturers | Short term (≤ 2 years) |

| Safety & fire incidents eroding consumer confidence | -1.6% | Urban centers, particularly in two-wheeler and e-rickshaw segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Critical-Mineral Import Dependence

India imported 18,200 t of lithium compounds worth USD 1.2 billion in 2025, with 68% dependent on China and 24% on Chile.[3]Ministry of Mines, “Critical Minerals Strategy,” mines.gov.in Cobalt shipments of 4,800 t arrived almost exclusively via Chinese refineries sourcing from the Democratic Republic of Congo, exposing a single-node risk for NMC supply. Although exploratory finds in Karnataka’s Mandya district indicate 14,100 t lithium oxide equivalent, commercial extraction is unlikely before 2028. The Critical Mineral Mission has earmarked INR 2,500 crore (USD 300 million) for overseas mine stakes, yet until operational, cell manufacturers will continue to hedge by stockpiling three-month inventories, inflating working-capital cycles.

Under-Developed Battery-Recycling Ecosystem

National recycling capacity reached only 12,000 t pa in 2025, equal to processing 8% of end-of-life packs.[4]Central Pollution Control Board, “Battery Waste Management Review,” cpcb.nic.in Extended producer responsibility rules delivered just 22% compliance due to patchy enforcement, leaving informal channels to handle most returned batteries. Hydrometallurgical plants need a 25,000 t pa break-even scale, yet Attero Recycling and Lohum Cleantech together processed only 8,400 t in 2025. Lithium carbonate recovered via recycling costs USD 18 per kg, roughly 30% above virgin imports, discouraging uptake. Absence of a rural reverse-logistics network deepens the problem as 38% of electric two-wheelers now sell beyond metro areas.

Segment Analysis

By Product Type: LFP Gains on NMC’s Dominance

India's lithium-ion battery market size for NMC chemistry was USD 1.87 billion in 2025, equal to a 33.3% share. LFP's superior cycle life and cobalt-free design underpin its forecast 27.1% CAGR, propelling it to near-parity with NMC by 2031, especially in stationary storage and commercial EVs. Exide Industries and Ola Electric both aim to shift 60% of sourcing to LFP by 2027. Although NMC retains an edge in premium passenger cars demanding 400 km+ range, stricter thermal-propagation tests under AIS-156 tilt mass-market models toward LFP. Minor chemistries like LTO and LMO will remain niche, serving public buses and power tools where rapid charging and temperature resilience override energy density.

India's lithium-ion battery market share for LFP is projected to close the gap as SECI and NTPC tenders mandate iron-phosphate chemistry for safety and lifecycle reasons. Consumer-electronics OEMs still prefer high-density NMC and LCO cells, but rising smartphone battery capacities are gradually cannibalizing LCO volumes. Panasonic Energy's small NCA niche supplies luxury EVs, yet volumes stay marginal due to cost and supply-risk issues.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form Factor: Pouch Cells Challenge Cylindrical Hegemony

Cylindrical formats generated USD 3.13 billion of the India lithium-ion battery market size in 2025, equal to 55.8% share, reflecting deep legacy supply chains and automated assembly lines. The 21700 cell, widely used by Ather and Ola, delivers 35% more energy than 18650, lowering per-kWh pack cost by 8–10%. Pouch cells, while only 16.2% share now, are forecast to grow 24.3% CAGR as skateboard EV platforms demand thin, high-utilization modules. LG Energy Solution’s 5 GWh Pune plant, due in 2026, will feed this trend with 250 Wh/kg NMC pouches.

Thermal-expansion risks in India’s 45 °C summers necessitate enhanced cooling, adding USD 20-30 per kWh to pouch-pack costs, but weight savings of 12-18% are compelling for two-wheeler OEMs chasing sub-100 kg designs. Prismatic cells dominate stationary storage as they simplify racking and BMS integration, despite an 8–12% cost premium. BYD’s blade battery technology is under evaluation by Indian bus OEMs for structural integration benefits.

By Power Capacity: Large-Format Cells Accelerate

Cells up to 3,000 mAh held 40.1% of India's lithium-ion battery market share in 2025, thanks to the 180 million smartphones shipped every year. Larger above-60,000 mAh formats will post a 28.5% CAGR through 2031 as OEMs shift to large prismatic modules that lower assembly labor by nearly one-third. Exide's 12 GWh Bengaluru plant will prioritize these large-format cells, aligning with the phased manufacturing requirement for 60% domestic value addition by 2027.

Mid-range 10,000–60,000 mAh cells, used in e-rickshaws and light commercial vehicles, face price pressure from Chinese imports that undercut domestic offers by 15–20% even after the GST differential. As carmakers migrate to 100,000 mAh modules, economies of scale in coating and formation are expected to trim per-kWh costs by another 15% by 2028.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-Use Industry: Automotive Overtakes Consumer Electronics

Consumer electronics consumed 35.5% of shipments in 2025, but automotive demand is set to dominate by 2029, expanding at a 25.9% CAGR as two-wheeler electrification spreads from Tier-1 cities to peri-urban districts. Passenger EV sales tripled to 120,000 units in 2025, each carrying 30–50 kWh packs that dwarf phone batteries in material terms. The India lithium-ion battery market size for stationary storage reached USD 1.01 billion in 2025 and is the fastest-growing non-mobility application thanks to tender-led visibility.

Industrial power tools, at 12% share, continue migrating from nickel-cadmium to lithium-ion as OEMs chase 40% weight savings. Aerospace and defense volumes remain niche but lucrative, with Bharat Electronics shipping LTO packs that meet MIL-STD-810 vibration requirements. Marine applications such as Kerala’s 500 kWh ferry demonstrate untapped potential as inland waterways modernize.

Geography Analysis

Tamil Nadu, Gujarat, and Maharashtra together host 72% of announced cell capacity, underpinning regional specialization within the India lithium-ion battery market. Tamil Nadu’s Krishnagiri district houses Ola Electric’s 20 GWh gigafactory, backed by a 15% capital subsidy capped at INR 150 crore. Proximity to Chennai and Bengaluru EV assembly plants and streamlined port logistics shorten raw-material lead times. Gujarat’s Jamnagar cluster, led by Reliance New Energy’s 10 GWh project, benefits from renewable-energy surpluses that shave formation-stage electricity costs by up to 20%.

Maharashtra leverages industrial infrastructure and skilled labor, anchoring Exide’s 12 GWh Chakan site and Amara Raja’s 16 GWh Pune plan, both eligible for state-level fiscal incentives. Karnataka is carving a recycling and second-life niche, with Attero Recycling’s 18,000 t pa hydrometallurgical plant in Bengaluru reclaiming 92-95% of metals from spent packs. Rajasthan and Gujarat dominate grid-scale storage demand, hosting 68% of SECI-awarded BESS capacity, thanks to high solar output and network congestion. The diffusion of electric two-wheelers into Tier-2 and Tier-3 cities creates logistics challenges for battery-swapping networks, a gap Sun Mobility addresses via 9 kWh LFP swap stations now spanning eight cities.

Competitive Landscape

India’s lithium-ion battery arena is moderately fragmented, with the top five players controlling roughly 48% of committed domestic capacity. Vertically integrated challengers like Ola Electric and Reliance New Energy seek to internalize cell output, using PLI incentives to insulate supply and capture margin, whereas traditional lead-acid leaders Exide and Amara Raja pivot via technology partnerships with Leclanché and others. LG Energy Solution’s 5 GWh Pune entry signals that global majors prefer localized production to bypass GST headwinds.

Value-chain whitespaces persist in battery-management systems (BMS) and thermal solutions. Inverted Energy’s cloud-connected BMS, rolled out in 45,000 electric three-wheelers, commands a 12–15% premium by offering predictive maintenance. Process innovation is also underway: Tata AutoComp’s dry-electrode coating line in Chennai trimmed solvent use by 85%, reducing cell costs by 8–10%. Stricter AIS-156 Amendment 3 mandates heightened compliance requirements, favoring players with in-house safety labs and pushing smaller assemblers toward consolidation. International cell giants eye joint ventures as an entry wedge, but technology transfer terms remain tight amid IP-protection concerns.

India Lithium-ion Battery Industry Leaders

TDS Lithium-Ion Battery Gujarat Pvt. Ltd.

Nexcharge (Exide & Leclanché)

Amperex Technology Ltd. (ATL)

Exicom Tele-Systems Ltd.

Okaya Power Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: Waaree Energy Storage Solutions secured INR 1,003 crore (USD 111 million) to bolster the establishment of a 20 GWh lithium-ion cell and battery pack manufacturing plant.

- January 2026: Servotech Renewable Power System Ltd. has made its debut in the electric three-wheeler market, unveiling a lithium-ion battery alongside a specialized charger. The newly introduced SULTAN lithium-ion battery comes in two configurations: 51.2V/105Ah and 64V/105Ah, catering specifically to e-rickshaws, e-autos, and e-cargo vehicles.

- September 2025: India has launched its inaugural advanced lithium-ion battery plant in Haryana. This facility is poised to meet roughly 40% of the country's battery demand, enhancing India's self-reliance in electronics. The plant's output will cater to electric vehicles (EVs), consumer electronics, and energy storage solutions, all while fortifying local supply chains.

- June 2025: India's inaugural lithium-ion battery production has been unveiled by Boson Cell, debuting the 18350 B-30A and 21700 B-50A cells tailored for drones, electric vehicles, and renewable energy applications.

India Lithium-ion Battery Market Report Scope

A lithium-ion battery is a rechargeable battery that consists of an anode, cathode, and electrolyte. Different types of anode and cathode materials give designers the flexibility to design batteries depending on their applications. Lithium-ion batteries are preferred over other batteries mainly due to their high energy density.

The India lithium-ion battery market is segmented by product type, form factor, power capacity, end-user industry, and geography. By product type, the market is segmented into lithium cobalt oxide (LCO), lithium iron phosphate (LFP), lithium nickel manganese cobalt (NMC), lithium nickel cobalt aluminium (NCA), lithium manganese oxide (LMO), and lithium titanate (LTO). By form factor, the market is segmented into cylindrical, prismatic, and pouch. By power capacity, the market is segmented into up to 3,000 mAh, 3,000 to 10,000 mAh, 10,000 to 60,000 mAh, and above 60,000 mAh. By end-user industry, the market is segmented into automotive, consumer electronics, industrial and power tools, stationary energy storage, aerospace and defense, and marine.

Each segment's market sizing and forecasts are based on revenue (USD).

By Product Type

| Lithium Cobalt Oxide (LCO) |

| Lithium Iron Phosphate (LFP) |

| Lithium Nickel Manganese Cobalt (NMC) |

| Lithium Nickel Cobalt Aluminium (NCA) |

| Lithium Manganese Oxide (LMO) |

| Lithium Titanate (LTO) |

By Form Factor

| Cylindrical |

| Prismatic |

| Pouch |

By Power Capacity

| Up to 3,000 mAh |

| 3,000 to 10,000 mAh |

| 10,000 to 60,000 mAh |

| Above 60,000 mAh |

By End-use Industry

| Automotive (EV, HEV, PHEV) |

| Consumer Electronics |

| Industrial and Power Tools |

| Stationary Energy Storage |

| Aerospace and Defense |

| Marine |

| By Product Type | Lithium Cobalt Oxide (LCO) |

| Lithium Iron Phosphate (LFP) | |

| Lithium Nickel Manganese Cobalt (NMC) | |

| Lithium Nickel Cobalt Aluminium (NCA) | |

| Lithium Manganese Oxide (LMO) | |

| Lithium Titanate (LTO) | |

| By Form Factor | Cylindrical |

| Prismatic | |

| Pouch | |

| By Power Capacity | Up to 3,000 mAh |

| 3,000 to 10,000 mAh | |

| 10,000 to 60,000 mAh | |

| Above 60,000 mAh | |

| By End-use Industry | Automotive (EV, HEV, PHEV) |

| Consumer Electronics | |

| Industrial and Power Tools | |

| Stationary Energy Storage | |

| Aerospace and Defense | |

| Marine |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How fast is India shifting to electric two-wheelers?

Electric two-wheelers captured 48% of total two-wheeler sales in India's top 10 cities during 2025, boosted by FAME-II incentives and rising fuel prices.

What chemistry will dominate Indian battery plants by 2031?

LFP is projected to grow 27.1% CAGR, overtaking NMC in utility storage and commercial EVs due to cost and safety advantages mandated by SECI and NTPC tenders.

Why are pouch cells gaining share?

Pouch cells offer 10-15% higher volumetric energy density and weigh 12-18% less than cylindrical equivalents, suiting new skateboard EV platforms despite the need for advanced cooling.

Which states lead in battery manufacturing investment?

Tamil Nadu, Gujarat, and Maharashtra account for 72% of committed cell capacity, thanks to state incentives, port access, and existing automotive clusters.

How is India addressing critical-mineral reliance?

The Critical Mineral Mission allocates INR 2,500 crore for overseas mine stakes and domestic processing, but commercial output is unlikely before 2028, keeping near-term supply dependent on imports.

What is the projected size of India’s lithium-ion battery market by 2031?

The India lithium-ion battery market is expected to reach USD 15.17 billion by 2031, growing at a 17.65% CAGR from 2026.