India Data Center Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2032 |

|---|---|

| Forecast Data Period | 2026 - 2032 |

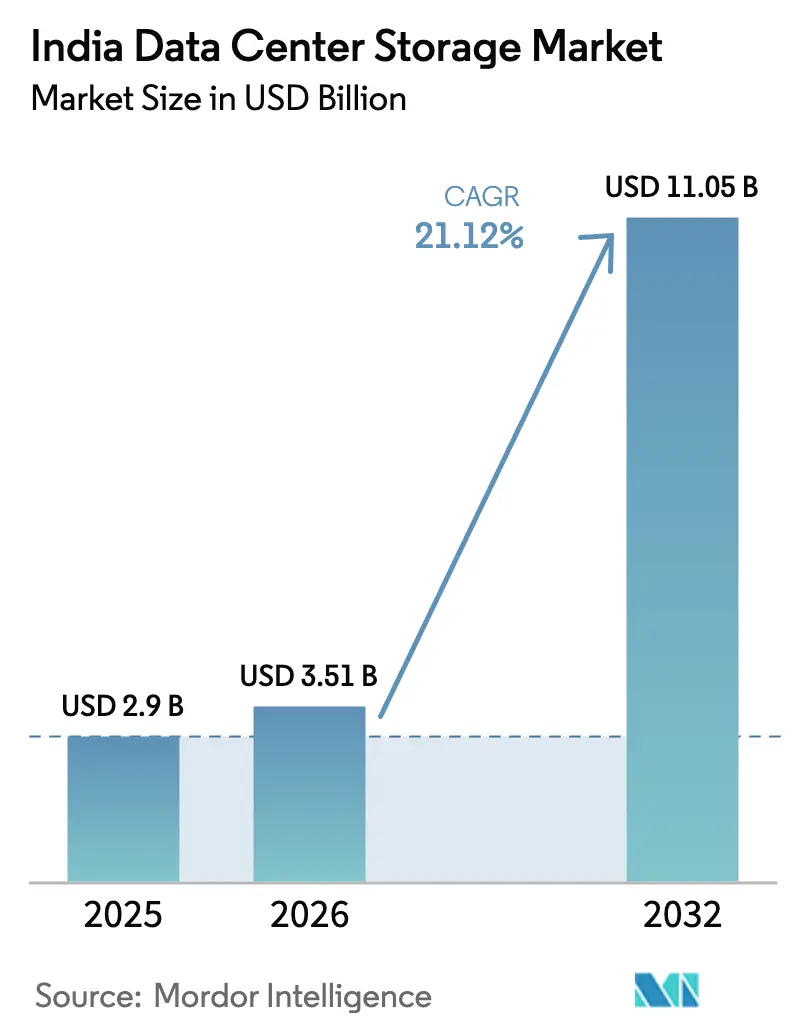

| Base Year Market Size (2025) | USD 2.90 Billion |

| Market Size (2026) | USD 3.51 Billion |

| Market Size (2032) | USD 11.05 Billion |

| Growth Rate (2026 - 2032) | 21.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Data Center Storage Market Analysis by Mordor Intelligence

India data center storage market size in 2026 is estimated at USD 3.51 billion, growing from 2025 value of USD 2.90 billion with 2032 projections showing USD 11.05 billion, growing at 21.12% CAGR over 2026-2032. Momentum stems from surging cloud adoption, sovereign data mandates, and the rapid shift of critical enterprise workloads toward localized infrastructure. AI-ready flash platforms, rising sovereign cloud projects, and capacity additions from both domestic and multinational hyperscalers are widening addressable demand pools for the India data center storage market. Sector growth also benefits from declining $/GB for flash, greater availability of renewable energy for high-density campuses, and tier-2 city incentives that are de-risking greenfield builds. Supply-chain strategies that emphasize local assembly and flexible consumption models are helping vendors offset NAND price volatility, thereby sustaining investment appetite throughout the India data center storage market.

Key Report Takeaways

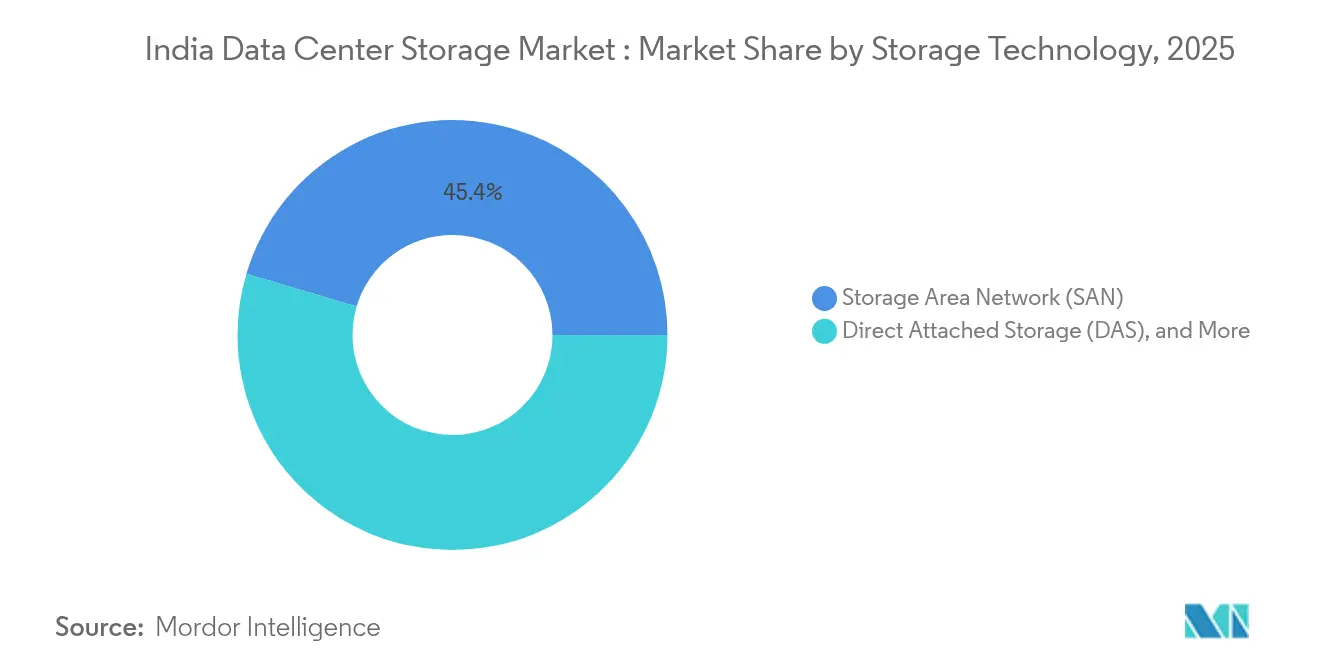

- By storage technology, Storage Area Networks led with 45.40% of the India data center storage market share in 2025; Network Attached Storage is projected to grow at a 18.97% CAGR through 2032.

- By storage type, all-flash arrays accounted for a 38.10% share of the India data center storage market size in 2025 and are advancing at a 17.05% CAGR to 2032.

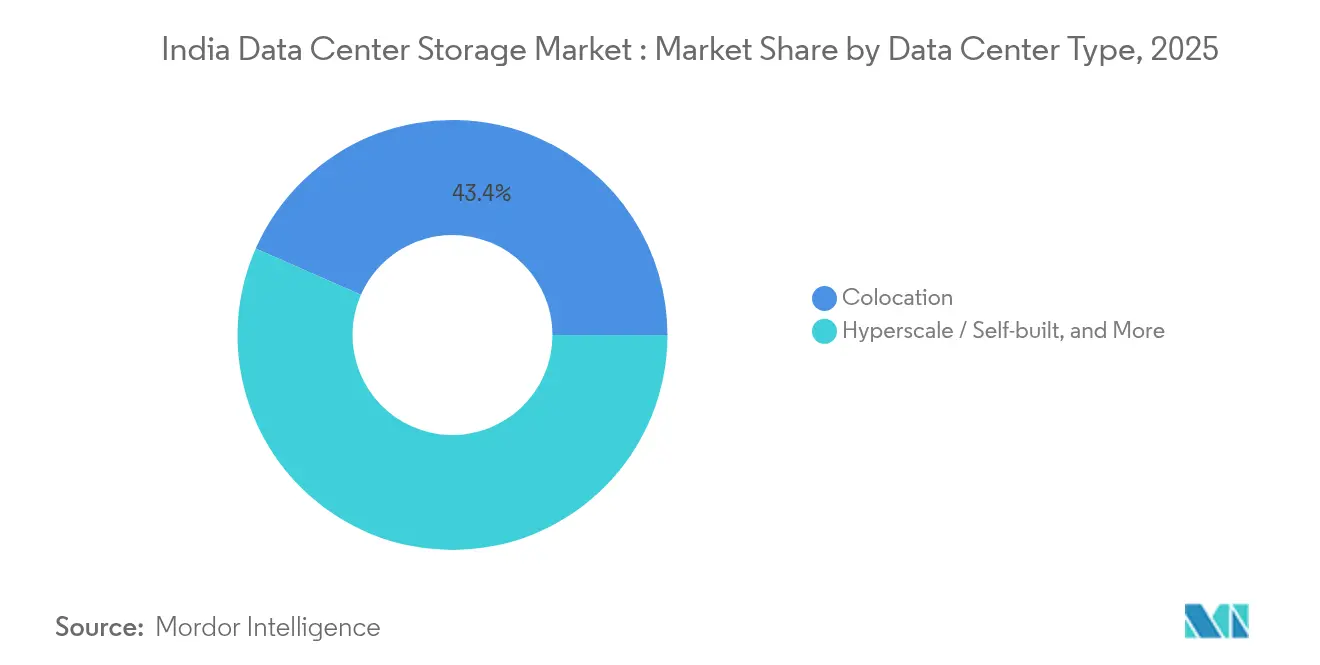

- By data center type, colocation providers held 43.40% of the India data center storage market share in 2025, while hyperscale and self-built deployments are expanding at a 15.28% CAGR through 2032.

- By end-user industry, IT and telecommunications captured 41.60% of the India data center storage market share in 2025; media and entertainment is progressing at an 17.68% CAGR to 2032.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Data Center Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of IT infrastructure | +3.20% | National, concentrated in Mumbai, Bengaluru, Chennai | Medium term (2-4 years) |

| Increased investments in hyperscale data centers | +4.10% | Mumbai, Chennai, Hyderabad with tier-2 expansion | Long term (≥ 4 years) |

| Government data-localization mandates | +2.80% | National, particularly BFSI and government sectors | Short term (≤ 2 years) |

| AI/ML workload proliferation driving high-performance arrays | +3.50% | Major metros with spillover to edge locations | Medium term (2-4 years) |

| Rise of edge data centers in tier-2/3 cities | +2.10% | Tier-2/3 cities including Jaipur, Nagpur, Chandigarh | Long term (≥ 4 years) |

| Growth of fintech and digital payments ecosystem | +1.90% | National with concentration in financial hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of IT Infrastructure

Enterprise modernization continues to double national capacity, rising from 1,255 MW to an expected 2,070 MW by end-2025. Data center capex programs tied to the Digital India initiative inject over USD 100 billion through 2027, pulling forward demand for next-generation arrays that underpin hybrid-cloud rollouts. Federal projects such as the National Informatics Centre’s USD 600 million Guwahati build add regional nodes that stimulate vendor ecosystems serving northeastern states. Storage architects are retiring direct-attached deployments in favor of software-defined stacks that interoperate across public, private, and edge clouds, reinforcing revenue visibility for the India data center storage market. Secondary hubs such as Nagpur and Raipur gain relevance because land and power pricing widen TCO advantages over saturated metros, further decentralizing opportunities.

Increased Investments in Hyperscale Data Centers

Landmark capital outlays are reshaping the India data center storage market. Reliance Industries’ planned USD 30 billion Jamnagar campus targets a record 3 GW IT load and is optimized for AI training clusters that need massively parallel flash arrays. In parallel, the USD 30 billion Project MGX consortium—anchored by Microsoft, BlackRock, and Temasek—selects Mumbai among fourteen Asia sites, underscoring sustained hyperscale momentum.

Google’s USD 6 billion Visakhapatnam facility cements the sovereign-cloud narrative, further locking in localized storage demand. Such megaprojects tilt procurement toward NVMe-oF, erasure coding, and advanced tiering that help hyperscalers curb latency and power draw. The ripple effect compels incumbent vendors in the India data center storage market to pivot toward open APIs and consumption-based contracting.

Government Data-Localization Mandates

Reserve Bank of India regulations require payment data to reside exclusively onshore, triggering immediate capacity upgrades across financial clouds [1]Reserve Bank of India, “Storage of Payment System Data,” rbi.org.in. The Digital Personal Data Protection Act of 2023 extends these obligations to most multinationals, accelerating sovereign platform builds and the adoption of granular audit capabilities. Domestic firms such as Jio Haptik completed SAR audits to validate compliance, illustrating how certifications influence vendor short-lists. Prospects of AI model localization requirements are poised to add further layers of storage residency, locking in multi-year investment pipelines within the India data center storage market.

AI/ML Workload Proliferation Driving High-Performance Arrays

A Pure Storage survey shows 52% of Indian enterprises already deploy AI, and 41% have doubled storage consumption, prompting 74% to budget for innovative arrays [2].Chris Mellor, “Pure Storage passes USD 3 billion revenue,” blocksandfiles.com Training large language models demands sustained >1 M IOPS, pushing buyers toward NVMe-based all-flash and parallel file systems. Vendors’ responses include Western Digital’s Ultrastar DC SN861 SSD at 16 TB and KIOXIA’s 122.88 TB PCIe 5.0 drive, which reduce rack footprints and energy per inference. BFSI and tech firms lean toward all-flash to maintain sub-millisecond latency SLA, whereas public health agencies prefer hybrid builds that satisfy compliance yet moderate capex. This segmentation expands SKU diversity across the India data center storage market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial investment cost | -2.30% | National, particularly affecting SME adoption | Short term (≤ 2 years) |

| Unreliable power supply in secondary cities | -1.80% | Tier-2/3 cities with grid infrastructure challenges | Medium term (2-4 years) |

| Import-dependent component price volatility | -1.50% | National, affecting all storage vendors | Short term (≤ 2 years) |

| Shortage of skilled storage professionals | -1.20% | National with acute impact in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Investment Cost

Average build costs hover at USD 5.4 million per MW, with storage absorbing 15-20% of budgets, impeding cash-constrained adopters [3]Jingyue Hsiao, “NAND flash prices surge,” semicone.com. All-flash arrays, while performance-superior, command higher ASPs than hybrid peers, delaying refresh cycles within small enterprises. Premium colocation rents in Mumbai and Bengaluru compound TCO concerns, making opex-based storage-as-a-service models more enticing. Vendors such as Hitachi Vantara and Dell are scaling pay-per-use offerings that flex in capacity and performance, partially offsetting this restraint within the India data center storage market.

Import-Dependent Component Price Volatility

NAND flash spot prices spiked over 10% in March 2025 after producer output cuts, instantly lifting BOM costs across SSD portfolios. India’s semiconductor market, estimated at USD 38 billion in 2023, remains import heavy despite incentive schemes slated through 2030. Currency swings and geopolitical uncertainties magnify pricing swings, compelling distributors to adopt dynamic quotation engines that may limit price-sensitive deployments. Successful execution of the Electronics Component Manufacturing Scheme 2025 could temper volatility, but timelines extend beyond the immediate horizon of the India data center storage market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Technology: SAN Leadership Meets NAS Acceleration

Storage Area Networks continued to dominate the India data center storage market in 2025 with a 45.40% share, driven by BFSI and telecom platforms that mandate block-level throughput for mission-critical databases. Although capital intensive, SAN fabrics deliver consistent latency and robust zoning required for high-transaction workloads. State Bank of India’s YONO expansion underscores SAN relevance by anchoring 64 million mobile users on low-latency Oracle RAC clusters. The India data center storage market size for SAN-based deployments is projected to rise steadily as tier-1 banks consolidate databases. At the same time, Network Attached Storage posts a 18.97% CAGR through 2032, fueled by streaming, design collaboration, and analytics workloads in media production houses around Mumbai and Hyderabad.

Migration from cumbersome file servers to clustered NAS advances data democratization and simplifies scale-out growth. Vendors such as QNAP and NetApp now bundle multiprotocol access, enabling customers to toggle between SAN and NAS modalities within unified arrays. Direct-attached configurations retain niche roles at edge nodes where simplicity trumps scalability, while software-defined storage is carving early footholds among tech startups attracted to commodity hardware economics. Overall, blended protocol strategies are expected to elevate flexibility across the India data center storage market as compliance rules favor architectures providing audit trails and immutable snapshots.

By Storage Type: Flash Gains Center Stage

All-flash arrays already captured 38.10% of the India data center storage market share in 2025 and are projected to compound at 17.05% annually, reflecting maturing price-performance economics. Large AI training clusters require petabyte-scale flash pools to minimize GPU idle time, an imperative that conventional HDD tiers cannot satisfy. The India data center storage market size for flash systems is poised to grow as organizations execute latency-critical fintech and OTT workloads.

Traditional spinning media endures within archival tiers, where cost per TB remains decisive. Hybrid arrays marry SSD front-ends with HDD back-ends, offering transitional economics for cautious CIOs. Industry alliances such as Samsung-Acro aim to widen SSD accessibility and localize supply to cushion NAND price swings. As PCIe 5.0 and zoned-namespace SSDs mainstream, unit energy per I/O is set to decline, reinforcing flash momentum within the India data center storage market.

By Data Center Type: Colocation Predominance, Hyperscale Steep Climb

Colocation captured 43.40% of the India data center storage market share during 2025, enabled by carrier-neutral interconnect and compliance certifications that shorten enterprise migration cycles. Monetization models based on cross-connect density and shared chillers keep opex predictable for SaaS, gaming, and ERP vendors. Meanwhile, hyperscale and self-built campuses are sprinting at a 15.28% CAGR, driven by sovereign cloud commitments from Amazon, Google, and domestic internet majors. The India data center storage market size attached to hyperscalers could surpass colocations in the out-years as workloads consolidate onto mega-campuses.

Edge and modular footprints are emerging in Jaipur, Nagpur, and Guwahati to slash first-mile latency for regional fintech and ed-tech apps, creating micro-storage nodes often under 50 racks. STT GDC’s 6 MW Jaipur project is illustrative, inserting smaller yet high-density pods to reduce hop counts for IoT gateways. Storage vendors targeting these deployments emphasize ruggedized enclosures and autonomous management stacks tuned for limited staff sites.

By End-User Industry: IT-Telco Mainstay, Media-Entertainment Breakout

IT and telecommunications commanded 41.60% of the India data center storage market share in 2025, reflecting core dependency on rapid packet processing, subscriber analytics, and 5G core virtualization. Operators funnel capex toward NVMe grids that sustain network-slicing control planes and subscriber data management. The India data center storage market size anchored in telco clouds keeps expanding as 5G densification multiplies data per cell site.

Media and entertainment advances at an 17.68% CAGR, a function of booming OTT subscriptions and localized dubbing workflows that inflate transcode footprints. High-bit-rate 4K and volumetric video assets are pushing studios toward petabyte flash caches connected by 100 GbE. BFSI modernization, catalyzed by digital onboarding and real-time fraud detection, drives appetite for encrypted SAN volumes compliant with RBI directives. Government departments extend e-services across states and pilot sovereign clouds that require tamper-proof audit logs, injecting new RFPs into the India data center storage market. Healthcare, edu-tech, and manufacturing verticals form the next demand wave, seeking sector-tuned compliance features such as HL7 tagging and shop-floor time-series retention.

Geography Analysis

Mumbai retained leadership in 2025 with 53.20% of installed capacity, underpinned by submarine cable gateways and dense capital markets traffic. Chennai follows as the fastest supply-adding hub, projected to contribute 24.10% of new racks through 2032 on the back of pro-investment policies and renewable-powered campuses. Delhi-NCR and Bengaluru round out the core cluster, together hosting multitenant facilities favored by SaaS exporters and federal agencies. This quartet accounts for roughly 89.20% of current compute footprints, a concentration that crystallizes vendor sales efforts inside the India data center storage market.

A discernible pivot toward tier-2 cities is underway as operators chase land savings and edge latency gains. Jaipur, Nagpur, Chandigarh, and Raipur now offer multi-megawatt plots, tax holidays, and expedited clearances, making them credible alternatives for secondary nodes. State level policies—Maharashtra’s NAINA science data initiative and Tamil Nadu’s Green Data Centre Park framework—showcase a policy arms race that pledges USD 40 billion in cumulative incentives. Power mapping by the Ministry of Power anticipates 3.2 GW of data center electricity load by FY28, funneling renewable procurement into site-selection calculus. Expansion beyond metros diversifies seismic and flood risk exposure but raises logistical concerns such as dual-grid redundancy and fiber backhaul availability. Vendors responding to the India data center storage market therefore invest in regional distribution warehouses and partner academies to groom local talent. As clusters mature, storage demand patterns will increasingly mirror edge population densities, turning capacity forecasting into a geo-spatial exercise rather than solely a metro-centric model.

Competitive Landscape

The India data center storage market is moderately concentrated yet fluid, as hyperscalers dilute incumbent dominance. Strategic moves reflect a race to AI optimization. Western Digital rolled out the AI Data Cycle framework, integrating workload classifiers into firmware to cut provisioning times. Samsung appointed Acro Engineering as national distributor to localize SSD channels and hedge against import shocks. Domestic conglomerates are also active: Reliance’s partnership with NVIDIA includes GPU and storage procurement bundles for the Jamnagar megacenter. White-space opportunities concentrate around edge appliances, sovereign cloud orchestrators, and finite-element simulation storage where latency determinism trumps raw capacity.

Local assembly gains strategic importance as component volatility persists. Both Micron and Foxconn evaluate Indian packaging plants, a shift that could reshape BOM economics for arrays sold into the India data center storage market. Vendors differentiate through service tiers offering capacity on demand, carbon accounting dashboards, and quantum-ready namespace designs, positioning themselves for the impending quantum compute rollout in Andhra Pradesh. Over the medium term, ecosystem alliances and regional manufacturing footprints will be pivotal differentiators.

India Data Center Storage Industry Leaders

Dell Inc.

Hewlett Packard Enterprise

NetApp Inc.

Hitachi Vantara LLC

Kingston Technology Company Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: MeitY restarted talks on a national data center policy aimed at single-window clearances and Data Centre Economic Zones.

- August 2025: Samsung appointed Acro Engineering as national SSD distributor, expanding Gen 4 and Gen 5 offerings.

- August 2025: Google confirmed USD 6 billion Visakhapatnam data center with 1 GW capacity.

- July 2025: TCS and CDAC partnered to build India’s sovereign cloud, strengthening domestic storage control.

India Data Center Storage Market Report Scope

Data center storage refers to the devices, hardware, networking equipment, and software technologies that enable data storage and applications within data center facilities. It stores, manages, retrieves, distributes, and back up digital information within data center facilities.

The India Data Center Storage Market is Segmented by Storage Technology (Network Attached Storage (NAS), Storage Area Network (SAN), Direct Attached Storage (DAS)), by Storage Type (Traditional Storage, All-Flash Storage, Hybrid Storage), by End User (IT & Telecommunication, BFSI, Government, Media & Entertainment and Other End User). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Network Attached Storage (NAS) |

| Storage Area Network (SAN) |

| Direct Attached Storage (DAS) |

| Other Technologies |

| Traditional Storage |

| All-Flash Storage |

| Hybrid Storage |

| Colocation |

| Hyperscale / Self-built |

| Enterprise / Edge / Modular |

| IT and Telecommunication |

| BFSI |

| Government |

| Media and Entertainment |

| Other End Users |

| By Storage Technology | Network Attached Storage (NAS) |

| Storage Area Network (SAN) | |

| Direct Attached Storage (DAS) | |

| Other Technologies | |

| By Storage Type | Traditional Storage |

| All-Flash Storage | |

| Hybrid Storage | |

| By Data Center Type | Colocation |

| Hyperscale / Self-built | |

| Enterprise / Edge / Modular | |

| By End-User Industry | IT and Telecommunication |

| BFSI | |

| Government | |

| Media and Entertainment | |

| Other End Users |

Key Questions Answered in the Report

What is the projected value of India’s data center storage segment by 2032?

It is forecast to reach USD 11.05 billion by 2032, expanding at a 21.12% CAGR from 2026.

How quickly are data-localization rules shaping storage demand in India?

Reserve Bank of India mandates and the Digital Personal Data Protection Act are already adding roughly +2.8% to the sector’s CAGR by forcing on-premise storage for regulated data.

Which storage technology currently holds the largest share in India?

Storage Area Networks led with 45.40% share in 2025 because BFSI and telecom workloads favor block-level throughput and low-latency zoning.

Why are hyperscale investments important to India’s future capacity?

Projects such as Reliance’s planned 3 GW Jamnagar campus and Google’s Visakhapatnam build need ultra-dense flash arrays and NVMe-over-Fabrics, driving large incremental demand for high-performance storage.

What challenge do component price swings pose to storage providers?

NAND flash spot prices jumped more than 10% in 2025, lifting bill-of-materials costs and forcing vendors to adopt dynamic pricing that can slow purchases among cost-sensitive buyers.

How does the Digital Personal Data Protection Act affect enterprise storage strategy?

The Act keeps personal data inside national borders, so multinationals must deploy compliant onshore arrays with fine-grained access controls and audit logs to meet residency and governance rules.

Page last updated on: