South Africa Data Center Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

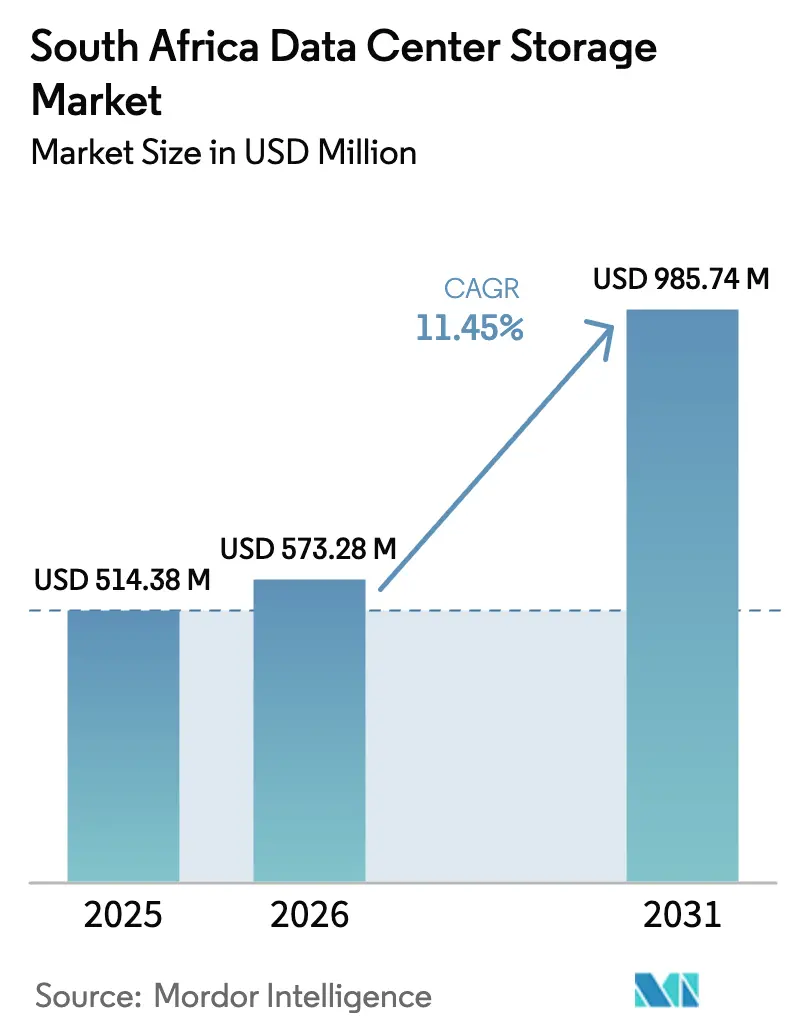

| Base Year Market Size (2025) | USD 514.38 Million |

| Market Size (2026) | USD 573.28 Million |

| Market Size (2031) | USD 985.74 Million |

| Growth Rate (2026 - 2031) | 11.45% CAGR |

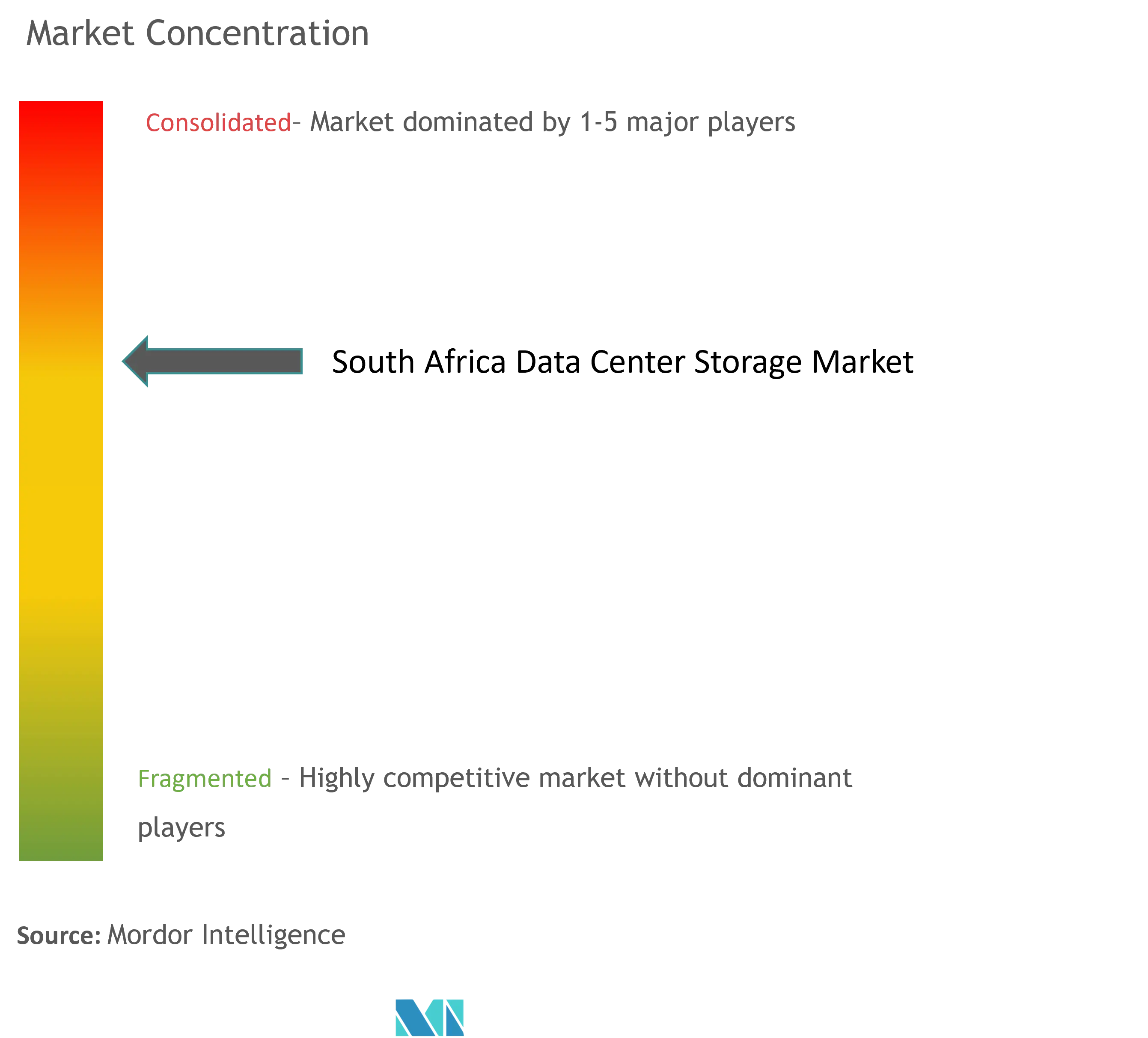

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Data Center Storage Market Analysis by Mordor Intelligence

The South Africa data center storage market size was valued at USD 514.38 million in 2025 and estimated to grow from USD 573.28 million in 2026 to reach USD 985.74 million by 2031, at a CAGR of 11.45% during the forecast period (2026-2031). Regulatory mandates, enterprise digitization, and sustained cloud build-outs position South Africa as Africa’s storage bellwether. POPIA-driven data-residency rules, widespread digital payment use, and an uptick in analytics workloads together spur steady refresh cycles for both on-premises and colocation environments. Growing hyperscale footprints, the shift from HDD to flash, and the drive for energy-efficient designs further accelerate capital spending across Johannesburg, Cape Town, and Durban. Vendors able to combine localization support with hybrid-cloud orchestration capture most purchasing decisions, while ongoing load-shedding pushes operators toward renewable-backed microgrids and low-power storage architectures.

Key Report Takeaways

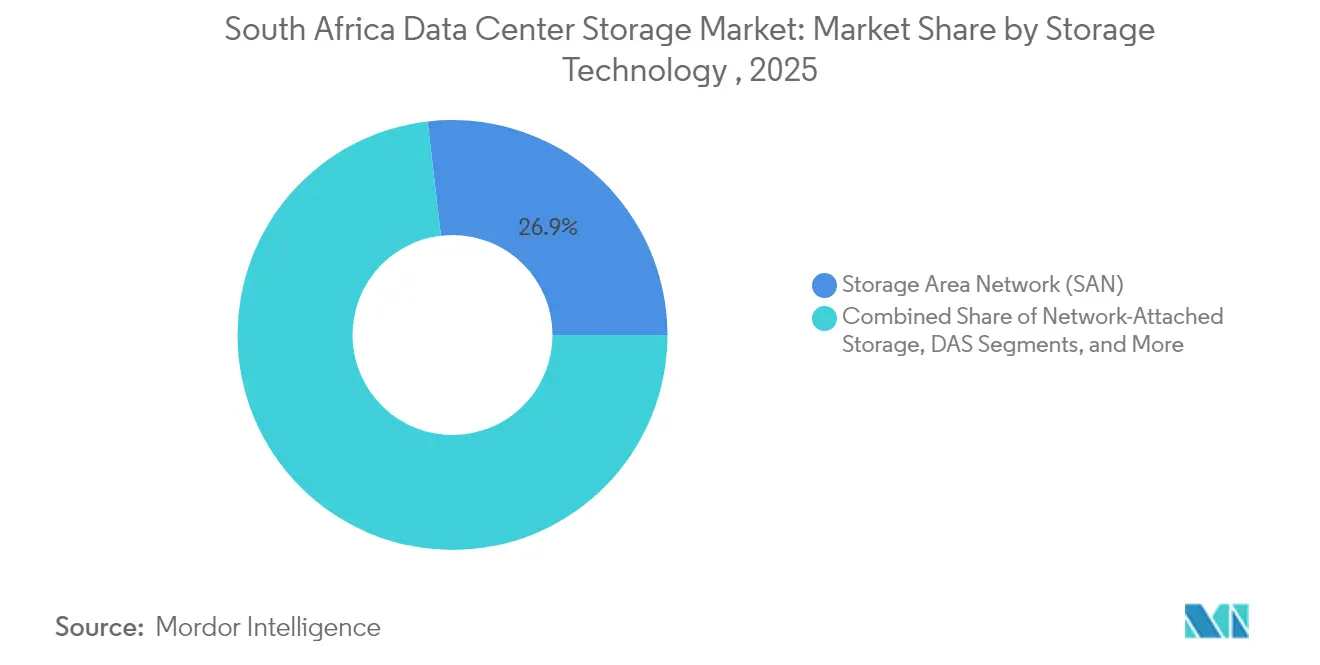

- By storage technology, Storage Area Network solutions led with 26.85% of South Africa data center storage market share in 2025, whereas Network Attached Storage records the highest 11.55% CAGR through 2031.

- By storage type, traditional HDD arrays held 42.60% share of the South Africa data center storage market size in 2025, while all-flash arrays are advancing at a 12.15% CAGR to 2031.

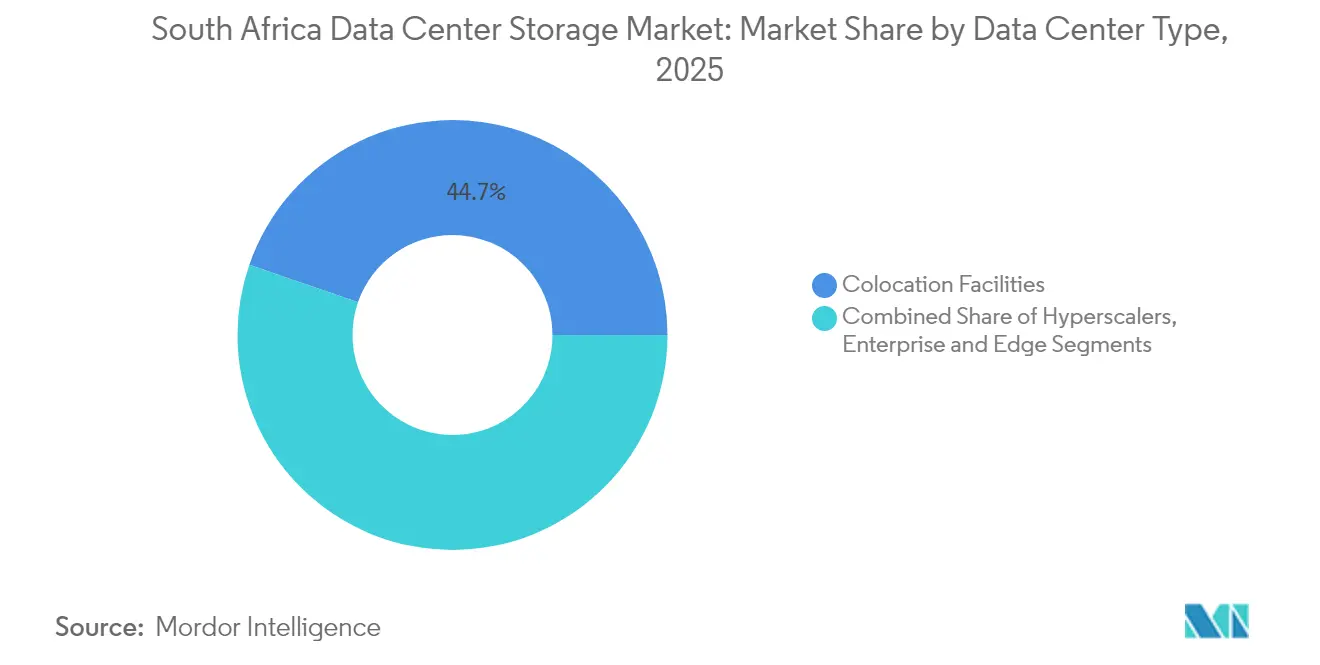

- By data-center type, colocation facilities captured 44.70% of the South Africa data center storage market size in 2025; hyperscaler deployments post the fastest 12.35% CAGR to 2031.

- By end user, IT & telecommunications retained 21.95% of the South Africa data center storage market share in 2025, whereas BFSI is projected to grow at 12.95% CAGR through 2031.

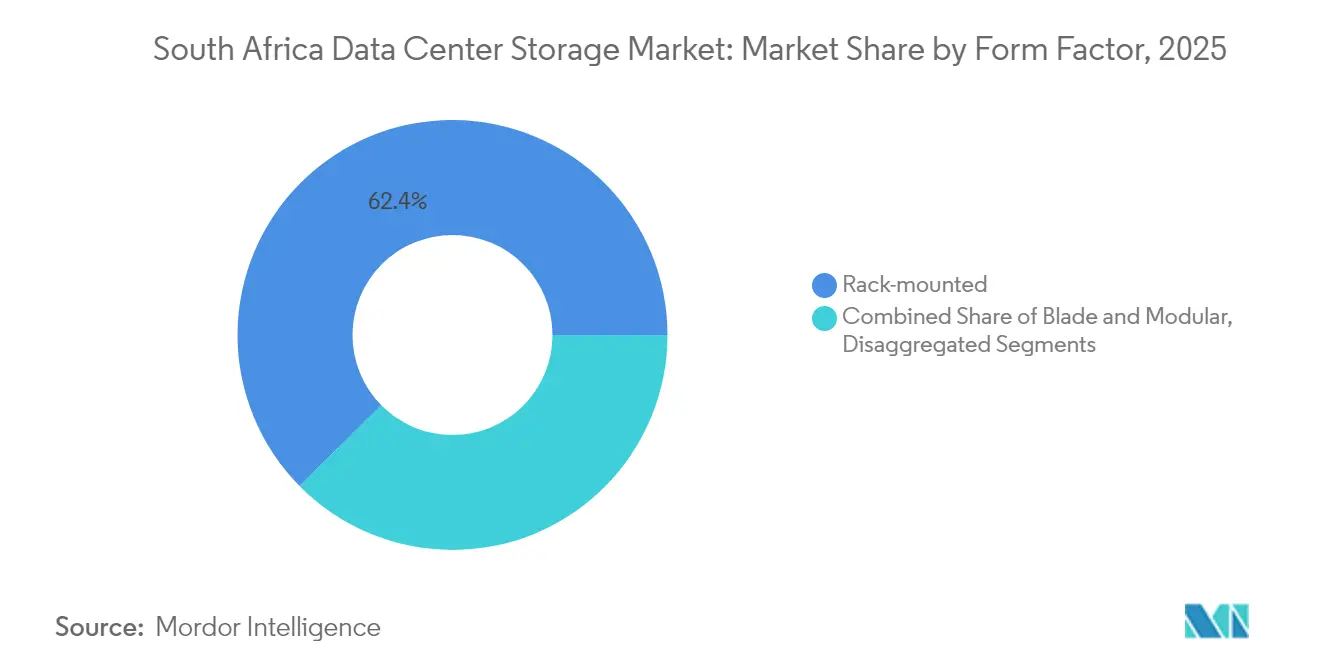

- By form factor, rack-mounted systems captured 62.40% share in 2025, with disaggregated architectures advancing at a 10.75% CAGR.

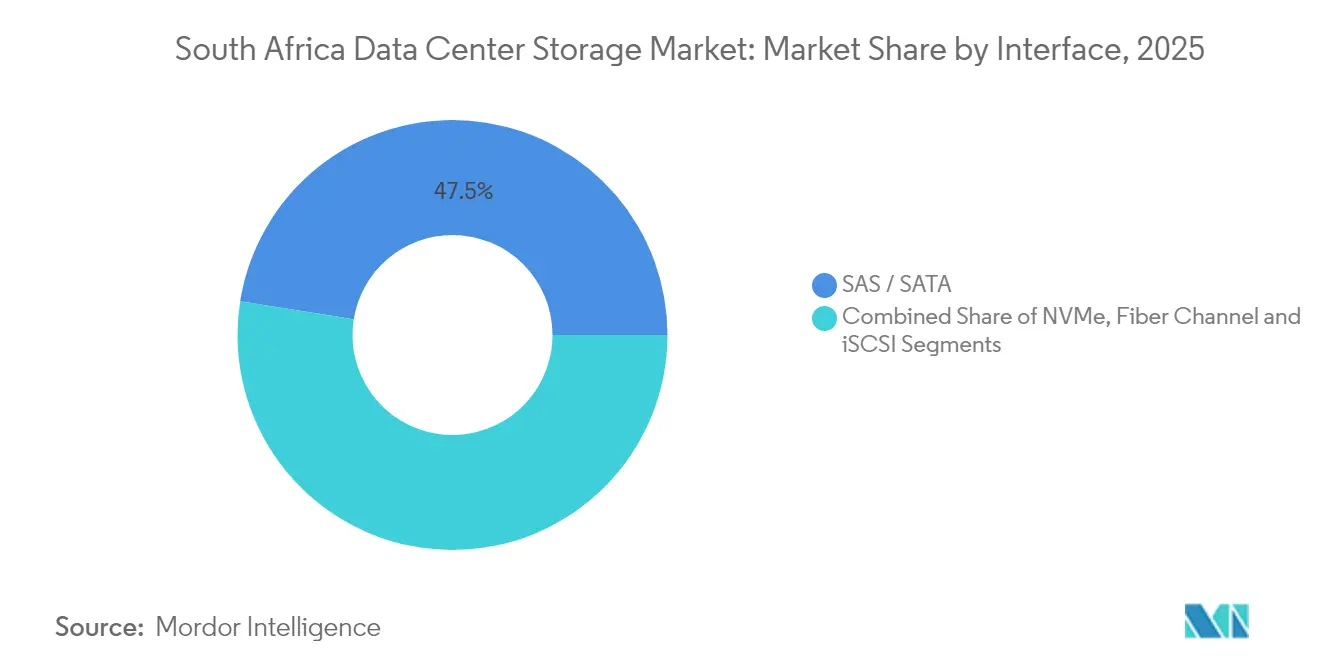

- By interface, SAS/SATA combined for 47.50% revenue in 2025; NVMe rises the quickest at 11.85% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Data Center Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing digitalization & data-centric applications | +2.8% | National (Johannesburg, Cape Town, Durban) | Medium term (2-4 years) |

| Evolution of hybrid flash arrays | +1.9% | National finance hubs | Short term (≤ 2 years) |

| Surge in hyperscale cloud deployments | +2.1% | Major metros | Medium term (2-4 years) |

| Rising adoption of all-flash storage | +1.7% | BFSI and telecom | Short term (≤ 2 years) |

| Renewable-energy-backed microgrids | +1.4% | Western Cape pilots | Long term (≥ 4 years) |

| POPIA-driven local data residency | +1.8% | All regulated sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Digitalization & Data-Centric Applications

Mass migration to digital channels fuels a sharp rise in structured and unstructured data volumes. Banks process millions of real-time payments daily, the Social Security Agency digitizes beneficiary records, and telecom operators capture high-resolution usage data. Each workload demands low-latency storage and seamless scale-out capacity. Enterprises therefore, prioritize architectures that balance throughput, capacity, and predictable quality of service, pushing the South Africa data center storage market toward multi-tier flash plus HDD estates.[1]DocuWare Editorial Team, “POPIA Compliance: Key Storage Considerations,” docuware.com

Evolution of Hybrid Flash Arrays

Hybrid flash arrays give local operators flash-class performance without committing budget to fully-flash racks. Automated tiering tools place hot data on NVMe modules and colder blocks on cost-optimized HDD or QLC flash, cutting total cost of ownership while safeguarding service-level agreements. BFSI and public-sector buyers use the model to consolidate sprawling database silos, aligning well with depreciation cycles for legacy arrays.[2]Scott Brown, “How Hybrid Flash Arrays Balance Performance and Cost,” cio.com

Surge in Hyperscale Cloud Deployments by Global Providers

AWS, Microsoft, and Google anchor new zones in Gauteng and Western Cape to meet POPIA compliance and regional growth goals. Hyperscale environments rely on object and block storage clusters topping multiple petabytes, creating downstream demand for high-density NVMe shelves, erasure-coded software-defined stacks, and interoperable on-prem gateways that tether enterprise systems to public cloud APIs

Rising Adoption of All-Flash Storage for Mission-Critical Workloads

Falling USD/GB, inline compression, and deduplication broaden all-flash viability beyond core banking to telecom mediation, media rendering, and manufacturing analytics. Enterprises measure gains not just in IOPS but in reduced floor space and power draw, key metrics given local electricity costs and carbon goals. When paired with modern backup appliances, flash arrays achieve sub-minute recovery point objectives that satisfy Basel III and King IV compliance frameworks.[3]Seagate Technology, “Mozaic 3+ and NVMe HDD Announcement,” seagate.com

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compatibility & optimum storage performance issues | -1.3% | National, particularly affecting multi-vendor environments | Medium term (2-4 years) |

| High upfront capex for flash & hybrid arrays | -1.6% | National, particularly affecting SME segment | Short term (≤ 2 years) |

| Power-supply instability impacting data-center uptime | -2.1% | National, with severe impact in industrial areas | Medium term (2-4 years) |

| Water-usage restrictions complicating cooling for dense storage | -1.2% | Regional, concentrated in Western Cape and drought-prone areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex for Flash & Hybrid Arrays

Currency volatility widens the sticker gap between rotational media and enterprise flash. Even when lifecycle models show lower operational expenses, mid-market CFOs hesitate to approve large capital outlays. Leasing, pay-per-use, and managed storage services gain traction, yet procurement friction stretches refresh cycles and can delay migration away from aging spinning disks

Power-Supply Instability Impacting Data-Center Uptime

National-grid load shedding forces operators to size UPS, diesel, or lithium battery systems beyond global norms. Frequent power cycling shortens drive life and interrupts write caching, raising both maintenance and data-loss risks. Facilities counters this by adding photovoltaic arrays, on-site wind turbines, and flywheel technologies, but capital intensity remains high and project delivery times can exceed two years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Technology: SAN Infrastructure Dominates Enterprise Deployments

SAN platforms maintained 26.85% share in 2025, confirming their role as the performance cornerstone of the South Africa data center storage market. Fibre Channel and iSCSI fabrics isolate critical banking and telecom databases, while next-gen SANs introduce NVMe-over-TCP to further cut latency. As virtualization ratios climb, shared pools alleviate stranded capacity across hosts and speed disaster recovery replication.

NAS is set to post 11.55% CAGR through 2031. Simplified file services, scale-out clusters, and multiprotocol support attract media studios, government archives, and DevOps teams. Meanwhile, object storage keeps expanding within hyperscaler pods, cementing the South Africa data center storage market as a multi-protocol landscape where software abstraction masks hardware heterogeneity.

By Storage Type: Flash Transition Accelerates Despite HDD Persistence

HDD arrays still accounted for 42.60% of the South Africa data center storage market size in 2025 because bulk data lakes and surveillance archives remain price-sensitive. Yet all-flash arrays now top every short list for core OLTP, VDI, and AI inference clusters, growing at 12.15% CAGR. Inline compression doubles effective capacity and power savings reach 40%, enhancing ROI calculations. Hybrid configurations pair TLC or QLC flash with shingled magnetic recording drives, letting enterprises incrementally refresh without forklift swaps. As controller firmware matures, tiering is seamless, driving broader acceptance across the South Africa data center storage market

By Data Center Type: Colocation Facilities Lead Market Adoption

Colocation sites hosted 44.70% of installations in 2025. Carrier-neutral campuses in Isando, Rondebosch, and eThekwini bundle resilient power and diverse fiber paths, ensuring POPIA compliance while capping capital budgets. Clients deploy custom racks yet rely on operator cooling and security. Hyperscale builds, while comparatively small today, are forecast to notch a 12.35% CAGR. Cloud operators pre-order entire warehouse-scale halls, driving land acquisition, submarine cable upgrades, and talent reskilling. This growth feeds a virtuous cycle that lifts the entire South Africa data center storage market.

By End User: BFSI Sector Drives Fastest Growth

IT & telecommunications remained the largest buyer at 21.95% share in 2025, a testament to bandwidth-heavy traffic monitoring, billing, and customer-experience platforms. The BFSI vertical, however, is primed for 12.95% CAGR as mobile-money, core banking upgrades, and regulatory analytics compound storage demand.

Government, media, and healthcare contribute steady volumes by digitizing citizen services, UHD streaming, and imaging diagnostics respectively. Manufacturing expands as IIoT telemetry, quality analytics, and digital twins mature, illustrating the widening footprint of the South Africa data center storage market across verticals.

By Form Factor: Rack-Mounted Solutions Maintain Dominance

Rack enclosures comprised 62.40% of shipments in 2025. Standard 19-inch footprints simplify spares logistics and slot directly into existing cold-aisle layouts, a key deciding factor for retrofit projects. High-density drawers push per-rack capacities past 1 PB while maintaining 15 kW power envelopes.

Composable disaggregated systems are expected to grow 10.75% CAGR through 2031. By pooling NVMe drives over PCIe or Ethernet fabrics, operators dynamically assign resources to fluctuating AI and analytics clusters, reinforcing operational agility within the South Africa data center storage market.

By Interface: NVMe Adoption Accelerates Performance Transition

SAS / SATA maintained 47.50% share in 2025 owing to broad HDD compatibility and mature tooling. NVMe, posting 11.85% CAGR, is now standard for every premium array and most white-box nodes. Latency drops from millisecond to microsecond scale, unlocking real-time fraud detection and streaming analytics use cases.

NVMe-over-Fabrics extends these gains across SANs, allowing centralized pools to rival direct-attach performance. Fibre Channel and iSCSI remain entrenched for legacy workloads, but roadmap announcements from all major vendors confirm NVMe as the long-term anchor for the South Africa data center storage market.

Geography Analysis

Johannesburg anchors over half of current deployments thanks to its concentration of financial headquarters, carrier hotels, and subsea cable landing stations. Cape Town ranks second, leveraging abundant renewable energy and municipal incentives that lower operational overheads. Durban rounds out the top three, serving manufacturing and port logistics clusters that demand edge caching for low-latency decision support.

Across provinces, POPIA enforcement compels in-country data processing, preventing wholesale lift-and-shift to offshore clouds. This dovetails with regional ambitions: South African facilities increasingly export low-latency services to Namibia, Botswana, and Mozambique, extending the influence of the South Africa data center storage market without violating sovereignty rules.

Infrastructure resilience remains uneven. Western Cape’s solar-plus-battery microgrids demonstrate viable alternatives to diesel gensets, while Eastern Cape sites still battle voltage fluctuations. Consequently, buyers evaluate storage gear not only for IOPS but for tolerance to brownouts, reinforcing the demand profile unique to the South Africa data center storage market.

Competitive Landscape

Global incumbents Dell Technologies, Hewlett Packard Enterprise, and IBM leverage established channel ecosystems and certified local support teams to win multi-year frame contracts. Their portfolios span arrays, software-defined stacks, and managed-services overlays, simplifying procurement for risk-averse enterprises.

NetApp and Pure Storage differentiate through data-fabric software that unifies on-prem NVMe shelves with AWS, Azure, and Google Cloud, aligning well with hybrid mandates. Seagate and Western Digital concentrate on high-capacity drives, tapping demand for economical cold-data tiers.

Regional specialists Teraco, Africa Data Centres, and Liquid Intelligent Technologies invest in energy-efficient campuses and submarine-cable endpoints, creating adjacent opportunities for array vendors bundled with colocation footprints. As spending shifts from technology specifications to measured business outcomes, total-cost-of-ownership calculators and compliance dashboards increasingly influence deal closure across the South Africa data center storage market.

South Africa Data Center Storage Industry Leaders

Dell Inc.

Hewlett Packard Enterprise

Huawei Technologies Co., Ltd.

Hitachi Vantara

NetApp Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Dell Technologies unveiled its Concept Astro platform for data center power optimization, combining agentic AI, digital twins, and automation to cut energy use in real time.

- June 2025: Seagate Technology introduced Mozaic 3+ and NVMe HDD technologies to boost high-capacity, high-performance storage aimed at AI data centers in emerging markets such as South Africa.

- February 2025: Equinix reported expansion to 270 IBX data centers across 35 countries with 56 builds underway, citing recurring-revenue growth drivers in Africa.

- February 2025: Alphabet, Microsoft, and Meta jointly outlined infrastructure outlays topping USD 215 billion for 2025, while Amazon alone will add USD 75 billion, intensifying global demand for storage and networking.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the South African data-center storage market as revenues generated from on-premise or colocation facilities inside the country that deploy dedicated storage appliances, SAN, NAS, DAS, object and tape systems, delivered on HDD, hybrid or all-flash arrays.

The value tracks hardware plus embedded firmware; software-only SDS, backup appliances located outside a data-center hall, and cloud-native storage sold as a managed service are excluded.

Segmentation Overview

- By Storage Technology

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

- Direct Attached Storage (DAS)

- Object and Tape Storage

- By Storage Type

- Traditional HDD Arrays

- All-Flash Arrays (AFA)

- Hybrid Storage

- By Data Center Type

- Colocation Facilities

- Hyperscalers/Cloud Service Providers

- Enterprise and Edge

- By End User

- IT and Telecommunication

- BFSI

- Government and Public Sector

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing

- By Form Factor

- Rack-mounted

- Blade and Modular

- Disaggregated / Composable

- By Interface

- SAS / SATA

- NVMe

- Fibre Channel and iSCSI

Detailed Research Methodology and Data Validation

Primary Research

Mordor's team spoke with storage architects at hyperscalers, colocation planners in Johannesburg and Cape Town, and CIOs in banking, telecom, and mining to verify utilization ratios, refresh cycles, average selling prices, and flash-penetration trajectories that desktop work alone cannot reveal.

Desk Research

Our analysts review tier-1, public data streams such as Statistics SA hardware import codes, South African Reserve Bank capital-formation tables, Department of Communications & Digital Technologies data-center project filings, and Uptime Institute outage reports.

Trade-body releases from the Africa Data Centres Association, POPIA compliance audits, and patent families gathered through Questel enrich technology trend mapping.

Company financials and shipment disclosures are pulled from D&B Hoovers, Dow Jones Factiva, and local JSE filings.

The sources named illustrate the breadth consulted; numerous additional documents were assessed for corroboration and context.

Market-Sizing & Forecasting

We begin with a top-down build anchored on the live rack footprint published by colocation operators, which is multiplied by typical storage spend per MW of new IT load.

Results are stress-tested against selective bottom-up checks, supplier shipment tallies, sampled ASP × unit volumes, and channel stock movements that fine-tune totals.

Variables guiding the model include quarterly MW additions, rack density shifts, the share of storage within overall IT infrastructure CAPEX, NVMe adoption, and power-cost trends that influence flash mix.

Five-year outlooks use multivariate regression blended with scenario analysis vetted by interviewed experts; gaps in bottom-up evidence are bridged with conservative interpolation from adjoining periods.

Data Validation & Update Cycle

Outputs pass a two-step analyst peer review, variance checks against external market signals, and a manager sign-off.

The dataset is refreshed annually, with interim updates triggered by events such as large campus launches or sudden currency swings, so clients always receive the latest view.

Credibility Anchor: Why Mordor's South Africa Data Center Storage Baseline Earns Trust

Published figures often diverge because each firm frames scope, currency timing, and refresh cadence differently.

By isolating only in-country data-center hardware spend and aligning it with rack deployment logs and audited ASP trends, we keep estimates transparent and directly traceable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 514.38 M (2025) | Mordor Intelligence | |

| USD 460 M (2024) | Regional Consultancy A | Excludes hyperscaler flash arrays and edge deployments |

| USD 2.16 B (2024) | Global Consultancy B | Bundles full IT stack and facility construction costs into storage tally |

Taken together, the comparison shows that Mordor's narrowly scoped, frequently refreshed baseline offers decision-makers a balanced middle ground, broad enough to capture genuine hardware shifts, yet disciplined enough to avoid inflation through unrelated spend.

Key Questions Answered in the Report

What is the current value of the South Africa data center storage market?

The South Africa data center storage market stands at USD 573.28 million in 2026 and is on track to reach USD 985.74 million by 2031, reflecting an 11.45% CAGR.

Which storage technology is most deployed in South Africa?

Storage Area Network systems lead with 26.85% share, favored for high-performance shared-block workloads across banking and telecom environments

Why is flash adoption growing despite higher upfront costs?

Falling USD/GB, stronger compression, and lower power draw make all-flash arrays economical for mission-critical workloads, spurring a 12.15% CAGR segment expansion.

How does POPIA influence storage buying decisions?

The act mandates local processing of personal data, pushing enterprises to deploy or rent in-country storage that meets compliance and audit requirements.

Page last updated on: