South Africa Data Center Rack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

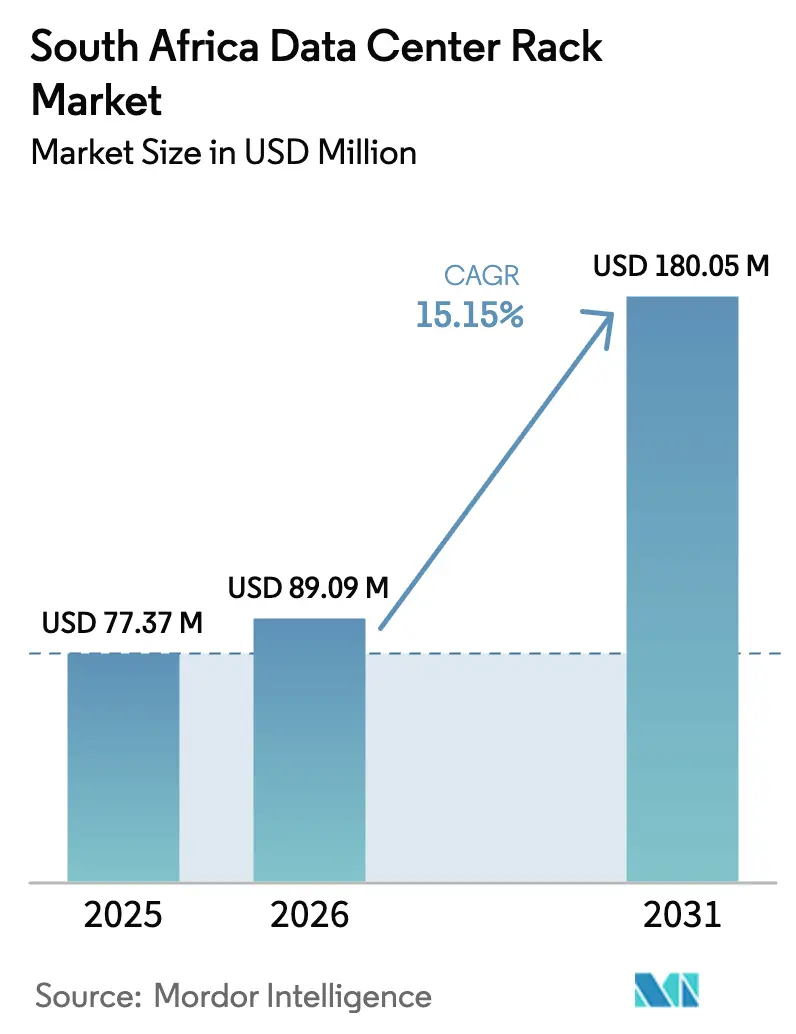

| Base Year Market Size (2025) | USD 77.37 Million |

| Market Size (2026) | USD 89.09 Million |

| Market Size (2031) | USD 180.05 Million |

| Growth Rate (2026 - 2031) | 15.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Data Center Rack Market Analysis by Mordor Intelligence

The South Africa data center rack market size was valued at USD 77.37 million in 2025 and estimated to grow from USD 89.09 million in 2026 to reach USD 180.05 million by 2031, at a CAGR of 15.15% during the forecast period (2026-2031). Heightened hyperscale investments, expanding enterprise cloud migration, and greater reliance on AI workloads are propelling demand for standardized, high-density racks across both new builds and facility retrofits. Microsoft’s ZAR 5.4 billion (USD 300 million) AI infrastructure commitment highlights the scale of capital flowing into the country’s digital backbone. At the same time, Teraco’s syndicated R8 billion loan and Google Cloud’s Johannesburg region have elevated South Africa to Africa’s preferred connectivity hub. Market momentum is also supported by 5G roll-outs, FTTH/B expansion, and new submarine-cable landings that together push compute closer to users and ignite edge rack demand. Supply-chain realignments—including the closure of ArcelorMittal’s long-steel line and Hillside Aluminium’s capacity expansion—are reshaping material choices and cost structures within the South Africa data center rack market

Key Report Takeaways

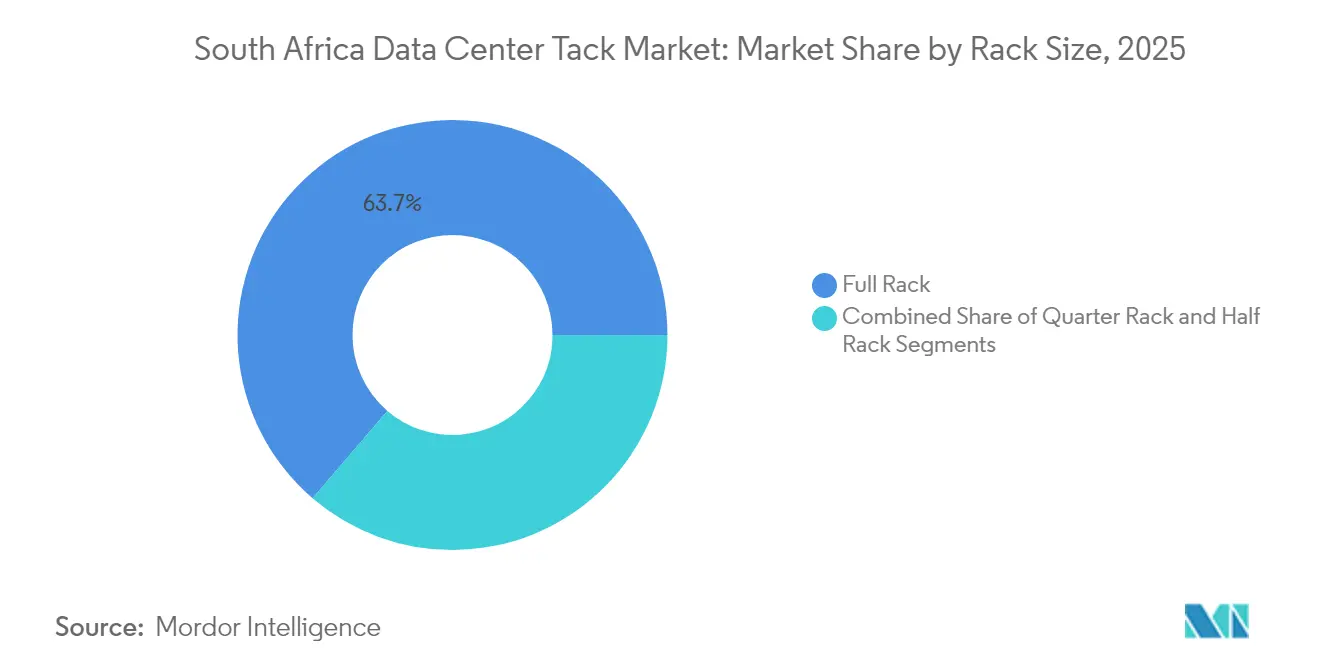

- By rack size, full racks led with 63.72% of South Africa data center rack market share in 2025; quarter racks recorded the fastest 16.65% CAGR through 2031.

- By rack height, the 42U segment held 51.45% revenue share of the South Africa data center rack market size in 2025, while 48U is projected to advance at a 15.74% CAGR to 2031.

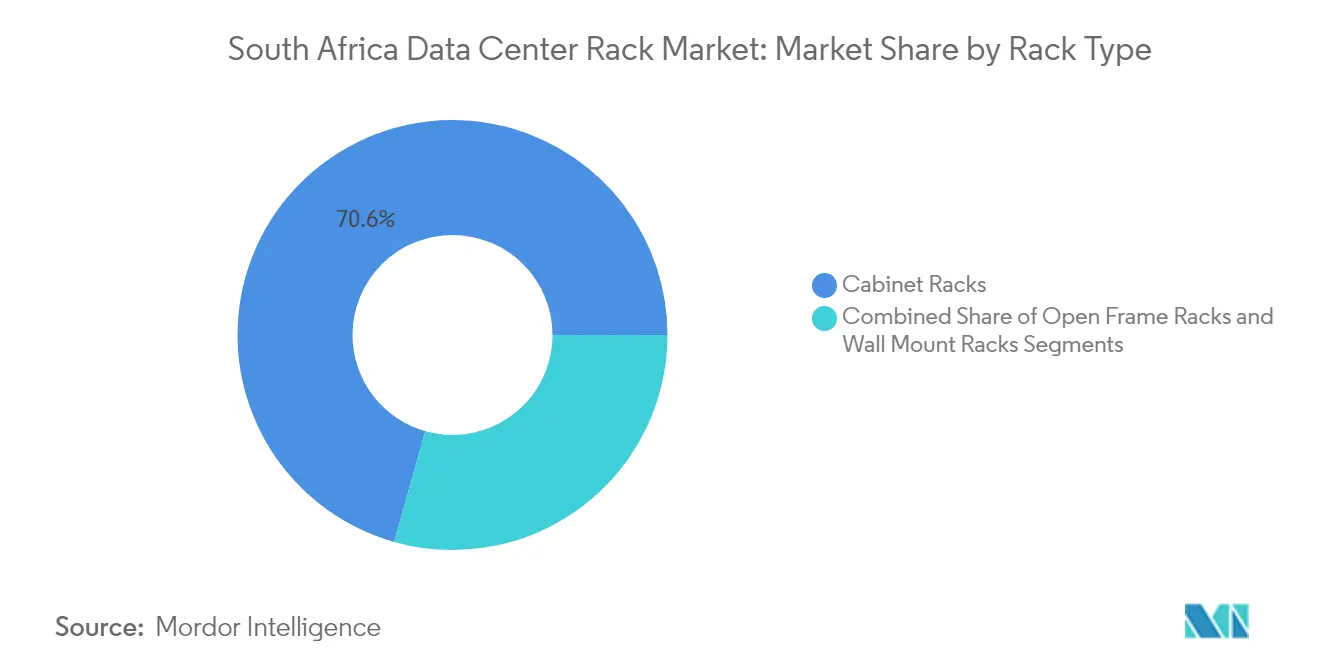

- By rack type, cabinet racks accounted for 70.62% of 2025 revenue; open-frame racks are poised for a 15.35% CAGR through 2031.

- By data-center type, colocation facilities captured 52.88% of 2025 deployments; hyperscale and cloud service providers are expanding at a 17.05% CAGR.

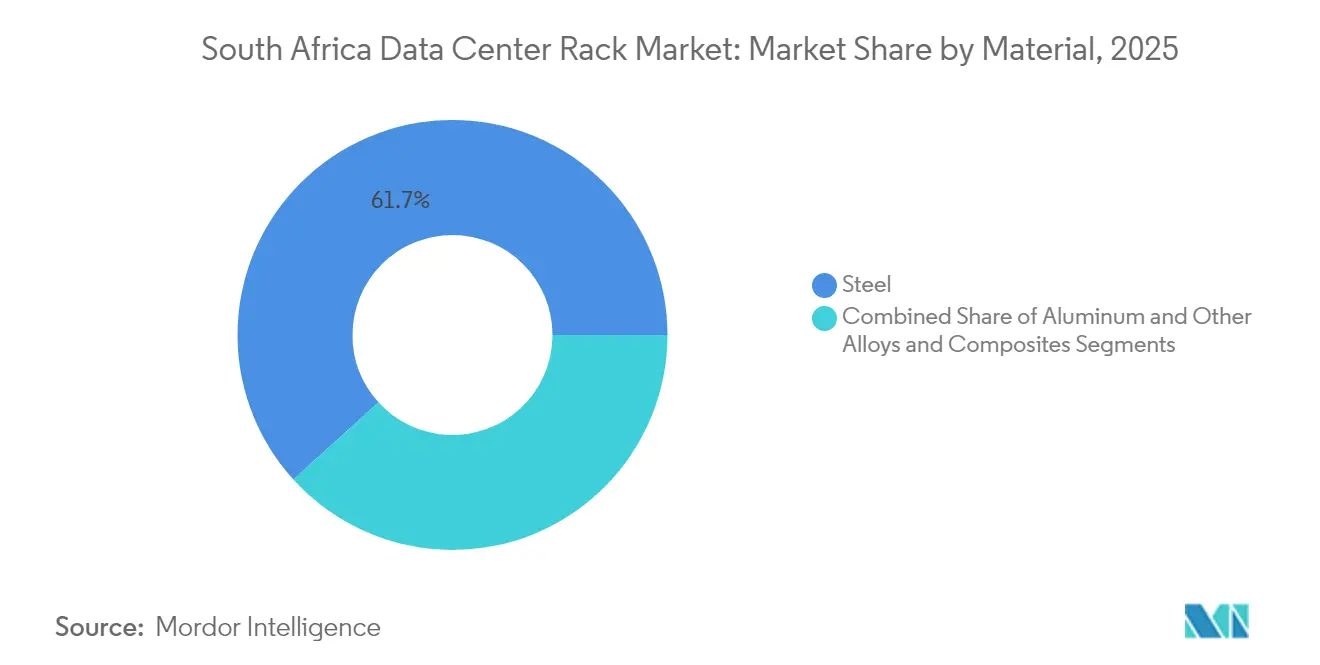

- By material, steel commanded 61.74% of 2025 revenue, whereas aluminum is forecast to grow at a 15.62% CAGR as operators seek lighter, corrosion-resistant alternatives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South africa contributes to an international system whose character is defined by the collective interaction of multi-country, multi-region parts. Our global data center rack market report represents that combined structure.

South Africa Data Center Rack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of hyperscale and local cloud regions | +3.2% | National, concentrated in Johannesburg and Cape Town | Medium term (2-4 years) |

| Surging 5G & FTTH/B penetration driving edge racks | +2.8% | National, with early gains in Gauteng, Western Cape, KwaZulu-Natal | Long term (≥ 4 years) |

| Enterprise shift from on-prem to colocation facilities | +2.1% | National, primarily Johannesburg financial district | Short term (≤ 2 years) |

| Upcoming submarine-cable landings boosting traffic | +1.9% | Coastal regions, Cape Town and Durban landing points | Medium term (2-4 years) |

| Eskom grid-modernization incentives for onsite renewables | +1.4% | National, prioritizing grid-constrained areas | Long term (≥ 4 years) |

| Local‐content procurement boosting domestic rack build | +1.1% | National, manufacturing hubs in Gauteng | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Full Rack is Expected to Grow Significantly

Hyperscale operators now set the pace for the South Africa data center rack market. Microsoft’s record domestic investment, AWS’s Cape Town presence, and Google Cloud’s new Johannesburg region drive uniform rack requirements that allow enterprises to adopt multi-cloud strategies with minimal integration risk.[1]Google Cloud, “Johannesburg Cloud Region Now Open,” cloud.google.comThese facilities demand fully loaded, 42U- or 48U-high racks engineered for 30 kW-plus thermal envelopes, spurring suppliers to deliver precision-cooled enclosures with tool-less cable management. Capital outlays from Vantage Data Centers—backed by a EUR 1.4 billion (USD 1.61 billion) EMEA fund raise—reinforce confidence in the local hyperscale pipeline.

Surging 5G & FTTH/B Penetration Driving Edge Racks

National 5G coverage surpassed 50% of the population in 2024 and, coupled with nearly 2 million fiber-to-home lines, is pushing compute workloads toward smaller, hardened racks in base-station shelters and roadside cabinets. MTN and Vodacom specify short-depth racks with integrated dust filters and DC-power buses suited to telecom power plants, while industrial firms adopt ruggedized enclosures for mining sites where latency requirements preclude centralized processing.[2] ITWeb, “Edge Computing in Industrial Sectors,” itweb.co.za

Enterprise Shift from On-Prem to Colocation Facilities

Power-supply instability and escalating security standards are encouraging South African companies to exit self-hosted server rooms. Old Mutual’s full migration of 215 applications to AWS typifies this pivot, while Takealot’s relocation of core databases to Google Cloud underscores the shift toward hybrid cloud architectures. As a result, colocation providers standardize full-rack footprints that blend high-density power shelves with modular blanking panels, supporting rapid capacity scale-out without custom engineering.

Upcoming Submarine-Cable Landings Boosting Traffic

The 2Africa, Equiano, and newly announced Meta Mumbai route cables will more than triple international bandwidth landing in South Africa by 2027, lowering transit prices and drawing CDN nodes into Cape Town and Durban. Content providers respond by leasing contiguous rack lines for cache clusters requiring 400 Gbps spine fabrics, advancing full-rack sales ,and accelerating demand for non-blocking power distribution units.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High data-centre CAPEX & security requirements | -2.3% | National, affecting all facility types | Short term (≤ 2 years) |

| Electricity-supply instability & costly backup power | -3.1% | National, severe in industrial areas | Short term (≤ 2 years) |

| Volatile local steel prices after safeguard duties | -1.8% | National, manufacturing centers | Medium term (2-4 years) |

| Skilled‐labour shortage in precision fabrication | -1.4% | National, concentrated in Gauteng manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Data-Center CAPEX & Security Requirements

New Tier III/Tier IV facilities require redundant feeds, biometrics, and rack-level access logs that lift enclosure costs 25-30% above commodity frames.[3]Government of South Africa, “National Cybersecurity Policy Framework,” gov.za Teraco’s JB7 build illustrates the capital burden, with rack systems representing nearly one-fifth of the project spend . Some enterprises delay refresh cycles or extend equipment life, which tempers near-term volume growth across the South Africa data center rack market.

Electricity-Supply Instability & Costly Backup Power

Load-shedding stages throughout 2024 forced operators to install larger battery strings and diesel generators, prompting rack designs that accommodate in-row UPS modules and busway redundancy. Teraco’s 120 MW solar plant addresses long-term resilience but also shifts specification toward racks pre-wired for renewable-friendly DC buses. Smaller facilities struggle to fund similar upgrades, limiting broad-based rollouts in the South Africa data center rack industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Size: Full Racks Enable Standardized Growth

Full racks captured 63.72% revenue in 2025 and are forecast to expand at 16.12% CAGR, a dual leadership underpinned by hyperscale purchasing frameworks favoring uniform footprints. This dominance steers manufacturers toward volume production that lowers per-unit cost and reduces supply risk across the South Africa data center rack market. Quarter racks remain essential for micro-edge cabinets deployed in 5G base stations, while half-rack uptake centers on mid-tier enterprises consolidating into suburban colocation halls.

The standardization of full racks converges with the 42U and 48U height formats, enabling shared accessory ecosystems—rails, PDUs, blanking panels—that simplify stocking for distributors. Operators such as Microsoft design AI clusters around full racks that sustain 80 kg per-U static loads, necessitating reinforced frames with cold-aisle containment kits. These functional convergences continue to broaden the customer base for full racks throughout the South Africa data center rack market.

By Rack Height: 48U Ascends While 42U Retains Core Position

The 42U format held 51.45% revenue in 2025 but loses incremental share to 48U racks advancing at 15.74% CAGR. Hyperscalers prize the taller design for augmented GPU count per footprint, thereby improving facility power-usage effectiveness without lengthening build timelines.

Edge sites, in contrast, prefer shorter enclosures that fit beneath false ceilings or inside street cabinets. Consequently, suppliers offer convertible kits that allow 42U frames to stack 600 mm extensions, maintaining backwards compatibility while letting clients test higher-density layouts. This adaptability helps balance legacy support with emergent 48U demand across the South Africa data center rack market.

By Rack Type: Cabinet Security Sustains Premium Demand

Cabinet racks accounted for 70.62% of 2025 shipments and continue to outpace open-frame alternatives due to mandatory compliance with the National Cybersecurity Policy Framework. Financial institutions require swing-handle locks and dual-factor access logging, features natively integrated into sealed cabinets but costly to retrofit on open frames.

Open-frame racks serve high-airflow zones and test labs where fast hardware swaps eclipse security. Wall-mount racks cater to edge deployments at cellular base-stations. This tiered mix encourages manufacturers to maintain three distinct product lines while channel partners bundle in-rack cooling or door-mounted power meters that raise margins in the South Africa data center rack market.

By Data Center Type: Hyperscale Growth Outruns Colocation Base

Colocation halls delivered 52.88% of 2025 rack deployments, reflecting enterprise preferences for hosted infrastructure that preserves hardware control. Hyperscale and cloud provider builds, however, post a 17.05% CAGR as Amazon, Microsoft, and Google extend regional footprints and align with data-residency mandates.

Hyperscale procurement favors bulk orders of thousands of identical racks, often sourced through global framework contracts. Domestic OEMs compete by offering last-mile modifications—solar-ready busbars, tamper-evident doors, or high-altitude ventilation kits—that international suppliers cannot deliver within tight lead times. This localization edge differentiates local contenders within the South Africa data center rack market.

By Material: Aluminum Climbs Despite Steel Supremacy

Steel secured 61.74% of 2025 sales, aided by Buy-Local rules and well-established milling capacity. Yet ArcelorMittal’s long-steel shutdown and volatile import duties raise price variance, nudging operators toward aluminum frames that cut weight by 35% and improve corrosion resistance.

Hillside Aluminium’s 719,000 ton plant supplies raw billet, but limited precision-fabrication skills constrain domestic rack output. Importers bridge gaps with knock-down kits assembled in Johannesburg free-zones to satisfy local-content thresholds. Composite alloys serve EMI-shielded cabinets for military and financial clients, but remain niche in the broader South Africa data center rack market.

Geography Analysis

Gauteng province dominates rack demand, anchored by Johannesburg’s financial hub and Pretoria’s government agencies. The cluster contains four hyperscale campuses and more than 60% of colocation white-space, creating sustained pull for full racks and spurring local assembly plants that shorten delivery cycles.

The Western Cape follows, driven by AWS’s Cape Town region and proximity to Equiano and 2Africa cable landings. Coastal latency advantages encourage CDN operators to lease contiguous rows of GPU-oriented racks for video streaming and generative AI inference. The South Africa data center rack market size attributed to the Western Cape is growing at a high-teens CAGR as these operators layer new halls onto existing sites.

KwaZulu-Natal ranks third, leveraging Durban’s role as a logistics gateway and emerging manufacturing zone. Provincial incentives support modular containerized data centers serving maritime and petrochemical operations that require hardened, salt-spray resistant racks. The Eastern Cape and Free State trail due to limited backhaul fiber and grid constraints, but renewable-energy corridors under Eskom’s modernization program could unlock future rack deployments if micro-grid pilots prove viable.

The data center rack market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Africa, North America, and Middle East. This is complemented by country-specific insights for Nigeria, Canada, Saudi Arabia, Philippines, Taiwan, and India, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Competition centers on a blend of global OEMs and agile domestic fabricators. Schneider Electric, Vertiv, and Rittal capture large enterprise and hyperscale contracts thanks to global certifications, on-shore spare parts, and 24/7 service desks They bundle racks with PDUs, intelligent monitoring, and containment aisles, positioning themselves as one-stop infrastructure vendors in the South Africa data center rack market.

Local suppliers—Modac Data Centre Design, CPS Technologies, and Server-Racks Africa—leverage quick turn-around, custom metalwork, and BBBEE compliance to win mid-size and edge projects. Their familiarity with Eskom’s grid codes enables bespoke busbar integrations that global rivals rarely offer on short notice.

Strategic moves underscore widening moats:

- Schneider Electric opened a Johannesburg experience center in 2024 to showcase liquid-cooling-ready cabinets.

- Vertiv expanded its BBBEE-compliant partnership with i-Rack Africa to assemble Italian frame designs locally.

- Teraco’s 120 MW solar-powered campus incorporates Vertiv’s SmartAisle ECO system, illustrating co-innovation between operator and rack vendor

South Africa Data Center Rack Industry Leaders

Schneider Electric SE

Vertiv Group Corporation

Rittal GmbH & Co. KG

Delta Electronics (Delta Power & Cooling)

Eaton Corporation plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Vantage Data Centers allocated EUR 1.4 billion to scale its EMEA footprint, with Johannesburg and Cape Town campuses slated for delivery by 2027

- January 2025: Microsoft invested ZAR 5.4 billion (USD 300 million) in AI infrastructure across South Africa, specifying GPU-optimized racks and liquid-ready door heat exchangers.

- January 2025: ArcelorMittal South Africa confirmed the closure of long-steel operations, signaling prolonged raw-material volatility for rack makers.

- November 2024: Teraco opened its JB7 hall and secured an R8 billion expansion loan, lifting total installed white-space to 73 MW

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South Africa data center rack market as all new, factory-built enclosures, open frame or cabinet, that house servers, storage, or network gear inside colocation, hyperscale, enterprise, and edge facilities. Each rack sale is valued at the invoice price paid by the end user, expressed in constant 2024 US dollars.

Scope exclusion: Passive wall-mounted boxes for branch offices and retrofit cage extensions fall outside this scope.

Segmentation Overview

- By Rack Size

- Quarter Rack

- Half Rack

- Full Rack

- By Rack Height

- 42U

- 45U

- 48U

- Other Heights (52U and Custom)

- By Rack Type

- Cabinet (Closed) Racks

- Open-Frame Racks

- Wall-Mount Racks

- By Data Center Type

- Colocation Facilities

- Hyperscale and Cloud Service Provider DCs

- Enterprise and Edge

- By Material

- Steel

- Aluminum

- Other Alloys and Composites

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts hold semi-structured interviews with facility engineers, local system integrators, and procurement heads spanning Gauteng, Western Cape, and KwaZulu-Natal. These conversations clarify typical rack fill rates, ASP trends, and lead-time constraints, and they validate soft assumptions harvested from desk work before figures are locked.

Desk Research

We begin by mapping the nation's active and planned white-space inventory with open sources such as Statistics South Africa's building approvals, SARS customs codes for HS 847330, ICASA licensing releases, the African Data Centres Association census, and Eskom grid-reliability bulletins. Company filings, investor decks, and credible media retrieved through Dow Jones Factiva and D&B Hoovers complement these fundamentals. Technical benchmarks are enriched with patent abstracts from Questel and shipment traces from Volza that reveal average rack heights, densities, and landed values. The sources cited illustrate, not exhaust, the secondary reservoir we mine for baseline evidence.

Market-Sizing & Forecasting

A blended top-down and bottom-up model underpins the numbers. Installed and committed IT load (MW) is converted to rack counts using density distributions (≤10 kW, 11-29 kW, ≥30 kW) that our interviews confirm; revenue arises once weighted by segment-specific average selling prices. Selective bottom-up checks, vendor shipment tallies and sampled project bills, anchor the totals. Key drivers include new submarine-cable landings, FTTH subscriptions, server refresh cycles, utility-scale renewable PPAs, and prevailing ASP erosion. Forecasts draw on an ARIMA with exogenous variables routine, then are stress-tested through scenario analysis for power-grid volatility.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance scans, senior analyst peer checks, and sector lead sign-off. Models refresh annually; material events such as load-shedding reforms or hyperscale campus launches trigger interim revisions, ensuring clients always see the latest viewpoint.

Why Mordor's South Africa Data Center Rack Baseline Commands Confidence

Published estimates frequently diverge because firms pick different rack types, density cut-offs, forecast windows, and currency conversion points.

Key gap drivers include whether quarter racks and edge micro-sites are counted, how aggressively hyperscale build plans are discounted, and the refresh cadence that captures or misses rapid ASP compression during 2024-25.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 77.37 M (2025) | Mordor Intelligence | - |

| USD 50.10 M (2023) | Global Consultancy A | Excludes quarter racks and edge closets, applies lower density profile. |

| USD 50.60 M (2024) | Regional Consultancy B | Uses historical FX average and focuses only on cabinet racks. |

Illustrative summary of leading gap sources versus Mordor's scope. In short, by aligning scope to every active rack form factor, refreshing assumptions soon after each hyperscale announcement, and triangulating ASPs with on-the-ground procurement insights, Mordor delivers a balanced, traceable baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the projected size of the South Africa data center rack market by 2031?

The South Africa data center rack market size is expected to reach USD 180.05 million by 2031, representing a 15.15% CAGR over the forecast period (2026-2031).

Which rack configuration leads current adoption?

Full racks dominate with 63.72% market share in 2025 due to hyperscale and colocation standardization requirements.

How does power instability affect rack design?

Frequent load-shedding has pushed operators to specify racks with integrated UPS shelves and renewable-ready busbars to maintain uptime during grid outages.

Which provinces generate the most demand for racks?

Gauteng and the Western Cape lead because of concentrated hyperscale campuses, submarine-cable landings, and deep enterprise footprints that require large volumes of standardized racks.

Page last updated on: