India Blood Glucose Monitoring Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

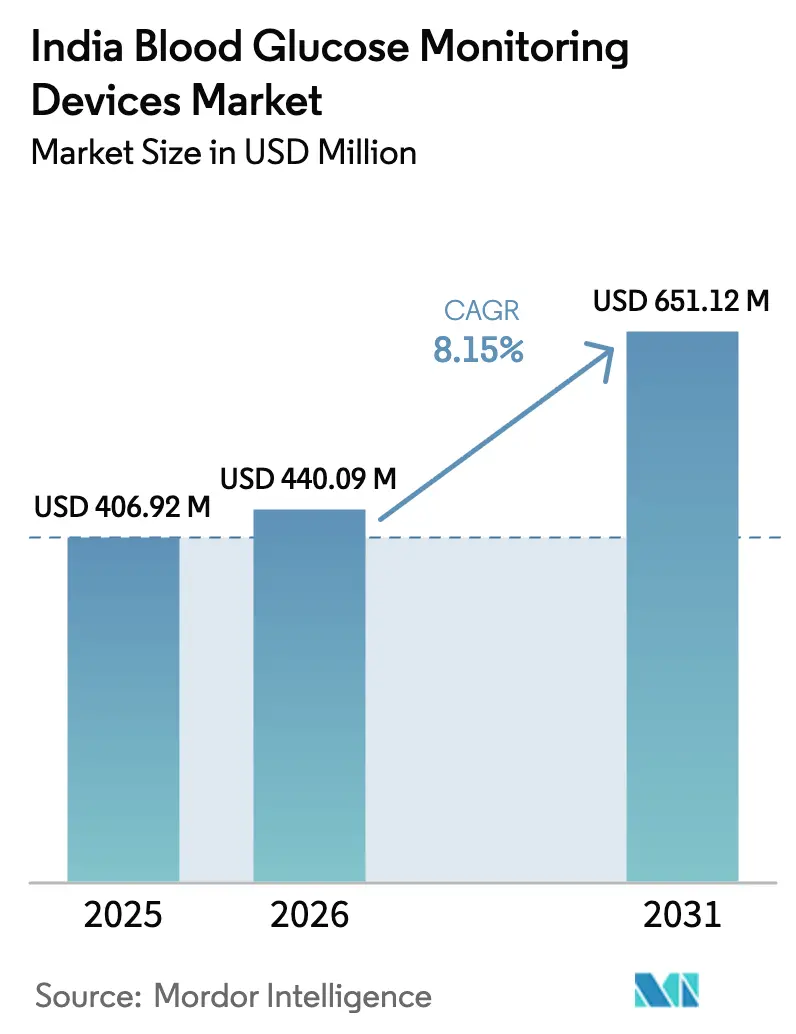

| Base Year Market Size (2025) | USD 406.92 Million |

| Market Size (2026) | USD 440.09 Million |

| Market Size (2031) | USD 651.12 Million |

| Growth Rate (2026 - 2031) | 8.15% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Blood Glucose Monitoring Devices Market Analysis by Mordor Intelligence

The India blood glucose monitoring devices market size was valued at USD 406.92 million in 2025 and estimated to grow from USD 440.09 million in 2026 to reach USD 651.12 million by 2031, at a CAGR of 8.15% during the forecast period (2026-2031). Rising diabetes prevalence, aggressive policy support for affordable devices, and the rapid shift toward digitally enabled care are underpinning this expansion. Wider Jan Aushadhi distribution of low-priced test strips is doubling per-patient testing frequency, while tele-diabetes platforms have normalized remote monitoring in more than 40% of urban consultations[1]Source: Indian Brand Equity Foundation, “Pradhan Mantri Bhartiya Janaushadhi Pariyojana (PMBJP),” ibef.org . Growing e-pharmacy penetration, production-linked incentives for domestic manufacturing, and new insurance guidance on continuous glucose monitoring reimbursement are further broadening access to advanced technologies. At the same time, manufacturers face cost pressure from grey-market strips and fragmented prescribing habits that still favor legacy glucometers, although ongoing regulatory crackdowns and targeted physician education are starting to close these gaps.

Key Report Takeaways

- By product type, self-monitoring blood glucose devices led with 83.70% of the India blood glucose monitoring devices market share in 2025, while continuous glucose monitoring systems are projected to expand at an 8.78% CAGR through 2031.

- By end user, home-care settings accounted for 52.74% of the India blood glucose monitoring devices market size in 2025 and are advancing at a 8.91% CAGR during 2026-2031.

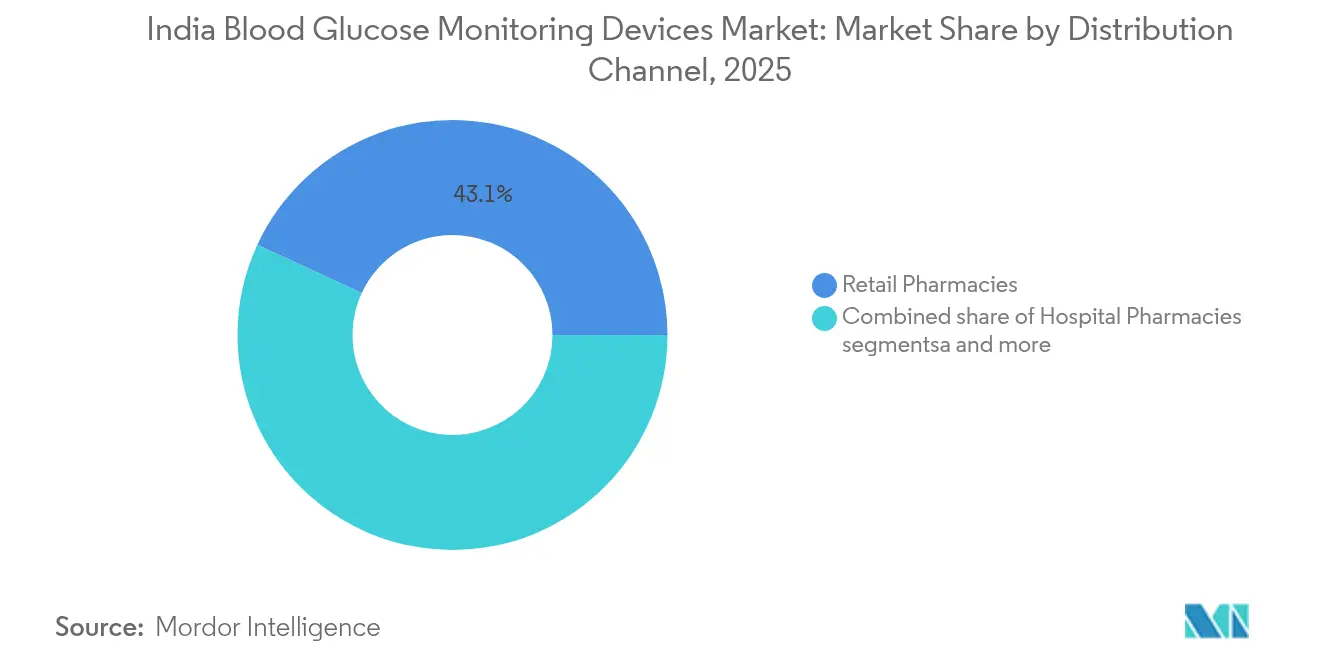

- By distribution channel, retail pharmacies held 43.10% revenue share in 2025, whereas online pharmacies record the fastest growth at 8.73% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Blood Glucose Monitoring Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing diabetes prevalence & earlier screening | +2.1% | National, with higher concentration in urban metros | Long term (≥ 4 years) |

| Rapid penetration of affordable SMBG strips via Jan Aushadhi stores | +1.8% | National, with accelerated gains in Tier 2/3 cities | Medium term (2-4 years) |

| Widespread adoption of tele-diabetes platforms post-COVID-19 | +1.5% | National, with early adoption in Karnataka, Tamil Nadu, Maharashtra | Short term (≤ 2 years) |

| GST reductions on essential diabetes devices | +1.2% | National | Medium term (2-4 years) |

| Insurance regulator mandating CGM reimbursement | +0.9% | Urban centers with organized healthcare systems | Long term (≥ 4 years) |

| App-linked loyalty programs boosting test-strip adherence | +0.7% | Metro cities and Tier 1 urban areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Diabetes Prevalence & Earlier Screening

National screening drives have identified an addressable base of more than 100 million people, including 25-30 million undiagnosed cases, lifting demand across all categories in the India blood glucose monitoring devices market. Screening at primary-care facilities now detects disease five to seven years earlier than a decade ago, stretching each patient's lifetime need for monitoring devices to as long as three decades. Intensive screening in semi-urban belts is accelerating device uptake among younger cohorts that show higher comfort with connected solutions. This shift is also guiding policymakers to support reimbursement for continuous monitoring because early adopters achieve superior glycemic control, lowering long-run complication costs. Collectively, these factors add more than +2.0 percentage points to the forecast CAGR of the India blood glucose monitoring devices market.

Rapid Penetration of Affordable SMBG Strips via Jan Aushadhi Stores

The Jan Aushadhi network supplies strips at half to one-tenth the branded price, cutting monthly monitoring outlay to INR 300-500 and doubling average weekly testing frequency. Affordable consumables are unlocking latent demand in Tier 2/3 cities where branded glucometer ownership languished below 15% as recently as 2022. Higher test-strip throughput improves glycemic control, reinforcing device stickiness and encouraging private manufacturers to introduce value-engineered meters tailored for these price-sensitive markets. The surge in strip volumes exerts significant positive pressure on the India blood glucose monitoring devices market, reflected in a +1.8% uplift to CAGR forecasts.

Widespread Adoption of Tele-diabetes Platforms Post-COVID-19

Remote consultations have normalized, with urban usage exceeding 40% and tribal pilot projects closing access gaps for 104 million underserved citizens. Studies covering more than 7,000 patients recorded a 9.6% drop in fasting glucose and a 58.5% fall in hypoglycemia when digitally supported self-monitoring guided real-time counseling. Government backing via the Ayushman Bharat Digital Mission, which links over 800 health-tech apps, ensures that meter data flows directly into electronic health records. Strong early evidence of clinical benefit spurs iterative demand for IoT-enabled meters and continuous sensors, adding +1.5% to overall growth momentum.

GST Reductions on Essential Diabetes Devices

Policy debate within the GST Council suggests classification of essential monitoring products alongside life-saving drugs, which already enjoy concessional taxes. A cut from 12-18% to 5% would shave 10-13% off consumer prices, especially benefiting high-value CGM kits that currently rely on imports subject to customs duties. Manufacturers anticipate volume lift sufficient to offset margin compression, implying another +1.2% to CAGR forecasts once the reform takes effect.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented physician Rx habits favouring legacy glucometers | -1.4% | National, with higher impact in rural and semi-urban areas | Long term (≥ 4 years) |

| Grey-market import of low-quality strips diluting brand trust | -1.1% | Border states and major trade hubs | Medium term (2-4 years) |

| Low public-hospital budget for CGM procurement | -0.8% | Public healthcare system nationwide | Long term (≥ 4 years) |

| Data-privacy concerns over cloud-linked monitoring apps | -0.5% | Urban educated segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Physician Rx Habits Favoring Legacy Glucometers

General practitioners deliver 70% of diabetes care but allocate only three to five minutes per visit, limiting discussion of advanced monitoring tools. As a result, many continue prescribing older glucometers they first encountered in medical school. Rural clinicians, serving two-thirds of the population, rarely receive manufacturer training on continuous systems, perpetuating brand inertia that slows CGM diffusion. Inconsistent guidance across multiple providers confuses patients and depresses adherence to optimal testing regimes. This entrenched conservatism removes roughly 1.4 percentage points from projected CAGR for the India blood glucose monitoring devices market.

Grey-Market Import of Low-Quality Strips Diluting Brand Trust

Counterfeit strips, often entering through informal border trade, retail at prices up to 70% lower than regulated products but can deviate 20% from actual glucose levels. Patients who experience inaccurate readings sometimes abandon self-monitoring altogether, undermining long-term demand. The Central Drugs Standard Control Organization launched random sampling drives, yet enforcement remains patchy in Punjab, West Bengal, and Rajasthan. Brand owners face added marketing costs to rebuild consumer confidence, shaving 1.1 percentage points off growth forecasts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: SMBG Dominance Faces CGM Disruption

Self-monitoring blood glucose devices generated 83.70% of 2025 revenue, primarily via meter-strip bundles sold at INR 800-1,500 and replenished with low-cost consumables distributed through Jan Aushadhi outlets. Test strips remain the largest contributor because each new reader drives recurring consumable demand. However, continuous glucose monitoring sensors outpace overall market growth at an 8.78% CAGR as price points fall and clinical outcome data becomes mainstream. The potential launch of a domestic INR 1,000/month CGM solution by FY26 could reset affordability and spur mass adoption.

The SMBG base maintains steady expansion because first-time buyers in Tier 2/3 cities continue to prefer upfront affordability and simple operation. Yet endocrinologists in metros are shifting high-risk patients to continuous sensors that capture glycemic variability and minimize nocturnal hypoglycemia. If domestic price compression materializes, the India blood glucose monitoring devices market size for CGM could triple its 2024 base by 2030, progressively eroding SMBG share. Leading brands now bundle cloud dashboards with traditional meters to defend position, reflecting the converging feature set between the two categories.

By End User: Home-Care Settings Drive Market Evolution

Home-care collected 52.74% of 2025 revenue, a lead reinforced by pandemic-era telemedicine that normalized remote dosage adjustment. Patients prefer testing at home to avoid transport cost and lost wages, especially where clinics remain distant. Hospitals and clinics rely on intermittent public budgets that often exclude advanced sensors; thus continuous systems still see limited use in inpatient settings. Nevertheless, tertiary centers in metros run pilot CGM programs for gestational and pediatric diabetes, demonstrating tangible outcome gains that could justify future procurement.

Ongoing loyalty-app promotions and auto-replenishment subscriptions expand testing compliance in urban homes. Policy focus on non-communicable disease management inside Ayushman Arogya Mandirs is also encouraging rural households to accept home monitoring under community-health-worker guidance. These forces combine to support a 8.91% CAGR in the home segment through 2031. Clinics continue accounting for complex case management and periodic calibration but will cede transaction volume to the home-care arena as devices become plug-and-play with smartphone back-ends.

By Distribution Channel: Online Pharmacies Reshape Market Access

Retail pharmacies captured 43.10% of 2025 value owing to entrenched neighborhood presence, yet online outlets are recording an 8.73% CAGR on the back of same-day fulfillment and aggressive discounting. Acquisition-driven scale, as seen in Reliance-Netmeds and Tata 1mg, extends reach into Tier 3 cities where physical outlets struggle to stock wide SKU ranges. Hospital pharmacies remain vital for acute-care supplies but face budget ceilings that limit innovation.

Urban millennials opt for app-based ordering even for first-time glucometer purchase because onboarding videos and chatbot counseling replicate in-store guidance. Rural adoption lags but climbs as logistic networks expand under the Digital India initiative. Manufacturers tailor channel strategy by reserving premium CGM sensors for tightly controlled e-pharmacy and hospital sales to curb counterfeit risk, while pushing entry-level SMBG bundles through Jan Aushadhi and conventional chemists.

Competitive Landscape

Global majors Abbott, Roche, and Medtronic dominate advanced technology supply but confront pricing headwinds in a market where sophisticated devices are still imported. Abbott’s FreeStyle platform leads CGM penetration, yet its recent withdrawal of a low-cost sensor underscores profitability challenges. Domestic champion Morepen Laboratories holds significant share of SMBG meters and is doubling capacity while developing an INR 1,000/month CGM slated for FY26.

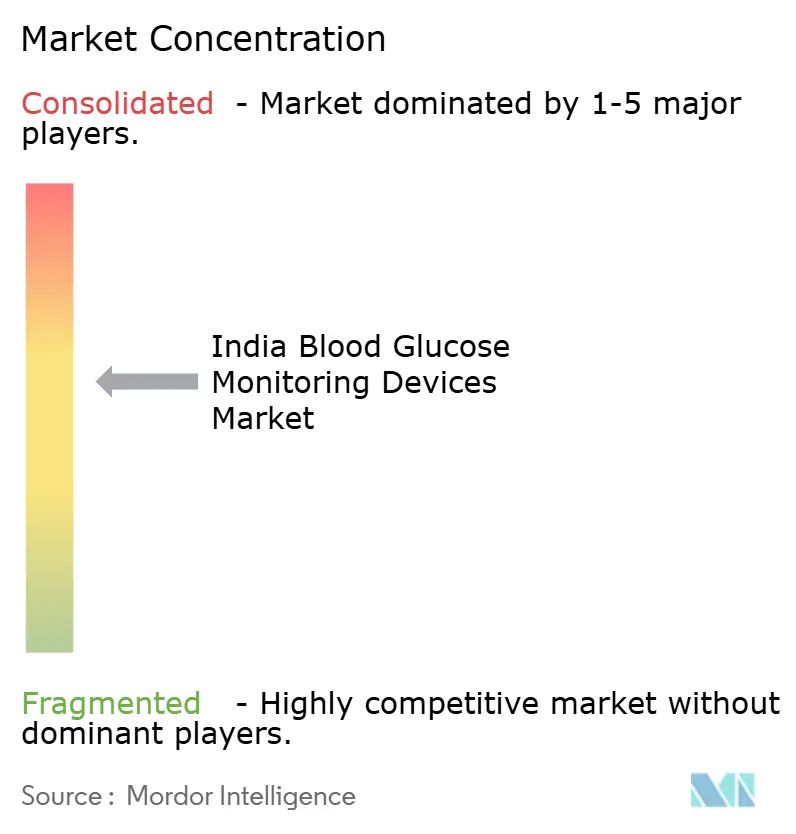

Strategic alliances are redefining competition: Abbott and Medtronic plan to integrate FreeStyle Libre with closed-loop insulin pumps, targeting patients on intensive therapy with an end-to-end digital ecosystem. Wearable innovators such as GOQii and Eyva test non-invasive sensors that could open adjacent wellness segments. The Production Linked Incentive scheme underwrites 19 device projects, helping local firms upgrade from assembly to full-stack manufacturing, which may compress costs for both sensors and strips[2]Source: Oommen C. Kurian, “Jan Aushadhi's Rapid Expansion: A Sub-National Analysis,” orfonline.org . Overall, the top five suppliers account for slightly under 60% of revenue, reflecting a moderately concentrated arena that is steadily diffusing as indigenous capacity grows.

India Blood Glucose Monitoring Devices Industry Leaders

Abbott

F. Hoffmann-La Roche Ltd

Medtronic plc.

Ascensia Diabetes Care Holdings AG

Arkray Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Abbott halted the Libre Pro low-cost sensor, forcing many Type 1 users to shift to higher priced imports

- March 2024: Thirteen greenfield plants came online under the PLI scheme, producing 138 device categories that include glucose meters and CGM consumables

India Blood Glucose Monitoring Devices Market Report Scope

As per the scope of the report, blood glucose monitoring comprises a variety of monitoring tools tailored for diabetes management. They empower patients to regulate their blood glucose levels, ensuring effective diabetes management. Monitoring blood sugar stands as a pivotal pillar in diabetes management, particularly for individuals with type 1 diabetes or those reliant on insulin. Blood sugar levels can be tracked through a glucose meter paired with test strips or a CGM system.

The Indian blood glucose monitoring market is segmented by device and end user. By device, the market is segmented into self-monitoring blood glucose devices and continuous blood glucose monitoring devices. By end user, the market is segmented into hospital/clinical usage and home/personal usage. For each segment, the market size and forecast are provided in terms of value (USD).

| Self-Monitoring Blood Glucose (SMBG) Devices | Glucometer Devices |

| Test Strips | |

| Lancets | |

| Continuous Glucose Monitoring (CGM) Systems | Sensors |

| Durables (Receivers and Transmitters) |

| Hospitals & Clinics |

| Home-Care Settings |

| Diagnostic Centers |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| By Product Type | Self-Monitoring Blood Glucose (SMBG) Devices | Glucometer Devices |

| Test Strips | ||

| Lancets | ||

| Continuous Glucose Monitoring (CGM) Systems | Sensors | |

| Durables (Receivers and Transmitters) | ||

| By End User | Hospitals & Clinics | |

| Home-Care Settings | ||

| Diagnostic Centers | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

Key Questions Answered in the Report

How large is the India blood glucose monitoring devices market in 2026?

The market is valued at USD 440.09 million in 2026 and is on track to reach USD 651.12 million by 2031.

What is the forecast CAGR for blood glucose monitoring devices in India?

Aggregate revenue is set to rise at an 8.15% CAGR between 2026 and 2031.

Which product category dominates sales?

Self-monitoring blood glucose devices lead with 83.70% share, though continuous systems are gaining fastest.

Why are home-care settings growing quickest?

Tele-medicine adoption and Jan Aushadhi strip affordability make at-home testing more convenient and cost-effective, driving a 8.91% CAGR.

How are online pharmacies changing device distribution?

E-pharmacies leverage fast delivery and deep discounts, posting 8.73% CAGR and expanding access to advanced meters beyond metros.

What policy moves could lower device costs?

Proposed GST cuts on essential medical devices and Production Linked Incentive grants for local manufacturing aim to reduce end-user prices and raise domestic output.

Page last updated on: