Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

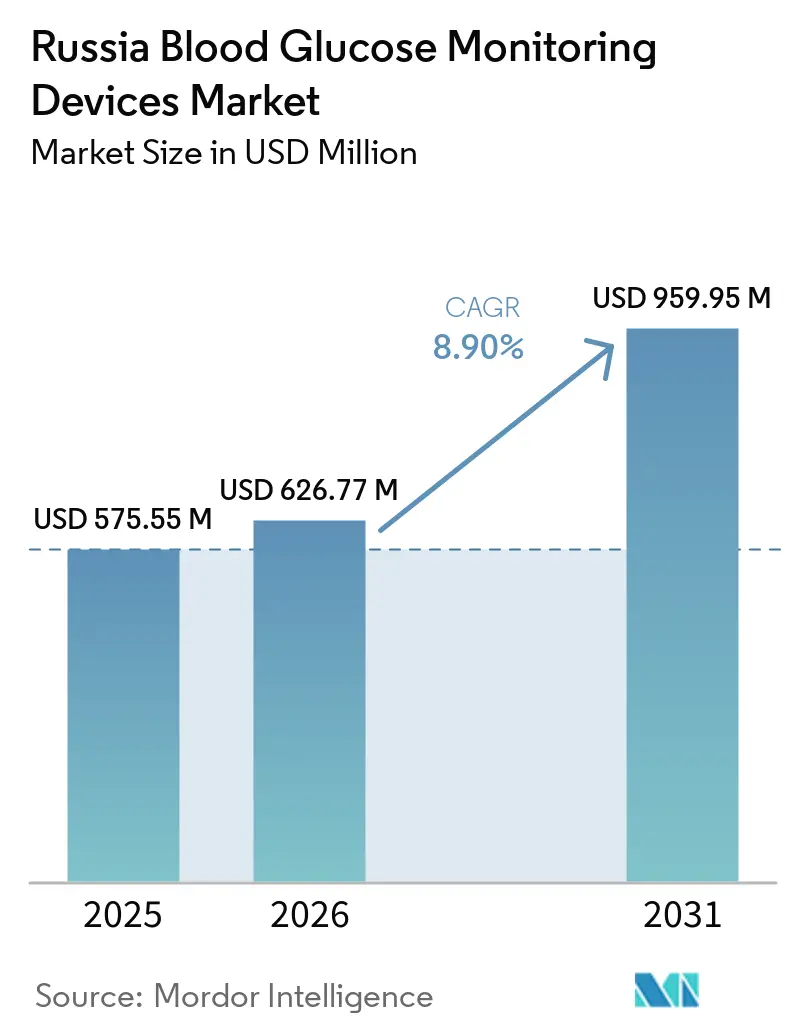

| Base Year Market Size (2025) | USD 575.55 Million |

| Market Size (2026) | USD 626.77 Million |

| Market Size (2031) | USD 959.95 Million |

| Growth Rate (2026 - 2031) | 8.90% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Blood Glucose Monitoring Devices Market Analysis by Mordor Intelligence

The Russia Blood Glucose Monitoring Devices Market size is expected to increase from USD 575.55 million in 2025 to USD 626.77 million in 2026 and reach USD 959.95 million by 2031, growing at a CAGR of 8.90% over 2026-2031.

Federal reimbursement that now covers continuous glucose monitoring (CGM) for all children aged 2-17 and pregnant women, the domestic sensor-production mandate embedded in GOST R 72213-2025, and an 80% CGM retail share held by Abbott Diabetes Care are the three structural forces reshaping the Russia blood glucose monitoring devices market. Import dependence above 75% created price inflation once parallel shipments from Kazakhstan, Belarus, and Turkey became the dominant logistics route, yet the Ministry of Health’s November 2024 grant of RUB 5.5 billion (USD 0.07 billion) to modernize endocrinology centers anchors policy continuity for real-time glycemic control. While hospitals still represent nearly one-half of spending, home-care usage of Bluetooth-enabled glucometers and CGM applications rose after a 1,572-patient study showed median HbA1c improvement from 7.6% to 7.2% within twelve months. Over the forecast horizon, the Russia blood glucose monitoring devices market will pivot to domestic platforms that can integrate automatically into the Unified Medical Information System (UMIS) and pass the ≤15% mean absolute relative deviation (MARD) requirement.

Key Report Takeaways

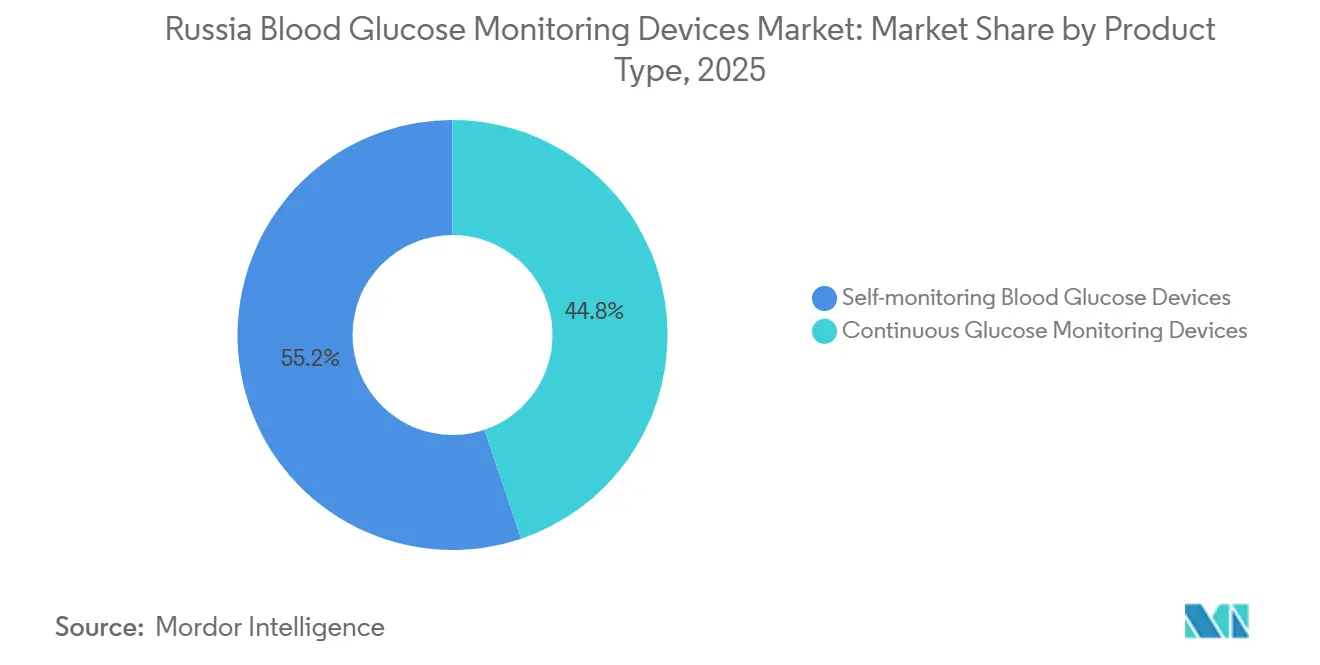

- By product type, self-monitoring blood glucose products accounted for 55.18% revenue in 2025, while CGM devices will deliver the fastest growth at a 12.22% CAGR through 2031.

- By end user, hospitals held 47.21% spending in 2025; the home-care segment posts the leading 11.65% CAGR for 2026-2031.

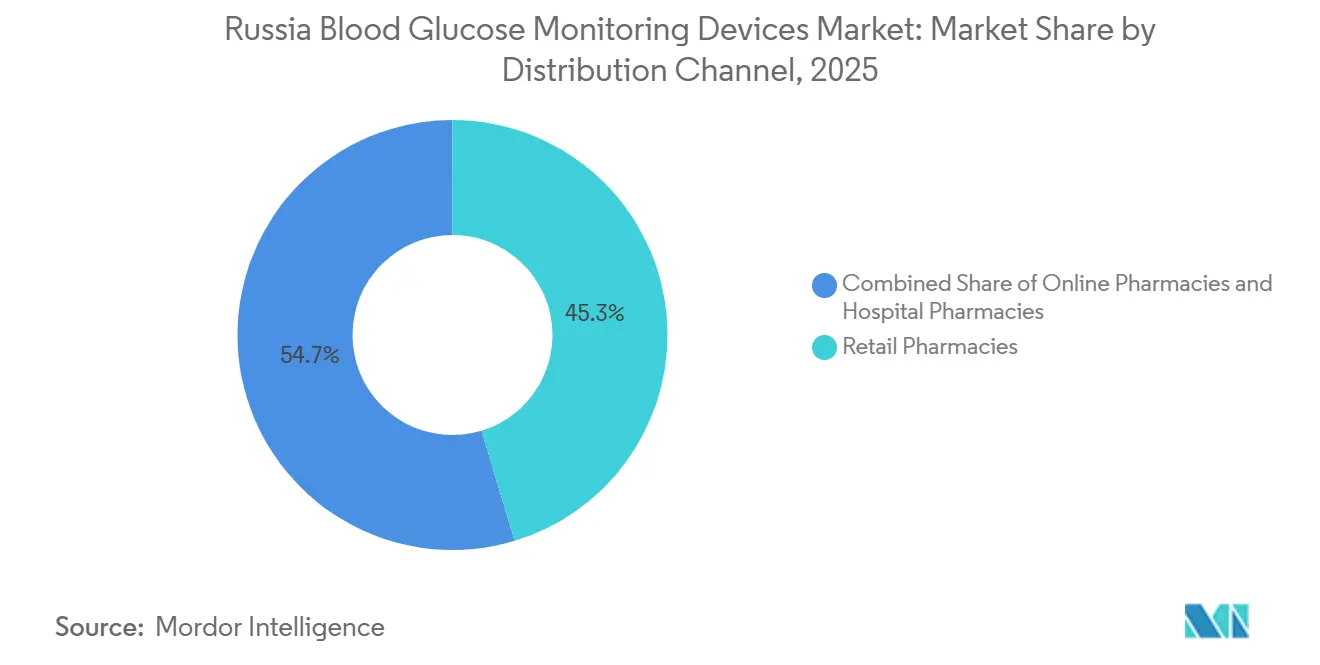

- By distribution channel, retail pharmacies captured 45.32% distribution value in 2025 yet online channels record the highest 13.12% CAGR going forward.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Russia Blood Glucose Monitoring Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diabetes prevalence and earlier onset | +2.1% | National, with highest burden in Moscow, Saint Petersburg, Tatarstan | Medium term (2-4 years) |

| Government screening and reimbursement programs | +1.8% | National, federal project covers 90 regional + 155 interregional endocrinology centers | Short term (≤ 2 years) |

| Adoption of CGM supported by new reimbursement codes | +2.5% | National, prioritizing children aged 2-17 and pregnant women | Medium term (2-4 years) |

| Expansion of e-commerce and pharmacy chains | +1.3% | National, with Moscow and Saint Petersburg accounting for 36-39% of online orders; Far East regions (Khabarovsk, Primorsky, Amur) show highest penetration | Short term (≤ 2 years) |

| Domestic sensor manufacturing initiatives | +1.0% | National, concentrated in Zelenograd (Elta), Tula (NOVA), KorolevPharm (Diacont) | Long term (≥ 4 years) |

| Integration with Russia's Unified Medical Information System | +0.8% | National, mandatory for AI-enabled devices per Ministry of Health Order No. 181n | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Prevalence And Earlier Onset

Russia logged roughly 6 million diagnosed cases in 2025, yet epidemiology models place the real figure closer to 12 million, exposing a 50% diagnostic gap the federal screening program aims to close. Type 2 mortality rose 63.5% during the same period, while type 1 mortality fell 38%, signaling that structured home and hospital monitoring protocols favor insulin-dependent cohorts. Despite guidelines recommending four daily measurements for type 1 and three for type 2, regional budgets in Tatarstan funded free strips only for 5,219 insulin users, forcing 107,810 patients to self-purchase packs. This affordability gap underpins long-run volume growth for lower-cost CGM consumables once reimbursement scales beyond pediatric and pregnancy groups.

Government Screening And Reimbursement Programs

A November 2024 federal outlay of 5.5 billion RUB modernized 90 regional and 155 inter-regional endocrinology centers with HbA1c analyzers and CGM systems. More than 60,000 children and 53,000 pregnant women already receive CGM at zero out-of-pocket cost, and eleven separate CGM product lines currently hold Roszdravnadzor registration numbers. The July 1 2026 transition to centralized procurement aggregates regional tenders into one federal envelope that will compress sensor prices, but an announced 13% rollback, in the “Combating Diabetes Mellitus” budget threatens to curtail adult coverage.

Adoption Of CGM Supported By New Reimbursement Codes

GOST R 72213-2025, effective January 1 2026, demands MARD ≤15%, stability for at least 14 days, and ≥15,000 paired measurements in domestic clinical trials, giving manufacturers clear technical targets. Complementary Ministry of Health Order 181n obliges every AI-enabled device to push data to the Roszdravnadzor repository as a condition of marketing. A cost-utility study found the incremental cost-effectiveness ratio of remote CGM at RUB 3.1 million (USD 0.04 million) per life-year, below the RUB 4.1 million (USD 0.05 million) willingness-to-pay ceiling, offering economic validation for expansion[1]Dmitry Laptev et al., “Remote glycemic control…,” Problems of Endocrinology, probl-endojournals.ru. Implementation gaps persist; 7,000 Moscow adults were denied sensors in spring 2025 despite medical approvals, reflecting administrative bottlenecks.

Expansion of E-Commerce and Pharmacy Chains

Russia counts roughly 77,000 brick-and-mortar pharmacies, 91.7% of which are chain owned. Legalization of electronic prescriptions for antibiotics, antivirals, and hormones in 2025 broadened digital uptake, and buy-online-pickup-in-store orders rose from 8% in 2023 to 18% in 2024. Embedded finance via buy-now-pay-later (BNPL) lifted average diabetes-device ticket sizes at Rigla chain stores by 110% in January 2025. Far-East oblasts exhibited online pharmacy penetration up to 2.25 times their internet-audience share because physical pharmacy density is low, underscoring e-commerce’s role in geographic equalization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High out-of-pocket costs for advanced devices | -1.4% | National, most acute in regions with lower per-capita income (Tatarstan, North Caucasus, Siberia) | Short term (≤ 2 years) |

| Regulatory approval delays and frequent changes | -0.9% | National, Roszdravnadzor registration timelines up to 120 business days | Medium term (2-4 years) |

| Supply-chain disruptions caused by sanctions | -1.2% | National, affecting all import-dependent devices | Short term (≤ 2 years) |

| Data-sovereignty driven cloud-data privacy concerns | -0.6% | National, compliance costs highest for foreign vendors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Out-Of-Pocket Costs For Advanced Devices

Adult patients outside disability registers pay RUB 3,500-4,320 (USD 37-46) per 14-day CGM sensor, equating to RUB 100,800-124,416 (USD 1,062-1,311) annually, unaffordable for pensioners whose median income is RUB <20,000 per month[2]Russian Government Procurement Portal, “Regional CGM Tender Data 2024-2025,” zakupki.gov.ru . Planned federal cuts of RUB 8.4 billion (USD 0.11 billion) will narrow eligibility, further enlarging the self-pay cohort. BNPL financing covers only three-to-six-month installments, solving cash-flow but not lifetime affordability.

Regulatory Approval Delays And Frequent Changes

Roszdravnadzor registration can consume 120 business days and fines reach RUB 1 million (USD 0.013 million) for documentation errors. New pediatric-cohort trial mandates under GOST R 72213-2025 prolong time-to-market, while software audit obligations introduced by MOH Order 181n add an extra three-to-six months.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Technology Shift From SMBG To CGM

Self-monitoring blood glucose devices maintained a 55.18% revenue share in 2025, yet the Russia blood glucose monitoring devices market size for CGM technology is projected to climb at a 12.22% CAGR through 2031. The Russia blood glucose monitoring devices market share in consumable test strips remains high because guidelines prescribe up to four finger-stick readings daily, but provincial rationing still limits free supply to <5% of diagnosed cases. Commoditization pressures push glucometer kits down to 1,550 RUB retail, compressing margins for domestic incumbents Elta, Diacont, and Arkray.

The CGM subsector represented the remaining 44.82% in 2025, with sensors driving recurring revenue given a standard 14-day replacement rate. Abbott’s Libre family dominates, yet Chinese brand Sinocare secured Roszdravnadzor approval (RZN 2024/23862) in April 2025 and now targets federal procurement. A pediatric trial of Medtronic’s MiniMed 780G hybrid loop cut median HbA1c from 7.1% to 6.6% over one year, underscoring clinical demand if supply stabilizes.

By End User: Rapid Home-Care Uptake

Hospitals captured 47.21% of 2025 spend because 1,100 inpatient laboratories received HbA1c analyzers during the federal upgrade program. The home-care setting will, however, exhibit an 11.65% CAGR through 2031 as UMIS-linked Bluetooth glucometers demonstrated a jump from 10.91% to 26.06% HbA1c goal attainment in 180 days.

Diagnostic centers now hold the smallest share; expansions of hospital labs erode standalone demand. Yet policy gaps, 7,000 approved Moscow adults left without sensors in 2025, constrain migration from institutional to community channels. Infrastructure weaknesses surfaced when November 2024 internet outages blocked CGM apps statewide, illustrating that home-care scalability depends on network resilience.

By Distribution Channel: Online Acceleration

Retail pharmacies delivered 45.32% of revenue in 2025, but the Russia blood glucose monitoring devices market anticipates a 13.12% CAGR for online pharmacies after prescription digitization widened permissible SKUs. Chain ownership of 91.7% of outlets equips retailers with last-mile capacity; BNPL at Rigla increased average transaction value by 110% in early 2025.

Hospital pharmacies occupy the smallest share yet may gain once centralized tenders launch on July 1 2026, consolidating purchasing under a single federal buyer. Parallel import mark-ups above 50% still channel CGM transactions toward marketplaces that enable rapid price comparison, though warranty voidance remains a deterrent for some consumers.

Geography Analysis

Federal spending concentrates equipment upgrades in Moscow and Saint Petersburg, yet Far-East oblasts such as Khabarovsk, Primorsky, and Amur show e-commerce penetration up to 2.25 times their internet-user share, revealing latent demand where brick-and-mortar density is sparse. Imports arrive mainly via Kazakhstan, Belarus, and Turkey, inflating sticker prices more acutely in North Caucasus and Siberia, regions that already report lower per-capita income[3]U.S. Bureau of Industry and Security, “License Exception MED,” bis.doc.gov .

Domestic production centers cluster in Zelenograd, Tula, and Korolev; Elta’s new CGM line positions Technopolis Moscow as a future export hub once localization surpasses the 50% public-procurement threshold. Still, the Russia blood glucose monitoring devices market remains 75-80% dependent on imports, a vulnerability formalized by a 149.8 import-to-output ratio in 2024.

Centralized procurement scheduled for July 1 2026 will equalize device specifications across Russia’s 85 federal subjects, lowering price variance but also centralizing supply-chain risk. Budget pressure looms: an 8.4 billion RUB cut threatens provincial allocations, especially outside the two capital cities, so online channels and domestic suppliers able to undercut Western pricing could expand fastest.

Competitive Landscape

The Russia blood glucose monitoring devices market is fragmented. Abbott Diabetes Care captured the majority of CGM retail sales, granting it scale leverage during the upcoming federal tender. Domestic trio Elta, Diacont, and Arkray compete mainly in low-margin SMBG strips and lancets but now invest in sensor R&D to comply with GOST R 72213-2025.

White-space growth lies with adult type 2 diabetics, who currently self-fund glucose monitoring. Sensors priced below 3,000 RUB and bundled with installment plans could penetrate this segment once accredited. The student-engineered wireless insulin pump from Moscow Aviation Institute, now entering trials, exemplifies how university spin-outs may disrupt incumbent pump-CGM ecosystems by 2027.

Russia Blood Glucose Monitoring Devices Industry Leaders

Abbott Diabetes Care

Roche Holding AG

LifeScan

Dexcom Inc.

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Ministry of Digital Development pledged that remote glucose monitoring services will stay operational during any future mobile-data restrictions.

- January 2026: Moscow Aviation Institute unveiled the first Russian smartphone-controlled wireless insulin pump and slated clinical trials within 12 months.

Russia Blood Glucose Monitoring Devices Market Report Scope

As per the scope of the report, blood glucose monitoring devices are medical tools used to measure and track the level of glucose (sugar) in a person's blood. These devices help individuals with diabetes or other health conditions manage their blood sugar levels effectively by providing real-time or periodic readings.

The segmentation for the Russia blood glucose monitoring devices market is categorized by product type, end user, and distribution channel. By product type, it includes self-monitoring blood glucose devices such as glucometers, test strips, and lancets, along with continuous glucose monitoring devices comprising sensors and durables (receivers and transmitters). By end user, the market is segmented into hospitals, home care settings, and diagnostic centers. By distribution channel, it is divided into retail pharmacies, online pharmacies, and hospital pharmacies. The market forecasts are provided in terms of value (USD).

By Product Type

| Self-monitoring Blood Glucose Devices | Glucometer Devices |

| Test Strips | |

| Lancets | |

| Continuous Glucose Monitoring Devices | Sensors |

| Durables (Receivers & Transmitters) |

By End User

| Hospitals |

| Home Care Settings |

| Diagnostic Centers |

By Distribution Channel

| Retail Pharmacies |

| Online Pharmacies |

| Hospital Pharmacies |

| By Product Type | Self-monitoring Blood Glucose Devices | Glucometer Devices |

| Test Strips | ||

| Lancets | ||

| Continuous Glucose Monitoring Devices | Sensors | |

| Durables (Receivers & Transmitters) | ||

| By End User | Hospitals | |

| Home Care Settings | ||

| Diagnostic Centers | ||

| By Distribution Channel | Retail Pharmacies | |

| Online Pharmacies | ||

| Hospital Pharmacies | ||

Key Questions Answered in the Report

What is the projected value of the Russia blood glucose monitoring devices market in 2031?

It is forecast to reach USD 959.95 million by 2031, expanding at an 8.9% CAGR from 2026 to 2031.

Which product category is growing fastest through 2031?

Continuous glucose monitoring devices hold the leading 12.22% CAGR through 2031 due to federal reimbursement expansion and the new GOST R 72213-2025 standard.

How big was the self-monitoring blood glucose segment in 2025?

Self-monitoring products captured 55.18% of 2025 revenue, benefiting from a vast installed base of glucometers and test strips.

What share of spending did hospitals control in 2025?

Hospitals contributed 47.21% to overall revenue in 2025 but will be overtaken in growth pace by the home-care setting post-2026.

Page last updated on: