Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

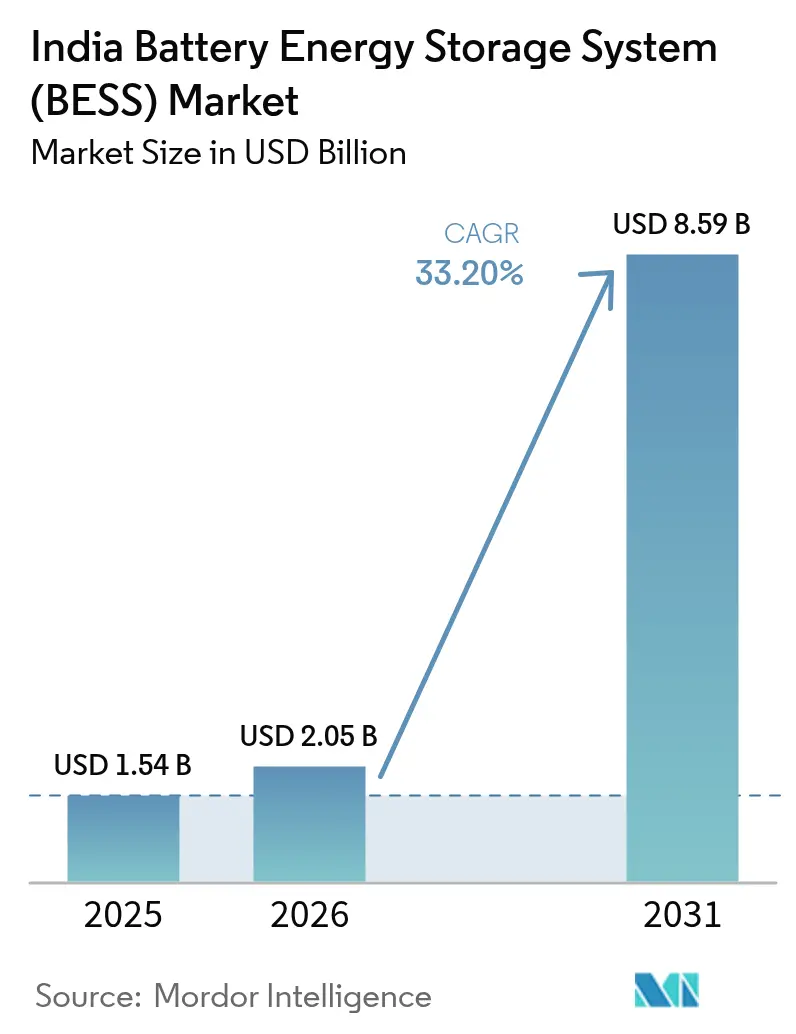

| Base Year Market Size (2025) | USD 1.54 Billion |

| Market Size (2026) | USD 2.05 Billion |

| Market Size (2031) | USD 8.59 Billion |

| Growth Rate (2026 - 2031) | 33.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Battery Energy Storage System (BESS) Market Analysis by Mordor Intelligence

The India Battery Energy Storage System Market size was valued at USD 1.54 billion in 2025 and estimated to grow from USD 2.05 billion in 2026 to reach USD 8.59 billion by 2031, at a CAGR of 33.2% during the forecast period (2026-2031).

Rapid renewable additions, sovereign incentives, and falling lithium-ion costs are tightening the gap between intermittent generation and grid-balancing capacity. The Central Electricity Authority projects a 47 GW storage need by 2030, yet installed grid-scale capacity was under 1 GW in early 2024, prompting utilities to accelerate procurement through multi-hour standalone tenders.(1)Ministry of New and Renewable Energy, “BESS Capacity Status 2024,” mnre.gov.in Policy support includes a Production Linked Incentive pool of INR 18,100 crore for domestic cells, a Viability Gap Funding grant covering up to 40% of standalone BESS capex, and rising Energy Storage Obligations that compel DISCOMs to source a share of supply from storage-backed contracts. At the same time, lithium-iron-phosphate pack prices slipped below USD 100 per kWh in 2024, bringing levelized storage costs to around INR 5 per kWh in high-cycle projects.(2)BloombergNEF, “Lithium-Ion Battery Pack Prices Hit Record Low,” about.bnef.com These factors position the India battery energy storage systems market for an expansion that outpaces underlying renewable capacity growth.

Key Report Takeaways

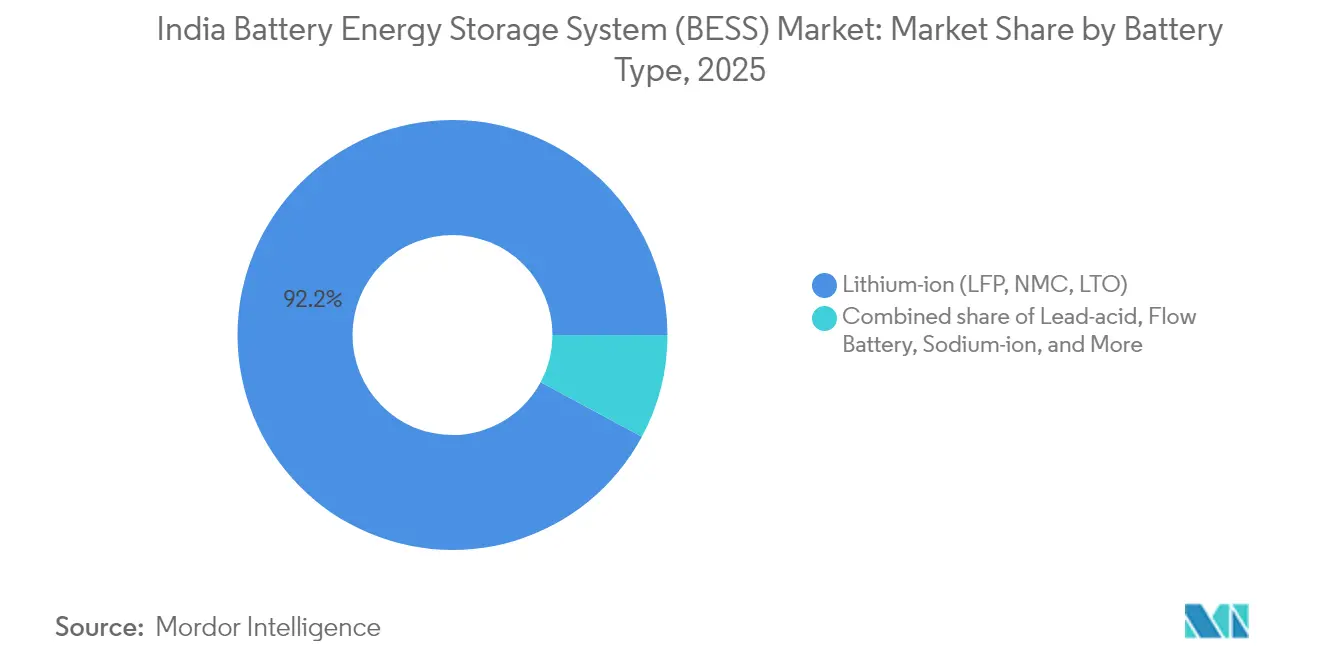

- By battery type, lithium-ion batteries captured 92.15% of India's battery energy storage systems market share in 2025 and are projected to advance at a 35.2% CAGR through 2031.

- By connection type, on-grid utility installations led with 78.30% share in 2025, while off-grid deployments are set to grow at a 36.9% CAGR to 2031.

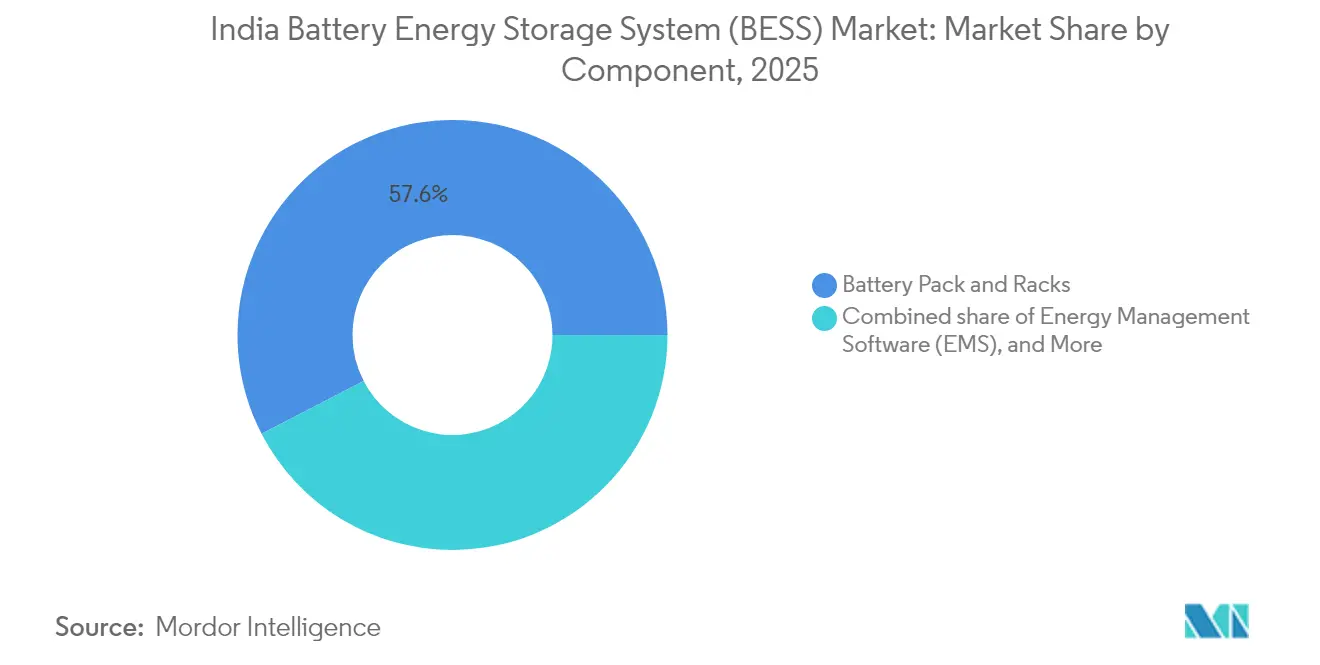

- By component, battery packs and racks commanded 57.60% of the India battery energy storage systems market size in 2025; energy-management software is projected to expand at a 38% CAGR to 2031.

- By capacity range, the 10-100 MWh segment accounted for 47.00% of the India battery energy storage systems market size in 2025, whereas projects exceeding 500 MWh are forecast to post a 38.6% CAGR to 2031.

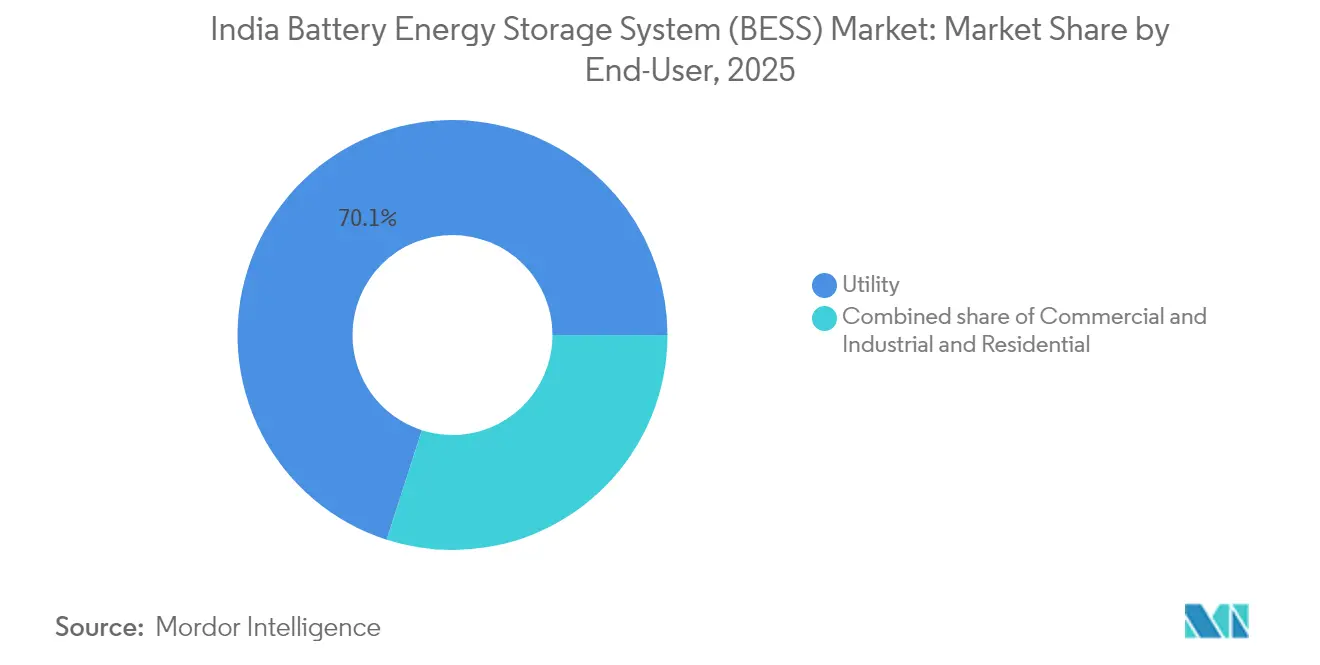

- By end user, utilities accounted for 70.05% of the revenue in 2025; commercial and industrial customers showed the fastest uptake at a 36.2% CAGR through 2031.

- By geography, Rajasthan led with 280 MWh of operating capacity in 2024; Gujarat is the fastest-growing state, with pipeline awards exceeding 1,500 MWh.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Battery Energy Storage System (BESS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining lithium-ion battery costs | 8.50% | National; early benefits in Gujarat, Rajasthan, Karnataka | Medium term (2-4 years) |

| Government VGF and PLI incentives | 7.20% | National; centered on manufacturing hubs in Gujarat and Tamil Nadu | Short term (≤ 2 years) |

| 500 GW renewables target creates storage gap | 9.30% | National; led by solar-rich Rajasthan, Gujarat, Andhra Pradesh | Long term (≥ 4 years) |

| Mandatory Energy Storage Obligation for DISCOMs | 6.10% | National; phased in Rajasthan, Maharashtra, Karnataka | Medium term (2-4 years) |

| Surge of multi-hour standalone tenders | 5.80% | National; anchored by SECI | Short term (≤ 2 years) |

| Peak-tariff arbitrage for C&I and data centers | 4.90% | Urban and industrial clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining Lithium-Ion Battery Costs

Lithium iron phosphate cell prices fell to USD 89 per kWh in Q2 2024, 14% below the 2023 level, after Chinese gigafactories ramped up their output and cathode chemistries improved. The drop cut the capex of a 100 MWh utility project from USD 40 million in 2022 to about USD 30 million in 2024, pushing levelized storage costs below INR 5 per kWh in high-utilization nodes. Developers have locked in multi-year supply contracts with CATL and BYD, covering 68% of imported cells in 2024, thereby insulating near-term projects from price spikes.(3)Press Information Bureau, “Production Linked Incentive for ACC Batteries,” pib.gov.in LFP’s 6,000-cycle life aligns with 25-year PPAs, minimizing mid-life replacement risk.(4)Tata Power, “Annual Report 2024,” tatapower.com Although lithium carbonate hit USD 85,000 per tonne in early 2024 before easing to USD 12,000, most Indian bids now include indexation clauses that hedge raw-material volatility.

Government VGF & PLI Incentives

The Ministry of Power’s Viability Gap Funding, launched in June 2023, offers a one-time grant up to 40% of the eligible standalone BESS capex, capped at INR 6.6 crore per MW. By September 2024, the scheme had sanctioned 1,200 MWh across eight projects, valued at INR 4,800 crore, catalyzing USD 580 million of private equity investment.(5)Press Information Bureau, “Production Linked Incentive for ACC Batteries,” pib.gov.in In parallel, the PLI program for advanced-chemistry cells provides a 6% sales incentive for five years, contingent on 50% local value addition and 5 GWh minimum capacity; Reliance, Ola Electric, and Rajesh Exports secured 50 GWh of awards in 2024 with first production targeted for late 2025. These levers shrink the landed-cost differential between imported and domestic cells from 22% in 2023 to a projected 8% by 2027.

500 GW Renewables Target Creates Storage Gap

India’s pledge to add 500 GW of non-fossil capacity by 2030, up from 180 GW in 2024, implies annual solar and wind additions of nearly 45 GW. The grid requires four-hour storage for at least 10% of incremental capacity, or 47 GW/188 GWh cumulatively, yet operating BESS stood below 1 GW in early 2024. The Solar Energy Corporation of India tendered 13 GWh of standalone systems in 2024, with tariff caps of approximately INR 5.75 per kWh. Rajasthan issued a 1,000 MWh procurement in March 2024, specifying a one-second response, which implicitly favors lithium-ion chemistries. Evening ramp rates of 15-20 GW compel coal plants to cycle inefficiently, adding INR 12,000 crore in annual system costs, a gap BESS can monetarily bridge through capacity and energy payments.

Mandatory Energy Storage Obligation for DISCOMs

Rajasthan mandated that DISCOMs source 1% of supply from storage-backed contracts in FY 2024-25, rising to 3% by FY 2026-27. Maharashtra and Karnataka issued similar rules in October 2024, starting at 0.5% and 0.75%, respectively. Non-compliance penalties of INR 1-2 per kWh make it cheaper to contract BESS even at tariffs above marginal generation costs. A tradable storage-certificate market enables over-procured DISCOMs to sell their surplus obligations, thereby creating liquidity. Jaipur DISCOM’s November 2024 agreement for 50 MW/200 MWh, priced at INR 5.85 per kWh, represents an early cost-effectiveness, as it offers a discount to the INR 7.20 per kWh evening tariff.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Asset-class and tariff-cap ambiguity | -4.30% | National; acute where no BESS policy exists | Medium term (2-4 years) |

| Import-heavy battery supply chain | -3.70% | National; steeper in remote zones | Short term (≤ 2 years) |

| Tender undersubscription and execution delays | -2.90% | National; pronounced in weak DISCOM states | Short term (≤ 2 years) |

| Geopolitical critical-minerals risk | -2.20% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Asset-Class & Tariff-Cap Regulatory Ambiguity

Cost-recovery rules vary by state, with some classifying BESS as a form of generation, while others classify it as a form of transmission. Where BESS is involved in tagged transmission, returns depend on regulated tariffs set 12-18 months after expenditure, which deters equity investors who seek stable cash flows. Draft national guidelines proposed a separate asset class with cost-plus tariffs, but the final rules were still pending as of late 2024. SECI tariff caps, between INR 5.50 and INR 6.00 per kWh, squeeze returns when the weighted average cost of capital exceeds 11%. Lenders request DSCR above 1.4x, implying breakeven tariffs closer to INR 6.50 per kWh. Uncertainty persists in Uttar Pradesh, Bihar, and West Bengal, where no BESS orders clarify wheeling or banking charges.

Import-Heavy Battery Supply Chain Raises Capex

India imported 85% of cells in 2024, adding 18-22% to landed costs through customs duty, GST, freight, and working capital. The basic customs duty on cells is 10% plus 18% GST, while concessional duty routes require advance authorization, which extends procurement by two months. Freight from Shenzhen to Mumbai averaged USD 4,200 per container in 2024, amid Red Sea diversions, compared to USD 1,800 in 2022. Last-mile haulage to desert sites incurs an additional USD 50-80 per kWh due to the use of specialized, shock-resistant trailers. First-generation Indian cell plants are likely to operate at 60-70% of the cost efficiency of Chinese plants until they reach a 10 GWh output, maintaining high near-term import reliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Lithium-Ion Dominance Anchors Grid-Scale Shift

Lithium-ion batteries held 92.15% of the installed capacity in 2025, with LFP accounting for 75% due to their 6,000-cycle life and intrinsic thermal stability, which is critical for desert climates. NMC’s share slipped to 17% as developers prioritized lifecycle cost over energy density. Lithium titanate remains a niche option under 1% for ultra-fast response markets, while lead-acid fell to 4.2% because its 1,500-cycle life no longer offsets capital expenditure savings. Flow and sodium-ion chemistries together make up 2.6% but offer long-duration potential once costs fall.

As prices drop, the Indian battery energy storage systems market expects lithium-ion to cement its lead, though pilot flow batteries, such as Reliance’s 50 MWh vanadium unit, test seasonal storage economics. Developers favor LFP because passive air cooling reduces balance-of-system spend by 12-15%. Lithium-ion’s modularity also speeds construction timelines, a key factor in meeting SECI’s tight commissioning schedules.

By Connection Type: Off-Grid Hybrids Outpace Utility Deployments

Off-grid and microgrid installations are projected to grow at a 36.9% annual rate as telecom towers, mines, and island grids replace diesel generators with solar-plus-storage hybrids. Bharti Airtel’s 2,500-site rollout saved 18 million liters of diesel in 2024 and reduced operating expenses (opex) by INR 140 crore. Nevertheless, on-grid systems still comprise 78.30% of the 2025 capacity, driven by SECI tenders and ancillary services revenues. The Indian battery energy storage systems market balance is expected to tilt gradually toward distributed assets as virtual power plant software enables the aggregation of smaller systems into grid services.

By Component: Software Gains as Hardware Commoditizes

Battery packs and racks supplied 57.60% of India's battery energy storage systems market value in 2025, but face margin compression from Chinese scale economies. In contrast, energy-management software revenue is climbing at a 38% CAGR as utilities demand predictive algorithms that stack arbitrage, frequency, and capacity payments. Cyber-security mandates under draft guidelines IEC 62351 elevate software requirements, giving incumbents with encryption and intrusion-detection capabilities an edge.

By Energy Capacity Range: Gigawatt-Hour Projects Reshape Procurement

Tenders above 500 MWh are the fastest-growing segment, expanding 38.6% annually due to economies of scale that reduce the per-MWh capital expenditure (capex) from USD 350,000 at 100 MWh to USD 280,000 at 1,000 MWh. Mid-scale 10-100 MWh projects still held 47.00% share in 2025, aligning with DISCOM obligations and SECI’s standard bid blocks. Below 10 MWh, growth is tied to C&I tariffs; a daily-cycling 1 MWh unit can save INR 20 lakh annually in Maharashtra’s time-of-day tariff regime.

By End-User Application: C&I Arbitrage Drives Distributed Adoption

Utilities owned 70.05% of the capacity in 2025, but C&I uptake is rising at a rate of 36.2% per year, as peak tariffs diverge from off-peak rates by INR 6 per kWh in some states. Data centers shift from diesel gensets to lithium-ion BESS, improving sustainability credentials and uptime. Residential adoption remains below 3% due to the high upfront cost; yet, pilot subsidies in Kerala and Tamil Nadu are shortening paybacks to six years.

Geography Analysis

Rajasthan, Gujarat, Karnataka, and Maharashtra contributed 67.80% of the national capacity in 2025. Rajasthan leads with 280 MWh, anchored by Tata Power’s 100 MW/200 MWh Jaisalmer system that charges at INR 2.50 per kWh and discharges near INR 7.00 during evening peaks. Gujarat follows at 220 MWh, leveraging the Dholera Solar Park and upcoming offshore wind, while Adani’s 40 MW/120 MWh BESS delivers round-the-clock power at INR 5.95 per kWh.

Karnataka and Tamil Nadu deploy storage to curb renewable curtailment; Karnataka alone curtailed 1,200 GWh in 2024, prompting JSW Energy’s 120 MWh hybrid installation that shifts midday solar into evening load. Tamil Nadu floated a 500 MWh tender targeting six-hour wind reshaping for coastal industrial clusters. Andhra Pradesh offers a 10% capital subsidy and waives wheeling charges to reach 2 GWh by 2027. Northern and eastern states trail due to weaker DISCOM balance sheets and limited renewable energy sources. Uttar Pradesh has only 40 MWh of operating BESSs and lacks a clear cost-recovery mechanism, while Bihar and West Bengal lack policies specific to BESSs. In isolated grids, the Andaman & Nicobar Islands piloted 15 MWh of solar-plus-storage to replace diesel at INR 18 per kWh generation cost.

Competitive Landscape

The Indian battery energy storage systems market is moderately fragmented; the top five players held roughly 45% share in 2024. Indian conglomerates, such as Tata Power, Adani Energy Solutions, JSW Energy, and Reliance New Energy, leverage their large balance sheets to bid aggressively, sometimes accepting tariffs 5-8% below those of international developers to secure 25-year PPAs. Global integrators Fluence, Hitachi Energy, and Siemens Energy differentiate through turnkey EPC, proprietary EMS, and bankable performance warranties; Fluence's Mosaic platform is active in 400 MWh of Indian assets.

Battery makers CATL, BYD, LG Energy Solution, and Panasonic move downstream through supply-and-service agreements; CATL's 5 GWh deal with ReNew Power bundles cells, fire suppression, and 10-year performance guarantees. Domestic assembly entrants Ola Electric and Exide Energy Solutions are ramping up PLI-supported factories targeting both the EV and stationary segments. The technology edge is shifting to software; Delta Electronics' cloud-based EMS aggregates distributed C&I assets into virtual power plants that earn INR 2-3 per kWh through demand response. Long-duration and behind-the-meter niches present opportunities. Reliance's 50 MWh vanadium flow pilot assesses the economics of eight-hour discharge. Cybersecurity compliance under forthcoming IEC 62351 rules favors vendors with embedded encryption, likely accelerating consolidation around platforms that can meet utility audit requirements.

India Battery Energy Storage System (BESS) Industry Leaders

Tata Power Renewable Energy Ltd.

AES Corporation (Fluence JV)

Reliance New Energy Ltd.

Exide Energy Solutions Ltd.

Amara Raja Energy & Mobility Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Adani Energy Solutions commissioned a 40 MW/120 MWh BESS in Gujarat, paired with 300 MW solar, under a 25-year PPA at INR 5.95 per kWh.

- September 2024: JSW Energy and Fluence formed a JV to deploy 500 MWh across Karnataka and Maharashtra by 2026 with a USD 150 million investment.

- September 2024: Reliance New Energy has energized a 5 MW/50 MWh vanadium flow battery in Gujarat, India, marking the country’s first utility-scale non-lithium long-duration energy storage system.

- August 2024: Tata Power commissioned a 100 MW/200 MWh standalone project in Rajasthan at INR 5.85 per kWh under a 25-year PPA.

- July 2024: Tamil Nadu GENCO issued a 500 MWh storage tender requiring six-hour discharge to time-shift nighttime wind.

- June 2024: Gujarat Energy Development Agency tendered 1,500 MWh for offshore wind integration with tariff caps at INR 6.00 per kWh.

India Battery Energy Storage System (BESS) Market Report Scope

Battery energy storage systems (BESS) are rechargeable batteries that can store and discharge energy from various sources when needed. BESS consists of one or more batteries and can be utilized to balance the electric grid, deliver backup power, and improve grid stability.

India's battery energy storage systems market is segmented by battery and connection types. The market is segmented by battery type into lithium-ion, lead-acid, flow, and other battery types. By connection type, the market is segmented into on-grid and off-grid. The market sizing and forecasts have been conducted for each segment in terms of revenue (USD).

By Battery Type

| Lithium-ion (Lithium Iron Phosphate (LFP), Nickel-Manganese-Cobalt (NMC), Lithium Titanate (LTO)) |

| Lead-acid |

| Flow Battery (Vanadium Redox, Zinc-Bromine) |

| Sodium-ion |

| Other Battery Technologies (NiCd, Hybrid Super-capacitors) |

By Connection Type

| On-Grid (Utility Interconnected) |

| Off-Grid (Micro-Grid, Hybrid) |

By Component

| Battery Pack and Racks |

| Power Conversion System (PCS) |

| Energy Management Software (EMS) |

| Balance-of-Plant and Services |

By Energy Capacity Range

| Below 10 MWh |

| 10 to 100 MWh |

| 100 to 500 MWh |

| Above 500 MWh |

By End-user Application

| Utility |

| Commercial and Industrial |

| Residential |

| By Battery Type | Lithium-ion (Lithium Iron Phosphate (LFP), Nickel-Manganese-Cobalt (NMC), Lithium Titanate (LTO)) |

| Lead-acid | |

| Flow Battery (Vanadium Redox, Zinc-Bromine) | |

| Sodium-ion | |

| Other Battery Technologies (NiCd, Hybrid Super-capacitors) | |

| By Connection Type | On-Grid (Utility Interconnected) |

| Off-Grid (Micro-Grid, Hybrid) | |

| By Component | Battery Pack and Racks |

| Power Conversion System (PCS) | |

| Energy Management Software (EMS) | |

| Balance-of-Plant and Services | |

| By Energy Capacity Range | Below 10 MWh |

| 10 to 100 MWh | |

| 100 to 500 MWh | |

| Above 500 MWh | |

| By End-user Application | Utility |

| Commercial and Industrial | |

| Residential |

Key Questions Answered in the Report

What was the value of the India battery energy storage systems market in 2026?

The market was valued at USD 2.05 billion in 2026.

How fast is grid-scale storage expected to grow in India by 2031?

Market value is projected to reach USD 8.59 billion by 2031, posting a 33.2% CAGR.

Which battery chemistry dominates current deployments?

Lithium-ion, led by LFP, made up 92.15% of installed capacity in 2025.

Why are utilities procuring multi-hour systems above 500 MWh?

Larger projects cut per-MWh costs and provide six-hour discharge to meet evening peaks cost-effectively.

How do Viability Gap Funding grants support projects?

The scheme covers up to 40% of standalone BESS capex, lowering delivered tariffs to below INR 6 per kWh.

Which states lead deployment today?

Rajasthan and Gujarat together accounted for about 500 MWh of operational capacity in 2024.

Page last updated on: