Hydrazine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

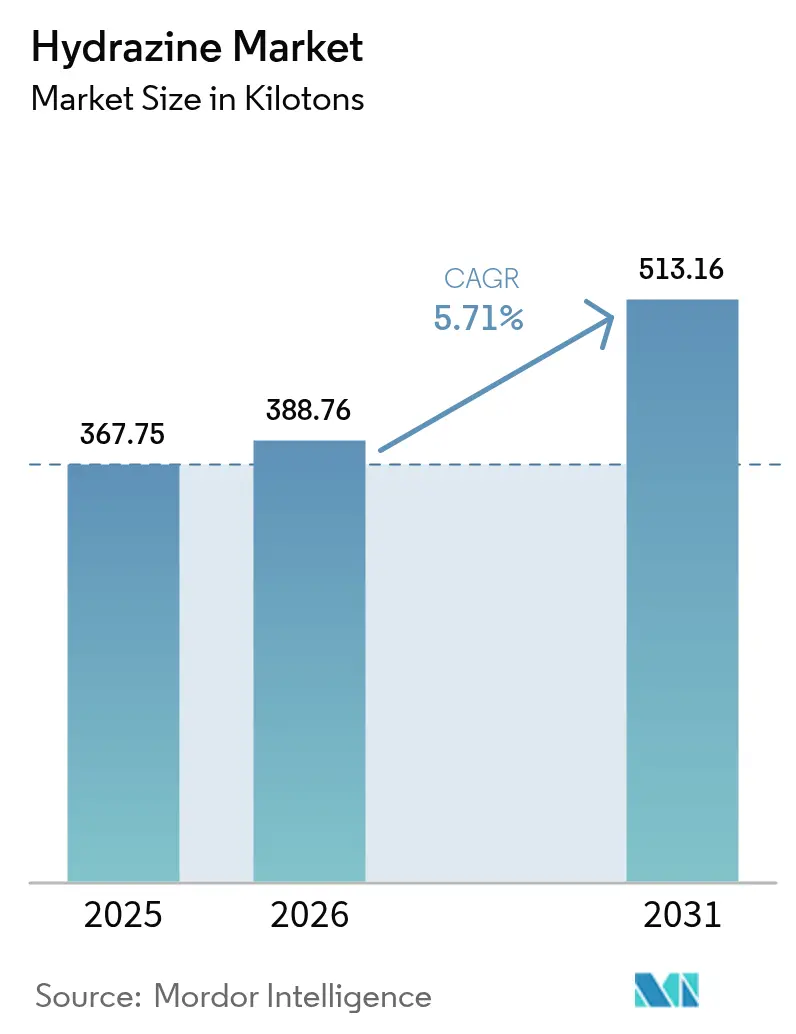

| Market Volume (2026) | 388.76 kilotons |

| Market Volume (2031) | 513.16 kilotons |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydrazine Market Analysis by Mordor Intelligence

The Hydrazine Market size was valued at 367.75 kilotons in 2025 and estimated to grow from 388.76 kilotons in 2026 to reach 513.16 kilotons by 2031, at a CAGR of 5.71% during the forecast period (2026-2031). Demand resilience stems from hydrazine’s irreplaceable role in agrochemicals, corrosion control, polymer foams, and emerging energy systems. Regulatory scrutiny in Europe and North America continues to tighten, yet capacity additions in Asia–Pacific offset potential volume losses elsewhere. Supply-side investments concentrate on safer production routes for hydrazine hydrate, while downstream users in pharmaceuticals and fuel-cell technology create fresh growth avenues. Competitive positioning focuses on vertical integration and long-term contracts to secure feedstock and manage compliance costs.

Key Report Takeaways

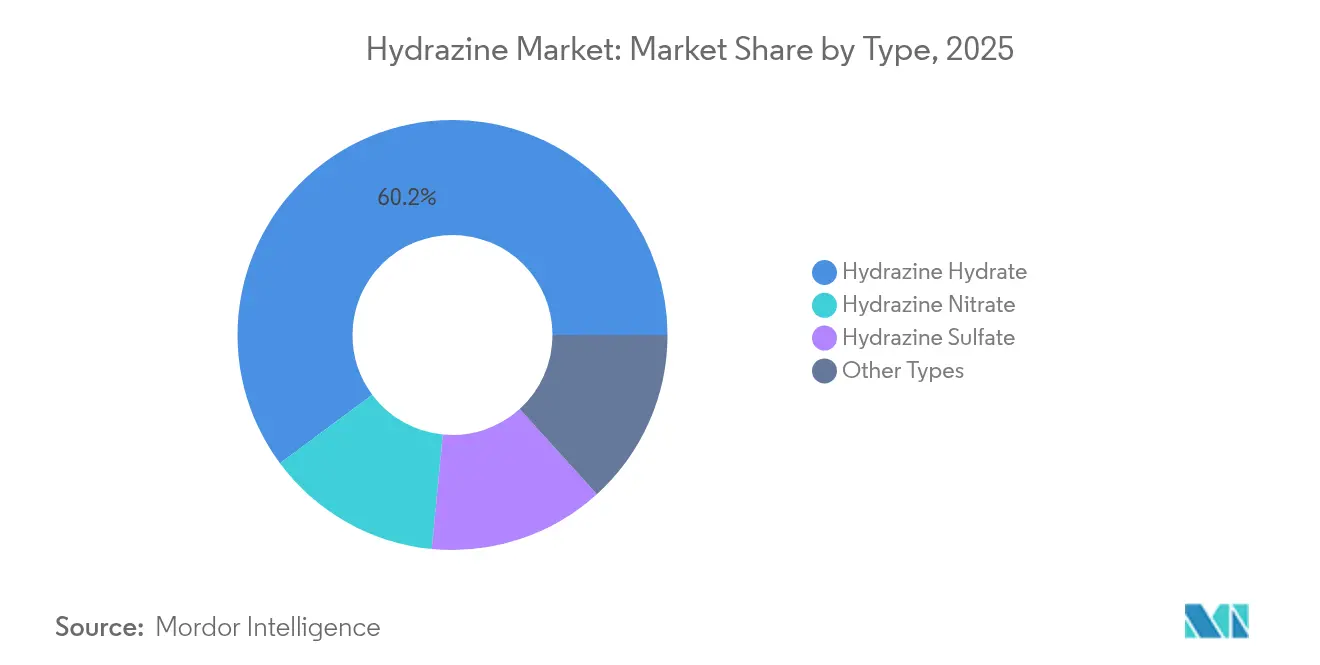

- By type, hydrazine hydrate held 60.17% of the hydrazine market share in 2025 and is expanding at a 5.89% CAGR through 2031.

- By application, corrosion inhibitors accounted for a 36.25% slice of the hydrazine market size in 2025 and are growing at 5.96% CAGR to 2031.

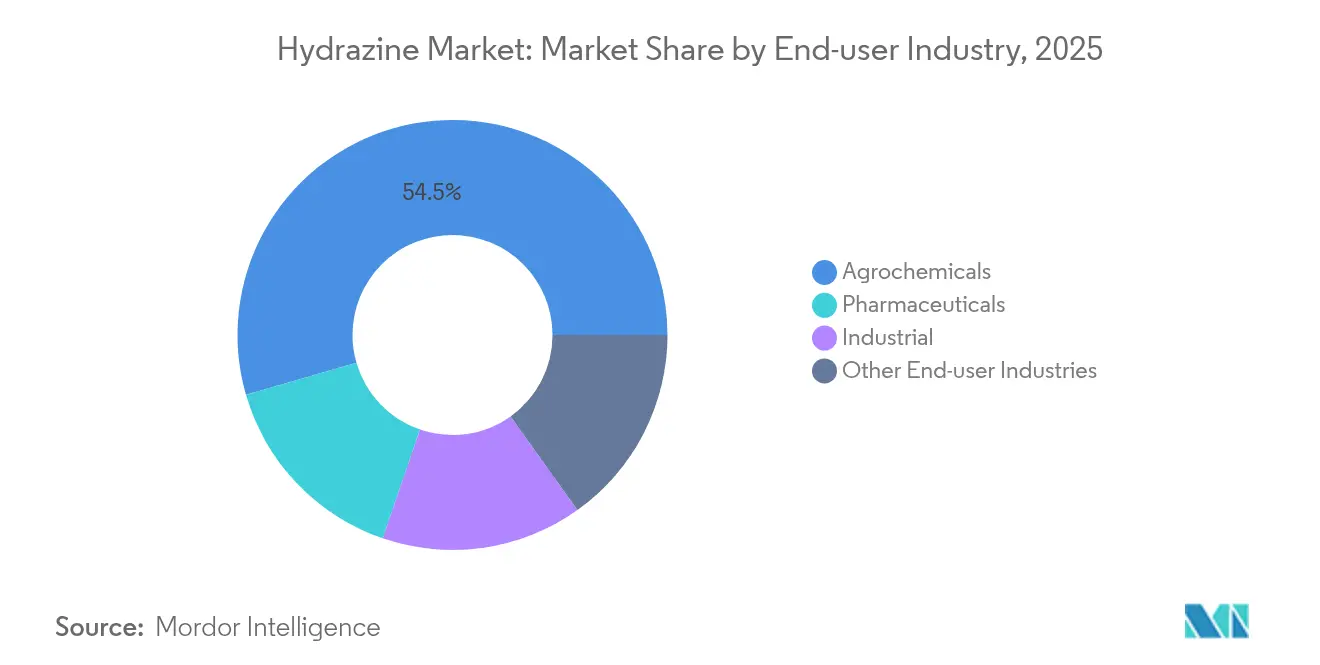

- By end-user industry, agrochemicals led with 54.49% of the hydrazine market share in 2025, whereas pharmaceuticals are advancing at a 5.98% CAGR over the same horizon.

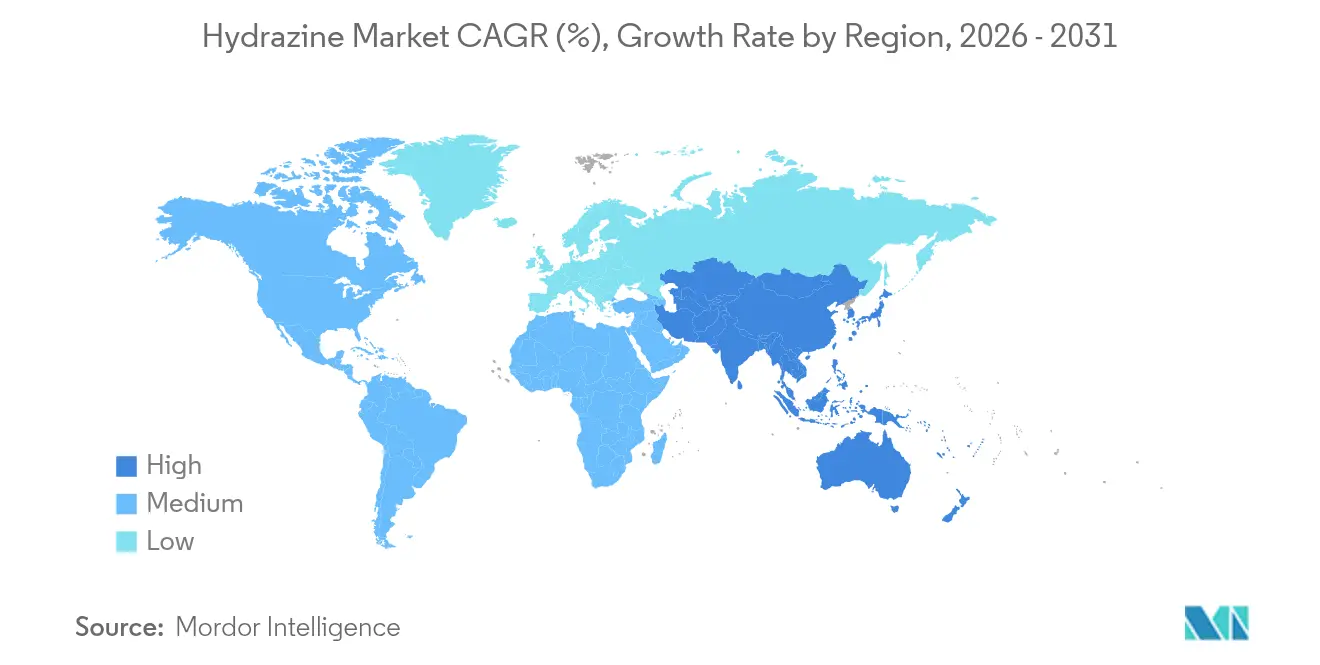

- By geography, Asia–Pacific commanded 55.51% of the 2025 volume and is forecast to register the fastest 6.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydrazine Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from agrochemicals | +1.8% | Global, with concentration in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Growing use as pharmaceutical intermediate | +1.2% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Increasing adoption as blowing agent in polymer foams | +0.9% | Global, led by Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Expansion of water-treatment infrastructure | +0.7% | Asia-Pacific core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Hydrazine-based hydrogen carrier for fuel-cell systems | +0.6% | North America and EU, with pilot projects in Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Agrochemicals

Escalating agricultural intensification in China, India, and Brazil keeps pesticide consumption high, and hydrazine remains the indispensable intermediate for maleic hydrazide, isoxazolidinone, and other growth-regulator actives. Large Chinese producers report dedicated capacities above 200,000 tons that feed both domestic and export pipelines, supporting supply security for formulating companies. Research into nano-engineered hydrazine derivatives achieves full pest mortality at lower dosage, signaling potential for reduced environmental loading while preserving efficacy. Regulatory focus on food security in these regions outweighs immediate environmental bans, thus sustaining the hydrazine market.

Growing Use as Pharmaceutical Intermediate

Hydrazine scaffolds enable the selective synthesis of anti-tubercular, anti-inflammatory, and antidepressant molecules, and recent process innovations deliver 89–97% yields under mild, solvent-efficient conditions. Clinical candidates such as pyrrole hydrazones inhibit Mycobacterium tuberculosis at therapeutic concentrations, widening demand among active pharmaceutical ingredient (API) manufacturers in the United States and India. To tackle toxicity concerns, producers are scaling indirect routes that avoid bulk hydrazine handling, yet still leverage its unique nucleophilic profile. As a result, the pharmaceutical segment is expected to remain the fastest-growing user base within the hydrazine market.

Increasing Adoption as Blowing Agent in Polymer Foams

Automotive light-weighting and building-insulation programs propel demand for azodicarbonamide and para-toluenesulfonyl hydrazide, both synthesized from hydrazine. Asia–Pacific houses the majority of PVC and EVA foam converters, translating into steady offtake for regional hydrazine suppliers. Process refinements that embed nano-dispersion technology cut required gassing agent levels without compromising cell structure, giving converters cost and sustainability advantages. Lack of functionally equivalent substitutes maintains pricing power for hydrazine-based systems.

Expansion of Water-Treatment Infrastructure

New combined-cycle gas-turbine installations in India, Indonesia, and Vietnam rely on high-pressure boilers that mandate oxygen scavengers, where hydrazine’s reactivity secures metal integrity at elevated temperatures. Desalination plants across the Middle East are also specifying hydrazine dosage for corrosion control, generating incremental demand from municipal operators. Modular dosing systems and in-line monitoring improve worker safety, supporting continued adoption despite regulatory pressure.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Highly toxic nature and tightening regulations | -1.4% | EU and North America, expanding globally | Short term (≤ 2 years) |

| Volatility in ammonia prices | -0.8% | Global, with acute impact in Asia-Pacific production hubs | Short term (≤ 2 years) |

| Shift toward green monopropellants in space | -0.5% | Global aerospace sector, led by EU and US | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Highly Toxic Nature and Tightening Regulations

Hydrazine features on the European Chemicals Agency’s Substances of Very High Concern list, triggering strict authorization and occupational exposure limits. Compliance now demands sealed transfer lines, scrubber systems, and continuous air monitoring, pushing operating costs higher for formulators across Germany, France, and the United States[1]European Chemicals Agency, “Substance Information – Hydrazine,” echa.europa.eu. Liability linked to liver toxicity and carcinogenicity also forces insurers to raise premiums, discouraging new entrants. Although Asia–Pacific regulations are comparatively lenient today, multinational customers increasingly require global compliance, slowly extending higher safety standards worldwide.

Shift Toward Green Monopropellants in Space

Satellite integrators are migrating from hydrazine to hydroxyl-ammonium-nitrate or ammonium-dinitrimide blends that offer similar impulse with lower handling risks. The European Space Agency’s LMP-103S and NASA’s AF-M315E propulsion programs both cleared critical milestones in 2024, signaling accelerated fleet conversion[2]European Space Agency, “Considering hydrazine-free satellite propulsion,” esa.int . Private launch providers respond by phasing hydrazine ground infrastructure out of new sites, which will steadily erode demand from the aerospace vertical. However, legacy spacecraft refueling and military platforms will maintain limited hydrazine usage in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hydrazine Hydrate Dominance Reflects Handling Advantages

Hydrazine hydrate accounted for 60.17% of 2025 volume within the hydrazine market and recorded the segment-leading 5.89% CAGR outlook. Preference for aqueous grades stems from lower vapor pressure, simplified ISO-tank logistics, and smoother regulatory certification versus anhydrous material. Boiler-water treatment, polymer foaming, and API synthesis plants install dedicated hydrate storage to reduce on-site risk profiles, reinforcing demand stability. Specialty salts such as hydrazine sulfate serve electronics and analytical niches where tighter stoichiometric control is essential.

Regulators now explicitly recommend hydrate grades when feasible, catalyzing supplier investments in high-purity, low-metal formulations engineered for pharmaceutical compliance. Fuel-cell developers also gravitate toward monohydrate for liquid-carrier prototypes that balance power density with managed volatility, sustaining incremental offtake. Collectively, these trends entrench hydrazine hydrate’s leadership and shield the segment from the full force of impending restrictions on anhydrous forms, supporting the broader hydrazine market.

By Application: Corrosion Inhibition Leads Despite Pharmaceutical Momentum

Corrosion inhibitors represented 36.25% of 2025 demand and should post a 5.96% CAGR through 2031, driven by new ultrahigh-pressure boilers in Asia and the refurbishment of aging North American utilities. Hydrazine’s rapid oxygen-reduction kinetics under high temperature remain unmatched, especially in closed-loop systems where stainless steel passivation is critical. Power-sector maintenance contracts typically secure multi-year hydrazine supply, offering producers predictable baseline volumes.

Explosive and blowing-agent applications together supply resilience by tapping construction, mining, packaging, and automotive end-markets. Although rocket-fuel consumption is projected to contract under the green-propellant pivot, pharmaceutical synthesis will offset losses as pipeline molecules scale up. Emerging research on hydrazine-assisted hydrogen generation could unlock new downstream uses later in the decade, adding optionality for suppliers and safeguarding the hydrazine market size from abrupt demand shocks.

By End-User Industry: Agrochemicals Anchor Growth While Pharmaceuticals Accelerate

Agrochemicals retained a 54.49% hydrazine market share in 2025, reflecting continued reliance on hydrazine-derived maleic hydrazide, herbicide synergists, and sprout-inhibition agents. Regional pesticide regulations in China and India still permit hydrazine intermediates, allowing local formulators to offer cost-effective crop-protection products amid rising food-security priorities.

Pharmaceuticals, while smaller, deliver the top 5.98% CAGR to 2031, powered by tuberculosis, oncology, and neuropsychiatric drug development pipelines. Contract development and manufacturing organizations in India and Singapore are scaling hydrazine-dependent APIs using continuous-flow techniques that mitigate exposure risks and improve atom economy. Industrial end-users, encompassing water treatment and metal surface preparation, provide dependable offtake tied to infrastructure expansion. Together, these segments ensure diversified demand and underpin medium-term growth across the hydrazine industry.

Geography Analysis

Asia–Pacific dominated the hydrazine market with a 55.51% hydrazine market share in 2025 and is forecast to post the fastest 6.05% CAGR through 2031. China’s integrated value chain, from ammonia feedstock to downstream pesticides, confers cost leadership, while India’s pharmaceutical build-out boosts high-purity hydrate imports. Government incentives for local specialty-chemical production stimulate further capacity additions despite safety headwinds.

North America remains a mature yet evolving arena. Regulatory compliance elevates operating costs, but defense applications and corrosion-control contracts sustain baseline hydrazine consumption. The 2024 private-equity acquisition of Calca Solutions underscores investor belief in steady free cash flow and future volume support from next-generation solid rocket motor programs.

Europe confronts the stiffest hurdles as REACH authorization pressures escalate. Several mid-tier formulators have trimmed capacity or shifted sourcing to affiliates in Turkey and Eastern Europe to circumvent licensing delays. Collectively, divergent regulatory regimes create a two-speed hydrazine market in which Asia–Pacific accelerates while Europe consolidates and North America balances between risk management and strategic necessity.

Competitive Landscape

Global hydrazine supply is moderately fragmented. Strategic capital expenditure targets debottlenecking and digital process control rather than greenfield megaplants, reflecting a capital-disciplined stance in light of uncertain Western demand. Asian leaders invest in zero-discharge wastewater treatment and automated drum filling to appease rising ESG expectations from multinational buyers. The Calca Solutions deal illustrates financial appetite for assets serving regulated defense and water-treatment markets. At the same time, technology partnerships with catalyst developers explore hydrazine’s function as a hydrogen carrier, opening optionality beyond traditional domains.

Hydrazine Industry Leaders

Arkema

Lanxess

Nippon Carbide Industries Co., Inc.

Otsuka Chemical Co.,Ltd.

Yibin Tianyuan Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Research published in Materials Horizons reported hydrazine-assisted water-electrolysis achieving enhanced hydrogen output, signaling future demand from distributed energy systems.

- March 2024: AE Industrial Partners acquired Calca Solutions and announced an expansion of hydrazine capacity at Lake Charles, Louisiana, to support rising defense and aerospace contracts.

Global Hydrazine Market Report Scope

Hydrazine is an inorganic compound. It is a colorless, flammable liquid with an ammonia-like smell. Hydrazine is highly toxic unless handled in solution. Hydrazine is used in several applications, such as a precursor to polymerization catalysts, as rocket fuels, to prepare the gas precursors used in airbags, as a foaming agent in preparing polymer foams, and as a storable propellant for in-space spacecraft propulsion, and is used in pharmaceuticals and agrochemicals, among others.

The hydrazine market is segmented by type, application, end-user industry, and geography. By type, the market is segmented into hydrazine hydrate, hydrazine nitrate, hydrazine sulfate, and other types (hydrazine carbonate, etc.). By application, the market is segmented into corrosion inhibitors, explosives, rocket fuel, medicinal ingredients, precursors to pesticides, blowing agents, and other applications (foaming agents, fuels, etc.). By end-user industry, the market is segmented into pharmaceuticals, agrochemicals, industrial, and other end-user industries (water treatment, etc.). The report also covers the market size and forecasts for the market in 15 countries across the globe. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Hydrazine Hydrate |

| Hydrazine Nitrate |

| Hydrazine Sulfate |

| Other Types |

| Corrosion Inhibitor |

| Explosives |

| Rocket Fuel |

| Medicinal Ingredient |

| Precursor To Pesticides |

| Blowing Agent |

| Other Applications |

| Pharmaceuticals |

| Agrochemicals |

| Industrial |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Hydrazine Hydrate | |

| Hydrazine Nitrate | ||

| Hydrazine Sulfate | ||

| Other Types | ||

| By Application | Corrosion Inhibitor | |

| Explosives | ||

| Rocket Fuel | ||

| Medicinal Ingredient | ||

| Precursor To Pesticides | ||

| Blowing Agent | ||

| Other Applications | ||

| By End-user Industry | Pharmaceuticals | |

| Agrochemicals | ||

| Industrial | ||

| Other End-user Industries | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the hydrazine market in 2026?

The hydrazine market size reached 388.76 kilo tons in 2026.

What is the expected growth rate through 2031?

Volume is projected to expand at a 5.71% CAGR, approaching 513.16 kilo tons by 2031.

Which region leads consumption?

Asia-Pacific held 55.51% of global volume in 2025 and is also the fastest-growing region.

Which end-user segment is growing fastest?

Pharmaceuticals are forecast to rise at a 5.98% CAGR, outpacing other sectors.

What are the main regulatory headwinds?

Strict classification under EU REACH and the shift toward green monopropellants constrain future demand growth in Western markets.

Why is hydrazine hydrate preferred?

Its aqueous form lowers vapor pressure and simplifies transport, explaining its 60.17% share of 2025 demand.

Page last updated on: