Hybrid System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

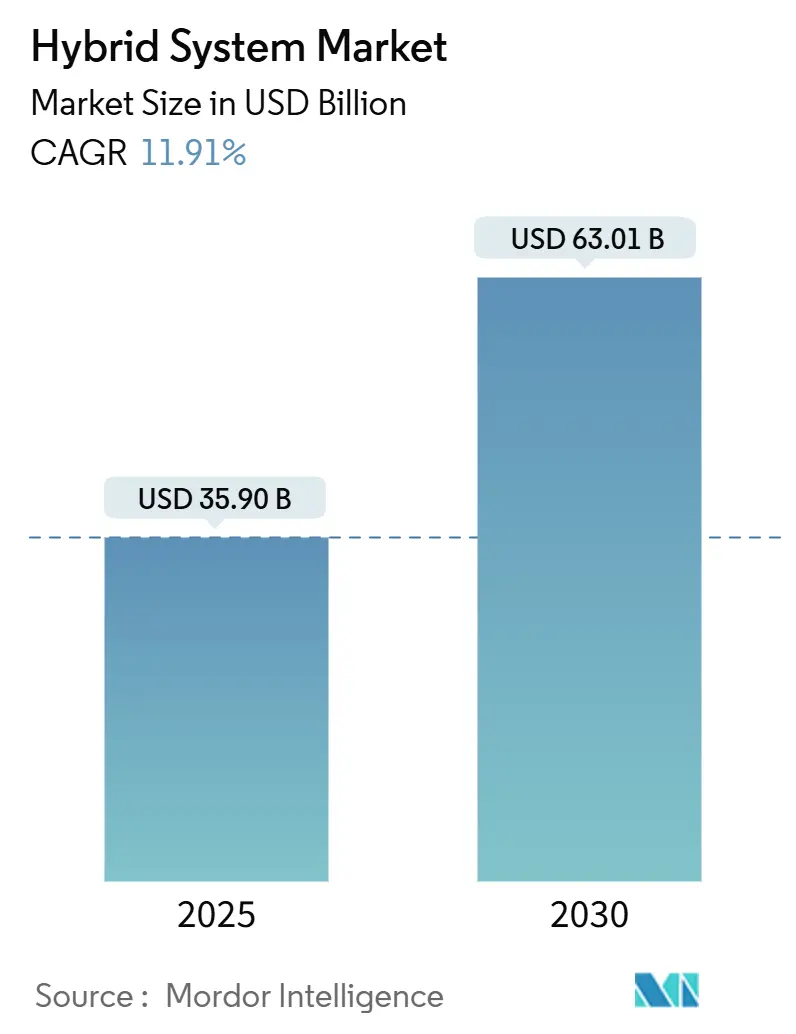

| Market Size (2025) | USD 35.90 Billion |

| Market Size (2030) | USD 63.01 Billion |

| Growth Rate (2025 - 2030) | 11.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid System Market Analysis by Mordor Intelligence

The hybrid system market size reached USD 35.90 billion in 2025 and is forecast to climb to USD 63.01 billion by 2030, reflecting an 11.91% CAGR over the period. The growth outlook benefits from a synchronized surge in vehicle electrification mandates, broader availability of consumer incentives, and sustained declines in battery pack costs. Automakers are pairing compliance strategies with strategic alliances that compress development cycles and mitigate capital risk. Consolidation among Tier-1 suppliers is streamlining component supply, and vertical integration by leading Asian manufacturers is shrinking production costs. The competitive field is also expanding into software-enabled revenue models that monetize bi-directional power flow, setting the stage for ancillary income streams that can offset upfront drivetrain premiums.

Key Report Takeaways

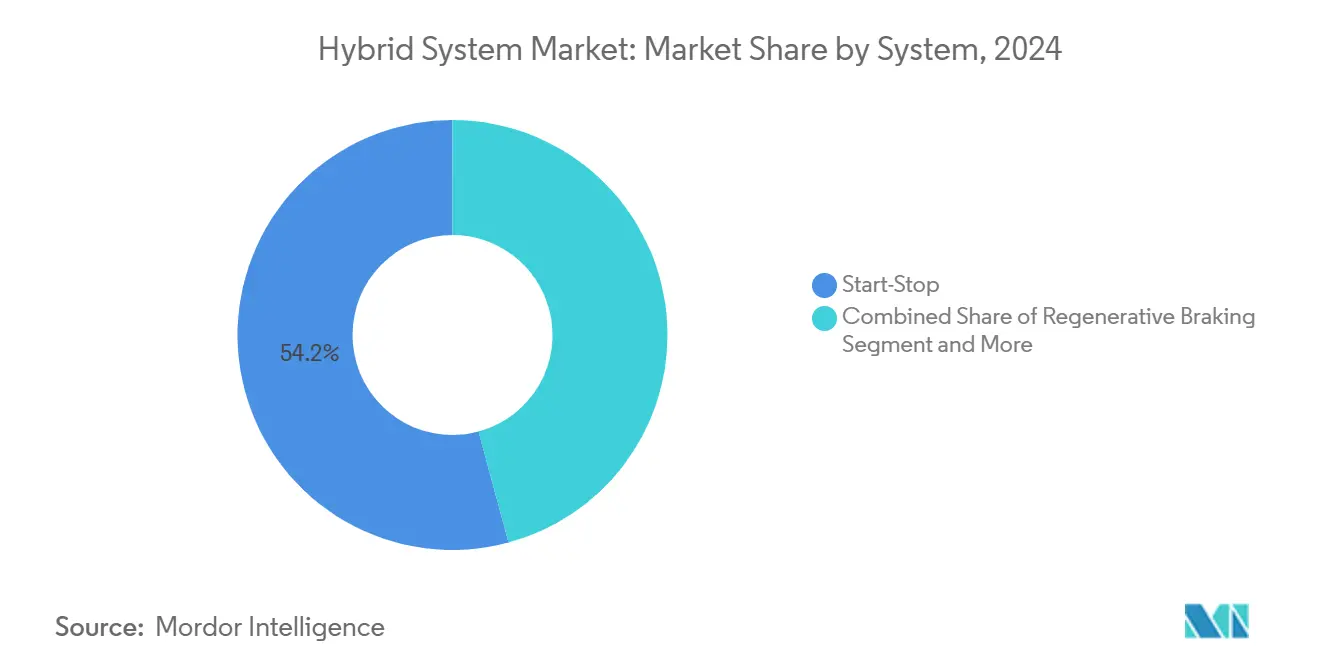

- By system, start-stop technology led with 54.15% of the hybrid system market share in 2024, while electric-vehicle drive systems are projected to register the fastest 13.75% CAGR through 2030.

- By component, battery packs accounted for 39.04% of the hybrid system market share in 2024, while eMotor/ISG units are forecast to expand at a 14.12% CAGR through 2030.

- By battery chemistry, lithium-ion accounted for 72.33% of the hybrid system market share in 2024, and is forecast to expand at a 12.37% CAGR through 2030.

- By vehicle type, mild hybrid vehicles accounted for 43.11% of the hybrid system market share in 2024, while plug-in hybrid electric vehicles are forecast to expand at a 15.06% CAGR through 2030.

- By geography, Asia-Pacific commanded 47.24% of the hybrid system market share in 2024 and is projected to witness the fastest growth, with a 12.86% CAGR through 2030.

Global Hybrid System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Global Emissions Rules | +2.8% | Global, early gains in Australia, the EU, and California | Medium term (2-4 years) |

| Incentives for Hybrid and EVs | +2.1% | North America, core APAC, spill-over to MEA | Short term (≤ 2 years) |

| Cheaper Lithium-Ion Battery Packs | +1.9% | Global, led by the Chinese manufacturing scale | Medium term (2-4 years) |

| Proliferation of 48-V Hybrids | +1.6% | Europe, North America, and expanding into APAC | Long term (≥ 4 years) |

| Use of SiC Power Electronics | +1.4% | Global, premium segments first | Long term (≥ 4 years) |

| Vehicle-to-Grid and V2X Models | +1.2% | North America and EU pilot programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global CO₂ / Fuel-Economy Regulations

Regulators are tightening tailpipe norms in every major auto hub, creating direct pull for the hybrid system market. Australia introduced its first CO₂ limits for new light vehicles in May 2024, targeting 141 g CO₂/km by 2029, down from 180 g CO₂/km [1]“New Vehicle Efficiency Standard 2024,” Australian Department of Climate Change, climatechange.gov.au. The European Union approved Euro 7 measures effective 2025 that cut particulate matter in urban drive cycles, advantaging powertrains able to decouple engine load. California’s Advanced Clean Cars II framework requires 35% zero-emission sales by 2026, making plug-in hybrids vital compliance bridges for OEMs that lag in BEV capacity. Collectively, these rules reposition hybrids from optional efficiency add-ons to essential certification tools across mass and premium segments.

Government Incentives for Hybrid and Electrified Drivetrains

Monetary carrots sharpen consumer appetite for electrified vehicles and widen the hybrid system market. The U.S. Inflation Reduction Act extends a credit to hybrids with batteries above certain limits, swinging purchase math in favor of electrified trims. Thailand’s EV3.5 framework grants, as per hybrid, nearly halve the incremental outlay in sub-compact classes. China’s dual-credit system awards positive scores for fuel use below 4 L/100 km, letting manufacturers monetize credits to offset penalties on legacy fleets. These incentives establish immediate retail pull and bolster planning certainty for suppliers deciding where to locate new factories.

Rapid Cost Decline in Lithium-Ion Battery Packs

Pack prices fell in 2024 and are forecast to slip further by 2030, improving the value equation for every architecture within the hybrid system market. Chinese groups CATL and BYD now operate more than 200 GWh each of yearly capacity, harvesting scale gains that cascade into vehicle BOM savings. A larger battery can represent 35-40% of plug-in hybrid cost, so each decline widens gross margin or permits price cuts that expand addressable demand. Tesla’s cylindrical 4680 format highlights further savings potential when cells serve as structural elements, though mass deployment remains limited to premium platforms.

Proliferation of 48-V Mild-Hybrid Architectures

A 48-V system can trim CO₂ by up to 15% yet costs only one-quarter of a full hybrid, opening electrification to mainstream segments and enlarging the hybrid system market [2]“48-Volt Hybrid Systems White Paper,” Continental AG, continental.com. Mercedes-Benz rolled 48-V packages across its C- and E-Class families, confirming consumer readiness to pay for smoother stop-start and gliding functions. Valeo’s integrated starter-generator delivers 25 kW peak and electric creep in traffic while retaining the 12-V backbone, minimizing redesign expense. Adoption is extending into emerging-market compacts where price ceilings once blocked even basic hybridization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost Premium | -1.8% | Global, strongest in price-sensitive emerging regions | Short term (≤ 2 years) |

| Critical Material Supply Constraints | -1.5% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Policy Shifts to Zero Mandates | -1.2% | California, Norway, United Kingdom, Netherlands | Long term (≥ 4 years) |

| Thermal Management Limits for EBoost | -0.9% | Europe, North America compact segment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Premium of Hybrid Systems

Hybrids still carry premiums over combustion comparables, with plug-in variants nearing USD 12,000 in sub-compact classes, slowing penetration in the hybrid system market. Emerging economies where average transaction prices linger see hybrids relegated to upscale trims. Toyota targets significant cost reduction by 2026 via commonized modules and higher global volumes, but savings require more than 500,000 units per platform year. Price pressure intensifies as lithium spot trades oscillated per ton during 2024, keeping BOM forecasts volatile.

Critical-Material Supply-Chain Constraints (Li, Ni, Rare Earths)

Increased lithium demand signals potential bottlenecks that could choke the hybrid system market [3]“Mineral Commodity Summary: Lithium 2025,” U.S. Geological Survey, usgs.gov. Indonesia’s nickel ore export ban adds risk to high-nickel chemistries prized for range. China runs a major share of rare-earth refining, exposing the neodymium magnet supply for traction motors to geopolitical shocks. Domestic-content rules in the United States elevate logistics complexity, requiring new refining capacity that may come online only after mid-decade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System: Start-Stop Dominance Faces Electric-Drive Disruption

Start-stop units retained 54.15% of the hybrid system market share in 2024 on the strength of modest pricing and compatibility with virtually every combustion layout. Many emerging-market regulators grant partial CO₂ credits simply for equipping vehicles with automatic idle cutoff, so OEMs deploy the feature as an easy compliance lever. Yet electric-drive hybrid systems are forecast to grow at 13.75% CAGR through 2030, redirecting capital toward higher voltage platforms that promise full-electric operation at suburban speeds. The hybrid system market size for electric-drive solutions will grow further if battery pack cost targets hold. Urban duty cycles amplify the advantages of regenerative braking and zero-tailpipe emissions in traffic, persuading city governments to issue access perks that raise resale values for owners.

Start-stop technology will not vanish but will gradually compress into the entry tier. Many Tier-1 suppliers already bundle low-cost 48-V alternator replacements that layer torque assist on top of idle cut, migrating value from legacy hardware toward electronics. Continental logged a significant penetration rate for 48-V eBoost hardware in newly launched European compacts during 2024. Suppliers are also adding integrated DC-DC converters that pave a future upgrade path to plug-in capability, preserving residual value and reinforcing the hybrid system market.

By Component: Battery Packs Lead Value While eMotors Drive Growth

Battery packs captured 39.04% of the hybrid system market value in 2024, thanks to their sizable cost per kilowatt-hour and non-substitutable role in every architecture. Cost declines have trimmed average pack pricing year on year, opening segments that had struggled to justify electrification. eMotor and integrated starter-generator assemblies are the fastest-growing component line at 14.12% CAGR as 48-V systems migrate across brand portfolios.

SiC inverter adoption lifts output while shrinking weight, aligning with city car packaging limits. DC-DC converters account for a significant component share, and bidirectional designs are becoming standard as V2G trials expand. Valeo’s motor generator achieves 4 kW/kg density, ensuring enough room in compact hatches for collision structures. CATL’s low-profile LFP packs further free cabin space, although energy density is lower than NCM chemistries. Altogether, the component mix evidences the shift from basic idle-stop accessories toward multi-functional electrification modules that elevate the hybrid system market.

By Battery Chemistry: Lithium-Ion Consolidation Accelerates Evolution

Lithium-ion cells held 72.33% of the hybrid system market share in 2024 and will expand fastest at 12.37% CAGR thanks to gains in volumetric energy and falling cost trajectories. Nickel-metal hydride holdings persist mainly inside Toyota applications but are fading as the brand migrates to lithium packs for new launches. Enhanced flooded and AGM lead-acid batteries retain utility for 12-V stop-start, but their growth is capped by rising fuel-economy targets that necessitate deeper electrification.

Lithium iron phosphate surges in light commercial fleets where thermal stability and long cycle life trump gravimetric density. CATL’s LFP modules reach 4,000 cycles before 20% capacity fade, meeting duty demands for ride-hailing and parcel fleets. Manufacturers are slicing cobalt content through high-manganese or LFP solutions, a trend that reduces exposure to price swings and human-rights scrutiny. Chemistry shifts mirror a maturing hybrid system market, adjusting tech stacks for cost, safety, and application-specific needs.

By Vehicle Type: MHEV Leadership Challenged by PHEV Momentum

Mild hybrid electric vehicles possessed 43.11% of the hybrid system market share in 2024, leveraging entry-level price points and limited charging demands. Plug-in hybrids are ascending at 15.06% CAGR due to improved electric-only range and financial incentives that narrow total-cost gaps. The hybrid system market size attributable to plug-in variants will grow by 2030 if infrastructure rollouts match forecasts. Traditional HEVs continue contributing to significant growth, upheld by brand reputations for durability and ease of use.

Consumer segmentation is precise. Price-sensitive buyers prize mild hybrids for incremental fuel savings, while environmentally driven or regulation-pressured users adopt plug-ins to access subsidies and low-emission zones. Ford’s Escape PHEV delivers significant electric range, covering average daily commutes while retaining ICE backup for long trips. The rise of dual-motor architectures capable of rear-axle torque fill positions plug-ins as legitimate performance upgrades, further broadening their appeal inside the hybrid system market.

Geography Analysis

Asia-Pacific anchored 47.24% of the hybrid system market revenue in 2024 and will expand at the swiftest 12.86% CAGR through 2030 as China and Japan cement hybrid pathways into national emission programs. As of December 2023, China’s dual-credit scheme demanded 28% new-energy penetration in 2024, rising to 38% in 2025, channeling OEM capital into hybrids where BEV charging access is uneven. Japan exported a significant volume of hybrid units in 2024, directed toward Southeast Asia, where duties favor electrified powertrains and where consumer trust in Japanese brands remains strong.

Europe accounted for a notable share, spurred by Euro 7 and dense public charging that raises plug-in hybrid practicality. Germany committed significant investments to hybrid R&D, and Volkswagen earmarked a notable share of its electrification budget for hybrid drivelines to handle regions with lagging fast-charge networks. Across the Atlantic, North America contributed a potential hybrid system market share, helped by retooled federal credits and state ZEV quotas that position hybrids as compliance bridges until BEV price parity lands.

South America and the Middle East & Africa captured a combined significant share but hold long-run upside. Brazil’s Rota 2030 law offers rebates to models beating baseline fuel use, a threshold readily met by mild hybrids. Gulf Cooperation Council states are drafting fuel-economy targets that echo European norms, prompting Japanese and Korean OEMs to line up 48-V model launches. Infrastructure gaps and price sensitivities favor MHEV solutions now, but policy headwinds suggest plug-ins will gain traction later in the decade, feeding incremental growth into the hybrid system market.

Competitive Landscape

The hybrid system market shows moderate concentration. Toyota counts more than 15 million hybrid vehicles on road, capitalizing on two decades of battery and power split technology to preserve reliability leadership and marginal cost advantages. Alliances serve as scale multipliers: Ford teams with SK Innovation on battery sourcing, and General Motors partners with LG Energy Solution, slashing cell cost curves and sharing R&D on next-generation chemistries. Traditional Tier-1s such as Bosch and Denso supply electronics and motors to multiple brands, anchoring themselves as indispensable yet faceless enablers.

Emerging disruptors fill specialized niches. Sila Nanotechnologies develops silicon-rich anodes that promise 20% energy density uplift, while Wolfspeed extends the SiC inverter frontier into sub-premium price tiers. BYD integrates batteries, power electronics, and assembly under one roof, granting enough cost slack to price hybrids aggressively in Latin America and Southeast Asia. CATL is carving similar vertical paths and is exploring joint ventures to hedge geopolitical limits on direct exports.

Consolidation is quietly advancing. BorgWarner closed 2024 with acquisitions that fold advanced eMotor IP into its catalog and expects ePowertrain revenue to grow significantly in the coming years. Panasonic aligns with Toyota to mass-produce prismatic cells that fit the marque’s fifth-generation hybrid lineup. The competitive narrative suggests that differentiation is migrating away from basic hybrid functionality, which is nearing commoditization, toward software-enabled features, bidirectional power flow, and proprietary cell chemistries that extend life or unlock new revenue modes in the hybrid system market.

Hybrid System Industry Leaders

Toyota Motor Corporation

Robert Bosch GmbH

Continental AG

Denso Corporation

BYD Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Hyundai Motor Group rolled out a next-generation hybrid powertrain that lifts output by 19% and improves fuel economy by 45% over comparable combustion engines.

- September 2024: Toyota introduced a 48-V mild-hybrid system on the Hilux pickup, combining a 48-V lithium-ion pack, motor-generator, and DC-DC converter to deliver smoother acceleration and improved regenerative braking.

Global Hybrid System Market Report Scope

| Start-Stop |

| Regenerative Braking |

| Electric-Vehicle Drive |

| eBoost / 48-V Power Assist |

| Battery Pack |

| DC/DC Converter |

| DC/AC Inverter |

| eMotor / ISG |

| Lithium-ion |

| Lead-Acid (EFB / AGM) |

| Nickel-Metal Hydride (NiMH) |

| Mild Hybrid Vehicle (MHEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Battery Electric Vehicle (with Hybrid Sub-Systems) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of the Middle East and Africa |

| By System | Start-Stop | |

| Regenerative Braking | ||

| Electric-Vehicle Drive | ||

| eBoost / 48-V Power Assist | ||

| By Component | Battery Pack | |

| DC/DC Converter | ||

| DC/AC Inverter | ||

| eMotor / ISG | ||

| By Battery Chemistry | Lithium-ion | |

| Lead-Acid (EFB / AGM) | ||

| Nickel-Metal Hydride (NiMH) | ||

| By Vehicle Type | Mild Hybrid Vehicle (MHEV) | |

| Hybrid Electric Vehicle (HEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Battery Electric Vehicle (with Hybrid Sub-Systems) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

How large is the hybrid system market in 2025?

The hybrid system market size reached USD 35.90 billion in 2025 and is projected to grow at an 11.91% CAGR to 2030.

Which region currently leads in hybrid system adoption?

Asia-Pacific holds 47.24% hybrid system market share thanks to policy incentives in China and export-oriented strategies in Japan.

What component contributes the greatest value to hybrid systems?

Battery packs account for 39.04% of 2024 revenue because they are the costliest and most indispensable element.

Why are 48-V mild hybrids gaining momentum?

They deliver up to 15% CO₂ reduction at only one-quarter of the cost of full hybrids, making them affordable for entry-level segments.

Page last updated on: