Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

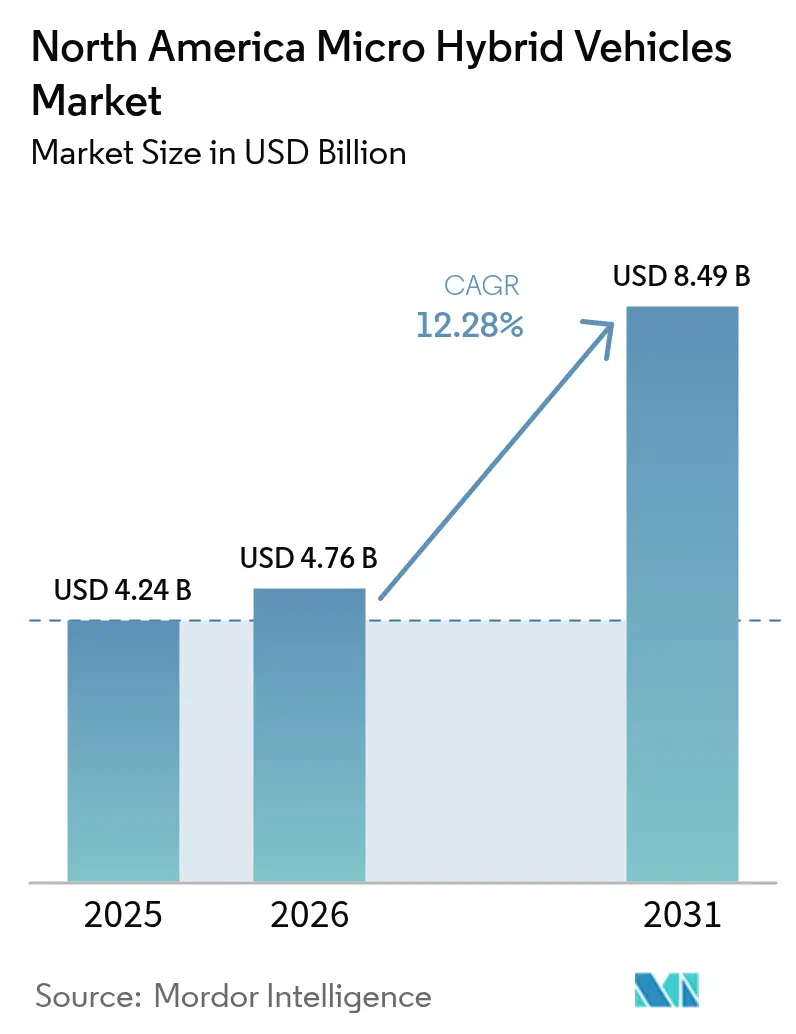

| Base Year Market Size (2025) | USD 4.24 Billion |

| Market Size (2026) | USD 4.76 Billion |

| Market Size (2031) | USD 8.49 Billion |

| Growth Rate (2026 - 2031) | 12.28% CAGR |

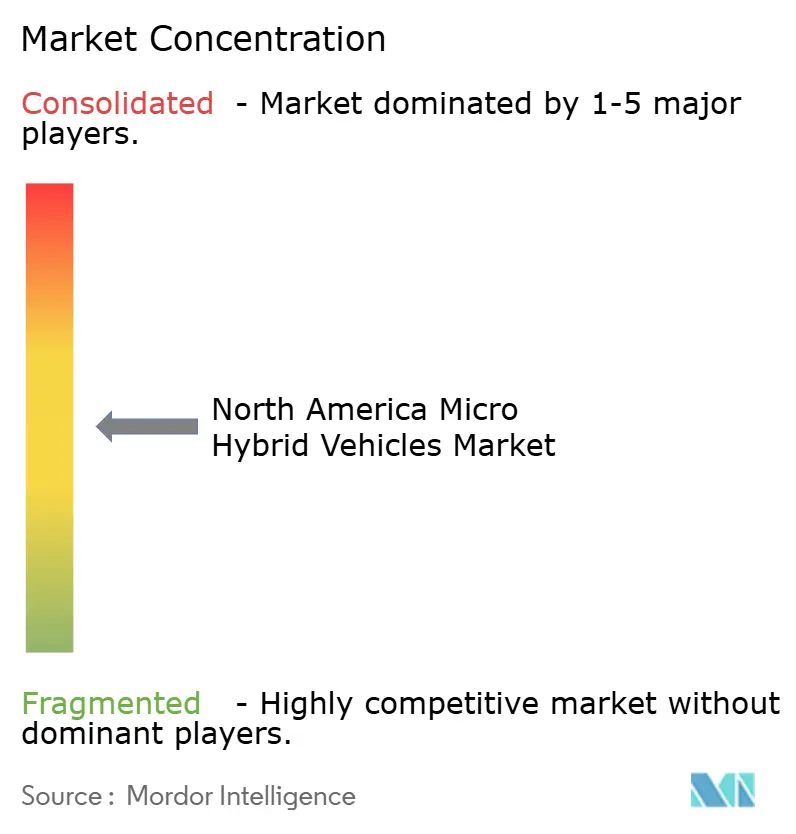

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Micro Hybrid Vehicles Market Analysis by Mordor Intelligence

The North America micro-hybrid vehicles market size was valued at USD 4.24 billion in 2025 and estimated to grow from USD 4.76 billion in 2026 to reach USD 8.49 billion by 2031, at a CAGR of 12.28% during the forecast period (2026-2031). Rising regulatory pressure, aggressive fleet electrification targets, and the automotive industry’s strategic preference for cost-effective 48V architectures underpin this outlook. Technology delivers 10-15% fuel-efficiency gains at nearly one-third the cost of full hybrids, so it offers a pragmatic bridge between conventional powertrains and high-voltage electrification. A decisive move toward 48 V platforms also satisfies growing ADAS power loads without subjecting vehicles to safety regimes exceeding 60 V, further strengthening momentum.

Key Report Takeaways

- By capacity type, 48 V systems held 63.45% of the North America micro-hybrid vehicles market share in 2025 and are set to expand at a 13.4% CAGR through 2031.

- By battery type, lead-acid technologies captured 72.55% revenue share in 2025, while lithium-ion is expected to grow at 15.75% CAGR to 2031.

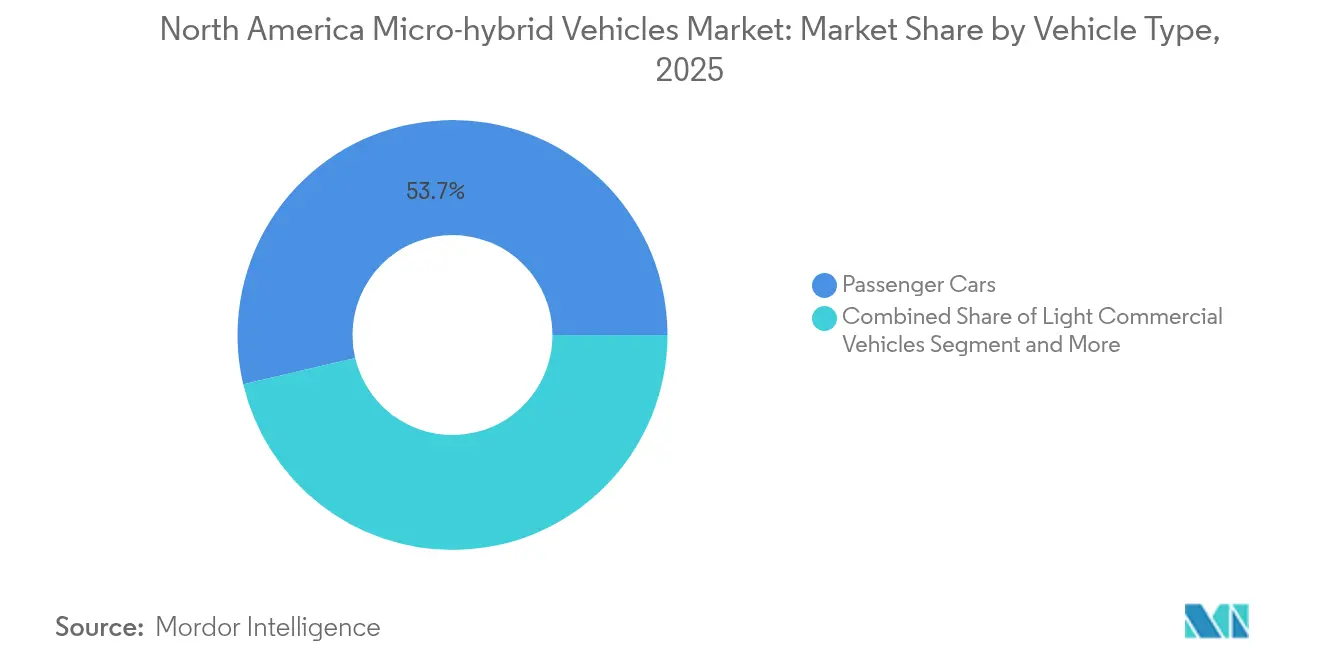

- By vehicle type, passenger cars accounted for 53.68% of the North America micro-hybrid vehicles market size in 2025 and will advance at a 13.09% CAGR.

- By end-user, OEM-fitted systems commanded a 93.02% share in 2025, whereas aftermarket and fleet retrofits will post the fastest 15.26% CAGR.

- By country, the United States retains market leadership with 79.85% share in 2025, while Canada records the highest projected CAGR at 13.72% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Micro Hybrid Vehicles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter CAFE and GHG Standards | +2.2% | United States, Canada | Medium term (2-4 years) |

| Rapid OEM Rollout of 48 V Mild-hybrid Architectures | +2.1% | North America | Short term (≤2 years) |

| 48 V Power Net Meets ADAS Loads without HV Packs | +1.7% | North America | Short term (≤2 years) |

| Consumer Shift to Fuel-efficient Pickups and SUVs | +1.5% | United States, Canada | Medium term (2-4 years) |

| Cost-down Curve of Advanced AGM/EFB Lead-acid Batteries | +1.2% | Global, North America focus | Long term (≥4 years) |

| US-Mexico Battery-Supply Incentives | +1.1% | United States, Mexico | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stricter CAFE and GHG standards drive micro-hybrid adoption

The Environmental Protection Agency’s Multi-Pollutant Emissions Standards require fleet CO₂ emissions to fall to 85 g/mi by 2032, nearly halving 2026 levels, while NHTSA’s CAFE rules demand roughly 50.4 mpg by 2031 [1]“Multi-Pollutant Emissions Standards for 2027–2032,” Environmental Protection Agency, epa.gov. Automakers view 48V mild-hybrids as an immediate route to compliance because they deliver double-digit efficiency gains, integrate with existing ICE platforms, and maintain profitability. Ford plans hybrid variants across all remaining ICE nameplates by 2030, and GM has announced plug-in hybrids starting in 2027 after earlier EV-only ambitions. Program timing aligns well with the 2027–2032 phase-in schedule, letting OEMs spread investment over normal model updates.

Rapid OEM rollout of 48 V mild-hybrid architectures

The speed at which automakers are adopting 48 V systems reflects a confluence of technology readiness and regulatory necessity. Tesla’s decision to eliminate 12 V components in favor of 48 V wiring exemplifies the shift toward lighter harnesses and lower resistive losses. Continental notes that a 48 V belt-starter generator can trim tailpipe CO₂ by up to 15% and power electric turbochargers and regenerative braking. Tier-1 suppliers such as BorgWarner and Valeo have secured multi-year contracts for 48 V e-motors and power electronics on platforms launching through 2028, indicating that OEMs favor a modular strategy that scales from basic stop-start to ADAS support.

48 V power net enables ADAS power loads without HV packs

Growing ADAS content demands peak electrical loads of 2-5 kW, and a 48 V bus provides quadruple the power of 12 V while staying below the 60 V high-voltage threshold. NHTSA will require automatic emergency braking on all light vehicles by September 2029, making a scalable low-voltage upgrade essential for future compliance. Development of the Low-Voltage Connector Standard (LVCS) by USCAR is accelerating part commonality, which in turn lowers costs and simplifies service [2]“Low-Voltage Connector Standard,” USCAR, uscar.org.

Consumer shift to fuel-efficient pickups and SUVs

Hybrid sales grew five times faster than EV deliveries during 2024, reflecting mainstream shoppers’ preference for familiar refueling routines and lower running costs. Sixty-seven percent of respondents say cheaper ownership motivates hybrid interest, and 59% highlight environmental benefits. Vehicles such as the Ford Maverick Hybrid reach 38 mpg while preserving utility, underscoring why mild-hybrid powertrains resonate in larger formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Incremental Cost vs. Legacy 12 V Stop-Start | -1.8% | North America | Short term (≤2 years) |

| Tightening Lithium-ion Supply may Crowd R&D Budgets | -1.3% | Global, North America exposure | Medium term (2-4 years) |

| Limited Consumer Awareness of “Micro-hybrid” Value | -0.9% | United States, Canada rural | Long term (≥4 years) |

| Absence of Nationwide 48 V Repair Ecosystem | -0.7% | United States | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High incremental cost vs. legacy 12 V stop-start

A 48 V mild-hybrid adds roughly USD 800-1,500 per vehicle over a standard 12 V stop-start system, equal to 2–4% of an average U.S. transaction price. Forty percent of surveyed buyers cite upfront cost as the biggest barrier, even though lifetime fuel savings can exceed USD 600. Economies of scale and broader parts commonality are expected to trim system costs 20-30% by 2027, but short-term price sensitivity still curbs uptake.

Tightening lithium-ion supply may crowd R&D budgets

Lithium prices from their 2022 peak to three-year lows in Q1 2025, while nickel hovered around USD 15,000–16,000 per ton as a supply glut persisted through 2024-2025, leading several suppliers to trim engineering budgets. U.S. refining capacity handles less than 5% of battery-grade lithium, a strategic risk to North American electrification ambitions. With China controlling a dominant share of cathode and anode manufacturing, automakers must juggle near-term raw-material volatility with long-term diversification plans. These financial pressures can delay micro-hybrid software optimization and component miniaturization efforts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity Type: 48 V dominance accelerates electrification

The 48 V class represented 63.45% of the North America micro-hybrid vehicles market share in 2025 and is projected to record a 13.4% CAGR through 2031. Because a 48 V belt-starter generator delivers 10-20 kW without triggering high-voltage safety rules, OEMs view it as the sweet spot for quick efficiency gains. Tesla’s blueprint to retire 12 V wiring reinforces a likely standardization path, while the Low-Voltage Connector Standard removes cross-platform headaches. The 12 V segment still appeals to value-oriented models, especially in aftermarket retrofits. Meanwhile, 24 V solutions serve specialized commercial assets that need slightly higher power but cannot justify a 48 V architecture.

The 48 V pathway also future-proofs vehicles for additional ADAS content because it can power electric superchargers, active suspension, and steering boosts without major redesign. Parts commonality across ICE, MHEV, and future PHEV platforms lets suppliers amortize tooling costs and reach volume quicker. As more OEMs unify electrical backbones, price parity with 12 V stop-start is likely within the forecast horizon, strengthening the segment’s leadership in the North America micro-hybrid vehicles market.

By Battery Type: Lead-acid resilience amid lithium-ion pressure

Lead-acid technologies held a 72.55% share in 2025, underpinned by mature recycling systems and a low cost per kilowatt-hour. AGM and EFB variants offer enhanced charge acceptance and life-cycle stability suited to high-frequency start-stop cycles. Lithium-ion’s 15.75% CAGR signals a swift shift for more power-intensive 48 V functions as cell prices continue to moderate, but supply security concerns and raw-material volatility temper short-term penetration.

Hybrid capacitor projects that blend supercapacitors with lead-acid are under evaluation, promising rapid charge delivery that supports regenerative braking. Clarios and other suppliers are piloting these chemistries to keep lead-acid relevant even as lithium-ion matures. The net result is a diversified battery landscape that balances cost, energy density, and sourcing risk across the North America micro-hybrid vehicles market size.

By Vehicle Type: Passenger cars lead commercial adoption

Passenger cars accounted for 53.68% of the North America micro-hybrid vehicles market size in 2025, with a 13.09% CAGR outlook. Stringent fleet-average efficiency rules make mild-hybrids a cost-effective tool for sedans, crossovers, and compact SUVs. In light trucks and full-size pickups, early successes such as the Ford Maverick Hybrid confirm customer acceptance when towing capacity and cabin space stay intact.

Light commercial vehicles are next in line because last-mile delivery firms can cut idling fuel costs rapidly with stop-start. NHTSA’s heavy-duty pickup rules from 2030 place additional pressure on medium-duty fleets, opening a viable retrofit channel. BorgWarner’s recent transfer-case awards for hybrid pickup programs highlight how suppliers are positioning for this curve.

By End-User: OEM integration dominates aftermarket emergence

OEM-fitted systems captured 93.02% of 2025 revenues, largely because 48 V integration touches engine calibration, infotainment power budgets, and chassis electronics that are impractical for field installation. Regulatory compliance credits also accrue only to factory-built hybrids, strengthening OEM control of the value chain.

Aftermarket activity is scaling from a low base yet posts a 15.26% CAGR as fleets retrofit buses, vans, and specialty trucks to meet municipal emissions rules. Independent retrofit kits that combine belt-starter generators, DC-DC converters, and AGM batteries can slash idle fuel use by double-digit percentages, building a bridge for older assets until replacement cycles kick in. Service-tool standardization and technician certification remain the hinge for broader adoption.

Geography Analysis

The United States held 79.85% share of the North America micro-hybrid vehicles market in 2025. Regulatory certainty through 2032 gives OEMs a clear payback framework and a robust supply base, from power electronics in Michigan to battery assemblies in Tennessee, shortens development loops. Consumer data points to hybrids growing five times quicker than BEVs, proof that mainstream buyers see fuel savings without range anxiety. Still, nationwide 48 V service coverage is incomplete, especially outside major metro areas, which could slow penetration in rural states.

Canada is smaller but faster, expanding at a 13.72% CAGR toward 2031, due to a 100% ZEV sales target by 2035 and layered rebates worth up to CAD 13,000 in Quebec. ZEV penetration reached 13.8% in 2024 versus under 10% south of the border, making Canada an early-adoption lab for cold-weather optimization and consumer outreach . GM eclipsed Tesla in Q1 2025 EV registrations, demonstrating that domestic OEMs profit under incentive-rich policy frameworks.

Mexico rounds out the region. Generous tax offsets under “Plan Mexico,” Mexico’s cost-competitive labor, and USMCA rules of origin are pulling lithium-ion cell and 48 V module production closer to U.S. assembly plants. BMW’s San Luis Potosí project will ship battery packs northward starting in 2027. Trade tensions tied to Chinese investment could complicate long-term strategy but, in the near term, nearshoring boosts logistics agility and positions Mexico as a key pillar of the North America micro-hybrid vehicles market.

Competitive Landscape

Moderate concentration characterizes the North America micro-hybrid vehicles market, with top Tier-1 suppliers controlling core technologies yet leaving niche gaps for challengers. BorgWarner, Continental, and Bosch command integrated portfolios of belt-starter generators, inverters, and battery management systems, leveraging decades-long OEM relationships. BorgWarner secured contracts for high-voltage coolant heaters on 2027 PHEVs and for 48 V e-motors on next-generation pickup trucks, underscoring incumbents’ ability to cross-sell across powertrain roadmaps.

Disruptors exploit white spaces. Tesla’s 48 V wiring initiative forces the supply base to redesign relays, fuses, and connectors, which gives agile specialists a chance to leapfrog legacy catalogues. The Renault–Geely Horse Powertrain JV targets turnkey hybrid systems suitable for retrofit, while Visteon partners with Shinry to co-develop compact 48V power electronics. As USCAR finalizes LVCS, interoperability could commoditize connectors, shifting value toward software and system integration.

Aftermarket dynamics are fluid. Fleet retrofits lack large-scale kit suppliers, but Gates and other component makers are piloting modular solutions that bolt onto diesel delivery vans. With lithium-ion prices volatile and lead-acid sustainability strong, battery suppliers differentiate through circular-economy credentials. Redwood Materials’ tie-up with BMW to recycle up to 98% of valuable minerals illustrates the pivot toward closed-loop models in anticipation of tighter ESG reporting rules.

North America Micro Hybrid Vehicles Industry Leaders

Toyota Motor Corporation

Ford Motor Company

Hyundai Motor Group

General Motors Company

Stellantis N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Mitsubishi confirmed a mild-hybrid Outlander for the U.S. in early 2026, promising around 10% better fuel efficiency than its ICE counterpart.

- September 2024: BMW partnered with Redwood Materials to recycle lithium-ion batteries from its hybrid and electric models across the U.S., targeting 95-98% mineral recovery.

- July 2024: BMW launched the X6 xDrive40i in Argentina, featuring a 3.0 L six-cylinder engine complemented by a 48 V mild-hybrid system, pushing total output to 375 hp.

North America Micro Hybrid Vehicles Market Report Scope

The North American micro-hybrid vehicles market covers the latest trends and technological development and provides analysis on the market demand by capacity type, vehicle type, battery, country, and market share of major micro-hybrid vehicle manufacturing companies in North America.

By Capacity Type

| 12 V Micro-hybrid |

| 24 V Micro-hybrid |

| 48 V Micro-hybrid |

By Battery Type

| Lead-acid (AGM/EFB) |

| Lithium-ion (LFP, LTO, NMC) |

| Others |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

By End-User

| OEM-fitted Vehicles |

| Aftermarket/Fleet Retrofit |

By Country

| United States |

| Canada |

| Rest of North America |

| By Capacity Type | 12 V Micro-hybrid |

| 24 V Micro-hybrid | |

| 48 V Micro-hybrid | |

| By Battery Type | Lead-acid (AGM/EFB) |

| Lithium-ion (LFP, LTO, NMC) | |

| Others | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | |

| By End-User | OEM-fitted Vehicles |

| Aftermarket/Fleet Retrofit | |

| By Country | United States |

| Canada | |

| Rest of North America |

Key Questions Answered in the Report

What is the current value of the North America micro-hybrid vehicles market?

The market stood at USD 4.76 billion in 2026 and is projected to grow to USD 8.49 billion by 2031.

How fast is the North America micro-hybrid vehicles market expected to grow?

It is forecast to post a 12.28% CAGR during 2026-2031.

Which capacity type leads the market?

48 V systems lead with a 63.45% share in 2025 and exhibit the quickest 13.4% CAGR.

Which country is the fastest growing within North America?

Canada records a 13.72% CAGR through 2031, driven by strong ZEV mandates and purchase incentives.

Page last updated on: