Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2019 - 2024 |

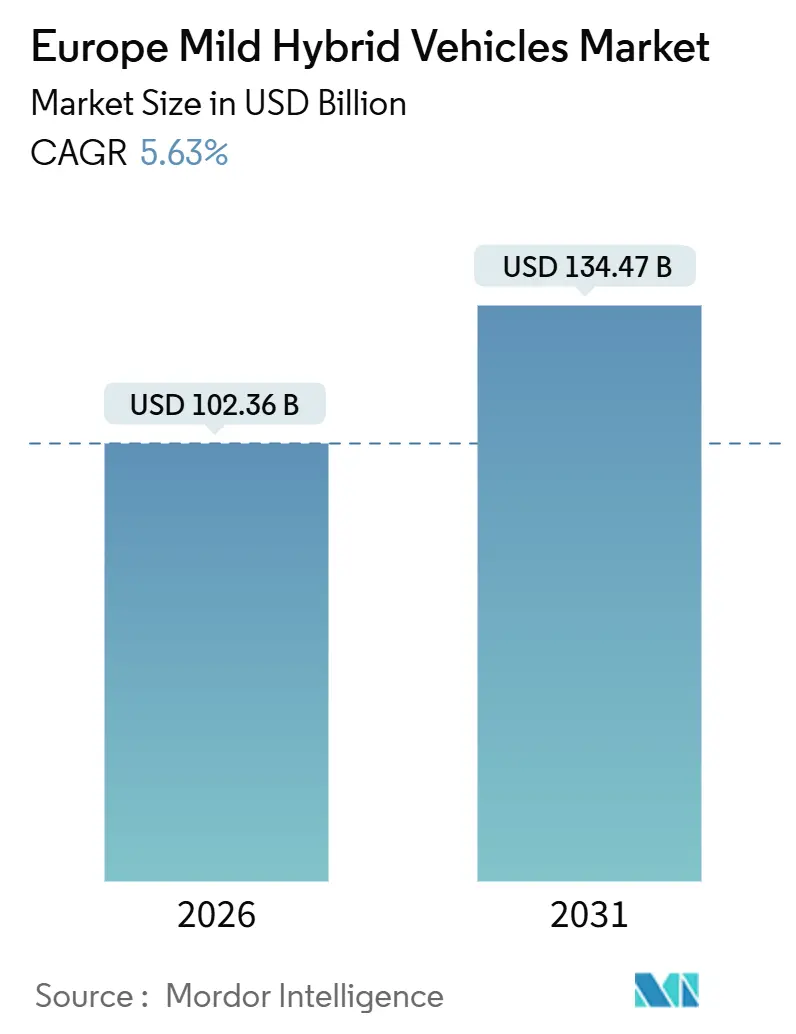

| Market Size (2026) | USD 102.36 Billion |

| Market Size (2031) | USD 134.47 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Mild Hybrid Vehicles Market Analysis by Mordor Intelligence

The European mild hybrid vehicles market size stood at USD 102.36 billion in 2026 and is projected to reach USD 134.47 billion by 2031, expanding at a 5.63% CAGR. Fleet CO₂ ceilings, coupled with a EUR 95 (approximately USD 110) penalty for every excess gram, make 48-volt architectures an attractive hedge against the capital outlay required for full-battery-electric platforms. Corporate buyers favor mild hybrids because they lower the total cost of ownership without range-anxiety trade-offs. Unlike full battery-electric architectures, 48-volt mild-hybrid systems deliver compliance headroom without the capital intensity of dedicated BEV platforms.

Key Report Takeaways

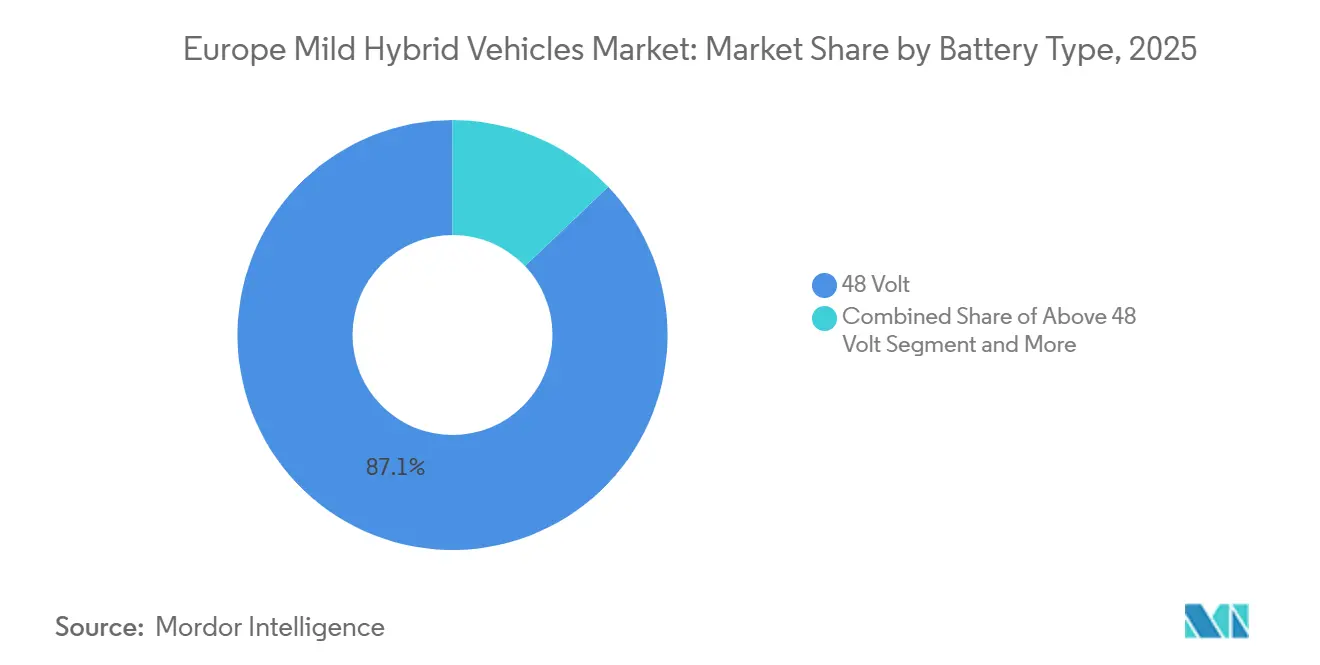

- By battery type, 48-volt systems led with 87.13% of Europe's mild hybrid vehicles market share in 2025, while above-48-volt captured the fastest 21.37% CAGR through 2031.

- By vehicle type, passenger cars held 81.26% share of the European mild hybrid vehicles market size in 2025, and commercial vehicles are expanding at a 14.18% CAGR to 2031.

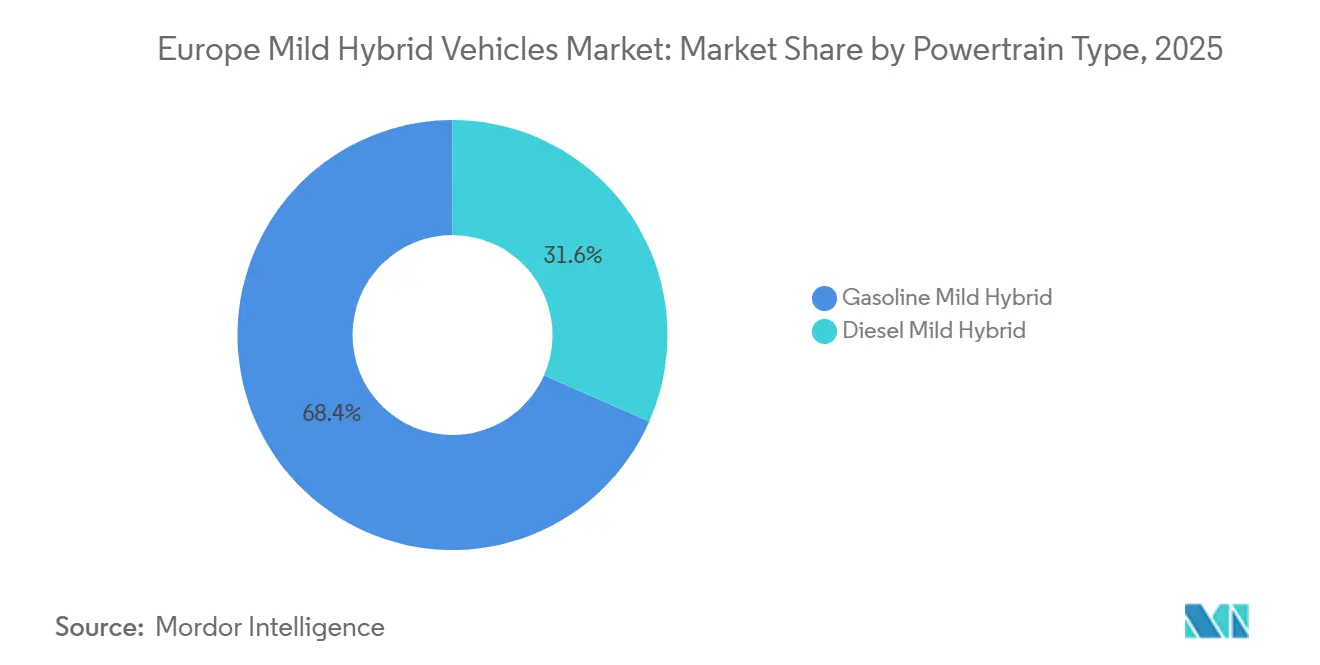

- By powertrain, gasoline mild hybrids accounted for 68.42% of Europe's mild hybrid vehicle market size in 2025, whereas diesel mild hybrids are advancing at a 17.63% CAGR through 2031.

- By propulsion technology, belt-driven starter generators captured 56.08% share of the European mild hybrid vehicles market in 2025; integrated starter generators record the highest 18.92% projected CAGR to 2031.

- By country, Germany commanded a 29.31% market share in 2025, and the rest of Europe is expected to grow at a 6.84% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Mild Hybrid Vehicles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU CO₂-Target Tightening | +1.2% | Europe-Wide, Strongest in Germany, France, Italy | Short Term (≤ 2 Years) |

| Diesel Decline Accelerating 48V Adoption | +0.9% | Western Europe Core, Spillover to Eastern Europe | Medium Term (2–4 Years) |

| Falling 48V System Costs | +0.8% | Global, with Manufacturing Concentration in Germany | Medium Term (2–4 Years) |

| Consumer Shift from BEV to Hybrids | +0.7% | Northern and Western Europe, Urban Markets | Short Term (≤ 2 Years) |

| 48V Needed to Power ADAS L2 | +0.6% | Premium Segments in Germany, United Kingdom, Nordics | Long Term (≥ 4 Years) |

| BEV Plant-Conversion Gaps Back-Filled by MHEV Production | +0.4% | Manufacturing Hubs in Germany, Czech Republic, Slovakia | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

EU CO₂-Target Tightening 2025–2030

The European Union's fleet-average CO₂ ceiling of 93.6 g/km for passenger cars, effective January 2025, imposes a EUR 95 (approximately USD 110) penalty per excess gram multiplied by total annual registrations, creating a huge compliance cost for volume manufacturers missing the target by 5 g/km[1]"2025 Automotive Package – Proposed revision of the Regulation on CO₂ standards for cars and vans," European Commission, climate.ec.europa.eu.. The regulation's zero- and low-emission vehicle crediting mechanism, which awards super-credits for battery electric vehicles (BEVs) and plug-in hybrids, paradoxically incentivizes mild-hybrid deployment as a hedge; manufacturers can meet the 2025 target by blending 15% BEVs with 40% mild hybrids rather than committing to 25% battery electric vehicles (BEVs) alone, preserving capital for the steeper 49.5 g/km threshold arriving in 2030.

Diesel Decline Accelerating 48V Adoption

In Q1 2025, diesel vehicles captured a 9.5% market share, following a 27.1% decline in the diesel car market[2]Andy Cormack, "New car registrations: -1.9% in Q1 2025; battery-electric 15.2% market share," EPMA, epma.com., as urban low-emission zones in Paris, Madrid, and Milan tighten access for Euro 6d-TEMP vehicles. This contraction forces automakers with legacy diesel-engine capacity to repurpose production lines; Stellantis's decision to equip its 1.5-liter MultiJet diesel with a 48-volt belt-driven starter generator across the Peugeot 3008 and Opel Grandland platforms exemplifies this strategy, extracting residual value from sunk tooling investments while meeting CO₂ targets. Mild-hybrid vehicles, whether diesel or gasoline, enhance fuel economy modestly in urban settings, due to features like regenerative braking and start-stop functionality. Although diesel engines have been known for their efficiency on highways, the fuel savings in urban stop-and-go scenarios are not as pronounced as once thought, diminishing the perceived advantage of diesel efficiency. Fleet operators are now leaning towards 48-volt mild-hybrid gasoline systems. These systems not only simplify maintenance and sidestep the complexities of diesel particulate filter regeneration but also offer urban fuel savings without significant added costs.

Falling 48V System Costs

BloombergNEF's annual surveys reveal a consistent decline in lithium-ion battery pack prices over the years. Since 2010, global average prices have seen a notable drop. In 2023, the average price stood at approximately USD 139 per kWh, marking a decrease from prior years. Looking ahead, 2025 surveys project an average price of around USD 108 per kWh across all segments. As automakers seek cost-effective methods to improve fuel efficiency and comply with stringent emissions regulations, the adoption of 48-volt mild-hybrid systems is increasing. Analysis reveals that 48 V belt-driven starter generators (BSGs) dominate the landscape of mild-hybrid propulsion systems, striking a commendable balance between performance and cost.

Consumer Shift from BEV to Hybrids Amid Cost and Charging Anxiety

A survey commissioned by the Society of Motor Manufacturers and Traders (SMMT) reveals that most respondents in the United Kingdom view the scarcity of public charging infrastructure as a hurdle to buying electric vehicles. Notably, 44.4% highlighted a lack of local chargepoints, while 37.6% pointed out the limited number of operational chargepoints for extended journeys. These infrastructure challenges, alongside increasing vehicle prices and changes in incentives, lead consumers to favor hybrid powertrains. Mild hybrids, in particular, provide fuel efficiency advantages without relying on public charging stations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid BEV Price Parity | −0.5% | Western Europe, Premium Segments First | Medium Term (2–4 Years) |

| Non-Harmonized Tax Rules for Mild Hybrids | −0.3% | EU-Wide, Varying by Member State | Short Term (≤ 2 Years) |

| Belt-Drive Durability and Warranty Risk | −0.2% | Global OEM Platforms Using 48V Belt Starter Generators | Medium Term (2–4 Years) |

| 80–100 V MOSFET Supply Constraints | −0.1% | Semiconductor Hubs in Germany, Netherlands, and Taiwan | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Rapid BEV Price Parity Eroding MHEV Value

Battery-electric vehicles (BEVs) continued to gain traction in Europe in 2025, supported by expanding model availability and more competitive pricing strategies. Several entry-level electric models, particularly in the small-car segment, are now priced around or below EUR 25,000 (approximately USD 27,148) in select European markets, improving affordability relative to internal-combustion alternatives. Tesla has also adopted aggressive pricing in Europe, introducing lower-priced Model 3[3]Marie Mannes, "Tesla launches low-cost Model 3 variant in Europe," Reuters, reuters.com. variants to stimulate demand and enhance competitiveness against premium internal-combustion and hybrid sedans. These developments reflect intensifying price competition in the European battery electric vehicle market as manufacturers seek to accelerate adoption and defend market share amid tightening emissions regulations.

Non-Harmonized Tax Rules for Mild Hybrids

Across Europe, vehicle taxation and incentive regimes for mild hybrids remain non-harmonized, presenting challenges for both manufacturers and buyers. The United Kingdom's Vehicle Excise Duty (VED) reform eliminates preferential discounts for hybrid vehicles, aligning CO₂-based taxation with that of conventional petrol and diesel models. Consequently, mild hybrids will be taxed based on their emissions band, similar to traditional vehicles. In contrast, zero-emission vehicles will benefit from reduced rates during their first year. In Italy, the current Ecobonus schemes prioritize electric and low-emission vehicles, with no formal incentives available for mild hybrids. As a result, the adoption of mild hybrids is expected to rely primarily on private economic considerations rather than government subsidies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: 48-Volt Dominance Anchored in ADAS and Compliance Economics

The 48-volt segment captured an 87.13% Europe mild hybrid vehicles market share in 2025 as OEMs exploited its ability to trim 8-12 g/km CO₂ at a fraction of full-hybrid cost. DC-DC converters let them retain legacy 12-volt loads, avoiding wholesale redesign. Above-48-volt packs, required for regenerative braking in 3.5-ton vans, are projected to grow at a 21.37% CAGR through 2031.

Automakers are turning to 48-volt mild-hybrid systems as a budget-friendly solution to boost fuel efficiency and curb emissions, especially in light of tightening standards like Euro 7. These 48V systems enable advanced features such as regenerative braking, torque assist, and improved start-stop functionality, leading to greater reductions in fuel consumption and CO₂ emissions compared to traditional 12V systems.

By Vehicle Type: Corporate Fleets Anchor Passenger-Car Volume While LCV Operators Chase TCO Gains

Passenger cars accounted for 81.26% of the 2025 volume as fleet buyers optimized benefit-in-kind taxation. Commercial vehicles, however, are set to clock a 14.18% CAGR to 2031 as last-mile operators target sub-EUR 40,000 (approximately USD 47,000) vans that sidestep payload penalties.

In Germany, the taxation of company cars employs a standard 1% "Benefit-in-Kind" (BIK) rule for internal combustion vehicles. In contrast, fully electric vehicles enjoy a reduced tax base of 0.25% of their gross list price, albeit up to certain thresholds. Plug-in hybrids, contingent on meeting specific range and CO₂ criteria, are taxed at intermediate rates. This approach underscores a fiscal differentiation rooted in the vehicle's powertrain type. Notably, hybrids failing to meet these stringent criteria forfeit their preferential status, reverting to the standard 1% rate, a shift that significantly impacts corporate fleet choices.

By Powertrain Type: Gasoline Leads but Diesel Finds High-Mileage Niches

Gasoline mild hybrids held 68.42% of the mix in 2025, due to lower particulate output suited to low-emission zones. Diesel mild hybrids, though smaller, are poised for a 17.63% CAGR as Euro 7’s delay gives high-torque fleets breathing room.

Gasoline mild hybrids, with their lower upfront costs compared to diesel variants, sidestep the maintenance complexities tied to diesel particulate filters. These filters often elevate service needs throughout a vehicle's lifespan. As a result, the total cost of ownership leans towards gasoline mild hybrids, particularly in urban and suburban settings.

By Propulsion Technology: Belt-Driven Systems Rule on Retrofit Economics

Belt-Driven Starter Generator (BSG) held a 56.08% share in 2025 because it drops into existing engine bays with minimal tooling. Integrated starter-generators are poised to expand at an 18.92% CAGR through 2031 as Bosch and Valeo scale compact, belt-free units that erase warranty risk.

Southern Europe’s heat-related belt failures highlight the retrofit trade-off, yet belts remain cheapest for volume B- and C-segment cars. The European mild hybrid vehicles industry, therefore, balances retrofit affordability against long-term durability in propulsion choices.

Geography Analysis

Germany commands 29.31% of market share in 2025, anchored by Volkswagen's MQB-platform scale and the Bundesamt für Wirtschaft und Ausfuhrkontrolle's continued inclusion of 48-volt hybrids in its CO₂-based vehicle-tax bands. BMW's decision to extend 48-volt mild-hybrid availability across its 3 Series lineup, including diesel variants, reflects the technology's compliance role in Europe's largest automotive economy, where manufacturers face penalties for every gram per kilometer above the fleet target.

In 2025, Italy saw a notable surge in hybrid vehicle adoption, largely propelled by compact hatchbacks like the Fiat Panda, tailored for the country's narrow urban roads. The Italian market showcases a preference for compact mild-hybrid hatchbacks, a choice influenced by the nation's tight urban streets and the scarcity of home-charging facilities. Additionally, the growing emphasis on reducing emissions and government incentives for hybrid vehicles have further contributed to the increasing adoption of these vehicles in Italy. Automakers are also focusing on expanding their hybrid offerings to cater to this demand, ensuring a wider range of options for consumers.

The Nordic countries and Benelux, where battery electric vehicle penetration exceeded 30% in 2024, show the steepest mild-hybrid share declines among buyers under 45 years old, a demographic that prioritizes digital connectivity and over-the-air updates, features more commonly bundled with BEV platforms. Eastern Europe, where average household income trails Western Europe by 40%, gravitates toward sub-EUR 25,000 (approximately USD 29,393) mild-hybrid hatchbacks that deliver 15 to 20% fuel savings over conventional gasoline engines without the range anxiety of battery electric vehicles.

Competitive Landscape

The top five OEMs, Volkswagen, Stellantis, Mercedes-Benz, BMW, and Renault, account for a significant share of the 2025 volume, resulting in a moderate concentration profile for the European mild hybrid vehicles market. Stellantis’s eDCT roll-out across four brands trims per-unit drivetrain cost by double digits, matching Asian rivals that leverage vertically integrated 48-volt supply chains. BMW’s blanket rollout across the 3 Series preserves CO₂ compliance flexibility amid uncertain battery electric vehicle uptake.

The competitive dynamic tilts toward automakers that have production between BEV, plug-in hybrid, and mild-hybrid variants on a single platform. For example, Volkswagen's MQB architecture, which accommodates all three powertrains with 70% parts commonality, exemplifies this strategy and enabled the group to backfill battery electric vehicle shortfalls with mild-hybrid volume at its Wolfsburg and Zwickau plants in 2025.

White-space opportunities concentrate in the commercial-vehicle segment, where mild-hybrid penetration lags passenger cars despite last-mile delivery operators' need for sub-EUR 40,000 (approximately USD 47,000) light commercial vans that meet urban low-emission-zone thresholds.

Europe Mild Hybrid Vehicles Industry Leaders

-

Volkswagen AG

-

Audi AG

-

BMW Group

-

Toyota Motor Corporation

-

Nissan Motor Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: As of November 2025, in the mild hybrid electric vehicle (MHEV) segment, the BMW pool and the Mercedes‑Volvo‑Polestar‑Smart pool continued to dominate European registration shares, capturing 37% and 36%, respectively, year-to-date.

- September 2025: DAF Components showcased its mild‑hybrid solution for buses and coaches at Busworld Europe 2025 in Brussels, presenting the system alongside its new PACCAR MX‑11 and MX‑13 engine series. The mild‑hybrid drivetrain, developed in collaboration with Voith and already implemented in over 110 city buses in Rome.

Europe Mild Hybrid Vehicles Market Report Scope

A mild hybrid refers to a vehicle with an internal combustion engine supported by a small electric drive. The electric motor recovers braking energy (recuperation) and makes it available later as additional drive power to reduce fuel consumption. Mild hybridization always requires installing an e-machine with an inverter in the powertrain in addition to the combustion engine.

The European mild hybrid vehicles market is segmented by battery type, vehicle type, powertrain type, propulsion technology, and country. By battery type, the market is segmented into less than 48-volt battery, 48-volt battery, and above 48-volt battery. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By powertrain type, the market is segmented into gasoline mild hybrid and diesel mild hybrid. By propulsion technology, the market is segmented into belt-driven starter generator, integrated starter generator, and crankshaft-mounted starter generator. By country, the market is segmented into Germany, the United Kingdom, France, Italy, Spain, and the Rest of Europe.

The report offers market size and forecasts for mild hybrid vehicles in value (USD) and volume (units) for all the above segments.

By Battery Type

| Less Than 48 Volt |

| 48 Volt |

| Above 48 Volt |

By Vehicle Type

| Passenger Cars |

| Commercial Vehicles |

By Powertrain Type

| Gasoline Mild Hybrid |

| Diesel Mild Hybrid |

By Propulsion Technology

| Belt-Driven Starter Generator (BSG) |

| Integrated Starter Generator (ISG) |

| Crankshaft-Mounted Starter Generator |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Battery Type | Less Than 48 Volt |

| 48 Volt | |

| Above 48 Volt | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By Powertrain Type | Gasoline Mild Hybrid |

| Diesel Mild Hybrid | |

| By Propulsion Technology | Belt-Driven Starter Generator (BSG) |

| Integrated Starter Generator (ISG) | |

| Crankshaft-Mounted Starter Generator | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How large will the Europe mild hybrid vehicles market be by 2031?

How large will the Europe Mild Hybrid Vehicles Market be by 2031?

Which battery architecture dominates European mild hybrids?

48-volt packs held 87.13% share in 2025 and remain the standard for CO₂ compliance and ADAS power needs.

Why do corporate fleets prefer mild hybrids over BEVs?

Fleet operators avoid range anxiety and upfront BEV premiums while still meeting CO₂ targets and benefiting from favorable tax rules.

Which segment is growing fastest within the market?

Light commercial vehicles are set to expand at a 14.18% CAGR as last-mile operators seek sub-EUR 40,000 vans with urban-zone access.

How are falling BEV prices affecting mild-hybrid demand?

Rapid BEV price parity narrows the cost gap, trimming the mild-hybrid value proposition, especially in high-mileage fleets.

What is the main technical challenge with belt-starter-generators?

Elevated heat shortens belt life to 60,000 km in Southern Europe, driving warranty costs and interest in integrated starter-generators.

Page last updated on: