Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

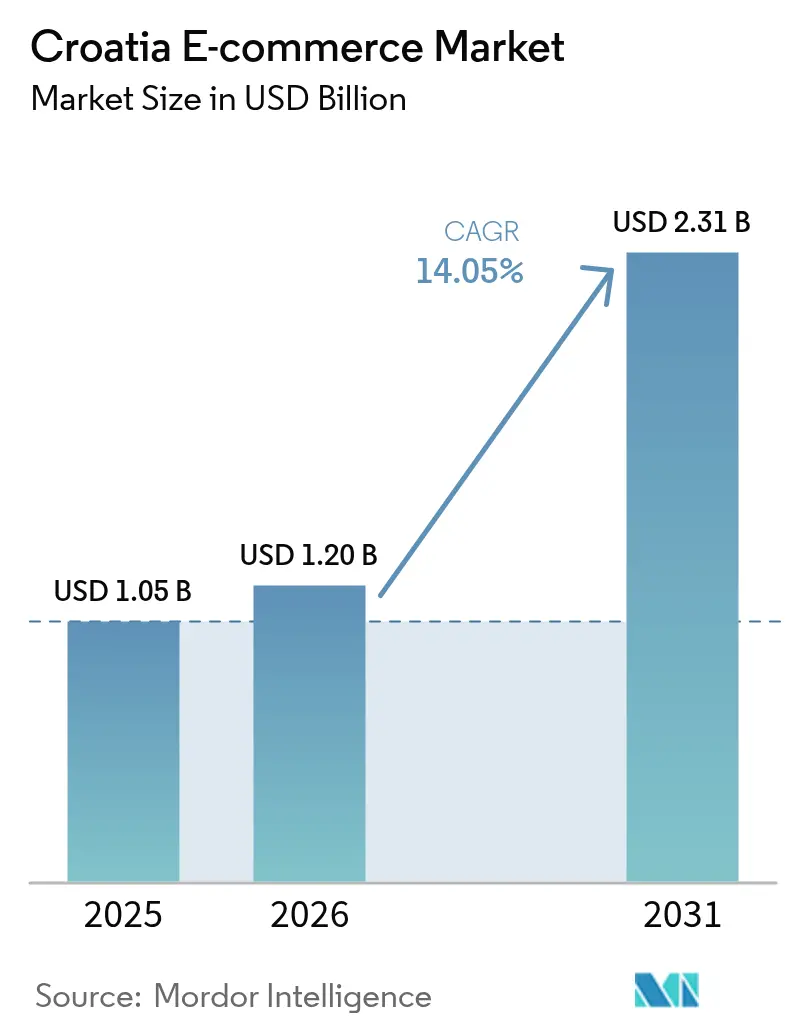

| Base Year Market Size (2025) | USD 1.05 Billion |

| Market Size (2026) | USD 1.2 Billion |

| Market Size (2031) | USD 2.31 Billion |

| Growth Rate (2026 - 2031) | 14.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Croatia E-commerce Market Analysis by Mordor Intelligence

The Croatia e-commerce market size is expected to grow from USD 1.05 billion in 2025 to USD 1.2 billion in 2026 and is forecast to reach USD 2.31 billion by 2031 at 14.05% CAGR over 2026-2031. Rising internet access (84% of the population) and an e-shopper base that now equals 62% of all internet users anchor this trajectory.[1]: Ecommerce Europe, “European E-Commerce Report 2024,” Ecommerce Europe, ecommerce-europe.eu. Government stimulus—most notably the EUR 308 million (USD 336 million) in digitalisation loans and grants disbursed under the National Recovery and Resilience Plan—continues to lower entry barriers for local merchants.[2]European Commission, “Croatia's Recovery and Resilience – Supported Projects,” European Commission, commission.europa.eu. Mobile-first shopping behaviour, a wave of SME web-store launches, and mandated B2B e-invoicing from 2026 are reinforcing demand across consumer and corporate channels. Competitive intensity is escalating as domestic champions eKupi and Konzum defend share against global platforms, prompting a logistics arms race centred on faster fulfilment and automated parcel-locker roll-outs. Meanwhile, seasonal tourism inflows stabilise delivery economics along the Adriatic coast, creating a virtuous cycle of higher order density and lower per-parcel costs.

Key Report Takeaways

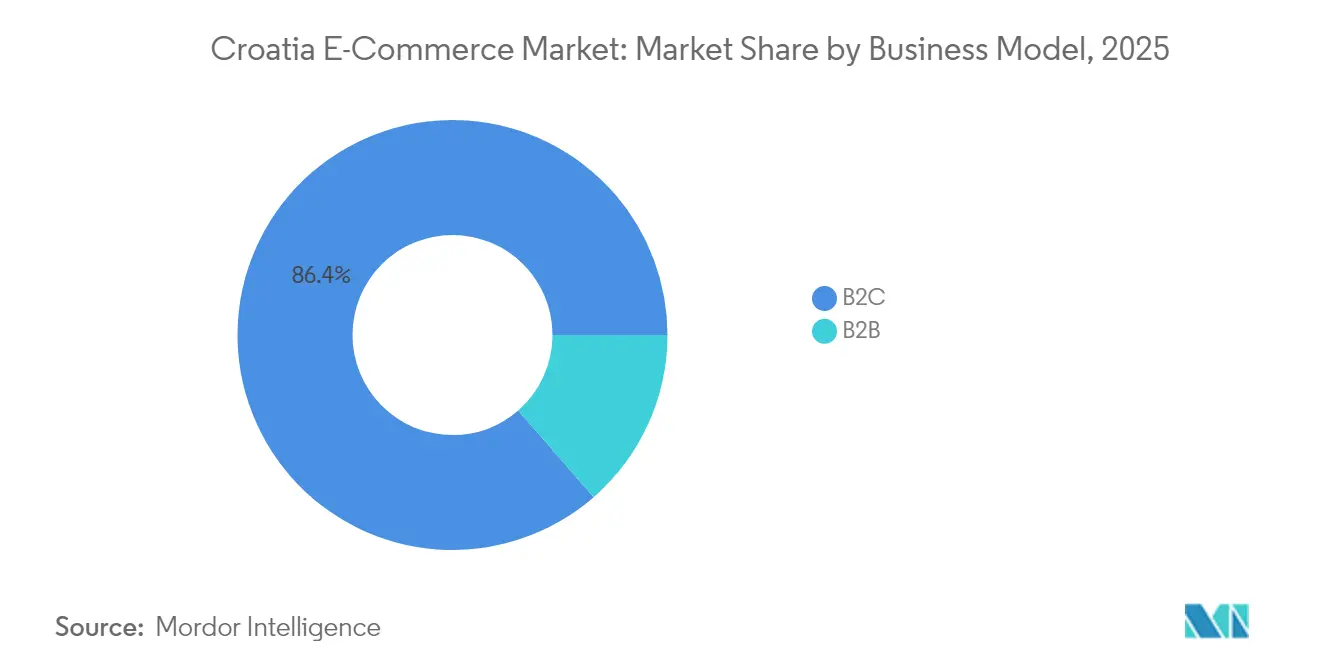

- By business model, the B2C segment held 86.40% of the Croatia e-commerce market share in 2025, while B2B is projected to grow at the fastest 17.48% CAGR through 2031.

- By device type, smartphones commanded 61.45% of the Croatia e-commerce market size in 2025; the “other devices” cluster (smart TVs, voice assistants, wearables) is forecast to expand at a 15.88% CAGR to 2031.

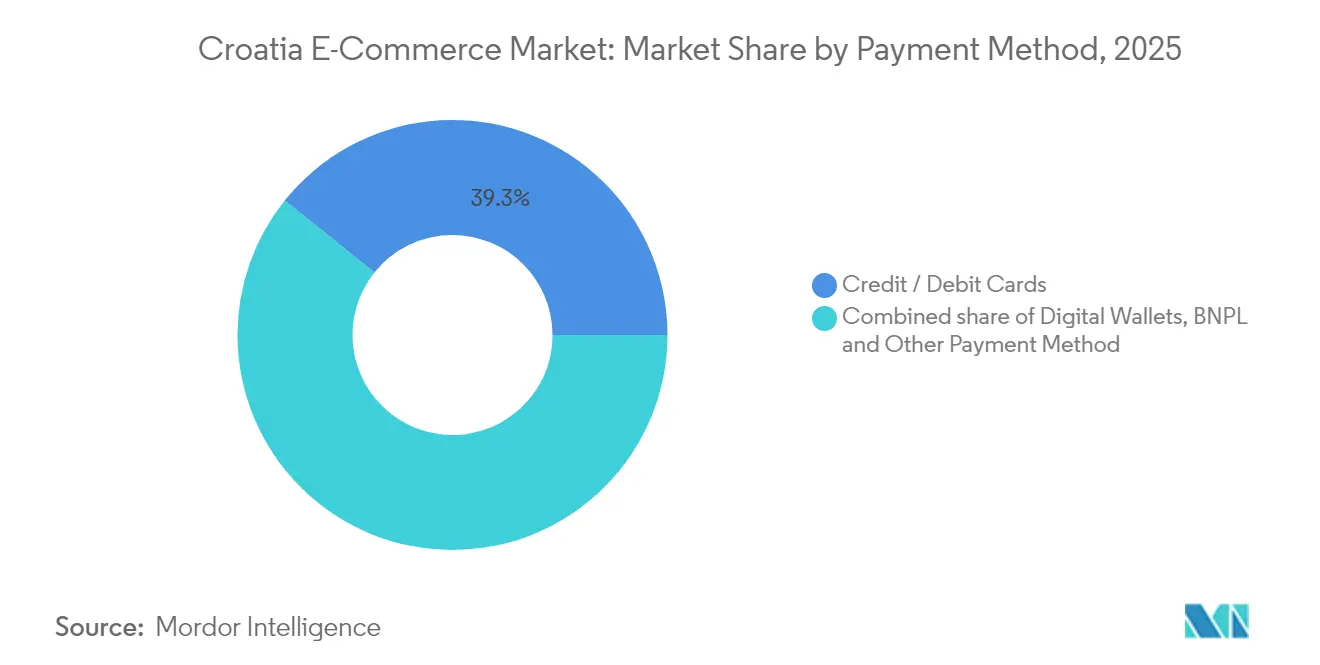

- By payment method, cards led with 39.25% of the Croatia e-commerce market size in 2025, whereas digital wallets are advancing at a 21.63% CAGR through 2031.

- By B2C product category, consumer electronics accounted for 20.60% of the Croatia e-commerce market size in 2025 and food & beverages is accelerating at a 17.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Croatia E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-subsidised SME digital-voucher programme accelerating webshop adoption | 5.7% | National, with concentration in Zagreb and major urban centers | Medium term (2-4 years) |

| Proliferation of automated parcel lockers along Adriatic transport hubs | 4.3% | Coastal regions, particularly tourist destinations | Short term (≤ 2 years) |

| EU eIDAS-compliant digital signature roll-out boosting online B2B procurement | 3.6% | National, with emphasis on business districts | Medium term (2-4 years) |

| Surge in mobile-only bank accounts (e.g., Revolut HR) widening addressable card base | 2.9% | Urban centers, with spillover to smaller towns | Short term (≤ 2 years) |

| Tourism-led seasonal demand peaks stabilise e-grocery last-mile economics | 2.1% | Adriatic coast and islands | Medium term (2-4 years) |

| Digital-native Gen-Z share of disposable income surpassing 25% in 2024 | 1.4% | National, with concentration in university cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-subsidised SME Digital-Voucher Programme Accelerating Webshop Adoption

Croatia’s voucher scheme offers up to EUR 10,000 (USD 10,900) per SME for technology upgrades, catalysing a 51.4% increase in programming enterprises between 2019 and 2023.[3]OECD, “Digital and Green SMEs: Accelerating the Twin Transitions in the Western Balkans,” OECD Publishing, oecd.org. The subsidy removes capital constraints that once delayed online launches and now funds inventory systems, CRM platforms, and secure checkout modules. More than 30,000 firms had drawn on the vouchers by 2025, materially enlarging the Croatia e-commerce market’s merchant base. The initiative also stimulates private-sector demand for local IT service providers, tightening feedback loops between tech talent and retail innovation. Over the medium term, the programme is expected to propagate omnichannel norms even among micro-retailers, broadening category depth and regional coverage.

Proliferation of Automated Parcel Lockers Along Adriatic Transport Hubs

Carriers and retailers have installed self-service lockers at ferry terminals and major coastal transit points, cutting last-mile costs by 22% and failed deliveries by 37%.[4]World Bank, “Croatian Logistics: Opportunities for Sustainable Competitiveness,” World Bank Group, worldbank.org. The 24/7 access resolves the “island premium” cost gap that historically discouraged online shopping among archipelago residents. Locker density also absorbs sharp seasonal surges when tourist volumes push order counts 65-85% above off-peak norms. Short-term benefits include higher first-try delivery success and reduced courier congestion, while long-term gains appear in customer loyalty scores as convenience rises. Operators are layering digital advertising panels on lockers, opening incremental revenue streams and reinforcing coastal brand visibility during peak visitor months.

EU eIDAS-compliant Digital Signature Roll-out Boosting Online B2B Procurement

Croatia’s alignment with EU eIDAS protocols enables friction-less, legally binding digital signatures embedded in its eRačun platform. Approval cycles for cross-border orders now fall by 64%, unlocking working-capital efficiencies for SMEs engaged in EU trade. Mandatory e-invoicing for VAT payers from 2026 reinforces the new normal, anchoring the projected 18.1% CAGR for B2B commerce. Procurement portals integrate the signature layer with Peppol, accelerating supplier onboarding and catalogue updates. Over the medium term, buyers shift repetitive spot purchases to digital frameworks, shrinking manual paperwork and elevating audit-trail transparency, which, in turn, attracts foreign partners seeking compliant sourcing hubs within the EU.

Surge in Mobile-only Bank Accounts Widening Addressable Card Base

Neobanks such as Revolut simplify KYC and deliver loyalty-led rewards, driving mobile-based payments to 28% of all Croatian online transactions—well above the euro-area mean. The friction-less onboarding expands card issuance among younger cohorts and first-time banking customers in second-tier cities. Embedded analytics fine-tune credit risk, enabling instant buy-now-pay-later decisions that lift average order values. Wallet providers also experiment with local merchant cashback to stimulate repeat purchases, reinforcing the Croatia e-commerce market’s conversion funnel. Short-term gains materialise in higher checkout completion rates, while in the long term, richer transaction data informs hyper-personalised promotions and micro-credit offers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High domestic courier tariffs to island municipalities inflate shipping costs | -3.6% | Adriatic islands and remote coastal areas | Medium term (2-4 years) |

| Card-on-file reluctance among 55+ cohort limits conversion rates | -2.9% | National, more pronounced in rural areas | Long term (≥ 4 years) |

| Warehouse labour shortages in Zagreb–Karlovac logistics corridor | -2.1% | Central Croatia, particularly Zagreb metropolitan area | Short term (≤ 2 years) |

| Fragmented address database causing delivery-first-attempt failure >8% | -1.4% | National, with higher impact in newly developed areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Domestic Courier Tariffs to Island Municipalities Inflate Shipping Costs

Parcel surcharges run 35-45% above mainland rates, tightening category economics for low-margin staples. Ferry dependencies and weather-linked disruptions elongate delivery windows and erode the perceived convenience premium of e-commerce. While hub-and-spoke pilots in coastal centres show promise, sustained cost parity remains elusive because route density outside peak tourist months is thin. SME merchants often exclude islands from free-shipping promotions, dampening order volumes and constraining the overall Croatia e-commerce market’s geographic expansion. Mid-term mitigation hinges on coordinated maritime timetable optimisation and shared micro-fulfilment nodes financed through EU cohesion funds.

Card-on-file Reluctance Among 55+ Cohort Limits Conversion Rates

Customers aged 55 and above abandon carts at 2.4 times the rate of younger users when confronted with saved-card prompts. Security and privacy concerns rooted in pre-digital banking habits deter credential storage, prolonging checkout flows and suppressing lifetime value. Guest-checkout workarounds lift single-purchase conversions but forfeit repeat-buy efficiency. Cash-on-delivery still appeals in rural zones yet raises return risk and logistics overhead. Over the long term, education campaigns led by banks and consumer-protection agencies, coupled with tokenised payment rails, aim to narrow the trust deficit and unlock incremental demand within this demographic.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Growth Outpaces Dominant B2C

The B2C segment controlled 86.40% of the Croatia e-commerce market size in 2025, generating USD 509 in average revenue per active shopper. Continuous smartphone adoption and intuitive payment interfaces keep entry barriers low for mass-market categories such as fashion and electronics. Domestic multi-category platforms leverage local inventory pools to promise next-day delivery across mainland urban clusters, while cross-border marketplaces augment SKU breadth at competitive prices. Marketing spend tilts toward social-commerce integrations that resonate with Gen Z, whose disposable-income share exceeded 25% in 2024.

B2B commerce, at 13.60% of turnover, is forecast to compound at 17.48% annually through 2031—outstripping the wider Croatia e-commerce market. Mandated e-invoicing and eIDAS-grade signatures compress transaction lead times and broaden procurement networks across the EU. Industrial distributors migrate catalogues online, inserting punch-out integrations into enterprise resource-planning systems to capture long-tail orders. Early adopters report internal process-cost savings of up to 30%, validating the economic case for further digital migration. As corporate buyers automate approval chains, order frequency rises, deepening vendor lock-in and lifting platform stickiness.

By Device Type: Mobile Commerce Dominates While Alternative Devices Emerge

Smartphones captured 61.45% of the Croatia e-commerce market share in 2025, reflecting superior 4G/5G coverage and a mobile internet culture anchored in chat-based service interactions. Retailers optimise glide-paths with one-hand checkout, biometric authentication, and push-notification re-engagement loops. Seamless in-app loyalty widgets drive higher repeat purchase propensity relative to desktop sessions.

Alternative devices—smart TVs, voice assistants, wearables—are poised for a 15.88% CAGR, signalling the next shopper interface wave. Media-streaming platforms embed “buy-as-you-watch” overlays, while voice commerce gains traction for routine household replenishment. Desktop relevance persists for high-involvement, research-heavy purchases such as enterprise IT gear, underscoring the omnichannel imperative. Device-agnostic payment tokens harmonise experience quality, reinforcing the total Croatia e-commerce market size advantage built on frictionless access across screens.

By Payment Method: Digital Wallets Challenge Card Dominance

Cards remained the primary tender with 39.25% of the Croatia e-commerce market size in 2025, underpinned by widespread issuer coverage and strong consumer chargeback protection. A surge in tokenisation, 3-DS2 protocols, and instant refund features helps sustain trust.

Digital wallets are scaling at a 21.63% CAGR, closing the gap via embedded loyalty, cross-border fee transparency, and behavioural-data-driven offers. Revolut’s RevPoints programme signed up 100,000 Croatian users within one month of debut, accelerating wallet penetration. BNPL volumes double-digit grow, especially in fashion baskets, as zero-interest instalments resonate with budget-sensitive millennials. Cash-on-delivery recedes yet retains relevance in rural same-day niches. Regulatory PSD2 support for open-banking APIs paves the way for account-to-account pay-by-link flows, broadening choice and fee competition.

By B2C Product Category: Food & Beverages Surge While Electronics Lead

Consumer electronics held a 20.60% share of the Croatia e-commerce market size in 2025, propelled by standardised SKUs and high value-to-weight economics. Specialist sites deploy augmented reality configurators and AI-powered product guides to mitigate feature complexity and reduce returns. Cross-border sellers maintain price pressure, pushing domestic players toward service bundles such as extended warranties and onsite installation.

Food & beverages, advancing at a 17.31% CAGR, benefits from grocery chains’ dark-store investments and cold-chain fleet upgrades. Konzum’s EUR 10 million (USD 10.9 million) injection into fulfilment infrastructure in 2024 accelerated slot availability and reduced substitution rates. Seasonal tourism skews volume toward the coast, enabling density-driven cost optimisation. Fashion and beauty categories continue to scale on the back of free returns and influencer-led discovery, whereas furniture growth is moderated by bulky-goods logistics constraints.

Geography Analysis

Zagreb and its wider metropolitan zone account for roughly 39.60% of Croatia e-commerce market transactions owing to dense broadband coverage, high purchasing power, and proximity to the Zagreb–Karlovac logistics corridor. Fulfilment centres cluster near highway junctions, allowing next-day delivery across central Croatia even under peak Black Friday loads. Warehouse labour shortages, however, inflate operating costs and necessitate robotics adoption for picking and packing.

The Adriatic coastal belt, anchored by Split, Rijeka, and Dubrovnik, posts the sharpest seasonal swings as tourism inflates basket volumes by up to 85% during summer. Automated parcel-locker networks at ports absorb off-hours pickups, enhancing customer experience and dampening courier overtime expenses. Retailers calibrate regional stock buffers to prevent stock-outs of consumables popular with visitors, such as sunscreen and convenience snacks.

Island municipalities and interior rural areas still trail in order frequency due to elevated shipping surcharges and patchy address databases. The government has earmarked EUR 133 million (USD 145 million) for gigabit connectivity to 100,000 underserved households by 2026. As coverage improves, mobile commerce is expected to leapfrog desktop adoption, offering merchants new growth corridors once last-mile costs normalise through locker mini-hubs and maritime schedule optimisation.

Competitive Landscape

The top ten platforms capture an estimated 65% of Croatia e-commerce market turnover, evidencing moderate concentration. Local leaders eKupi, Konzum, and Sancta Domenica anchor share on the strength of domestic warehousing, proximity sourcing, and Croatian-language after-sales support. International entrants Zalando and About You deploy data-science-driven assortment curation and cross-border shipping subsidies to win fashion-savvy millennials. Amazon and AliExpress, while present through direct-to-consumer imports, face longer transit times that cap share growth in impulse categories.

Competition pivots on fulfilment speed, payment choice, and niche category mastery. Konzum’s EUR 15 million (USD 16.4 million) automated Zagreb facility triples e-grocery throughput, signalling a shift toward high-automation fulfilment as labour markets tighten. eKupi’s acquisition of Chipoteka consolidates the electronics long tail and yields buying-power synergies. Lidl’s same-day coastal delivery pilot tests the viability of micro-fulfilment nodes targeting tourist hotspots.

Regulatory change also shapes strategic agendas. The upcoming Digital Product Passport under CWA 18186 will heighten transparency in sustainability attributes, favouring early adopters able to surface traceability data at point of sale. Meanwhile, SME voucher recipients intensify competitive churn as an influx of newly online micro-retailers fragments share in artisanal and region-specific product lines. Larger incumbents counter by integrating these SMEs into marketplace formats, preserving traffic scale while enriching assortment diversity.

Croatia E-commerce Industry Leaders

Ekupi d.o.o

Sancta Domenica d.o.o.

Fliba d.o.o.

Bauhaus-Zagreb k.d.

Pevex d.d.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Konzum opened an automated fulfilment centre in Zagreb, investing EUR 15 million (USD 16.4 million) to triple e-grocery order capacity and cut picking errors by 300%, supporting its fresh-produce same-day pledge.

- April 2025: eKupi acquired Chipoteka, adding high-margin PC components and strengthening its negotiating leverage with global electronics vendors.

- March 2025: Lidl Hrvatska rolled out same-day delivery in coastal cities, allocating EUR 12 million (USD 13.1 million) to seasonal-capacity hubs ahead of the tourist surge.

- January 2025: Croatian Post installed 150 parcel lockers along Adriatic transport hubs after a EUR 8.5 million (USD 9.3 million) spend, lowering failed delivery rates in island zones.

- December 2024: Revolut launched RevPoints in Croatia, signing 100,000 users in one month and accelerating wallet uptake across fashion and travel bookings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines Croatia's e-commerce market as the total gross merchandise value generated when businesses or consumers located in Croatia purchase physical goods through any internet-enabled interface (web or app) and have them fulfilled by courier, postal service, parcel locker, or in-store pickup. Digital-only content, travel bookings, and purely financial transfers sit outside this boundary, keeping our value strictly focused on tangible retail transactions.

Scope exclusion: Pure-play digital media, online gambling, and cross-border flows that are neither billed nor fulfilled in Croatia are omitted from the model.

Segmentation Overview

- By Business Model

- B2C

- B2B

- By Device Type

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method

- Credit / Debit Cards

- Digital Wallets

- BNPL

- Other Payment Method

- By B2C Product Category

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Detailed Research Methodology and Data Validation

Primary Research

We spoke with executives at domestic marketplaces, third-party logistics providers, parcel-locker operators, and payment gateways across Zagreb, Split, and Rijeka. Their feedback on conversion funnels, average basket values, and COD prevalence helped us validate secondary ratios, surface gray-market leakage, and refine channel splits.

Desk Research

Our analysts reviewed open datasets from Eurostat, the Croatian Bureau of Statistics, the National Bank of Croatia, and the International Telecommunication Union, alongside trade bodies such as Ecommerce Europe and the Croatian Chamber of Economy. These sources calibrate population, income, device usage, parcel volumes, and VAT receipts linked to webshops. Company filings, investor presentations, customs manifests, and news archives captured through Dow Jones Factiva and D&B Hoovers supplied firm-level insights on turnover and pricing. The sources listed illustrate, but do not exhaust, the range of material screened before numbers are finalized.

Market-Sizing & Forecasting

A top-down model starts with household final consumption, splits retail spend by category, and then applies verified online-penetration rates and average ticket values. Shipment statistics and payment-gateway volumes cross-check totals. Select bottom-up roll-ups of leading merchants' revenue and sampled ASP × order counts temper over- or under-reporting. Key inputs include internet-user growth, smartphone share of checkouts, parcel-locker density, VAT e-invoice counts, and credit-card authorization volumes. Forecasts to 2030 rely on a multivariate regression blended with ARIMA to capture macro trends and seasonality, while scenario analysis adjusts for policy shocks such as mandatory e-invoicing.

Data Validation & Update Cycle

Outputs undergo variance scans against alternate data series, peer review by a second analyst, and leadership sign-off. Reports refresh annually; any material event, major tax change, regulatory shift, or M&A triggers an interim update, ensuring clients access the most current baseline.

Why Mordor's Croatia E-commerce Baseline Commands Reliability

Published market values often differ because firms choose distinct scope cut-offs, data vintages, and refresh cadences. Our disciplined separation of domestic GMV from cross-border imports, combined with annual model rebuilds, keeps Mordor's figure closely aligned with on-the-ground spending patterns.

Key gap drivers include whether digital content is counted, how basket values are escalated, the treatment of COD leakage, and the exchange-rate year applied for euro to dollar conversion. Rivals that extrapolate global averages or roll forward pandemic-era penetration can overstate today's baseline, while conservative forecasts may miss policy-driven inflection points such as the 2026 B2B e-invoice mandate.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.05 B (2025) | Mordor Intelligence | - |

| USD 4.96 B (2024) | Global Consultancy A | Includes travel and digital services; no COD adjustment |

| USD 1.17 B (2024) | Data Provider B | Uses modeled averages; refresh cadence biennial |

| USD 0.89 B (2024) | Trade Journal C | Omits B2B transactions and locker-fulfilled orders |

In sum, Mordor Intelligence offers a balanced, transparent baseline grounded in clearly traceable variables and repeatable steps, giving decision-makers a dependable starting point for strategy.

Key Questions Answered in the Report

How large is the Croatia e-commerce market in 2026 and how fast is it growing?

The Croatia e-commerce market is valued at USD 1.2 billion in 2026 and is on track for a 14.05% CAGR to reach USD 2.31 billion by 2031.

Which business model is expanding the fastest in Croatian e-commerce?

B2B commerce, currently 13.60% of turnover, is rising at an 17.48% CAGR as mandatory e-invoicing and digital signatures streamline corporate procurement.

What payment method is gaining the most traction online?

Digital wallets, boosted by Revolut’s RevPoints launch, are set to grow at a 21.63% CAGR, challenging the 39.25% share still held by cards.

Why are automated parcel lockers important for Croatia’s market?

Lockers reduce last-mile costs by 22% and failed deliveries by 37% along the coast, mitigating high courier tariffs and seasonal volume spikes.

Which product category tops online sales and which is growing fastest?

Consumer electronics leads with a 20.60% share, while food & beverages is the fastest-growing category at a 17.31% CAGR to 2031.

How concentrated is the competitive landscape?

The top ten platforms command about 65% of sales, reflecting moderate concentration with ongoing space for specialist entrants and regional niches.

Page last updated on: