Human Papillomavirus Vaccine Market Size and Share

Market Overview

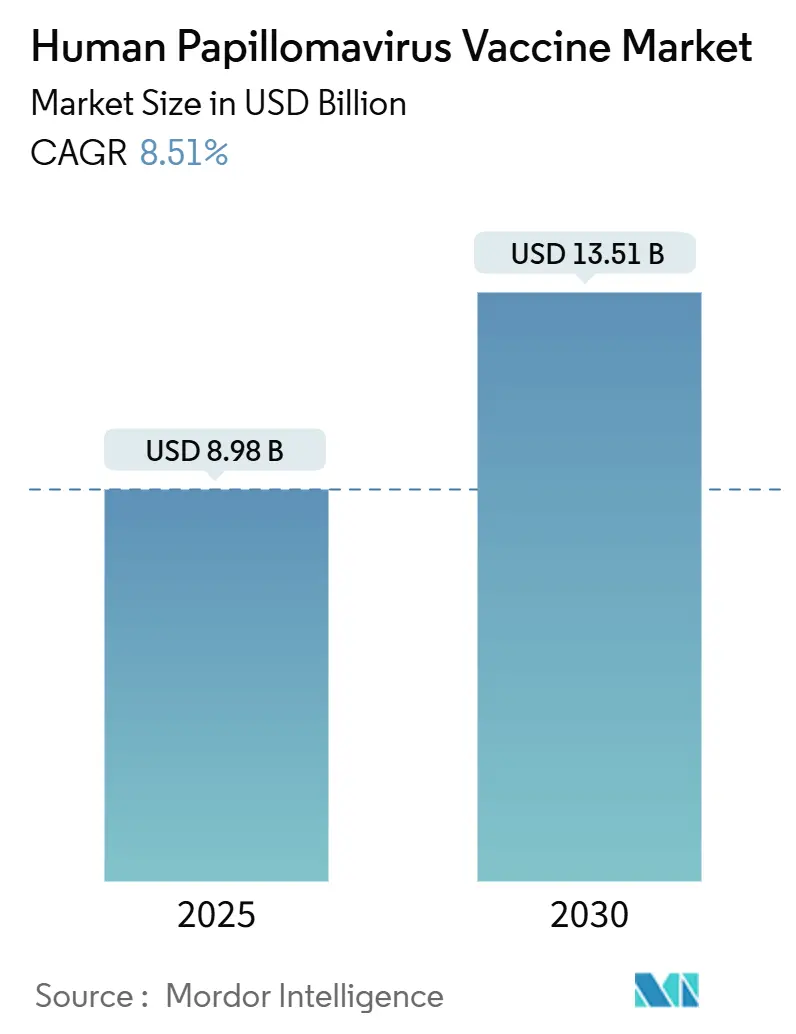

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 8.98 Billion |

| Market Size (2030) | USD 13.51 Billion |

| Growth Rate (2025 - 2030) | 8.51% CAGR |

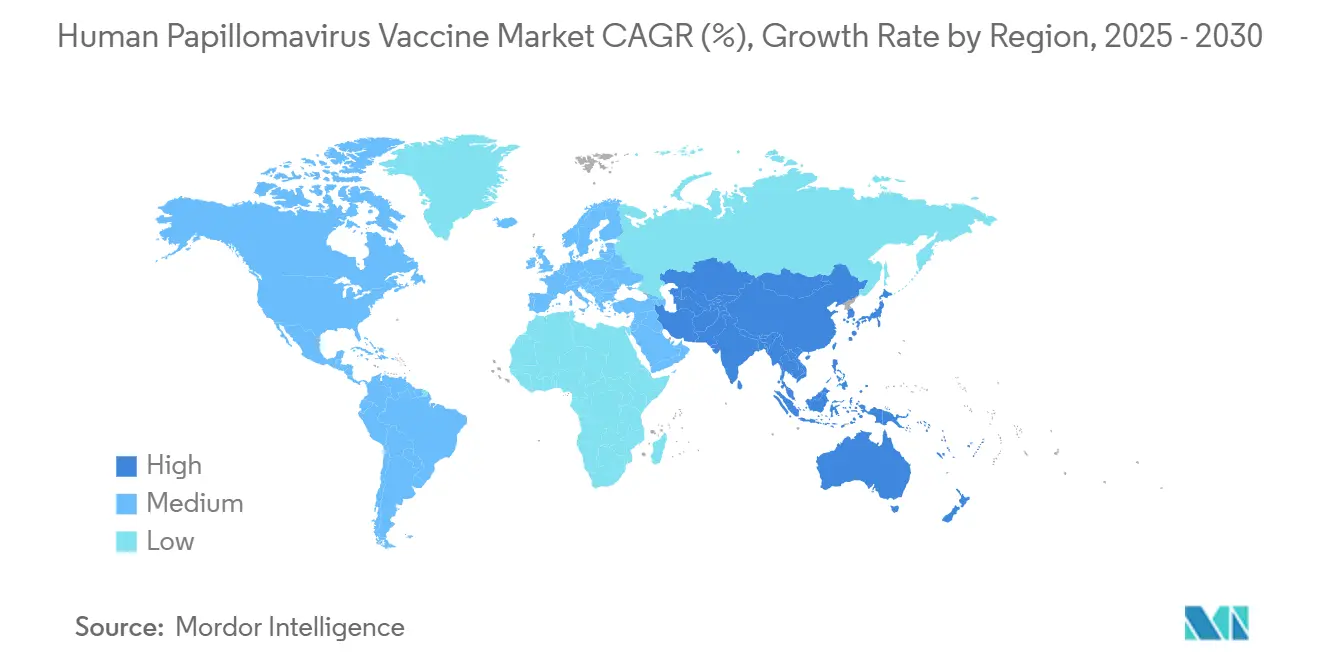

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Human Papillomavirus Vaccine Market Analysis by Mordor Intelligence

The human papillomavirus vaccine market is valued at USD 8.98 billion in 2025 and is on track to reach USD 13.51 billion by 2030, advancing at an 8.51% CAGR. Single-dose schedules endorsed by the World Health Organization (WHO) in late-2024 [1]World Health Organization, “Single-Dose HPV Vaccine Position Paper,” who.int , a surge of low- and middle-income country (LMIC) manufacturers, and widening gender-neutral policies are redefining clinical demand patterns. The rapid uptake of nonavalent formulations, large-scale government funding commitments in India, China and the European Union, and the extension of FDA labels to cover head-and-neck cancers together sustain robust volume growth. Manufacturers are simultaneously re-tooling production for single-dose regimens and region-specific multivalent platforms, while payers negotiate tiered pricing that broadens access without eroding margins. These forces position the human papillomavirus vaccine market for sustained expansion across public programs and premium private segments worldwide.

Key Report Takeaways

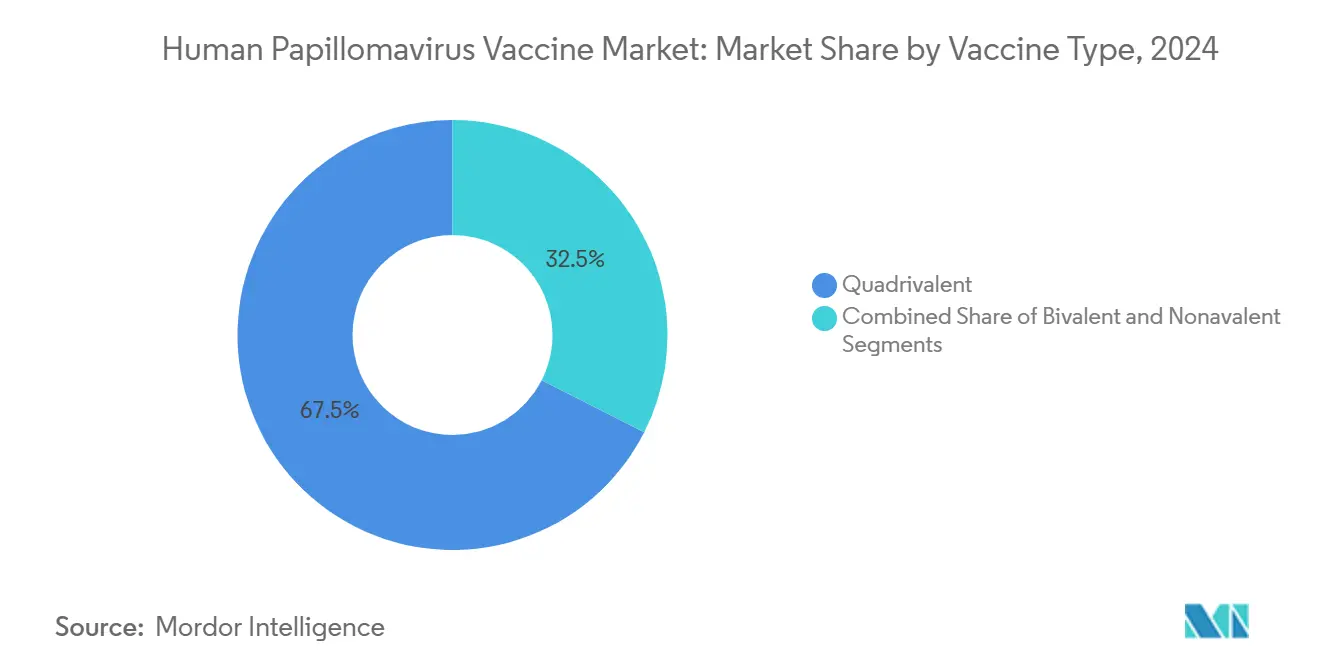

- By vaccine type, quadrivalent products led with 67.53% revenue share in 2024, while nonavalent formulations are projected to expand at a 9.24% CAGR to 2030.

- By indication, cervical cancer prevention held 69.98% of the human papillomavirus vaccine market share in 2024, whereas anal cancer prevention is advancing at a 9.31% CAGR through 2030.

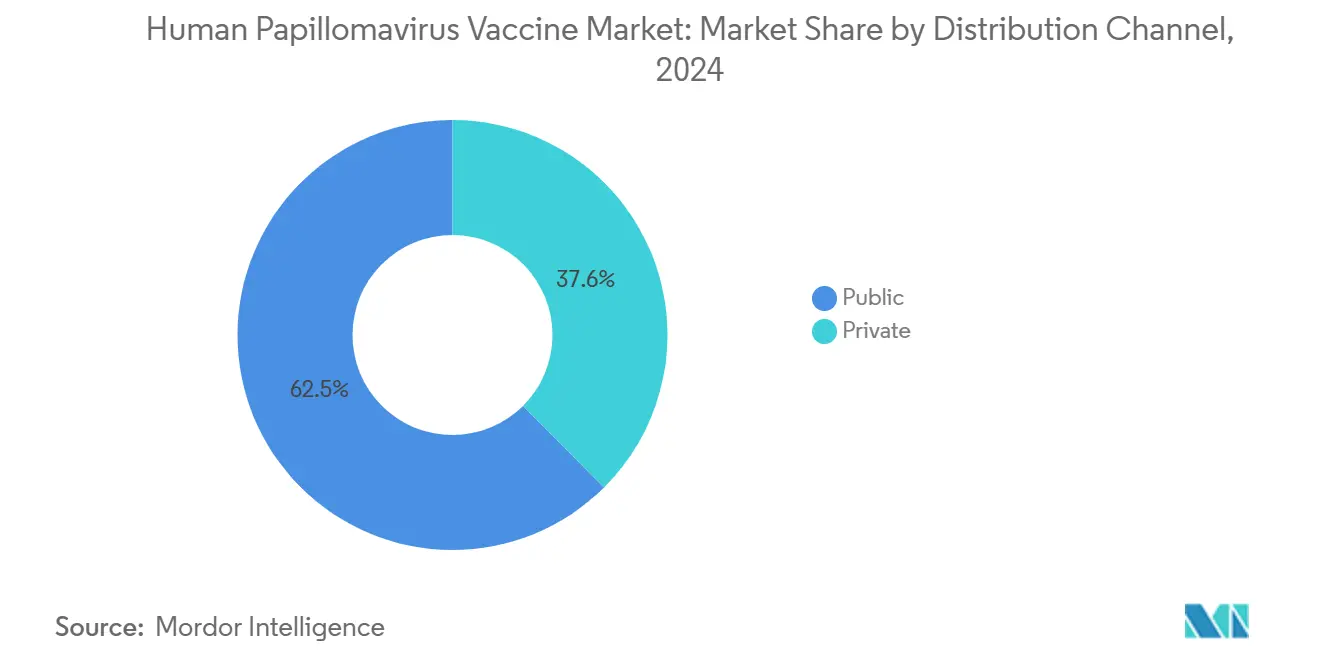

- By distribution channel, public programs commanded 62.45% of the human papillomavirus vaccine market size in 2024, while private healthcare outlets are growing at 9.42% CAGR during the forecast period.

- By age group, adults accounted for 59.65% share of the human papillomavirus vaccine market size in 2024, yet pediatric vaccination is set to post the fastest 9.13% CAGR to 2030.

- By geography, North America captured 39.48% share of the human papillomavirus vaccine market in 2024, but Asia-Pacific is on course for the strongest 9.22% CAGR through 2030.

Global Human Papillomavirus Vaccine Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Approval of new multivalent HPV vaccines | +1.8% | Global; early adoption in North America & EU | Medium term (2-4 years) |

| Government & multi-lateral funding accelerators | +2.1% | LMIC focus; Gavi-supported countries; India & China | Long term (≥ 4 years) |

| Gender-neutral immunization policies | +1.5% | North America; EU; Australia; expanding to Asia-Pacific | Medium term (2-4 years) |

| Rising HPV-linked cancer incidence | +1.2% | Global; especially oropharyngeal cancers in developed markets | Long term (≥ 4 years) |

| One-dose schedule endorsed by WHO | +1.7% | Worldwide; accelerated adoption in LMICs | Short term (≤ 2 years) |

| Emergence of LMIC-based vaccine manufacturers | +0.9% | Asia-Pacific; Africa; Latin America | Long term (≥ 4 years) |

Source: Mordor Intelligence

Approval of New Multivalent HPV Vaccines

Recent FDA clearance of Gardasil 9 for head-and-neck cancer prevention extends protective reach beyond gynecological malignancies and opens male adult segments. Merck and several Asian developers are advancing next-generation multivalent candidates aimed at HPV types highly prevalent in Africa and South-East Asia, reinforcing the premium tier of the human papillomavirus vaccine market. WHO’s pipeline review lists more than 20 therapeutic vaccines, signalling future convergence of preventive and therapeutic modalities [2]World Health Organization, “HPV Vaccine R&D Pipeline,” who.int . Collectively, these innovations underpin volume growth and encourage price differentiation across regions.

Government & Multi-Lateral Funding Accelerators

India’s 2024 budget funded a national girls’ program using locally produced Cervavac at USD 24 per private-sector dose, creating the largest single expansion in the human papillomavirus vaccine market. Gavi’s USD 600 million commitment and UNICEF’s aggregate procurement surpassing 93 million doses since 2013 provide stable demand forecasts that justify capacity builds in Asia and Latin America [3]Gavi, “HPV Vaccine Programme Commitments,” gavi.org . Similar agreements under PAHO in 2025 further aggregate regional orders, lowering unit cost and widening access.

Gender-Neutral Immunization Policies

The transition from female-only to gender-neutral programs effectively doubles the eligible cohort in several high-income markets. Taiwan’s June 2025 decision to vaccinate boys free of charge underscores widening regional acceptance. European Union funding under the PROTECT-EUROPE project accelerates the same pivot, reinforcing long-term demand within the human papillomavirus vaccine industry. Clinical evidence from ASCO shows vaccinated males experiencing a lower incidence of HPV-related malignancies, strengthening the policy rationale.

One-Dose Schedule Endorsed By WHO

WHO guidance of October 2024 concludes that a single dose offers comparable protection to multi-dose regimens, a finding already operational in 57 countries by September 2024. The simplified schedule eases cold-chain logistics, halves per-capita vaccine cost, and unblocks uptake in settings where school attendance and follow-up are challenging. Manufacturers are reformulating existing nonavalent platforms into single-dose vials while LMIC producers see faster regulatory pathways, sharpening competition in the human papillomavirus vaccine market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent biologics regulations | -1.4% | Global; particularly complex in emerging markets | Medium term (2-4 years) |

| Vaccine hesitancy & misinformation | -2.3% | Worldwide; amplified by social media | Short term (≤ 2 years) |

| High procurement cost for MICs | -1.1% | Middle-income countries; non-Gavi eligible | Long term (≥ 4 years) |

| Cold-chain & last-mile gaps in LMICs | -0.8% | Sub-Saharan Africa; rural Asia; remote Latin America | Medium term (2-4 years) |

Source: Mordor Intelligence

Stringent Biologics Regulations

Complex biologics frameworks require exhaustive safety and potency data, driving development costs above USD 1 billion per candidate and delaying approvals for regional manufacturers. European Medicines Agency dossiers add another tier of compliance, while WHO prequalification remains essential for multilateral tenders. These layers heighten time-to-market and favor incumbents with deep capital reserves, tempering the growth of smaller entrants in the human papillomavirus vaccine market.

Vaccine Hesitancy & Misinformation

Social-media-driven skepticism, especially around adolescent sexuality, suppresses uptake even where vaccines are subsidized. Studies publishing increased parental refusals in metropolitan Nigeria and comparable patterns in parts of Europe illustrate the headwind. Counter-campaigns involving religious and community leaders succeed, but demand sustained financing and coordination, slowing trajectory in the near term.

Segment Analysis

By Vaccine Type: Nonavalent Innovation Challenges Quadrivalent Dominance

Quadrivalent vaccines retained 67.53% share in 2024, underpinning broad national program penetration. Their entrenched status supports predictable revenue flow, yet premium-priced nonavalent products are outpacing at a 9.24% CAGR. The human papillomavirus vaccine market size for nonavalent offerings is expanding strongly in North America and Europe as payers endorse wider oncogenic strain coverage. This shift also benefits middle-income consumers willing to pay for broader protection, even while procurement agencies in LMICs continue purchasing cost-efficient quadrivalent or bivalent doses.

Global clinical evidence shows Gardasil 9 delivering near-universal cervical cancer protection and 90% efficacy against other HPV-related conditions. WHO prequalification of Cecolin for single-dose schedules and Walrinvax for two-dose regimes broadens supply options, pressuring price points in the human papillomavirus vaccine market. Looking forward, region-specific multivalent candidates designed for African and Asian strain prevalence may further fragment the competitive field.

By Indication: Cervical Cancer Prevention Expands to Male-Focused Applications

Cervical cancer prevention accounted for 69.98% of 2024 revenue thanks to entrenched public-health focus and decades of supportive data. Yet anal cancer prevention is rising fastest at 9.31% CAGR because gender-neutral policies recognize growing male disease burden. The human papillomavirus vaccine market share for cervical applications will gradually erode as non-cervical indications gain prominence, though absolute revenues continue growing.

FDA extension of Gardasil 9 to head-and-neck cancers validates expansion beyond female-centric indications and informs adult catch-up programs. Peer-reviewed data reveal a rising incidence of oropharyngeal cancer among men, catalyzing policy updates worldwide. Manufacturers are therefore repositioning value propositions toward comprehensive cancer prophylaxis that appeals to both sexes.

By Distribution Channel: Private Sector Growth Outpaces Public Programs

Public tenders controlled 62.45% of doses in 2024, dominated by Gavi, UNICEF and national ministries. Nevertheless, private outlets are posting a 9.42% CAGR as urban middle-classes seek convenience and earlier vaccination. This dual structure compels suppliers to calibrate differential pricing; for instance, Serum Institute offers Cervavac at INR 2,000 (USD 24) privately versus INR 300-400 in government schemes.

European procurement showcases efficiency, with average tender prices sliding from EUR 101.8 in 2007 to EUR 28.4 by 2017. CDC data echo payment-linked disparities, where privately insured adolescents display higher completion than Medicaid or uninsured cohorts. Future volume gains in the human papillomavirus vaccine market stem from hybrid public-private models that expand reach while protecting manufacturer margins.

By Age Group: Adult Catch-Up Programs Drive Market Expansion

Adults represented 59.65% sales in 2024, reflecting legacy cohorts that missed early immunization. Catch-up demand remains strong after the CDC broadened recommendations to 27-45-year-olds, though uptake is uneven at 16% in that bracket. Conversely, pediatric programs deliver the fastest 9.13% CAGR as countries introduce vaccination at 9 years and adopt single-dose regimens.

Evidence that earlier initiation improves series completion from 47% to over 60% by age 13 guides strategy. Long-term surveillance finds 79% fewer cervical precancers among women aged 20-24 who received adolescent vaccination, reinforcing cost-effectiveness arguments. In turn, this encourages governments and insurers to fund earlier, broader coverage, cementing lifetime value within the human papillomavirus vaccine market.

Geography Analysis

North America’s 39.48% share reflects early adoption, broad insurance coverage, and ongoing gender-neutral catch-up initiatives. The United States still shows payment-linked gaps, yet Canada’s 2024 single-dose recommendation for those aged 9-20 positions it as a policy bellwether. Mexico’s participation in PAHO’s elimination roadmap promises synergies in pricing and procurement across the sub-region.

Asia-Pacific leads growth at a 9.22% CAGR, propelled by India’s fully funded girls’ program and China’s surge of domestic producers challenging Western incumbents. Merck’s 41% Q1-2025 sales decline in China highlights intensifying price competition and regulatory complexity. Japan’s shift to 9-valent vaccines for boys and girls, together with Australia’s mature elimination strategy, illustrates the diversity of policy models that collectively enlarge the human papillomavirus vaccine market size across the region.

Europe continues policy innovation through its 90% female coverage and expanding male vaccination mandate, underwritten by EUR 20 million in EU4Health funds. Competitive tenders sustain affordability without compromising supply security. The Middle East and Africa face cold-chain and hesitancy barriers, yet Nigeria’s 2024-2025 drive to reach 7.7 million girls shows that community-centric engagement can secure high utilization. In South America, PAHO’s 2025 partnership with Spanish agencies enhances access to 9-valent vaccines, while differential economics across the continent necessitate phased rollouts.

Competitive Landscape

The human papillomavirus vaccine industry is moderately concentrated. Merck continues to dominate with the Gardasil franchise but faces unprecedented legal and commercial headwinds, including USD 8 billion in safety litigation and rapid share loss in China. Investments in an expanded Elkton, Virginia plant and single-dose Gardasil 9 formulations are designed to defend leadership.

GSK maintains a cost-centric niche through Cervarix, while Serum Institute’s Cervavac and newly WHO-prequalified Chinese entrants erode price floors, especially in LMIC tenders. Emerging pipelines feature therapeutic gene therapies such as Precigen’s PRGN-2012 for recurrent respiratory papillomatosis, pending FDA priority review in August 2025. Digital tracking platforms integrated with electronic medical records are becoming a differentiator, allowing companies to document coverage evidence and reinforce value propositions with payers.

White-space segments include adult male vaccination, therapeutic vaccines, and region-specific multivalent formulations. Suppliers able to navigate complex biologics regulation, deploy tiered pricing, and support community-driven education campaigns will capture outsized gains in the human papillomavirus vaccine market through 2030.

Human Papillomavirus Vaccine Industry Leaders

-

Serum Institute of India Pvt. Ltd.

-

Wantai BioPharm

-

INOVIO Pharmaceuticals

-

Merck & Co., Inc.

-

GSK plc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Taiwan confirmed free HPV vaccinations for boys from September 2025, benefiting an estimated 90,000 beneficiaries annually.

- February 2025: PAHO and Spanish development agencies agreed to scale cervical cancer elimination programs, expanding 9-valent vaccine access in Latin America.

- January 2025: The Philippines Department of Health launched a fully funded HPV immunization program targeting 95% female coverage nationwide.

- November 2024: Merck presented Gardasil 9 adult data at the International Papillomavirus Conference, reinforcing the rationale for gender-neutral vaccination up to age 45.

Global Human Papillomavirus Vaccine Market Report Scope

As per the scope of this report, human papillomavirus vaccines are vaccines that are utilized to prevent HPV infection. HPV is a group of more than 100 viruses, of which 13 can cause cancer, and nearly all cases of cervical cancer are attributed to HPV. The human papillomavirus vaccine market is segmented by type (bivalent, quadrivalent, nonavalent), indication (cervical cancer, anal cancer, penile cancer, oropharyngeal cancer, genital warts, and others), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| By Vaccine Type | Bivalent | ||

| Quadrivalent | |||

| Nonavalent | |||

| By Indication | Cervical Cancer | ||

| Anal Cancer | |||

| Penile Cancer | |||

| Oropharyngeal Cancer | |||

| Genital Warts | |||

| Others | |||

| By Distribution Channel | Public | ||

| Private | |||

| By Age Group | Adults | ||

| Pediatric | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Bivalent |

| Quadrivalent |

| Nonavalent |

| Cervical Cancer |

| Anal Cancer |

| Penile Cancer |

| Oropharyngeal Cancer |

| Genital Warts |

| Others |

| Public |

| Private |

| Adults |

| Pediatric |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the projected value of the human papillomavirus vaccine market by 2030?

The market is expected to reach USD 13.51 billion by 2030, growing at an 8.51% CAGR.

Why are single-dose HPV schedules significant for LMICs?

Single-dose regimens cut follow-up visits in half and lower delivery cost, which improves coverage in settings with limited healthcare infrastructure.

Which vaccine type is growing fastest in the human papillomavirus vaccine market?

Nonavalent formulations show the quickest trajectory, expanding at a 9.24% CAGR through 2030 due to broader strain protection.

How are gender-neutral policies affecting demand?

Including boys effectively doubles the eligible population, accelerating uptake in North America, Europe and increasingly in Asia-Pacific.

Which region offers the highest growth potential to 2030?

Asia-Pacific is forecast to post the strongest 9.22% CAGR, driven by large-scale national programs and expanding domestic manufacturing.

What role do private channels play in vaccine distribution?

Private outlets are the fastest growing channel at 9.42% CAGR, catering to middle-income consumers willing to pay for convenience and early access.

Page last updated on: July 1, 2025