Home Draft Beer Dispensers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 132.12 Million |

| Market Size (2031) | USD 181.19 Million |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Draft Beer Dispensers Market Analysis by Mordor Intelligence

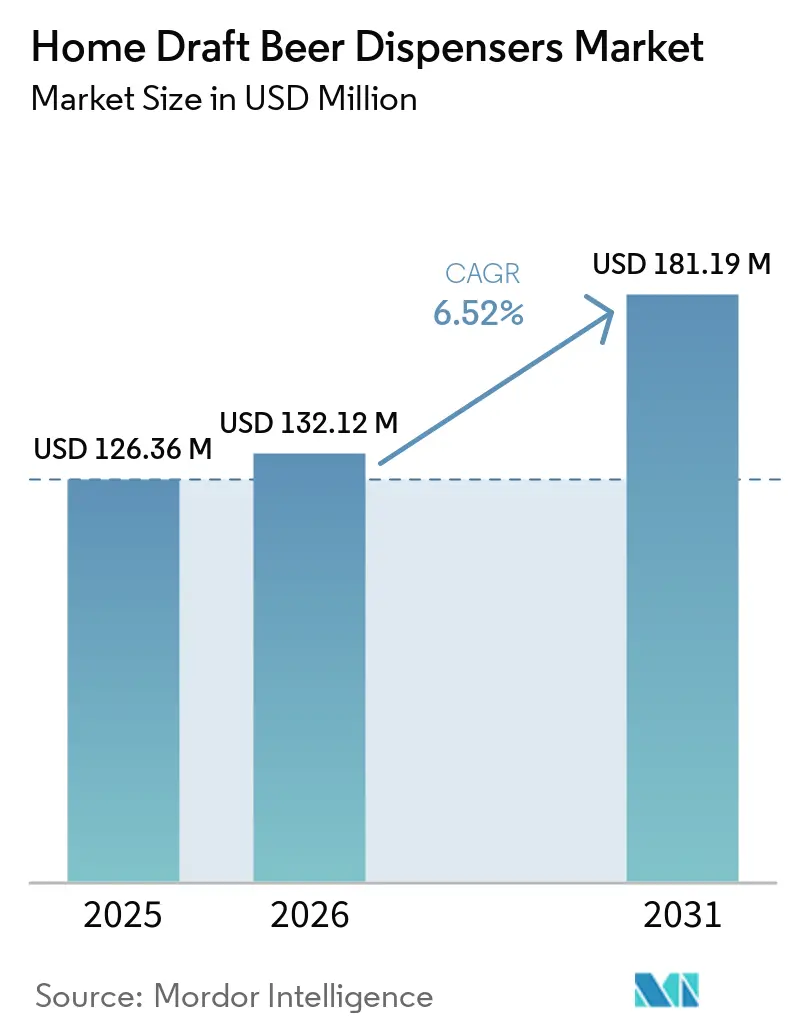

The home draft beer dispensers market size is expected to increase from USD 126.36 million in 2025 to USD 132.12 million in 2026 and reach USD 181.19 million by 2031, growing at a CAGR of 6.52% over 2026-2031. Growth reflects a steady transition from novelty gadgets to functional premium appliances as 5 to 8 L countertop draft ecosystems reduce the gap between bar-quality pours and home convenience. Manufacturers prioritize better refrigeration, compact footprints, and integrated pressure control to extend freshness windows to 30 days and to simplify use for first-time buyers who prefer plug-and-pour experiences over traditional kegerator setups. Smart connectivity adds value by enabling app-based temperature management, pour tracking, and predictive maintenance, which shifts differentiation from hardware alone toward a connected dispensing ecosystem supported by DTC keg logistics where regulations allow. Compliance updates in India around safety and energy performance raise product standards and discourage grey imports, which tend to advantage established brands that design energy-efficient compressors, compliant electronics, and recyclable refrigerants into their bill-of-materials from the outset.

Key Report Takeaways

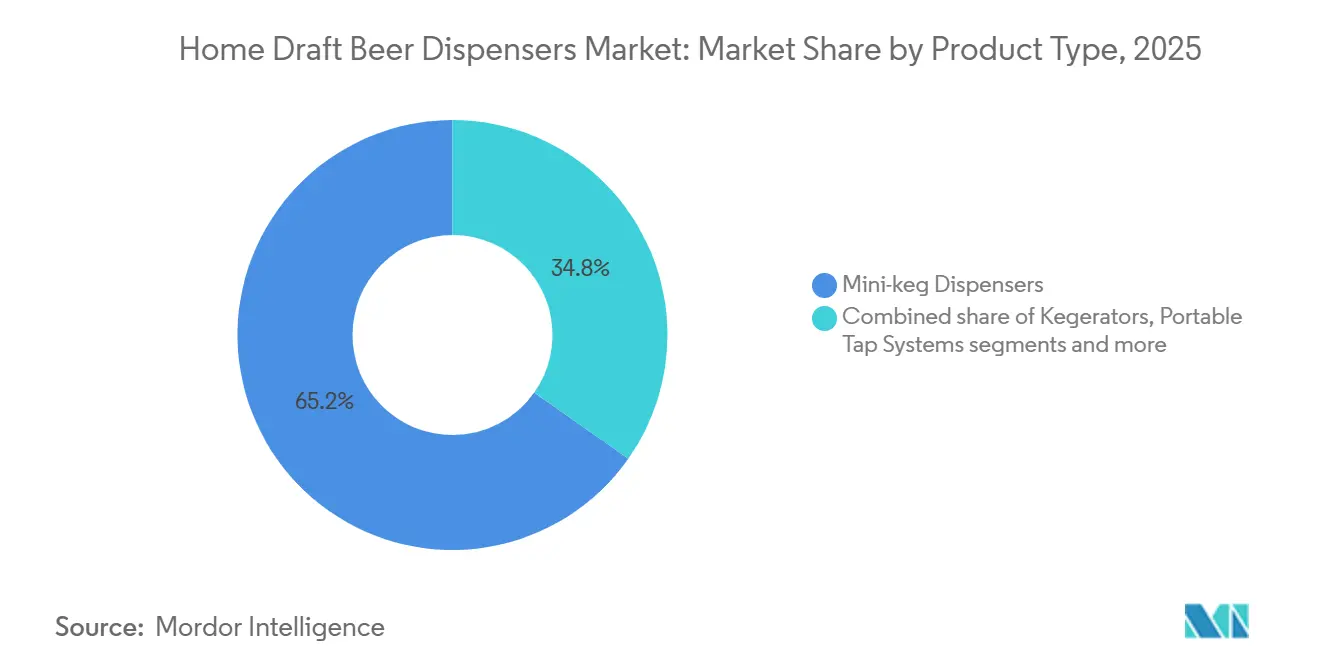

- By product type, mini-keg dispensers captured 65.23% of the home draft beer dispensers market share in 2025. By product type, countertop draft systems are projected to grow at 7.01% CAGR between 2026 and 2031.

- By technology, direct-draw refrigeration held 52.91% share of the home draft beer dispensers market size in 2025. By technology, smart IoT-enabled systems are projected to grow at 7.20% CAGR between 2026 and 2031.

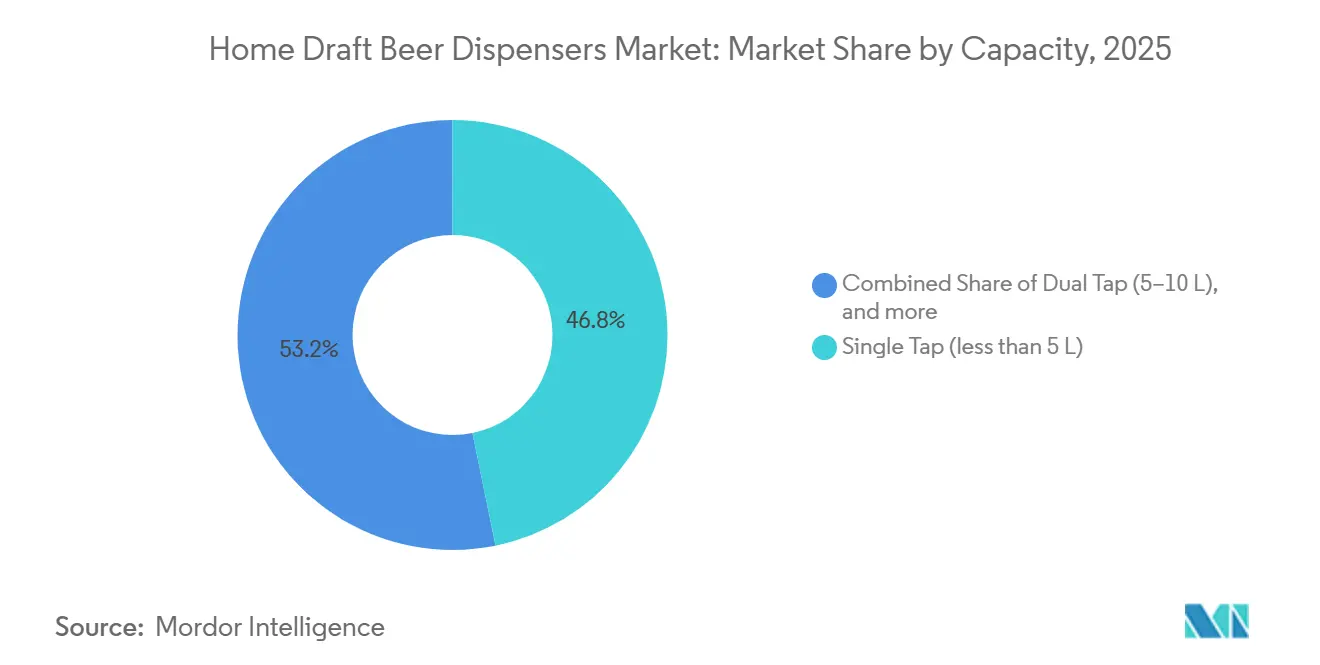

- By capacity, single-tap systems below 5 liters captured 46.80% of the home draft beer dispensers market share in 2025. By capacity, dual-tap systems from 5 to 10 liters are projected to grow at 6.88% CAGR between 2026 and 2031.

- By distribution channel, specialty retailers held 64.24% share of the home draft beer dispensers market size in 2025. By distribution channel, online retail and DTC are projected to grow at 8.65% CAGR between 2026 and 2031.

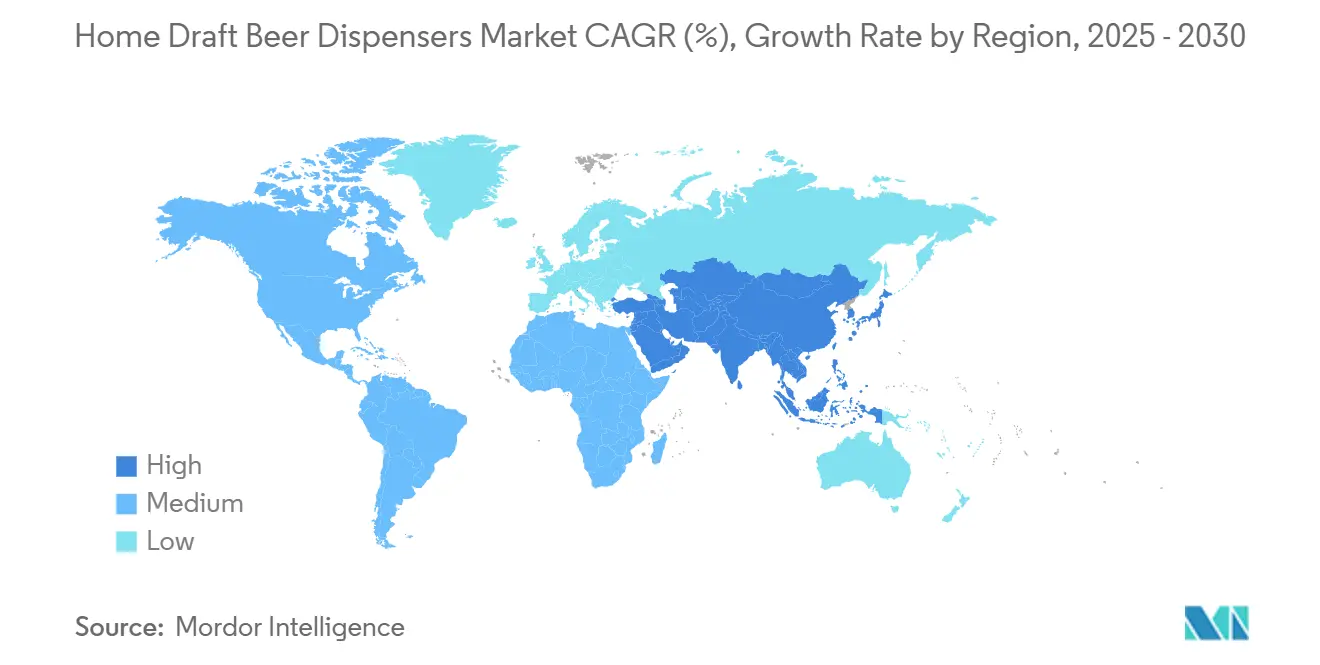

- By geography, North America accounted for 36.61% share in 2025. By geography, Asia-Pacific is projected to grow at 7.96% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Home Draft Beer Dispensers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost advantage of keg-format vs bottles/cans at home | +0.9% | Global, stronger in North America and Western Europe | Medium term (2-4 years) |

| Expansion of at-home premium draft experiences via retail and DTC | +1.1% | Asia-Pacific core with spill-over to urban Latin America and Middle East and Africa | Medium term (2-4 years) |

| Energy-efficient, compact refrigeration and improved pour control | +0.7% | EU, India, North America | Long term (≥ 4 years) |

| Ease-of-use, freshness windows up to 30 days | +1.0% | Global, strongest in tier-I cities | Short term (≤ 2 years) |

| Shift from 2L micro-keg systems to 5-8L countertop ecosystems | +1.3% | North America and Europe leading, Asia-Pacific premium corridors | Medium term (2-4 years) |

| Smart, app-connected features improving UX and engagement | +1.5% | North America, EU, Japan, South Korea, tech-forward Asia-Pacific cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost Advantage of Keg-Format Versus Bottles/Cans at Home

Purchasing craft beer by the keg can deliver a 25% to 35% per-liter saving relative to six-pack premiums when brewers bypass distributor markups through direct-to-consumer subscriptions and closed-loop deposit schemes. AB InBev’s PerfectDraft ecosystem processed over 76 million e-commerce orders and generated USD 550 million in FY25 across Zé Delivery, TaDa Delivery, and PerfectDraft, alongside £5 Beer Tokens per returned 6-liter keg, equivalent to USD 6.35, which subsidizes repeat purchases and recaptures return logistics [1]PerfectDraft, “How to Return Your PerfectDraft Kegs,” PerfectDraft, perfectdraft.com. This keg-credit logic inverts the traditional retail model by returning a share of distribution margins to consumers through loyalty credits while improving brewer data on consumption and preferences through app interfaces tied to order histories. Regulatory structures vary by market, and in India, excise regimes continue to govern alcohol logistics at the state level, which shapes the feasibility of direct keg deliveries even as appliance certifications remain centralized under BIS for household electrical devices. This balance of keg economics, DTC logistics, and state-level alcohol rules shapes adoption patterns in the home draft beer dispensers market, where markets are liberalizing slowly, while premium buyers focus on value and quality.

Expansion of At-Home Premium Draft Experiences via Retail and DTC

Specialty retailers held a large share of 2025 sales, but the online and DTC channels are scaling faster as buyers seek subscription bundles that pair connected dispensers with curated keg assortments and offer return credits. Category momentum aligns with India’s premiumization cycle, where monthly consumer-durables spending rose sharply in FY25, which highlights a broader willingness to invest in smart and energy-efficient home appliances and supports a shift toward at-home premium experiences. Keg subscription models that bundle hardware and logistics, such as Ridge Rock Brewing’s higher-tier plan that includes a branded two-tap kegerator, illustrate how equipment costs can be amortized against contracted volumes to deliver predictable household inventory and smoother production planning for brewers. DTC players also communicate verified efficiency and performance metrics through digital channels more effectively than in-store sales, especially as India’s BEE strengthens testing, labeling, and dispute-resolution infrastructure with the National Test House for appliance claims. These digital journeys encourage trial among consumers who prioritize convenient delivery, easy returns, and transparent lifecycle cost, which collectively support DTC growth within the home draft beer dispensers market even as brick-and-mortar remains important for demonstrations and installation advice.

Energy-Efficient, Compact Refrigeration and Improved Pour Control

Direct-draw refrigeration maintained the largest 2025 share, while thermoelectric and smart systems scale on the strength of variable-speed compressors, precise thermal control, and tighter temperature tolerances that protect carbonation and flavor stability. Micro Matic’s FlexiDraft Countertop, launched in 2026, uses contact cooling to chill slim 10-liter kegs quickly, isolates beer from atmospheric oxygen with one-way lines, and supports 30-day freshness with an internal CO₂ supply, which expands placement options for homes and micro-venues that lack space for external tanks. EdgeStar’s dual-tap kegerator highlights the category’s power-use transparency with Energy Star designation, 85-watt operation, and digital controls from 32°F to 50°F, which helps buyers estimate electricity bills as they size equipment to their space and style preferences. India’s 2024 policy wave across 18 appliance points to 2030 electricity saving targets and lower refrigerant GWP thresholds by 2026, which catalyzes the move to R290 or R600a in compressor platforms and penalizes older-imported systems still using R134a, a shift that carries through to kegerators and beverage refrigerators[3]CLASP, “India Unveils 18 New Appliance Efficiency Policies,” CLASP, clasp.ngo . Consistent pour quality improves through dual-gauge regulators and better pressure control across 5 to 15 PSI, while portable growler systems like GrowlerWerks’ uKeg sustain carbonation in double-wall insulated steel for two weeks, which extends use cases beyond fixed installations into outdoor and casual settings.

Ease-of-Use, Freshness Windows (Up to 30 Days) Expanding Addressable Users

Next-generation countertop systems reduce setup friction to minutes and extend freshness from a few days to up to 30 days, which addresses a key barrier for mainstream adoption in the home draft beer dispensers market. Heineken’s BLADE employs 8-liter pre-pressurized kegs with factory-set regulation and steady 2°C cooling, eliminating the need for external CO₂ canisters and reducing component complexity for novice users who prefer turnkey experiences. Summit Appliance’s patent-pending Floating Tap design separates the tap from the cabinet to enable countertop placement without permanent modifications, which helps renters and seasonal users switch between draft and standard refrigeration quickly[4]PTC, “Celli Case Study: IoT in Food and Beverage Industry,” ptc.com. iGulu’s F1 integrates app-enabled controls for fermentation, preservation, and dispensing in a 3.8 liter chamber with RFID activation and external CO₂ support like SodaStream, which supports up to 30 days of freshness or a 24-hour air mode for quick sessions. In India, strong demand for appliance convenience in 2026 aligns with premiumization and home-ownership trends in major and tier-II cities, which supports the adoption of dishwasher-safe trays, tool-free loading, and auto-clean cycles that match dual-income household needs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront and running costs for premium units | -0.8% | Global, sharper in price-sensitive Asia-Pacific and South America | Short term (≤ 2 years) |

| Maintenance/cleaning complexity and CO₂ logistics | -0.6% | Regions with sparse distributor networks | Medium term (2-4 years) |

| Product discontinuation risk reducing buyer confidence | -0.4% | Global, particularly impacting early adopters in North America and EU who invested in proprietary ecosystems | Medium term (2-4 years) |

| DIY conversion kits cannibalizing new-unit sales | -0.3% | North America and Europe, where homebrewing culture is established, minimal in the Asia-Pacific markets, lacking technical expertise or aftermarket parts distribution | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront and Running Costs for Premium Units

Mid to high-tier kegerators range between USD 799 and USD 1,249, and recurring costs like CO₂ refills at USD 13.99 per 60-liter cylinder, cleaning kits, and gasket replacements raise the total cost of ownership for price-sensitive buyers. Kegco’s digital single-tap unit lists at USD 938.70 and consumes near 85 watts, which can add USD 60 to USD 84 annually to electricity costs at USD 0.12 per kWh, a hidden cost that buyers often overlook during in-store evaluations. India’s EMI schemes help spread payments, though fees can lift effective prices by 8% to 12%, which prolongs payback for households that benchmark per-serve costs against 650 ml bottles priced INR 150 to INR 200, equivalent to USD 1.8 to USD 2.4 using 2025 exchange assumptions. GrowlerWerks’ uKeg 128, at USD 205.99 to USD 229.99 depending on finish, uses 16-gram CO₂ cartridges priced near USD 1.50 each, which is manageable for casual use but adds to perceived maintenance for value-focused buyers. Power draw varies widely by model class, and commercial-oriented 50-liter-per-hour units like PortaPint’s 50C draw 480 watts and 2.5 amperes, which can push monthly power bills well above residential-class units if run continuously. Industry groups in India continue to lobby for rate relief on large appliances, which could improve affordability for energy-efficient draft units that adopt low-GWP refrigerants and inverter compressors.

Maintenance/Cleaning Complexity and CO₂ Logistics

Beer-line hygiene requires consistent cleaning every 3 to 4 weeks to prevent off-flavors and biofilm, which involves disassembly and recirculation procedures that can deter casual users of the home draft beer dispensers market. Summit’s Floating Tap design reduces friction by allowing quick tap removal for sink cleaning and reversible conversion to standard refrigeration, but the discipline of regular sanitation remains a must for quality pours. CO₂ logistics are straightforward in major North American metros with welding-supply exchanges and homebrew shops, but sparse distributor networks in rural regions and many tier-III Indian cities force mail-in exchanges with multi-day turnarounds and added shipping fees. Mail-in exchange services that integrate with smartphone workflows help, but they require advance planning that clashes with spontaneous entertaining, where bottled inventory can be replenished on routine store visits. Pre-pressurized ecosystems like BLADE simplify setup by eliminating external tanks, but they introduce proprietary keg lock-in and reliance on brewer-specific filling lines that can limit local assortment depth. India’s BIS certification focuses on electrical safety, including thermal cut-offs and pressure-relief mechanisms, but hygiene and CO₂ handling protocols remain largely manufacturer-led, which leaves education gaps for first-time owners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Portability and Installation Simplicity Redefine Entry Points

Mini-keg dispensers accounted for a 65.23% share of the home draft beer dispensers market size in 2025, helped by sub-USD 200 price points and compatibility with disposable 2 to 5 liter kegs that avoid external CO₂, while countertop draft systems are the fastest-growing on 7.01% CAGR as users graduate to 6 to 10 liter ecosystems with integrated cooling, better pour control and brewer-aligned logistics. Full-size kegerators serve dedicated home bars and micro-venues with dual and triple taps, but their taller height and heavier loaded weights limit mobility and call for space planning that apartment dwellers often avoid. Portable tap systems like GrowlerWerks’ uKeg offer tailgate and outdoor utility at USD 205.99 to USD 229.99, which extends category reach beyond fixed installations. Countertop units such as Micro Matic’s FlexiDraft Countertop and PerfectDraft lean on 6 to 10 liter formats with plug-and-pour simplicity and return credits that foster repeat purchasing patterns and app-based engagement. Production capacity expansions in India for refrigerators and ACs inform cost-downs in shared compressor and control architectures, which encourage domestic assemblers to extend into beverage-dispensing SKUs with local compliance baked in.

Category boundaries also blur as countertop ecosystems support proprietary keg formats, bundled glassware and loyalty credits, which pull hardware into a services-led journey in the home draft beer dispensers market. Full-size units maintain an edge for high-volume entertaining and variety on tap, while portable growlers keep short-session freshness viable for users who cannot dedicate floor space. India’s BIS IS 302 update extends to DC and battery-powered appliances up to 480 V, which clears a path for portable dispensers with integrated batteries that satisfy outdoor and events use cases without mains power. As buyers weigh portability, footprint and freshness, the product-type hierarchy splits between entry-level mini-keg convenience and rising countertop ecosystems that deliver a balance of volume and quality in compact spaces. This mix supports a broad funnel for the home draft beer dispensers industry, from first-time trial to premium-owned systems with closed-loop keg returns.

By Technology: IoT Connectivity Outpaces Legacy Refrigeration as Differentiation Shifts Digital

Direct-draw refrigeration held a 52.91% share of the home draft beer dispensers market size in 2025, given reliability, wide temperature ranges, and service familiarity, while smart IoT-enabled systems posted the fastest 7.20% growth pace as connectivity turned appliances into data and engagement platforms. CO₂-based systems remain standard for flexible pressure control from 5 to 15 PSI, with sealed-keg ecosystems like BLADE removing external tanks to simplify setup and reduce component count for users who prefer fewer touchpoints. Thermoelectric cooling attracts noise-sensitive applications with lower wattage draws, although performance can degrade at high ambient temperatures that exceed indoor cooling deltas during summers in many markets. Smart platforms such as iGulu’s BrewOS and GrowlerWerks’ app-enabled uKegs enable remote monitoring, recipe libraries, and integration with voice assistants, which sustains user engagement along the ownership journey. Regulatory momentum in India under BEE accelerates the move to low-GWP refrigerants while BIS requires updated electronic-circuit evaluations and software safety interlocks, which shape both thermal architectures and cybersecurity for connected devices.

As smart capabilities expand, replenishment nudges, predictive maintenance and keg-level alerts integrate with DTC ordering to streamline ownership for frequent users in the home draft beer dispensers market. Direct-draw remains a practical default in markets with strong service ecosystems, while sealed formats and thermoelectric units appeal to buyers willing to trade flexibility for simplicity or lower noise. EdgeStar’s Energy Star unit underscores how transparent power data supports lifecycle-cost decisions, especially where electricity tariffs increase the total cost of ownership over multi-year horizons. BIS’s software and telecom-interface provisions align with global expectations for safe and secure connected appliances, which is relevant as over-the-air updates become normal in premium dispensing ecosystems. This technology mix positions the home draft beer dispensers industry to serve both analog and app-centric households while connectivity drives the fastest incremental value.

By Capacity: Dual-Tap Configurations Balance Variety and Footprint Constraints

Single-tap systems below 5 liters captured 46.80% of the home draft beer dispensers market share in 2025 by addressing small apartments and first-time buyers, while dual-tap systems from 5 to 10 liters grew at 6.88% as households prioritize style variety without sacrificing space. Multi-tap units above 10 liters fit dedicated home bars and micro-venues but require larger footprints and heavier cabinetry, which narrows their buyer base to owners with permanent-space options. Portable single-tap formats like Klarstein’s 5-liter unit chill quickly from room temperature on compact power draws, which suits city flats with premium space constraints. Subscription ecosystems from PerfectDraft and brewer clubs that bundle two kegs per month reinforce dual-tap use cases as consumers rotate IPAs with lagers or seasonal specials. EdgeStar’s configuration flexibility to support either a single full-size keg or two sixth kegs allows households to scale serving capacity for events, then revert to lower-volume setups during routine weeks.

Capacity choices are shaped by housing-stock attributes such as ceiling height, kitchen layouts, and the presence of wet-bar alcoves in newer developments, which drive demand for compact dual-tap units over towering multi-tap towers in many urban markets. This pattern supports progressive upgrades within the home draft beer dispensers market as users trial single-tap formats then step up to dual-tap for variety once habits are established. Power efficiency and noise considerations factor into capacity decisions, and buyers compare operating costs as part of payback calculations tied to the frequency of entertaining and keg size. In markets with limited CO₂ refill density, sealed 8-liter kegs and smaller tanks favor lower-capacity systems that still deliver consistent carbonation and reduced maintenance. These variables yield a capacity ladder that helps the home draft beer dispensers industry appeal to casual and enthusiast users through practical trade-offs aligned with living space and beverage goals.

By Distribution Channel: Direct-to-Consumer Platforms Erode Specialty-Retail Incumbency

Specialty retailers held 64.24% of 2025 sales while online retail and DTC advanced at 8.65% CAGR as subscription bundles, return credits and digital merchandising reduced showroom friction in the home draft beer dispensers market. Mass merchandisers position entry models near undercounter refrigerators and wine coolers, which frames dispensers as part of premium kitchens and supports add-on installation services. Home-improvement stores capture renovation budgets and reinforce the built-in appliance view with adjacent SKU categories that cluster complementary purchases. AB InBev’s DTC network processed over 76 million orders and generated USD 550 million in FY25 within its consumer ecosystem, which validates how closed-loop logistics and credit incentives like £5 Beer Tokens can drive repeat orders at scale. In India, regulatory positions on low-alcohol delivery continue to evolve across states, and policy signals since 2024 suggest formalization efforts that would enable controlled home delivery where pilot programs are endorsed.

E-commerce-native brands benefit when BIS approvals are streamlined for battery-powered and DC-appliance certifications, which lowers time-to-market for localized compressor and refrigerant specifications. Specialty retailers still matter for on-floor demos of pour quality and for sizing advice, while online channels improve assortment breadth and deliver replenishment prompts that keep kegs rotating without store visits. As DTC data visibility expands, replenishment timing, style recommendations and promotional bundles align with past consumption, which increases attachment to specific ecosystems in the home draft beer dispensers market. Over time, return logistics and closed-loop credits can become differentiators that reduce breakage and improve keg-turn velocity for high-frequency households. This channel mix reflects enduring roles for both showrooms and digital storefronts as consumers balance in-person experience with delivery convenience and credit incentives.

Geography Analysis

Asia-Pacific is projected to grow at 7.96% through 2031, supported by India’s premiumization and rising consumer durable spending, which sustains household investment in compact, energy-efficient appliances linked to at-home experiences. Within India, large metros with higher disposable incomes and broader craft ecosystems attract early-adopting households and micro-venues able to manage CO₂ logistics and keg returns. Tier-II cities gain traction as newer residential projects add wet-bar alcoves and dedicated appliance spaces, which lowers installation hurdles for countertop systems. Seasonal temperature swings influence purchase timing in northern states where summer heat raises compressor duty cycles and power bills, which can shift buying to cooler months when the total cost of ownership falls. Coastal and southern regions with more stable climates exhibit smoother adoption patterns, as ambient temperatures are less punishing for small compressors.

North America held 36.61% of the home draft beer dispensers market size in 2025, supported by mature specialty retail, established CO₂ networks, and brewer-managed DTC platforms that streamline replenishment and returns. AB InBev’s FY25 disclosure highlighted strong beyond-beer growth led by Cutwater, which nudges dispenser makers to accommodate multiple beverage types since consumers split fridge space among beer, cocktails, and non-alcoholic options. Summit’s Floating Tap targets renters and condos wary of permanent countertop holes, which reflects housing churn and HOA rules that influence appliance choices in urban cores. In Europe, closed-loop return systems like PerfectDraft’s USD 5 token credit improve keg-turn velocity through a broad collection network, which deepens engagement and reduces logistics friction for repeat buyers. The Middle East and Africa show more gradual uptake due to alcohol policy constraints and patchy cold-chain infrastructure, although South Africa and Nigeria present opportunities for ruggedized units tuned for 220 V/50 Hz operation and intermittent power conditions.

Competitive Landscape

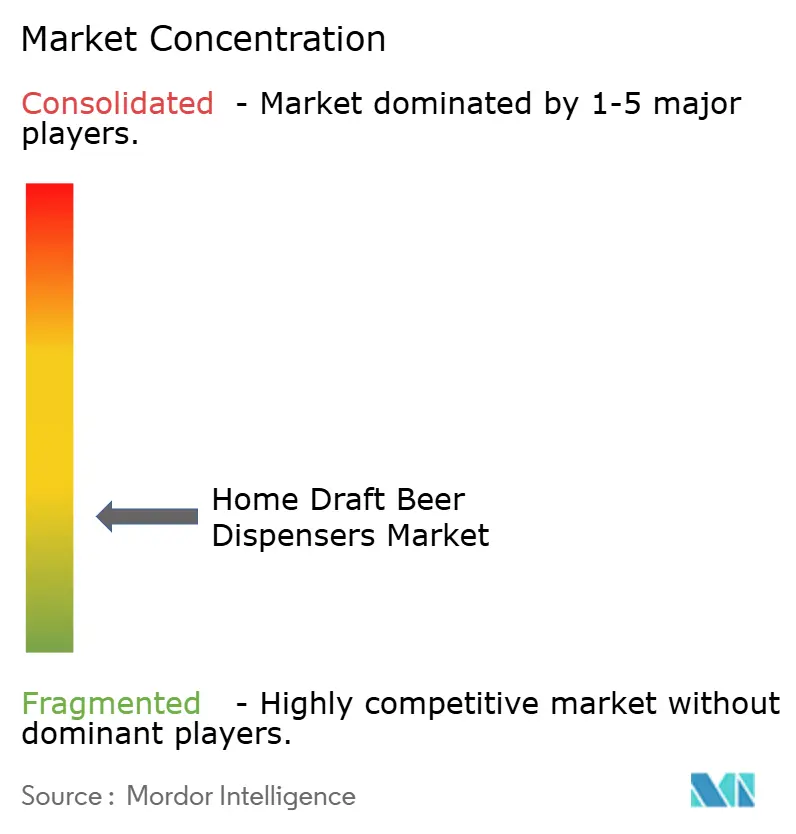

Global share remains fragmented with no single player above 15%, as appliance makers like Summit and EdgeStar compete with brewer-anchored ecosystems such as PerfectDraft and BLADE, alongside specialists including Micro Matic and emerging smart entrants like iGulu and GrowlerWerks. Appliance brands leverage shared manufacturing with other refrigeration lines to extend into kegerators, while brewer-backed models emphasize keg lock-in, return credits and data-driven replenishment that makes hardware a gateway to recurring beverage revenue. PerfectDraft’s FY25 results showcase how a DTC platform, return incentives and multi-brand portfolios can align with consumer demand cycles to sustain repeat orders. Summit’s Floating Tap solution differentiates on installation flexibility for rental-heavy markets, which unlocks households that avoided permanent modifications. Micro Matic’s compact FlexiDraft Countertop addresses small venues and home installs where glycol loops and fixed tap lines are not feasible, which broadens the served market for draft experiences.

Strategic moves over 2024 to 2026 reveal two playbooks. Ecosystem-led strategies use proprietary kegs, app telemetry and return logistics to shape loyalty and drive higher keg-turns in the home draft beer dispensers market. Hardware-led strategies focus on compact form factors, energy performance and configuration flexibility to fit evolving living spaces and cost-of-ownership expectations. iGulu’s BrewOS enables direct recipe libraries and fermentation control to add value beyond dispensing, which positions the unit as a multi-function countertop brewer-dispenser. GrowlerWerks adds app telemetry to pressure regulation and serving guidance, which expands brand touchpoints through mobile interactions and voice controls. These approaches reflect distinct margins and capabilities, yet both rely on reliability, hygiene simplicity and energy efficiency to sustain satisfaction and reviews.

Regulation remains a competitive factor in India and select Asia-Pacific markets. BIS certification under IS 302 and BEE’s refrigerant rules encourage early compliance integration in design and sourcing, which advantages established brands over opportunistic importers in the home draft beer dispensers market. Closed-loop return credits and broad collection networks in Europe enable brewer ecosystems to consolidate repeat buyers over time. Appliance players counter with broader retail reach and installation services that position kegerators alongside kitchen upgrades and outdoor entertaining plans. The result is a dynamic equilibrium where brands can win on ecosystem stickiness or on fit, finish and total cost of ownership, while consumers choose pathways based on living space, beverage variety and service expectations.

Home Draft Beer Dispensers Industry Leaders

PerfectDraft (AB InBev)

Kegco (Beverage Factory)

EdgeStar (Living Direct/NJ Trading)

Summit Appliance (Felix Storch)

U-Line

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: AB InBev reported full-year 2025 results revealing its direct-to-consumer ecosystem, including PerfectDraft home dispensers alongside Zé Delivery and TaDa Delivery platforms, generated USD 550 million in revenue, an 8% increase versus FY24, while processing over 76 million e-commerce orders and expanding its closed-loop keg-return program offering £5 Beer Tokens per returned unit across 650-plus Majestic stores and 14,000 Collect+ locations in the United Kingdom.

- May 2025: Kegco announced expansion into convenience retail at the National Restaurant Association Show, unveiling the V32ADA kegerator with ADA-compliant 31-inch cabinet height, the HK-46 mini kegerator optimized for Bag-in-Box beverages and a dual-temperature Kegerator Vending Machine for hot and cold drinks.

- May 2025: CLASP reported 18 appliance-efficiency policies in 2024 targeting 180 TWh savings and 146 megatons CO₂ avoidance by 2030 with revised refrigerator and fan standards effective January 1, 2026

- April 2025: Summit Appliance introduced a patent-pending Floating Tap kegerator series with standalone tap kits resting on countertops and connected via tubing, eliminating permanent modifications and enabling reversible conversion to standard refrigeration with included shelving.

Global Home Draft Beer Dispensers Market Report Scope

| Kegerators (Full-size) |

| Counter-top Draft Systems |

| Mini-keg Dispensers |

| Portable Tap Systems |

| Direct-draw Refrigeration |

| Pump / Pressurised CO₂ |

| Thermoelectric Cooling |

| Smart IoT-enabled Systems |

| Single Tap (<5 L) |

| Dual Tap (5–10 L) |

| Multi-Tap (>10 L) |

| Specialty Retailers |

| Online Retail / DTC |

| Mass Merchandisers |

| Home-Improvement Stores |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | Kegerators (Full-size) | |

| Counter-top Draft Systems | ||

| Mini-keg Dispensers | ||

| Portable Tap Systems | ||

| By Technology | Direct-draw Refrigeration | |

| Pump / Pressurised CO₂ | ||

| Thermoelectric Cooling | ||

| Smart IoT-enabled Systems | ||

| By Capacity | Single Tap (<5 L) | |

| Dual Tap (5–10 L) | ||

| Multi-Tap (>10 L) | ||

| By Distribution Channel | Specialty Retailers | |

| Online Retail / DTC | ||

| Mass Merchandisers | ||

| Home-Improvement Stores | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the projected growth rate for the home draft beer dispensers market through 2031?

The home draft beer dispensers market size is expected to increase from USD 126.36 million in 2025 to USD 132.12 million in 2026 and reach USD 181.19 million by 2031, growing at a CAGR of 6.52% over 2026-2031.

Which product type leads and which grows fastest within home draft beer dispensers?

Mini-keg dispensers led with a 65.23% share in 2025, while countertop draft systems are the fastest-growing at 7.01% CAGR between 2026 and 2031.

What technologies are most relevant to future differentiation in this space?

Direct-draw units held the largest share in 2025, but smart IoT-enabled systems post the fastest growth as connectivity adds logging, inventory and replenishment features

How are regulations in India affecting home draft beer dispensers?

BIS’s IS 302 (Part 1): 2024 and BEE policies tighten safety and efficiency, which favor compliant brands and accelerate low-GWP refrigerant adoption from January 1, 2026

What channel dynamics are reshaping how consumers buy home draft systems?

Specialty retail still anchors sales, but online retail and DTC show the fastest growth due to subscription bundles, return credits and app-based replenishment

Which region is expected to grow fastest in home draft beer dispensers by 2031?

Asia-Pacific is the fastest-growing region with a 7.96% CAGR to 2031, buoyed by premiumization and appliance upgrades in India and other key Asia-Pacific markets.

Page last updated on: