Underfill Dispenser Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 71.33 Billion |

| Market Size (2031) | USD 96.28 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Underfill Dispenser Market Analysis by Mordor Intelligence

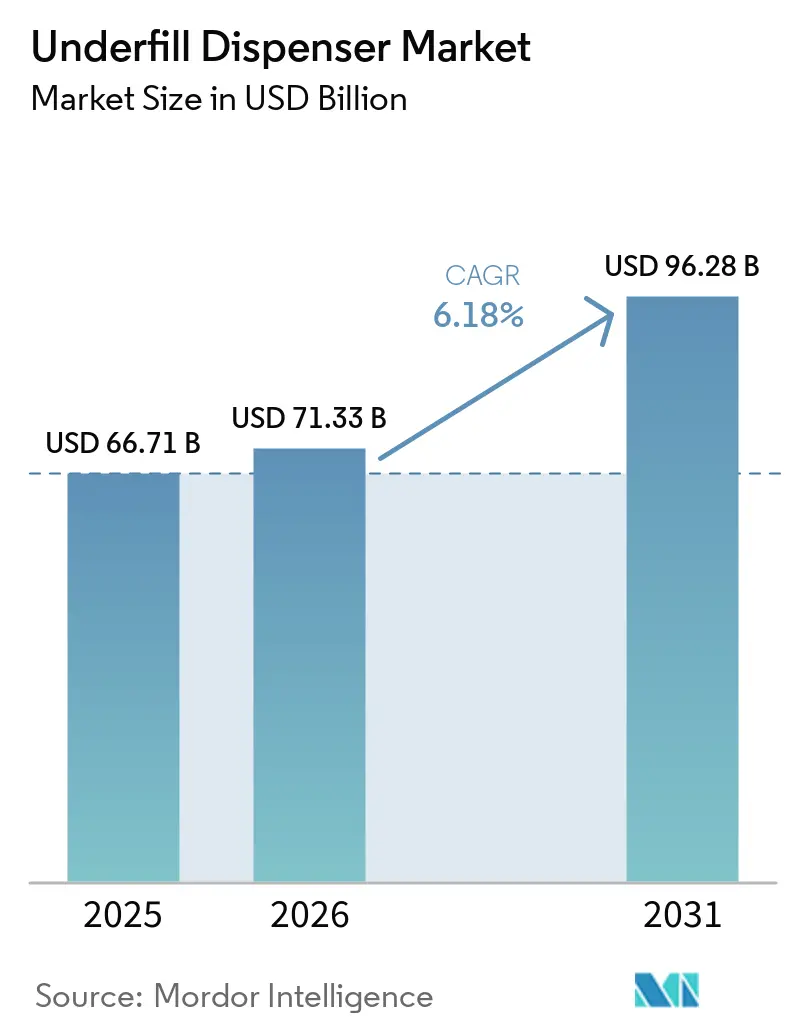

The underfill dispenser market size was valued at USD 66.71 billion in 2025 and estimated to grow from USD 71.33 billion in 2026 to reach USD 96.28 billion by 2031, at a CAGR of 6.18% during the forecast period (2026-2031). Heterogeneous integration is scaling quickly, and chiplet-based architectures now dominate the advanced-node roadmaps of leading foundries. Equipment builders are responding with piezoelectric jetting platforms that deposit sub-5-nanoliter volumes and maintain ±1 micrometer placement accuracy, features that help eliminate void formation in 3D-stacked packages. Materials suppliers have introduced silica-filled epoxy chemistries with glass transition temperatures above 200 °C to match the thermal budget of high-temperature logic and power devices, tightening the link between dispense hardware and chemistry development. Asia-Pacific continues to anchor demand as contract assembly houses expand capacity in Taiwan, South Korea, and mainland China, while new sovereign investment programs in the Middle East create fresh greenfield opportunities for the underfill dispenser market.

Key Report Takeaways

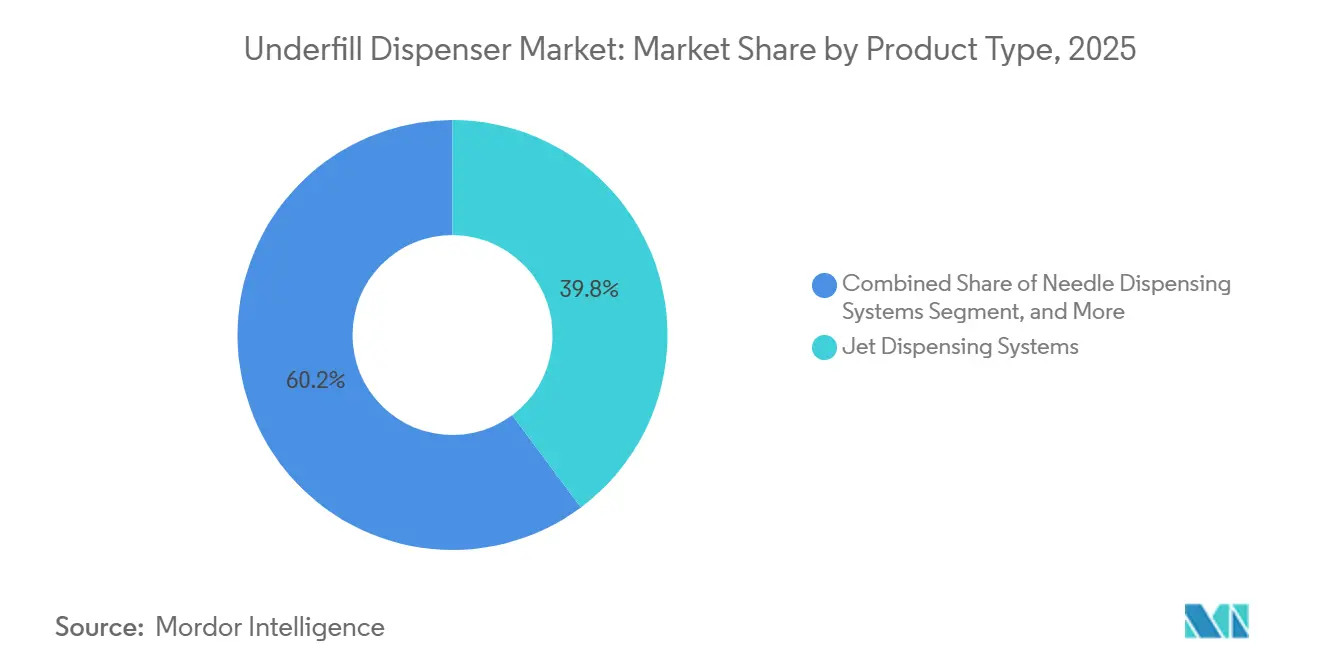

- By product type, jet dispensing systems accounted for 39.81% revenue of the underfill dispenser market share in 2025 and are projected to expand at a 6.77% CAGR through 2031.

- By technology, piezoelectric jetting led with 34.54% of the underfill dispenser market share in 2025, while the same segment records the fastest forecast CAGR at 6.94% to 2031.

- By application, flip chip packaging captured 30.22% of 2025 revenue, whereas photonics and optoelectronic packaging is advancing at a 6.83% CAGR during 2026-2031.

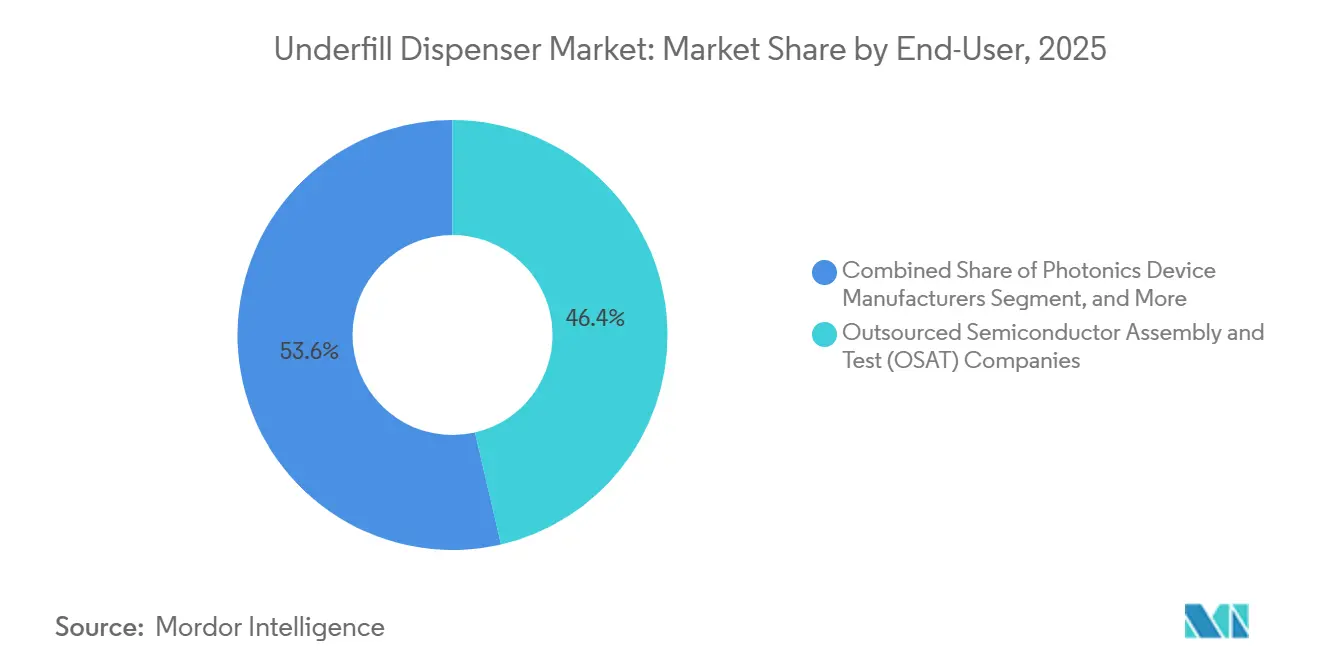

- By end-user, outsourced semiconductor assembly and test companies held 46.38% revenue share in 2025, yet photonics device manufacturers represent the fastest-growing cohort at a 6.88% CAGR through 2031.

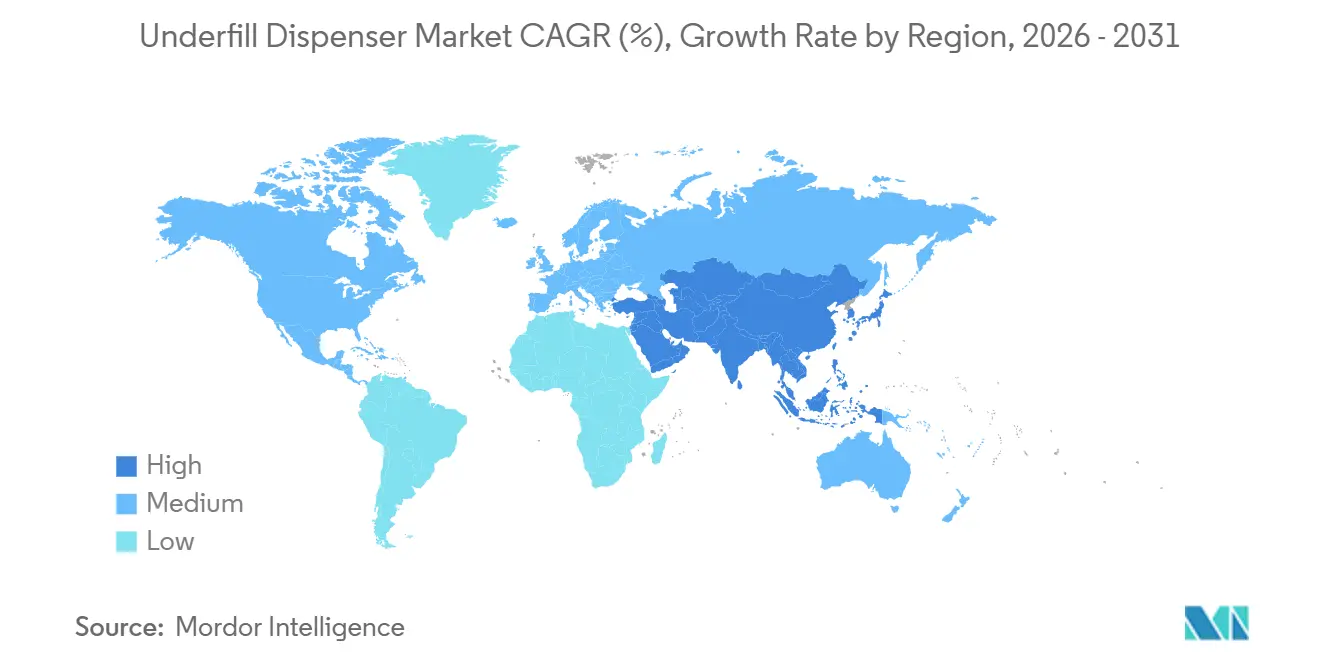

- By geography, Asia-Pacific dominated with 53.73% revenue share in 2025, while the Middle East is set to register the highest regional CAGR of 6.57% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Underfill Dispenser Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Optimized Dispense Path Planning Reduces Cycle Time | +1.2% | Global, early adoption in Taiwan, South Korea, Japan | Short term (≤ 2 years) |

| Adoption of High-Density Heterogeneous Integration Packages | +1.5% | North America and Asia-Pacific core, spillover to Middle East | Medium term (2-4 years) |

| Transition to 3D Chip-Stacking Demands Void-Free Underfill | +1.3% | Asia-Pacific core, North America advanced packaging hubs | Medium term (2-4 years) |

| Increasing Demand for Automotive-Grade Power Semiconductors | +0.9% | Europe and North America, China electric-vehicle influence | Long term (≥ 4 years) |

| Growth of Silicon Photonics and Co-Packaged Optics Assemblies | +0.8% | North America hyperscale data centers, Asia-Pacific contract manufacturers | Medium term (2-4 years) |

| Emergence of Chiplet-Based Substrates with Narrow Gap Spacing | +0.7% | Global, concentrated in Taiwan and United States advanced packaging sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Optimized Dispense Path Planning Reduces Cycle Time

Machine-learning algorithms embedded in vision systems now generate dispense trajectories that cut underfill cycle time by 15-25%, compared to rule-based programming, a capability that Coherix introduced in its 3D vision inspection systems deployed at TSMC's CoWoS packaging lines in 2025.[1]Coherix, “Predator3D Vision Inspection System,” coherix.com These models assess the topography, substrate warpage, and reflow temperature history, then adjust nozzle approach angles and pressure in real time. Major assembly houses deploying the technology report that recipe development time has fallen from 50 hours to less than 10, freeing engineering resources for new package qualifications. Reliability gains are notable in silicon carbide power modules, where non-Newtonian underfill chemistries demand pressure profiles that legacy rule-based controllers cannot sustain. Faster path planning also raises equipment utilization, a key metric, as capital costs for top-tier jetting systems exceed USD 1 million.

Adoption of High-Density Heterogeneous Integration Packages

Chiplet topologies permeate artificial-intelligence accelerators and high-performance CPUs, driving die-to-die bump pitch below 40 micrometers. Underfill materials must carry filler particles no larger than 2 micrometers to avoid bridging between solder joints, pushing dispensers to deliver 1-4 nanoliter dots with ±1 micrometer accuracy. Dual-valve jetting platforms now switch instantly between capillary-flow and molded underfill chemistries, reducing line changeover from 90 minutes to 15 minutes. Assembly houses handling multiple substrate layouts inside the same shift report throughput lifts of 20-25%, reinforcing the competitive case for precision jetting in the underfill dispenser market.

Transition to 3D Chip-Stacking Demands Void-Free Underfill

Vertical integration using through-silicon vias allows memory and logic arrays to co-locate in stacks that exceed 800 interconnects per square millimeter. Any void larger than 50 micrometers propagates delamination during thermal cycling, jeopardizing data links above 56 Gbps. New epoxy blends lower surface tension to 28 dyn/cm and maintain viscosity stability across 25-120 °C, cutting shrinkage void incidence below 2%. Dispensers equipped with closed-loop substrate heaters that track ±2 °C are therefore essential, and market demand is shifting toward equipment that embeds these controls natively instead of relying on external hot plates.

Increasing Demand for Automotive-Grade Power Semiconductors

Electric vehicles now favor silicon carbide devices rated beyond 900 V and 400 A, pushing underfill chemistries to survive 1,000 thermal cycles from -40 °C to 150 °C. Automotive qualification (AEC-Q100) caps permissible void levels at 0.2%, an order of magnitude tighter than consumer specifications. Dispensers must therefore accommodate high-viscosity molded underfills at 80 °C while preventing ionic contamination below 10 ppm. Stainless-steel fluid paths, PTFE seals, and automated solvent-purge routines are emerging as differentiators in bids issued by European and North American tier-one suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex of Advanced Jetting Platforms | -0.8% | Global, acute in Southeast Asia and Eastern Europe | Short term (≤ 2 years) |

| Limited Dispensing Throughput for Panel-Level Packaging Lines | -0.6% | Asia-Pacific pilot lines, North America R and D facilities | Medium term (2-4 years) |

| Shrinking Die Gaps Intensify Flux/Contamination Risk | -0.4% | Global advanced packaging sites | Long term (≥ 4 years) |

| Talent Shortage in Process Engineering for Wafer-Level Underfill | -0.3% | Europe and North America, emerging in Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex of Advanced Jetting Platforms

Next-generation piezoelectric jetting dispensers bundled with inline vision, dual-valve setups, and Class-100 enclosures command USD 800,000-1,200,000 per unit. Small and mid-size assembly houses that process legacy ball-grid-array packages at modest margins cannot absorb these costs without external financing. The semiconductor equipment industry's aggregate capital expenditure reached USD 200 billion in 2026, yet equipment utilization rates for underfill dispensers averaged 65-70% as assembly lines cycled between flip chip, ball grid array, and wafer-level packaging processes that require different dispense recipes and material changeovers consuming 2-4 hours per transition.[2]SEMI, “Semiconductor Equipment Capex Reaches USD 200 Billion in 2026,” semi.org The ROI equation becomes more challenging when line utilization averages 65-70%, since crews change recipes several times per shift. Consequently, many second-tier providers still opt for pneumatic needle dispensers priced below USD 250,000, even though those tools cannot meet void targets for automotive or aerospace programs.

Limited Dispensing Throughput for Panel-Level Packaging Lines

Fan-out panel-level packaging employs 310 mm × 310 mm substrates that carry 3-5 times more die than strip formats. Yet dispenser gantries longer than 400 mm experience resonance, forcing speed reductions to preserve ±5 micrometer accuracy, capping output at around 300 panels per hour. Early production ramps in Taiwan recorded rework rates above 8% due to substrate warpage exceeding 200 micrometers, distorting programmed dispense coordinates. Multi-head spider-style platforms now split a panel into four quadrants, each served by a dedicated dispense module, but the architecture remains costly and is adopted mainly by pilot lines focused on flip chip and heterogeneous integration trials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Jetting Systems Gain Precision Advantage

Jet dispensers accounted for the largest share of 2025 revenue, and the underfill dispenser market for jet platforms is forecast to grow at a 6.77% CAGR over 2026-2031. Their non-contact operation eliminates substrate scratches and allows sub-5-nanoliter dots, attributes crucial for chiplets separated by 25 micrometers or less. Hybrid machines that combine capillary-flow and jetting heads in a single frame now cut floor space by 40% and help factories consolidate multiple legacy processes onto a single line.

Needle systems still dominate high-viscosity encapsulants above 50,000 cP, but interest is waning as material suppliers reformulate chemistries to match the shear profiles of piezoelectric ejectors. Cost sensitivity keeps capillary-flow dispensers relevant in consumer electronics, where 3-5% void levels remain acceptable. Even so, AI-driven path planning lifts utilization for jetting platforms to nearly 80%, narrowing the total cost of ownership gap. As a result, the underfill dispenser market is seeing procurement budgets tilt decisively toward jet systems at both multinational and regional OSATs.

By Technology: Piezoelectric Jetting Extends Lead

Piezoelectric jetting captured 34.54% of the revenue share in 2025, and its share of the underfill dispenser market is on track to widen, with a 6.94% CAGR projection. Printheads packing more than 1,500 nozzles now fire at 20 kHz, pushing hourly dot counts beyond 90,000 while holding ±2 micrometer positional tolerance.[3]Kyocera Corporation, “1,584-Nozzle Piezoelectric Printhead,” kyocera.co.jp Pneumatic needle tools keep a share in Southeast Asian lines running 0.5 mm-pitch BGAs, but every major advanced-package roadmap specifies piezoelectric capability for die gaps below 20 micrometers.

Positive-displacement pumps and auger screws fill a niche for wafer-level packaging that requires sustained flow above 10 mL/min, volumes outside the comfort zone of piezo stacks. Film transfer has gained a foothold among ultra-thin MEMS modules under 200 μm tall, yet the lack of broad chemical support limits growth today. Overall, expanded machine vision integration and real-time dispense verification consolidate piezoelectric technology's leadership across mainstream heterogeneous integration programs in the underfill dispenser market.

By Application: Photonics Packaging Ramps Fastest

Flip chip accounted for 30.22% of 2025 revenue, as GPU and CPU die continue to demand void-free encapsulation for power-dense cores larger than 800 mm². This growth is driven by the increasing adoption of advanced semiconductor technologies, which require precise underfill solutions to ensure reliability and performance. However, photonics and optoelectronic assemblies are set to outpace all other uses with a 6.83% CAGR. The rising demand for hyperscale data centers, driven by the need for faster data processing and transmission, is pushing operators to migrate to co-packaged optics. These optics require underfill materials specifically designed to match glass interposers and silicon photonics die, specifications that traditional capillary-flow processes cannot meet effectively.

Ball-grid-array work remains a volume cushion for pneumatic dispensers, providing a steady demand for conventional underfill solutions. However, the underfill dispenser market is rapidly shifting its focus toward smaller, higher-margin photonics modules that rely on premium jetting equipment for precise application. Additionally, wafer-level packaging is gaining significant relevance as foundries increasingly adopt flow-under-mold sequences. These sequences allow packages to be singulated only after underfill curing, reducing test time and minimizing the risk of die-handling errors, thereby improving overall efficiency and yield in the manufacturing process.

By End-User: Photonics Manufacturers Accelerate

OSATs delivered 46.38% of 2025 revenue and remain anchor customers because fabless chip vendors continue to partner on backend innovation. Outsourced Semiconductor Assembly and Test (OSAT) companies play a critical role in the underfill dispenser market by providing advanced packaging solutions that meet the evolving needs of fabless semiconductor companies. These partnerships are essential for driving backend innovation, ensuring that the latest chip designs are efficiently packaged and tested. Even so, photonics device makers log the fastest 6.88% CAGR, leveraging glass-compatible underfills to integrate lasers and detectors right next to switch ASICs. The rapid growth in photonics device manufacturing is driven by the increasing demand for high-speed data transmission and advanced optical communication systems. Integrated device manufacturers deepen in-house capabilities to tighten IP control, exemplified by USD 12.9 billion committed for a new South Korean HBM packaging hub. This significant investment highlights the strategic importance of high-bandwidth memory (HBM) packaging in supporting next-generation computing and AI applications.

Foundries expanding CoWoS and fan-out lines add incremental pull, while electronics manufacturing services providers deploy dispensers to meet IPC-A-610 Class 3 void thresholds for automotive control units. The expansion of Chip-on-Wafer-on-Substrate (CoWoS) and fan-out packaging lines by foundries reflects the growing demand for advanced packaging technologies that enhance performance and reduce form factors. Electronics manufacturing services providers are also increasingly adopting underfill dispensers to meet stringent quality standards, such as IPC-A-610 Class 3 void thresholds, which are critical for ensuring the reliability of automotive control units. Research institutions and pilot fabs round out demand with cryogenic quantum packages and wafer-level prototypes, collectively keeping utilization high across a widening user base in the underfill dispenser market. These institutions and pilot fabs contribute to the market by driving innovation and testing new packaging technologies, such as cryogenic quantum packages and wafer-level prototypes, which are essential for advancing semiconductor manufacturing processes.

By Dispensing Volume Range: Sub-5 Nanoliter Dots Move Mainstream

Sub-5-nanoliter patterns continue to represent a smaller portion of total shots; however, they are the fastest-growing segment as chiplet gaps shrink below 30 micrometers. This high-precision subsegment of the underfill dispenser market is predominantly served by piezoelectric jets, which can fire droplets in the 1-4 nanoliter range. The 5-30 nanoliter range still holds the majority share because mainstream flip chip designs can accommodate slightly wider gaps. This allows for a practical balance between throughput and accuracy, making it a preferred choice for many applications.

Dispensing volumes above 30 nanoliters remain relevant for power modules and older BGA (Ball Grid Array) designs, where achieving complete coverage takes precedence over precise placement. However, as each new generation of HBM (High Bandwidth Memory) or AI accelerators emerges, packaging engineers are increasingly driven toward smaller droplet sizes to meet the demands of advanced designs. Equipment suppliers are responding to this trend by introducing roadmaps that aim to achieve stable ejection volumes as low as 0.5-1 nanoliter by 2028, signaling a significant advancement in dispensing technology.

Geography Analysis

Asia-Pacific generated 53.73% of 2025 revenue, anchored by Taiwan’s cluster of advanced packaging plants that together consume more than 500 high-precision dispensers. South Korea added momentum in 2026 as a USD 12.9 billion HBM complex broke ground, underwriting orders for at least 40 top-tier jetting tools. Mainland China’s 2.5D initiatives, driven by domestic GPU startups, lifted local demand by double digits even as export controls constrained EUV wafer capacity. Japan remains steady but leans on domestic suppliers that deliver incremental upgrades favored by automotive customers with conservative qualification schedules.

The Middle East is poised for a 6.57% CAGR and is the fastest regional climber. Sovereign wealth funds back multiple fabs in the United Arab Emirates and Saudi Arabia, including a USD 16 billion logic line bundled with chiplet assembly capability. Regional policy targets 50 homegrown semiconductor firms by 2028, and procurement documents already specify narrow-gap underfill dispensers matching those used in Taiwan.

North America and Europe progress at mid-single-digit rates as CHIPS Act incentives subsidize domestic packaging but struggle with engineering talent shortages. Pilot lines in Arizona and Saxony have installed precision jetters yet report extended operator-training times because only a few hundred engineers worldwide specialize in wafer-level underfill. South America and Africa remain nascent, although Brazilian automotive suppliers have begun qualifying void-free encapsulants for flex-fuel controllers, hinting at future uptick in regional orders for the underfill dispenser market.

Competitive Landscape

The underfill dispenser market exhibits moderate concentration, with the top three suppliers, Nordson, Musashi Engineering, and Mycronic, collectively commanding roughly 45-50% revenue in 2025. Nordson’s IntelliJet and PICO Pulse XP lines dominate sub-5 nL deployments, offering ±1 μm accuracy that rivals cannot yet match in high-volume production.[4]Nordson Corporation, “IntelliJet Dispensing System,” nordson.com Mycronic’s BA 01 ejector, launched in late 2025, is tuned for 1-4 nL dots at 20 kHz and has already secured design wins in leading chiplet assemblies slated for 2026 ramp. Musashi maintains leadership in Japan thanks to robust local service, a differentiator prized by automotive Tier-1s.

Chinese entrants such as Shenzhen Second Intelligent Equipment supply pneumatic dispensers priced 30-40% below imported gear, expanding share among second-tier OSATs focused on consumer BGAs. European providers concentrate on spider-type multi-head architectures tailored for panel-level pilot lines. Materials vendors have started bundling process recipes with equipment qualification, creating a quasi-ecosystem lock-in that raises switching costs for assembly houses.

Technology leadership is shifting toward integrated machine vision and AI-driven path optimization. Dispensers now ship with embedded 3D profilers that build real-time height maps and adjust jet parameters to eliminate voids and compensate for substrate warpage. Suppliers capable of fusing software analytics with hardware reliability are therefore best positioned to capture incremental share as the underfill dispenser market moves deeper into heterogeneous integration.

Underfill Dispenser Industry Leaders

Nordson Corporation

Musashi Engineering, Inc.

Henkel AG & Co. KGaA

Illinois Tool Works Inc. (Camalot Systems)

Mycronic AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Nordson showcased its Vantage cleanroom jetting platform at SEMICON China, highlighting a dual-valve changeover that trims downtime from 90 minutes to 15 minutes.

- March 2026: Mycronic debuted the MYD10 and MYD50 in-line dispensers, bringing tool-free transitions between capillary-flow and molded underfill chemistries to high-mix production.

- March 2026: Henkel presented glass-compatible underfill formulations at METPACK 2026, targeting silicon photonics assemblies scheduled for data-center deployment in 2027.

- January 2026: Henkel consolidated Asia-Pacific packaging materials R and D into a new Singapore Science Park facility focused on chiplet and 3D-IC underfills.

Global Underfill Dispenser Market Report Scope

The underfill dispenser market is the global industry focused on the development, manufacturing, and deployment of precision dispensing systems for applying underfill materials in semiconductor packaging processes. Underfill dispensers play a critical role in enhancing the mechanical strength, thermal stability, and reliability of microelectronic assemblies by filling gaps between chips and substrates, particularly in advanced packaging technologies where miniaturization and performance demands are high.

The Underfill Dispenser Market Report is Segmented by Product Type (Capillary Flow, Jet Dispensing System, Combination/Hybrid Systems, and Needle Dispensing Systems), Technology (Piezoelectric Jetting, Pneumatic Needle, Auger Screw, Positive Displacement Pump, and Film Transfer Systems), Application (Flip Chip Packaging, Ball Grid Array (BGA) Packaging, Wafer Level Packaging (WLP), MEMS and Sensor Packaging, Photonics and Optoelectronic Packaging, and Power Semiconductor Packaging), End-User (Outsourced Semiconductor Assembly and Test (OSAT) Companies, Integrated Device Manufacturers (IDMs), Foundries, Electronics Manufacturing Services (EMS) Providers, Photonics Device Manufacturers, and Research and Development Institutions / Labs), Dispensing Volume Range (<5 Nanolitres, 5–30 Nanolitres, and >30 Nanolitres), and Geography(North America, Europe, Asia-Pacific, Middle East, Africa, and South Africa). The Market Forecasts are Provided in Value (USD).

| Capillary Flow Underfill Dispensers |

| Jet Dispensing Systems |

| Combination / Hybrid Systems |

| Needle Dispensing Systems |

| Piezoelectric Jetting |

| Pneumatic Needle |

| Auger Screw |

| Positive Displacement Pump |

| Film Transfer Systems |

| Flip Chip Packaging |

| Ball Grid Array (BGA) Packaging |

| Wafer Level Packaging (WLP) |

| MEMS and Sensor Packaging |

| Photonics and Optoelectronic Packaging |

| Power Semiconductor Packaging |

| Outsourced Semiconductor Assembly and Test (OSAT) Companies |

| Integrated Device Manufacturers (IDMs) |

| Foundries |

| Electronics Manufacturing Services (EMS) Providers |

| Photonics Device Manufacturers |

| Research and Development Institutions / Labs |

| Less than 5 Nanolitres |

| 5–30 Nanolitres |

| More than 30 Nanolitres |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Capillary Flow Underfill Dispensers | |

| Jet Dispensing Systems | ||

| Combination / Hybrid Systems | ||

| Needle Dispensing Systems | ||

| By Technology | Piezoelectric Jetting | |

| Pneumatic Needle | ||

| Auger Screw | ||

| Positive Displacement Pump | ||

| Film Transfer Systems | ||

| By Application | Flip Chip Packaging | |

| Ball Grid Array (BGA) Packaging | ||

| Wafer Level Packaging (WLP) | ||

| MEMS and Sensor Packaging | ||

| Photonics and Optoelectronic Packaging | ||

| Power Semiconductor Packaging | ||

| By End-User | Outsourced Semiconductor Assembly and Test (OSAT) Companies | |

| Integrated Device Manufacturers (IDMs) | ||

| Foundries | ||

| Electronics Manufacturing Services (EMS) Providers | ||

| Photonics Device Manufacturers | ||

| Research and Development Institutions / Labs | ||

| By Dispensing Volume Range | Less than 5 Nanolitres | |

| 5–30 Nanolitres | ||

| More than 30 Nanolitres | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the underfill dispenser market by 2031?

The underfill dispenser market size is forecast to reach USD 96.28 billion by 2031, growing at a 6.18% CAGR between 2026 and 2031

Which product type holds the largest revenue share today?

Jet dispensing systems led with 39.81% of 2025 revenue, reflecting strong adoption for high-precision chiplet and 3D-stacked packages

Which technology segment is expanding the fastest?

Piezoelectric jetting is projected to post the highest 6.94% CAGR during 2026-2031 as die gaps shrink below 20 micrometers

Which end-user group is growing the quickest?

Photonics device manufacturers are slated for a 6.88% CAGR through 2031 as data-center operators shift to co-packaged optics

Which region will record the highest growth rate?

The Middle East is expected to advance at a 6.57% CAGR, supported by sovereign investments in new chiplet assembly facilities

What is the key barrier limiting wider adoption of advanced jetting systems?

High capital expenditure, often exceeding USD 1 million per tool, remains the main hurdle for smaller assembly houses seeking precision jetting capability.

Page last updated on: