Holter Monitor Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

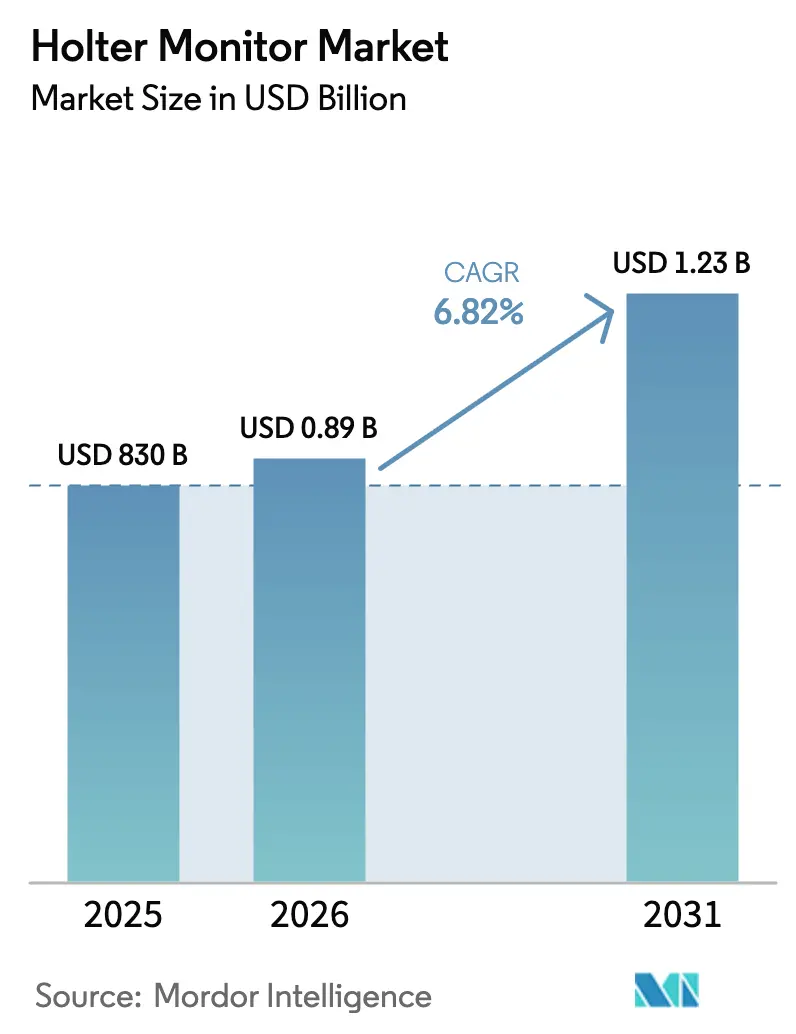

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.23 Billion |

| Growth Rate (2026 - 2031) | 6.82% CAGR |

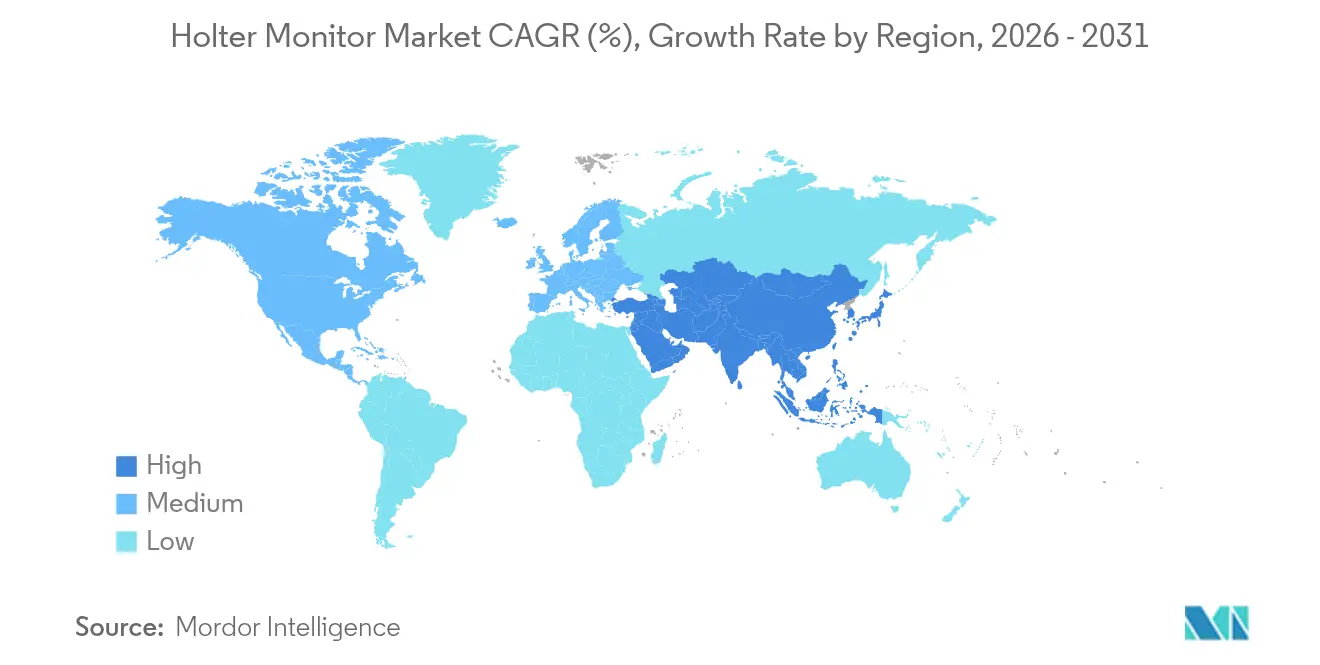

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

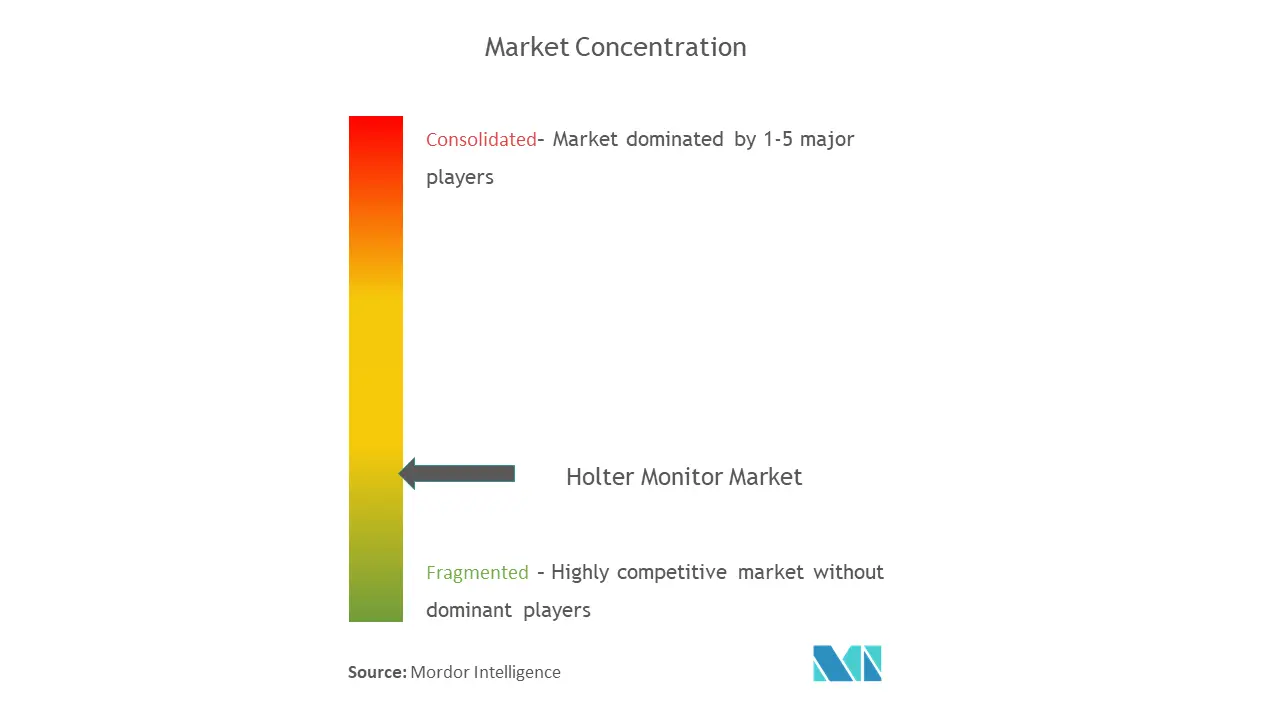

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Holter Monitor Market Analysis by Mordor Intelligence

The Holter monitor market size is expected to grow from USD 830 million in 2025 to USD 886.6 million in 2026 and is forecast to reach USD 1,233.37 million by 2031 at 6.82% CAGR over 2026-2031. Industry momentum stems from a broad reimbursement reset, fresh Current Procedural Terminology codes that simplify billing, and stronger Medicare coverage for artificial-intelligence (AI)–enabled rhythm assessment tools. Provider demand for faster electrocardiogram (ECG) interpretation is accelerating as algorithms cut reading times from hours to minutes, while single-use patch designs reduce infection risk and improve patient comfort. Hospitals continue to drive revenue, yet home-based monitoring programs are scaling quickly, supported by value-based care incentives and the demonstrated cost savings from preventing readmissions through continuous surveillance. Competitive intensity is rising as incumbents and start-ups deliver devices that integrate cloud connectivity, machine learning, and energy-harvesting technologies, narrowing the performance gap between short-term wearable patches and longer-term implantable loop recorders.

Key Report Takeaways

- By product type, patch-based devices led with 37.05% of Holter monitor market share in 2025; implantable loop recorders are poised to expand at a 6.98% CAGR through 2031.

- By end user, hospitals held 44.35% share of the Holter monitor market in 2025, while home healthcare is projected to advance at a 7.38% CAGR to 2031.

- By geography, North America accounted for 35.25% of the Holter monitor market in 2025, whereas Asia-Pacific is forecast to register an 8.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Holter Monitor Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement expansion for remote cardiac monitoring | +1.8% | Global, with early adoption in North America & EU | Short term (≤ 2 years) |

| Rising prevalence of atrial fibrillation & cardiac arrhythmias | +1.2% | Global, concentrated in aging populations | Long term (≥ 4 years) |

| Growing adoption of ambulatory ECG in primary care settings | +0.9% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| AI-powered auto-diagnostic algorithms cut reading time | +0.8% | Global, led by developed markets | Short term (≤ 2 years) |

| Shift toward single-use patch Holters in infection-control protocols | +0.6% | Global, accelerated in hospital settings | Short term (≤ 2 years) |

| Insurance incentives for post-ablation long-term rhythm tracking | +0.4% | North America & EU primarily | Medium term (2-4 years |

| Source: Mordor Intelligence | |||

Reimbursement expansion for remote cardiac monitoring

Broader payer recognition of AI-enabled diagnostics is reshaping financial outcomes for providers. Medicare’s 2025 Outpatient Prospective Payment System added explicit coverage for algorithm-enhanced ambulatory ECG analysis, prompting commercial insurers to follow suit[1]Source: Centers for Medicare & Medicaid Services, “Local Coverage Determination 39840,” cms.gov . Physicians can now code extended monitoring sessions with AI decision support and receive parity payments that rival more expensive in-office procedures. Smaller clinics, previously priced out of continuous rhythm surveillance, are bringing services in-house to retain revenue. A direct consequence is higher penetration of Holter monitor market contracts with primary-care networks that historically referred patients to external diagnostic centers. Post-ablation reimbursement bonuses further encourage 90-day rhythm tracking, creating predictable demand cycles. The new payment environment tightens the feedback loop between early arrhythmia detection and reimbursement, driving sustained device adoption.

AI-powered auto-diagnostic algorithms cut reading time

Software classified as Software-as-a-Medical-Device is now identifying atrial fibrillation, hypertrophic cardiomyopathy, and low ejection fraction with accuracy above 90%. Algorithms compress a day of manual review into minutes, freeing cardiologists for higher-value interventions. iRhythm’s cloud platform automatically triages anomalous beats, pushing only actionable events to clinicians, while Medtronic’s AI suite integrates with electronic health records to suggest guideline-directed therapy. Early adopters report 25–30% productivity gains within six months, reducing backlog and accelerating billing cycles. Although algorithm validation still varies across demographic cohorts, ongoing FDA clearances signal growing regulatory confidence. As hospital groups standardize on predictive analytics, procurement departments cite quantifiable labor savings when negotiating multi-year Holter monitor market contracts.

Growing adoption of ambulatory ECG in primary care settings

Extended monitoring protocols, once reserved for specialty cardiology, are moving into family-practice workflows. Evidence shows 14-day recordings uncover intermittent arrhythmias missed by 24-hour studies, prompting guideline revisions that recommend longer wear periods. Electronic health record integrations—such as the iRhythm–Epic connector—automatically flag high-risk episodes and populate structured notes, removing transcription overhead hitconsultant.net. Primary-care adoption democratises access, particularly in rural areas where cardiologist density is low. The result is a flatter referral pyramid, with Holter monitor market devices dispatched directly to patients’ homes from central warehouses. Continuous data streams also support population-health contracts, enabling pay-for-performance metrics tied to reduced stroke incidence.

Shift toward single-use patch Holters in infection-control protocols

COVID-19 era sterilization standards pushed hospitals to retire multi-patient cables in favor of disposable patches. Current patch platforms employ hypoallergenic adhesives and ultra-thin batteries, achieving 72-hour to 14-day wear without skin lesions. Wireless Bluetooth links eliminate tethered leads, allowing patients to shower and exercise while recording. Comparative trials confirm diagnostic equivalence with higher patient satisfaction and lower device return rates. Environmental concerns are addressed by biodegradable substrates that degrade within six months of disposal. Hospitals that switched entirely to single-use patches reported double-digit declines in nosocomial infection audits, reinforcing procurement preference. The resulting volume contracts reinforce component supply chains, making the disposable segment a resilient pillar of the Holter monitor market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of trained cardiac technicians for Holter data analysis | -0.8% | Global, acute in developed markets | Long term (≥ 4 years) |

| Data-privacy & cybersecurity compliance costs | -0.5% | Global, stringent in EU & North America | Medium term (2-4 years) |

| Limited battery life in ultra-compact devices hampers long-term monitoring | -0.6% | Global, affecting all device categories | Medium term (2-4 years) |

| Reimbursement exclusion of asymptomatic screening in several countries | -0.4% | APAC, MEA, and select European markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of trained cardiac technicians for Holter data analysis

Global cardiology staffing gaps are widening as retirements outpace new entrants, leaving many hospitals unable to manage surging ECG volumes. Burnout rates exceed 40%, and training pipelines lag because fellowship programs limit intake. Rural networks routinely outsource reads, adding two-day delays and higher fees. AI triage reduces workload, yet regulations still require human over-read, locking in demand for certified technicians. In the Holter monitor market, under-resourced centers defer equipment upgrades, slowing penetration of advanced recorders. Public-private partnerships that subsidize certification programs show promise, but capacity relief is unlikely before 2029.

Limited battery life in ultra-compact devices hampers long-term monitoring

While implantable loop recorders now promise six-year longevity, sub-cutaneous patches and miniaturized wearables still face power density trade-offs. Every millimeter shaved from thickness reduces battery capacity, capping recording sessions or requiring frequent recharge cycles. Medtronic’s Micra AV2 extends pacemaker life by 40%, yet broader adoption awaits supporting reimbursement for longer follow-up [2]Source: Medtronic, “Micra Leadless Pacing Systems Receive CE Mark,” medtronic.com . Academic prototypes that harvest mechanical energy from heartbeats or use light-powered circuits signal a future without lithium cells, but regulatory pathways remain untested. Until alternative energy scales, battery constraints will curb the upper boundary of continuous capture, limiting certain long-term clinical studies within the Holter monitor market

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Patch-based devices extend clinical reach

Patch platforms captured 37.05% of Holter monitor market share in 2025 as their walk-and-forget form factor improved adherence across all age groups. Implantable loop recorders posted a 6.98% CAGR, fueled by algorithmic upgrades that enable remote reprogramming and threshold adjustment without office visits. Traditional 3-lead recorders remain popular in price-sensitive procurement rounds, especially in emerging markets where reimbursement levels are modest. Twelve-lead Holter monitor systems, though niche, retain value in ischemia evaluation for complex cases requiring vector information beyond arrhythmia detection. Wireless clip-on sensors now integrate cloud APIs that deliver raw ECG files in FHIR-compatible formats, allowing analytics vendors to overlay predictive models as a service. High-quality audio channel correlation is being explored to discriminate cough-induced artefacts from true premature beats, elevating diagnostic yield. Component miniaturization has freed space for temperature and motion sensors, creating multiparameter datasets that appeal to pharmaceutical trial sponsors. These shifts collectively underpin the long-run competitiveness of patch solutions, anchoring them as the spiritual center of the Holter monitor market.

The cumulative benefits translate into tangible productivity gains. iRhythm’s Zio patch raised arrhythmia detection to 80.9% in the AVALON registry, yet lowered skin-irritation complaints by two-thirds, a dual metric that resonates with purchasing committees. Abbott’s six-year insertable monitor establishes the feasibility of decade-long surveillance protocols, enabling stroke prevention strategies previously hindered by battery constraints. Rapid prototyping, powered by printed flexible circuits, reduces the design-to-trial cycle, letting manufacturers respond to emerging reimbursement triggers almost in real time. Consequently, the Holter monitor market sees faster refresh rates, with flagship lines updated biennially instead of the historical four-year cadence.

By End User: Home healthcare moves center stage

Hospitals held 44.35% of 2025 revenue, but patient-centric care pathways are unlocking a parallel distribution channel defined by mail-order fulfillment, web dashboards, and nurse triage hubs. Home-based monitoring is projected to post 7.38% CAGR, underpinned by Medicare’s Remote Physiologic Monitoring codes that reimburse device setup, education, and thirty-day data review. Value propositions extend beyond convenience; health systems deploying home ECG patches report 18% lower all-cause readmissions in heart-failure cohorts. Ambulatory surgical centers tap Holter devices mainly for 72-hour post-procedural monitoring, a workflow that de-risks same-day discharge. Diagnostic laboratories remain relevant for complex arrhythmia work-ups requiring multi-lead correlation or tilt-table integration.

Remote patient monitoring platforms now serve nearly 50 million Americans, and cardiology commands 21% of that base intuitionlabs.ai. Integration of wireless blood pressure and weight scales with ECG uploads feeds machine-learning models that forecast decompensation days ahead. Device makers tailor subscription bundles that include hardware, portal access, and third-party notification services, aligning with capitated payment contracts. User-friendly adhesive formulations and silent haptic alerts optimize adherence among older adults. The evolving service mix pushes the Holter monitor market toward recurring revenue models, in turn attracting venture capital eager for SaaS-like multiples.

Geography Analysis

North America generated 35.25% of 2025 revenue thanks to a mature reimbursement grid, high EHR penetration, and early access to FDA-cleared AI algorithms. Hospital groups establish preferred-vendor panels, often bundling ECG hardware with cloud analytics and workforce training. Regional payers, seeking value-based savings, now subsidize 90-day monitoring for atrial fibrillation post-ablation, positioning the Holter monitor market as a frontline prevention tool against stroke.

Europe maintains double-digit share as the Medical Device Regulation’s centralized review streamlines cross-border approvals. National health services in the Nordics pilot AI-supported triage lines that direct rhythm data to virtual cardiologists, allowing same-day anticoagulation starts. Meanwhile, iRhythm’s 2024 launch in Austria, Netherlands, Switzerland, and Spain underscores momentum in continental adoption.

Asia-Pacific, advancing at 8.55% CAGR, is propelled by large-scale digitization drives and aging demographics. China’s 25% jump in medical-device registrations signals regulatory openness to imported and domestic monitors. Japan prepares demonstration zones for remote monitoring ahead of the 2025 World Expo Osaka, leveraging 5G infrastructure for continuous data streaming. India’s Tier-2 cities form public-private cardiology hubs that bundle patch rentals with teleconsultations. Growth prospects in South America and the Middle East remain tempered by reimbursement heterogeneity, device import tariffs, and uneven internet coverage, yet pilot programs funded by multilateral banks hint at upside potential. These regional nuances collectively shape procurement priorities and guide go-to-market tactics within the Holter monitor market.

Competitive Landscape

The Holter monitor market exhibits moderate fragmentation with traditional conglomerates—Medtronic, Philips, and GE—provide full cardiac portfolios, cross-selling monitors alongside imaging and cath-lab equipment. Pure-play specialists such as iRhythm hone algorithmic leadership, reporting 20.3% year-on-year revenue growth in Q1 2025 to USD 158.7 million. Strategic acquisitions typify market behavior; BD’s USD 4.2 billion purchase of Edwards Lifesciences’ Critical Care unit adds hemodynamic data streams to its connected-care platform, strengthening cross-sell synergies in ICU and step-down wards.

Industry rivalry now centers on software differentiation. AI firms license algorithms that detect decompensation risk within 30-second ECG snippets, turning commoditized hardware into subscription services. Consumer-electronics entrants leverage smartwatch ecosystems, sparking debates about clinical-grade accuracy versus wellness metrics. Component innovation drives next-generation devices; light-powered pacemakers and heartbeat energy harvesters promise battery-free operation within ten years. Vendors piloting biodegradable patches position sustainability as a procurement criterion, anticipating institutional carbon-reduction mandates.

Pricing pressure remains contained because devices embed proprietary analytics subject to regulatory clearance, limiting generic substitution. However, cloud-native challengers apply software margins to undercut hardware-centric incumbents, creating tiered offerings—premium AI analytics, mid-range standard patches, and entry-level basic recorders. As payers tie reimbursement to diagnostic yield benchmarks, algorithm-accuracy league tables are emerging, prompting public validation studies. Collectively, these dynamics forge a competitive environment defined by speed of innovation and breadth of digital services, rather than unit cost alone, reinforcing persistent evolution within the Holter monitor market.

Holter Monitor Industry Leaders

Nihon Kohden

Medtronic

ScottCare Corporation,

Nasiff Associates, Inc

GE HealthCare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BD completed acquisition of Edwards Lifesciences’ Critical Care product group for USD 4.2 billion, adding hemodynamic monitoring capabilities used in more than 10,000 hospitals worldwide.

- May 2025: FDA approved Element Science’s Jewel Patch Wearable Cardioverter Defibrillator with AI algorithms that reduce false alarms and provide real-time data for up to one-week monitoring.

- February 2025: VitalConnect secured USD 100 million to accelerate VitalPatch biosensor development for cardiac monitoring.

Global Holter Monitor Market Report Scope

A Holter monitor is a small, wearable device that records the heart's rhythm. It detects and determines the risk of irregular heartbeats (arrhythmias).

The Holter monitor market is segmented by product, lead type, end user, and geography. Based on product type, the market is segmented into wired and wireless types. Based on lead type, the market is segmented as patch type lead Holter monitor, 3-lead monitor, 6-lead monitor, 12-lead monitor, and other lead types. Based on end-users, the market is segmented into hospitals, cardiac centers, ambulatory surgical centers, and other end-users. Based on geography, the market is segmented as North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers market size and forecast in terms of value (USD) for the above segments.

| Traditional 3-Lead Holter Monitors |

| 12-Lead Holter Monitors |

| Patch-based Holter Monitors |

| Wireless Holter Monitors |

| Implantable Loop Recorders (ILR) |

| Hospitals |

| Ambulatory Surgical Centers |

| Diagnostic Centers |

| Home Healthcare Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe (incl. Russia) | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Traditional 3-Lead Holter Monitors | |

| 12-Lead Holter Monitors | ||

| Patch-based Holter Monitors | ||

| Wireless Holter Monitors | ||

| Implantable Loop Recorders (ILR) | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Diagnostic Centers | ||

| Home Healthcare Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe (incl. Russia) | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Holter Monitor Market?

The Holter Monitor Market size is expected to reach USD 886.6 million in 2026 and grow at a CAGR of 6.82% to reach USD 1.23 billion by 2031.

What is the current Holter Monitor Market size?

In 2026, the Holter Monitor Market size is expected to reach USD 886.6 million.

Who are the key players in Holter Monitor Market?

Nihon Kohden, Medtronic, ScottCare Corporation,, Nasiff Associates, Inc and GE HealthCare are the major companies operating in the Holter Monitor Market.

Which is the fastest growing region in Holter Monitor Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Holter Monitor Market?

In 2025, the North America accounts for the largest market share in Holter Monitor Market.

What years does this Holter Monitor Market cover, and what was the market size in 2025?

In 2025, the Holter Monitor Market size was estimated at USD 0.89 billion. The report covers the Holter Monitor Market historical market size for years: 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Holter Monitor Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: