Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

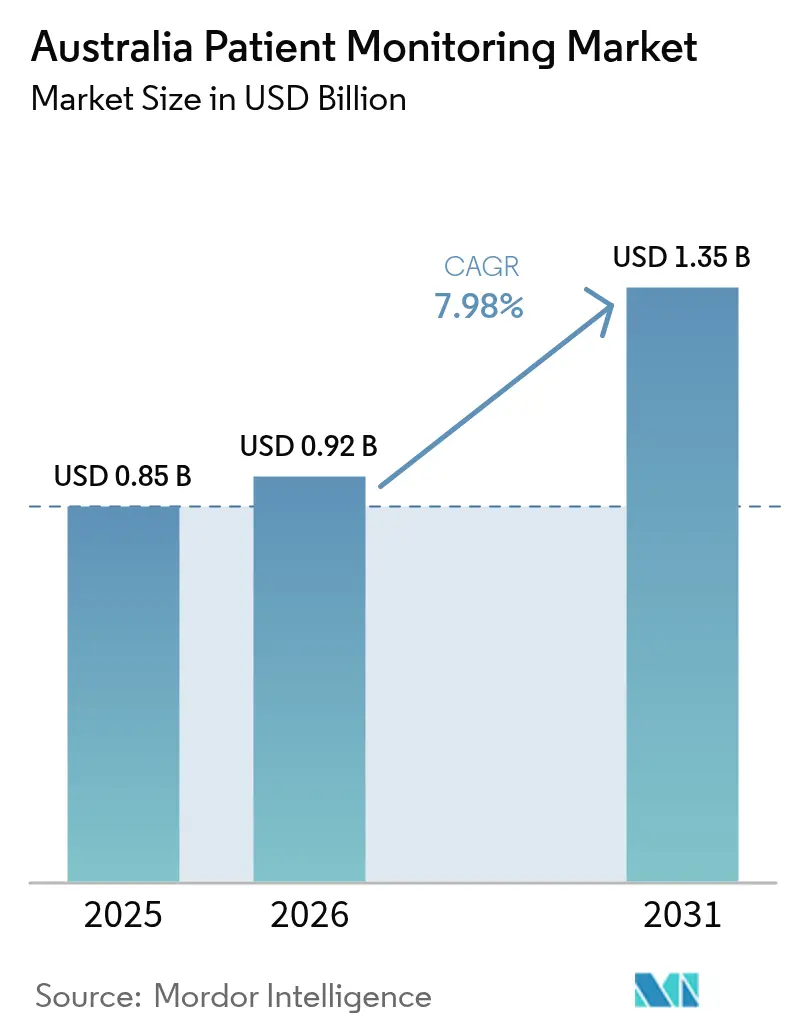

| Base Year Market Size (2025) | USD 0.85 Billion |

| Market Size (2026) | USD 0.92 Billion |

| Market Size (2031) | USD 1.35 Billion |

| Growth Rate (2026 - 2031) | 7.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Patient Monitoring Market Analysis by Mordor Intelligence

The Australia patient monitoring market size was valued at USD 0.85 billion in 2025 and estimated to grow from USD 0.92 billion in 2026 to reach USD 1.35 billion by 2031, at a CAGR of 7.98% during the forecast period (2026-2031). Momentum stems from accelerated 4G/5G coverage following the 3G network shutdown, permanent Medicare telehealth reimbursements and streamlined software-as-a-medical-device rules that shorten approval timelines. Public-sector grants for cybersecurity, direct-to-device satellite connectivity and hospital-at-home pilots encourage continuous multiparameter monitoring in urban and rural facilities. Intensifying partnerships between global manufacturers and local telehealth operators embed AI triage dashboards that reduce nuisance alarms and elevate nurse productivity.

Key Report Takeaways

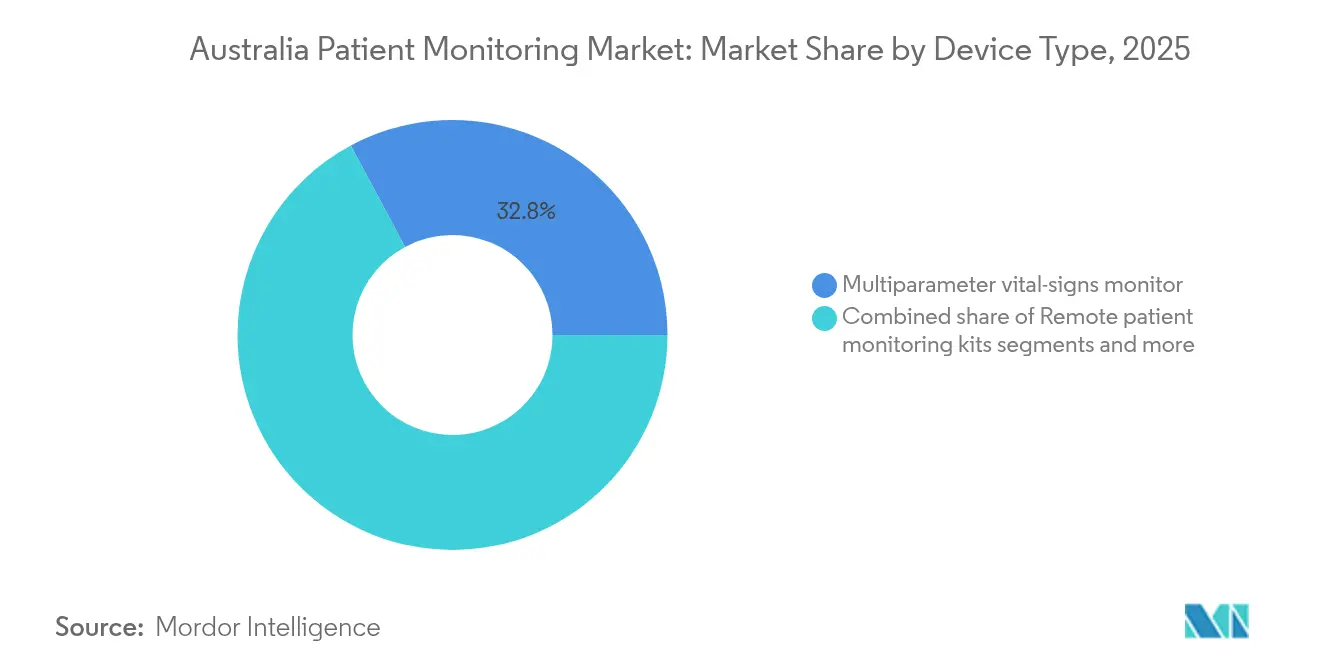

- By product type, multiparameter monitors led with 32.84% of Australia patient monitoring market share in 2025, while remote patient monitoring kits are on pace for an 8.05% CAGR through 2031.

- By modality, bedside systems represented 49.35% of the Australia patient monitoring market size in 2025; wearable and patch devices are forecast to expand at a 9.01% CAGR to 2031.

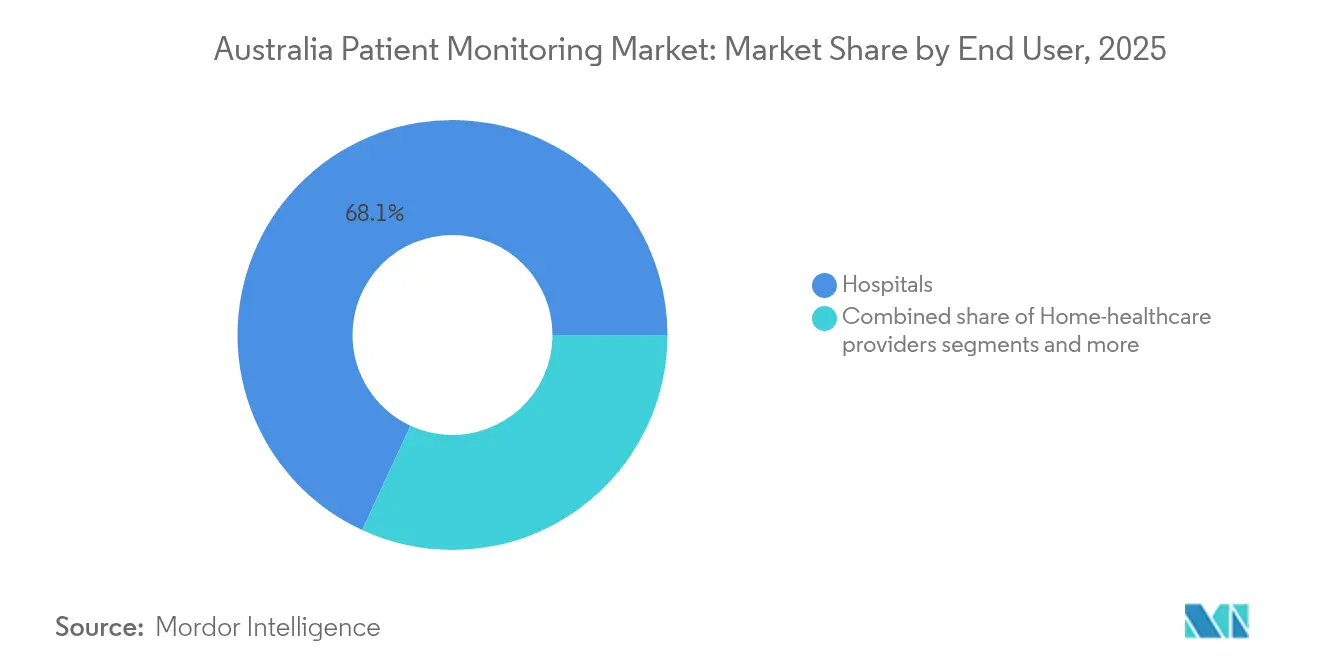

- By end user, hospitals held 68.10% of Australia patient monitoring market share in 2025, while home-healthcare providers register the fastest 8.18% CAGR over the outlook period.

- By application, cardiology captured 24.88% of the Australia patient monitoring market size in 2025; chronic-disease management is projected to grow at an 8.62% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Patient Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic diseases & ageing population | +2.1% | National, with higher impact in metropolitan areas | Long term (≥ 4 years) |

| Expansion of telehealth reimbursement & government digital health initiatives | +1.8% | National, with enhanced benefits for rural/remote areas | Medium term (2-4 years) |

| Rapid adoption of IoT-enabled wireless & wearable monitors | +1.5% | Urban centers initially, expanding to regional areas | Short term (≤ 2 years) |

| Hospital-at-home & shift toward home healthcare services | +1.3% | Metropolitan areas with strong digital infrastructure | Medium term (2-4 years) |

| AI-powered predictive analytics in Indigenous remote health programs | +0.9% | Remote and very remote areas, Northern Territory focus | Long term (≥ 4 years) |

| Emergence of smart wound-care patches for chronic ulcer monitoring | 0.4% | National, with emphasis on aged care facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising burden of chronic diseases & aging population

Diabetes mortality among Indigenous Australians is 4.4 times higher than for non-Indigenous peers, intensifying demand for continuous glucose, cardiac and wound-healing surveillance. Federal investment of USD 50 million in a total artificial heart and USD 3 billion in chronic-wound management highlights cardiovascular priorities. Smart wound patches from RMIT detect inflammatory markers in real time for roughly 500,000 chronic-wound cases annually. Short-Term Restorative Care pilots preserved 99% of client independence, demonstrating technology’s cost-avoidance potential for elder care. Population aging therefore amplifies needs for predictive analytics that pre-empt emergency admissions.

Expansion of telehealth reimbursement & government digital-health initiatives

Permanent Medicare telehealth items and triple bulk-billing incentives for vulnerable citizens create durable revenue for remote patient monitoring services. Tasmania’s Care@home extension shows state-level scaling of infection surveillance with around-the-clock clinician oversight. The National Healthcare Interoperability Plan has delivered one-third of its milestones, upgrading My Health Record so device data flows seamlessly across locations. A USD 3.5 billion federal allocation to triple bulk-billing incentives further pushes providers toward connected care and away from on-site consults.

Rapid adoption of IoT-enabled wireless & wearable monitors

The October 2024 3G shutdown spurred manufacturers to retrofit pacemakers, CPAPs and telemetry systems with 4G/5G radios. Abbott’s glucose feeds now stream into Epic EHRs, removing manual uploads and improving metabolic management. BIOTRONIK’s BIOMONITOR IV slashes false arrhythmia alerts by 86% while preserving 98% clinical relevance. Direct-to-device satellite programs extend IoT reach into outback communities previously outside mobile footprints.

Hospital-at-home & shift toward home-healthcare services

Analysts calculate hospital-at-home could save USD 1 billion yearly in operating expense and USD 6.4 billion in deferred bricks-and-mortar spend by 2030 as 350,000 admissions migrate home. South Australia’s My Home Hospital has treated 15,000 patients with high satisfaction and released bed capacity for acute cases. The Smarter Hospitals Project studies workforce readiness for virtual wards, while Silverchain’s nurse-supervised infusions document practical pathways from pilot to scale. Activity-based funding guidance now embeds remote-monitoring codes, giving hospitals income certainty when care occurs off-campus.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device cost & limited private reimbursement | -1.2% | National, with higher impact in rural/remote areas | Medium term (2-4 years) |

| Increasing cybersecurity & data-privacy compliance costs | -0.8% | National, with emphasis on large healthcare networks | Short term (≤ 2 years) |

| Patchy broadband & digital infrastructure in rural Australia causing RPM dropout | -0.6% | Rural and remote areas, particularly Northern Territory/Western Australia | Long term (≥ 4 years) |

| Clinician alert fatigue and medico-legal liability concerns | -0.4% | Hospital-based settings, ICU and critical care units | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High device cost & limited private reimbursement

Continuous glucose monitors and premium implantables remain expensive, especially for Indigenous patients with limited private cover. Modified Monash upgrades in 2025 raised bulk-billing rates in 34 regional towns, yet out-of-pocket device costs persist. Surveys show 80% of rural adults are digitally engaged but cite price and product complexity as leading adoption barriers. Private insurance seldom covers home-use monitoring hardware, stalling chronic-disease programs outside hospital walls.

Increasing cybersecurity & data-privacy compliance costs

Healthcare remains the nation’s most-targeted vertical, prompting USD 6.4 million in federal funding for information-sharing nodes across 750 hospitals and 6,500 clinics. The Cyber Security Act 2024 imposes minimum protections and breach-report mandates that inflate device R&D overhead. Expanded OAIC penalties amplify breach liabilities, while AI scribes used by 25% of GPs often lack TGA certification, creating medico-legal ambiguity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Multiparameter Monitors Lead Comprehensive Care

Multiparameter monitors contributed 32.84% to the Australia patient monitoring market size in 2025 thanks to plug-and-play compatibility with electronic health records and rapid display of ECG, SpO₂ and NIBP on a single screen. Remote patient monitoring kits will outpace all peers at an 8.05% CAGR by bundling Bluetooth wearables, AI triage engines and Medicare-reimbursable data services. Cardiac lines strengthen as BIOMONITOR IV delivers 86% nuisance-alarm reduction, elevating clinician trust in implantable loop recorders.

Hemodynamic platforms consolidate under BD’s USD 4.2 billion deal for Edwards’ Critical Care group, creating an advanced waveform analysis leader with cloud-ready integration. Fetal and neonatal innovators such as VitalTrace use real-time lactate to cut emergency C-sections in half. Respiratory and neuro lines now embed edge AI that flags apnea or neurologic decline seconds after onset. Wearable monitors inherit smartphone design cues yet comply with TGA’s unique-device-identifier rules, bridging consumer ergonomics and hospital governance across the Australia patient monitoring market.

By Modality: Wearables Challenge Bedside Dominance

Bedside systems retained 49.35% of Australia patient monitoring market share in 2025 because ICU workflows rely on trusted central stations. Wearable and patch monitors, however, advance at a 9.01% CAGR as patients demand untethered mobility and clinicians see earlier ambulation shorten average length of stay. Portable devices straddle step-down wards, slashing unplanned ICU returns by relaying spot-check vitals every two minutes versus manual four-hour intervals.

Implantable sensors such as Abbott’s AVEIR leadless pacemaker now include conduction-system pacing, widening therapeutic reach. Satellite-backed data links push wearable telemetry to cattle stations and mining camps, reflecting government dual-use space-industry strategy. Regulatory mutual recognition for FDA-cleared hardware speeds upgrades, letting providers abandon 3G-era boxes without repeating full conformity assessments.

By End User: Home Healthcare Disrupts Hospital Centricity

Hospitals captured 68.10% of Australia patient monitoring market share in 2025 through bulk procurement and ICU demand. Yet home-healthcare and aged-care operators post the swiftest 8.18% CAGR as virtual wards win public funding and family preference for at-home convalescence. Ramsay Health Care logged 9.4% FY 2024 revenue after linking remote rehabilitation pathways to acute discharges.

General-practice clinics leverage MyMedicare enrollment to boost telehealth rebates, with AI scribes freeing three minutes per consult. Telehealth corporations mirror New South Wales’ free virtual urgent-care blueprint, predicting 85,000 fewer emergency-department visits annually. Aged-care chains receive USD 13 million to pilot fall-detection lidars and sensor-enabled medication management, while public services adopt national digital-health blueprints.

By Application: Chronic-Disease Management Accelerates

Cardiology retained 24.88% of Australia patient monitoring market size in 2025 as pacemakers and Holters remained core. Chronic-disease management exhibits the fastest 8.62% CAGR because COPD, hypertension and diabetes programs shift to algorithm-guided home models fully reimbursed by the MBS. Neurology categories benefit from continuous EEG patches that detect seizure precursors, offering early evacuation for rural patients via the Royal Flying Doctor Service.

Respiratory applications rise on ResMed’s 10% Q4 2025 revenue growth from cloud-linked CPAP ecosystems. ICU modules install smart-alarm routing that filters 70% of non-actionable alerts, fighting burnout identified in systematic nurse reviews. Perioperative wards pilot 72-hour continuous SpO₂ and respiration patches, cutting post-op ICU transfers in half. Rehabilitation programs integrate inertial sensors to quantify home-based physio, aligning with the 99% functional-independence score seen in restorative-care trials.

Geography Analysis

Australia’s patient monitoring devices market demonstrates a pronounced urban-rural divide. Metro centers—Sydney, Melbourne, Brisbane, Perth and Adelaide—account for more than two-thirds of installs owing to robust fiber backbones, tertiary hospitals and specialist density. New South Wales’ statewide virtual urgent-care network alone is scheduled to add 200,000 RPM endpoints by 2030. Victoria’s virtual ED mirrors this scale by funneling vitals to cloud dashboards accessed by 200 aged-care homes.

Regional momentum improved after 34 communities received Modified Monash upgrades in March 2025, unlocking richer bulk-billing and clinician recruitment pools. Nevertheless, more than 50,000 connectivity complaints lodged with the telecommunications ombudsman in 2024 show persistent coverage gaps. Telstra–Starlink direct-to-device pilots now deliver 256 kbps bursts, supporting patch monitors in cattle stations that historically relied on paper vitals.

Northern Territory and Western Australia face vast distances and high Indigenous-care loads. The Central Australian Aboriginal Congress funds mobile clinics that tour eight remote settlements every eight weeks to provide diabetes monitoring and ulcer screening. Tasmania’s Care@home expansion reveals how smaller states can run seven-day virtual wards staffed by pharmacists, dietitians and nurse practitioners. Interoperability Plan milestones—14 achieved, 27 on track—lay nationwide healthcare-identifier rails, ensuring that telemetry captured in one state flows securely to another.

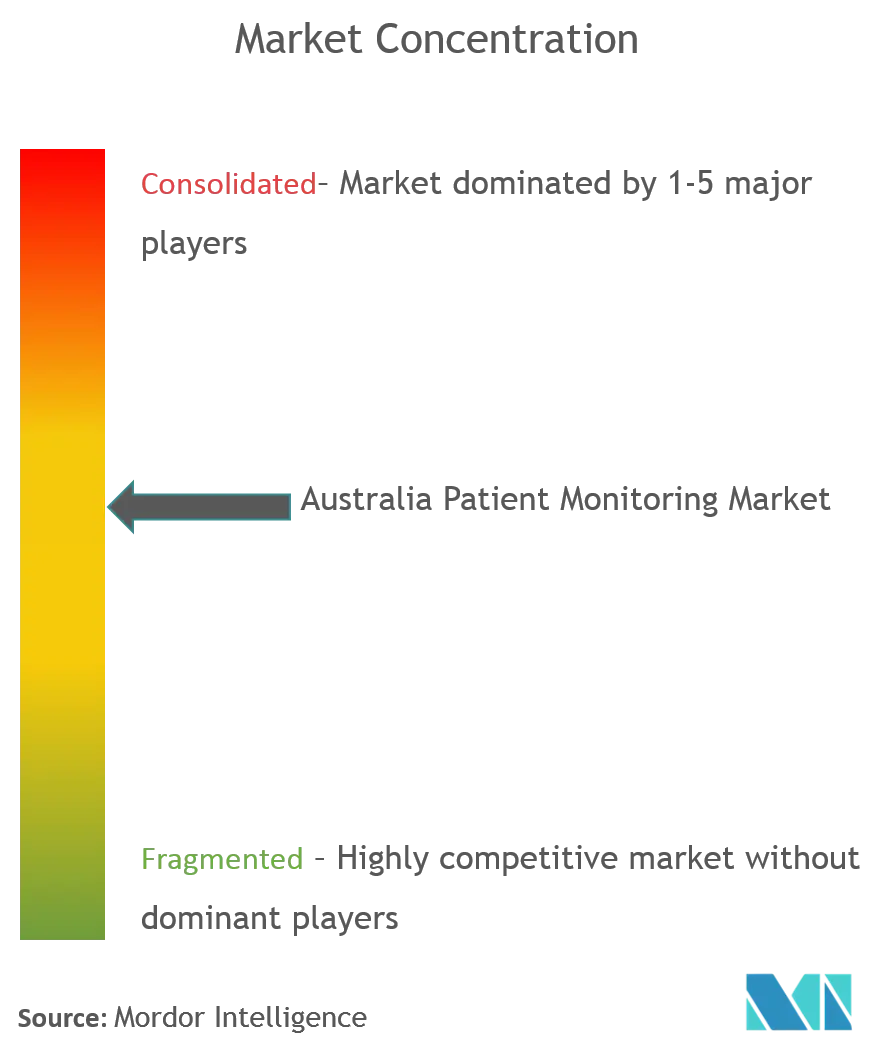

Competitive Landscape

The Australia patient monitoring market is moderately fragmented yet trending toward consolidation. BD’s USD 4.2 billion purchase of Edwards Lifesciences’ Critical Care group creates a global hemodynamic powerhouse serving 10,000 hospitals. Medtronic–Philips partnerships integrate Nellcor pulse-oximetry and Microstream capnography into Philips IntelliVue monitoring suites, backed by a pledge program validating joint safety claims. BIOTRONIK trims false arrhythmia alerts through SmartECG AI, complementing ResMed’s cloud-backed adherence data as hospitals demand device-agnostic dashboards. Domestic innovators such as VitalTrace aim for 2027 TGA clearance, while RMIT-origin smart-wound startups exploit aging-related ulcers as white-space growth pockets.

Competitive edges increasingly hinge on cyber-secure APIs, open FHIR transports and ready-mapped My Health Record feeds. Vendors able to bundle AI triage, device management and reimbursement analytics under a single subscription appeal most to public purchasers operating on activity-based funding models across the Australia patient monitoring market.

Australia Patient Monitoring Industry Leaders

Koninklijke Philips N.V

Mindray Medical International Co. Ltd.

Nihon Kohden Corporation

Baxter International Inc.

Siemens Healthcare GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Calvary Health Care completed joint venture transition with Amplar Health, with Calvary exiting to focus on core business while Amplar advances standalone virtual hospital operations.

- July 2024: TGA implemented new medical device regulation changes including updated software classification rules and mandatory application audits for Class III devices, affecting patient monitoring device approval pathways

Australia Patient Monitoring Market Report Scope

As per the scope of this report, patient monitoring devices are monitoring devices that continuously monitor the patient's vital parameters, like blood pressure and heart rates, by using a medical monitor and collecting medical (and other) data from individuals. The Australia Patient Monitoring Market is segmented by Type of Devices (Hemodynamic Monitoring Devices, Neuromonitoring Devices, Cardiac Monitoring, Multi-parameter Monitors, Respiratory Monitoring Devices, Remote Patient Monitoring Devices and Other Types of Devices), Application (Cardiology, Neurology, Respiratory, Fetal and Neonatal, Weight Management and Fitness Monitoring, and Other Applications), End-User ( Home Healthcare, Hospitals and Clinics and Other End Users). The report offers the value (in USD million) for the above segments.

By Product Type (Value, AUD mn)

| Multi-parameter Monitors |

| Cardiac Monitoring Devices (ECG, Holter, MCT) |

| Hemodynamic Monitoring Devices |

| Fetal & Neonatal Monitors |

| Neuro Monitoring Devices |

| Respiratory Monitoring Devices |

| Remote Patient Monitoring Kits & Platforms |

| Vital Signs Monitors |

| Wearable Patient Monitors |

By Modality

| Bedside / Stationary |

| Portable / Compact |

| Wearable / Patch |

| Implantable Sensors |

By End User

| Hospitals & Public Health Services |

| Private Hospitals & Day Surgery Centers |

| Home Healthcare & Aged-Care Facilities |

| Ambulatory Care & GP Clinics |

| Telehealth Providers |

By Application

| Cardiology |

| Neurology |

| Respiratory Care |

| Critical Care & ICU |

| Chronic Disease Management (Diabetes, Hypertension, COPD) |

| Perioperative & Anesthesia Monitoring |

| Post-Acute & Rehabilitation |

By Technology

| Wired |

| Wireless (Bluetooth, Wi-Fi) |

| Cloud-connected / AI Analytics |

| By Product Type (Value, AUD mn) | Multi-parameter Monitors |

| Cardiac Monitoring Devices (ECG, Holter, MCT) | |

| Hemodynamic Monitoring Devices | |

| Fetal & Neonatal Monitors | |

| Neuro Monitoring Devices | |

| Respiratory Monitoring Devices | |

| Remote Patient Monitoring Kits & Platforms | |

| Vital Signs Monitors | |

| Wearable Patient Monitors | |

| By Modality | Bedside / Stationary |

| Portable / Compact | |

| Wearable / Patch | |

| Implantable Sensors | |

| By End User | Hospitals & Public Health Services |

| Private Hospitals & Day Surgery Centers | |

| Home Healthcare & Aged-Care Facilities | |

| Ambulatory Care & GP Clinics | |

| Telehealth Providers | |

| By Application | Cardiology |

| Neurology | |

| Respiratory Care | |

| Critical Care & ICU | |

| Chronic Disease Management (Diabetes, Hypertension, COPD) | |

| Perioperative & Anesthesia Monitoring | |

| Post-Acute & Rehabilitation | |

| By Technology | Wired |

| Wireless (Bluetooth, Wi-Fi) | |

| Cloud-connected / AI Analytics |

Key Questions Answered in the Report

What is the projected value of Australia patient monitoring devices by 2031?

The market is expected to reach USD 1,347.2 million in 2031, expanding at an 7.98% CAGR from 2026.

Which product type currently dominates device demand in Australia?

Multiparameter monitors command the largest share at 32.84% of 2025 revenues.

Why are wearables growing faster than bedside monitors?

Wearables deliver mobility, reduce nurse workload and align with hospital-at-home models, delivering a 9.01% CAGR through 2031.

How does government telehealth funding influence demand?

Permanent MBS telehealth items and triple bulk-billing incentives create sustainable revenue for remote patient monitoring providers, boosting adoption.

What are the main cybersecurity challenges for device makers?

New regulations mandate minimum security features and breach reporting, raising compliance costs even as healthcare remains the most targeted sector.

Which end-user segment shows the highest growth?

Home-health and aged-care providers are expanding fastest with an 8.18% CAGR as virtual wards scale nationally.

Page last updated on: