Thermoplastic Starch (TPS) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

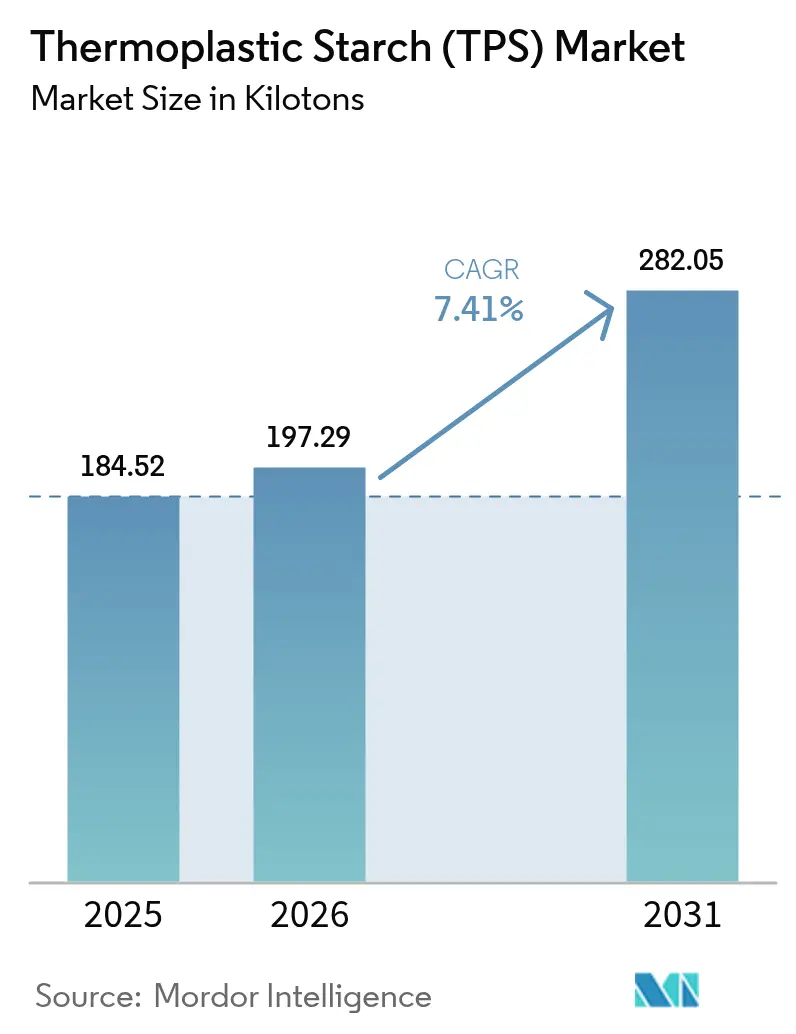

| Market Volume (2026) | 197.29 kilotons |

| Market Volume (2031) | 282.05 kilotons |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermoplastic Starch (TPS) Market Analysis by Mordor Intelligence

The Thermoplastic Starch Market size is expected to increase from 184.52 kilotons in 2025 to 197.29 kilotons in 2026 and reach 282.05 kilotons by 2031, growing at a CAGR of 7.41% over 2026-2031. Brand-owner sustainability targets, escalating bans on single-use plastics, and advances in moisture-barrier chemistry are steering converters toward starch-based resins that can run on existing polyethylene lines. Europe leads because the Packaging and Packaging Waste Regulation (PPWR 2025/40) accelerates the switch to certified-compostable formats, while Asia-Pacific gains momentum as China, India, and ASEAN tighten import and disposal rules for conventional plastics. Extrusion remains the dominant processing route for high-volume film and bag grades, yet medical trials are boosting demand for injection-moldable TPS composites with tighter dimensional tolerances. Supply security hinges on diversified, low-grade starch feedstocks that decouple resin costs from food-grade corn and cassava price spikes.

Key Report Takeaways

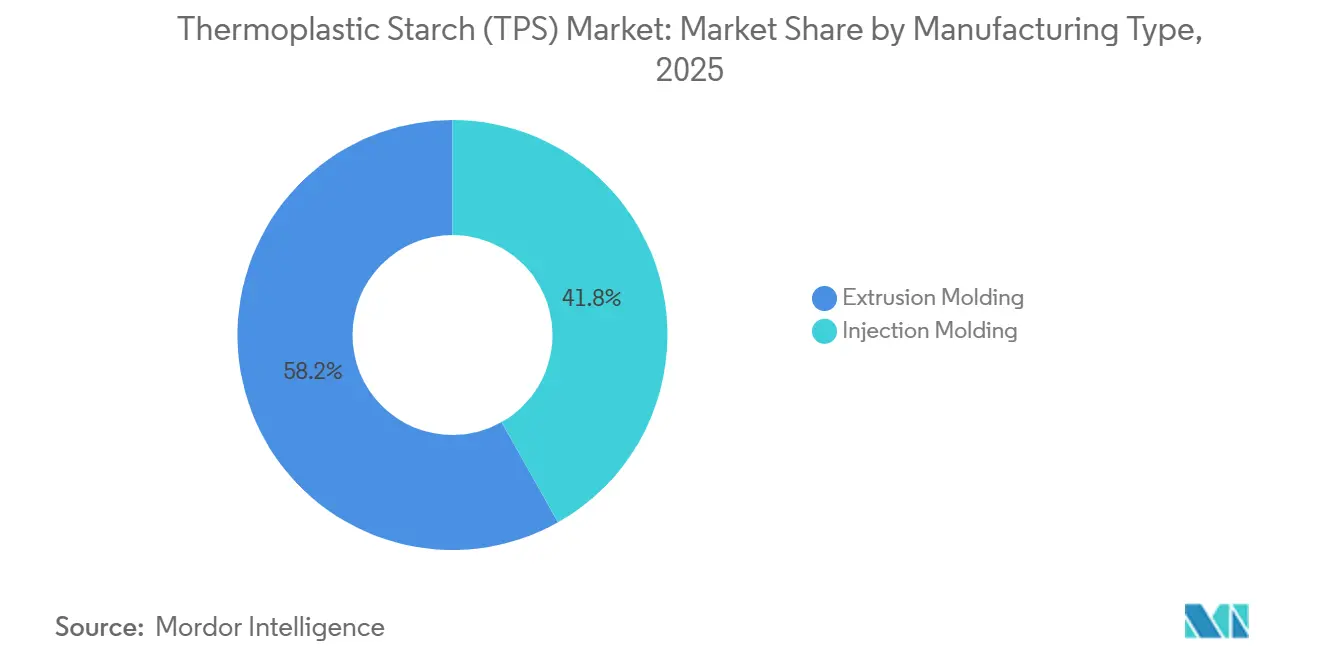

- By manufacturing type, extrusion molding held 58.17% of the thermoplastic starch market share in 2025, while injection molding is projected to post the highest 7.89% CAGR to 2031.

- By application, films commanded 47.80% of the thermoplastic starch market size in 2025; bags are set to grow the fastest at an 8.38% CAGR through 2031.

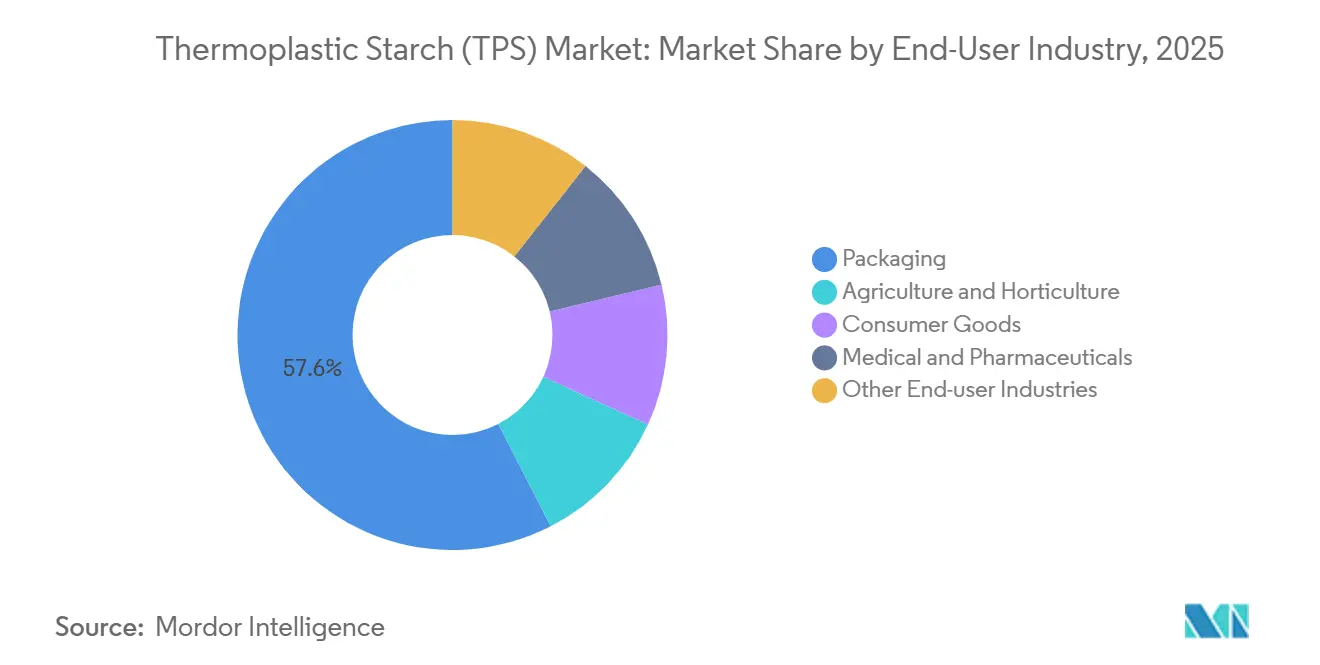

- By end-user industry, packaging dominated with 57.55% of the thermoplastic starch market share in 2025, whereas medical and pharmaceuticals will expand at an 8.90% CAGR during 2026-2031.

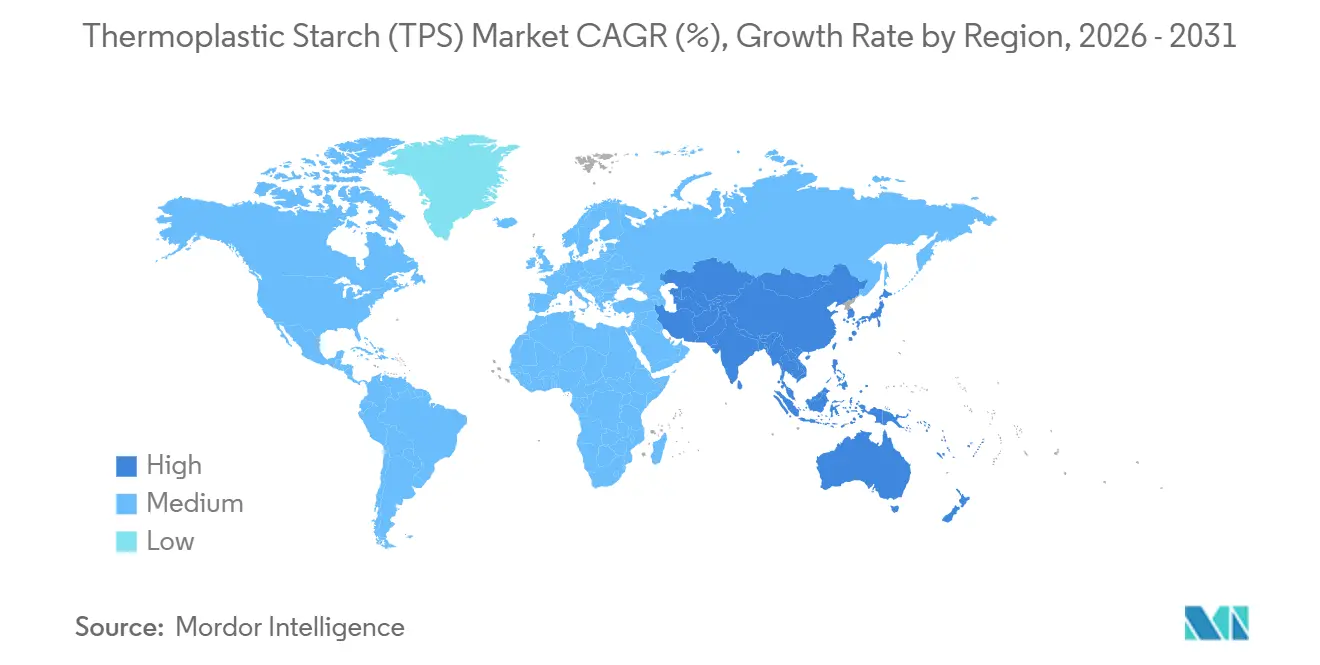

- By geography, Europe led with a 39.82% thermoplastic starch market share in 2025, and Asia-Pacific is expected to record the quickest 8.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thermoplastic Starch (TPS) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for biodegradable packaging | +2.1% | Global, with EU and North America leading | Medium term (2-4 years) |

| Ban on single-use plastics in major economies | +1.8% | EU, UK, Canada, China, India, select U.S. states | Short term (≤ 2 years) |

| Brand-owner sustainability pledges beyond regulatory mandates | +1.3% | Global, concentrated in North America and EU | Medium term (2-4 years) |

| Shift toward home-compostable e-commerce mailers | +0.9% | North America, EU, Australia | Short term (≤ 2 years) |

| Pharma blister-pack replacement trials with TPS composites | +0.6% | North America, EU, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Biodegradable Packaging

Under the PPWR 2025/40 regulation, converters are racing against the clock to meet the 2030 deadlines for recyclability or compostability. This urgency is compressing research and development cycles and accelerating material substitutions. By blending TPS with PLA or PBAT, manufacturers can meet EN 13432 and ASTM D6400 standards, allowing brand owners to upgrade their materials without overhauling major equipment. In Germany, France, and the Netherlands, municipal organics-collection initiatives have begun accepting certified TPS films, smoothing the path for wider adoption. Major FMCG companies are on track to eliminate non-recyclable plastics by 2028, shifting their procurement focus to pouches and sachets with higher renewable content. Collectively, these developments are driving up the baseline demand for TPS packaging grades across both consumer and industrial sectors[1]EUROPEAN BIOPLASTICS, “Market Data and Industry Information,” European-bioplastics.org.

Ban on Single-Use Plastics in Major Economies

National prohibitions on polyethylene checkout bags, straws, and food-service items compel rapid TPS substitutions. Canada’s regulations entered full enforcement in December 2024, sweeping food-service operators into compliance overnight. India tightened penalties in 2025, prompting domestic converters to switch to starch blends that meet local compostability norms. China’s revised Solid Waste Law levies fees on non-degradable packaging, pushing leading e-commerce firms toward TPS mailers for urban deliveries. Because starch resins can be certified under multiple regional standards, suppliers capture demand across jurisdictions that previously required separate formulations[2]GOVERNMENT OF CANADA, “Single-Use Plastics Prohibition Regulations,” Canada.ca.

Brand-Owner Sustainability Pledges Beyond Regulatory Mandates

PepsiCo and Mars Wrigley have each committed to TPS-based film development, aiming to achieve science-driven carbon targets ahead of mandated deadlines. These voluntary pledges not only surpass the EU's recycled-content benchmarks but also bolster the demand for suppliers who can ensure traceability from farm to resin. In 2025, long-term offtake agreements were inked, integrating TPS volumes into packaging strategies. This move enhances the financial viability of starch expansion initiatives and reduces borrowing costs for local processors.

Shift Toward Home-Compostable E-Commerce Mailers

California's organic-waste diversion rules now embrace backyard-compostable mailers. This niche is particularly suited for TPS grades, which are coated with thin wax layers. These layers retain moisture during transit but decompose within 26 weeks after use. In 2025, both Australian and U.S. startups witnessed a surge, boasting significant sales growth. This uptick was largely driven by small merchants adopting these eco-friendly mailers to cater to environmentally-conscious consumers. Furthermore, certification logos have emerged as key marketing differentiators, establishing a formidable entry barrier against untested imports.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Moisture sensitivity limiting shelf-life | -1.2% | Global, acute in tropical Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Inferior mechanical strength vs. petro-plastics | -0.9% | Global, particularly in heavy-duty packaging | Medium term (2-4 years) |

| Food-versus-materials debate around starch feedstock | -0.7% | Global, concentrated in regions with food-security concerns | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Moisture Sensitivity Limiting Shelf-Life

Unmodified TPS can absorb significant water within two days at high relative humidity, causing swelling and early tearing in tropical logistics chains. PBAT-rich blends lower water uptake but dilute renewable-content claims and raise cost. Surface coatings, while helpful, must remain under a small percentage of total weight to keep EN 13432 certification, adding process complexity. Consequently, TPS remains preferred for short-lived produce bags and mulch films rather than multi-month shelf-stable goods.

Inferior Mechanical Strength vs. Petro-Plastics

While TPS's tensile strength is lower than polypropylene, this disparity restricts TPS's application in stretch-wrap and shipping sacks. Although nanofiller reinforcement and specialized compatibilizer chemistry help bridge this gap, they also elevate formulation costs. Consequently, converters are compelled to thicken the film gauge, undermining the lightweighting benefits brands seek from their packaging overhauls.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Manufacturing Type: Extrusion Dominates, Injection Gains in Healthcare

Extrusion molding held 58.17% volume in 2025, reflecting its compatibility with existing polyethylene blown-film lines and the high-throughput economics prized by converters. This route lets regional processors retrofit rather than retool, speeding market entry and anchoring standard-grade volumes that reinforce the thermoplastic starch market. Injection molding captured a smaller base but is projected to outpace at 7.89% CAGR as medical-device makers adopt TPS composites for blister packs, trays, and diagnostic housings. The willingness of hospitals to pay a quality premium insulates injection grades from the cost pressures felt in commodity film markets.

Extrusion’s cost leadership spurs capacity additions in China and India that may temper average selling prices worldwide. Yet medical-grade injection compounds demand ISO 13485 certification and tight tolerances that shield margins. Suppliers that master both processing routes can tier their portfolios, positioning standard grades for retail bags while reserving high-amylose or nanoclay-reinforced grades for healthcare. This dual strategy allows producers to defend their share as petrochemical incumbents leverage compounding assets to challenge the thermoplastic starch market.

By Application: Films Lead, Bags Accelerate on Retail Mandates

Films controlled 47.80% application volume in 2025 and remain the anchor segment because agricultural mulch, e-commerce mailers, and fresh-produce wraps all require thin-gauge, high-surface-area formats well suited to blown extrusion. Mulch adoption surged after Spain and Italy linked farm subsidies to biodegradable film use, cementing Europe’s leadership. Bags, however, are on track for the fastest growth at 8.38% CAGR, lifted by checkout-bag bans that exclude all but ASTM D6400-compliant materials. Together, these two uses safeguard baseline demand and account for more than half of the overall thermoplastic starch market size through 2031.

Technical diversification is also underway. PLA-TPS filaments for 3D printing are winning prototype packaging work for luxury brands that want novel shapes without injection tooling. Smaller but lucrative niches such as loose-fill, plant pots, and coated paper cups extend the addressable space, giving converters multiple on-ramps into the thermoplastic starch industry. Suppliers that secure certifications across these end-uses deepen customer lock-in and can command a price premium over untested imports.

By End-User Industry: Packaging Commands, Medical Surges

Packaging consumed 57.55% of TPS volume in 2025, driven by grocery bags, courier mailers, and flexible food wraps. The segment’s regulatory exposure means volumes will climb as additional states and provinces copy California’s compostable-bag rules. Medical and pharmaceuticals, although smaller, are forecast to grow at 8.90% CAGR, the highest among end-users, because hospitals target single-use plastic reductions and generic drug makers seek packaging differentiation. This shift positions specialty grades to capture premium margins and elevates the thermoplastic starch market share of medical applications by the decade’s close.

Agriculture and horticulture benefit from in-soil degradability, eliminating costly mulch retrieval. Consumer goods, ranging from cutlery to clamshells, fill compliance gaps for quick-service restaurants facing extended producer responsibility fees. Collectively, these outlets diversify revenue streams and buffer suppliers against price swings in any single sector.

Geography Analysis

Europe kept 39.82% global volume leadership in 2025 as PPWR 2025/40 and country-level levies made non-compostable packaging economically unattractive. Germany, France, and Italy pooled more than half of continental demand, underpinned by mature composting infrastructure that validates the thermoplastic starch market size leadership. The United Kingdom’s 2024 plastic packaging tax, although outside the EU, further expanded certified-compostable demand. Nordic pilots that accept TPS films in municipal organics bins remove a historic barrier and promise steady incremental growth across Scandinavia.

Asia-Pacific is the fastest-growing region at an 8.54% CAGR to 2031. China's extended producer responsibility fees target non-degradable cartons, while India's regulations on bag thickness are steering major retail chains towards starch blends. Japan's Plastic Resource Circulation Act sets a reduction target for single-use plastics by 2030, urging retailers to adopt compostable display and produce bags. In ASEAN, harmonized standards introduced in 2024 are slashing certification costs for exporters, facilitating smoother cross-border trade in TPS packaging.

North America's adoption of these trends is uneven. States like California, Washington, and Oregon have mandated compostable food serviceware, but many interior states have yet to catch up. In Canada, a nationwide ban on polyethylene checkout bags set for 2024 has spurred TPS demand among fast-food chains. Meanwhile, Mexican states initiated their own rolling bans in 2025. A notable surge in certification volume at BPI in 2025 underscores a growing acknowledgment of starch-based compliance. However, South America and the Middle-East and Africa lag, hindered by a lack of composting infrastructure and a policy emphasis on mechanical recycling rather than organic diversion.

Competitive Landscape

The thermoplastic starch market remains moderately consolidated. Emerging challengers pursue three white-space themes. First, waste-derived feedstocks such as potato peels cut raw-material costs and sidestep the food-versus-materials debate. Second, medical-grade formulations that pass ISO 11607 and EMA stability tests address an underserved, high-margin niche. Third, hybrid barrier technologies—thin PVOH or chitosan layers below the 5% weight threshold—expand TPS use cases to humid-climate snack and pharma wraps. Certification under multiple compostability regimes erects a compliance moat that favors producers with in-house labs or partnerships with accredited testing centers. Competitive intensity is rising as petrochemical incumbents retrofit compounding assets for bioplastics, compressing spot margins for pure-play TPS suppliers. Yet vertically integrated starch processors enjoy cost advantages in feedstock sourcing and can customize plasticizer chemistries for regional climate needs. Strategic collaborations with FMCG brand owners and medical-device OEMs provide volume visibility that de-risks capacity expansions, illustrating how demand-side partnerships now influence capital allocation across the thermoplastic starch industry.

Thermoplastic Starch (TPS) Industry Leaders

Novamont S.p.A (Versalis S.p.A.)

BASF

Danimer Scientific

Rodenburg Biopolymers

BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Kuraray launched PLANTIC EP, a thermoplastic starch-based, compostable polymer aimed at coffee, tea, pet-food, and modified-atmosphere packaging applications.

- October 2023: Versalis completed the acquisition of the remaining 64% stake in Novamont, strengthening its biopolymer portfolio.

Global Thermoplastic Starch (TPS) Market Report Scope

Thermoplastic starch (TPS) is a homogenous product made from native starch, water, and additional plasticizers such as glycerol, sorbitol, and glucose. It is used mainly in packaging materials, and some utilize bio-fillers or fiber in the formulation to enhance bio-based plastic.

The market is segmented by manufacturing type, application, end-user industry, and geography. By manufacturing type, the market is segmented into extrusion molding and injection molding. By application, the market is segmented into bags, films, 3-D printing, and other applications. By end-user industry, the market is segmented into packaging, agriculture and horticulture, consumer goods, medical and pharmaceuticals, and other end-user industries. The report also covers the market size and forecasts for the market in 15 countries across the major regions. For each segment, the market sizing and forecasts have been done based on volume (Tons).

| Extrusion Molding |

| Injection Molding |

| Bags |

| Films |

| 3-D Printing |

| Other Applications |

| Packaging |

| Agriculture and Horticulture |

| Consumer Goods |

| Medical and Pharmaceuticals |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Manufacturing Type | Extrusion Molding | |

| Injection Molding | ||

| By Application | Bags | |

| Films | ||

| 3-D Printing | ||

| Other Applications | ||

| By End-User Industry | Packaging | |

| Agriculture and Horticulture | ||

| Consumer Goods | ||

| Medical and Pharmaceuticals | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

Key growth driver through 2031?

Enforced bans on single-use polyethylene bags and films in the EU, Canada, China, and India are the strongest uplift factors for certified-compostable TPS grades.

Leading application segment by 2025 volume?

Films, including agricultural mulch and courier mailers, represented 47.80% of global tonnage in 2025.

Fastest-growing region?

Asia-Pacific is projected to expand at an 8.54% CAGR during 2026-2031 due to synchronized regulatory measures across China, India, and ASEAN.

What is the current global demand for the thermoplastic starch market and its expected growth by 2031?

Global consumption is 197.29 kilotons in 2026 and is projected to reach 282.05 kilotons by 2031, reflecting a 7.41% CAGR.

Page last updated on: