Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.78 Billion |

| Market Size (2031) | USD 5.36 Billion |

| Growth Rate (2026 - 2031) | 7.20% CAGR |

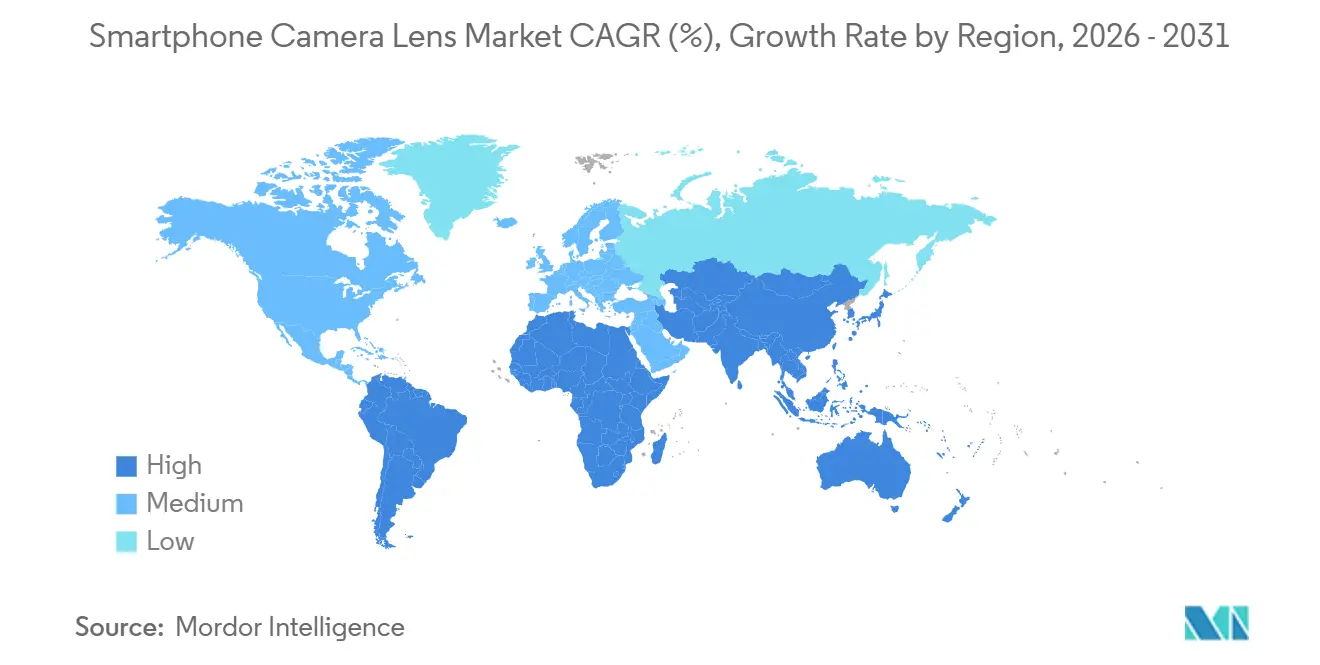

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smartphone Camera Lens Market Analysis by Mordor Intelligence

The smartphone camera lens market size was valued at USD 3.54 billion in 2025 and estimated to grow from USD 3.78 billion in 2026 to reach USD 5.36 billion by 2031, at a CAGR of 7.20% during the forecast period (2026-2031). Average selling prices for lens modules continue to climb as device makers replace basic plastic optics with 7- or 8-element glass-plastic hybrids, especially in periscope and variable-aperture assemblies. Telescopic zoom capability is expanding into mid-range handsets, giving suppliers a lucrative path to offset stagnant global smartphone shipments. Demand also benefits from multi-camera configurations that require ultra-wide, macro, and depth lenses to support AI-driven computational photography. Precision glass-molding capacity, already operating near full utilization, is set to tighten further as per-unit defects remain higher than conventional wide-angle modules.

Key Report Takeaways

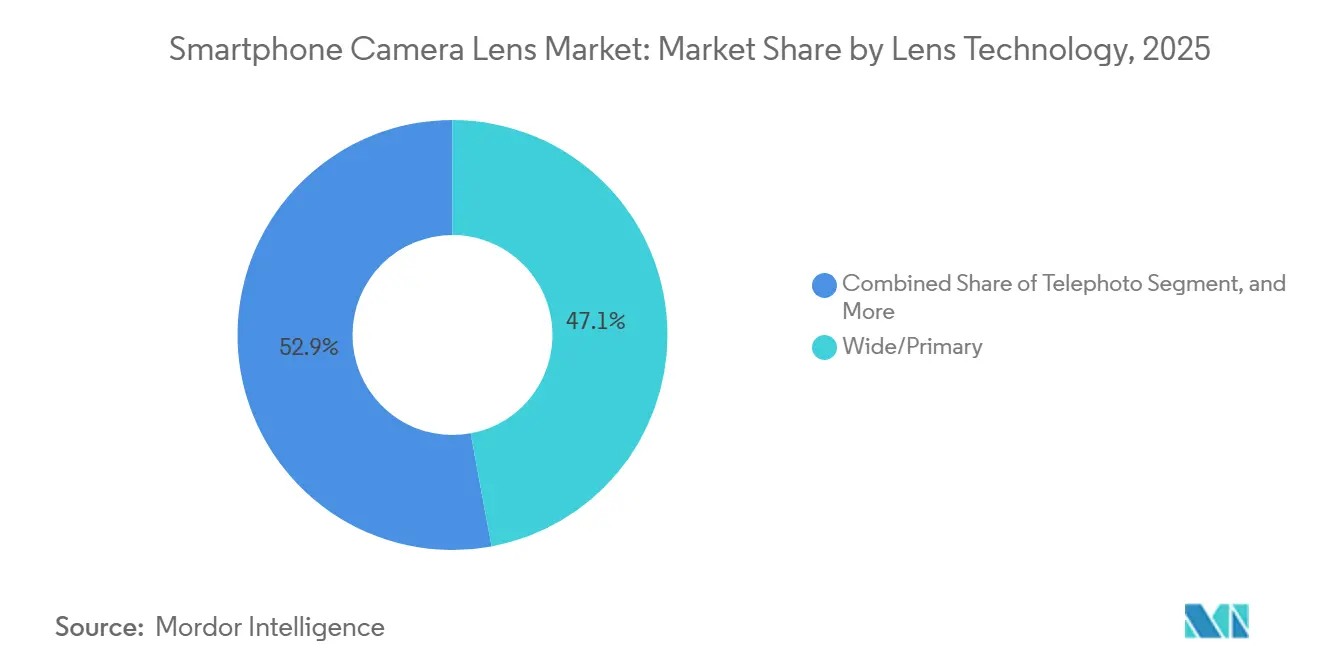

- By lens technology, wide/primary lenses commanded 46.91% of revenue in 2025; telephoto optics are forecast to grow at an 9.40% CAGR through 2031.

- By lens material, glass-plastic hybrids captured 58.01% of the market share in 2025; the all-glass category is projected to grow at an 11.64% CAGR through 2031.

- By camera position, rear-primary modules accounted for 46.64% of 2025 demand; rear-secondary lenses are expected to post an 8.26% CAGR over the forecast period.

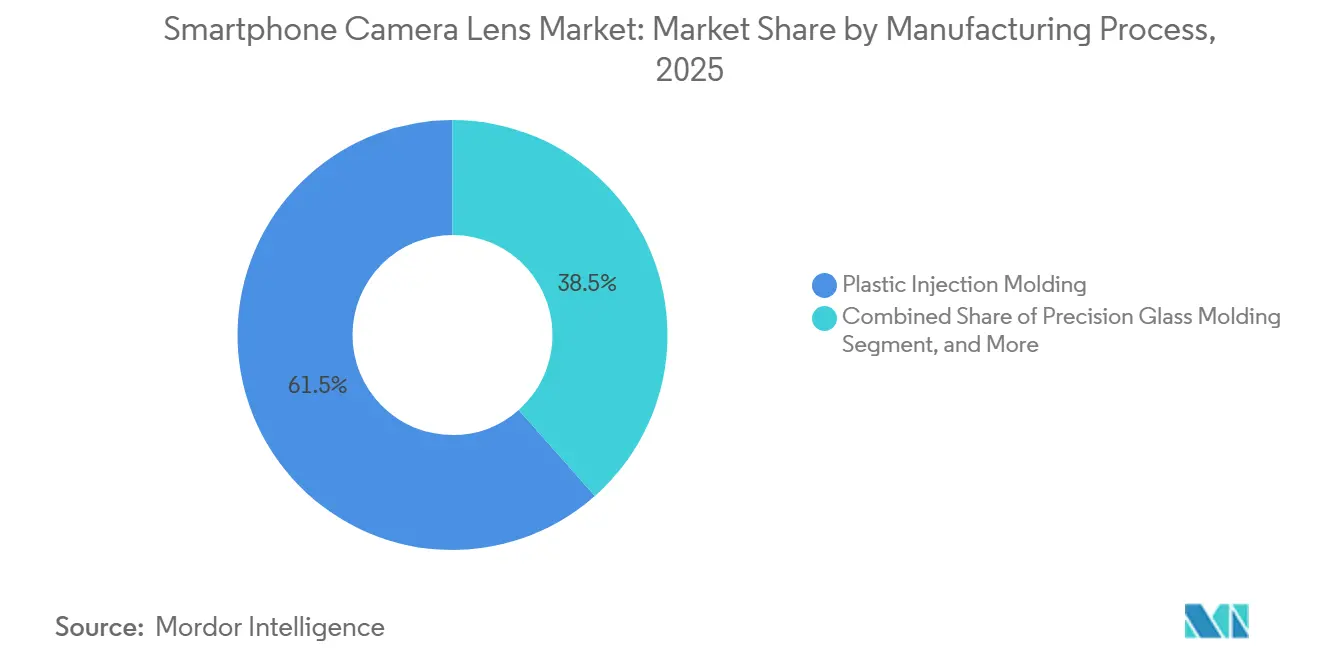

- By manufacturing process, plastic injection molding led with a 61.52% share in 2025, and wafer-level/hybrid optics manufacturing is the fastest-growing, with an 11.44% CAGR through 2031.

- By smartphone tier, mid-range devices accounted for 44.96% of lens demand in 2025; flagship handsets are set to grow at an 9.44% CAGR through 2031.

- By geography, Asia-Pacific dominated with 53.56% of 2025 revenue, and the region is poised to expand at an 9.22% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smartphone Camera Lens Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Periscope and Telephoto Modules | +1.5% | Global, with early gains in China, South Korea, India | Medium term (2-4 years) |

| Megapixel Race Above 50 MP Lifting Lens ASPs | +1.3% | Global, concentrated in Asia-Pacific and North America | Short term (≤ 2 years) |

| AI-Centric Computational Photography Requirements | +1.2% | Global, spill-over to Middle East and South America | Medium term (2-4 years) |

| Proliferation of Multi-Camera Smartphones | +1.0% | Global, mature in Asia-Pacific, accelerating in South America | Long term (≥ 4 years) |

| Localised Lens Supply-Chain Build-Out in India and Vietnam | +0.9% | Asia-Pacific core, with indirect benefits to North America | Long term (≥ 4 years) |

| Glass-Plastic Free-Form Lenses for Foldables and Wearables | +0.7% | Asia-Pacific and North America, niche in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Periscope and Telephoto Modules

Periscope telephoto modules moved from USD 1,000 flagships to USD 400-600 handsets in 2025, shrinking the optical-zoom gap between premium and mid-range devices.[1]Android Authority staff, “Huawei Pura 80 Ultra, OPPO Find X9 Ultra, and vivo X300 Ultra Camera Specifications,” AndroidAuthority.com Each assembly relies on 7- or 8-element glass-plastic hybrids plus a prism, so average selling prices jump 18-22% when periscope zoom is added. Shipments rose 34% year over year at Largan Precision, yet prism alignment tolerances below 5 µm keep reject rates roughly 12-15 points higher than for wide-angle lenses. OEM marketing now highlights 5x to 10x optical zoom as a headline feature, reinforcing consumer awareness of lens quality. Capacity constraints in precision glass molding suggest that periscope penetration will continue to lift supplier margins through 2027.

Megapixel Race Above 50 MP Lifting Lens ASPs

Sony’s 200 MP LYT-901 sensor sets an optical benchmark of modulation-transfer-function values above 0.6 at 100 lp/mm, forcing lens makers to use aspheric glass and advanced coatings.[2]Sony Semiconductor Solutions, “LYT-901 200 MP Sensor Launch,” Sony-semicon.co.jp Samsung’s ISOCELL HP5 keeps camera stacks thinner but raises module cost, pushing flagship optical subsystems toward USD 80-100 per phone. The gulf between high-end and entry optics now reaches a 3-6× price multiple, so vendors prioritize premium projects even while global handset volumes flatten. Higher pixel counts also widen image circles, which drives larger lens diameters and additional elements. These requirements explain why hybrid lenses gained nearly half the market in 2025.

AI-Centric Computational Photography Requirements

On-device AI delivers full-HD image fusion in about 5 ms on GPUs such as Qualcomm’s Adreno 830, letting mid-tier lenses relax certain surface tolerances while still producing flagship-grade output.[3]Qualcomm Technologies, “Adreno 830 GPU Computational Photography Performance,” Qualcomm.comYet AI algorithms like Apple Deep Fusion need ≥92% light transmission to maximize low-light signal-to-noise ratios, which in turn accelerates glass adoption. Sunny Optical credited triple-digit hybrid-lens revenue growth in early 2025 to AI-driven optical demand from flagship launches. Algorithmic rectilinear correction also encourages ultra-wide lenses with 120-degree fields of view, pushing free-form aspheric designs into mainstream phones. The interplay of software and optics therefore raises both performance ceilings and material costs.

Proliferation of Multi-Camera Smartphones

Average camera count reached 3.5 per phone in 2024, but brands now swap low-value 2 MP macro sensors for high-resolution telephotos that deliver true zoom and macro capability through cropping. South American shipments of sub-USD 300 multi-camera models climbed to 61% in 2025, evidence that auxiliary optics drive purchase decisions even in value segments. Samsung’s Galaxy S25 Ultra kept a quad-camera layout yet upgraded its telephoto sensor to 50 MP, underscoring a pivot from quantity to quality. Each rear-secondary module relies on glass-plastic hybrids to match primary-lens performance, raising average material costs. Multi-camera demand therefore secures incremental revenue for lens suppliers despite handset unit saturation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global Smartphone Unit Saturation | -1.2% | Global, acute in North America, Europe, and mature Asia markets | Short term (≤ 2 years) |

| Aggressive Pricing Pressure in Mid- and Low-Tier Handsets | -0.9% | Global, concentrated in South Asia, South America, Africa | Medium term (2-4 years) |

| High-Layer Hybrid Lens Yield Challenges | -0.6% | Asia-Pacific core, indirect impact on global supply | Medium term (2-4 years) |

| Export-Control Risk on Precision Glass-Moulding Tools | -0.4% | China, with spill-over to Asia-Pacific supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Smartphone Unit Saturation

Worldwide shipments stalled near 1.2 billion units and India’s market slid 1% in 2025, as replacement cycles stretched beyond three years. TechInsights tracked only 4% global unit growth in 1H 2025 versus 8% revenue growth for devices above USD 600, highlighting a shift to value over volume. This saturation caps lens demand growth at single-digit rates even while premium tiers thrive. Suppliers face revenue concentration risk because flagship models represent under one-quarter of units yet almost half of lens income. Any downturn in premium demand could therefore compress margins quickly.

Aggressive Pricing Pressure in Mid- and Low-Tier Handsets

Component inflation lifted DRAM and NAND costs by 5-8% in 2025, but wholesale smartphone ASPs edged up only 0.5%, forcing OEMs to squeeze lens prices. Entry devices in India and Latin America now target USD 5-8 lens modules, so suppliers substitute all-plastic optics that deliver 10-15% lower image quality. LG Innotek’s AI defect-detection system cut reject rates 90%, trimming unit costs 12-15% and protecting margins, yet smaller vendors lack similar automation. Persistent price pressure leaves several second-tier lens makers with operating margins below 8%, down from 12-14% in 2022. Continued commoditization may trigger industry consolidation as cost leadership becomes critical.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lens Technology: Telephoto Ascendancy Reshapes Module Economics

Telephoto optics posted a 9.40% CAGR through 2031, the fastest pace among all technologies, so their slice of the smartphone camera lens market is expanding even as total handset units plateau. Shipments rose when periscope zoom modules migrated into USD 400-600 phones, allowing brands to advertise 5x to 10x optical zoom as a mainstream feature. Wide-angle lenses still held 46.91% of the smartphone camera lens market share in 2025, but their growth stalled as innovation dollars now chase auxiliary cameras. Ultra-wide designs gained relevance after AI rectilinear correction unlocked 120-degree fields of view, while macro sensors began to disappear as high-resolution telephotos can crop in for close-ups. Canon’s 26-stop-range SPAD prototype suggests future telephotos will demand >95% light transmission, which pushes even more glass into lens stacks.

Higher element counts and prism assemblies lift telephoto module prices 40-50% above wide units, so suppliers such as Largan and Sunny Optical funnel capacity toward this richer mix. Each periscope lens requires 7-8 glass-plastic hybrid elements, raising both tooling complexity and yield risk. Prism alignment tolerances of 5 µm or less keep per-unit defect rates roughly 12-15 points above those of conventional modules, yet profit margins remain attractive because ASPs rise 18-22% when periscope zoom is added. Ultra-wide modules, bolstered by rectilinear algorithms, now feature free-form aspheric glass that costs 25-30% more than earlier plastic designs. Macro and depth functions consolidate into higher-resolution secondaries, trimming sensor counts while sustaining total lens revenue per phone.

By Lens Material: Glass-Plastic Hybrids Dominate Premium Tiers

Glass-plastic hybrids captured 58.01% of 2025 revenue, while the all-glass lens material segment is the fastest-growing, with a CAGR of 11.64%, indicating they will overtake all-plastic designs in smartphone camera lenses over the forecast period. Hybrid stacks mix two or three glass elements with four or five plastic ones, marrying chromatic-aberration control to weight savings. All-glass lenses remain confined to foldables and ultra-premium models because a seven-element glass stack weighs 15-20% more and costs up to 40% extra to build. All-plastic optics remain in sub-USD 200 devices, but their share erodes as mid-range makers tout hybrid upgrades to differentiate their cameras. Sunny Optical more than doubled hybrid-lens revenue in 1H 2025, as Huawei, OPPO, and vivo launched multi-element telephoto lenses.

Process capability is the swing factor. Precision glass molding from Largan achieves surface accuracy below 0.2 µm, an impossible level with plastics, ensuring MTF above 0.6 at 100 lp/mm for 200 MP sensors. New polymer formulas reduce thermal expansion from 70 ppm/°C to 50 ppm/°C, narrowing the focus-shift gap with glass, but not enough for periscope designs. Foldable phones also favor hybrids because plastic keeps hinge-side weight down, while glass stiffens the stack to withstand repeated folding. As AI imaging pushes transmission targets past 92%, hybrids become the default for mid- and high-end tiers, locking in their path to majority status in the smartphone camera lens market.

By Camera Position: Rear-Secondary Modules Gain Share

Rear-secondary lenses, ultra-wide, telephoto, macro, and depth expanded at an 8.26% CAGR, so their share of the smartphone camera lens market is rising faster than the rear-primary category. Rear-primary optics still held 46.64% share in 2025, but growth cooled as OEMs turned to specialized secondaries for product storytelling. Samsung’s Galaxy Z Fold6 featured a 4.9 mm-thick rear secondary array, proving that high-end optics can live in slim foldables. Under-display selfie cameras remain niche because the OLED layer blocks 20-30% of incoming light, but when adopted, they demand higher-grade glass to compensate for transmission loss. Ultra-wide lenses increasingly use free-form aspheres to keep corners sharp at 120-degree views, elevating module prices by about one-quarter.

Over the longer term, AI depth-mapping and AR applications favor multi-spectral capture, keeping two to three rear-secondary cameras on most flagships. Telephotos earn the highest ASP, while ultra-wides and macro-replacement sensors carry thinner margins yet ship in greater numbers. Front-facing modules feature 32 MP or 50 MP sensors with autofocus, but ASPs remain low because element counts remain under five. For suppliers, the balancing act is clear, chase premium-priced telephotos to expand margin, yet maintain volume in ultra-wide and selfie optics to keep factories loaded. Altogether, secondary demand secures a vital growth lane even as global smartphone units flatten.

By Manufacturing Process: Precision Glass Molding Leads Innovation

Plastic injection molding accounted for 61.52% in 2025, and wafer-level / hybrid optics manufacturing is growing at an 11.44% CAGR over the forecast period, giving it the largest share of the smartphone camera lens market among fabrication methods. Tungsten-carbide tooling presses molten glass above 600 °C to yield sub-0.2 µm surfaces, which enables aspheric and free-form geometries critical for periscope zoom and 200 MP sensors. Injection molding of plastic elements still dominates volume. Yet, cycle-time cuts from 45 s to 30 s only move the cost needle, not the performance ceiling. Glass compression molding offers cheaper, spherical parts for entry devices. Still, it cannot achieve the tolerances high-MP optics require, limiting its role to the value tier.

Yield remains the main bottleneck. Largan flagged variable-aperture reject rates 12-15 points above fixed-aperture norms and set a 2026 target to push below 10%. Genius Electronic Optical is adding Southeast Asian capacity that will come online in late 2026, reflecting industry urgency to expand glass-molding throughput. Meanwhile, LG Innotek relies on AI defect detection to cut plastic-lens scrap by 90%, shaving 12-15% off per-unit costs. These divergent strategies, premium precision versus volume efficiency, will coexist as long as handset makers keep segmenting cameras across flagship, mid-range, and entry lines.

By Smartphone Tier: Mid-Range Dominance Masks Flagship Acceleration

Mid-range models are expected to generate the fastest CAGR of 9.44% over the forecast period, and the segment accounted for 44.96% share in 2025. Yet flagships above USD 800 are forecast to grow 8.31% a year, outpacing every other tier because they bundle periscope, variable-aperture, and 100 MP sensors. These premium phones represent under 22% of units but almost half of lens revenue, given module bills of materials that run USD 80-100. Entry-level devices grow only 5.5% and rely on dual-camera all-plastic optics, limiting upside for suppliers chasing that volume. Thus, revenue and profit pools skew heavily toward the high end.

Flagship trickle-down is already reshaping the mid-tier. OPPO’s Reno13 Pro introduced periscope zoom around USD 500, while Xiaomi’s 17 Ultra uses a DSLR-style focus ring for content-creator appeal. As features migrate downward, the mid-range maintains volume leadership but increasingly relies on glass-plastic hybrids, raising average ASPs without matching flagship margins. Entry-level phones still cut costs by dropping depth sensors or downgrading lenses, so suppliers protect factory utilization but sacrifice profitability. Overall, tier dynamics confirm why strategic investment tilts toward cutting-edge optics even as the broader handset market matures.

Geography Analysis

Asia-Pacific retained 53.56% of 2025 revenue and is the fastest-growing region, with a CAGR of 9.22% over the forecast period, thanks to China’s dominance in lens fabrication and assembly, with Guangdong and Jiangsu provinces hosting the majority of global capacity. India’s Production-Linked Incentive scheme is redirecting camera module work to Tamil Nadu and Karnataka, trimming lead times for Apple and Samsung. Tata Electronics’ takeover of Wistron’s iPhone plant exemplifies this shift, accelerating the localization of lens and actuator sourcing. Vietnam is emerging as a secondary center as LG Innotek’s V3 expansion doubles local output.

South America is propelled by 5G rollouts and a rising preference for mobile video, averaging 9 GB per month. Chinese OEMs HONOR, OPPO, and vivo capture share in Brazil, Argentina, and Chile, where smartphones priced under USD 200 doubled shipments in 2024, yet a premium segment above USD 600 is also expanding. This bifurcation fuels lens demand for both cost-sensitive modules and high-margin hybrids.

North America and Europe together account for roughly one-third of global revenue but trail the worldwide growth rate at 6.5-7.0% CAGR because replacement cycles now exceed 3.5 years. Middle East and Africa collectively hold under 10% share; 5G network investments lift penetration, yet affordability keeps lens ASPs in the USD 8-12 range and supports mainly all-plastic designs. Currency volatility and tariffs in Nigeria and Egypt add further constraints.

Competitive Landscape

The market is highly concentrated: Largan Precision, Sunny Optical, and Samsung Electro-Mechanics account for roughly 55-60% of global lens shipments. Largan finished December 2025 with NTD 5.62 billion (USD 183 million) in revenue but cited variable-aperture yield as its top 2026 challenge. Sunny Optical generated RMB 38.29 billion (USD 5.27 billion) in 2024 revenue and revealed triple-digit hybrid-lens growth in early 2025. Samsung Electro-Mechanics leverages in-house actuator production to integrate folded zoom optics more tightly.

Second-tier firms are enlarging capacity. Genius Electronic Optical invested heavily in Southeast Asia plants scheduled for 2H 2026, seeking periscope and variable-aperture qualifications. AAC Technologies and Kantatsu, meanwhile, focus on precision glass molding to chase premium programs. White-space innovation includes metalens prototypes from MetaOptics that aim to flatten camera bumps below 3 mm, though commercialization is at least 3 years away. LG Innotek’s AI-enabled defect detection reduced rejects by 90%, offering a cost advantage that late entrants struggle to match.

Supply chain diversification continues. Luxshare Precision became Apple’s third folded-zoom OIS actuator source in October 2025, intensifying price pressure on Alps Alpine and Mitsumi Electric. Sharp exited entirely, selling its camera module unit to Foxconn affiliate FIT Hon Teng, underscoring margin compression in legacy segments. Export controls on precision optics tools, imposed by the United States in 2024, complicate Chinese capacity expansion but also spur domestic tooling development that could reshape long-term competitive dynamics.

Smartphone Camera Lens Industry Leaders

Largan Precision Co. Ltd.

Sunny Optical Technology (Group) Co. Ltd.

Samsung Electro-Mechanics Co. Ltd.

Genius Electronic Optical Co. Ltd.

AAC Technologies Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Largan Precision set a 2026 target to cut variable-aperture reject rates below 10%, funding new alignment metrology systems.

- December 2025: Largan Precision posted NTD 5.62 billion (USD 183 million) revenue, noting a 34% rise in periscope shipments.

- November 2025: Sony Semiconductor Solutions released its 200 MP LYT-901 sensor, now shipping in multiple flagships.

- November 2025: Genius Electronic Optical reported NTD 2.269 billion (USD 74 million) revenue, confirming plans for variable-aperture certification.

Global Smartphone Camera Lens Market Report Scope

The Smartphone Camera Lens Market comprises the global industry that designs, manufactures, integrates, and commercializes optical lens modules for smartphone camera systems. These lenses are critical components that capture, focus, and direct light onto image sensors, enabling functions such as photography, videography, zoom, low-light imaging, computational photography, and advanced imaging applications. The market encompasses a wide range of lens technologies, including wide/primary, ultra-wide, telephoto, macro, and other auxiliary lenses, as well as various lens materials and manufacturing processes developed to meet evolving smartphone imaging requirements.

The Smartphone Camera Lens Market Report is Segmented by Lens Technology (Wide/Primary, Ultra-Wide, Telephoto, Macro Lens and Other Auxiliary Lenses), Lens Material (All-Glass, All-Plastic, and Glass-Plastic Hybrid), Camera Position (Rear-Primary, Rear-Secondary, and Front-Facing), Manufacturing Process (Plastic Injection Molding, Precision Glass Molding, Wafer-Level/Hybrid Optics Manufacturing, and Other Manufacturing Process), Smartphone Tier (Flagship, Mid-Range, and Entry-Level), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Lens Technology

| Wide/Primary |

| Ultra-Wide |

| Telephoto |

| Macro Lens and Other Auxiliary Lenses |

By Lens Material

| All-Glass |

| All-Plastic |

| Glass-Plastic Hybrid |

By Camera Position

| Rear-Primary |

| Rear-Secondary |

| Front-Facing |

By Manufacturing Process

| Plastic Injection Molding |

| Precision Glass Moulding |

| Wafer-Level/Hybrid Optics Manufacturing |

| Other Manufacturing Process |

By Smartphone Tier

| Flagship |

| Mid-Range |

| Entry-Level |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Lens Technology | Wide/Primary | ||

| Ultra-Wide | |||

| Telephoto | |||

| Macro Lens and Other Auxiliary Lenses | |||

| By Lens Material | All-Glass | ||

| All-Plastic | |||

| Glass-Plastic Hybrid | |||

| By Camera Position | Rear-Primary | ||

| Rear-Secondary | |||

| Front-Facing | |||

| By Manufacturing Process | Plastic Injection Molding | ||

| Precision Glass Moulding | |||

| Wafer-Level/Hybrid Optics Manufacturing | |||

| Other Manufacturing Process | |||

| By Smartphone Tier | Flagship | ||

| Mid-Range | |||

| Entry-Level | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will worldwide revenue from smartphone camera lenses be by 2031?

It is projected to reach USD 5.36 billion, reflecting a 7.20% CAGR from 2026 to 2031.

Which lens technology is expanding the fastest?

Telephoto optics, driven by periscope zoom adoption, are advancing at an 9.40% CAGR.

What share does Asia-Pacific hold in global demand today?

The region commanded 53.56% of 2025 revenue owing to its dominant manufacturing base.

Why are glass-plastic hybrid lenses gaining popularity?

They combine glass clarity with plastic weight savings, offering 58.01% 2025 market share and superior aberration control.

Which manufacturing process leads the supply chain?

Plastic injection molding holds 61.52% share and supports the complex aspheric elements required for high-resolution sensors.

How concentrated is supplier power in this field?

The top three vendors provide about 55-60% of shipments, giving the market a high but not monopolistic concentration level.

Page last updated on: