High Density Polyethylene (HDPE) Bottle Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

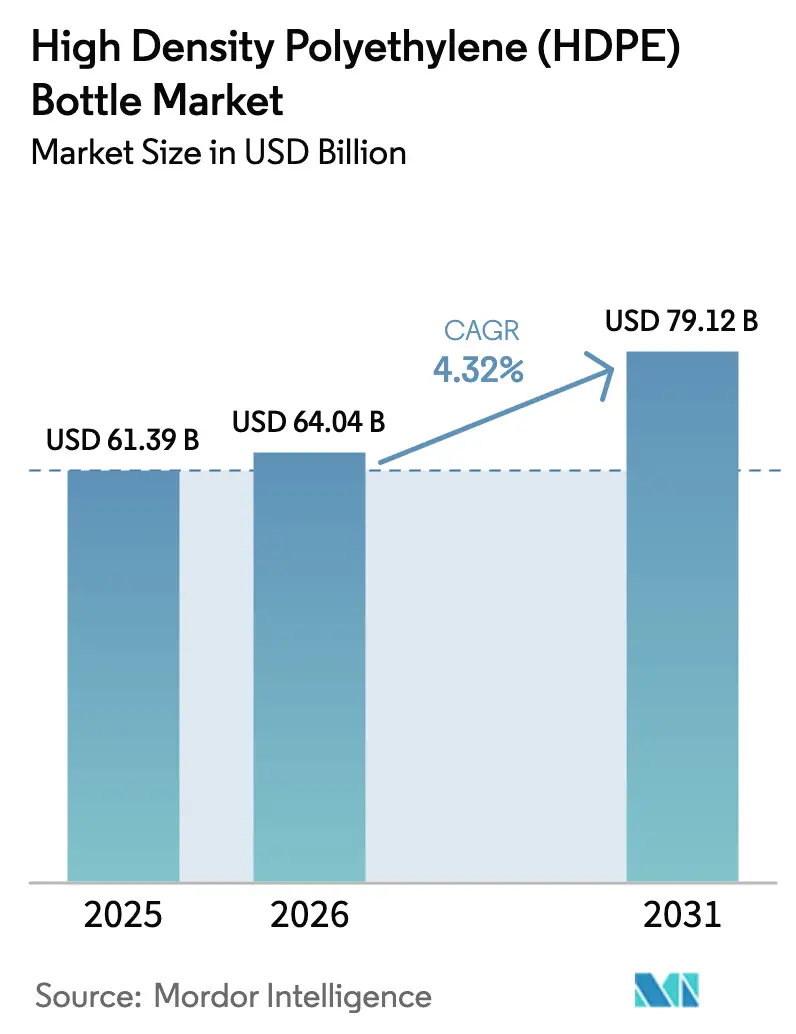

| Market Size (2026) | USD 64.04 Billion |

| Market Size (2031) | USD 79.12 Billion |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

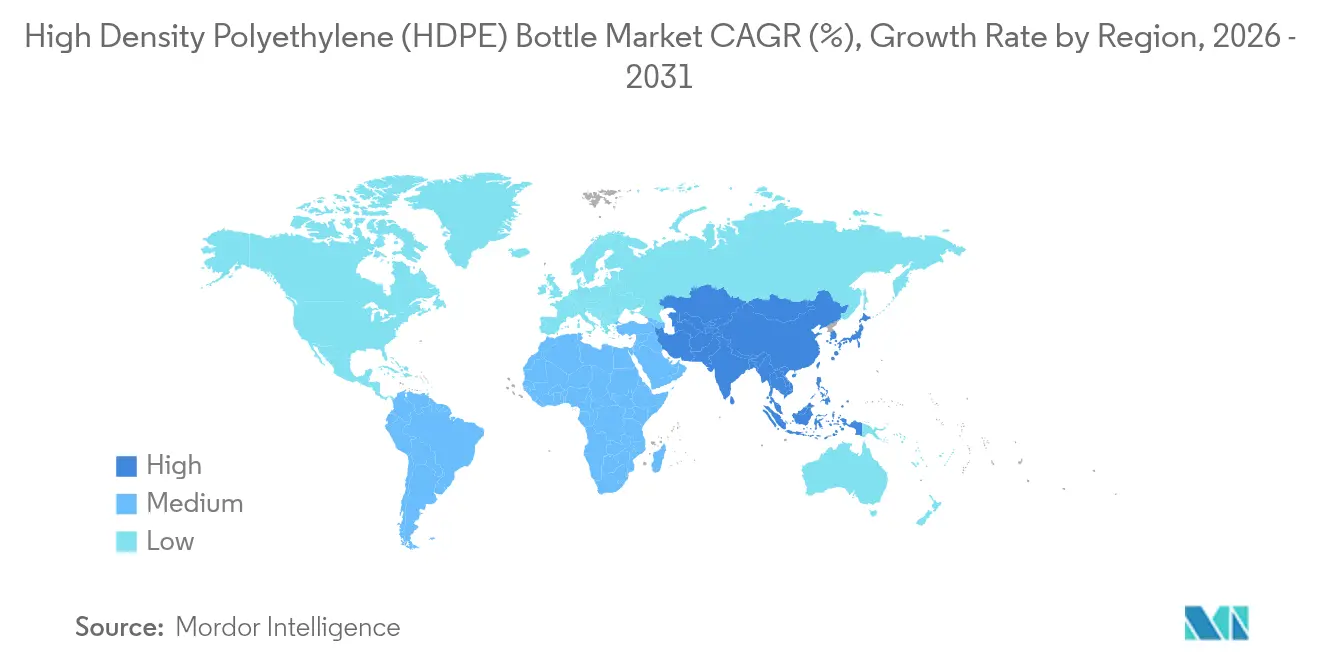

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Density Polyethylene (HDPE) Bottle Market Analysis by Mordor Intelligence

high-density polyethylene bottle market size in 2026 is estimated at USD 64.04 billion, growing from 2025 value of USD 61.39 billion with 2031 projections showing USD 79.12 billion, growing at 4.32% CAGR over 2026-2031. Rising demand for impact-resistant primary packaging in pharmaceuticals, household chemicals, and online grocery drives steady volume gains. Regulatory shifts such as the EU Single-Use Plastics Directive, which mandates tethered caps on beverage containers up to 3 liters, catalyze closure redesigns and lightweighting programs that trim material use and carbon footprint.[1]European Parliament, “Tethered bottle caps,” europarl.europa.eu Funding momentum in advanced recycling—illustrated by LyondellBasell’s long-term offtake deal for 24,000 tons of chemically recycled HDPE feedstock—supports brand targets for higher recycled content. Meanwhile, healthcare cold-chain expansion in emerging Asia sustains demand for sterile, low-temperature-tolerant containers.

Key Report Takeaways

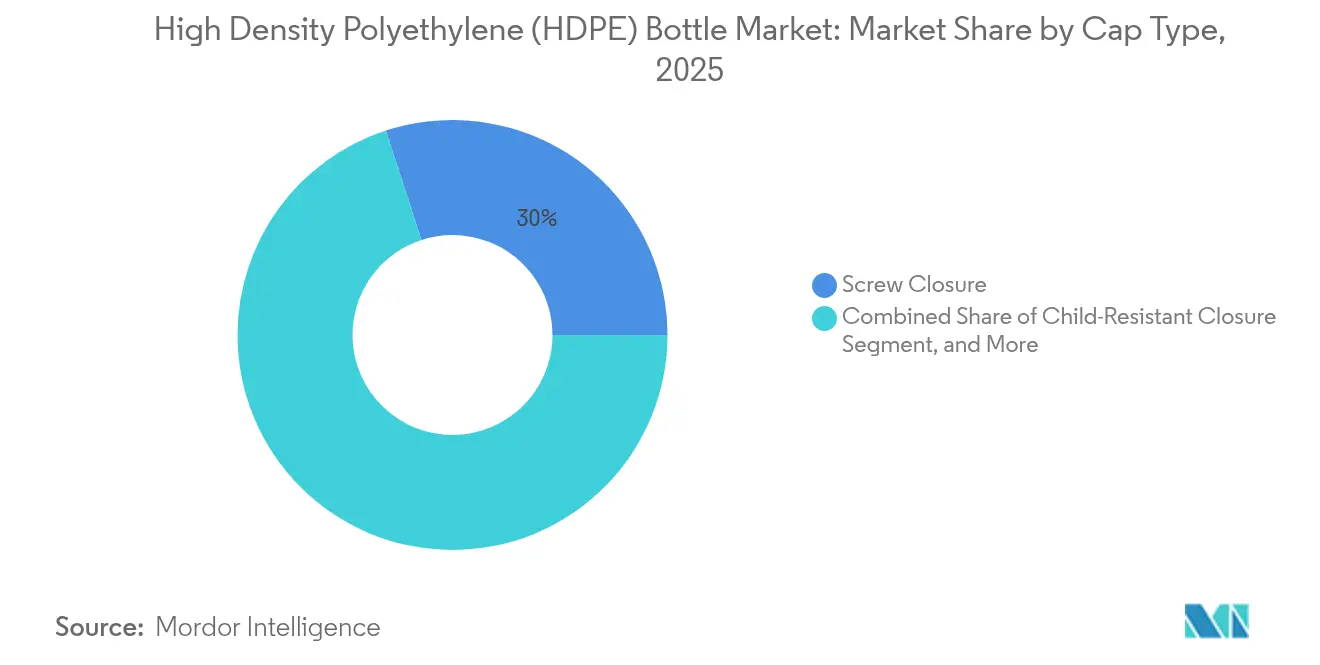

- By cap type, screw closures held 30.02% of high-density polyethylene bottle market share in 2025, while child-resistant closures are forecast to expand at a 6.48% CAGR through 2031.

- By bottle capacity, the 101–500 ml segment accounted for 30.05% share of the high-density polyethylene bottle market size in 2025; sub-30 ml formats are projected to grow at 7.28% CAGR to 2031.

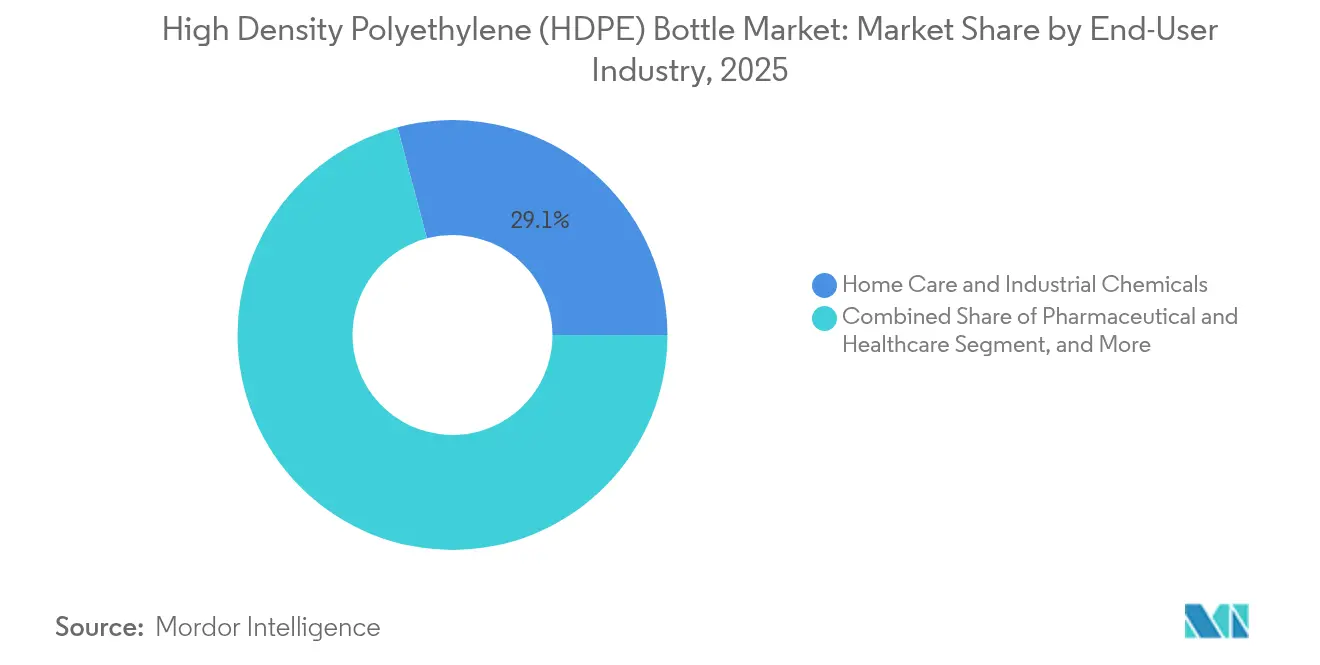

- By end-user industry, home care and industrial chemicals led with 29.12% revenue share in 2025, whereas pharmaceutical and healthcare packaging is advancing at a 7.42% CAGR through 2031.

- By resin source, virgin HDPE represented 67.98% of the high-density polyethylene bottle market size in 2025, while r-HDPE records the fastest CAGR at 5.62% between 2026 and 2031.

- By geography, North America commanded 34.20% of high-density polyethylene bottle market share in 2025; Asia-Pacific is projected to grow at 7.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High Density Polyethylene (HDPE) Bottle Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce-led SKU proliferation in food and beverage | +0.8% | Global; strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Rapid shift toward tethered and lightweight closures | +0.6% | EU core; UK and North America catching up | Short term (≤ 2 years) |

| Healthcare cold-chain expansion in emerging Asia | +0.9% | Asia-Pacific with spillover to MEA | Long term (≥ 4 years) |

| r-HDPE supply surge from chemical-recycling start-ups | +0.7% | North America and EU first movers | Medium term (2-4 years) |

| Next-generation high-barrier mono-material coatings | +0.5% | North America and EU; Asia-Pacific to follow | Long term (≥ 4 years) |

| AI-driven design-for-recyclability platforms | +0.4% | Early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce-led SKU proliferation in food and beverage

Online grocery growth fuels unprecedented SKU diversity, prompting beverage and condiment brands to launch smaller batches and multi-flavor variety packs that favor HDPE’s drop-resistance during parcel shipping. Warehouse automation and last-mile delivery require packaging that maximizes cube utilization, driving new high-stack strength bottle geometries. Material converters report rising inquiries for thin-wall HDPE bottles capable of withstanding five-foot drop tests. Equipment suppliers such as Yale Lift Truck Technologies have introduced ergonomic carts tailored to direct-store delivery, highlighting operational shifts triggered by SKU expansion. Brand owners moving contract filling in-house to manage rapid-fire product launches further reinforce baseline demand in the high-density polyethylene bottle market.

Rapid shift toward tethered and lightweight closures

The EU directive mandating tethered caps since July 2024 has pushed global beverage brands to standardize tethered designs on all lines to avoid dual tooling and regional SKUs. Berry Global has already supplied more than 400 million tethered lids to Coca-Cola, validating large-scale adoption . Lightweighting reduces resin consumption by nearly 39,000 tons per year across Europe, translating into 100,000 tons of CO₂ savings . US states such as California are preparing similar rules, accelerating North American line retrofits. This regulatory cascade boosts closure system revenue in the high-density polyethylene bottle market.

Healthcare cold-chain expansion in emerging Asia

Government incentives in South Korea, Singapore, India, and China are scaling up mRNA and biologics production, raising demand for sterile HDPE bottles that tolerate -80 °C storage without brittleness . DHL’s EUR 2 billion spend on GDP-certified pharma hubs, with a quarter allocated to Asia-Pacific, signals logistics capacity that underpins future volume.[2]DHL Group, “Invest EUR 2 billion in DHL Health Logistics,” group.dhl.comLocal regulators are harmonizing inspection protocols, shortening approval times and stimulating earlier packaging orders. The trend reinforces long-run growth in the high-density polyethylene bottle market.

r-HDPE supply surge from chemical-recycling start-ups

Advanced recycling facilities convert mixed polyolefin waste into near-virgin feedstock, easing historical quality bottlenecks in post-consumer resin. LyondellBasell’s offtake agreement with Nexus Circular secures 24,000 tons of recycled HDPE annually, guaranteeing supply for premium applications. Borealis is adding a compounding line using Borcycle M technology that turns scrap flakes into high-performance pellets. As brand-owner recycled-content pledges intensify, chemically recycled resin mitigates ESCR challenges and supports pricing premiums in the high-density polyethylene bottle market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PET up-trading in Latin-American dairy and juice | -0.3% | Brazil and Mexico focus | Medium term (2-4 years) |

| Tightening microplastic legislation in EU and California | -0.5% | EU and select US states | Short term (≤ 2 years) |

| Post-consumer r-HDPE ESCR failure limiting reuse loops | -0.4% | Higher impact in developed markets | Long term (≥ 4 years) |

| Logistics inflation squeezing low-margin mass segments | -0.6% | Global; acute in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening microplastic legislation in EU and California

REACH Regulation (EU) 2023/2055 restricts synthetic polymer microparticles above 0.01 % w/w in consumer products, pressuring HDPE bottle makers to audit masterbatches and pigments. The European Commission also proposes pellet-loss rules requiring risk-management plans for facilities handling 5 tons or more each year. California’s attempted mirror law signals likely US spillover even after AB 234’s failure, keeping compliance teams on alert . Certification, sampling, and reformulation costs weigh on margins across the high-density polyethylene bottle market.

Post-consumer r-HDPE ESCR failure limiting reuse loops

Academic studies show recycled HDPE’s environmental stress crack resistance diminishes when exposed to surfactants, raising failure risk in refill and reuse programs. Molecular degradation during repeated melt-processing shifts weight-average molecular mass and crystallinity, compounding brittleness. While chain-branching additives partially restore toughness, variability in curbside feedstock still deters adoption for high-stress applications. Reliability issues temper recycled content uptake within the high-density polyethylene bottle market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cap Type: Child-Resistant Innovation Drives Growth

Child-resistant closures secure a 6.48% CAGR to 2031 as pharmaceutical safety rules tighten and legalized cannabis channels expand. Screw caps nevertheless retained 30.02% of high-density polyethylene bottle market share in 2025, anchoring mainstream beverages and pantry staples. Snap and flip-top formats dominate quick-access personal care and condiment uses, while trigger sprayers cater to cleaning agents that exploit HDPE’s chemical resistance.

Designers integrate tethered features into child-resistant lines to comply with EU directives without sacrificing elder usability. Digital watermarking embedded in closure skirts assists sorting in optical recycling systems. The high-density polyethylene bottle market benefits from broader tooling orders as converters re-platform entire closure portfolios to future-proof against emerging mandates.

By Bottle Capacity: Small-Format Surge

The < 30 ml niche posts a 7.28% CAGR, propelled by ophthalmic therapies, fragrance samplers, and e-commerce travel kits. In contrast, the 101–500 ml band maintains 30.05% of the high-density polyethylene bottle market size in 2025, underpinned by household cleaners and table sauces. Mid-range 31–100 ml bottles address over-the-counter medicines, while 501 ml–1 L serves dairy, juice, and ready-to-drink tea. Formats above 1 L remain entrenched in bulk automotive fluids and institutional detergents.

TekniPlex Healthcare recently expanded injection-blow capacity for 5–30 ml ophthalmic bottles, illustrating capital shifts toward miniature formats. Online retailers prefer small bottles for higher revenue-to-weight ratios and lower dimensional weight charges. As fulfillment centers automate singulation processes, cube-optimized small bottles solidify their role in the high-density polyethylene bottle market.

By End-User Industry: Healthcare Transformation

Home care and industrial chemicals captured 29.12% share in 2025 because HDPE withstands acids, bleach, and surfactants. Nonetheless, pharmaceutical and healthcare applications top growth tables at 7.42% CAGR owing to biologics, specialty generics, and vaccine rollouts. Food and beverage brands value HDPE’s drop strength for refrigerated dairy, while personal-care marketers exploit its moisture barrier in bath and body lines.

Cold-chain drug protocols require thicker walls and tamper rings designed for -80 °C transit, commanding price premiums and raising the high-density polyethylene bottle market size per unit. Smart labels for temperature excursion logging are increasingly molded into pharma-grade bottles. Industrial chemicals remain price sensitive, but specification creep toward post-consumer content opens substitution space for r-HDPE grades with enhanced ESCR.

By Resin Source: Recycled Content Momentum

Virgin material retained 67.98% share in 2025, reflecting reliability needs in regulated drugs and food. Recycled resin logs a 5.62% CAGR through 2031 as chemical recycling output scales. Borealis and LyondellBasell investments accelerate availability of near-virgin quality pellets, enabling 20 %–30 % post-consumer blends in household cleaner bottles without crack failures.

Price spreads between r-HDPE and virgin peaked at USD 750–800 per ton in early 2025 as milk-jug collection volumes tightened. Chemical recycling dilutes these premiums and stabilizes supply, encouraging brand mandates that the high-density polyethylene bottle market adopt recycled-content baselines.

Geography Analysis

North America generated 34.20% of high-density polyethylene bottle market share in 2025 on the back of FDA-compliant pharma packaging and durable e-commerce supply chains. Logistics re-shoring to Mexico cuts lead times, with US converters installing extrusion-blow lines near border states. California’s draft tethered-cap rule signals regulatory convergence with Europe, nudging closure upgrades across the continent.

Europe remains technology leader, incubating tethered closures and advanced recycling pilots spawned by the Single-Use Plastics Directive. Berry Global’s 400 million-unit rollout to Coca-Cola underscores industrial scale. REACH microplastic limits and stricter food-contact rules effective March 2025 raise compliance bars, prompting continuous process audits that favor established players.

Asia-Pacific posts the highest CAGR at 7.75% as governments bankroll biologics clusters and cold-chain nodes. DHL’s multi-hub logistics spend accelerates infrastructure, while local regulators crack down on counterfeit drugs, boosting serialization-ready HDPE bottles. Rising middle-class incomes also spur premium personal-care formats, amplifying unit demand in the high-density polyethylene bottle market.

Competitive Landscape

The market shows fragmentation. Amcor’s USD 8.43 billion all-stock combination with Berry Global forms a packaging giant with USD 24 billion annual revenue and a USD 650 million synergy target.[3]Amcor, “Amcor and Berry to combine,” amcor.com Silgan Holdings deepened its dispensing portfolio by acquiring Weener Packaging for EUR 838 million .

Chemical recyclers partner with resin majors to secure feedstock pipelines; LyondellBasell’s stake in Alterra accelerates pilot commercialization . Equipment innovation centers on all-electric extrusion-blow platforms that cut energy use 30%, appealing to ESG scorecards. Proprietary materials like ExxonMobil’s unimodal Paxon™ grade raise ESCR by 25%, letting converters hike recycled-content percentages without performance loss .

AI-enabled design hubs differentiate suppliers able to compress development cycles from 18 months to 6 months. Converters that secure APR Design® recognition for recyclability gain preferred-supplier status with mass merchants, tightening competitive pressure on legacy bottle shapes . Overall, strategic focus converges on circular-ready materials, smart closures, and regional supply resilience, sustaining investment flows in the high-density polyethylene bottle industry.

High Density Polyethylene (HDPE) Bottle Industry Leaders

Amcor Group

Silgan Holdings Inc.

Graham Packaging Company

Canyon Plastics Inc.

Plastipak Packaging

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Novolex completed a USD 6.7 billion merger with Pactiv Evergreen, creating a leading manufacturer in food and specialty packaging.

- April 2025: DHL Group announced a EUR 2 billion investment to expand GDP-certified pharma hubs and cold-chain capacity, allocating 25% to Asia-Pacific.

- January 2025: Amcor completed its USD 8.43 billion merger with Berry Global, creating a global leader in consumer and healthcare packaging solutions, with projected USD 650 million in annual synergies.

- January 2025: LyondellBasell acquired a 50% share in a Dutch recycling firm and secured 24,000 tons of recycled feedstock annually via Nexus Circular, advancing circularity goals.

Global High Density Polyethylene (HDPE) Bottle Market Report Scope

High-Density Polyethylene (HDPE) is characterized by its high tensile strength, which makes HDPE bottles resistant to cracking, breaking, and puncturing. This durability renders them suitable for a wide range of products, particularly for packaging items that require enhanced protection during transportation and handling. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The high density polyethylene (HDPE) bottle market is segmented by cap type (Screw Closure, Snap Closure, Push-Pull Closure, Disc Top Closure, Spray Closure and Other Cap Types), by bottle capacity (Less than 30 Ml, 31 Ml - 100 Ml, 101 Ml - 500 Ml, Above 500 Ml), by end-user industry (Food & Beverage, Chemical, Pharmaceutical, Cosmetic & Personal Care and Other End-Use Industries) and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa), The market sizing and forecasts are provided in terms of value (USD) for all the above segments.

| Screw Closure |

| Snap Closure |

| Disc-Top Closure |

| Spray / Trigger Closure |

| Flip-Top Closure |

| Child-Resistant Closure |

| < 30 ml |

| 31 – 100 ml |

| 101 – 500 ml |

| 501 ml – 1 L |

| > 1 L |

| Food and Beverage |

| Pharmaceutical and Healthcare |

| Home Care and Industrial Chemicals |

| Cosmetic and Personal Care |

| Automotive and Lubricants |

| Other End-user Industry |

| Virgin HDPE |

| Recycled (r-HDPE) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Cap Type | Screw Closure | ||

| Snap Closure | |||

| Disc-Top Closure | |||

| Spray / Trigger Closure | |||

| Flip-Top Closure | |||

| Child-Resistant Closure | |||

| By Bottle Capacity | < 30 ml | ||

| 31 – 100 ml | |||

| 101 – 500 ml | |||

| 501 ml – 1 L | |||

| > 1 L | |||

| By End-User Industry | Food and Beverage | ||

| Pharmaceutical and Healthcare | |||

| Home Care and Industrial Chemicals | |||

| Cosmetic and Personal Care | |||

| Automotive and Lubricants | |||

| Other End-user Industry | |||

| By Resin Source | Virgin HDPE | ||

| Recycled (r-HDPE) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the high-density polyethylene bottle market?

The high-density polyethylene bottle market size is USD 64.04 billion in 2026.

Which region leads the market?

North America led with 34.20% high-density polyethylene bottle market share in 2025

Which application segment is growing fastest?

Pharmaceutical and healthcare packaging is expanding at a 7.42% CAGR through 2031.

How are regulations influencing closure design?

EU tethered-cap mandates effective 2024 are driving global adoption of lightweight, tethered closures across beverage lines.

What role does recycled HDPE play in future growth?

Chemically recycled r-HDPE is forecast to grow at 5.62% CAGR as investments secure high-quality feedstock for brand sustainability commitments.

Why are < 30 ml bottles important?

Small formats show the strongest 7.28% CAGR due to precision-dosing drugs and travel-size personal care items favored in e-commerce channels.

Page last updated on: