Mixed Tocopherols Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

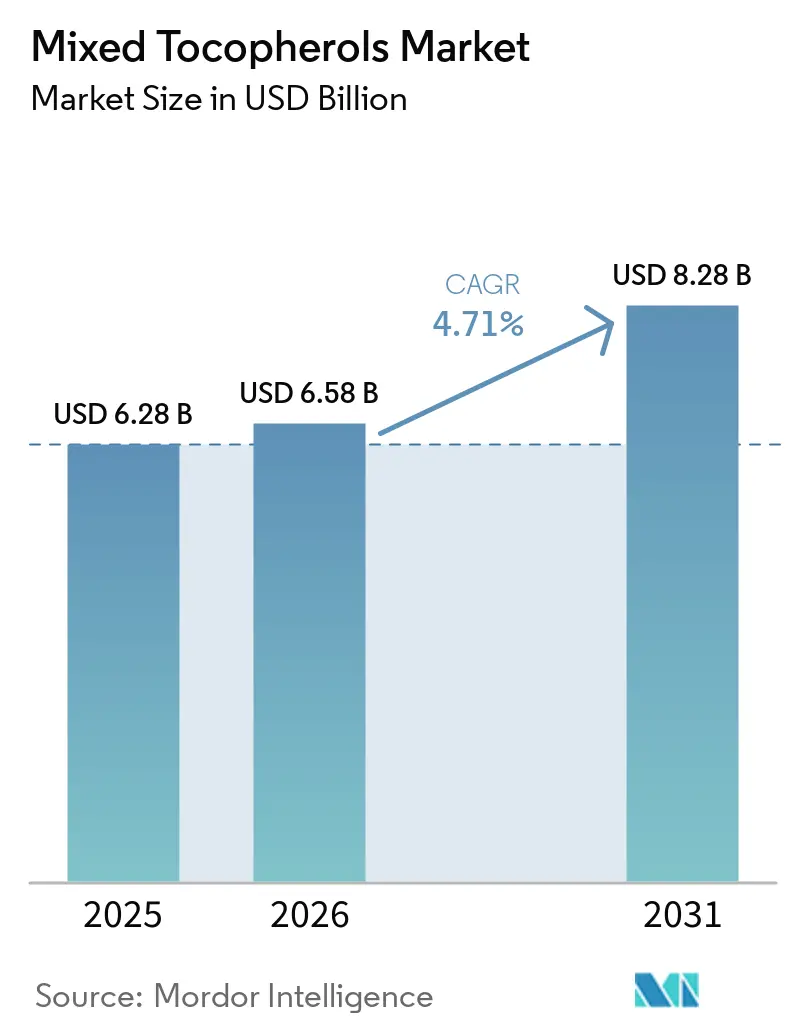

| Market Size (2026) | USD 6.58 Billion |

| Market Size (2031) | USD 8.28 Billion |

| Growth Rate (2026 - 2031) | 4.71% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mixed Tocopherols Market Analysis by Mordor Intelligence

The mixed tocopherols market size is projected to expand from USD 6.28 billion in 2025 and USD 6.58 billion in 2026 to USD 8.28 billion by 2031, registering a CAGR of 4.71% between 2026 and 2031. Stricter regulatory reviews of synthetic antioxidants by the United States and the European Union, expected in early 2026, are driving food, supplement, and cosmetics brands to adopt naturally sourced tocopherols. This shift is further supported by the heightened scrutiny of synthetic antioxidants by the U.S. Food and Drug Administration (FDA) in February 2026, which is accelerating substitution toward natural tocopherols that carry GRAS status, widening the addressable pool of clean-label reformulations [1]Source: European Food Safety Authority Journal, "Scientific Opinion on the re-evaluation of tocopherol-rich extract," efsa.onlinelibrary.wiley.com. However, fluctuations in feedstock prices remain a significant challenge for the market. The increasing clinical evidence highlighting gamma-rich tocopherol's ability to reduce inflammatory pathways is expanding opportunities in the nutraceutical segment, particularly in the Asia-Pacific region, where the adoption of vitamin E supplements is accelerating. In the personal care sector, advancements in encapsulation technology have enhanced the stability of alpha-rich tocopherol under high temperatures and ultraviolet exposure.

Key Report Takeaways

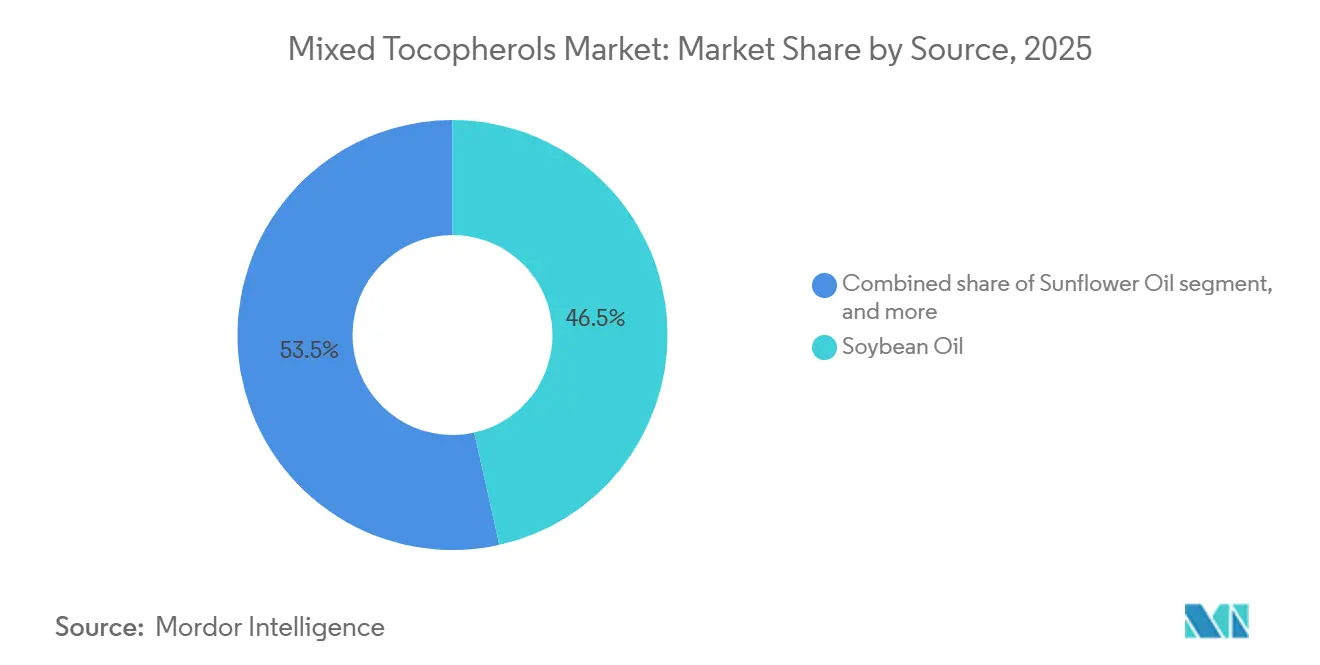

- By source, soybean oil held 46.51% of the mixed tocopherols market share in 2025, while sunflower oil is forecast to expand at a 6.18% CAGR through 2031.

- By compound, alpha-rich tocopherols captured 43.19% share in 2025, whereas gamma-rich variants are projected to advance at a 7.52% CAGR between 2026 and 2031.

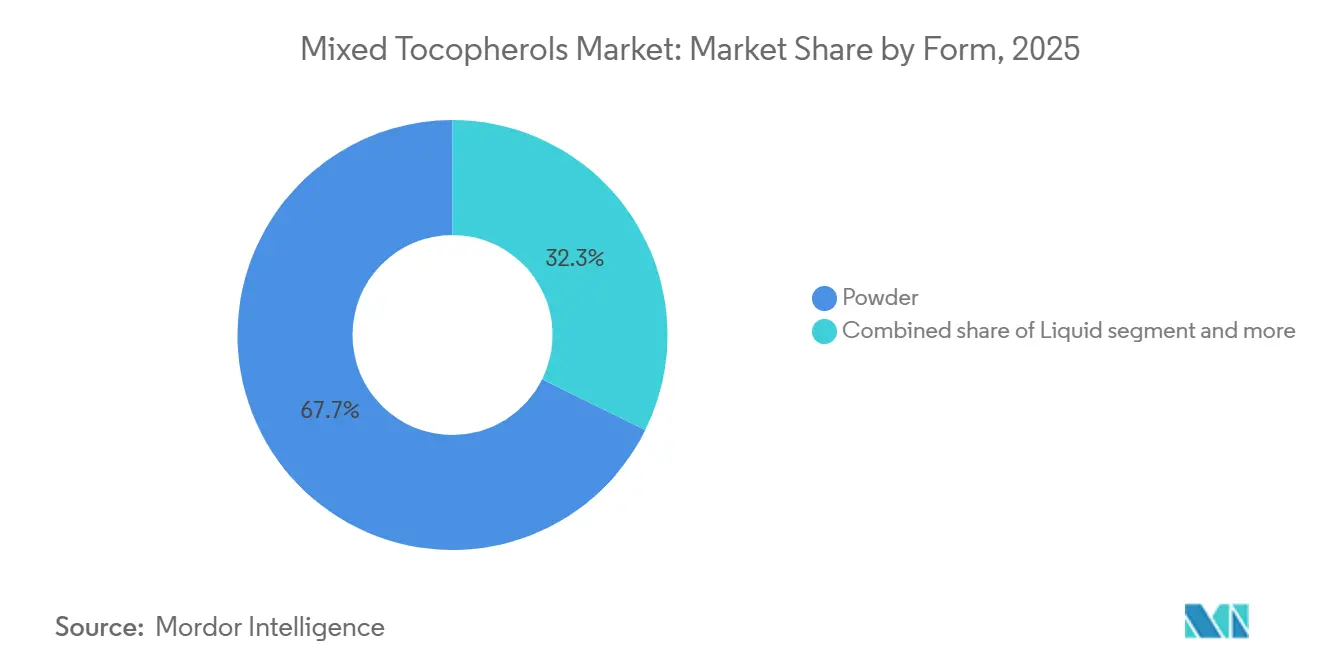

- By form, powder accounted for 67.64% share of the mixed tocopherols market in 2025; liquid formulations recorded the fastest 6.86% CAGR between 2026 and 2031.

- By application, food and beverages led with 41.77% revenue share in 2025, while cosmetics and personal care recorded the highest projected 8.35% CAGR through 2031.

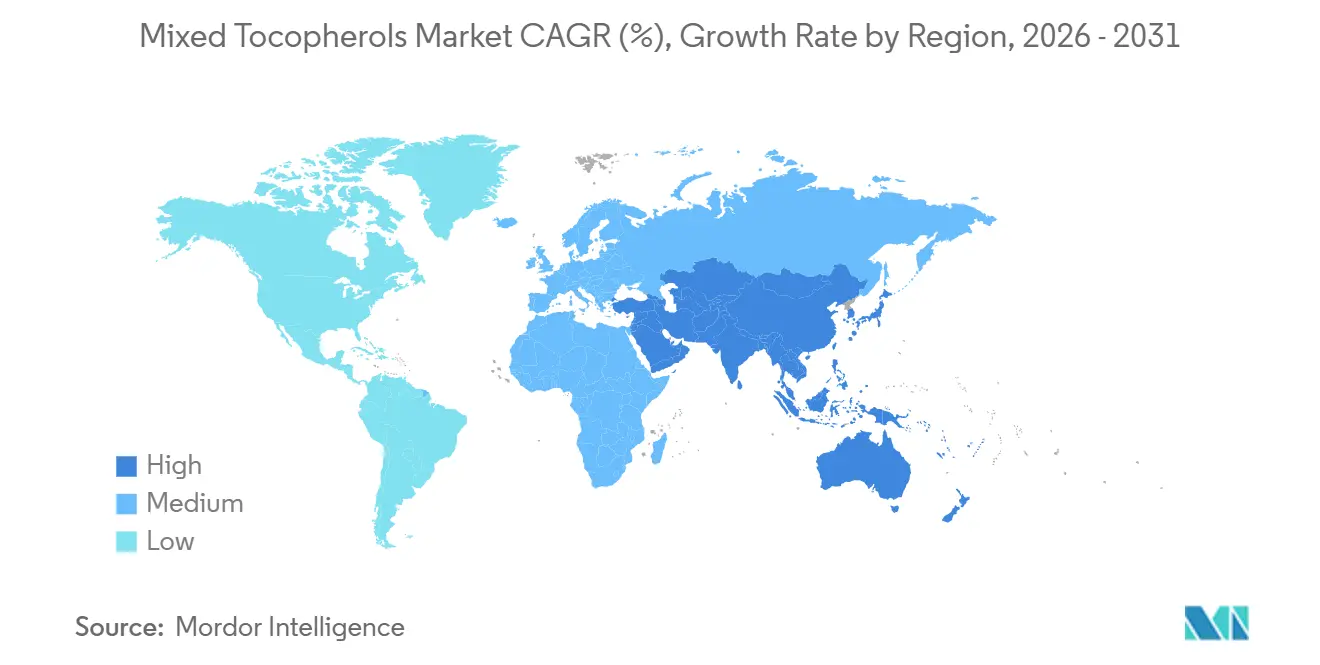

- By geography, North America accounted for 33.04% of the mixed tocopherols market in 2025, whereas Asia-Pacific is set to register the fastest 5.68% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mixed Tocopherols Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for natural antioxidant preservatives in processed and functional foods | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rising health-conscious consumer preference for vitamin-E fortified dietary supplements | +0.9% | Global, strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| Increasing preference for plant-based and non-synthetic additives | +0.8% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Regulatory shift away from BHA/BHT increasing natural-tocopherol uptake | +1.1% | North America and Europe, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Surplus soybean distillate valorization lowering cost curves | +0.5% | North America, South America (Brazil, Argentina) | Medium term (2-4 years) |

| Expanding applications in cosmetics and personal care | +0.7% | Global, fastest in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for natural antioxidant preservatives in processed and functional foods

Formulators incorporate tocopherols into bakery products, processed meats, and edible oils at concentrations up to 1,000 ppm to enhance shelf life while meeting clean-label requirements without E-numbers. Blends containing alpha-, gamma-, and delta-homologs demonstrate superior performance in lipid oxidation assays compared to a single alpha-rich tocopherol. This is due to the ability of gamma- and delta-species to regenerate alpha-radicals, thereby restoring antioxidant capacity. Regulatory frameworks support this shift, with the U.S. Food and Drug Administration permitting up to 300 ppb across most food categories and EFSA maintaining positive safety opinions for E306-E309, enabling multinational companies to transition seamlessly [2]Source: European Food Safety Authority Journal, "Scientific Opinion on the re-evaluation of tocopherol-rich extract," efsa.onlinelibrary.wiley.com. Combining tocopherols with ascorbic acid or rosemary extract provides additive protection, particularly in high-moisture ready-meal lines where fat oxidation accelerates under modified-atmosphere packaging. This layered approach not only extends product shelf life but also aligns with consumer demand for natural and clean-label solutions.

Rising health-conscious consumer preference for vitamin-E fortified dietary supplements

Rising health-conscious consumer preferences are driving demand for vitamin E-fortified dietary supplements, particularly in North America, Europe, and the Asia-Pacific. Consumers are increasingly aware of vitamin E's role in supporting immune, skin, and cardiovascular health, leading to a surge in the adoption of tocopherol-based supplements. The growing trend of preventive healthcare and the rising prevalence of lifestyle-related diseases, such as diabetes and hypertension, are further fueling this demand. Additionally, the aging population is seeking supplements to address age-related oxidative stress and maintain overall vitality, creating a robust market for vitamin E-enriched products. Manufacturers are responding to this trend by introducing innovative formulations, such as gamma-rich tocopherol blends and water-soluble vitamin E, to cater to diverse consumer needs.

Regulatory shift away from BHA/BHT increasing natural-tocopherol uptake

The global shift in regulatory frameworks is significantly influencing the adoption of natural tocopherols, particularly as food safety authorities move away from synthetic antioxidants like BHA and BHT. In January 2026, the European Food Safety Authority (EFSA) introduced stricter guidelines, reducing acceptable daily intake levels for synthetic phenolic antioxidants, accelerating the shift toward tocopherols because food and beverage companies need a safer, cleaner-label oxidation-control solution [3]Source: European Commission, "Additives - Food Safety - European Commission," food.ec.europa.eu. Similarly, the U.S. Food and Drug Administration (FDA) has intensified scrutiny of synthetic food additives. These regulatory changes are prompting manufacturers in the processed and packaged food industry to reformulate their products, replacing synthetic antioxidants with natural tocopherol blends. For instance, snack and confectionery producers in North America and Europe are increasingly incorporating mixed tocopherols at 200-400 ppm to ensure oxidative stability while meeting clean-label requirements. This trend is further supported by consumer preferences for natural, minimally processed ingredients, which are driving the uptake of tocopherols as a safer, more sustainable alternative.

Expanding applications in cosmetics and personal care

The cosmetics and personal care industry is increasingly incorporating tocopherols and tocotrienols into formulations due to their potent antioxidant properties, which help combat oxidative stress and improve skin elasticity. Tocotrienol-rich fractions, abundant in palm and rice-bran distillates, are gaining traction for their superior inhibition, signaling, and reduction of vascular cell adhesion molecule-1, positioning them as premium actives in anti-inflammatory and barrier-repair products. Nanostructured lipid carriers and beta-cyclodextrin complexation improve dermal retention and photostability, addressing the compound's sensitivity to ultraviolet light and oxygen. Advanced encapsulation technologies have further enhanced the stability of alpha-tocopherol, enabling its use in high-temperature and UV-exposed environments. This has unlocked opportunities for innovative product formats, such as serums, moisturizers, and sunscreens, that deliver measurable hydration and anti-aging benefits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing price volatility of vegetable-oil distillates | -0.9% | Global, acute in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Strict regulatory requirements and complex EU and US labeling/claim compliance | -0.6% | North America and Europe | Medium term (2-4 years) |

| Supply-chain disruptions for high-purity delta-tocopherol fractionation | -0.4% | Global, concentrated in Europe and North America | Medium term (2-4 years) |

| Risk of mycotoxin co-contamination in rapeseed distillates | -0.5% | Europe, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing price volatility of vegetable-oil distillates

The Food and Agriculture Organization Vegetable Oil Price Index surged 5.1% to 183.1 points in March 2026, driven by Indonesian palm-oil export restrictions, Ukrainian sunflower-crop shortfalls, and biofuel-mandate absorption of soybean and rapeseed volume. These factors have significantly impacted the availability and pricing of key feedstocks for tocopherol production. Deodorizer-distillate spot prices, which closely track crude-oil quotations with a 3- to 6-month lag, have led to substantial margin compression for tocopherol producers, particularly those without long-term feedstock contracts. Additionally, biofuel mandates in the EU and the United States are diverting soybean and rapeseed oil into biodiesel and renewable diesel production, further tightening the supply of deodorizer distillates and driving up costs. Smaller tocopherol producers, especially those without captive crushing operations, face heightened working-capital challenges as distillate costs fluctuate unpredictably.

Supply-chain disruptions for high-purity delta-tocopherol fractionation

Supply-chain disruptions for high-purity delta-tocopherol fractionation can significantly impact the availability of consistent raw feedstock. Production relies on specialized oil-derived concentrates and tightly controlled purification processes. When feedstock supply becomes volatile or import-dependent, manufacturers encounter delays, increased costs, and inconsistent output quality, complicating the procurement of reliable, high-purity fractions. Delta-tocopherol, which constitutes only 1-3% of typical soybean and rapeseed distillates, offers the highest antioxidant activity in lipid systems due to its unsubstituted aromatic ring. However, its fractionation demands capital-intensive processing and efficient logistics. Any disruption in sourcing, transportation, or refining can quickly affect production schedules. Consequently, buyers may opt for more readily available tocopherol grades, while producers of high-purity delta fractions face challenges related to margin pressures and supply stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Sunflower Gains on Superior Tocopherol Density

Soybean oil accounted for 46.51% of the Mixed Tocopherols Market in 2025, underscoring its dominance as the most-crushed oilseed globally and the primary source of deodorizer distillate. This abundance ensures a steady supply of raw materials for tocopherol extraction. However, sunflower oil is emerging as a significant competitor, projected to grow at a robust CAGR of 6.18% through 2031, the fastest among all sources. Sunflower oil has a tocopherol content of 150-957 mg/kg, significantly higher than that of soybean or rapeseed oil. Its deodorizer distillates can be enriched by molecular distillation, reducing downstream purification costs and enhancing its appeal for high-value applications.

Cold-pressed sunflower oils retain approximately 729 mg/kg of tocopherols, compared to 645 mg/kg in refined grades, creating a premium-quality tier increasingly leveraged by supplement and cosmetics brands targeting health-conscious consumers. Rapeseed oil, on the other hand, offers gamma-rich and delta-rich tocopherol profiles, which are particularly valued for their anti-inflammatory properties and applications in nutraceuticals. Corn oil and palm oil cater to cost-sensitive segments, primarily in food preservation, where mixed-tocopherol blends are sufficient to meet functional requirements.

By Compound: Gamma-Rich Variants Capture Anti-Inflammatory Premium

Alpha-rich tocopherols held 43.19% of the market share in 2025, anchored by their dominance in dietary supplements and cosmetics. Alpha-tocopherols are highly bioavailable due to their preferential binding to alpha-tocopherol transfer protein, making them a preferred choice for addressing oxidative stress and supporting immune health. In the cosmetics sector, alpha-tocopherol is widely used for its skin-repairing and anti-aging properties, as it helps neutralize free radicals and improve skin elasticity. Advancements in encapsulation technologies have enhanced the stability of alpha-tocopherols, enabling their incorporation into high-performance skincare formulations.

Gamma-rich tocopherols are expanding at 7.52% CAGR through 2031, the fastest among all compound types, propelled by clinical evidence that gamma-tocopherol scavenges reactive nitrogen species, inhibits cyclooxygenase-2 and 5-lipoxygenase, and reduces leukotriene B4 formation in leukocytes. This mechanistic differentiation is driving formulators to layer gamma-rich concentrates into cardiovascular and joint-health supplements, where anti-inflammatory positioning commands price premiums over generic vitamin E. Delta-rich tocopherols exhibit the highest antioxidant activity in lipid systems due to their unsubstituted aromatic ring, yet supply constraints limit adoption to premium cosmetics and pharmaceutical applications.

By Form: Powder Dominates on Stability and Handling

Powder formulations accounted for 67.64% of the Mixed Tocopherols Market in 2025, driven by their compatibility with dry-mix supplements, infant formula, and bakery premixes, where moisture-sensitive actives cannot tolerate liquid carriers. Spray-drying and freeze-drying encapsulation efficiency, with freeze-dried powders retaining higher tocopherol bioactivity but incurring higher processing costs. The powder segment's dominance reflects downstream customers' preference for stable, easy-to-handle ingredients that minimize formulation risk and extend product shelf life, particularly in tropical and subtropical markets where ambient temperatures accelerate oxidative degradation.

Liquid forms are expanding at a 6.86% CAGR through 2031, driven by their versatility in applications such as functional beverages, gummies, and liquid dietary supplements. Their ease of incorporation into emulsions and liquid matrices makes them particularly attractive for ready-to-drink products and fortified beverages. Additionally, advancements in solubilization technologies, such as micelle encapsulation and nanoemulsions, have enhanced the bioavailability of liquid tocopherols, further boosting their adoption.

By Application: Cosmetics Outpaces Food on Premium Positioning

Food and beverage applications captured 41.77% of the market share in 2025, driven by the growing demand for natural antioxidants in processed meats, baked goods, and edible oils. Tocopherols play a critical role in extending shelf life while meeting clean-label requirements, which consumers increasingly prioritize. The rising trend of fortified foods and beverages is further boosting the adoption of tocopherols in this segment. The ability of tocopherols to stabilize fats and oils without altering taste or texture makes them a preferred choice for manufacturers aiming to enhance product quality and longevity.

The cosmetics and personal care segment is projected to grow at a robust 8.35% CAGR through 2031, the fastest among all application segments. This growth is fueled by clinical evidence demonstrating that topical α-tocopherol improves skin hydration and elasticity and reduces UV-induced erythema. Advanced encapsulation technologies, such as liposomal delivery systems, have enhanced the stability and efficacy of tocopherols in cosmetic formulations, enabling their use in high-performance skincare products. Furthermore, the Asia-Pacific region is witnessing a surge in nutricosmetics that combine oral gamma-tocopherol with topical alpha-tocopherol, leveraging systemic supplementation to strengthen dermal antioxidant defenses.

Geography Analysis

North America held 33.04% of the Mixed Tocopherols Market in 2025, anchored by integrated oilseed processors such as Archer Daniels Midland and Cargill that embed tocopherol recovery into soybean and corn crushing operations, and by the FDA’s BHA reassessment, which catalyzed rapid snack-food reformulation. Canada and Mexico contribute through canola (rapeseed) distillate exports and maquiladora-based encapsulation of supplements, respectively. The region's mature regulatory framework, such as GRAS status under 21 CFR, and established health-claim pathways, reduces compliance friction, yet strict labeling requirements for organic and non-GMO certifications add to procurement costs.

Asia-Pacific is expanding at a 5.68% CAGR through 2031, the fastest among all regions, driven by rising dietary-supplement penetration in China and India, clean-label mandates, and the production of tocotrienol-rich palm derivatives in Malaysia and Indonesia. Wilmar's February 2026 acquisition of Natural Oleochemicals for USD 192 million consolidated Malaysian palm-distillate capacity, positioning the company to serve Southeast Asian and Middle Eastern markets with shorter lead times. Japan and Australia enforce stringent mycotoxin limits, favoring sunflower and soybean distillates over rapeseed, while India's supplement market is adopting gamma-rich tocopherols for cardiovascular and joint-health positioning.

Europe is growing, constrained by the region's structural rapeseed deficit, 18.5-18.8 million tonnes of domestic production versus 25 million tonnes of demand, and tightening mycotoxin regulations. DSM-Firmenich's Swiss plant remains Europe's primary high-purity fractionation hub, supplying pharmaceutical and cosmetics customers with Certificate of European Pharmacopoeia-compliant concentrates. South America is led by Brazil and Argentina, which host 60% of global soybean crushing capacity and are installing molecular-distillation units at refinery gates to capture tocopherol value before exporting crude oil. The Middle East and Africa market is driven by halal-certified supplement demand and fortified-food programs in the United Arab Emirates and South Africa.

Competitive Landscape

The mixed tocopherols market is moderately consolidated, with a few large players dominating the supply chain while leaving room for smaller specialized competitors. Key players such as BASF, DSM-Firmenich, ADM, Cargill, and Wilmar leverage feedstock access, molecular distillation capabilities, and global formulation expertise to maintain cost, scale, and quality advantages. Their strategies focus on backward integration, sourcing security, and premium-grade specialization, enabling them to cater to diverse regulatory and purity requirements across food, nutraceutical, pharmaceutical, and personal care sectors. BASF’s new investment program to increase vitamin E acetate capacity from 2027 underscores its long-term commitment despite an 18-month post-explosion supply gap. DSM-Firmenich protects the pharmaceutical share by holding the first Certificate of European Pharmacopeia for alpha-rich tocopheryl acetate concentrate.

Niche players like Kemin, Nanjing NutriHerb, and Fenchem focus on product specificity, certifications, and formulation flexibility, competing less on scale and more on tailored solutions. These companies emphasize organic-certified tocopherols, high-purity delta-rich fractions, and custom alpha-gamma-delta blends for supplements, cosmetics, and fortified foods. Chinese mid-cap producers are leveraging process improvements like supercritical CO₂ extraction to reduce costs, enabling them to underprice larger incumbents in certain channels. This dual market structure sees multinational suppliers competing on quality and compliance, while regional players focus on price and customization. Innovation now extends beyond chemistry to include process efficiency, certification depth, and niche buyer requirements.

Emerging opportunities are driven by application-specific innovation. Water-soluble tocopherols for beverages, gamma-rich concentrates for health blends, and toxin-free rapeseed-derived fractions for infant formulas are gaining traction by addressing unique formulation challenges. Competitive advantage will depend on traceability, clean-label positioning, regulatory readiness, and application support. Companies investing in upstream security, low-carbon extraction, and tailored ingredient systems will better defend against low-cost entrants while capturing premium demand in health-focused and functional product categories. The competitive landscape is evolving toward a solutions-led model where technical service and regulatory credibility are as critical as price.

Mixed Tocopherols Industry Leaders

-

BASF SE

-

DSM-Firmenich N.V.

-

Archer Daniels Midland (ADM)

-

Cargill Inc.

-

Wilmar International Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Wilmar International acquired Natural Oleochemicals for USD 192 million, consolidating Malaysian palm-derivative capacity and expanding its tocopherol and tocotrienol production footprint to serve Southeast Asian, Middle Eastern, and African markets with shorter lead times and lower freight costs.

- February 2026: The European Food Safety Authority renewed authorization for tocopherol-rich extracts as feed additives, expanding addressable markets into poultry and aquaculture, where synthetic antioxidants face stricter residue limits.

- August 2025: BASF increased its Vitamin E production capacity through investments in Ludwigshafen, Germany, and Shanghai, China, to strengthen its position in the animal nutrition and human health markets. This strategic expansion focuses on upgrading facilities and enhancing supply chain reliability across Europe and Asia.

- March 2025: Shandong New Element Biotechnology showcased SunGold VE-95 (95% purity, non-GMO tocopherols from sunflower oil) and SmartCapsule VE (temperature-stable, microencapsulated vitamin E) at Food Ingredients China 2025, attracting 23 partnership inquiries and announcing plans to triple its GMP-certified production capacity.

Global Mixed Tocopherols Market Report Scope

Mixed tocopherols are a natural form of Vitamin E, consisting of a blend of alpha, beta, gamma, and delta-tocopherols derived from vegetable oils. They function as potent fat-soluble antioxidants and are commonly used to prevent rancidity. The mixed tocopherols market is segmented by source, compound, form, application, and geography. Based on source, the market is segmented into soybean oil, rapeseed oil, sunflower oil, corn oil, palm oil, and others. By compound, the market is segmented into alpha-rich tocopherols, gamma-rich tocopherols, delta-rich tocopherols, and others. By form, the market has been segmented into liquid, powder, and others. By application, the market has been segmented into food and beverage, animal feed, dietary supplements, pharmaceuticals, cosmetics, and personal care, and others. By geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD).

| Soybean Oil |

| Rapeseed Oil |

| Sunflower Oil |

| Corn Oil |

| Palm Oil |

| Others |

| Alpha-Rich Tocopherols |

| Gamma-Rich Tocopherols |

| Delta-Rich Tocopherols |

| Other Blends |

| Liquid |

| Powder |

| Others |

| Food and Beverage |

| Animal Feed |

| Dietary Supplements |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Thailand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Rest of Middle East and Africa |

| By Source | Soybean Oil | |

| Rapeseed Oil | ||

| Sunflower Oil | ||

| Corn Oil | ||

| Palm Oil | ||

| Others | ||

| By Compound | Alpha-Rich Tocopherols | |

| Gamma-Rich Tocopherols | ||

| Delta-Rich Tocopherols | ||

| Other Blends | ||

| By Form | Liquid | |

| Powder | ||

| Others | ||

| By Application | Food and Beverage | |

| Animal Feed | ||

| Dietary Supplements | ||

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the mixed tocopherols market?

The mixed tocopherols market size stands at USD 6.58 billion in 2026 and is projected to reach USD 8.28 billion by 2031.

Which region is likely to witness the highest growth?

Asia-Pacific is projected to log the fastest 5.68% CAGR through 2031 on the back of dietary-supplement and cosmetics demand.

Which compound segment is expanding fastest through 2031?

Gamma-rich tocopherols are forecast to grow at a 7.52% CAGR, outpacing alpha-rich and delta-rich grades.

Why are powders preferred over liquid tocopherols in supplements?

Powder forms retain 95.4% activity at 60 °C for a month and offer superior flow, making them ideal for tablets and infant-formula blends.

Page last updated on: