Global 5G In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

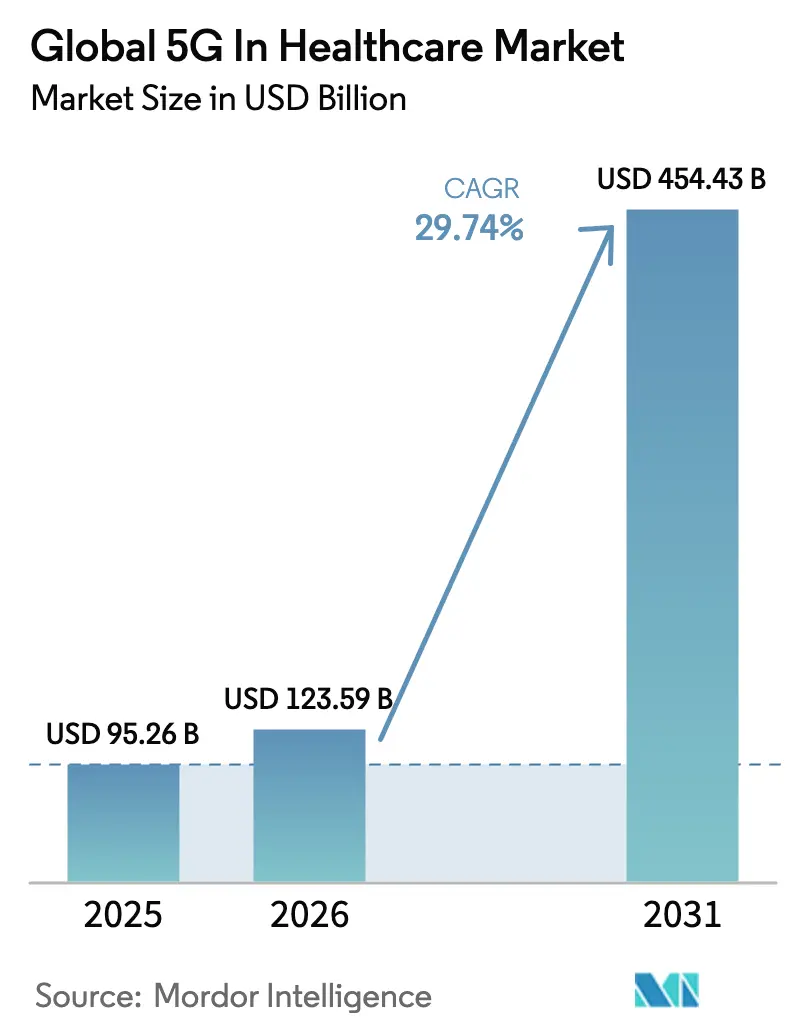

| Market Size (2026) | USD 123.59 Billion |

| Market Size (2031) | USD 454.43 Billion |

| Growth Rate (2026 - 2031) | 29.74% CAGR |

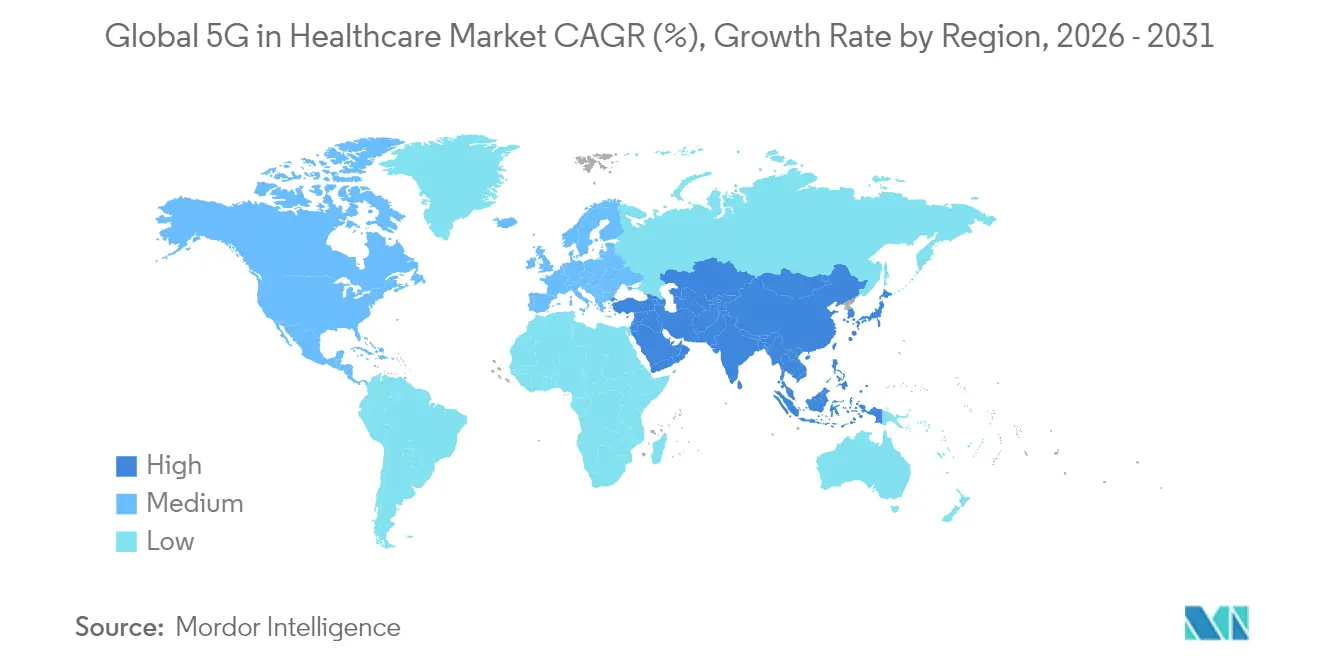

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

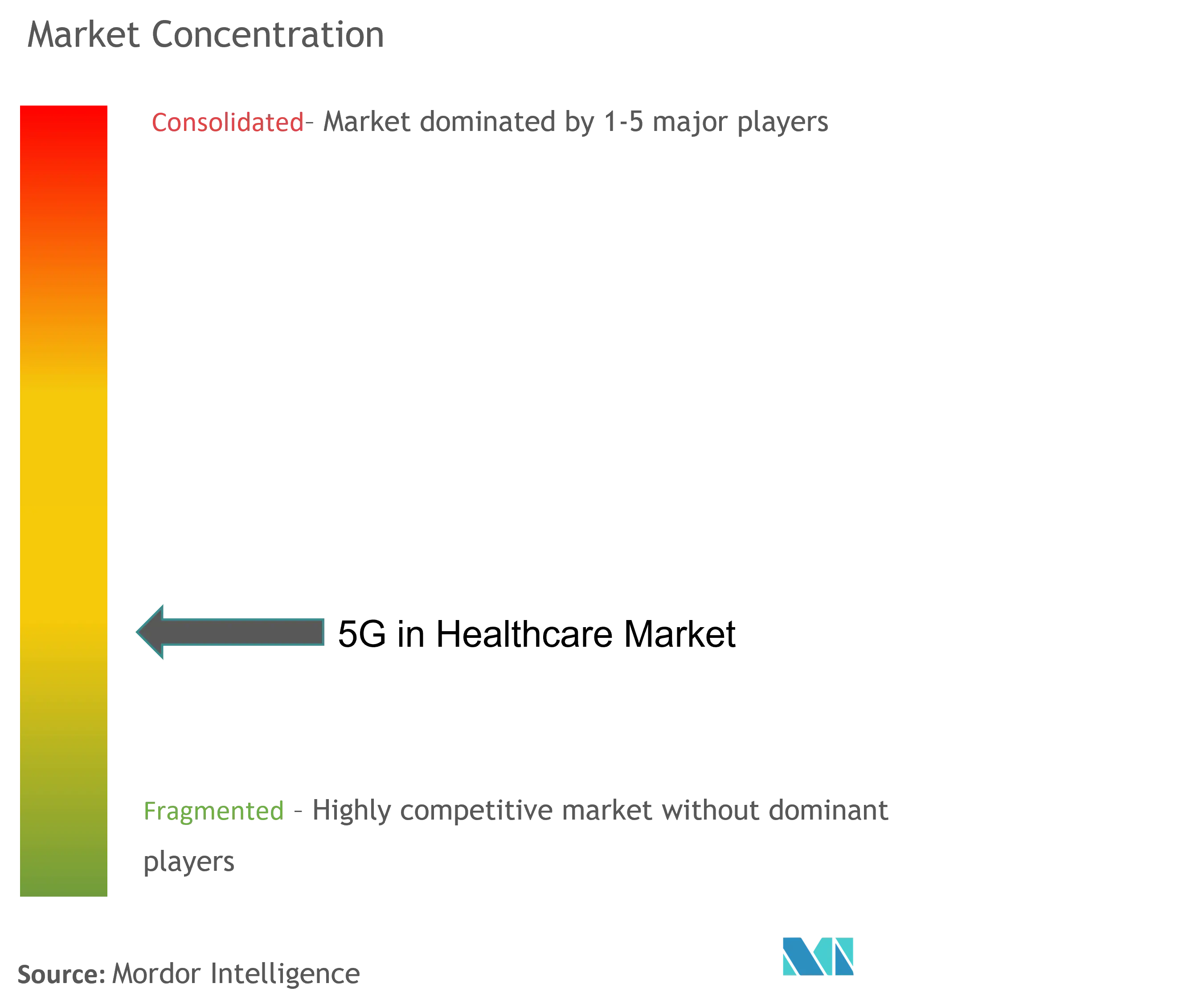

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global 5G In Healthcare Market Analysis by Mordor Intelligence

The 5G in healthcare market size was valued at USD 95.26 billion in 2025 and estimated to grow from USD 123.59 billion in 2026 to reach USD 454.43 billion by 2031, at a CAGR of 29.74% during the forecast period (2026-2031). Rapid scale-up from pilot projects to full commercial rollouts is accelerating demand, as millisecond-level latency unlocks remote surgery, real-time intensive-care collaboration, and high-resolution medical imaging. Hardware still attracts the largest capital outlay, yet managed service models are surging as hospitals seek turnkey deployments that avoid specialist staffing burdens. Regional momentum diverges: North America leans on private networks for mission-critical workloads, while Asia-Pacific gains speed through public-private build-outs that lower infrastructure costs. Spectrum pricing reform, tighter cybersecurity frameworks, and maturing edge-compute ecosystems will shape the competitive landscape—and determine how quickly the 5G in healthcare market captures untapped connectivity budgets.

Key Report Takeaways

- By geography, North America accounted for 39.78% of 5G in healthcare market share in 2025, whereas Asia-Pacific is projected to expand at the fastest 34.08% CAGR to 2031.

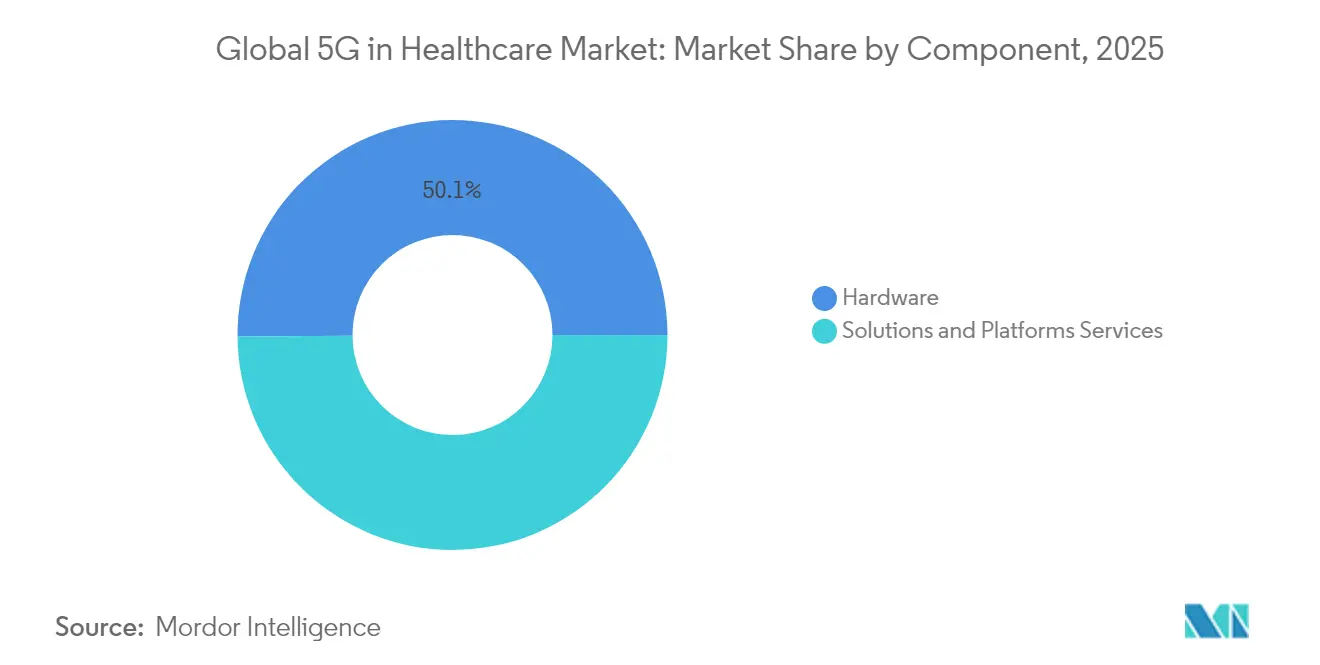

- By component, hardware led with 50.12% revenue share in 2025; services are poised for the highest 32.07% CAGR through 2031.

- By communication type, eMBB captured 51.85% share of the 5G in healthcare market size in 2025; URLLC is forecast to progress at a 32.12% CAGR between 2026-2031.

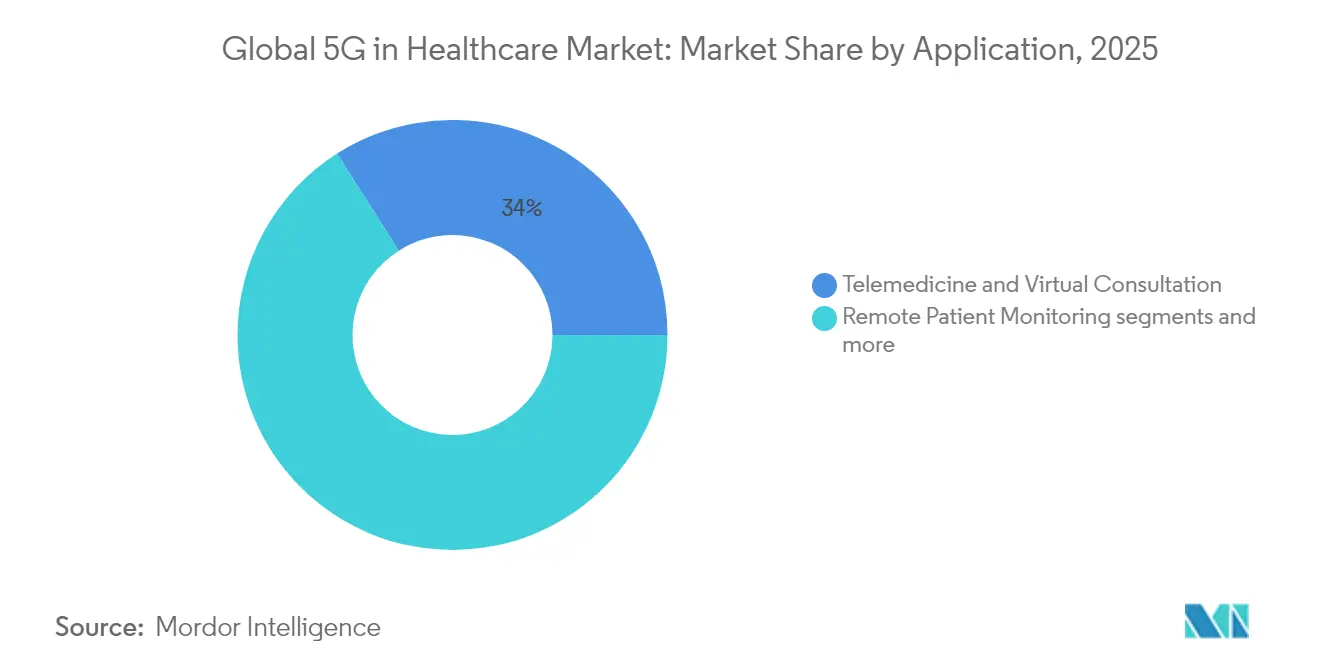

- By application, telemedicine and virtual consultation services held 34.02% of 5G in healthcare market size in 2025, while robotic & telesurgery is advancing at a 32.75% CAGR to 2031.

- By end user, hospitals and surgical centers commanded 45.83% market share in 2025; home healthcare is the fastest-growing user segment at 33.41% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 5G In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging tele-ICU and remote surgery pilots | +8.5% | Global, with early gains in China, US, Singapore | Medium term (2-4 years) |

| Telecom-provider push for private 5G networks in hospitals | +6.2% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Reimbursement expansion for video visits & RPM | +4.8% | North America core, expanding to EU | Short term (≤ 2 years) |

| mMTC-enabled asset tracking cuts hospital opex | +3.1% | Global | Medium term (2-4 years) |

| Hyper-converged edge datacenters in smart hospitals | +2.7% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| AI-assisted network slicing for clinical QoS | +1.9% | National, with early gains in South Korea, Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Tele-ICU and Remote Surgery Pilots

Tele-ICU programs are multiplying as health systems confront specialist shortages; Brazil’s national initiative treated 5,471 patients across 15 ICUs in 2022-2023, conducting 3,971 virtual rounds that matched bedside decision-making quality because 5G sustained sub-10 ms latency. China then validated cross-country robotic surgery by completing a 1,700 km thyroidectomy over 5G links with <99 ms latency, opening a new era of distance-neutral surgical care. Together with satellite-backed operations performed via the Apstar-6D platform, these milestones demonstrate clinical reliability at continental ranges, accelerating investment in nationwide 5G surgical corridors and expanding the addressable 5G in healthcare market.

Telecom-Provider Push for Private 5G Networks in Hospitals

Operators now court hospitals as enterprise customers, building private 5G stand-alone (SA) systems that guarantee quality-of-service for life-critical workloads. Boldyn Networks switched on Europe’s first hospital-grade SA network in Finland’s Oulu University Hospital, powering live biosensor data feeds and AR-guided procedures. Verizon installed an end-to-end 5G campus at Cleveland Clinic’s Mentor facility, integrating check-in kiosks and telemetry dashboards that trimmed administrative delays. Sweden’s USD 35 million VGR-5G program will replicate that model across 500+ hospitals, signalling that managed private-network contracts could outpace raw hardware demand within the wider 5G in healthcare market.

Reimbursement Expansion for Video Visits & RPM

Payment frameworks are catching up to connectivity innovation. The 2025 US Physician Fee Schedule introduced new CPT codes for virtual check-ins, chronic-care management, and remote physiologic monitoring, granting parity reimbursement for 5G-enabled services[1]Source: CMS, “2025 Physician Fee Schedule,” cms.gov . UnitedHealthcare’s updated policy now reimburses live audio-visual encounters and continuous vitals capture, providing clear revenue arcs for telehealth platforms. These policy shifts mitigate financial risk, empower providers to adopt bandwidth-intensive diagnostics, and inject fresh momentum into the 5G in healthcare industry.

mMTC-Enabled Asset Tracking Cuts Hospital Opex

Hospitals deploy massive machine-type communications (mMTC) tags to geolocate equipment within sprawling campuses. Texas Health Resources cut nurse search time after rolling out a 5G-ready real-time-location system, boosting satisfaction scores and slicing operational cost. AT&T’s rugged 5G asset-tags survive sterilization, while Borda Technology pairs Bluetooth-Low-Energy beacons with 5G backhaul, covering 1 million devices per km² and lowering asset loss by 15-30%. The ongoing shift from manual audits to predictive maintenance unlocks measurable savings and deepens the appeal of the 5G in healthcare market for hospital finance teams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum-licensing cost burden on healthcare systems | -4.2% | Global, with highest impact in developed markets | Short term (≤ 2 years) |

| Cyber-physical security vulnerabilities in connected devices | -3.8% | Global | Medium term (2-4 years) |

| Inter-vendor interoperability gaps | -2.1% | North America & EU | Medium term (2-4 years) |

| Clinician unions' latency-liability concerns | -1.3% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Spectrum-Licensing Cost Burden on Healthcare Systems

Spectrum fees often exceed USD 1 billion for national operators, and that capital burden filters down to medical campuses seeking dedicated frequencies. A 10-point jump in the spectrum-cost-to-revenue ratio can trim 5G coverage 6 points and drop speeds 8%, curbing tele-surgery reliability in densely populated cities. When deployment costs per base station run USD 100,000-200,000—and mmWave sits 1.5-2x higher—cash-constrained hospitals delay rollouts, slowing the near-term progress of the 5G in healthcare market.

Cyber-Physical Security Vulnerabilities in Connected Devices

Three in four 5G-connected medical devices contain exploitable weaknesses, exposing hospitals to cross-slice attacks that can hijack ventilators or manipulate infusion pumps. Ransomware incidents climbed 150% where 5G adoption surged, triggering rising insurance premiums and pushing providers toward zero-trust architectures. The FDA now mandates electromagnetic-compatibility testing and risk-management documentation for 5G medical devices, adding time and cost to product launches. Persistent threat pressure dampens short-term uptake but also fuels demand for managed cybersecurity services embedded in every 5G in healthcare market contract.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Drives Infrastructure Build-out

Hardware solutions commanded 50.12% of the 5G in healthcare market share in 2025, reflecting the heavy capital requirements of base stations, small cells, antennas, and edge servers. Early adopters treated connectivity as a construction project, funding multiyear campus overhauls that underpin surgical suites, imaging labs, and intensive-care units. Yet the services slice is scaling faster—32.07% CAGR—because hospitals prefer turnkey subscriptions that bundle spectrum, software, and compliance services. ZTE’s integrated 5G IoT network for Soochow University Hospital connected 3,000 devices, trimmed build time 90%, and cut total cost of ownership 30%. Similar “network-as-a-service” models shift 5G in healthcare market risk off hospital balance sheets, encourage phased adoption, and spur ecosystem innovation.

That migration reshuffles vendor power. Infrastructure OEMs partner with cloud hyperscalers and cybersecurity firms to defend margins, while integrators monetise lifecycle management. Hospitals gain predictable opex, on-demand network slices, and embedded threat monitoring. Over 2026-2031, managed services could eclipse hardware shipments in annual spend, marking a structural pivot within the 5G in healthcare market.

By Communication Type: eMBB Leads While URLLC Accelerates

Enhanced Mobile Broadband (eMBB) secured 51.85% share of the 5G in healthcare market size in 2025 by supporting 4K imaging, high-definition conferencing, and cloud PACS back-ups. Demand remains sticky as radiology departments shift to 8K workflows and medical schools stream volumetric video for remote training. Ultra-Reliable Low-Latency Communications (URLLC) races ahead at 32.12% CAGR, enabling precision robotics, AI-guided anaesthesia, and multi-site stroke intervention units. Singapore’s National University Health System recorded 1 Gbps downlink, 150 Mbps uplink, and sub-10 ms latency across 20 mixed-reality surgeries on 3.5 GHz spectrum. Massive Machine-Type Communications (mMTC) underpins billions of low-power sensors, from drug refrigerators to connected wearables, forming the glue for continuous care loops.

Inter-slice orchestration is emerging as the competitive pivot: vendors that seamlessly flex bandwidth between eMBB diagnostic transfers and URLLC surgical sessions will win enterprise contracts. Regulators now standardise quality-of-service thresholds, pushing suppliers to validate latency and jitter across complex hospital floorplans. These advances reinforce the climb of the 5G in healthcare market as next-generation workloads mature.

By Application: Telemedicine Dominance Faces Surgical Innovation

Telemedicine and virtual consultations captured 34.02% of 5G in healthcare market size during 2025, buoyed by pandemic-era behavioural change and stable reimbursement codes. Remote patient monitoring complements virtual visits, feeding real-time vitals to care teams via mMTC sensors. Yet robotic and telesurgery exhibit the fastest 32.75% CAGR: China’s 60-minute hepatic lobectomy performed 50 km from the patient through Huawei-powered 5G links proved that surgical dexterity survives distance. Connected ambulances, AR-assisted rehabilitation, and smart intensive-care dashboards broaden the application mix.

Integration of AI models at the network edge blurs traditional segment lines. Predictive imaging triage, automatic instrument tracking, and autonomous disinfection robots demand synchronous data, intensifying 5G bandwidth and latency requirements. As these platforms leap from trial to routine workflow, they bolster revenue diversity and attract software-centric entrants to the 5G in healthcare market.

By End User: Hospitals Lead While Home Healthcare Surges

Hospitals and surgical centers held 45.83% of 5G in healthcare market share in 2025, justified by critical-care workloads that cannot tolerate connectivity failure. They dominate early capex by deploying private cores, edge clusters, and device orchestration platforms. Home healthcare, however, is accelerating at 33.41% CAGR as insurers push care closer to patients. Boston Children’s Hospital uses a 5G hybrid network to connect clinicians across sites, enabling future in-home treatment and AI-driven triage. Ambulatory clinics and research institutes serve as innovation labs, piloting AR-aided endoscopy and smart lab inventories.

Consumer-grade devices certified for medical use will fuel the next wave of distributed care. When hospital-quality diagnostics reach living rooms, the 5G in healthcare market widens far beyond institutional walls, reinforcing demand for secure, scalable, and standards-compliant connectivity services.

Geography Analysis

North America retained 39.78% share of the 5G in healthcare market in 2025 thanks to early private-network investments, favourable reimbursement, and strong vendor ecosystems. Cleveland Clinic’s Mentor campus illustrates rapid ROI: 5G kiosks cut admission waits and telemetry wearables freed nursing time, validating enterprise cases for peers across the US and Canada. Structured payment for video visits and RPM further lowers adoption barriers, driving near-term revenue.

Asia-Pacific delivers the fastest 34.08% CAGR through 2031 as China’s national policy aligns spectrum allocation, infrastructure subsidies, and digital-health grants. Singapore’s NUHS and Singtel deployed a hybrid enterprise network that underpins the Holomedicine program—remote holographic visualisation that shortens surgical planning—while South Korea’s Samsung Medical Centre streams 3D CT scans onto AR headsets for trainee surgeons. Economies of scale and manufacturing depth make Asia-Pacific a cost-efficient hardware base, further amplifying regional momentum.

Europe advances more gradually. Only 2% of hospitals had 5G SA coverage in 2024 compared with 80% in China and 24% in the US, due in part to fragmented regulation and vendor swap-outs prompted by security reviews. Germany leads regional deployments, and Finland’s Oulu University Hospital hosts Europe’s most mature private medical 5G SA network. The European Commission’s Digital Compass seeks ubiquitous 5G by 2030; success will require harmonised spectrum fees, streamlined permits, and public-sector anchor projects to spur rural uptake—factors that will influence the continental slice of the 5G in healthcare market.

The Middle East and Africa trail on absolute spend but show pockets of innovation: the UAE’s e& enterprise and Burjeel Holdings launched 5G telemedicine clinics, and South African providers pilot connected ambulances with real-time sonography. Latin America, led by Brazil and Mexico, extends tele-ICU grids to address specialist deficits, with coverage gains hinging on cost-effective mid-band spectrum auctions. Each emerging-market proof point enlarges the global opportunity pool, keeping the 5G in healthcare market on its steep upward trajectory.

Competitive Landscape

Competition unfolds across three interlocking layers. Telecom infrastructure vendors—Huawei, Ericsson, Nokia, Qualcomm, and Samsung—supply radios, cores, and orchestration software. Healthcare technology leaders—Philips, GE Healthcare, Siemens Healthineers, Medtronic—embed clinical logic, imaging algorithms, and device integration. Systems integrators and hyperscalers bridge both worlds, packaging managed private-network services with security and analytics. This mosaic generates moderate fragmentation: no single firm exceeds 15% revenue share, yet the top five collectively command roughly 55%, underscoring a market concentration score of 6.

Partnerships dominate strategy. Verizon pairs with Cleveland Clinic to showcase private-5G reference architecture, while Cisco teams with Kajeet to roll out healthcare-specific managed services that de-risk adoption for midsized hospitals. Edge-compute alliances crop up as latency-sensitive workloads shift analytic engines closer to patient bedsides; Qualcomm and Microsoft integrate AI accelerators into hospital servers to classify imaging in real time. Regulatory collaboration also intensifies: the FDA’s 5G working group harmonises device certification, giving compliant suppliers a first-mover edge.

Sourcing dynamics evolve as hospitals seek vendor-agnostic orchestration. Open RAN pilots permit component interchangeability, pressuring incumbents to emphasise software differentiation and service quality. Cybersecurity capabilities grow decisive: providers favour partners offering zero-trust architectures, device attestation, and real-time anomaly detection. As competition shifts from pure bandwidth to packaged clinical value, the 5G in healthcare market increasingly rewards ecosystem orchestration over standalone hardware scale.

Global 5G In Healthcare Industry Leaders

AT&T

Verizon

Ericsson

T‑Mobile USA, Inc.

Cisco

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Artemis Hospitals and Medulance launched a 5G-connected ambulance in Gurugram to transmit vitals en route to emergency departments

- June 2025: Kajeet partnered with Cisco to deliver healthcare-specific 5G managed services targeting turnkey hospital deployments

- June 2025: China’s surgeons performed five satellite-enabled ultra-remote operations via the Apstar-6D broadband satellite.

Global 5G In Healthcare Market Report Scope

As per the scope of the report, 5G, or fifth generation, is the latest wireless mobile phone technology, first widely deployed in 2019. 5G is expected to increase performance and introduce a wide range of new applications, including strengthening e-health (telemedicine, remote surveillance, telesurgery).

The 5G in healthcare market is segmented by Component (Hardware, Services, and Connectivity), Application (Connected Medical Devices, Remote Patient Monitoring, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Hardware |

| Solutions & Platforms |

| Services |

| Enhanced Mobile Broadband (eMBB) |

| Ultra-Reliable Low-Latency Comm. (URLLC) |

| Massive Machine-Type Comm. (mMTC) |

| Telemedicine & Virtual Consultation |

| Remote Patient Monitoring |

| AR/VR Assisted Therapy & Training |

| Connected Ambulance & Emergency Care |

| Smart Wearables & In-Hospital IoT |

| Robotic & Telesurgery |

| Hospitals & Surgical Centers |

| Ambulatory & Specialty Clinics |

| Home Healthcare Providers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Component (Value) | Hardware | |

| Solutions & Platforms | ||

| Services | ||

| By Communication Type (Value) | Enhanced Mobile Broadband (eMBB) | |

| Ultra-Reliable Low-Latency Comm. (URLLC) | ||

| Massive Machine-Type Comm. (mMTC) | ||

| By Application (Value) | Telemedicine & Virtual Consultation | |

| Remote Patient Monitoring | ||

| AR/VR Assisted Therapy & Training | ||

| Connected Ambulance & Emergency Care | ||

| Smart Wearables & In-Hospital IoT | ||

| Robotic & Telesurgery | ||

| By End User (Value) | Hospitals & Surgical Centers | |

| Ambulatory & Specialty Clinics | ||

| Home Healthcare Providers | ||

| Academic & Research Institutes | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Global 5G in Healthcare Market size?

The Global 5G in Healthcare Market is projected to register a CAGR of 29.74% during the forecast period (2026-2031)

Who are the key players in Global 5G in Healthcare Market?

AT&T, Verizon, Ericsson, T‑Mobile USA, Inc. and Cisco are the major companies operating in the Global 5G in Healthcare Market.

Which is the fastest growing region in Global 5G in Healthcare Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global 5G in Healthcare Market?

In 2025, the North America accounts for the largest market share in Global 5G in Healthcare Market.

What years does this Global 5G in Healthcare Market cover?

The report covers the Global 5G in Healthcare Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global 5G in Healthcare Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: