Global NGS Sample Preparation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

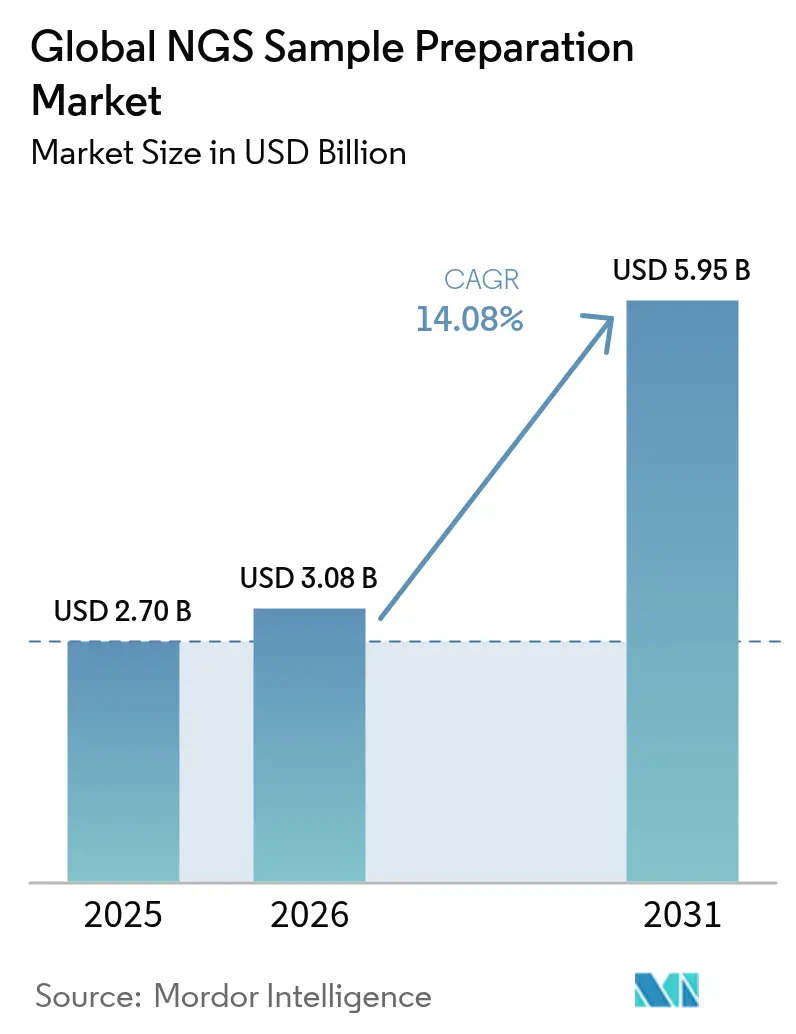

| Market Size (2026) | USD 3.08 Billion |

| Market Size (2031) | USD 5.95 Billion |

| Growth Rate (2026 - 2031) | 14.08% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global NGS Sample Preparation Market Analysis by Mordor Intelligence

The next-generation sequencing sample preparation market size is expected to grow from USD 2.7 billion in 2025 to USD 3.08 billion in 2026 and is forecast to reach USD 5.95 billion by 2031 at 14.08% CAGR over 2026-2031. Growth is propelled by falling sequencing-per-base costs, automation that trims hands-on time, and expanding clinical use cases such as oncology and non-invasive prenatal testing. Reagents and consumables continue to supply recurring revenue streams, while automation workstations capture budget reallocation toward labor-saving infrastructure. Regulatory clarity in North America and government-funded genomic programs across Asia Pacific sustain demand, even as supply-chain resilience and cold-chain-free chemistry reshape procurement strategies. Competitive intensity remains moderate: incumbents leverage vertical integration, and well-funded entrants differentiate on cost and platform flexibility.

Key Report Takeaways

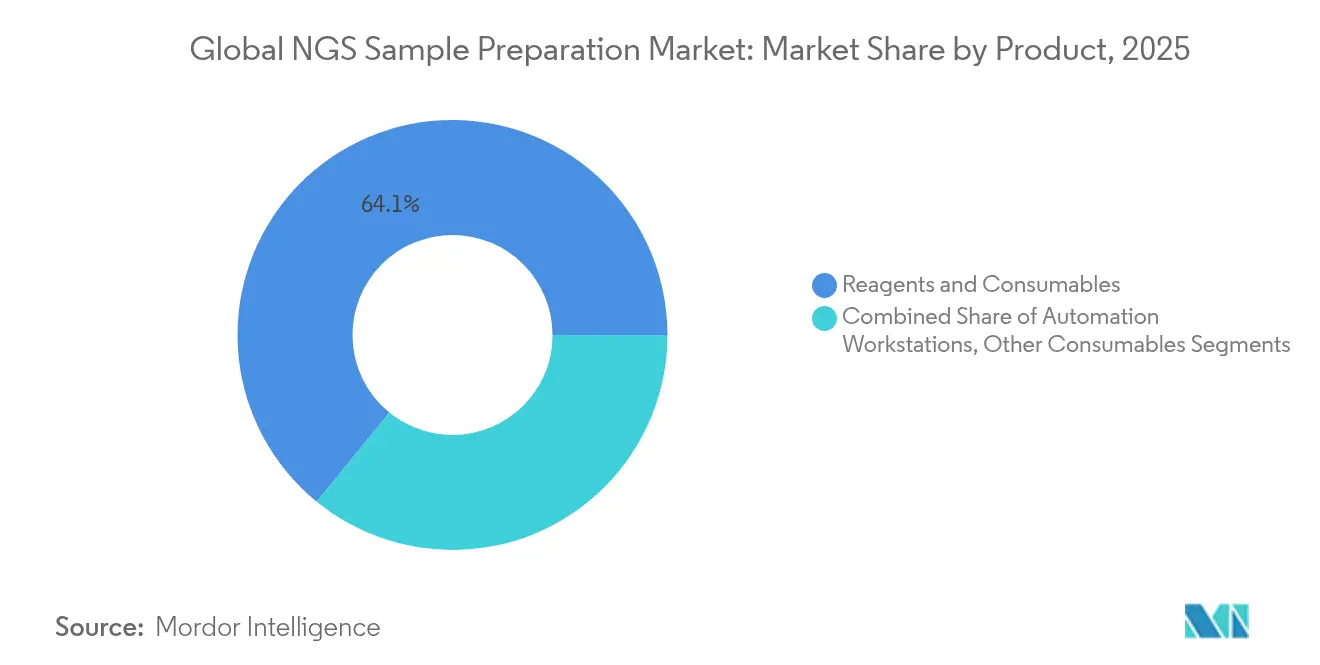

- By product class, reagents and consumables held 64.12% of the next-generation sequencing sample preparation market share in 2025, whereas automation workstations are projected to grow at an 18.28% CAGR through 2031.

- By application, diagnostics, including oncology, commanded a 53.62% revenue share in 2025; reproductive health (NIPT) is expected to expand at a 17.62% CAGR to 2031.

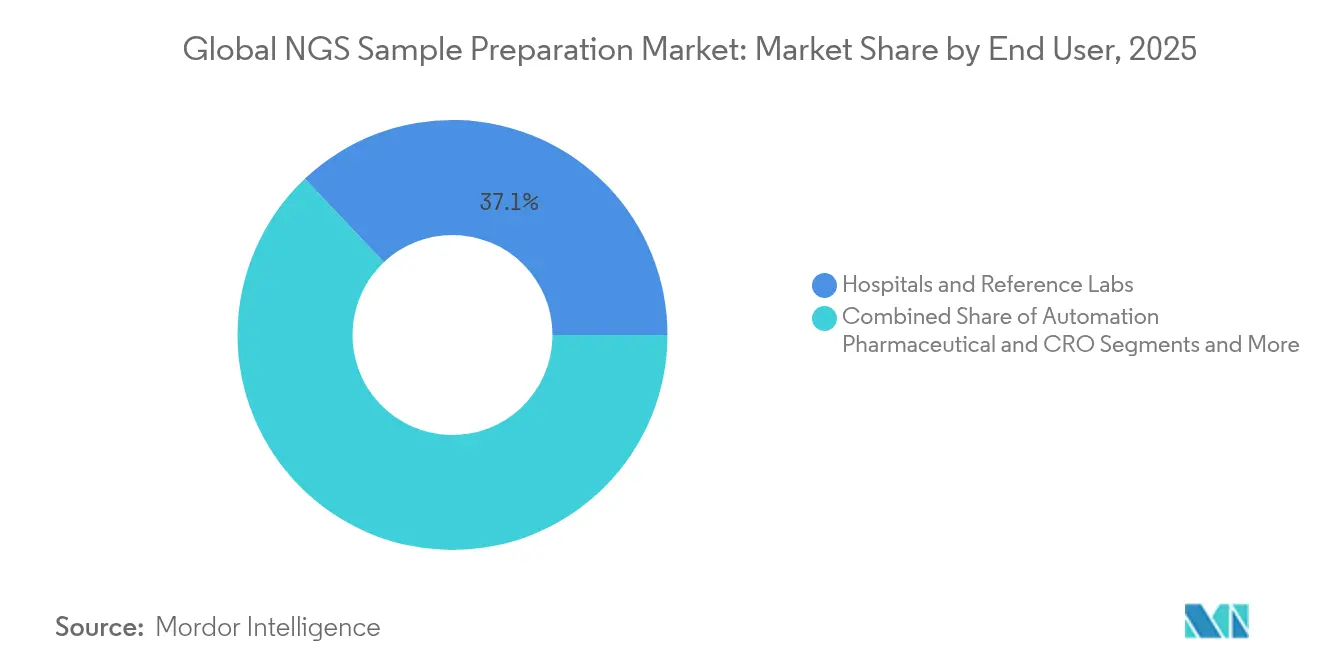

- By end-user, hospitals and reference laboratories accounted for 37.05% of the next-generation sequencing sample preparation market size in 2025, while contract research organizations recorded the fastest CAGR at 15.74% through 2031.

- By region, North America led with 39.10% revenue share in 2025; Asia Pacific is forecast to rise at a 14.22% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global NGS Sample Preparation Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of infectious and emerging pathogens | +2.10% | Sub-Saharan Africa, Asia Pacific | Medium term (2-4 years) |

| Falling sequencing-per-base costs and open-platform chemistry | +2.80% | North America, Europe | Short term (≤ 2 years) |

| Automation reducing hands-on time in high-throughput laboratories | +2.40% | North America, European Union, spill-over to core Asia Pacific markets | Medium term (2-4 years) |

| Clinical adoption of rapid on-board sample-to-answer systems | +1.90% | Developed healthcare systems globally | Short term (≤ 2 years) |

| Venture funding for sample-prep-as-a-service startups | +1.20% | North America, Europe, emerging Asia Pacific | Long term (≥ 4 years) |

| Expansion of precision oncology and companion diagnostics applications | +3.10% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Infectious and Emerging Pathogens

Over half of Sub-Saharan African nations now run in-country NGS surveillance platforms, accelerating pathogen tracking capacity built during the COVID-19 response.[1]Ogwell Ouma, “Building Pathogen Genomic Surveillance Capacity,” Tropical Medicine and Infectious Disease, mdpi.com Regional consortia, such as the Asia Pathogen Genomics Initiative, aggregate resources to mitigate persistent supply bottlenecks. Validated metagenomic assays reach 93.6% sensitivity for respiratory viruses in under 24 hours.[2]Chang-Yi Lin et al., “Metagenomic Sequencing for Respiratory Virus Detection,” Nature Communications, nature.com Coupling nanopore sequencing with antimicrobial-resistance calling delivers >90% concordance with phenotypic data, reinforcing sample-prep upgrades designed for diverse specimen matrices. Laboratories, therefore, prioritize kits compatible with low-input, pathogen-rich samples and shortened turnaround.

Falling Sequencing-Per-Base Costs and Open-Platform Chemistry

Component prices for flow cells, enzymes, and terminators continue to decline as multi-vendor supply chains mature, allowing new entrants to commercialize benchtop sequencers for below USD 100,000. Illumina’s on-flow-cell library chemistry, scheduled for commercial release in 2025, removes separate library prep steps and lowers overall per-run costs. Platform-agnostic kits such as CapTrap-seq give laboratories flexibility to switch instruments without revalidating upstream preparation. These developments shift capital budget decisions from hardware replacement cycles to chemistry and workflow optimization, reinforcing price competition across reagents.

Automation Reducing Hands-On Time in High-Throughput Laboratories

Acoustic liquid handlers compress an eight-hour manual workflow into roughly 30 minutes, freeing scarce technologist hours. High-throughput systems like MGISP-960 automate 96 plates in an unmanned run, aligning with hospitals that now process thousands of oncology and hereditary disease samples monthly. Artificial-intelligence scheduling modules further cut procurement delays and reduce consumable stockouts. Once automated, cytogenetics labs report lower inter-operator variability, underlining the reproducibility premium that justifies capital spending.

Clinical Adoption of Rapid On-Board Sample-to-Answer Systems

Liquid-biopsy programs in Canada achieve a median three-day turnaround—from draw to report—versus traditional tissue workflows that can exceed two weeks. FDA breakthrough approvals for metagenomic NGS assays in 2023 opened a fast track for infectious disease panels, incentivizing hospital labs to embed sequencing directly in emergency care settings.[3]U.S. Food and Drug Administration, “Laboratory Developed Tests (LDTs) Final Rule,” fda.gov Nanopore Q20+ chemistry now records ≥99% raw read accuracy, supporting rapid outbreak tracing while retaining long-read benefits. On-board prep modules integrated with sequencers strip away legacy library steps and meet oncology dosing windows.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-intensive automation and consumable costs for mid-size laboratories | -1.80% | Global, more acute in emerging markets | Medium term (2-4 years) |

| High variability in upstream sample quality impacting library yield | -1.20% | Resource-limited settings worldwide | Short term (≤ 2 years) |

| Fragmented regulatory guidance for laboratory developed tests across regions | -2.10% | Asia Pacific, Latin America | Long term (≥ 4 years) |

| Cold-chain constraints for reagent logistics in emerging markets | -1.40% | Sub-Saharan Africa, Southeast Asia, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Automation and Consumable Costs for Mid-Size Laboratories

Units such as the MGISP-960 demand six-figure investments and steady throughput; labs processing under 1,000 samples each month struggle to realize per-sample savings. Consumables can comprise up to 70% of total preparation cost, pressuring mid-volume facilities to outsource sequencing. Ambient-temperature stabilization chemistries from Biomatrica now maintain DNA integrity without a cold chain, offering a partial remedy and trimming logistics spend. Sample-prep-as-a-service providers bridge capability gaps, yet slow direct capital equipment growth.

Fragmented Regulatory Guidance for Laboratory Developed Tests Across Regions

The FDA’s May 2024 final rule phases out enforcement discretion over four years, mandating premarket review for high-risk LDTs. European IVDR pathways diverge in documentation requirements, whereas several Asia Pacific countries apply local registration schemes, forcing multinational labs to manage parallel validations. Smaller companies face added administrative costs, amplifying the advantage of incumbents with dedicated compliance teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Class: Automation Drives Premium Segment Growth

Reagents and consumables held 64.12% of the next-generation sequencing sample preparation market share in 2025, underscoring their recurring revenue profile. Automation workstations, though lower in absolute revenue, are expected to grow 18.28% annually as staffing shortages raise the cost of manual workflows. The NEBNext Ultra II enzymatic fragmentation kit cuts hands-on time to 15 minutes while maintaining high library complexity, exemplifying how chemistry advances complement automation. Within this segment, value-added devices that monitor reagent use and prevent pipetting errors secure premium pricing and pay-back periods of under 18 months for labs exceeding 500 monthly samples.

Laboratories increasingly bundle automation hardware with software dashboards that predict reagent depletion, aligning purchasing with just-in-time delivery. DISPENDIX’s I.DOT handler automates 80% of library prep steps and provides visual QC checkpoints, lowering re-run rates. As throughput rises, these integrated platforms optimize reagent consumption and strengthen vendor lock-in strategies.

By Application: Precision Medicine Accelerates Clinical Adoption

Diagnostics, led by oncology, generated 53.62% of 2025 revenue as genomic profiling became the standard of care across major cancer subtypes. NIPT is forecast to log a 17.62% CAGR through 2031, fueled by broader payer coverage and expanding paternal haplotype assays. Precision-oncology panels now detect minimal residual disease in early-stage tumors, guiding adjuvant therapy choices and heightening sensitivity requirements for sample prep. Labcorp’s alliance with Ultima Genomics on whole-genome-based residual-disease testing illustrates how clinical labs refine workflows for ultralow variant allele frequencies.

Drug discovery groups adopt single-cell sequencing to decipher tumor microenvironments, while agricultural researchers deploy targeted genotyping-by-sequencing to improve crop traits, diversifying revenue beyond human health. These varied use cases sustain the next-generation sequencing sample preparation market as kit manufacturers tailor chemistries for circulating DNA, FFPE tissue, or plant material, ensuring workflow adaptability.

By End-User: CROs Capitalize on Outsourcing Trends

Hospitals and reference laboratories secured 37.05% of 2025 revenue; however, contract research organizations are expanding at 15.74% CAGR as pharmaceutical developers offload genomics projects to specialized partners. Charles River now bundles microbial ID, RNA-Seq, and CRISPR editing services in turnkey packages that obviate internal infrastructure spend. Academic institutes remain steady buyers, yet mid-size biotechs increasingly partner with CROs for regulatory-grade sequence data, reinforcing third-party growth.

Automation makers respond by offering cloud-connected platforms that enable remote protocol updates and performance monitoring, features valued by distributed CRO networks handling multicenter clinical trials. These dynamics sustain demand for both equipment and consumables, cementing CROs as a pivotal downstream customer group.

By Workflow Phase: Integration Drives Efficiency Gains

Extraction quality determines downstream success, yet library construction remains the most error-prone phase. This has spurred the adoption of bead-linked transposon kits such as Illumina DNA Prep, which deliver even genome coverage from 1-500 ng input in 3.5 hours. Hybrid capture target-enrichment pushes sensitivity 10-100-fold, an essential benefit for liquid biopsy assays. Real-time QC modules now flag sub-optimal fragments mid-run, allowing on-the-fly protocol adjustments.

Workflow convergence is accelerating Illumina’s on-flow-cell chemistry, scheduled for 2025, which unites library prep and sequencing on a single consumable, promising lower contamination risk and shorter cycle times. Integrated suites that span extraction through data visualization are, therefore, reshaping procurement toward single-vendor ecosystems, further consolidating spend within the next-generation sequencing sample preparation market.

Geography Analysis

North America held 39.10% of 2025 revenue, anchored by robust healthcare reimbursement structures and clear regulatory pathways that reduce adoption risk. Illumina, Thermo Fisher Scientific, and Element Biosciences maintain regional manufacturing and support footprints, easing customer validation cycles. Canada’s community-hospital liquid-biopsy programs illustrate clinical uptake, while Mexico leverages proximity to U.S. suppliers to scale reference-lab capacity.

Europe benefits from coordinated research funding and infrastructural maturity across Germany, the United Kingdom, France, Italy, and Spain. Harmonized IVDR rules enable cross-border kit deployment, although additional documentation imposes cost overheads that smaller labs offset via consortium purchasing models. Emerging Eastern European markets gain technology transfer through joint projects with established genomic centers, broadening regional contribution to the next-generation sequencing sample preparation market size.

Asia Pacific is the fastest-growing region at a 14.22% CAGR as governments embed genomics in public-health agendas. India’s IndiGen initiative, which sequenced 1,000 genomes, jump-started local bio-banking capacity. China’s MGI Tech scales automated workstations domestically and exports to Southeast Asia, while Japan pioneers rapid sequencing in tertiary hospitals. Nonetheless, cold-chain logistics and varied regulatory standards remain hurdles that vendors address via ambient-temperature stabilizers and local compliance support offices.

Competitive Landscape

Market concentration is moderate: the top five vendors, such as Illumina, Thermo Fisher Scientific, Qiagen, Agilent, and MGI Tech, collectively control significant market share, reflecting both platform ownership and reagent attach rates. Illumina’s USD 350 million purchase of SomaLogic brings proteomics into its ecosystem, reinforcing multiomics cross-sell potential. Hitachi High-Tech’s majority stake in Nabsys expands electronic mapping capabilities, signaling a broader interest in structural-variant workflows.

Element Biosciences demonstrates how focused R&D and USD 277 million in fresh capital can quickly move from 40 to 190 sequencer installs in a year, challenging price-performance benchmarks. Vendors increasingly compete on total cost of ownership, workflow breadth, and integrated analytics rather than on read length or accuracy alone.

Strategic alliances with diagnostic labs, CROs, and agricultural genomic partners broaden application footprints and lock in consumable revenue.

Global NGS Sample Preparation Industry Leaders

Illumina, Inc.

Agilent Technologies, Inc.

Thermo Fisher Scientific Inc.

PerkinElmer Inc.

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Illumina agreed to acquire SomaLogic for USD 350 million to integrate the SomaScan proteomics assay with NGS workflows.

- February 2025: Agilent committed USD 725 million to double therapeutic nucleic acid manufacturing capacity, with new shipments slated for 2026.

- January 2025: GeneDx announced plans to acquire Fabric Genomics for up to USD 51 million to decentralize AI-powered genomic interpretation.

- July 2024: Labcorp broadened its Ultima Genomics partnership to apply whole-genome sequencing for minimal residual disease detection.

Global NGS Sample Preparation Market Report Scope

As per the scope of this report, next-generation sequencing (NGS) is a high-throughput technology that can acquire insight into any species at the genomic, transcriptomic, or epigenetic level. NGS has made it possible to gain genetic information from samples much faster with more reliability and low cost than ever before. Rapid developments in sequencing technologies have resulted in a significant increase in throughput capabilities and a cost reduction. The NGS Sample Preparation Market is Segmented by Product Class (Reagent and Consumables, Workstations), Application (Diagnostics, Drug Discovery, and Other Applications), End User (Hospitals and Clinics, Pharmaceutical and Biotechnology Companies, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

| Reagents & Consumables |

| Automation Workstations |

| Other Consumables |

| Nucleic-acid Extraction & Purification |

| Library Construction |

| Target Enrichment / Amplicon Generation |

| Quality Control & Quantification |

| Diagnostics |

| Drug Discovery / Functional Genomics |

| Agriculture & Animal Research |

| Other Research Applications |

| Hospitals & Reference Labs |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Contract Research Organizations |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Class | Reagents & Consumables | |

| Automation Workstations | ||

| Other Consumables | ||

| By Workflow Phase | Nucleic-acid Extraction & Purification | |

| Library Construction | ||

| Target Enrichment / Amplicon Generation | ||

| Quality Control & Quantification | ||

| By Application | Diagnostics | |

| Drug Discovery / Functional Genomics | ||

| Agriculture & Animal Research | ||

| Other Research Applications | ||

| By End-User | Hospitals & Reference Labs | |

| Pharmaceutical & Biotechnology Companies | ||

| Academic & Research Institutes | ||

| Contract Research Organizations | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the next-generation sequencing sample preparation market?

It is valued at USD 3.08 billion in 2026 and is projected to reach USD 5.95 billion by 2031.

Which product class dominates revenue?

Reagents and consumables account for 64.12% of 2025 revenue, reflecting recurring demand per sample.

Why is Asia Pacific considered the fastest-growing region?

Government-funded programs such as India’s IndiGen project, expanding pathogen surveillance, and rising healthcare investment drive a 14.22% CAGR in the region.

How are automation workstations impacting laboratory economics?

They reduce an eight-hour manual library prep to roughly 30 minutes, offering return on investment within 18 months for high-volume labs.

What regulatory changes affect laboratory developed tests in the United States?

The FDA’s May 2024 final rule phases out enforcement discretion over four years, requiring high-risk LDTs to undergo premarket review.

Page last updated on: