Market Overview

| Study Period | 2020 - 2031 |

|---|---|

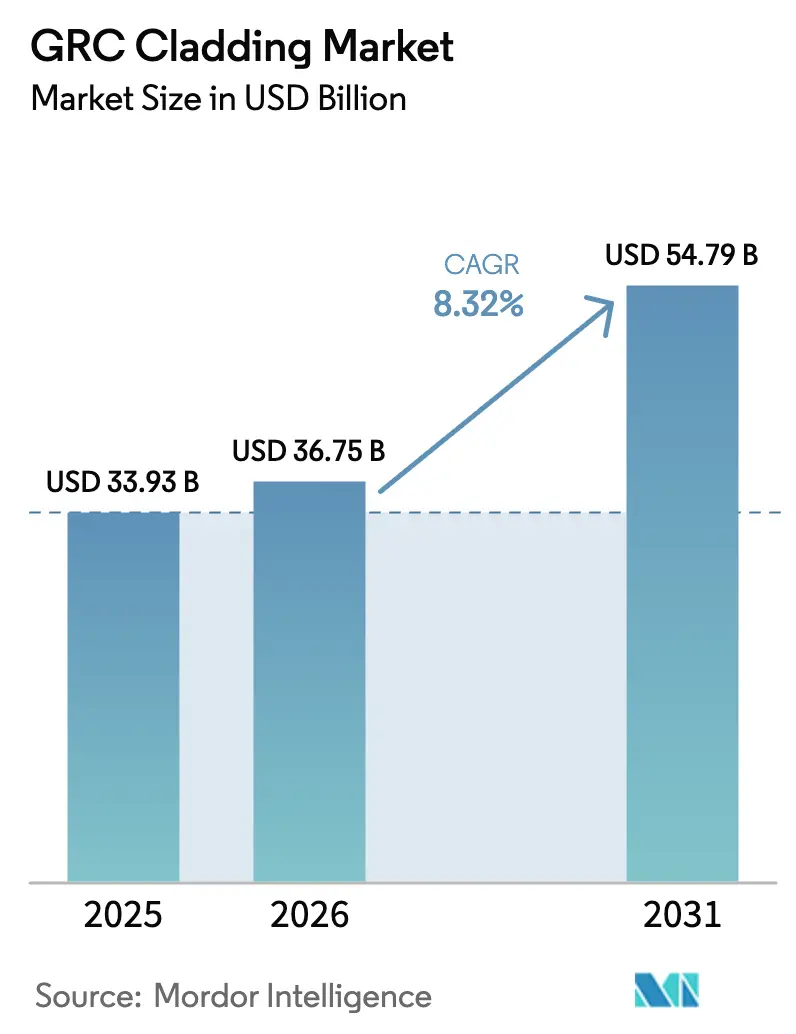

| Market Size (2026) | USD 36.75 Billion |

| Market Size (2031) | USD 54.79 Billion |

| Growth Rate (2026 - 2031) | 8.32% CAGR |

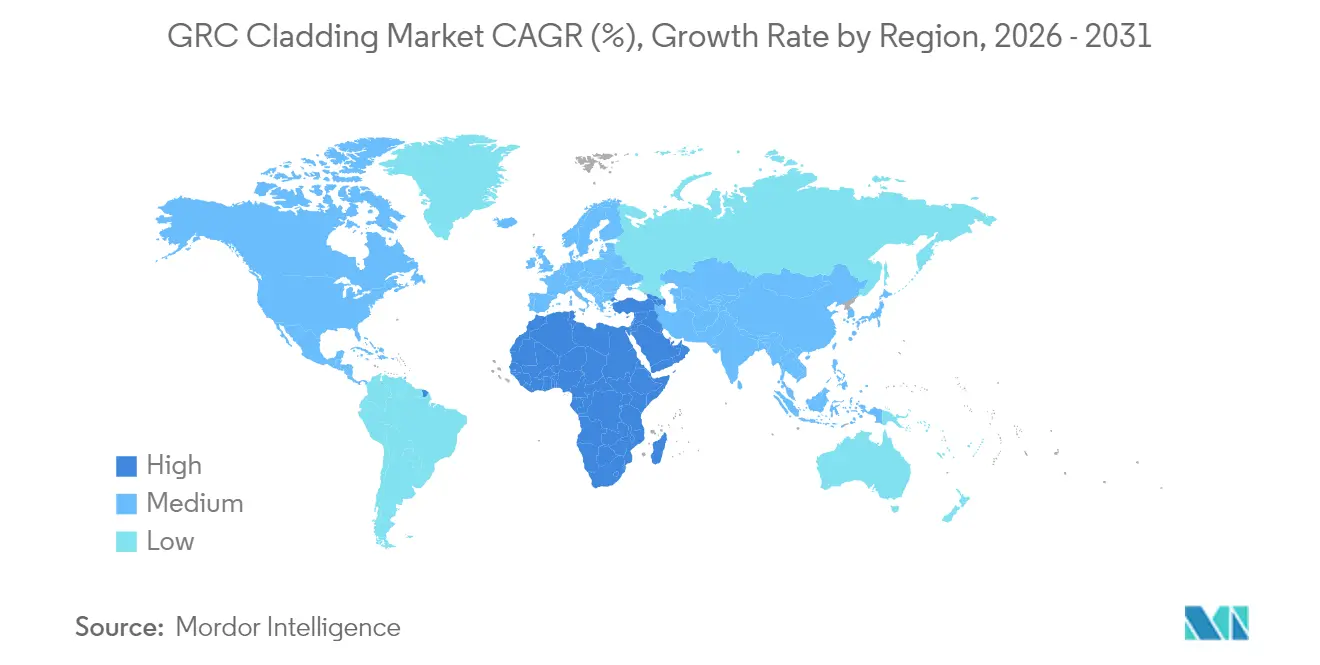

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GRC Cladding Market Analysis by Mordor Intelligence

The GRC cladding market size is expected to grow from USD 33.93 billion in 2025 to USD 36.75 billion in 2026 and is forecast to reach USD 54.79 billion by 2031 at 8.32% CAGR over 2026-2031. Growing preference for lightweight, non-combustible façades, combined with tighter fire-safety rules, positions glass-reinforced concrete (GRC) as the go-to alternative where traditional precast panels prove too heavy or inflexible. Developers value the material’s one quarter weight advantage over concrete, which trims structural loads and shortens construction cycles. Investment flows into smart city projects across Asia-Pacific, rapid adoption of modular construction in the Middle East, and the pursuit of lower life-cycle costs in North America reinforce demand. Meanwhile, industry players accelerate low-carbon formulations to match emerging embodied carbon regulations, keeping the GRC cladding market on an innovation path.[1]https://www.wbdg.org/resources/seismic-safety-building-envelope.

Key Report Takeaways

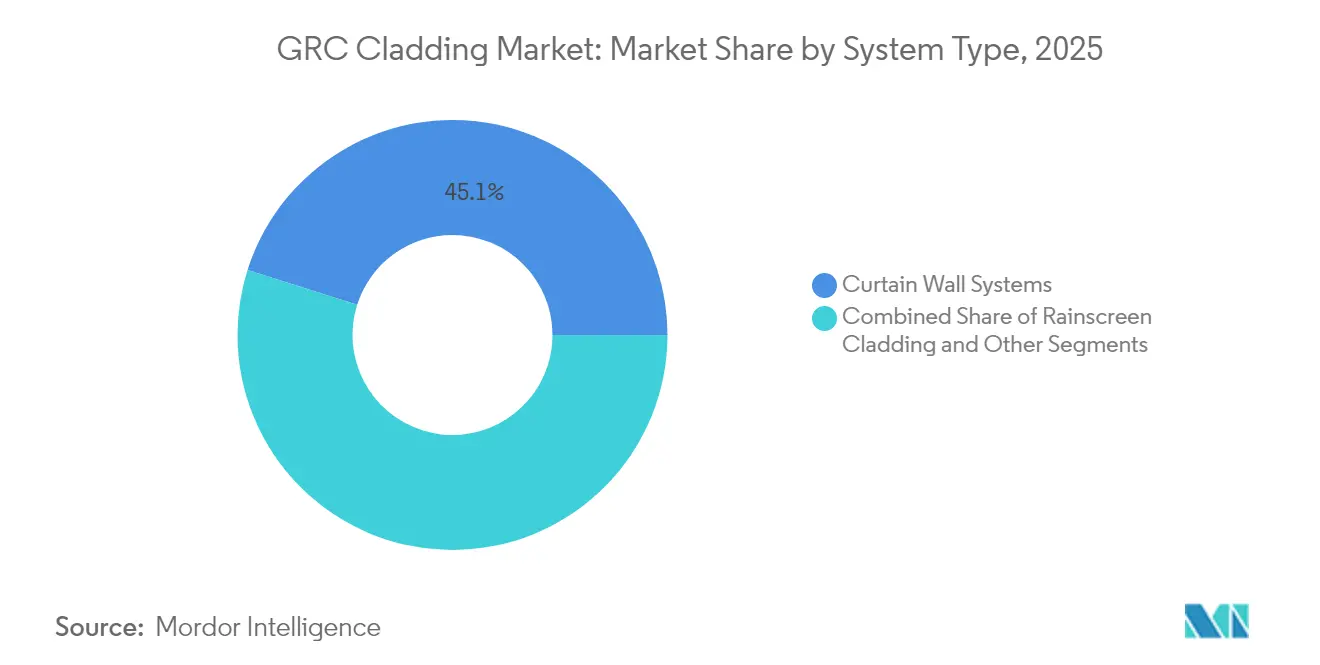

- By system type, curtain wall systems led with 45.12% revenue share in 2025 while the “Others” category primarily heritage skins and modular assemblies recorded the swiftest 9.12% CAGR through 2031.

- By application, commercial buildings controlled 51.88% of the GRC cladding market share in 2025; residential construction is poised to expand at a 9.74% CAGR to 2031.

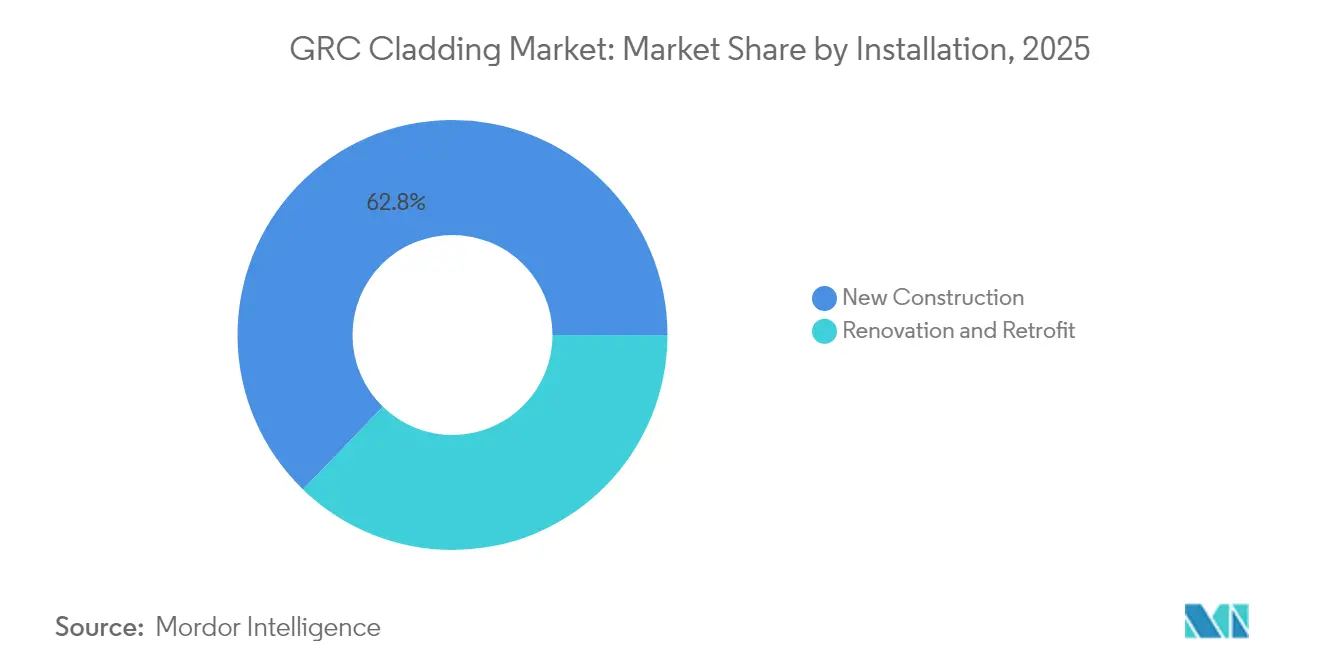

- By installation, new-build projects captured 62.76% of demand in 2025, whereas renovation and retrofit activity is advancing at the highest 9.76% CAGR as fire-safety remediation accelerates.

- By geography, Asia-Pacific dominated with 42.98% of 2025 revenues; the Middle East & Africa is growing the fastest at 9.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global GRC Cladding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization & smart-city construction boom | 2.1% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| High-rise demand for lightweight, high-strength facades | 1.8% | Global, concentrated in APAC & North America | Long term (≥ 4 years) |

| Stricter fire-safety & seismic codes for cladding | 1.5% | Australia, UK, North America with global adoption | Short term (≤ 2 years) |

| Superior durability & low life-cycle cost | 1.2% | Global | Long term (≥ 4 years) |

| Off-site modular construction uptake | 0.9% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Heritage façade retrofits using ultra-thin GRC skins | 0.3% | Europe, North America historic districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization & Smart-City Construction Boom

Surging city populations across China, India, and Southeast Asia stretch local infrastructure and energize demand for high-performance façades. India’s construction GDP jumped 13.3% year-on-year in Q3 2024 as Smart Cities and Make in India initiatives funneled public spending into mixed-use towers and transit hubs. Municipal design codes increasingly reward energy-efficient envelopes, steering architects toward GRC assemblies that blend thermal mass, intricate form, and compatibility with building-integrated photovoltaics. China National Building Materials’ 15.14% 2024 revenue rise signals a durable appetite for innovative cladding across the region’s megaproject pipeline[2]https://www.tipranks.com/news/company-announcements/china-national-building-material-reports-strong-financial-growth-for-bnbm-in-2024. Beyond tier-one cities, developers in India’s secondary metros and Vietnam’s emerging industrial zones specify GRC cladding market solutions to speed project delivery without sacrificing aesthetics.

Stricter Fire-Safety & Seismic Codes for Cladding

Post-Grenfell regulation reshaped façade procurement. Victoria’s audit flagged more than 800 buildings for immediate remediation, fueling demand for non-combustible, test-certified panels. GRC passes NFPA 285 without extensive fire-stopping details, simplifying compliance for North American projects. Accredited UAE producers, guided by International Fire Consultants, now export to multiple jurisdictions, signaling global standardization. Governments from Australia to Canada plan staged bans on combustible façades, locking in a multi-year tailwind for the GRC cladding market.

Superior Durability & Low Life-Cycle Cost

Fifty-year service-life expectations, UV stability, and low water absorption minimize maintenance. Proven products such as Rieder’s concrete skin series require only periodic washing, sidestepping the repaint cycles that burden metal panels. Life-cycle studies show that after 15-20 years, total ownership cost undercuts alternatives once repainting, sealant renewal, or corrosion mitigation enter the equation. When supplementary cementitious materials like fly ash cut embodied carbon by up to 40%, owners satisfy durability and sustainability targets in one specification. These attributes solidify the GRC cladding market as a premium yet economical choice for long-term assets.

Heritage Façade Retrofits Using Ultra-Thin GRC Skins

Conservation architects deploy 12-15 mm panels to replicate historical stonework on Victorian, Beaux-Arts, and Art Deco landmarks without overloading aging substrates. European grant programs fund energy upgrades that pair ventilated GRC rainscreens with insulation, merging preservation with performance. Specialized fabricators command premium pricing by mastering custom molds and color-matched surface treatments. As municipalities expand retrofit incentives, the GRC cladding market gains a resilient niche in culturally sensitive districts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher upfront cost versus conventional concrete panels | -1.8% | Global, particularly price-sensitive markets | Short term (≤ 2 years) |

| Competition from low-cost metal composite cladding | -1.2% | Emerging markets, value-engineering projects | Medium term (2-4 years) |

| Cement and glass fiber prices are volatile | -0.9% | Global, supply-chain dependent regions | Short term (≤ 2 years) |

| Embodied carbon scrutiny of cementitious facades | -0.6% | Europe, North America with green building mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Cost Versus Conventional Concrete Panel

Sprayed GRC requires alkali-resistant glass fibers and skilled applicators, elevating material and labor premiums. Yet structural savings from lighter envelopes shrink the delta when the entire project economics are tallied. On geometrically complex facades curved or perforated GRC’s moldability often undercuts stone or custom metal, pushing owners back to the GRC cladding market after value-engineering exercises.

Competition from Low-Cost Metal Composite Cladding

Aluminum composite systems remain 40-60% cheaper in initial bids, especially where enforcement of fire codes lags. Insurance carriers, however, now surcharge combustible façades, eroding long-term savings. As governments roll out blanket bans, price-driven choice narrows, steering projects toward the GRC cladding market despite capital-cost sensitivity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Curtain Wall Integration Drives Complexity

Curtain walls captured 45.12% of the GRC cladding market size in 2025, reflecting their prevalence on high-rise commercial facades where architects pair lightweight panes with generous glazing for a daylight strategy. The segment’s demanding tolerances and engineered anchors elevate barriers to entry, rewarding full-service manufacturers that offer design-assist and on-site technical crews. Rainscreen installations follow, leveraging GRC’s vapor permeability to manage condensation in humid zones, while ultra-thin heritage skins and modular units form the fastest-growing “Others” category at a 9.12% CAGR. Design offices increasingly explore perforated panels that double as solar-shading devices, and early prototype projects embed thin-film PV directly onto GRC substrates to create energy-positive façades.

In the longer-term outlook, the GRC cladding market sees system convergence, where hybrid curtain wall–rainscreen assemblies meet seismic, thermal, and acoustic goals in a single package. Manufacturers invest in digital twins and CNC mold production to serve bespoke geometry at scale. Engineering consultancies favor GRC over heavier concrete in hoist-restricted urban sites, and GRCA technical bulletins standardize testing to accelerate approvals. Sustainability mandates push for demountable curtain wall frames, enabling future material separation and recycling, a design ethos well matched to GRC’s cementitious recyclability.

By Application: Commercial Dominance Faces Residential Disruption

Commercial buildings held 51.88% of the GRC cladding market share in 2025, propelled by corporate headquarters, life-science labs, and civic buildings where expressive facades reinforce brand identity. Reconfigurable molds and color-matched surface treatments deliver signature looks without artisan stone costs, keeping GRC on architects’ shortlists for statement atria and lobby extensions. Health-care and education facilities add institutional volume, seeking non-combustible skins that withstand heavy foot traffic and stringent hygiene standards.

Residential construction grows at a brisk 9.74% CAGR as mid-rise developers embrace factory-installed wall panels that abbreviate site schedules and limit neighborhood disruption. Modular apartment blocks in London’s regeneration districts and Tokyo’s infill sites already specify GRC as a standard module finish. Data-center operators, classified under “Others,” adopt GRC for fire-rated walls that also shield electromagnetic interference. With global hyperscale capacity projected to double by 2026, demand from this niche could outpace legacy institutional segments, enlarging the total GRC cladding market addressable base.

By Installation: Retrofit Market Gains Momentum

New-build activity claimed 62.76% of the 2025 GRC cladding market size, supported by early integration of panelized envelopes into BIM workflows. Engineers optimize connection plates and story-height panels before groundbreaking, slashing rework and contingencies. Yet retrofit programs underpin the fastest 9.76% CAGR, propelled by mandatory replacement of combustible aluminum composites. In Australia, public funding offsets replacement costs, and specialty contractors offer turn-key swap-outs that keep occupants in place.

Heritage retrofits rely on ultra-thin GRC skins affixed over original masonry with stainless split-pins that preserve ventilation gaps. This approach raises thermal performance by 20-30% while honoring preservation charters. Retrofits also unlock embodied-carbon credits through life extension, appealing to investors tracking ESG metrics. As more insurance carriers refuse coverage for high-risk cladding, retrofit volumes could reach parity with new-build demand by the early 2030s, reshaping revenue allocation across the GRC cladding market.

Geography Analysis

Asia-Pacific commanded 42.98% of 2025 revenue, underpinned by China’s megacity pipeline and India’s USD 1.4 trillion construction roadmap to 2025. Local producers such as CNBM scale output via automated spray lines and robotic trimming, shortening lead times for cross-border projects in ASEAN. Smart-city blueprints stipulate low-carbon façades and integrated renewables, dovetailing with evolving GRC panels that host PV laminates. Rising labor costs in coastal China push some fabrication toward Vietnam and Indonesia, broadening regional supply and intensifying price competition within the GRC cladding market.

The Middle East & Africa records the highest 9.71% CAGR as Saudi Arabia’s NEOM, UAE’s cultural museums, and Egypt’s New Administrative Capital specify non-combustible façades resilient to 50 °C summers. Domestic champions in Oman and Qatar leverage GRCA membership to win public tenders, while European players partner locally to navigate import duties and heat-of-hydration challenges. New civil-defense codes promulgated in 2025 synchronize with NFPA 285, tightening envelope fire tests and elevating GRC’s risk-mitigation appeal.

North America and Europe exhibit lower but steady growth, driven by regulation over volume. U.S. jurisdictions adopt NFPA 285-based exceptions for non-combustible systems, simplifying approval of GRC rainscreens over traditional cavity-barrier layouts. Europe’s 2027 embodied-carbon ceiling accelerates low-clinker formulations as players seek Environmental Product Declarations to secure public-sector projects. Retrofit demand spikes in the UK, Ireland, and France, where combustible panels face legal removal deadlines, keeping order books robust across the mature yet lucrative GRC cladding market.

Competitive Landscape

The GRC cladding market remains moderately fragmented. The top five players account for roughly 35-40% of global revenue, while dozens of regional specialists fill domestic pipelines. European incumbents differentiate through color-consistent, through-pigmented skins and carbon-neutral formulations. Middle-East fabricators excel in supersized panel logistics, shipping 6 m-long units to desert megaprojects with integrated lifting lugs[4]https://www.grca.online/grca-memberships/full-members/zanette-srl. Asian producers emphasize cost efficiency, betting on high-volume residential towers to absorb capacity.

Technology shifts dictate competitive order. Firms deploying digitally driven mold routing can cut lead times by 25-30%, winning design-bid-build schedules that penalize delays. Adoption of three-dimensional glass-fiber weaves improves out-of-plane stiffness, permitting thinner panels with equal span capability and unlocking shipping savings. GRCA Full-Member certifications, renewed by several plants in January 2025, remain a hallmark of quality and influence specifier shortlists. Strategic exits underscore specialization pressures: Ibstock’s March 2025 withdrawal freed continental market share for Rieder and SigmaRoc’s cladding divisions. In April 2025, SigmaRoc sealed a partnership with Adaptavate to commercialize low-carbon wallboard chemistry that could migrate into GRC mixes, indicating cross-fertilization between façade and interior board technologies. Overall rivalry gravitates toward sustainability credentials, factory automation, and turnkey installation packages that lower total project risk for developers.

GRC Cladding Industry Leaders

Clark Pacific

Ultratech Cement Pvt Ltd

BB Fiberbeton

Sto Group

Rieder Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Ibstock announced its strategic withdrawal from GRC cladding to focus on core masonry products, opening supply opportunities in Europe

- April 2025: SigmaRoc partnered with Adaptavate under Project Crystal to industrialize low-carbon calcium-carbonate wallboards, signaling wider cement-alternative exploration

- March 2024: Henley Group expanded into GRC solutions, integrating architectural masonry experience with cladding fabrication

- January 2024: China National Building Material invested in advanced façade materials, underpinning a 15.14% revenue uptick

Global GRC Cladding Market Report Scope

GRC cladding, or glass fiber reinforced concrete, is a highly versatile product comprising numerous ingredients and elements, including fiberglass. By molding GRC concrete into thin, lightweight panels, it can be shaped and altered into a variety of different and extensive structures. This makes it one of the ideal options for alternative prefabricated cladding.

The GRC cladding market is segmented by application (commercial construction, residential construction, and infrastructure construction) and region (North America, Europe, Middle East and Africa, Asia-Pacific, and Latin America). The report offers market size and forecasts for GRC cladding in value (USD) for all the above segments.

By System Type

| Rainscreen Cladding |

| Curtain Wall Systems |

| Others |

By Application

| Residential |

| Commercial |

| Others |

By Installation

| New Construction |

| Renovation & Retrofit |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By System Type | Rainscreen Cladding | |

| Curtain Wall Systems | ||

| Others | ||

| By Application | Residential | |

| Commercial | ||

| Others | ||

| By Installation | New Construction | |

| Renovation & Retrofit | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the GRC cladding market by 2031?

The GRC cladding market is expected to reach USD 54.79 billion by 2031, reflecting an 8.32% CAGR over 2026-2031.

Which region accounts for the largest share of GRC cladding demand?

Asia-Pacific held 42.98% of global 2025 revenues, driven by rapid urbanization and infrastructure spending.

Why are developers switching from aluminum composite to GRC façades?

Stricter fire-safety codes and rising insurance premiums on combustible panels push owners toward non-combustible GRC systems that simplify compliance and lower long-term risk.

How does GRC support modular construction?

Lightweight panels integrate into factory-built volumetric modules, trimming project schedules by up to 50% and ensuring consistent quality under controlled conditions.

Page last updated on: