Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

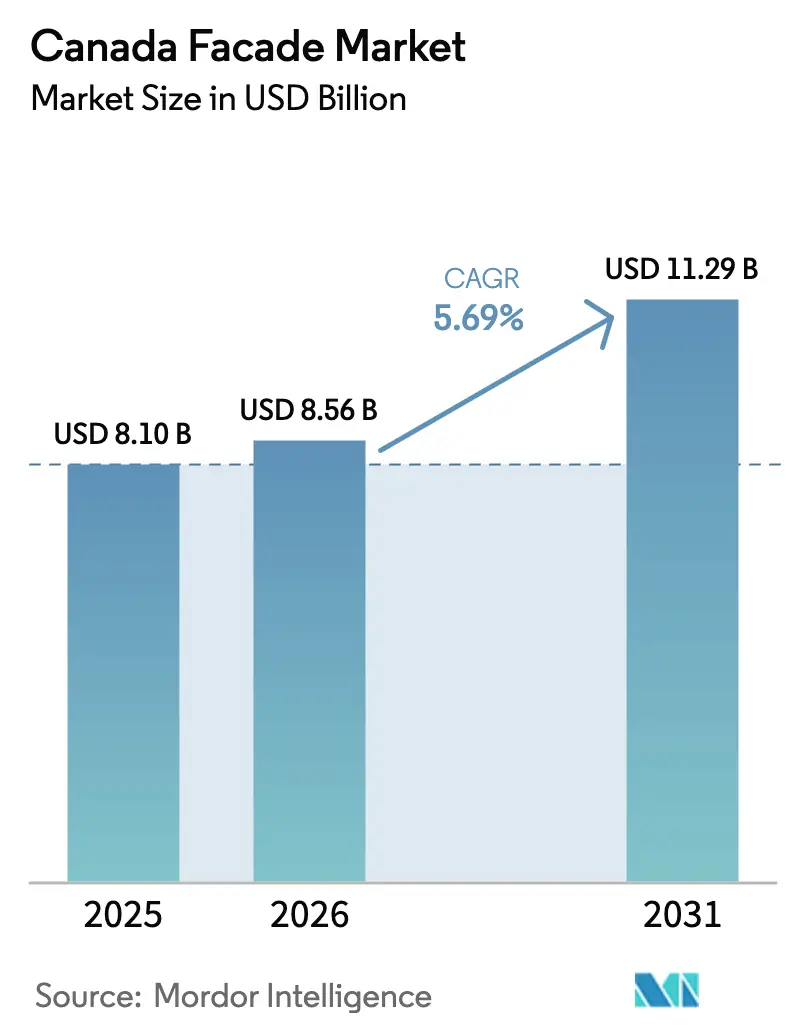

| Base Year Market Size (2025) | USD 8.10 Billion |

| Market Size (2026) | USD 8.56 Billion |

| Market Size (2031) | USD 11.29 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Facade Market Analysis by Mordor Intelligence

Canada facades market size in 2026 is estimated at USD 8.56 billion, growing from 2025 value of USD 8.10 billion with 2031 projections showing USD 11.29 billion, growing at 5.69% CAGR over 2026-2031. Performance-based energy codes, federal retrofit incentives, and a nationwide housing boom are expanding specification budgets and accelerating project pipelines. Rapid urban densification in Toronto and Vancouver is lifting demand for high-performance curtain walls and non-ventilated envelopes that satisfy NECB 2020 tiered efficiency targets. Supply chain tightness in architectural glass and aluminum continues to pressure bids, yet contractors are mitigating exposure through prefabricated panels and price-escalation clauses. Skilled-labor shortages remain the most immediate drag on project schedules, prompting owners to favor modular assemblies that reduce on-site hours and lessen certification bottlenecks. Opportunistic investors are also targeting deep-retrofit portfolios, expecting carbon-based asset valuations to solidify over the next decade.

Key Report Takeaways

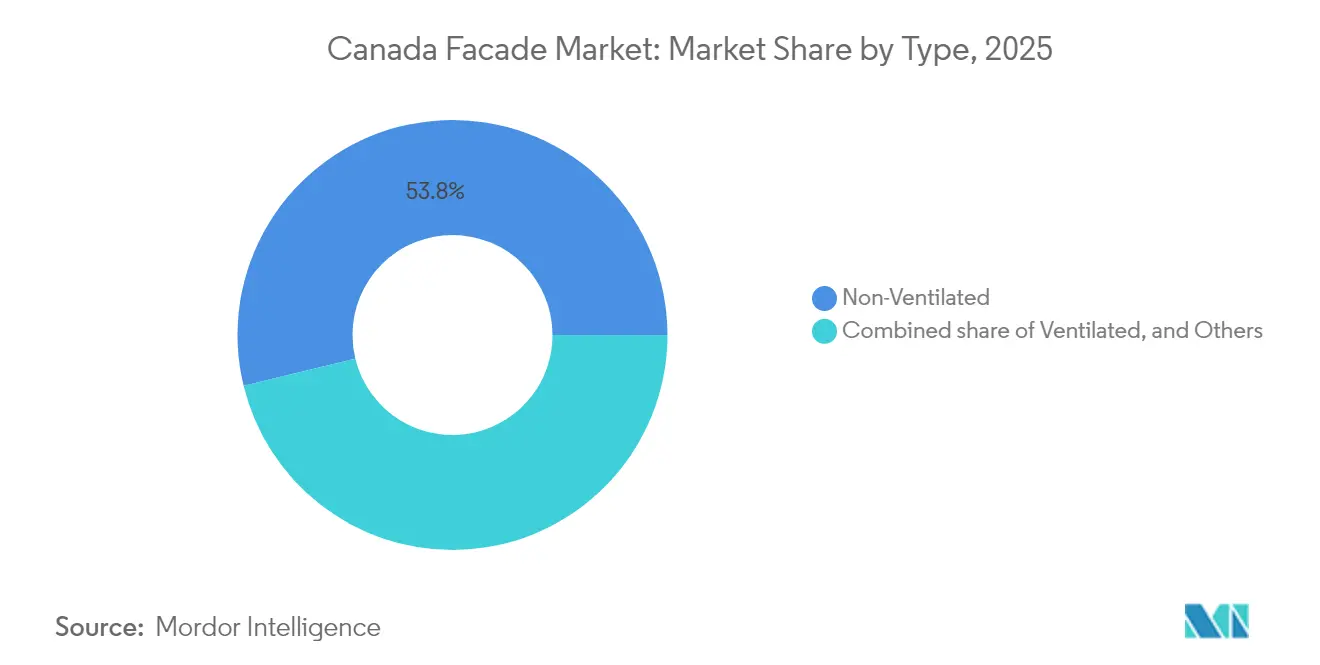

- By type, non-ventilated systems led with 53.80% of the Canada facades market share in 2025; the segment is advancing at a 6.19% CAGR through 2031.

- By façade system type, curtain wall assemblies captureda 44.60% share in 2025, while their high-rise focus supports a 6.28% CAGR to 2031.

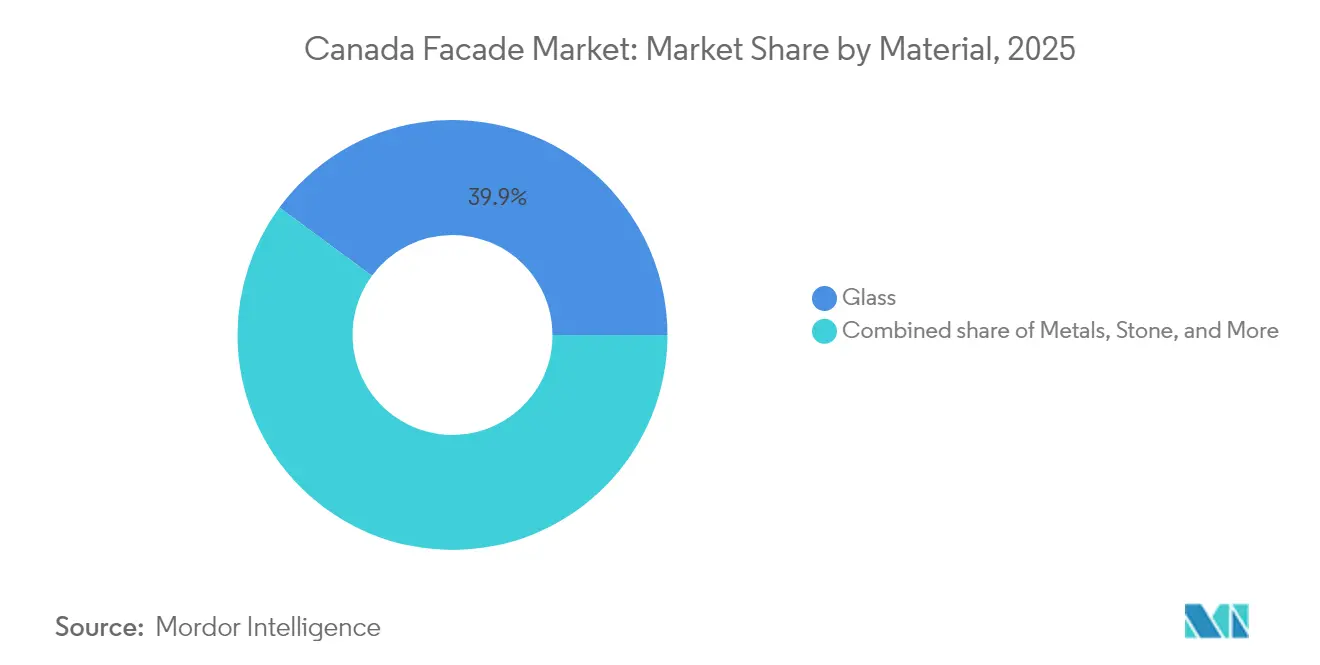

- By material, glass commanded 39.90% of the Canada facades market size in 2025 and is projected to grow at a 5.93% CAGR on the back of low-e and dynamic glazing adoption.

- By installation, new-construction projects accounted for a 55.50% share in 2025, with the category pacing a 6.25% CAGR amid federal housing targets.

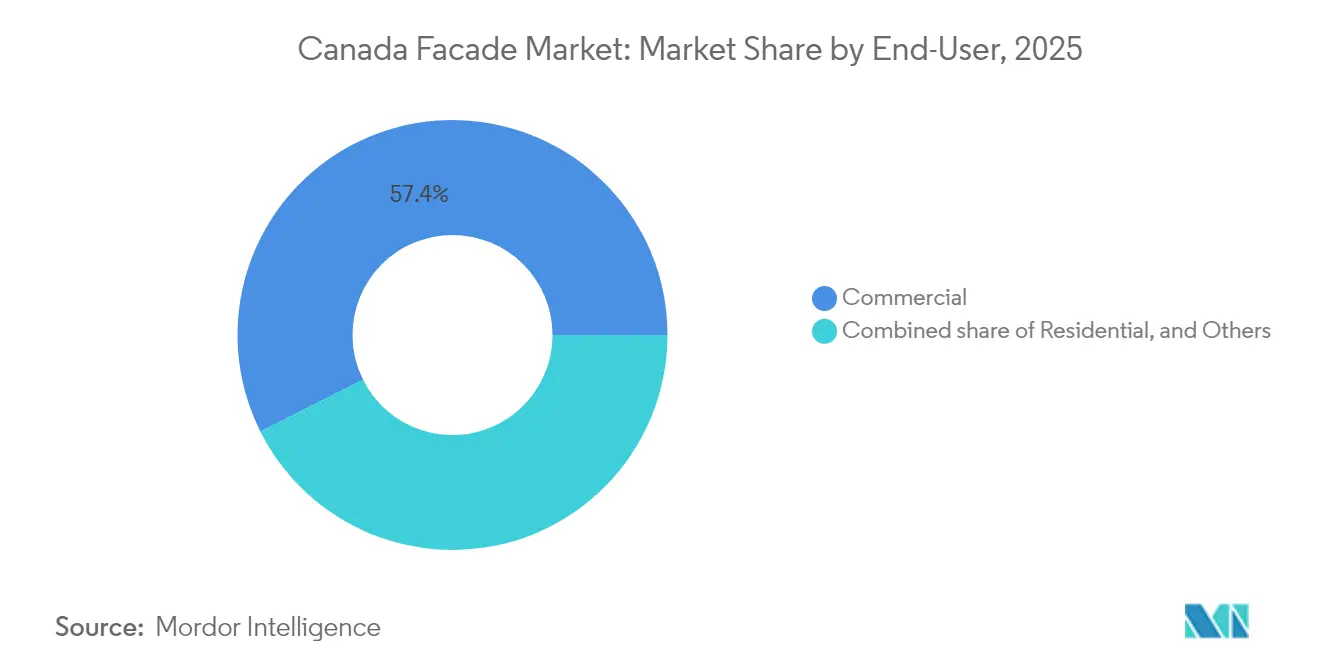

- By end-user, commercial buildings held a 57.40% share in 2025 and are expanding at a 6.38% CAGR as offices, retail, and institutional owners pursue net-zero retrofits.

- By geography, Ontario dominated with a 33.00% share in 2025; however, British Columbia’s policy environment is fueling faster 6.52% CAGR growth in Ontario, edging out other provinces by 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Facade Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in high-rise residential projects in GTA & Metro Vancouver | +1.2% | Ontario & British Columbia, spillover to Alberta | Short term (≤ 2 years) |

| Stricter NECB 2020 / Tiered Net-Zero codes adoption | +0.9% | National, with early adoption in BC, Ontario | Medium term (2-4 years) |

| Aging 1970-1990 building stock driving façade retrofits | +0.8% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Federal "Greener Homes" & CMHC deep-retrofit grants | +0.7% | National, higher uptake in Quebec, Ontario | Medium term (2-4 years) |

| Mass-timber mid-rise boom needing hybrid façade solutions | +0.5% | British Columbia, expanding to Ontario, Quebec | Long term (≥ 4 years) |

| Municipal zero-carbon mandates (Toronto, Vancouver) | +0.4% | Toronto, Vancouver, spreading to other major cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High-Rise Residential Projects in GTA & Metro Vancouver

Toronto’s One Bloor West and Vancouver’s cluster of zero-emission towers are redefining skyline profiles and stretching curtain-wall engineering limits. Developers in both metros are now specifying four-sided structural-glazed façades with triple low-e glass to withstand extreme wind pressures and meet Tier 4 airtightness thresholds[1]ConstructConnect, “Canada’s first supertall building: One Bloor West reaches major milestone,” canada.constructconnect.com. Contractors are forward-purchasing mullion stock to hedge aluminum volatility and reserving crane slots up to 18 months ahead, tightening supply across Canada facade market projects in smaller cities. Lending trends favor large multi-phase schemes, giving envelope suppliers predictable volume but concentrating risk in two metropolitan hubs. Provincial housing pledges for 1.5 million new units in Ontario and 0.5 million in British Columbia secure a multiyear pipeline; however, unionized labor shortages could delay occupancy certificates and escalate contractual penalties[2]CBC News, “Construction labour crunch leaves Canada in need of boosting ranks of home builders,” cbc.ca.

Stricter NECB 2020 / Tiered Net-Zero Codes Adoption

Whole-building airtightness testing and reduced assembly U-values embedded in NECB 2020 have made energy performance a core procurement criterion rather than an optional upgrade. Provinces deploying Tier 4 requirements (60% energy reduction versus baseline) are spurring orders for vacuum-insulated panels, thermally broken anchors and high-spectral-selectivity glazing. Disparate provincial timelines complicate national catalog strategies, forcing manufacturers to carry multiple SKUs for identical profile lines. The Reconciliation Agreement on Construction Codes aims to align compliance by 2025, promising a unified market specification that could cut design iteration costs by up to 15%. Third-party consultants are capitalizing on code complexity, providing integrated envelope modeling, blower-door calibration and commissioning services.

Aging 1970-1990 Building Stock Driving Façade Retrofits

Nearly half of Canadian rental units were constructed before energy codes became mainstream, and their thin aluminum frames and single glazing leak thermal energy and moisture. Owners are adopting Prefabricated Exterior Energy Retrofit (PEER) panels that combine insulation, cladding, and fenestration in a single lift, slashing install time from weeks to days [3]Natural Resources Canada, “Prefabricated Exterior Energy Retrofit Project Guide,” natural-resources.canada.ca. Community-housing pilots reveal heat-loss reductions of 65% and airtightness gains of 75% post-retrofit, results that are spurring provincial grant extensions beyond 2026. Heritage-age mid-century assets, once considered demolition candidates, are now earmarked for deep-energy retrofits that respect original façades while integrating fibrous-insulation cores and low-carbon cladding skins.

Federal Greener Homes & CMHC Deep-Retrofit Grants

More than 524,000 homeowner applications under the Canada Greener Homes program have accelerated demand for ENERGY STAR windows, triple-pane doors and integrated blinds. The USD 40,000 interest-free loan product finances whole-envelope overhauls and is steering small contractors toward volume-based purchasing agreements with facade component distributors. CMHC’s Greener Neighbourhoods Pilot validates the Energiesprong model, opening a pipeline for mass-customized panel production that could bring scale to retrofit supply. While new applications closed in several provinces due to budget exhaustion, industry lobbying seeks program renewal in 2026 to prevent job losses across window-fabrication corridors in Ontario and Quebec.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile aluminium & architectural glass prices | -0.6% | National, with higher impact in import-dependent regions | Short term (≤ 2 years) |

| Shortage of CSA-certified façade installers & inspectors | -0.8% | National, acute in Ontario, British Columbia, Nova Scotia | Medium term (2-4 years) |

| Rising insurance premiums for combustible cladding | –0.4% | National; higher risk-loading in high-rise urban cores | Medium term (2–4 years) |

| Patchwork demolition-waste bylaws complicating retrofits | –0.3% | Municipal hot-spots in British Columbia, Ontario, Quebec | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Aluminum & Architectural Glass Prices

Industrial Product Price Index data show non-ferrous metals up 7.6% year-over-year, squeezing margins on unitized curtain walls whose frame cost can exceed 40% of total assembly value[4]Statistics Canada, “Industrial product and raw materials price indexes, June 2025,” www150.statcan.gc.ca. Canadian buyers resisted 46% of manufacturer price increases in 2024, forcing a shift to escalation clauses pegged to LME averages. Tariff uncertainty on U.S. imports prompted some fabricators to reroute supply through European rolling mills, adding lead-time risk amid tight project schedules. Larger contractors hedge procurement through futures and swap agreements, but mid-tier installers lack financial instruments, exposing them to spot-price hikes that can erode entire project profits.

Shortage of CSA-Certified Façade Installers & Inspectors

Construction vacancy rates hover near 80,000 jobs, and 22% of the current workforce will retire by 2035. Ontario alone needs 100,000 additional tradespeople to hit housing targets, yet only 5,000 apprentices enroll annually in relevant programs. Curtain-wall crews require CSA A440 certification, and inspector backlogs are stretching occupancy timelines by up to six weeks in peak quarters. Contractors now “labor hoard,” paying full wages during slow periods to guarantee crews for upcoming projects, a tactic that inflates overhead costs and diminishes market efficiency. Immigration pathways and Temporary Foreign Worker permits offer relief, but housing shortages for new arrivals limit immediate scalability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Non-Ventilated Systems Drive Energy Performance

Non-ventilated assemblies accounted for 53.80% of the Canada facades market size in 2025 as designers prioritized airtightness and thermal continuity under NECB 2020. The segment’s 6.19% CAGR underscores owner preference for lower maintenance and simplified detailing when compared with back-ventilated rainscreens. Ventilated designs remain essential in high-precipitation coastal zones where pressure-equalized cavities mitigate moisture ingress. Hybrid panels integrating switchable air cavities emerged in 2025 pilot projects, promising seasonal flexibility between ventilated and non-ventilated modes.

Mass-timber mid-rise buildings, especially in British Columbia, favor lightweight non-ventilated panels that preserve wood’s thermal mass and limit concealed cavity fire risk. Prefabrication hubs in the Greater Toronto Area now ship cassette-style cladding sections complete with pre-glazed openings, reducing crane swings and on-site labor hours. Over the forecast horizon, embedded sensors in non-ventilated skins will feed commissioning data back to asset managers, a feature expected to sharpen warranty terms and reduce lifecycle carbon calculations.

By Façade System Type: Curtain Walls Lead Premium Segment

Curtain walls dominated the category with a 44.60% share, reflecting their ubiquity on Canada's facade market skyline projects and their 6.28% CAGR trajectory. Four-sided structural glazing, larger IGUs, and thermally broken unitized frames are now standard above 40 stories, shifting project specifications toward multinational fabricators with strong engineering support. Rainscreen cladding commands mid-rise and retrofit niches, aided by regional fabricators who can pivot quickly to local aesthetic codes.

Ontario’s supertall SkyTower integrates tuned-damper curtain wall segments to manage lateral drift, a first for Canadian residential towers. In Vancouver, point-fixed glass façades fitted with vacuum panels deliver R-values exceeding NECB Tier 4 targets without sacrificing daylight. “Others” in this category—such as photovoltaic curtain walls—are expected to outpace the broader segment post-2028 once feed-in tariffs stabilize.

By Material: Glass Dominance Reflects Architectural Preferences

Glass held a 39.90% share in 2025, a testament to the country’s daylighting ethos and tenant demand for unobstructed views. Despite embodied-carbon scrutiny, double-skin façades with automated blinds are enabling compliance with NECB 2020 while sustaining generous window-to-wall ratios. Metal follows as the default framing and cladding choice for industrial facilities where durability and insurance premiums drive specification.

High-selectivity coatings, inert gas fills and thermochromic layers are pushing center-of-glass U-values below 0.6 W/m²-K. AGC and Saint-Gobain both unveiled triple-silver low-e products optimized for Canadian HDD zones, enhancing the competitive landscape for premium glazing. Fiber-reinforced polymers are gaining traction in edge restraints for their lower thermal bridging and corrosion resistance, particularly in coastal British Columbia projects.

By Installation: New Construction Leads Despite Retrofit Growth

New-builds represented 55.50% of the Canada facades market size in 2025, buoyed by over USD 22.2 billion in building investment recorded for March 2025. High-rise condos and institutional expansions dominate volume, yet retrofit CAGRs inch upward as Greener Homes loans unlock capital for deep-envelope upgrades. Developers of purpose-built rentals now integrate façade prefabrication into pro-formas to offset rising interest rates and labor premiums.

Retrofit specialists are leveraging laser scanning and digital twins to produce panelized overlays that anchor to existing spandrels without intrusive demolition, shrinking tenant displacement time. Accelerated depreciation schedules for energy-efficient capital improvements further tilt ROI calculations toward envelope upgrades over purely mechanical interventions.

By End-User: Commercial Sector Drives Premium Demand

Commercial facilities captured a 57.40% share in 2025 and propelled a 6.38% CAGR amid office tower repositioning, retail-center facelifts, and hospital megaprojects. The Peter Gilgan Mississauga Hospital alone will consume 70,000 m² of curtain wall glass, illustrating how a handful of institutional jobs can sway annual material demand.

Residential demand is tied closely to provincial housing starts and municipal inclusionary zoning policies that sometimes mandate green-building certifications, nudging budget-constrained condo projects toward cost-optimized rainscreens. Industrial and data-center users are adopting insulated metal panels with integrated vapor barriers to satisfy temperature and humidity control requirements, widening supplier portfolios.

Geography Analysis

Ontario remained the epicenter with 33.00% of the Canada facades market share in 2025, fueled by the Greater Toronto Area’s super-tall pipeline and the province’s 1.5 million-home target. Provincial policy supports net-zero new builds by 2040, compelling developers to specify triple-glazed assemblies and thermally broken anchors. The province’s 6.52% CAGR through 2031 reflects both volume and a pivot toward premium specifications.

British Columbia is Canada’s policy laboratory for zero-carbon construction, and Vancouver’s 2025 mandate for near-zero-emission buildings is already redirecting supplier R&D budgets toward ultra-low-U glass and mass-timber-friendly cladding connections. Demolition bylaws that require 90% material recycling are accelerating the adoption of demountable façades designed for end-of-life disassembly. The province’s growth is amplified by a mass-timber mid-rise boom, necessitating hybrid façade solutions that pair light metal rainscreens with timber fire-stop details.

Quebec benefits from Saint-Gobain’s USD 126 million electrification of its Ste-Catherine wallboard line, positioning the province as a hub for low-carbon envelope materials. Provincial targets call for 860,000 new housing units by 2030, and Hydro-Québec’s low-cost renewable power supports electrification of façade manufacturing hubs. Alberta and the rest of Canada collectively absorb resource-sector capital and distributed infrastructure projects, offering steady but less concentrated opportunities for façade suppliers.

Competitive Landscape

The Canadian Façade Market is moderately fragmented: multinational glazing giants dominate super-tall curtain walls, while domestic cladding contractors compete aggressively in retrofit and mid-rise segments. Saint-Gobain’s USD 880 million purchase of Bailey Group added 12 regional plants and broadened its metal envelope portfolio. Kingspan’s leadership shuffle and the upcoming Mattoon insulated-panel plant underscore the firm’s North American growth trajectory.

Prefabrication and digital design are primary battlegrounds. Contractors deploying generative BIM and robotic welding lines can cut shop-floor cycle times by 35%, enabling rapid turnaround on congested project schedules. Environmental disclosures are now a big differentiator, with CarbonLow™ wallboard and low-carbon glass securing LEED and CaGBC credits that sway public-sector tenders.

Local content rules remain a flashpoint. The Ontario Glass and Metal Association’s plea to revoke a USD 140 million hospital façade award to a U.S. firm highlights political sensitivities around domestic employment and supply resilience. Firms that maintain CSA certification programs and apprenticeship pipelines are increasingly favored in public-private-partnership procurements.

Canada Facade Industry Leaders

Saint-Gobain Corporation

AGC Glass North America

Flynn Group of Companies

Enclos Corp.

Permasteelisa North America

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: ATCO Structures acquired NRB Modular Solutions for USD 40 million, deepening its modular housing footprint.

- July 2025: The federal government invested USD 10 million in a carbon-capture cement plant targeting 30,000 t CO₂ removal annually.

- October 2024: Saint-Gobain Canada launched CarbonLow™ wallboard, featuring up to 60% less embodied carbon.

- September 2024: Kingspan appointed new North America leadership to fast-track insulation and daylighting business lines

Canada Facade Market Report Scope

The facade of a building is its outer front and often consists of roofing, ventilation louvers, and street awnings, among other things. Its structure often incorporates materials like metal, wood, concrete, ceramic, glass, polyvinyl chloride (PVC), stone, etc. Some examples of typical façade types include siding, cladding, external insulation finishing systems (EIFS), curtain walls, etc. For the building, these facades offer weatherproofing, construction, durability, and aesthetic appeal.

The report provides a comprehensive background analysis of the Canada Facade market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry. Additionally, the COVID-19 impact has been incorporated and considered during the study. The Canada Facade Market is segmented By Type (Ventilated, Non-Ventilated, and Others), By Material (Glass, Metal, Plastics and Fibres, Stones, and Others), and By End Users (Commercial, Residential, and Others). The report offers the market size and forecasts in terms of value (USD billion) for all the above segments.

By Type

| Ventilated |

| Non-Ventilated |

| Others |

By Façade System Type

| Rainscreen Cladding |

| Curtain Wall Systems |

| Others |

By Material

| Glass |

| Metal |

| Plastic & Fibres |

| Stone |

| Others |

By Installation

| New Construction |

| Renovation & Retrofit |

By End-User

| Commercial |

| Residential |

| Others |

By Region

| Ontario |

| Quebec |

| British Columbia |

| Alberta |

| Rest of Canada |

| By Type | Ventilated |

| Non-Ventilated | |

| Others | |

| By Façade System Type | Rainscreen Cladding |

| Curtain Wall Systems | |

| Others | |

| By Material | Glass |

| Metal | |

| Plastic & Fibres | |

| Stone | |

| Others | |

| By Installation | New Construction |

| Renovation & Retrofit | |

| By End-User | Commercial |

| Residential | |

| Others | |

| By Region | Ontario |

| Quebec | |

| British Columbia | |

| Alberta | |

| Rest of Canada |

Key Questions Answered in the Report

What is the forecast value of the Canada facades market in 2031?

The market is projected to reach USD 11.29 billion by 2031.

How fast is the Canada facades market expected to grow?

It is forecast to expand at a 5.69% CAGR between 2026 and 2031.

Which façade system currently holds the largest share in Canada?

Curtain wall assemblies lead with a 44.60% revenue share as of 2025.

Why are non-ventilated façades popular in Canada?

They align with NECB 2020 airtightness requirements and offer simplified maintenance, driving their 53.80% share.

Which province shows the fastest façade market growth?

Ontario posts a 6.52% CAGR through 2031, outpacing other regions due to ambitious housing targets.

Page last updated on: