Gracey Curette Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 50.07 Million |

| Market Size (2031) | USD 79.91 Million |

| Growth Rate (2026 - 2031) | 9.80% CAGR |

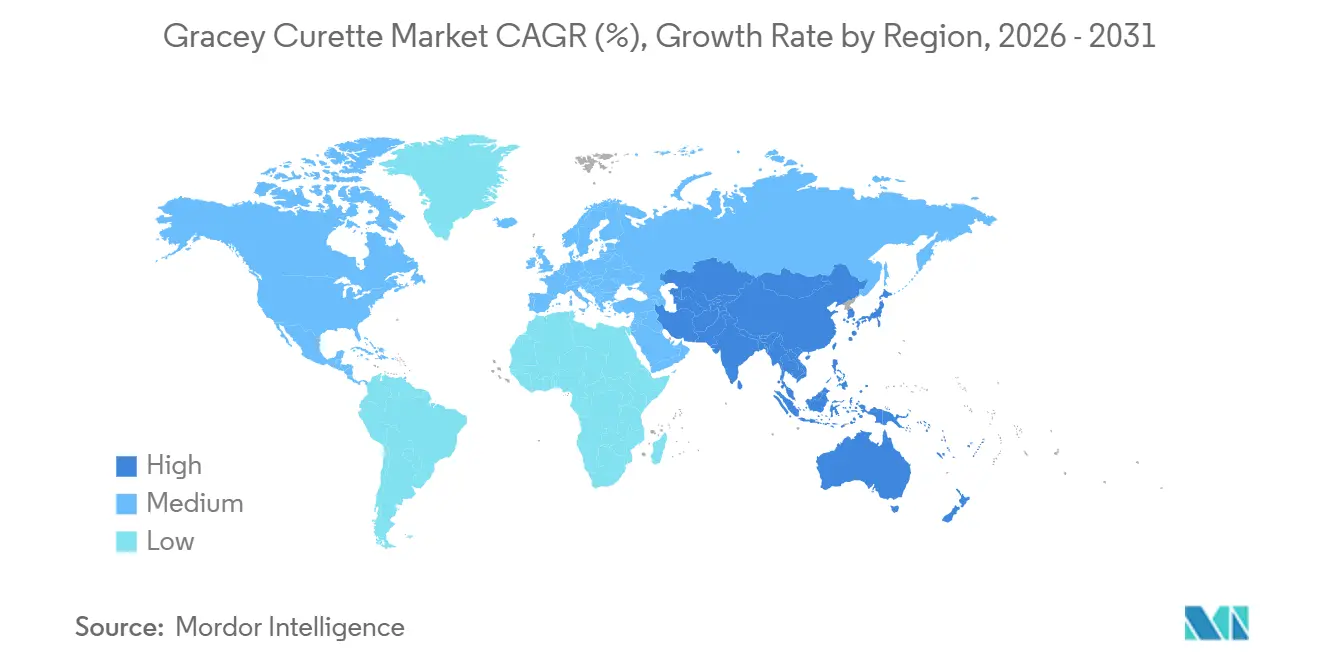

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

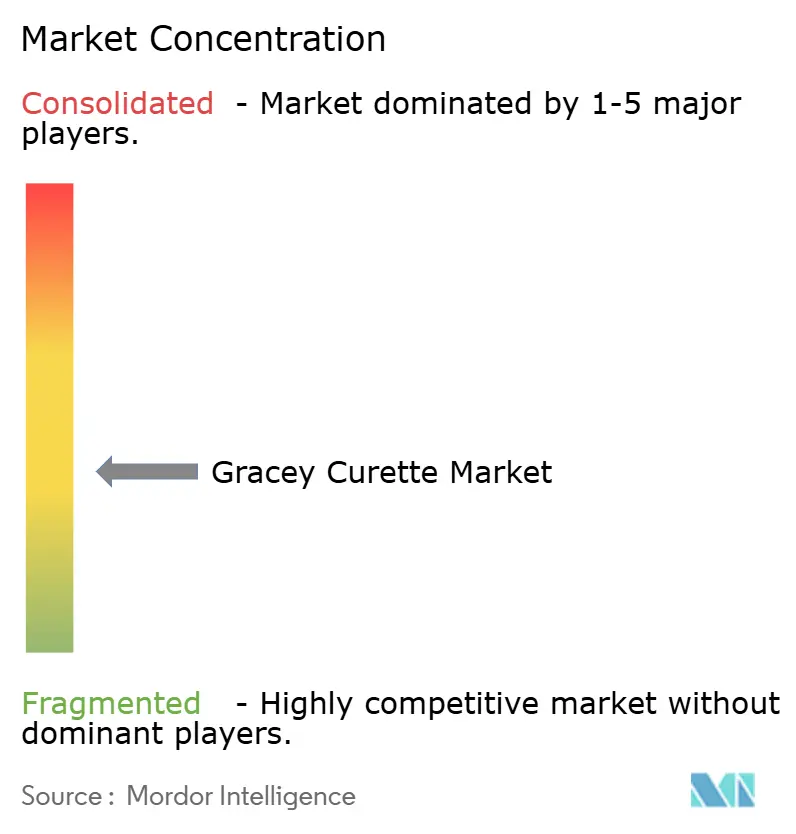

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gracey Curette Market Analysis by Mordor Intelligence

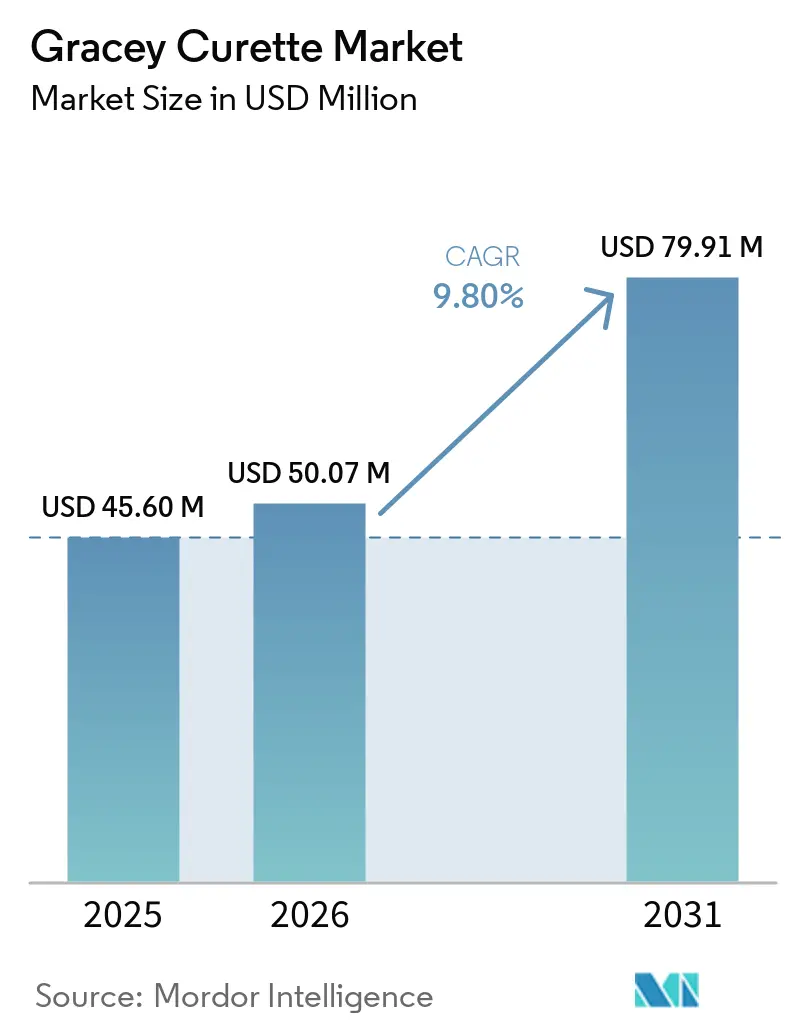

The Gracey Curette Market size was valued at USD 45.60 million in 2025 and is estimated to grow from USD 50.07 million in 2026 to reach USD 79.91 million by 2031, at a CAGR of 9.80% during the forecast period (2026-2031).

This growth reflects sustained clinical demand for precision periodontal instrumentation that can tackle a projected global severe periodontitis burden of 1.56 billion cases by 2050. Robust public-health focus on preventive oral care, new implant-maintenance billing codes, and ergonomic product innovations reinforce the upward trajectory. Standard and procedure-specific curettes continue to coexist as clinicians match instrument geometry to pocket depth, while titanium variants gain visibility in implant dentistry. Digital procurement platforms accelerate product accessibility, and consolidation among established manufacturers signals expanded R&D budgets aimed at minimally invasive designs.

Key Report Takeaways

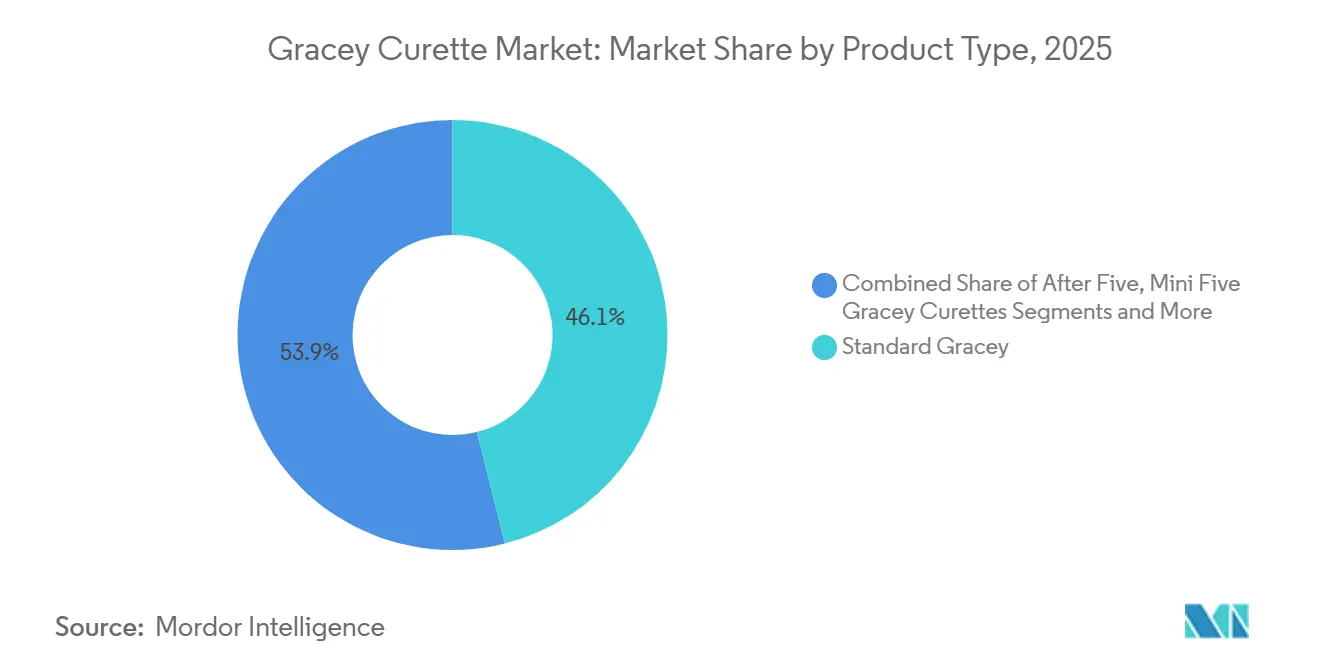

- By product category, Standard Gracey curettes held 46.1% of the Gracey curette market share in 2025, whereas Micro-Mini Five variants are projected to expand at a 10.95% CAGR through 2031.

- By material, stainless steel commanded 68.2% of the Gracey curette market size in 2025, while titanium is expected to have a 10.7% CAGR to 2031.

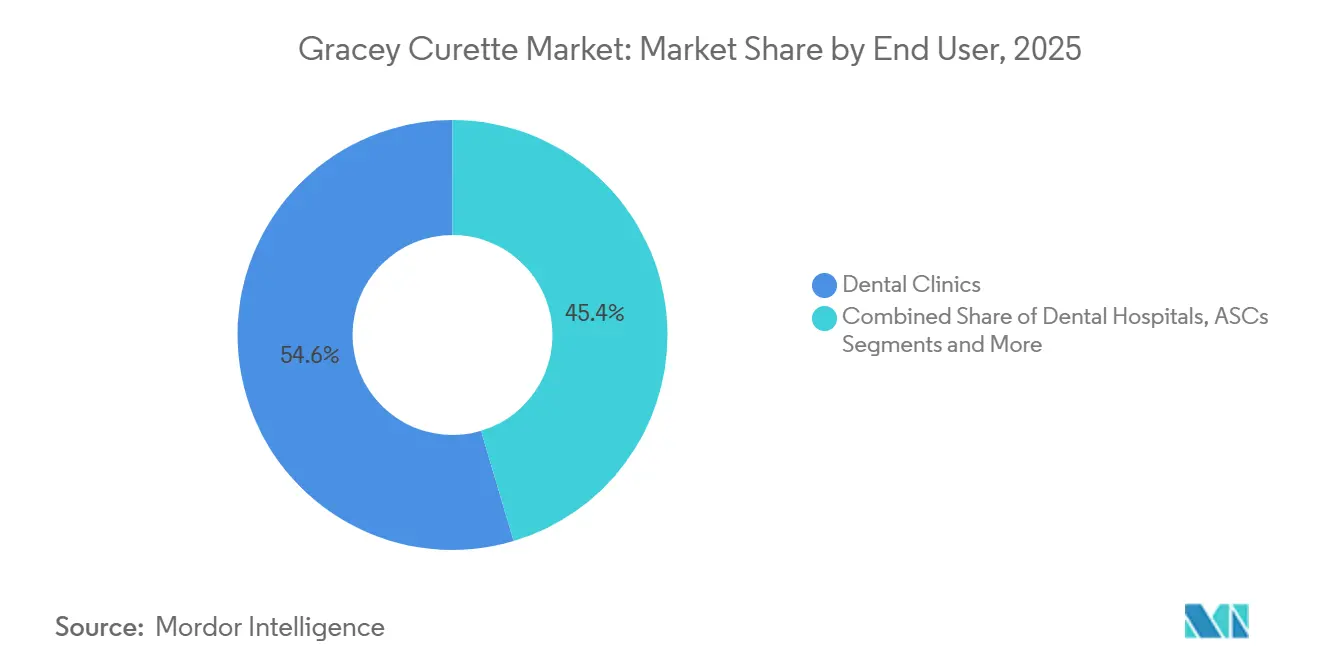

- By end user, dental clinics accounted for 54.6% of the Gracey curette market size in 2025; ambulatory surgical centers are expected to grow at an 10.9% CAGR through 2031.

- By distribution channel, distributors and wholesalers controlled 57.1% of the Gracey Curette market share in 2025, yet e-commerce is projected to rise at a 10.4% CAGR through 2031.

- By geography, North America led with a 35.7% gracey curette market share in 2025, and Asia-Pacific is anticipated to grow at a 11.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gracey Curette Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic periodontitis | +2.10% | Global; highest in Asia-Pacific | Long term (≥ 4 years) |

| Adoption of minimally-invasive periodontal surgery | +1.80% | North America & EU; expanding to Asia-Pacific | Medium term (2-4 years) |

| Uptake of single-use titanium curettes for implant maintenance | +1.40% | Developed markets | Medium term (2-4 years) |

| Ergonomic-handle innovations reducing clinician MSDs | +1.20% | North America & EU | Short term (≤ 2 years) |

| DSO & group-practice expansion driving bulk procurement | +0.90% | North America; global expansion | Medium term (2-4 years) |

| At-home tele-dental starter kits in emerging markets | +0.60% | Asia-Pacific & Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Periodontitis

Severe periodontitis cases are expected to escalate from 1 billion individuals in 2021 to 1.56 billion by 2050, shifting periodontal therapy from elective to essential care.[1]Haojie Fu et al., “Global Burden of Periodontal Diseases,” BMC Public Health, bmcpublichealth.biomedcentral.com Prevalence in countries such as China already approaches 90% of adults, intensifying demand for precision curettes able to debride deep pockets.[2]Yuangui Zhu, “The Research Progress on Periodontitis by the National Natural Science Foundation of China,” Nature, nature.com Health-economic evidence links periodontal status to systemic conditions, including diabetes and cardiovascular disease, prompting payers to reimburse earlier interventions. Working-age adults alone experienced 951.3 million periodontal cases in 2021, drawing employer-funded dental plans toward preventive scaling schedules. These conditions collectively underpin sustained growth for the gracey curette market as public health programs in emerging economies scale treatment capacity.

Adoption of Minimally-Invasive Periodontal Surgery

Micro- and mini-variant curettes are integral to periodontal flap-preserving techniques that deliver faster healing and less post-operative discomfort. Clinical case reports show multidisciplinary non-surgical protocols leveraging Gracey instruments to arrest stage IV, grade C periodontitis and improve clinical attachment levels.[3]Lingjun Li et al., “Multidisciplinary Non-Surgical Treatment of Advanced Periodontitis,” pubmed.ncbi.nlm.nih.gov Guided biofilm therapy, combining selective air-polishing systems with specialized curettes, is now referenced in EU practice guidelines, fostering demand for ultra-fine blades that accommodate restricted surgical fields. Procedural efficiencies that allow single-appointment therapy favor multi-angle, thin-blade instruments because they reduce chair time without sacrificing root-surface cleanliness.

Uptake of Single-Use Titanium Curettes for Implant Maintenance

New procedure codes D6080 and D6081, effective January 2025, establish standardized billing for implant maintenance and mucositis management, pushing clinics toward titanium instruments that avoid scratching abutment surfaces. Single-use titanium curettes such as the Pineyro Arch line enable access beneath fixed prosthetics without removal while eliminating reprocessing costs. As global implant placements rise, demand concentrates on tip geometries designed for platform-switched implants and narrow-diameter fixtures. Regulatory scrutiny of cleaning validation further accelerates the replacement of reusable steel tips with sterile, pre-packaged titanium SKUs, particularly in peri-implantitis recall programs.

Ergonomic-Handle Innovations Reducing Clinician MSDs

Musculoskeletal disorders (MSDs) among hygienists have prompted the release of larger-diameter, textured handles that lower pinch force by up to 65% and reduce tooth pressure by 37% in simulated use. Clinical fatigue data increasingly appear in procurement specifications of Dental Service Organizations (DSOs), positioning ergonomic curettes as a staff-retention tool. Broad acceptance of thicker silicone grips and color-coded identification rings also speeds instrument turnover between operatories, elevating demand in high-volume practices. Manufacturers that combine weight-optimized shafts with extended-wear blade metallurgy capture the premium tier of the gracey curette market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing versus generic instruments | -1.60% | Price-sensitive markets | Medium term (2-4 years) |

| Shift toward ultrasonic scalers in high-income clinics | -1.20% | North America & EU | Long term (≥ 4 years) |

| Stringent reprocessing standards for reusable tools | -0.80% | Developed markets | Short term (≤ 2 years) |

| Post-COVID single-use plastic restrictions | -0.50% | EU & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing Versus Generic Instruments

Branded curettes command notable price premiums by bundling advanced alloys and ergonomic features, yet procurement committees in public hospitals often favor low-cost generics when clinical outcomes appear comparable. This budget sensitivity is acute in emerging economies where single-unit cost can influence treatment uptake, limiting volume growth for premium SKUs despite demonstrated longevity and tactile advantages. Leading suppliers counteract by offering tiered portfolios and rebate programs tied to instrument-exchange services that extend blade life and prove cost-in-use savings over generic imports.

Shift Toward Ultrasonic Scalers in High-Income Clinics

Investment in multi-frequency ultrasonic platforms enables clinics to manage routine prophylaxis more efficiently, reducing appointment times. While manual curettes remain indispensable for root planing, the proportion of chair time allocated to hand instrumentation declines, placing a ceiling on unit volumes in affluent practices. Hybrid protocols that pair ultrasonic debridement with targeted manual scaling preserve some demand but force manufacturers to reposition curettes as indispensable adjuncts rather than primary tools.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Micro-Mini Variants Drive Precision Demand

Standard Gracey designs retained a 46.1% gracey curette market share in 2025, providing universal applicability across scaling procedures. The gracey curette market size for Micro-Mini Five blades is projected to advance at a 10.95% CAGR through 2031, fueled by minimally-invasive protocols that demand thin shanks for deep pocket access without flap reflection. Procedure-specific kits that bundle After Five and Rigid tips expand adoption in complex surgeries where calculus removal capacity matters. Manufacturers exploit laser-welded shank angles to ensure consistent blade adaptation, driving product differentiation within the gracey curette industry.

The need for precision continues to fragment the product landscape, encouraging clinics to stock instrument rolls tailored to anterior, posterior, furcation, and implant maintenance sites. This specialization underpins premium pricing, as each blade geometry serves a distinct tactile requirement. Portfolio breadth, therefore, becomes a competitive lever; suppliers offering complete assortments gain preferred-vendor status in DSO procurement agreements.

By Material: Titanium Innovation Challenges Steel Dominance

Stainless steel accounted for 68.2% of the gracey curette market size in 2025 owing to its balance of sharpness retention and cost efficiency. Titanium units track an 10.7% CAGR through 2031, propelled by implant-safety marketing and the elimination of galvanic corrosion. Manufacturers adapt proprietary heat treatments to extend edge longevity, closing the gap with hardened steel blades. Educational campaigns underscore the risk of scratching implant surfaces with steel, spurring periodontists to reserve titanium kits exclusively for implant recall visits. The shift illustrates how material science continues to reshape value propositions in the gracey curette market.

Lighter titanium handles also reduce operator fatigue, aligning with ergonomic trends. Some vendors integrate color-anodized shanks for rapid chair-side identification, facilitating instrument rotation in busy hygiene schedules. Steel, meanwhile, continues to evolve through cryogenic hardening and nano-coatings that raise Rockwell hardness without brittleness, ensuring it retains a dominant presence despite titanium’s rise.

By End User: ASCs Emerge as Growth Leaders

Dental clinics, including multi-site DSOs, held 54.6% of the gracey curette market size in 2025 because of their primary role in prophylaxis and root planing. Ambulatory surgical centers (ASCs) are on track for an 10.9% CAGR through 2031 as complex periodontal surgeries migrate out of hospitals to lower-cost outpatient settings, increasing instrument demand per procedure due to sterile-tray requirements. Academic institutions sustain niche demand for specialty variants used in postgraduate training, while research facilities drive collaborative trials examining new handle geometries.

DSOs leverage centralized purchasing to negotiate discounted tiered pricing, pressuring smaller practices to consolidate orders through buying groups. ASCs, conversely, prioritize rapid turnover of sterile packs, creating a secondary market for single-use kits that blend titanium tips with recyclable polymer handles. This dual-client mix prompts suppliers to maintain flexible manufacturing capable of both premium reusable lines and cost-efficient disposables.

By Distribution Channel: E-Commerce Disrupts Traditional Models

Distributors and wholesalers secured 57.1% gracey curette market share in 2025 because their value-added services, such as chair-side training and inventory management, remain indispensable to many practices. Yet e-commerce is accelerating at a 10.4% CAGR through 2031 as clinicians favor transparent pricing, 24/7 ordering, and direct access to technical datasheets. Manufacturers respond by offering exclusive online bundles, sometimes bypassing traditional dealers for commoditized SKUs while preserving distributor relationships for premium or service-intensive products.

Direct sales teams still target large DSOs and government tenders where tailored solutions and volume rebates matter. Catalog and mail-order channels maintain relevance in remote geographies lacking reliable internet infrastructure, though their growth lags digital platforms. Over time, hybrid fulfillment models that ship from local dealer stockrooms but transact through manufacturer websites may become dominant, integrating the strengths of both routes.

Geography Analysis

North America retained 35.7% gracey curette market share in 2025, due to a mature reimbursement ecosystem, high periodontal-disease awareness, and early adoption of ergonomic and implant-safe instruments. DSOs standardize protocols nationwide, generating predictable bulk orders that favor suppliers with broad SKUs and robust supply-chain support. New implant-maintenance procedure codes gave clinics clearer revenue streams for advanced curette use, sustaining premium purchases.

Asia-Pacific is forecast to deliver a 11.5% CAGR to 2031 on the back of expanding dental insurance coverage, sizeable periodontal disease prevalence, and clinic network growth in China and India. Public education drives patient demand for professional scaling, while urban clinics adopt imported titanium tips to service rising implant placement rates. Local manufacturers compete mainly on standard steel lines, but premium imports from Japan and South Korea capture high-end demand.

Europe, Middle East & Africa, and South America deliver steady contributions underpinned by universal healthcare and aging populations. Germany, the United Kingdom, and France support consistent replacement demand for sharpen-free instrument lines. In the Gulf Cooperation Council, government-funded dental programs and medical tourism underpin purchases of premium ergonomic sets. South Africa and Brazil benefit from expanding dental school enrolments, creating baseline demand for teaching kits. Currency fluctuations and procurement regulations require suppliers to deploy localized pricing and stock management to preserve margins.

Competitive Landscape

The gracey curette market exhibits moderate concentration. HuFriedyGroup, American Eagle, PDT Dental, Karl Schumacher, LM-Dental, and Dentsply Sirona collectively anchor the premium tier, each leveraging R&D pipelines that integrate metallurgy, surface engineering, and ergonomic research. HuFriedyGroup’s October 2024 acquisition by Peak Rock Capital provides fresh capital for product line expansions, reinforcing its reach into 100 countries. Portfolio breadth, more than 10,000 dental items, gives it scale economies in steel processing and global compliance.

Mid-sized competitors differentiate through niche innovations. PDT Dental focuses on implant-maintenance titanium arches, while LM-Dental markets sharpen-free diamond-coated blades to Scandinavian clinics challenged by staff shortages. American Eagle’s XP technology emphasizes extended cutting life, reducing sharpening labor and aligning with lean clinic workflows. Entry barriers remain elevated because FDA reprocessing guidance mandates rigorous validation dossiers, discouraging under-capitalized entrants. Distributor alignment is equally decisive; firms with entrenched ties to Patterson Dental or Henry Schein gain priority shelf space and education-center exposure.

Strategic moves revolve around bolt-on acquisitions and regional partnerships. HuFriedyGroup integrated SS White Dental’s bur portfolio in October 2024 to cross-sell instrumentation to restorative dentists. Dentsply Sirona completed an academic partnership in Egypt to seed brand loyalty among students using 756 treatment chairs equipped with its instruments. Competitive intensity is set to tighten as titanium adoption grows, encouraging tooling investments that smaller players may struggle to finance.

Gracey Curette Industry Leaders

HuFriedyGroup

Dentsply Sirona

American Eagle Instruments

ASA Dental

Karl Schumacher Dental

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: American Eagle Gold Corp. wrapped up its non-brokered private placement, issuing 9,650,550 common shares on a premium flow-through basis. That said, the offering is still subject to meeting certain conditions, including securing all necessary regulatory approvals, with final acceptance from the TSX Venture Exchange being a key requirement.

- February 2025: HuFriedyGroup enhanced EverEdge 2.0 scalers with harder steel alloys, including Mini Five Gracey tips, to lengthen sharpening intervals.

Global Gracey Curette Market Report Scope

As per the scope of the report, a gracey curette is a specialized periodontal instrument used by dental professionals to remove plaque, calculus, and tartar from the surfaces of teeth, particularly below the gumline. It features a thin, curved, and sharpened blade designed for effective scaling and root planing. The instrument is typically used in periodontal therapy to help manage gum disease and maintain oral health.

The gracey curette market is segmented by product type into standard Gracey curettes, after five Gracey curettes, mini five Gracey curettes, micro-mini five Gracey curettes, and rigid and extra-rigid Gracey curettes; by material into stainless steel, titanium, plastic-resin ergonomic handles, and other alloys and coatings; by end user into dental hospitals, independent and DSO dental clinics, ambulatory surgical centers, academic and research institutes, and other end users; by distribution channel into direct sales, distributors and wholesalers, e-commerce, catalog and mail-order, and other channels; and by geography into North America, Europe, Asia-Pacific, and rest of the world. For each segment, the market size and forecast are provided in terms of value (USD).

| Standard Gracey Curettes |

| After Five Gracey Curettes |

| Mini Five Gracey Curettes |

| Micro-Mini Five Gracey Curettes |

| Rigid & Extra-Rigid Gracey Curettes |

| Stainless-Steel |

| Titanium |

| Plastic-Resin Ergonomic Handles |

| Other Alloys & Coatings |

| Dental Hospitals |

| Dental Clinics (Independent & DSO) |

| Ambulatory Surgical Centers |

| Academic & Research Institutes |

| Other End Users |

| Direct Sales |

| Distributors & Wholesalers |

| E-commerce |

| Catalog & Mail-order |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Product Type | Standard Gracey Curettes | |

| After Five Gracey Curettes | ||

| Mini Five Gracey Curettes | ||

| Micro-Mini Five Gracey Curettes | ||

| Rigid & Extra-Rigid Gracey Curettes | ||

| By Material | Stainless-Steel | |

| Titanium | ||

| Plastic-Resin Ergonomic Handles | ||

| Other Alloys & Coatings | ||

| By End User | Dental Hospitals | |

| Dental Clinics (Independent & DSO) | ||

| Ambulatory Surgical Centers | ||

| Academic & Research Institutes | ||

| Other End Users | ||

| By Distribution Channel | Direct Sales | |

| Distributors & Wholesalers | ||

| E-commerce | ||

| Catalog & Mail-order | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

How large is the gracey curette market in 2025?

The gracey curette market size is USD 45.6 million in 2025.

What is the expected CAGR for curettes between 2026 and 2031?

The market is projected to advance at a 9.8% CAGR during the forecast window.

Which region is expanding the fastest for curette demand?

Asia-Pacific is forecast to grow at 11.5% per year due to rising periodontal awareness and healthcare investment.

Why are titanium curettes important for implant maintenance?

Titanium tips avoid scratching implant surfaces, reduce contamination risk, and align with new billing codes for implant maintenance.

Which distribution channel shows the strongest growth?

E-commerce leads at a 10.4% CAGR through 2031 as clinics favor online procurement for convenience and competitive pricing.

What drives ergonomic instrument design adoption?

Reducing clinician hand strain and improving procedural efficiency prompts clinics to adopt larger-handle, lightweight curettes validated to lower pinch force.

Page last updated on: