Mometasone Furoate Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

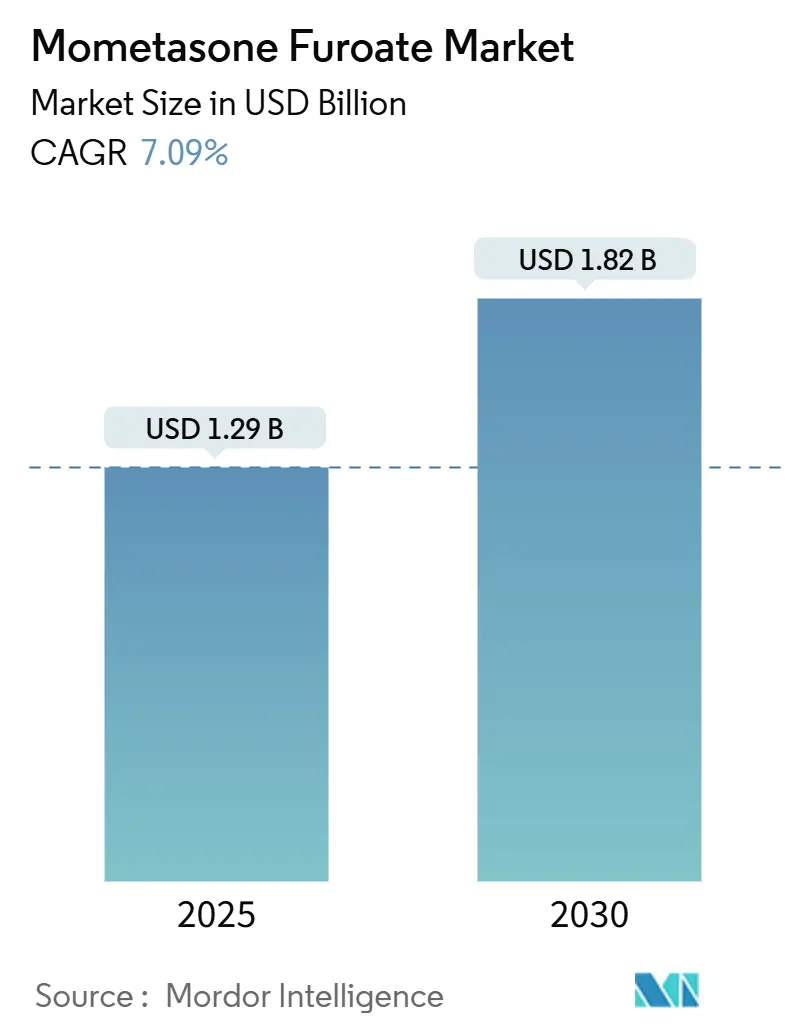

| Market Size (2025) | USD 1.29 Billion |

| Market Size (2030) | USD 1.82 Billion |

| Growth Rate (2025 - 2030) | 7.09% CAGR |

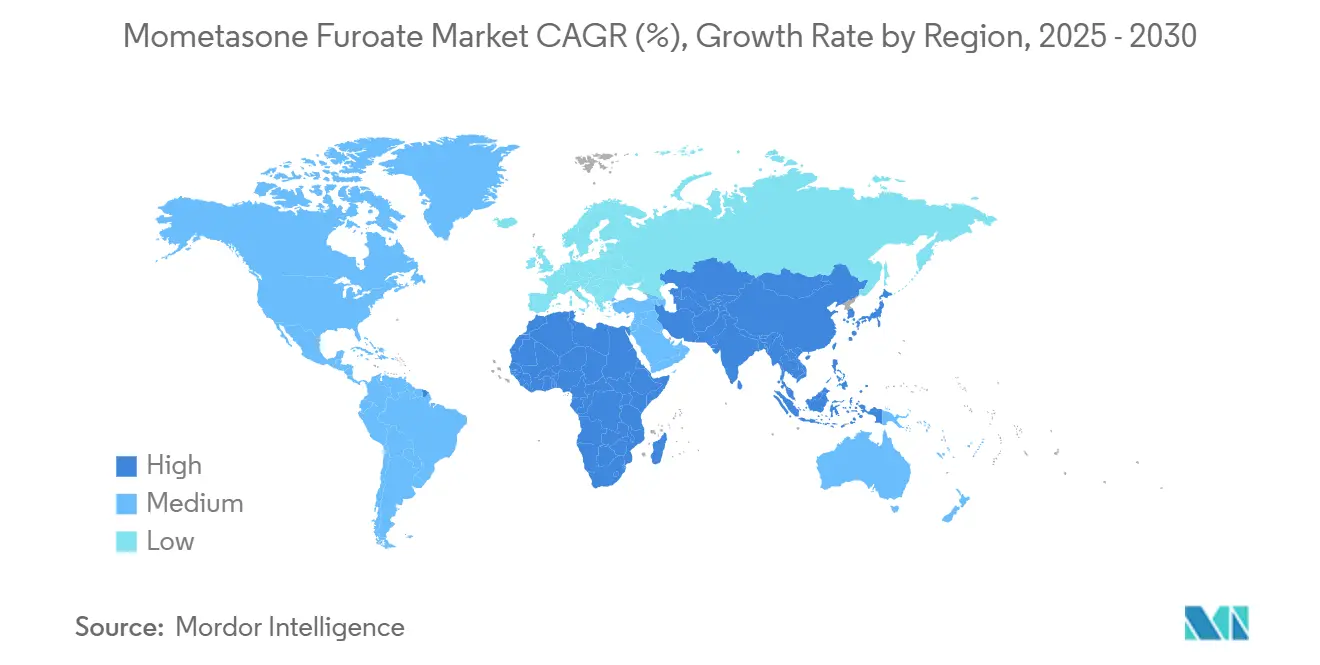

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mometasone Furoate Market Analysis by Mordor Intelligence

The mometasone furoate market size is valued at USD 1.29 billion in 2025 and is projected to reach USD 1.82 billion by 2030, reflecting a 7.09% CAGR during the forecast period. Momentum stems from patent expiries that accelerate generic launches, evolving over-the-counter (OTC) pathways, and the active repositioning of this synthetic corticosteroid in pediatric dermatology and chronic rhinosinusitis management. Expansion also benefits from Asia-Pacific manufacturing cost advantages, while North America maintains high treatment penetration rates supported by established reimbursement frameworks. Device innovation in inhalation powders, sustained demand for topical creams across skin disorders, and a strategic shift toward low-dose once-daily regimens collectively reinforce growth prospects for the mometasone furoate market.

Key Report Takeaways

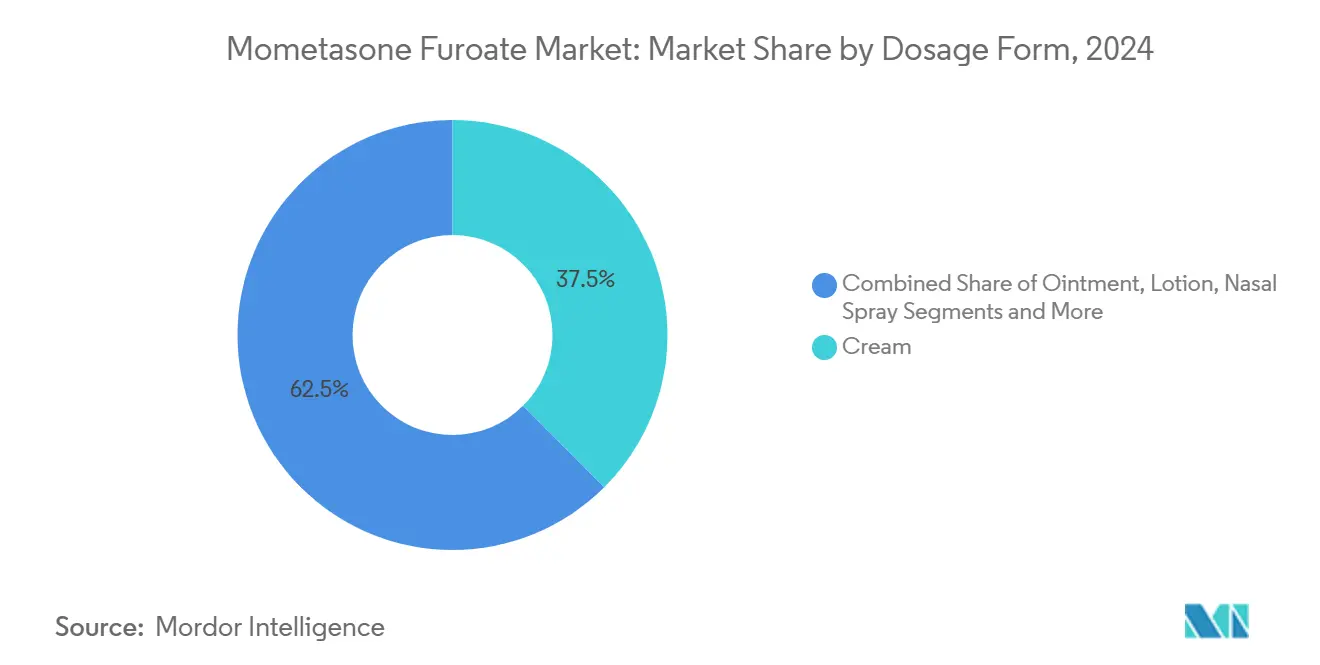

- Cream captured 37.52% of mometasone furoate market share in 2024; inhalation powders are forecast to expand at an 11.23% CAGR through 2030.

- Prescription products accounted for 71.34% of the mometasone furoate market size in 2024, whereas OTC formulations are poised to rise at a 10.52% CAGR to 2030.

- Adults aged 18-64 years held 62.68% revenue share in 2024; pediatric therapies are projected to advance at a 9.01% CAGR over the same horizon.

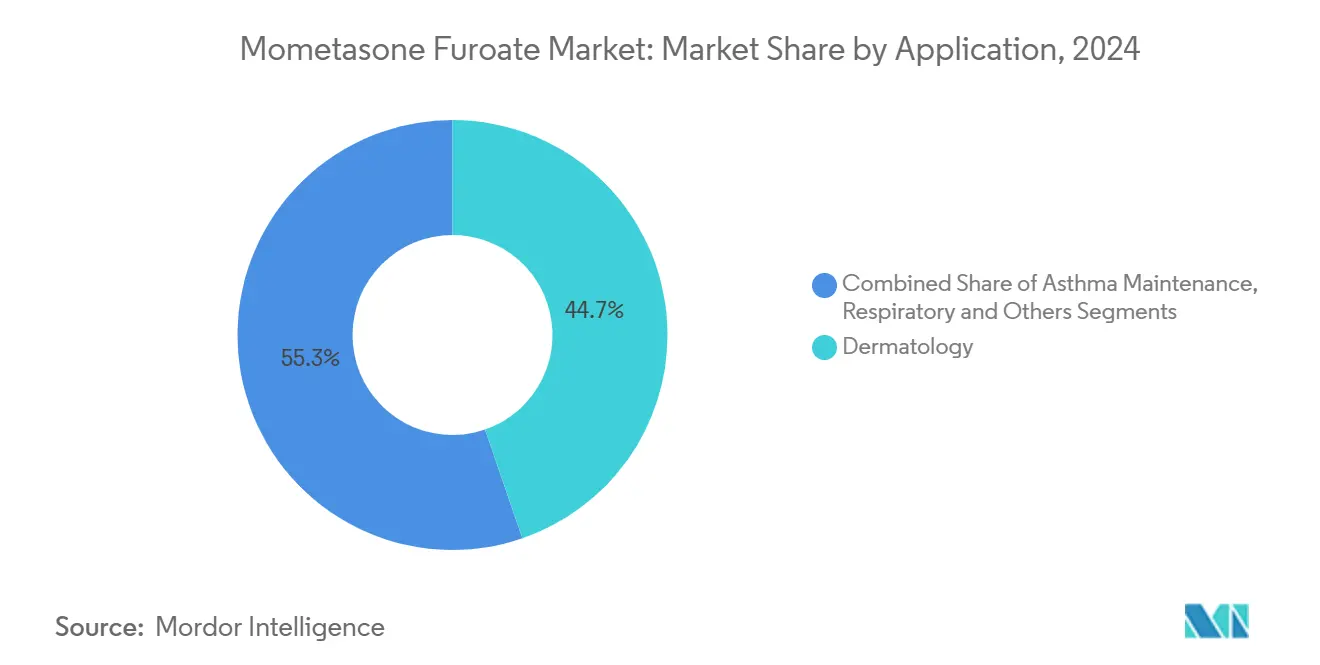

- Dermatological uses led with a 44.73% share of the mometasone furoate market, while asthma maintenance applications are expected to grow at 9.64% CAGR through 2030.

- Retail pharmacies controlled 53.46% of sales in 2024; online pharmacies are set to record 11.89% CAGR as digital health options broaden.

- North America commanded 33.36% of 2024 revenue, yet Asia-Pacific is projected to register the fastest 9.47% CAGR to 2030 on the back of rising healthcare access and contract manufacturing scale.

Global Mometasone Furoate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of dermatological disorders | +1.8% | North America & Europe | Medium term (2-4 years) |

| Growing incidence of allergic rhinitis & asthma | +1.5% | Global, APAC high growth | Long term (≥ 4 years) |

| Patent expiries accelerating generic approvals | +1.2% | North America & Europe | Short term (≤ 2 years) |

| Adoption of low-dose once-daily corticosteroids | +0.9% | Developed markets | Medium term (2-4 years) |

| Contract manufacturing expansion in emerging markets | +0.7% | Asia-Pacific, spill-over to MEA | Long term (≥ 4 years) |

| OTC switches of nasal mometasone in multiple markets | +0.6% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence Of Dermatological Disorders

Atopic dermatitis cases rose globally to 129 million in 2021 and are projected to reach 148 million by 2050, with industrialized nations reporting 10%–15% pediatric prevalence. Environmental pollutants and socioeconomic stressors intensify symptom burden, while aging societies in Northern Europe and North America create sustained need for topical corticosteroids that address skin barrier dysfunction. Mometasone furoate’s established safety in children positions it well for an expanded patient base across all age groups.[1]Wai Quen Lee, Kishore Manogalan, Pik Li Wong, Che Zubaidah Che Daud, Sabeera Begum Kader Ibrahim, and Kin Fon Leong, “Observational Study of the Changes in Skin Thickness Among Children with Atopic Dermatitis Treated with Topical Mometasone Furoate 0.1% Cream,” Journal of Skin and Stem Cell, jsscjournal.com

Growing Incidence Of Allergic Rhinitis & Asthma

Asthma cases are forecast to climb to 275 million by 2050, and urbanization drives higher allergic rhinitis incidence across developing economies. With high body mass index identified as the largest modifiable risk factor, integrated care models rely on corticosteroid maintenance therapy. Mometasone furoate is increasingly selected as first-line treatment for nasal polyposis, with systematic reviews confirming superior polyp size reduction versus other steroids.[2]Osamah H. Mohya, “Efficacy and Safety of Mometasone Furoate Nasal Spray in Treating Nasal Polyposis: A Systematic Review and Meta-Analysis,” Cureus, cureus.com The withdrawal of Flovent in 2024 created supply gaps for pediatric patients that Asmanex and other mometasone products are filling.[3]Erin D. Parker and Joseph M. Collaco, “Inhaled Corticosteroid Alternatives for Young Children After Flovent Withdrawal,” Contemporary Pediatrics, contemporarypediatrics.com

Patent Expiries Accelerating Generic Approvals

The January 2025 patent cliff for Ryaltris opens a USD 80 million revenue stream to generic competition, illustrating how expiration timelines compress price bands and broaden access. FDA guidance supports streamlined abbreviated new drug applications for nasal sprays, favoring producers with established corticosteroid expertise.

Adoption Of Low-Dose Once-Daily Corticosteroids

Once-daily regimens enhance adherence and reduce systemic exposure. Mometasone furoate’s glucocorticoid receptor affinity, 22-fold greater than dexamethasone, underpins efficacy at lower doses. Metered-dose innovations ensure precise delivery, and its <1% oral bioavailability curbs systemic side effects, strengthening payer arguments for chronic use.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory scrutiny on topical corticosteroids | -0.8% | Europe & North America | Medium term (2-4 years) |

| Supply-chain gaps in fluorination intermediates | -0.6% | Asia-centric manufacturing | Short term (≤ 2 years) |

| Physician shift to non-steroidal topical agents | -0.5% | North America & Europe | Long term (≥ 4 years) |

| Phase-down of HFA propellants inflates inhaler costs | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Scrutiny On Topical Corticosteroids

FDA’s 2025 guidance on nasal spray chemistry and pediatric labeling raises compliance costs through deeper stability and metering validation requirements. Over-the-counter monograph fees now exceed USD 559,777 for Tier 1 filings, placing financial strain on smaller firms. European harmonization further complicates approval pathways, potentially slowing new SKU launches.

Supply-Chain Gaps In Fluorination Intermediates

Regulatory focus on PFAS curtails fluorochemical capacity in Asia, threatening continuity of fluorinated corticosteroid intermediates. Sustainable precursors such as bio-derived furfural require capital-intensive process redesign, compelling firms to invest or diversify suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage Form: Cream Dominance Faces Inhalation Innovation

Cream formulations generated 37.52% of the mometasone furoate market share in 2024, underscoring entrenched dermatology protocols that favor patient-friendly textures for atopic dermatitis and psoriasis. The segment benefits from high physician familiarity and broad OTC eligibility, preserving brand loyalty even as generics enter.

Inhalation powders are poised for an 11.23% CAGR through 2030 as device advances heighten deposition efficiency and reduce propellant reliance, aligning with global HFC phase-down mandates. The mometasone furoate market size for inhalation formats is further amplified by clinical guidelines that elevate maintenance therapy adherence in pediatric asthma.

By Prescription Status: OTC Transitions Accelerate Access

Prescription products held 71.34% of the mometasone furoate market size in 2024, reflecting insurer reimbursement and clinician oversight for moderate-to-severe inflammatory disorders. Safety monitoring requirements and combination therapies maintain dominance within this channel.

Over-the-counter formulations grow at 10.52% CAGR to 2030, driven by ACNU pathways that integrate electronic questionnaires and pharmacist interventions to ensure appropriate self-selection. Retailers deploy educational campaigns that normalize moms’ purchasing decisions for mild allergic rhinitis, expanding consumer reach without physician visits.

By Patient Age Group: Pediatric Safety Drives Expansion

Adults aged 18-64 years accounted for 62.68% of 2024 revenue, mirroring the peak prevalence of chronic inflammatory conditions during working years. The mometasone furoate market now pivots toward pediatrics, where a 9.01% CAGR through 2030 reflects caregiver confidence in topical safety profiles devoid of clinically meaningful skin atrophy.

Pediatric formulations leverage lower dosage strengths, flavored inhalation variants, and pictogram-rich labeling. Manufacturers with pediatric clinical data enjoy a competitive moat, as regulatory agencies require age-stratified safety evidence prior to broader label expansions.

By Application: Dermatology Leadership Meets Respiratory Growth

Dermatological applications delivered 44.73% of 2024 revenue, anchored by high-volume prescriptions in atopic dermatitis and psoriasis clinics. The mometasone furoate market size for dermatology remains resilient however, biologic entrants intensify competition.

Asthma maintenance therapy is the fastest-growing application at a 9.64% CAGR, propelled by controller-focused guidelines and the exit of rival fluticasone formulations in pediatric segments. Nasal polyposis indications also benefit from evidence showing superior polyp regression versus comparator steroids.

By Distribution Channel: Online Growth Challenges Traditional Retail

Retail pharmacies captured 53.46% of 2024 sales due to embedded prescriber relationships and insurance adjudication workflows. They remain pivotal for prescription refills and pharmacist counseling on corticosteroid step-down regimens.

Online pharmacies expand at an 11.89% CAGR amid telemedicine’s post-pandemic normalization. The mometasone furoate market finds incremental volumes through direct-to-consumer portals that combine same-day delivery with electronic prior-authorization tools, reducing friction for chronic users.

Geography Analysis

North America’s leadership is underpinned by entrenched payer networks and a mature OTC aisle that normalizes corticosteroid self-care. High physician visitation rates funnel moderate-to-severe cases toward branded and authorized generic prescriptions, supporting resilience against price erosion from plain generics.

Europe pursues parallel trade strategies that harmonize pricing yet incentivize local production. The region’s dermatology-heavy case mix sustains topical mometasone uptake, although non-steroidal options gradually capture early-stage disease segments. Brexit logistics complexities have modestly delayed some SKU launches in the United Kingdom, prompting firms to hold higher inventory buffers.

Asia-Pacific’s double-digit expansion derives from healthcare infrastructure build-outs and government subsidy programs that broaden inhaler coverage. The mometasone furoate market size in China is buoyed by tiered hospital purchasing that rewards cost-effective generics, while India’s national production-linked incentive scheme encourages bulk steroid manufacture.

Competitive Landscape

Market concentration remains moderate. Top brands leverage GMP facilities and validated supply chains, while abbreviated new drug approvals invigorate price competition immediately after patent cliffs. Hovione’s dedicated 220 m² corticosteroid block—with FDA inspection completed in 2025—underscores capital intensity and regulatory scrutiny.

Combination innovation differentiates incumbents. Glenmark’s Ryaltris patent expiry triggers copycat filings, but its olopatadine-mometasone pairing demonstrated prescriber loyalty through dual-symptom relief. OTC entrants exploit ACNU rules to bypass prolonged prescription-to-OTC switch procedures, accelerating storefront presence. Digital pharmacy alliances and telehealth collaborations further blur boundaries between distribution and marketing.

The mometasone furoate industry observes escalating M&A: large-cap firms seek respiratory portfolio bolt-ons as biologics crowd severe asthma therapy. Meanwhile, dermatology-focused startups backed by USD 100 million in venture funding develop barrier repair adjuncts that may be co-prescribed with low-dose steroids, signaling a future of combination regimens over single-agent dominance.

Mometasone Furoate Industry Leaders

Organon & Co.

Teva Pharmaceutical Industries Ltd.

Glenmark Pharmaceuticals Ltd.

Perrigo Company plc

Viatris Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Top-line results released for the ENLIGHTEN 2 phase 3 trial of LYR-120, a bioabsorbable nasal implant delivering 7,500 µg mometasone furoate over six months to chronic rhinosinusitis patients.

- March 2024: Aurobindo Pharma obtained FDA approval for AB-rated mometasone furoate monohydrate nasal spray (50 µg/spray), a generic equivalent to Nasonex.

Global Mometasone Furoate Market Report Scope

| Cream |

| Ointment |

| Lotion |

| Nasal Spray |

| Inhalation Powder |

| Tablets |

| Prescription (Rx) |

| Over-the-Counter (OTC) |

| Pediatric (Less Than 12 yrs) |

| Adolescent (12–17 yrs) |

| Adult (18–64 yrs) |

| Geriatric (65 yrs +) |

| Dermatology | Psoriasis |

| Atopic Dermatitis | |

| Other Dermatoses | |

| Respiratory | Allergic Rhinitis |

| Chronic Rhinosinusitis | |

| Asthma Maintenance | |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Dosage Form | Cream | |

| Ointment | ||

| Lotion | ||

| Nasal Spray | ||

| Inhalation Powder | ||

| Tablets | ||

| By Prescription Status | Prescription (Rx) | |

| Over-the-Counter (OTC) | ||

| By Patient Age Group | Pediatric (Less Than 12 yrs) | |

| Adolescent (12–17 yrs) | ||

| Adult (18–64 yrs) | ||

| Geriatric (65 yrs +) | ||

| By Application | Dermatology | Psoriasis |

| Atopic Dermatitis | ||

| Other Dermatoses | ||

| Respiratory | Allergic Rhinitis | |

| Chronic Rhinosinusitis | ||

| Asthma Maintenance | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the mometasone furoate market?

The mometasone furoate market size stands at USD 1.29 billion in 2025.

How fast is the market expected to grow?

The market is projected to register a 7.09% CAGR through 2030.

Which dosage form leads revenue?

Topical cream formulations held 37.52% of global revenue in 2024.

Which region shows the fastest growth outlook?

Asia-Pacific is forecast to expand at a 9.47% CAGR through 2030.

Why are OTC products gaining traction?

FDA’s ACNU rule enables safe self-selection, driving a 10.52% CAGR in OTC formulations to 2030.

What impact does the Ryaltris patent expiry have?

The 2025 patent cliff ushers in generic rivals, intensifying price competition and widening access.

Page last updated on: