Swine Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.74 Billion |

| Market Size (2031) | USD 5.09 Billion |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

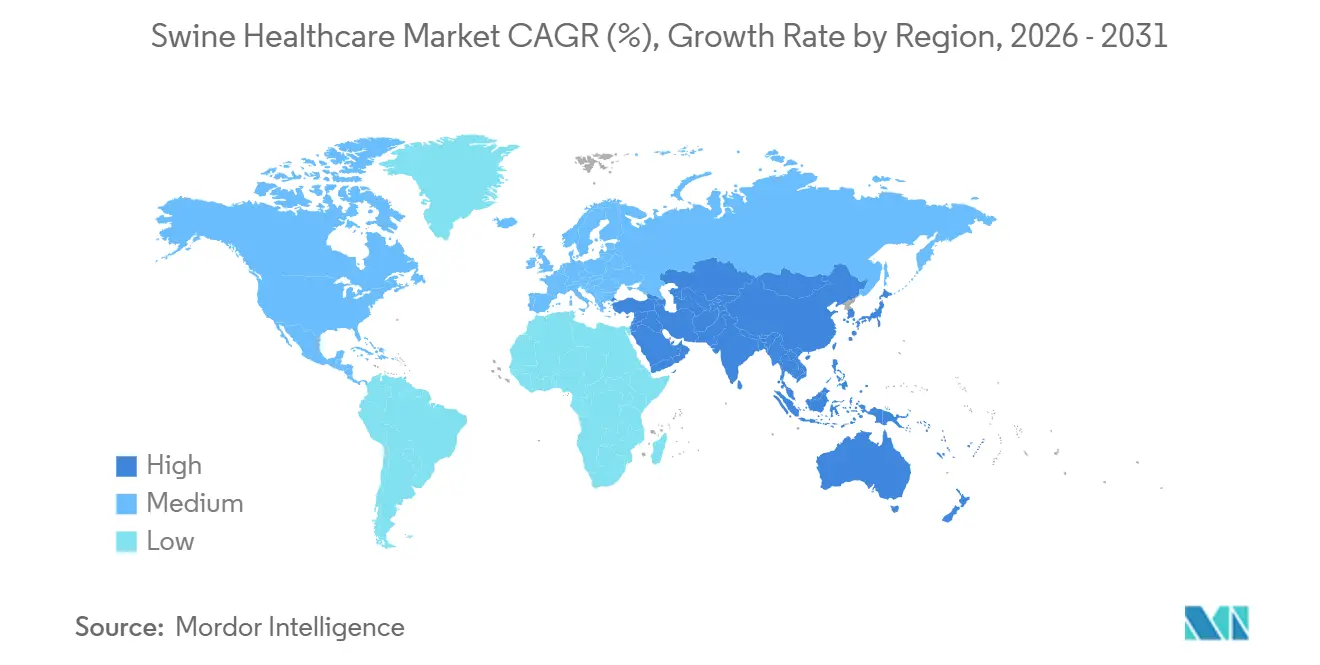

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Swine Healthcare Market Analysis by Mordor Intelligence

The Swine Healthcare Market size is projected to be USD 3.52 billion in 2025, USD 3.74 billion in 2026, and reach USD 5.09 billion by 2031, growing at a CAGR of 6.34% from 2026 to 2031.

African Swine Fever’s persistence, the rapid spread of precision-managed mega-farms, and global mandates curbing prophylactic antibiotics together sustain strong demand for vaccines, diagnostics, and feed additives. China’s localized ASF flare-ups in early 2025 highlighted the continuing biosecurity gap, while ASF detections in German and Polish wild boar during 2024 accelerated European surveillance spending [1]European Food Safety Authority, “ASF in Wild Boar: Germany and Poland 2024,” efsa.europa.eu. Concurrently, vertically integrated herds in North America, Europe, and Brazil adopt weekly PCR screening to protect export access, boosting sales of real-time molecular assays. The push to replace growth-promotion antibiotics with gut-health feed solutions in the European Union and China transitions revenue toward organic acid and phytogenic additives, and pilot gene-edited ASF-resistant pigs introduce long-run uncertainty but no near-term market cannibalization.

Key Report Takeaways

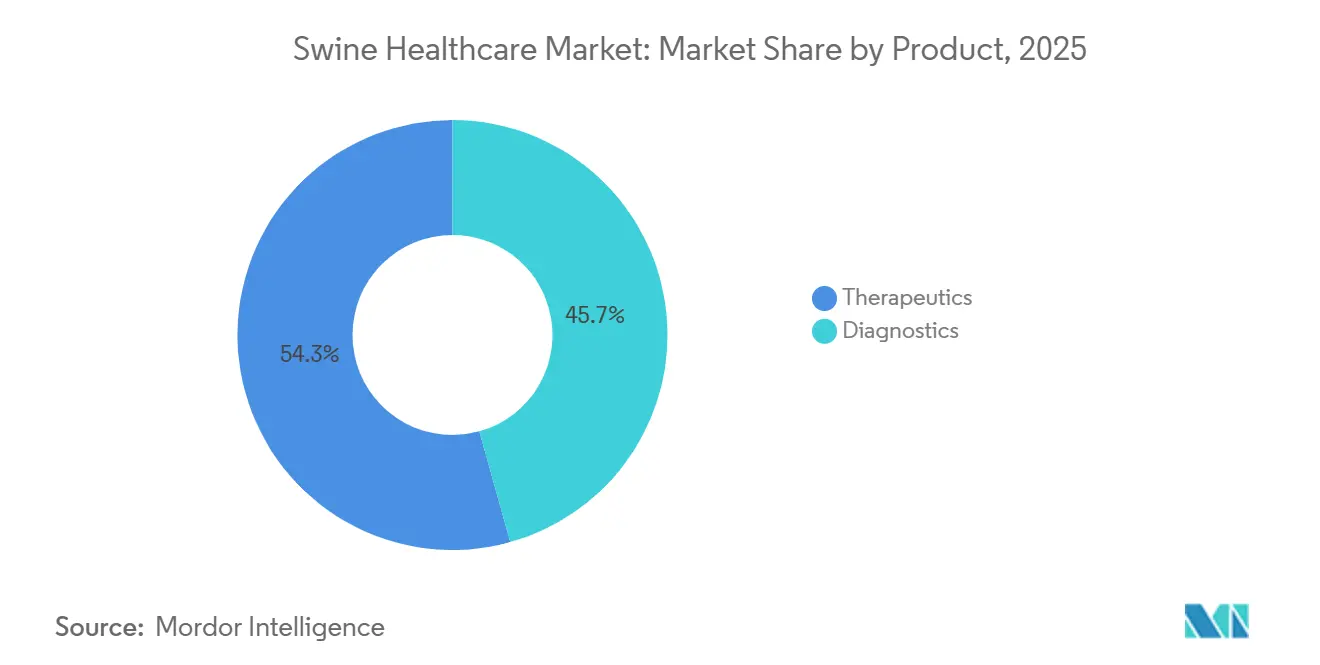

- By product type, therapeutics led with 54.33% of the swine healthcare market share in 2025, whereas diagnostics are forecast to expand at a 7.43% CAGR through 2031.

- By disease, respiratory conditions accounted for 39.98% of the swine healthcare market size in 2025, while emerging viral threats are projected to register an 8.12% CAGR to 2031.

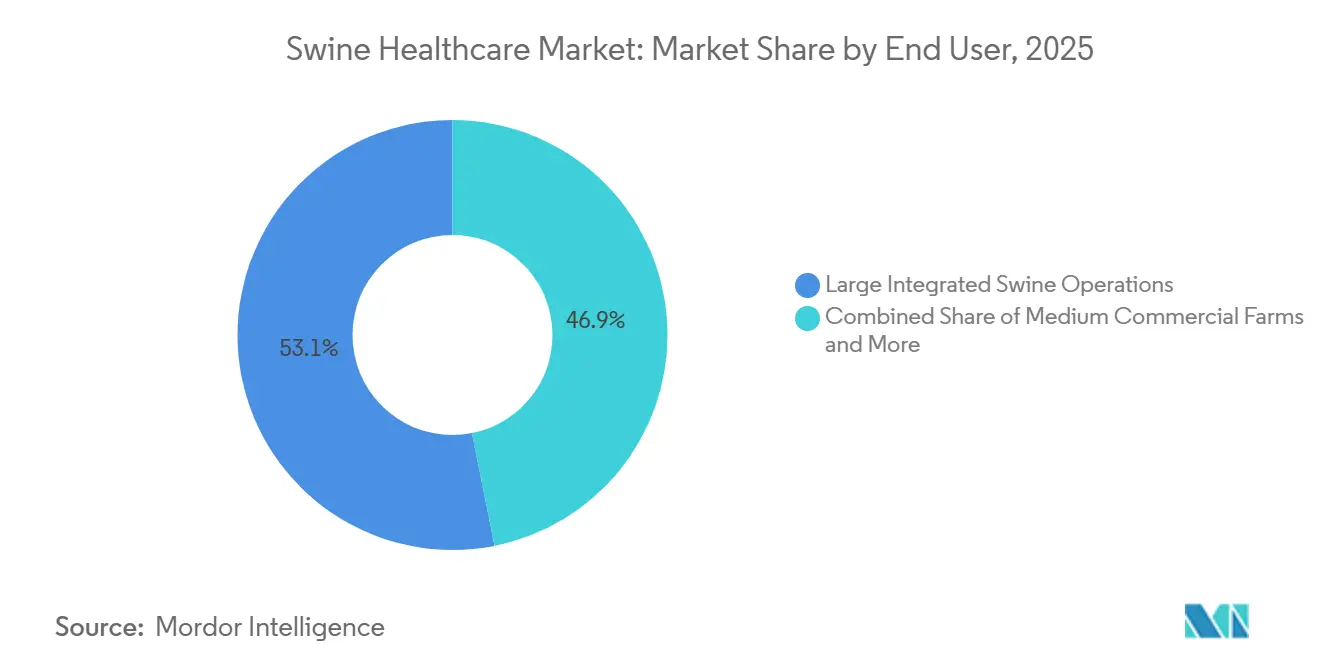

- By end user, large integrated swine operations held 53.12% of revenue in 2025, yet veterinary reference laboratories are advancing at a 7.23% CAGR through 2031.

- By geography, North America dominated with 45.3% revenue in 2025, as Asia-Pacific is poised to grow at a 7.54% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Swine Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of endemic & trans-boundary swine diseases | +1.8% | Global, with acute pressure in Asia-Pacific and Eastern Europe | Medium term (2-4 years) |

| Expanding global pork demand & intensifying production systems | +1.5% | Asia-Pacific core, spill-over to South America and MEA | Long term (≥ 4 years) |

| Surging R&D spend on novel vaccines, diagnostics & feed additives | +1.2% | North America & EU, with licensing to APAC | Medium term (2-4 years) |

| Stricter food-safety / preventive-health regulations worldwide | +1.0% | EU and North America, cascading to export-oriented APAC producers | Short term (≤ 2 years) |

| Rapid adoption of precision-livestock-farming analytics | +0.6% | North America, Northern Europe, pilot deployments in China | Long term (≥ 4 years) |

| Growth of autogenous & custom vaccines in vertically-integrated herds | +0.5% | North America, Brazil, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Endemic & Trans-boundary Swine Diseases

African Swine Fever remains the chief catalyst for vaccine and diagnostic investment, generating trade restrictions that force weekly PCR surveillance in high-risk zones [2]European Commission DG SANTE, “Regionalization Measures for ASF Control,” ec.europa.eu. Porcine reproductive and respiratory syndrome costs U.S. producers about USD 664 million annually through lower litter sizes and secondary infections. IDEXX and Thermo Fisher launched multiplex PCR panels in 2025 that differentiate ASF, Seneca Valley virus, and PCV-3 within hours, limiting needless movement bans and culling. Sustained disease pressure keeps the swine healthcare market’s preventive segment resilient even as gene-editing projects progress. Integrated producers, therefore, prioritize vaccine coverage and rapid diagnostics to avoid the steep direct and opportunity costs of outbreaks.

Expanding Global Pork Demand & Intensifying Production Systems

Per-capita pork intake climbed 8% in Vietnam, 6% in the Philippines, and 12% in India between 2020 and 2025 [3]Food and Agriculture Organization, “FAOSTAT: Pork Consumption Trends 2020-2025,” fao.org. To capture demand, developers financed 10,000-head facilities that copy North American closed-herd biosecurity, elevating baseline spending on vaccines, probiotics, and real-time monitoring. Brazil’s pork exports reached 1.2 million t in 2025 on the back of integrated giants BRF S.A. and JBS, both mandating autogenous vaccines to protect pathogen-free status. Concentrated buying power rewards suppliers that prove antibiotic-free performance, deepening adoption of diagnostics and feed additives. The structural shift to industrial production, therefore, entrenches multi-product purchasing contracts that enlarge the swine healthcare market.

Surging R&D Spend on Novel Vaccines, Diagnostics & Feed Additives

Boehringer Ingelheim raised swine-health R&D outlays 22% in 2025, targeting mRNA platforms for PRRS and ASF, plus oral dosing that trims injection labor. Zoetis moved its ASF candidate into Phase III field trials in Vietnam the same year, signaling a possible late-2027 launch. Hand-held PCR devices from Cepheid deliver barn-side results inside 90 minutes, converting diagnostics from lab expense into routine management tools. DSM-Firmenich and Kemin shipped micro-encapsulated organic acid blends that replace zinc oxide, addressing EU bans effective 2024. The innovation wave broadens solution choice and sustains premium pricing, reinforcing revenue momentum across the swine healthcare market.

Stricter Food-Safety / Preventive-Health Regulations Worldwide

FDA Guidance 263, finalized in June 2024, put all medically important antibiotics under veterinary oversight, shutting off over-the-counter channels. China banned colistin for growth promotion in January 2024, spurring a 28% spike in probiotic and organic-acid feed-additive sales by year-end. The EMA’s revised veterinary-vaccine pharmacovigilance rules, active March 2025, require post-authorization efficacy monitoring, lifting compliance costs but rewarding products with real-world data. These parallel mandates compress antibiotic use and tilt spend toward vaccines, diagnostics, and gut-health additives, cushioning the swine healthcare market against macro volatility.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex, region-specific regulatory approval timelines & costs | -0.9% | Global, acute in EU and China | Medium term (2-4 years) |

| High treatment & vaccination costs for smallholders in emerging markets | -0.7% | Sub-Saharan Africa, Southeast Asia, parts of South America | Long term (≥ 4 years) |

| Cold-chain & vaccine-handling gaps in backyard / informal sectors | -0.5% | Tropical Asia-Pacific, Sub-Saharan Africa, parts of Latin America | Medium term (2-4 years) |

| Gene-edited ASF-resistant pig lines could curb future demand | -0.4% | Global, early adoption in North America and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex, Region-Specific Regulatory Approval Timelines & Costs

mRNA and viral-vector vaccines face 5-to-7-year U.S. pathways and even longer EU vetting that demands multi-country field trials. Zoetis disclosed cumulative ASF vaccine development spend above USD 150 million through 2025, with revenues contingent on approvals in at least three large markets. China requires separate domestic trials, and the approval queue averaged 42 months in 2024. Protracted timelines raise opportunity costs as pathogens mutate and integrators pivot to interim autogenous vaccines, shrinking the eventual addressable pool once full licenses arrive. Smaller biotech firms thus struggle to finance elongated campaigns, concentrating innovation among cash-rich multinationals.

High Treatment & Vaccination Costs for Smallholders in Emerging Markets

Smallholders supply more than half of pigs in the Philippines, Vietnam, and Sub-Saharan Africa, yet per-dose vaccine prices equal 3%-5% of a finished pig’s sale value, curbing uptake. An ILRI survey showed that only 22% of Ugandan and Kenyan backyard operations were vaccinated against classical swine fever in 2024. Cold-chain gaps in tropical regions cause 30% potency loss during transport, effectively doubling cost and wasting doses. HIPRA’s thermostable ASF candidate, stable at 25 °C for 6 months, could ease logistics, but success depends on sub-USD 1 pricing. Until aggregation or subsidy schemes mature, underserved smallholders limit penetration in high-population growth regions, tempering the swine healthcare market’s longer-term upside.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Diagnostics Gain as Prevention Trumps Reaction

Therapeutics captured 54.33% of the swine healthcare market share in 2025, reflecting steady demand for PRRS and Mycoplasma vaccines, parasiticides, and anti-infectives. Diagnostics contributed a smaller slice in 2025, yet their value is projected to outpace drugs at a 7.43% CAGR through 2031 as large integrators adopt weekly PCR surveillance and serology benchmarking. ELISA kits still dominate routine herd screening, but multiplex real-time PCR panels that detect ASF, Seneca Valley virus, and PCV-3 from one sample are winning orders from U.S., EU, and Chinese mega-farms. Feed additives, classified within therapeutics, posted a notable CAGR between 2020 and 2025 after the EU zinc-oxide ban steered demand toward organic acids and phytogenics. Rapid lateral-flow tests that deliver results in 15 minutes are popular among Southeast Asian veterinarians who lack lab infrastructure, expanding diagnostics penetration beyond premium markets.

The shift from curative drugs to preventive screening lifts the segment’s revenue intensity and embeds subscription-style purchases of consumables. IDEXX reported North American swine PCR volume up significantly year-over-year in 2025, evidencing that higher testing frequency offsets lower per-test pricing. Portable ultrasound devices released in 2024 enable on-farm reproductive imaging, nudging diagnostics into previously under-served management tasks. Autogenous vaccines, once a niche service, now underpin long-tail revenue for custom manufacturers acquired by Boehringer Ingelheim and Ceva. As integrators use analytics to refine vaccine schedules, therapeutics growth moderates while diagnostics accelerate, preserving the overall swine healthcare market’s 6.34% CAGR trajectory

By Disease: Emerging Viral Threats Outpace Endemic Pathogens

Respiratory diseases occupied 39.98% of the swine healthcare market size in 2025, dominated by chronic PRRS infections that erode feed efficiency and litter viability. However, emerging viral threats, notably ASF, Seneca Valley virus, and PCV-3, are forecast to expand revenue at 8.12% annually through 2031 because commercial vaccines remain unavailable outside Vietnam’s limited ASF product, and differential diagnostics are essential for trade certification. Seneca Valley virus lesions mimic foot-and-mouth disease, compelling producers to deploy multiplex PCR panels for rapid clearance of export shipments. Resistance to tiamulin and lincomycin in Brachyspira hyodysenteriae prompted renewed investment in autogenous bacterins and alternative therapeutics, keeping endemic bacterial segments relevant.

Epidemic shocks are episodic, yet they create lasting procurement habits that favor bundled diagnostics and vaccines. Government surveillance mandates in the European Union and China require quarterly or movement-linked PCR testing, embedding testing costs into routine operations. The anticipated late-2027 launch of Zoetis’ ASF vaccine could rebalance spend toward prophylaxis, but many regulators will still oblige parallel diagnostics to validate vaccine-breakthrough events. Consequently, revenue from emerging-virus solutions is unlikely to cannibalize respiratory vaccine demand; instead it layers incremental growth on top of an already sizable therapeutic base, intensifying supplier competition across platforms.

By End User: Integrators Dominate, Labs Expand Fastest

Large integrated operations accounted for 53.12% of 2025 revenue, benefiting from scale-based pricing and the capacity to run closed-herd biosecurity programs that require continuous diagnostic inputs. Companies such as Smithfield Foods, Muyuan, and Seaboard Foods operate in-house veterinary teams and contract for farm-specific autogenous vaccines, ensuring bespoke pathogen coverage. Medium commercial farms, defined as 500-5,000 head, purchase mostly off-the-shelf vaccines and outsource laboratory testing, leaving them exposed to higher per-unit costs. Smallholder and backyard producers number in the tens of millions worldwide, but represent modest revenue because high per-dose prices and cold-chain weaknesses suppress vaccine uptake.

Veterinary reference laboratories show the fastest growth at a 7.23% CAGR through 2031, driven by regulatory reporting mandates and the complexity of multiplex PCR and sequencing assays. The USDA National Animal Health Laboratory Network expanded its swine panel in 2024, guaranteeing baseline volume for participating labs. Government animal-health agencies, though a smaller slice of the swine healthcare industry, shape market direction through eradication programs and emergency vaccine stockpiles, evidenced by AU-PANVAC’s 2025 ASF initiative. Precision livestock farming vendors continue to court integrators with outcome-based subscription models that bundle wearables, diagnostics, and data analytics; these arrangements lock in multi-year reagent demand and further concentrate spending among the largest corporate herds.

Geography Analysis

North America generated 45.3% of global revenue in 2025, supported by a 74 million head inventory and strict USDA biosecurity enforcement that obliges certification for export partners Mexico, Japan, and South Korea. Canada’s voluntary data-sharing framework, adopted in 2024, incentivizes producers to submit diagnostic results in exchange for benchmarking, creating a positive feedback loop for laboratory growth. Mexico’s pork production rose in 2025, and the integrated supply chain with the United States means disease events in one nation quickly elevate vaccine and diagnostic purchasing in the other.

Asia-Pacific is forecast to register a 7.54% CAGR during 2026-2031, marking the fastest regional advance in the swine healthcare market. China’s directive that all inter-provincial pig movements pass PCR testing structurally elevates diagnostic volume, while localized ASF flare-ups sustain vaccine demand despite gradual herd rebuild. Vietnam scaled pork output to 4.8 million tonnes in 2025 on the back of biosecurity subsidies and an emergency-use ASF vaccine, yet the lack of peer-reviewed efficacy data tempers neighboring import approvals. India’s urban middle class is increasing pork intake, but fragmented smallholder supply chains restrict veterinary service access, presenting future upside for low-cost thermostable vaccines.

Europe contributed significantly to global sales in 2025, led by Germany, Spain, and France, where animal-welfare rules and the zinc-oxide ban funnel expenditure into vaccines and feed additives with antibiotic-free claims. Spain shipped notable portion of pork to China in 2025, underscoring the region’s stake in pathogen-free certification. Integrated Brazilian producers copy North American herd-health models to protect 1.2 million t of exports, channeling spend toward multinational vaccine and diagnostic suppliers. Middle East and Africa remain small, but South Africa’s commercial sector and Nigeria’s rapid herd expansion could unlock latent demand if cold-chain and veterinary staffing improve.

Competitive Landscape

The swine healthcare market features moderate concentration: the top five suppliers hold the majority of therapeutic revenue, yet diagnostics, feed additives, and autogenous vaccines are fragmented. Zoetis booked about USD 780 million from its Fostera and Circumvent lines in 2025, while Boehringer Ingelheim strengthened its position through the January 2026 purchase of Wuhan Zhongbo Biological Technology, gaining captive autogenous capacity for Chinese mega-farms. Merck Animal Health and Elanco chase growth by linking vaccines with data analytics, exemplified by Merck’s 2025 tie-up with Cargill’s SmartFarm platform to deliver predictive disease modeling.

White-space differentiation revolves around thermostable vaccines for warm climates, point-of-care PCR kits that compress turnaround time, and microbiome-focused feed additives aligned with antibiotic bans. HIPRA submitted a room-temperature ASF candidate to the EMA in September 2025, aiming to solve cold-chain losses that erode a significant portion of doses shipped to tropical markets. BioNote sells a battery-operated PCR device that detects PRRS and ASF in 90 minutes, targeting Southeast Asian producers with minimal lab access. Patent filings for swine biologics rose notably between 2023 and 2025, highlighting active R&D in mRNA, recombinant subunit antigens, and oral delivery systems.

Digital convergence is redrawing competitive lines as nutrition firms, diagnostic players, and vaccine giants collaborate on outcome-based bundles. DSM-Firmenich expanded a Jiangsu feed-additive plant in March 2025 to meet China’s post-colistin demand, while Elanco divested non-core aquaculture assets to focus cash on swine and poultry. Large integrators increasingly sign multi-year master agreements that stipulate performance metrics, pressuring suppliers to deliver holistic solutions rather than single products. The blend of therapeutics, diagnostics, nutrition, and analytics directs M&A toward platform capabilities, suggesting further consolidation as competitors strive for end-to-end control of the swine healthcare market value chain.

Swine Healthcare Industry Leaders

Boehringer Ingelheim Pharma GmbH & Co. KG

Ceva Animal Health Inc.

Zoetis Inc.

Merck & Co., Inc.

Elanco Animal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Boehringer Ingelheim launched INGELVAC CIRCOFLEX AD, the first single-dose vaccine combining PCV2a and PCV2d antigens to protect against the most prevalent Porcine Circovirus Type 2 genotypes.

- September 2025: ProtonDx’s Dragonfly diagnostic platform won the Tesco Agri T-Jam for delivering rapid on-site detection of PRRSV and swine influenza, enabling faster therapeutic intervention.

- April 2025: Virbac introduced a combination vaccine covering leptospirosis and porcine parvovirus to close immunity gaps in breeding herd.

Global Swine Healthcare Market Report Scope

As per the scope of the report, pig production is an important component of global food security, agricultural economies, and local and international trade, and swine healthcare is associated with various diseases associated with pigs. The development of diagnostics and therapeutic products to prevent related ailments and disorders affects the stability and productivity of the global swine industry.

The swine healthcare market is segmented by product, disease, end users, and geography. By products, the market is segmented into diagnostics tests (enzyme-linked immuno-sorbent assay, rapid immune migration, polymerase chain reaction, diagnostic imaging, and other diagnostics) and therapeutics (vaccines, parasiticides, anti-infectives, feed additives, and other therapeutics), by disease, the market is segmented into exudative dermatitis, coccidiosis, respiratory diseases, swine dysentery, porcine parvovirus, and other diseases, by end users, the market is segmented into large integrated swine operations, medium commercial farms, smallholder/backyard farms, veterinary reference laboratories, and government animal-health agencies.

Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Diagnostics | ELISA | |

| Rapid Immuno Migration (RIM) | ||

| Polymerase Chain Reaction (PCR) | ||

| Diagnostic Imaging | ||

| Other Diagnostics | ||

| Therapeutics | Vaccines | Live Attenuated |

| Inactivated | ||

| Subunit / Recombinant | ||

| Autogenous / Custom | ||

| Parasiticides | ||

| Anti-infectives | ||

| Feed Additives | ||

| Other Therapeutics | ||

| Exudative Dermatitis (Greasy Pig) |

| Coccidiosis |

| Respiratory Diseases (incl. PRRS, MHyo) |

| Swine Dysentery |

| Porcine Parvovirus |

| Emerging Viral Diseases (ASF, Seneca Valley, PCV-3) |

| Large Integrated Swine Operations |

| Medium Commercial Farms |

| Smallholder / Backyard Farms |

| Veterinary Reference Laboratories |

| Government Animal-Health Agencies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of APAC | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Diagnostics | ELISA | |

| Rapid Immuno Migration (RIM) | |||

| Polymerase Chain Reaction (PCR) | |||

| Diagnostic Imaging | |||

| Other Diagnostics | |||

| Therapeutics | Vaccines | Live Attenuated | |

| Inactivated | |||

| Subunit / Recombinant | |||

| Autogenous / Custom | |||

| Parasiticides | |||

| Anti-infectives | |||

| Feed Additives | |||

| Other Therapeutics | |||

| By Disease | Exudative Dermatitis (Greasy Pig) | ||

| Coccidiosis | |||

| Respiratory Diseases (incl. PRRS, MHyo) | |||

| Swine Dysentery | |||

| Porcine Parvovirus | |||

| Emerging Viral Diseases (ASF, Seneca Valley, PCV-3) | |||

| By End User | Large Integrated Swine Operations | ||

| Medium Commercial Farms | |||

| Smallholder / Backyard Farms | |||

| Veterinary Reference Laboratories | |||

| Government Animal-Health Agencies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of APAC | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of MEA | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the swine healthcare market and its forecast growth rate?

The swine healthcare market size was USD 3.74 billion in 2026 and is projected to reach USD 5.09 billion by 2031 at a 6.34% CAGR.

Which product segment is expanding faster than the overall market?

Diagnostics are forecast to grow at 7.43% CAGR through 2031 as integrators adopt weekly PCR surveillance and multiplex assays.

What diseases are driving the highest future spending?

Emerging viral threats such as African Swine Fever, Seneca Valley virus, and porcine circovirus type 3 are projected to post 8.12% annual revenue growth to 2031.

Which geographic region shows the strongest growth outlook?

Asia-Pacific is expected to expand at 7.54% CAGR between 2026 and 2031, led by China, Vietnam, and India.

What recent technological advance could ease cold-chain constraints?

HIPRA’s thermostable African Swine Fever vaccine candidate, stable at 25 °C for six months, targets potency losses in tropical regions.

Page last updated on: