Suture Anchor Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

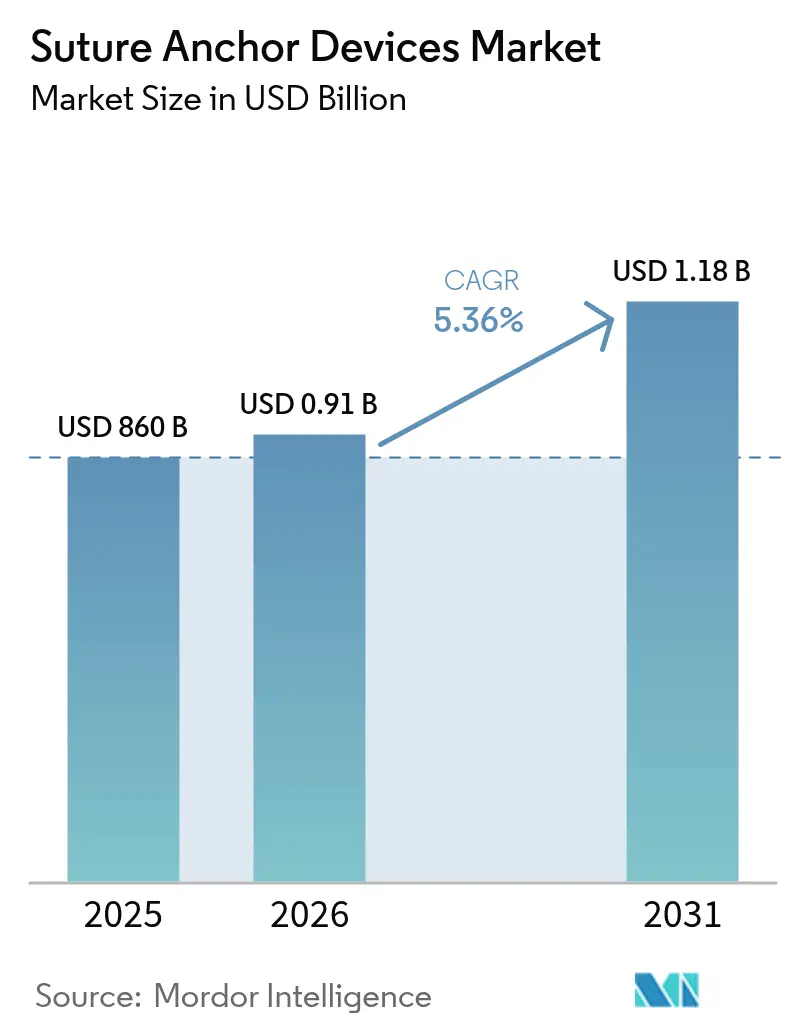

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.18 Billion |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

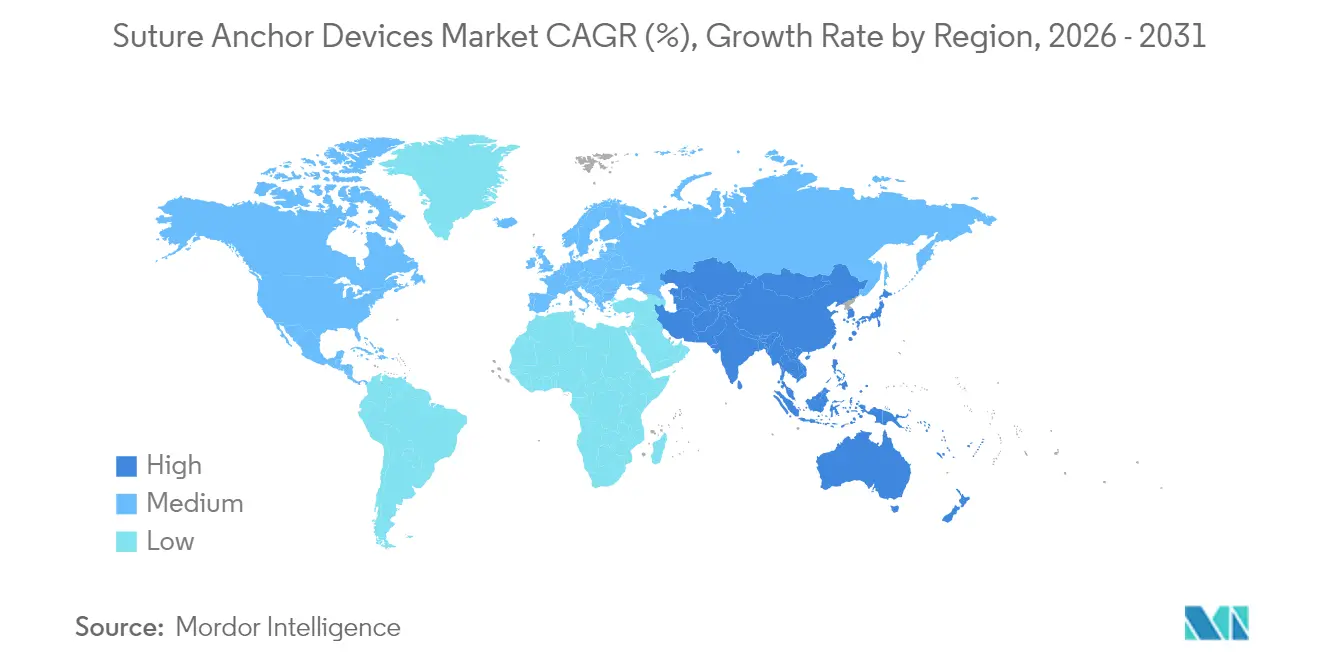

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

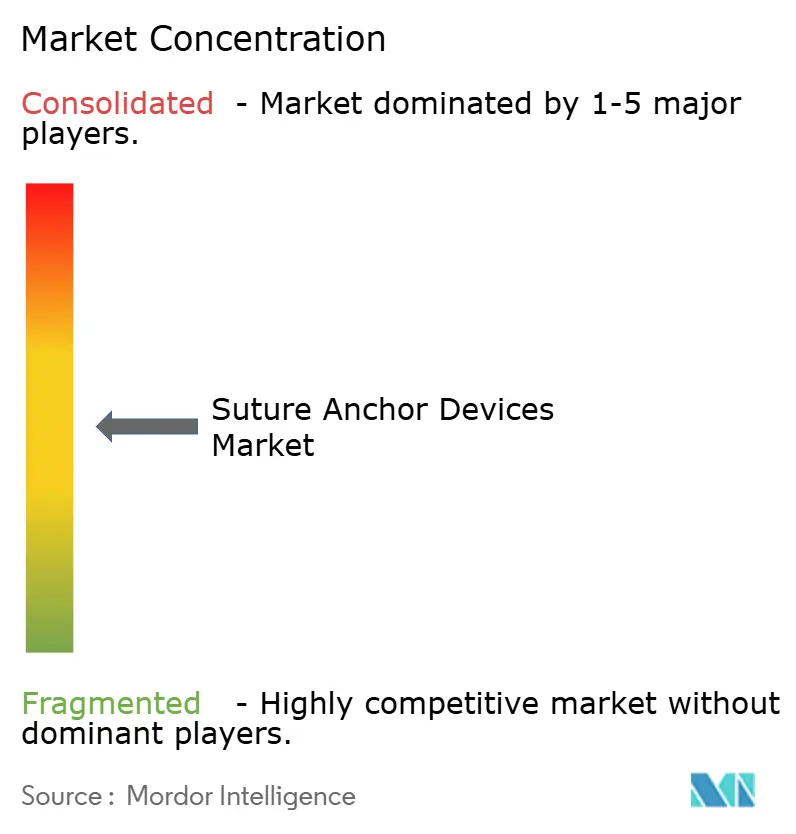

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Suture Anchor Devices Market Analysis by Mordor Intelligence

The global suture anchor devices market size was valued at USD 860 million in 2025 and estimated to grow from USD 906.1 million in 2026 to reach USD 1,176.74 million by 2031, at a CAGR of 5.36% during the forecast period (2026-2031). Growth reflects broader adoption of ambulatory surgical centers, advances in minimally invasive arthroscopy, and an aging population actively seeking elective orthopedic care. Knotless fixation, bio-absorbable materials, and tape-based constructs are shaping product differentiation as surgeons favor solutions that simplify technique while preserving post-operative imaging quality. Regulatory clarity around ASTM-recognized absorbable polymers is speeding product approvals, and reimbursement policies that lift outpatient payments by 2.9% in 2025 further stimulate procedure volumes[1]Centers for Medicare & Medicaid Services, “CY 2025 Medicare Hospital Outpatient Prospective Payment System and Ambulatory Surgical Center Payment System Final Rule (CMS 1809-FC),” cms.gov. Competitive intensity is moderate: incumbent multinationals are lengthening portfolios rather than introducing disruptive breakthroughs, while raw-material risk in PEEK supply and looming microplastics restrictions create supply-chain and compliance challenges. Demand in Asia-Pacific is accelerating on the back of expanding middle-class healthcare spending, positioning the region as the fastest-growing contributor to the suture anchor devices market through 2030.

Key Report Takeaways

- By product type, non-absorbable anchors led with 53.02% of the suture anchor devices market share in 2025, while absorbable variants are projected to grow at 8.13% CAGR to 2031.

- By material, PEEK and carbon-reinforced PEEK captured 35.12% of the suture anchor devices market size in 2025; bio-absorbable polymers are advancing at an 8.03% CAGR through 2031.

- By fixation mechanism, knotless systems accounted for 44.18% revenue in 2025, whereas tape-based platforms are forecast to expand at an 8.01% CAGR.

- By application, shoulder repairs held 37.25% of the suture anchor devices market size in 2025; hip procedures are the fastest-growing segment at 9.08% CAGR.

- By end-user, hospitals owned 67.05% revenue share in 2025, while ambulatory surgical centers are climbing at 10.06% CAGR to 2031.

- By geography, North America held 40.33% of 2025 revenue, while Asia-Pacific is advancing at a 9.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Suture Anchor Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-related orthopedic injuries surge | +1.2% | North America & Europe | Long term (≥ 4 years) |

| Growing demand for minimally-invasive arthroscopy | +0.9% | North America & Asia-Pacific | Medium term (2-4 years) |

| Increasing incidence of sports & recreation accidents | +0.7% | North America & Europe | Medium term (2-4 years) |

| Shift toward bio-absorbable anchors to reduce MRI artifacts | +0.6% | Global | Medium term (2-4 years) |

| Advancements in knotless, tape-based anchor platforms | +0.5% | Global | Short term (≤ 2 years) |

| US ASC reimbursement changes favoring anchor-based repairs | +0.4% | United States | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging-Related Orthopedic Injuries Surge

An expanding cohort of adults over 65 now drives roughly half of the 18.5 million orthopedic procedures performed annually in the United States. Higher life expectancy and active lifestyles mean more patients present with rotator-cuff tears, osteoarthritis, and hip fractures, all of which routinely require anchor fixation. Germany anticipates knee arthroplasty incidence to climb 55% by 2040, illustrating demographic pull across Europe. In parallel, U.S. outpatient reimbursement uplifts make anchor-based repairs viable in non-acute settings, reinforcing volume growth. These intersecting trends underpin durable demand for the suture anchor devices market.

Growing Demand For Minimally-Invasive Arthroscopy

Nano-arthroscopy has reduced portal size to 2 mm, enabling procedures under local anesthesia that bypass full-scale operating rooms. Arthrex’s NanoScope platform exemplifies this shift with single-use 1 mm imaging sensors that also serve as MRI alternatives. Clinical data show needle arthroscopy produces lower post-op pain scores compared with standard techniques, while ASCs can perform such cases at 26% lower cost than hospital outpatient departments. As minimally invasive preferences deepen, procedure counts—and by extension the suture anchor devices market—are set to rise.

Increasing Incidence Of Sports & Recreation Accidents

Structured surveillance records 128,761 lower-extremity injuries in U.S. track and field during the past decade, with sprains and strains forming nearly half of incidents. Soccer adds 843,063 cases, emphasizing constant ligament and tendon trauma across youth and adult athletes. ACL reconstructions exceed 400,000 annually; advanced anchors and emerging magnesium-based fixation solutions are vital for early mobilization. Such injury statistics create recurrent, procedure-driven pull for the suture anchor devices market.

Shift Toward Bio-Absorbable Anchors To Reduce MRI Artifacts

Permanent metal implants distort follow-up imaging, driving surgeons toward absorbable poly(lactide-co-glycolide) anchors now covered under ASTM F2579-18 standards[2]U.S. Food and Drug Administration, “Recognized Consensus Standards: Medical Devices,” fda.gov. Eliminating artifacts facilitates accurate re-evaluation and secondary interventions. Clinical studies confirm controlled degradation profiles and bone-substitution within 24 months, though polyglycolic acid anchors still trigger inflammatory events in 4.3% of patients. The trade-off between imaging clarity and biocompatibility keeps material innovation front and center across the suture anchor devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse tissue reactions to certain absorbable polymers | -0.8% | Global | Medium term (2-4 years) |

| Premium pricing versus conventional fixation methods | -0.6% | Price-sensitive markets | Long term (≥ 4 years) |

| Emerging micro-plastics regulations targeting degrading polymers | -0.4% | Europe | Long term (≥ 4 years) |

| PEEK supply-chain concentration elevating raw-material risk | -0.3% | Manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse Tissue Reactions To Certain Absorbable Polymers

Polyglycolic acid anchors evoke granulomatous inflammation requiring surgical drainage in 6.3% of cases, with hospital stays averaging 18 days[3]Bone & Joint Journal, “Foreign-body reactions to fracture fixation implants of biodegradable synthetic polymers,” boneandjoint.org.uk. Osteolytic tunnels can appear 12 weeks post-op, compromising fixation integrity. Carbon-fiber PEEK plates also shed particles that elevate local cytokine response. These biocompatibility hurdles temper near-term uptake of newer materials in the suture anchor devices market.

Premium Pricing Versus Conventional Fixation Methods

Advanced anchors can cost more than double stainless-steel screws, challenging adoption where centralized procurement emphasizes lowest-bid awards, as recently observed in China’s volume-based purchasing rounds. Cost-effectiveness studies still favor long-term benefits, but ASC facility managers often hesitate without clear reimbursement offsets, creating friction in expanding the suture anchor devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Absorbable Momentum Builds

Absorbable anchors represent the innovation vanguard. In 2025 non-absorbables retained the largest block at 53.02% revenue, yet absorbables are projected to outpace with an 8.13% CAGR. This divergence directly increases the suture anchor devices market size captured by degradable formats as hospitals shift to MRI-friendly post-op protocols. Smith & Nephew’s REGENESORB platform, which converts to bone within two years, embodies the clinical argument for resorption. Surgeons remain cautious because 4.3% of bio-polymer cases show adverse reactions, but ongoing polymer science is trimming complication rates. Government standards like ASTM F2579-18 certify performance criteria, easing tender participation and reinforcing confidence in the suture anchor devices market.

The non-absorbable category still commands surgeon loyalty where high-load bearing and long-term certainty are paramount. Metallic anchors excel in revision scenarios, while expanded PEEK lines deliver bone-like modulus to mitigate stress shielding. As competitive suppliers blend absorbable tips with non-absorbable cores, hybrid designs will blur categorical lines, sustaining wide choice within the suture anchor devices market.

By Material: PEEK Dominance Meets Bio-Polymer Challenge

PEEK and carbon-reinforced PEEK formed 35.12% of overall revenue in 2025, giving this high-performance polymer the single-largest material footprint in the suture anchor devices market share. Machinability and CT-compatibility make PEEK a default in complex shoulder and hip work. Evonik’s VESTAKEEP i4 3DF now enables ASTM F2026-compliant 3-D printed implants, unlocking surgeon-specific geometries. Yet bio-polymers such as PLLA and PLGA are accelerating at 8.03% CAGR, underpinned by degradability and osteoconductive fillers.

Titanium and stainless steel retain niches in trauma and hard-bone fixation where permanent strength overrides imaging concerns. Coralline graft composites and biphasic calcium phosphate-doped PEEK offer middle-ground solutions that encourage bone in-growth. Over the forecast period, material diversity is likely to intensify as suppliers hedge against PEEK supply concentration, cushioning the suture anchor devices market against raw-material shocks.

By Fixation Mechanism: Knotless Leads, Tape Gains Ground

Knotless anchors collected 44.18% revenue in 2025, exemplifying the shift toward streamlined workflows within the suture anchor devices market. Designs like Stryker’s CinchLock eliminate knot stacks, lowering subacromial irritation and speeding closures. Tape-based variants escalate at 8.01% CAGR, widening contact area that diffuses stress and supports biology; retrospective studies report 11% re-tear rates comparable to knotted repairs yet with thicker tendon healing.

Knotted anchors persist for surgeons who value tactile control or need to tailor tension intra-operatively. Second-generation all-suture platforms demonstrate 96.4% success at six months, validating soft anchors in bony avulsion repairs. Across mechanisms, intellectual-property jockeying around self-locking sleeves and expandable braids is expected to sharpen competition inside the suture anchor devices market.

By Application: Shoulder Volume, Hip Velocity

Rotator-cuff repair kept 37.25% revenue in 2025, confirming the shoulder as the volume engine of the suture anchor devices market size. Complex double-row “suture-bridge” configurations demand multiple anchors, multiplying unit consumption per case. Nonetheless, hip labral reconstructions and femoroacetabular impingement corrections show 9.08% CAGR, the fastest across joints. Surgeons attribute momentum to earlier MRI recognition and growing athlete populations seeking corrective hip work.

Meniscal, MCL, and ankle stabilization procedures increasingly rely on miniaturized anchors compatible with tight joint spaces. Robotic arthroscopic systems under development integrate automated anchor delivery, promising heightened accuracy and lower variability. These advances will continue to broaden procedure mix within the suture anchor devices market.

By End-user: Hospital Scale Versus ASC Agility

Hospitals still accounted for 67.05% global revenue in 2025, benefiting from integrated care pathways and trauma case inflow. Yet ambulatory surgical centers are projected to climb 10.06% CAGR, reflecting payer incentives and patient preference for same-day discharge. CMS added 21 codes—including rotator-cuff repairs—to the ASC-covered list for 2025, locking anchors into higher outpatient utilization. Specialty orthopedic clinics further fragment demand, targeting sports medicine and geriatric niches.

As hospitals adopt robotic suites and bundled payments, they will emphasize anchor systems compatible with efficiency metrics and digital tracking. In turn, ASCs will negotiate volume-based contracts anchored around knotless, absorbable lines that streamline turnover, collectively expanding the suture anchor devices market.

Geography Analysis

North America generated 40.33% of 2025 revenue and remains the technology bellwether for the suture anchor devices market. Medicare’s 36.2% rise in outpatient shoulder arthroplasty reimbursement, together with a 2.9% facility-wide uplift, reinforces hospital and ASC economics. Canadian universal coverage ensures consistent baseline volumes, while Mexican medical-tourism corridors broaden the regional patient pool.

Europe contributes stable but slower growth as national health systems impose strict cost containment. Medical Device Regulation (EU) 2017/745 compels recertification of legacy anchors, adding compliance costs yet heightening product quality. Germany’s knee and hip replacement projections underpin procedure demand, whereas microplastics rules effective October 2029 will steer material choices toward eco-compliant polymers.

Asia-Pacific is on a 9.14% CAGR trajectory, outpacing all regions. Japan showcases early adoption of robotic arthroplasty and absorbable anchors to manage an aging demographic. India and ASEAN nations prioritize capacity investments; reference-market inclusion changes in Australia simplify device approvals, speeding cross-border introduction. Manufacturers with regional assembly or price-band portfolios will capture outsized upside in this high-growth theater of the suture anchor devices market.

Competitive Landscape

Market concentration is moderate, with Smith & Nephew, Johnson & Johnson, Arthrex, and Zimmer Biomet controlling a majority share through broad catalogs rather than singular blockbuster devices. Platform ecosystems tether anchors to proprietary inserters and sutures, deepening switching costs. Recent examples include Smith & Nephew’s foot-and-ankle tension-adjustment suite and Stryker’s USD 4.9 billion acquisition of Inari Medical to diversify into venous care, both moves enhancing cross-selling leverage.

Emerging entrants exploit material niches—such as fully bio-composite anchors—or leverage additive manufacturing for patient-specific geometries. Tetrous’ EnFix patents extend preload retention mechanisms, highlighting IP skirmishes around fixation biomechanics. FDA technical amendments enabling predetermined change-control plans reduce regulatory friction for iterative upgrades, a boon for agile competitors.

Risk factors include PEEK resin concentration among a handful of suppliers and intermittent shortages affecting lead times. Additionally, bio-polymer biocompatibility events can trigger recalls, impacting brand reputation across the suture anchor devices industry. Strategic hedging through multi-source agreements and diversified material science pipelines is therefore central to sustaining leadership.

Suture Anchor Devices Industry Leaders

Smith & Nephew plc

Zimmer Biomet Holdings

ConMed Corporation

Arthrex, Inc.

Johnson and Johnson (DePuy Synthes, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Smith & Nephew launched a comprehensive foot-and-ankle repair portfolio in Australia and New Zealand, featuring adjustable tensioning technology for Achilles reconstruction and lateral ankle instability repair.

- January 2025: Stryker completed the USD 4.9 billion acquisition of Inari Medical, entering the fast-growing peripheral vascular segment to broaden its procedural ecosystem.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the suture anchor devices market as the worldwide sales of sterile, single-use implants, metallic, polymer, PEEK, or bio-composite, designed to secure soft tissue to bone during arthroscopic or open orthopedic procedures such as rotator-cuff, meniscal, and labral repairs. Our review tracks unit and revenue flows across hospitals, ambulatory surgical centers, and specialty orthopedic clinics in 17 major economies, converting all values to constant 2024 US dollars for consistency.

Scope exclusion: trauma plates, interference screws, and other ligament fixation devices lie outside this study to keep the anchor universe narrowly focused on soft-tissue reattachment.

Segmentation Overview

- By Product Type

- Absorbable

- Non-Absorbable

- By Material

- Metal (Titanium / Stainless)

- Bio-absorbable Polymer (PLLA, PLGA)

- PEEK & Carbon-reinforced PEEK

- Hybrid / Bio-composite

- By Fixation Mechanism

- Knotted

- Knotless

- Tape-based

- By Application

- Shoulder-Rotator Cuff

- Hip-Labral & FAIS

- Knee-Meniscal & MCL

- Foot & Ankle

- Elbow & Wrist

- By End-user

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty Orthopedic Clinics

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with orthopedic surgeons, ASC procurement leads, and regional distributors across North America, Europe, and Asia-Pacific. These discussions validated typical anchor mix shifts, toward knotless and bio-absorbable lines, triangulated average selling prices, and tested early forecasts against on-ground demand sentiment.

Desk Research

We began by sampling open datasets from bodies such as the WHO's Global Health Observatory, OECD Health Stats, and United States FDA 510(k) clearance logs, which reveal annual procedure counts and new device introductions. Trade and customs dashboards, UN Comtrade and Volza, helped us gauge cross-border anchor shipments, while peer-reviewed journals in Arthroscopy and The American Journal of Sports Medicine quantified anchor adoption trends. Subscription databases, including D&B Hoovers for company revenue splits and Dow Jones Factiva for price trackers, rounded out baseline inputs. This list is illustrative; numerous additional public and paid sources fed our desk research pipeline.

A second pass collated orthopedic society reports, AAOS and ESSKA, and national tariff codes, enabling our analysts to align volume series with ASP ranges by material type. These curated signals became the foundation on which subsequent primary research was layered.

Market-Sizing & Forecasting

A blended top-down view, hospital procedure pools multiplied by anchor utilization rates and calibrated with trade flow adjustments, generated our first cut. We then cross-checked totals through selective bottom-up roll-ups of leading vendor revenues and sample ASP × unit estimates, fine-tuning gaps before lock-in. Key variables in the model include arthroscopy volumes, geriatric population growth, sports injury incidence, and bio-absorbable price deltas. Multivariate regression, augmented by scenario analysis for reimbursement changes, projects the market through 2030.

Data Validation & Update Cycle

Outputs pass two-tier analyst reviews, variance screens against independent indicators, and a re-contact trigger when quarterly FDA approvals or major recalls shift demand. Reports update annually, with interim refreshes after material events, ensuring clients receive our latest calibrated baseline.

Why Mordor's Suture Anchor Devices Baseline Commands Reliability

Published figures often diverge because firms pick different device baskets, currency bases, and refresh cadences. Our disciplined scope, annual refresh, and dual-side validation make the 2025 value of USD 0.86 billion a dependable starting point.

Major gap drivers include: some studies fold interference screws into totals; others roll only hospital channels and miss fast-growing ASCs; a few rely on static ASPs or aged procedure data, inflating or deflating outcomes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.86 B (2025) | Mordor Intelligence | - |

| USD 0.84 B (2025) | Global Consultancy A | Includes limited country set and applies flat ASP, understating Asia-Pacific potential |

| USD 0.88 B (2025) | Industry Tracker B | Omits ASC volumes yet inflates totals via vendor shipment extrapolation without trade reconciliation |

Taken together, the comparison shows that Mordor Intelligence delivers a balanced, fully traceable baseline, rooted in transparent variables and repeatable steps, giving decision-makers confidence that our numbers reflect real-world orthopedic demand rather than model artifacts.

Key Questions Answered in the Report

What is the current size of the suture anchor devices market and how fast is it growing?

The market is valued at USD 906.1 million in 2026 and is forecast to reach USD 1,176.74 million by 2031, growing at a 5.36% CAGR.

Which product types are expanding the quickest?

Absorbable anchors show the fastest momentum, advancing at an 8.13% CAGR as surgeons favor MRI-friendly, resorbable solutions.

Why are knotless and tape-based fixation systems gaining popularity?

They shorten operating time, reduce soft-tissue irritation, and provide load distribution that supports better healing, driving an 8.01% CAGR for tape-based designs.

Which region offers the highest growth potential through 2031?

Asia-Pacific leads with a projected 9.14% CAGR, buoyed by expanding healthcare infrastructure and rising middle-class demand for advanced orthopedic care.

What key factors may restrain market growth?

Adverse tissue reactions to certain bio-polymers, premium pricing pressures in cost-sensitive markets, and upcoming microplastics regulations could temper adoption.

Page last updated on: