Stationery And Supplies Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

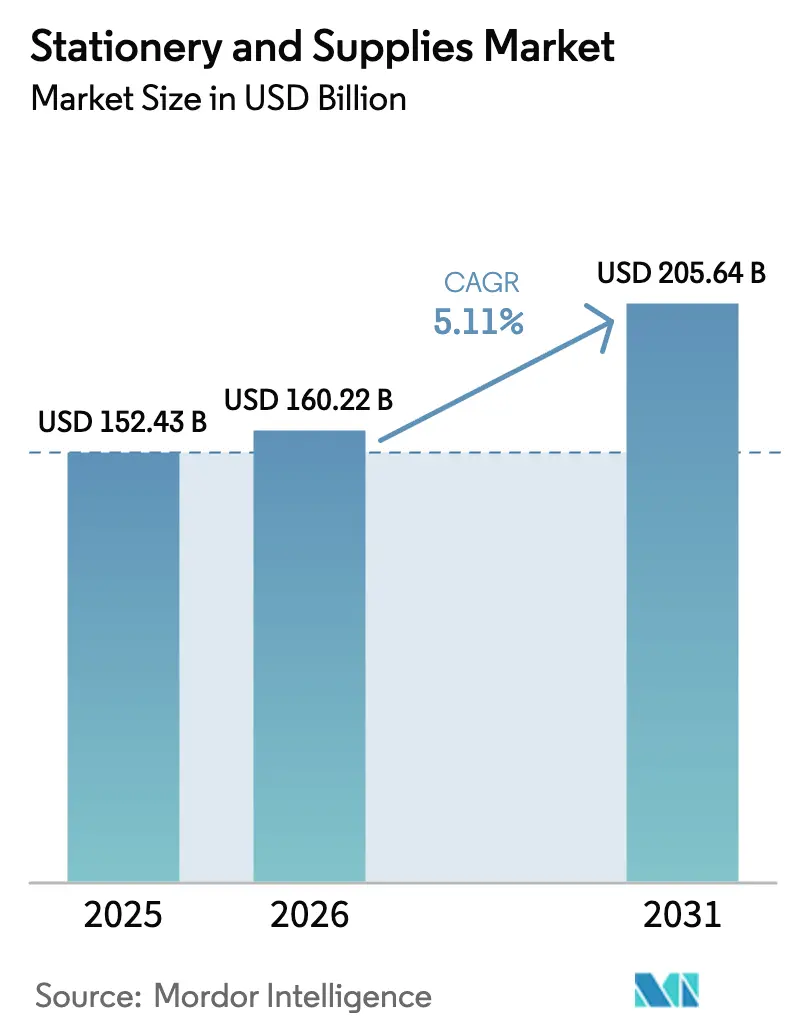

| Market Size (2026) | USD 160.22 Billion |

| Market Size (2031) | USD 205.64 Billion |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stationery And Supplies Market Analysis by Mordor Intelligence

The stationery and supplies market size is expected to grow from USD 152.43 billion in 2025 to USD 160.22 billion in 2026 and is forecast to reach USD 205.64 billion by 2031 at 5.11% CAGR over 2026-2031. Several forces converge to sustain this expansion even as device proliferation tempers low-value paper demand. Worldwide primary and tertiary enrolment increases keep institutional orders for exercise books, art supplies, and examination sheets buoyant. Corporate procurement teams now anchor purchasing criteria in environmental, social, and governance policies, which lifts revenue from recycled and certified-sustainable lines that sell at a premium. Omnichannel commerce reshapes shopper journeys. Discovery often starts on social or marketplace platforms before consumers complete tactile validation in specialty stores, enabling price discipline on high-touch items such as fountain pens. Finally, product innovation, reusable cloud-linked notebooks, refillable metal-barrel pens, and biodegradable adhesives unlock fresh price ladders that offset raw-material volatility and margin pressure.

Key Report Takeaways

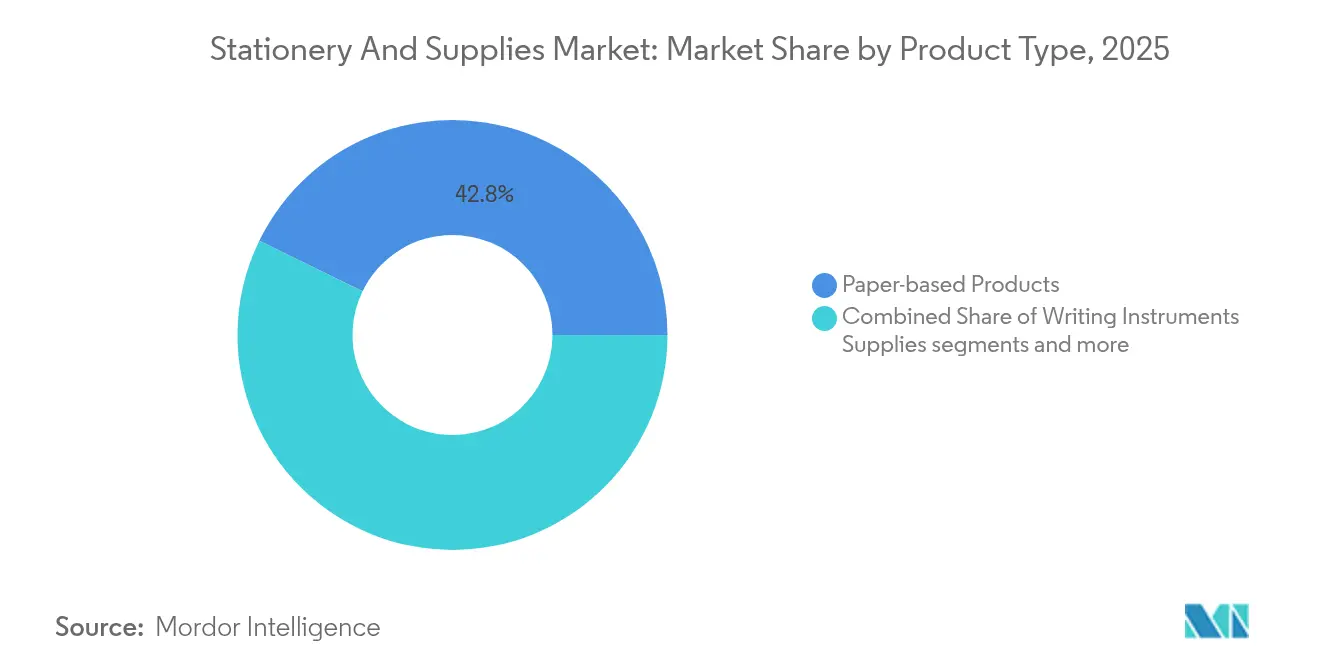

- By product type, paper-based products captured 42.78% of stationery and supplies market share in 2025. Office essentials posted the highest growth, expanding at a 6.29% CAGR to 2031.

- By distribution channel, offline specialty stores accounted for 55.72% of the stationery and supplies market size in 2025. Online marketplaces are advancing at a 6.86% CAGR through 2031.

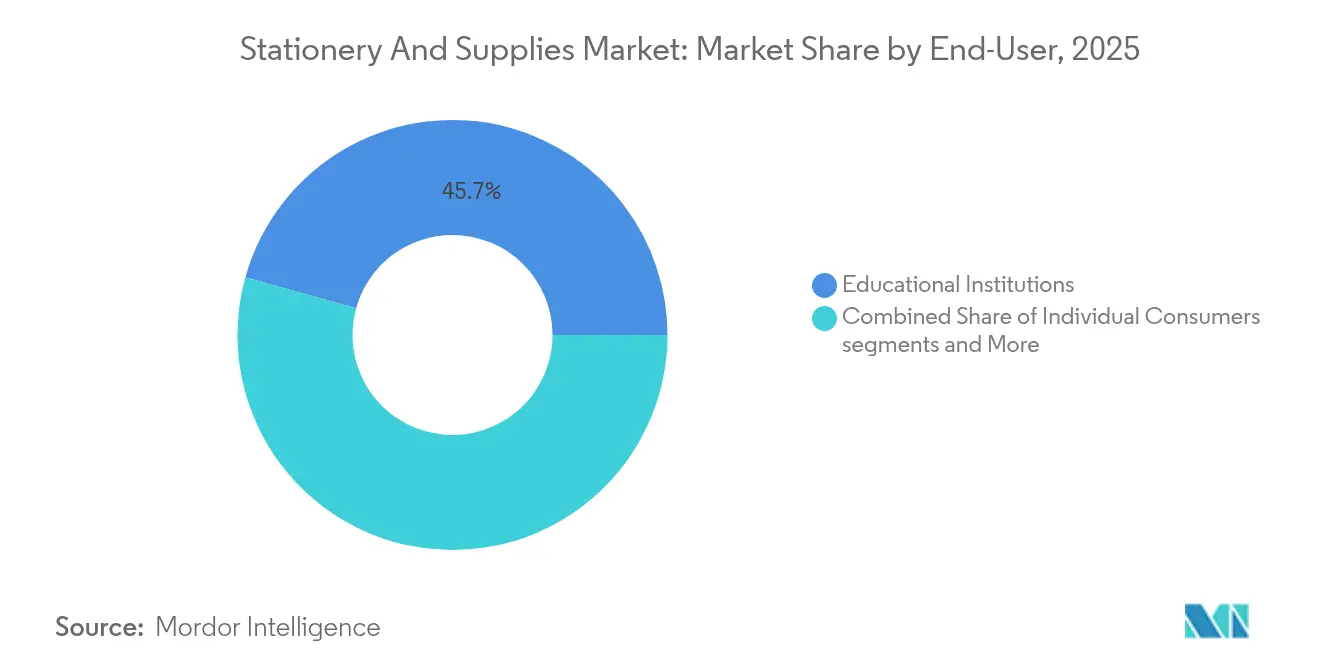

- By end-user, educational institutions led with 45.68% revenue in 2025. Individual consumers are forecast to grow at a 5.62% CAGR between 2026-2031.

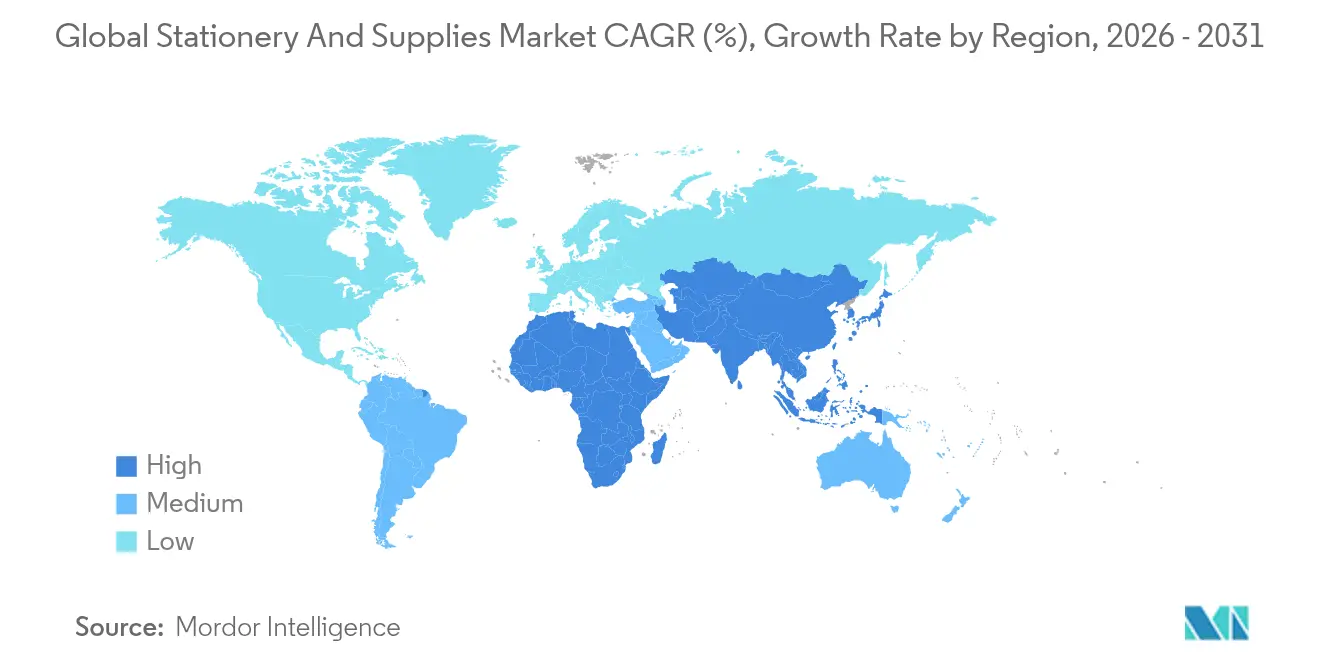

- By geography, Asia-Pacific held 35.30% of the global stationery and supplies market share in 2025, while the region also registers the fastest 6.02% CAGR out to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Stationery And Supplies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising e-commerce penetration for stationery and office supplies | +1.2% | North America, Asia-Pacific (global spillover) | Medium term (2-4 years) |

| Expanding enrolment rates in K-12 and tertiary education | +0.9% | Asia-Pacific, Africa | Long term (≥ 4 years) |

| Premium and customized writing instruments | +0.7% | Urban North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Smart reusable notebooks integrated with cloud services | +0.5% | North America, Europe, Japan, urban China | Short term (≤ 2 years) |

| Corporate ESG mandates for recycled stationery | +0.8% | North America, Europe, Australia | Medium term (2-4 years) |

| Revival of journaling / art-therapy trends among Gen-Z | +0.6% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising E-commerce Penetration for Stationery and Office Supplies

Online marketplaces post a 7.02% CAGR through 2030, far outpacing brick-and-mortar growth in the stationery and supplies market. Digital storefronts compress go-to-market timelines for niche brands, allowing them to test micro-collections of pens, inks, and planner inserts with minimal capital risk. Japanese exporters lifted revenue to JPY 120 billion (USD 0.8 billion) in 2023, a 15% rise from 2018, primarily by fulfilling small-lot cross-border e-commerce orders[1]FedEx, “Why the World Loves Japanese Stationery,” fedex.com. Brands that combine highly visual product pages, user-generated reviews, and transparent shipping calculators see reduced return rates and higher average order values. KOKUYO’s decision to complement its second Shanghai “Campus STYLE” flagship with a robust Chinese web-app underscores omnichannel complementarity and sets a benchmark for experiential cohesion. Midsize retailers unable to finance proprietary tech increasingly partner with platforms. Dynamic Supplies added 900 ACCO items to its digital catalogue to safeguard relevance.

Expanding Enrolment Rates in K-12 and Tertiary Education Worldwide

Global enrolment trends underpin roughly half of baseline volume in the stationery and supplies market. International student mobility climbed from 2 million in 1998 to 6.4 million in 2020 and is projected to grow 4-4.5% annually to 2030[2]British Council, “The Outlook for International Student Mobility,” britishcouncil.org. Developing regions witness parallel momentum: Ghana, Kenya, and Vietnam each allocated at least 20% of annual budgets to education in 2024, funneling capital into textbooks, lab workbooks, and classroom consumables. At the other end of the value spectrum, affluent parents in urban India now prioritize premium artist-grade sketchbooks, reflecting a shift from basic functional spending to aspirational purchases. Though 249 million children remain out of school, multilateral organizations have earned USD 4.5 billion for catch-up learning by 2028, which promises incremental demand as access deficits narrow.

Premium and Customized Writing Instruments Gaining Traction

In saturated smartphone environments, writing instruments reposition as identity statements. Collectors line up for serialized fountain pens featuring regional motifs, and price points exceed USD 800 for one-off artisan models. Corporate gifting revives post-pandemic, with investment banks, consulting firms, and law offices ordering engraved lacquer-finish pens for milestone deals. Custom pen kits that allow users to swap nib grades or barrel colors aid replenishment revenue—a tactic BIC has mirrored through refill subscription trials, supported by R&D spend equal to 10% of net sales. Independent pen tuners offering nib grinding on TikTok drive micro-influencer awareness, feeding long-tail brand equity across the stationery and supplies market.

Smart Reusable Notebooks Integrated with Cloud Services

Reusable notebook vendors leverage polymer-coated pages and microwave-safe inks that erase after heat exposure, guaranteeing hundreds of reuse cycles. Device-agnostic scanning apps use AI-based handwriting recognition to push notes to Google Drive, OneDrive and proprietary learning-management systems. In 2024, two U.S. community-college districts bundled cloud-linked notebooks into digital equity programs, lowering laptop dependence in low-income cohorts while maintaining submission compatibility. In Japan, cram-school providers partnered with notebook manufacturers to preload QR-coded practice sheets that sync with grading dashboards, reinforcing the stationery and supplies market as a pivot for ed-tech services. Key hurdles—battery-free tagging, spiral durability and licensing fees—remain, but gross profit still outperforms commodity notepads by 12-15 percentage points.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating digitalization by reducing paper consumption | -1.8% | North America, Europe, Japan | Long term (≥ 4 years) |

| Volatility in pulp and petro-chemical input prices | -0.9% | Global—biggest hit to commodity SKUs | Medium term (2-4 years) |

| Counterfeiting and grey-import channels | -0.4% | Southeast Asia, parts of Latin America | Medium term (2-4 years) |

| Pigment/ink supply shocks from geo-political conflicts | -0.3% | Global, specialty lines | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Pulp and Petro-Chemical Input Prices

Wild swings in key inputs destabilize production budgets and squeeze gross margins for notebooks, pens, and packaging. Corrugated cardboard benchmark prices jumped USD 70 per ton in early 2025 as pulp shortages, energy surcharges, and freight bottlenecks cascaded through the supply chain[3]Creative Edge Packaging, “Navigating the USD 70 Per Ton Increase in Corrugated Cardboard,” cepkg.com. Chinese paper mills quickly followed by raising list prices about USD 31.50 per ton to offset higher wood-fiber and electricity costs, passing fresh pressure onto converters worldwide. At the same time, explosions and shutdowns at Southeast Asian chemical plants created a nitrocellulose shortage that forced ink makers to levy 5-9% surcharges on specialty and bulk formulations. Color-pigment suppliers layered additional tariff-related fees for toluene- and xylene-based intermediates, adding another unpredictable variable to coating and barrel costs. While large multinationals hedge pulp and resin exposure through multi-year contracts, small and midsize stationery brands often must adjust catalog prices within weeks, risking volume loss to lower-cost private labels.

Accelerating Digitalization, Reducing Paper Consumption

Digital workflows continue to replace routine printing and copying across offices, classrooms, and public agencies, sharply curbing demand for low-grade graphic paper. Europe’s paper industry registered a 28% year-over-year fall in graphic-paper output during 2023 as employers accelerated e-signature rollouts and publishers shifted to digital formats[4]Pulpapernews, “Paper Industry Faced Unprecedented Decline in 2023,” pulpapernews.com. Japan experienced a 10% contraction in domestic stationery sales from 2019-2023 as consumers gravitated toward tablets for study and note-taking, even though export sales of premium pens and notebooks climbed on overseas demand. Local governments add to the shift: several California municipalities cut council-meeting print volumes by 60% after adopting paperless agenda software, setting a template other U.S. cities now study for replication. Education ministries still preserve handwritten exercises for early-grade literacy, yet the overall classroom mix tilts toward online assessments and e-textbooks, gradually eroding bulk exercise-book orders. As these trends coalesce, traditional paper suppliers face a structural, rather than cyclical, decline in their largest volume segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Paper Products Dominate Despite Digital Pressures

Paper goods anchor 42.78% of the stationery and supplies market size in 2025, proving resilient due to classroom mandates for notebooks, exam answer sheets, and art pads. Recycled-content copy paper gains traction after the U.S. federal directive eliminated virgin paper from procurement catalogues. Simultaneously, office essentials—staplers, desk organizers, labeling devices—log a 6.29% CAGR because flexible workspaces emphasize modular desk setups. Writing instruments enjoy value-added lift: metallic body finishes, hybrid gel-ball inks, and quick-dry technology answer user pain points identified in social-media feedback loops.

Smart stationery, though holding less than 5% revenue share in 2025, represents the fastest innovation channel. Start-ups bundle reusable books with cloud storage for a one-year subscription, after which renewal runs USD 2-3 monthly, creating a service layer absent in legacy paper. Art and craft items ride the Gen-Z creativity wave, but premiumization distinguishes winners: cotton-rag watercolor pads and alcohol-marker paper command 3-4 times commodity sheet pricing. Asian powerhouses like M&G booked +16.78% YoY growth in 2023. Product managers increasingly weigh carton cube efficiency and e-commerce damage rates at the design stage, aligning spec decisions with growing online volume in the stationery and supplies market.

By Distribution Channel: Digital Transformation Accelerates

Offline specialty stores controlled 55.72% of the global stationery and supplies market share in 2025, reflecting the enduring appeal of tactile product trials, on-site engraving services, and community workshops that online platforms cannot fully mimic. Shoppers often visit these boutiques to test fountain-pen nibs, compare paper textures, and access immediate personalization, activities that anchor premium price realization and generate repeat traffic. However, the channel’s growth pace trails the overall stationery and supplies market size because floor space limits SKU breadth, and staffing costs tighten margins. In response, leading chains invest in appointment scheduling, loyalty apps, and in-store events such as calligraphy classes to deepen engagement without relying solely on walk-in footfall. Some formats integrate coffee corners and maker spaces to lengthen dwell time, positioning the store as a lifestyle venue instead of a pure transaction point. Luxury brands further leverage flagship locations for limited-edition drops that align with social-media countdowns, thereby converting exclusivity into front-page visibility.

Online marketplaces and brand web shops, advancing at a 6.86% CAGR through 2031, add the most incremental revenue to the stationery and supplies market. Algorithmic recommendations bundle complementary items—dot-grid journals, brush pens, and mild liner sets—raising average order value and lowering discovery friction for niche products. Cross-border logistics agreements between Japan Post and USPS, introduced in 2024, reduced transit times for small parcels to the United States from 19 to 11 days, convincing more Japanese brands to sell direct. Distributors also pivot: Dynamic Supplies integrated 900 ACCO SKUs into its e-catalog, giving resellers real-time stock visibility and automated replenishment triggers that shrink out-of-stocks to below 2%. Hybrid models flourish as retailers like WHSmith employ click-and-collect, allowing consumers to combine online assortment depth with same-day pickup convenience. Supermarkets and hypermarkets still capture impulse notebook and pen purchases, yet their relative share declines as engaged buyers shift to digital subscriptions. Institutional e-procurement portals round out the channel mix, bundling recycled copier paper, toner, and filing supplies under multiyear contracts that favor vendors with stable fulfillment metrics and ESG credentials.

By End-User: Educational Dominance Meets Consumer Innovation

Educational institutions generated 45.68% of global revenue in 2025, a position rooted in compulsory schooling laws, rising tertiary enrollment, and steady textbook cycles. Ministries procure bulk exercise books, exam answer sheets, and art kits through competitive tenders that specify recycled content thresholds and durability standards. In emerging Asia, per-pupil public spending climbed 9% during 2024, and new curriculum mandates in India now require science-lab notebooks from grade 6 onward, adding fresh volume. Universities extend demand with specialized formats like carbonless lab logbooks and thesis-binding sets, each carrying higher gross margins than standard ruled pads. Campus bookstores diversify by pairing branded planners with wellness journals, capturing discretionary spend from student wellness budgets. Supplier consolidation benefits this segment because institutions favor vendors that can guarantee multi-year continuity, consistent paper opacity, and on-site delivery within narrow orientation-week windows.

Individual consumers, expanding at a 5.62% CAGR, have become the fastest-growing cohort within the stationery and supplies market. Gen-Z shoppers treat journals, stickers, and fine-liner pens as self-care tools, a trend amplified by social-media influencers who post desk setup videos and habit-tracker tutorials. Subscription services deliver themed boxes each month, smoothing seasonality for retailers and encouraging cross-selling of specialty paper and storage pouches. Corporate and home-office users occupy the middle ground, combining flexible work realities with ESG compliance targets that favour FSC-certified folders and carbon-neutral courier options. Small-business owners increasingly order branded notebooks in short digital-print runs, reinforcing identity at client meetings and trade fairs without tying up cash in large inventories. Government agencies complete the end-user matrix through framework agreements that lock in predictable quantities but impose strict documentation on recycled content and supply-chain transparency. Together, these diverse demand profiles balance cyclical swings and provide a multi-layered safety net for long-term growth.

Geography Analysis

Asia-Pacific owns 35.30% of global sales and climbs at a 6.02% CAGR through 2031. China’s M&G leverages automated lines to deliver 23% gross margin even as it scales domestic storefronts in tier-2 cities. Japanese exporters thrive on premium equity: fountain pens with urushi lacquer and notebooks with lightweight “Tomoe River” paper attract collectors worldwide, supporting a 120-billion-yen export figure in 2023. India’s National Education Policy expanded textbook outlays, and textbook publishers co-bundle art kits to boost per-student spending. Southeast Asian hubs like Vietnam lure contract manufacturing via competitive labor rates, feeding private-label pipelines for Western retailers and broadening the stationery and supplies market.

North America’s demand profile tilts toward smart devices and eco-labelled products. While U.S. office-supply sales dipped to USD 11.5 billion in 2024, Circana expects stabilization by 2027 as hybrid offices normalize ordering patterns. Canada’s federal green-procurement guidelines mirror U.S. thresholds, pushing domestic mills to certify FSC status. Europe displays similar maturity but imposes stricter waste-reduction directives. Germany’s Blue Angel ecolabel, for example, dominates tender requirements.

Middle East & Africa post double-digit growth off a small base, driven by urbanization, private-school chains, and public-sector digitization drives that still require hybrid stationery supplies. Latin America’s consumption rises with middle-class expansion but is tempered by currency swings, however, local pulp availability aids cost competitiveness in notebook exports to the United States. Across emerging regions, distributors that bundle teacher-training content with product orders secure stickier relationships and a higher share in the stationery and supplies market.

Competitive Landscape

The stationery and supplies market features moderate concentration: the top five firms hold roughly 40 -50% global revenue, ensuring price visibility without precluding niche insurgents. BIC’s 8% share stems from broad distribution, while Pilot, Faber-Castell, and Pentel occupy premium and professional corners. Packaging giants press in through M&A: International Paper’s USD 7.2 billion purchase of DS Smith pivoted capacity toward fiber-based boxes that double as bulk notebook covers. Smurfit Kappa’s merger with WestRock created a USD 34.0 billion entity able to integrate board, print, and finishing, offering turnkey school-supply kits to distributors. Xerox’s USD 1.5 billion Lexmark acquisition strengthened aftermarket toner leverage and cross-selling of paper to MPS clients.

Asian manufacturers inject volume agility, M&G’s patent trove facilitates design refreshes in under 90 days, matching social-media trend velocity. Japanese brands defend high gross margins via limited editions and museum collaborations. Digital-native entrants exploit influencer partnerships and zero-inventory print-on-demand, sidestepping traditional wholesale mark-ups. ESG leadership emerges as a moat: ACCO Brands’ progress on energy cuts and recycled materials wins framework agreements with federal buyers. Overall, sustainable sourcing, digital enablement, and speed-to-trend outrank scale alone in determining future winners within the stationery and supplies market.

Stationery And Supplies Industry Leaders

3M Company

ACCO Brands Corporation

Société BIC S.A.

Kokuyo Co., Ltd.

Faber-Castell AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BIC disclosed CEO transition effective Sep 2025 after surpassing EUR 2.0 billion (USD 2.16 billion )revenue and lifting innovation spend to 10% of sales.

- December 2024: Xerox finalized USD 1.5 billion Lexmark acquisition, projecting USD 200 million cost synergies.

- July 2024: Smurfit Kappa merged with WestRock forming Smurfit WestRock, a USD 34.0 billion packaging leader.

- April 2024: KOKUYO launched its second “Campus STYLE” Shanghai store featuring 2,000 SKUs, many China-exclusive.

Global Stationery And Supplies Market Report Scope

Stationery, such as paper, pens, and ink, is used in offices and educational institutes for writing, typing, and printing. This report aims to provide a detailed analysis of the stationery and supplies market. The market dynamics, new trends in the segments and local markets, and insights into the many kinds of products and applications are its main points of emphasis. It evaluates the competitive environment as well as the major players. The stationery and supplies market is segmented by product, which includes paper-based, ink-based, art-based, and others; by application, including educational institutes, corporations, and others; by distribution channel, including online and offline and by geography, including North America, Europe, Asia-Pacific, South America, and the Middle East. The report offers market size and forecasts for the stationery and supplies market regarding revenue (USD) for all the above segments.

| Paper-based Products |

| Writing Instruments |

| Art and Craft Supplies |

| Office Essentials (Non-paper) |

| Offline - Specialty Stationery Stores |

| Offline - Super/Hypermarkets & Bookstores |

| Online - E-commerce & Marketplaces |

| Educational Institutions |

| Corporate and Home-office Users |

| Individual Consumers |

| Government and Public Sector |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Australia | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Paper-based Products | |

| Writing Instruments | ||

| Art and Craft Supplies | ||

| Office Essentials (Non-paper) | ||

| By Distribution Channel | Offline - Specialty Stationery Stores | |

| Offline - Super/Hypermarkets & Bookstores | ||

| Online - E-commerce & Marketplaces | ||

| By End-User | Educational Institutions | |

| Corporate and Home-office Users | ||

| Individual Consumers | ||

| Government and Public Sector | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global stationery and supplies market in 2026?

The stationery and supplies market size sits at USD 160.22 billion and is forecast to reach USD 205.64 billion by 2031 at a 5.11% CAGR.

Which product category is growing fastest?

Office essentialsnon-paper desk accessorieslead growth at a 6.29% CAGR due to flexible workspace demand.

Why is Asia-Pacific critical for future sales?

The region already holds 35.30% share and benefits from expanding education budgets, rising disposable incomes and strong cultural affinity for premium stationery.

How are sustainability mandates shaping supplier strategies?

Regulations requiring 95% recycled content in government purchasing push vendors to certify materials and support premium pricing for eco-labelled lines.

What role does e-commerce play in market growth?

Online channels grow at 6.86% CAGR, enabling SKU variety, customization and cross-border sales that outpace store-only growth.

Are smart reusable notebooks a sizable opportunity?

While still under 5% of revenue, reusable cloud-enabled notebooks post double-digit growth and introduce subscription revenue streams, raising margins beyond commodity pads.

Page last updated on: