Satellite Parts and Components Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

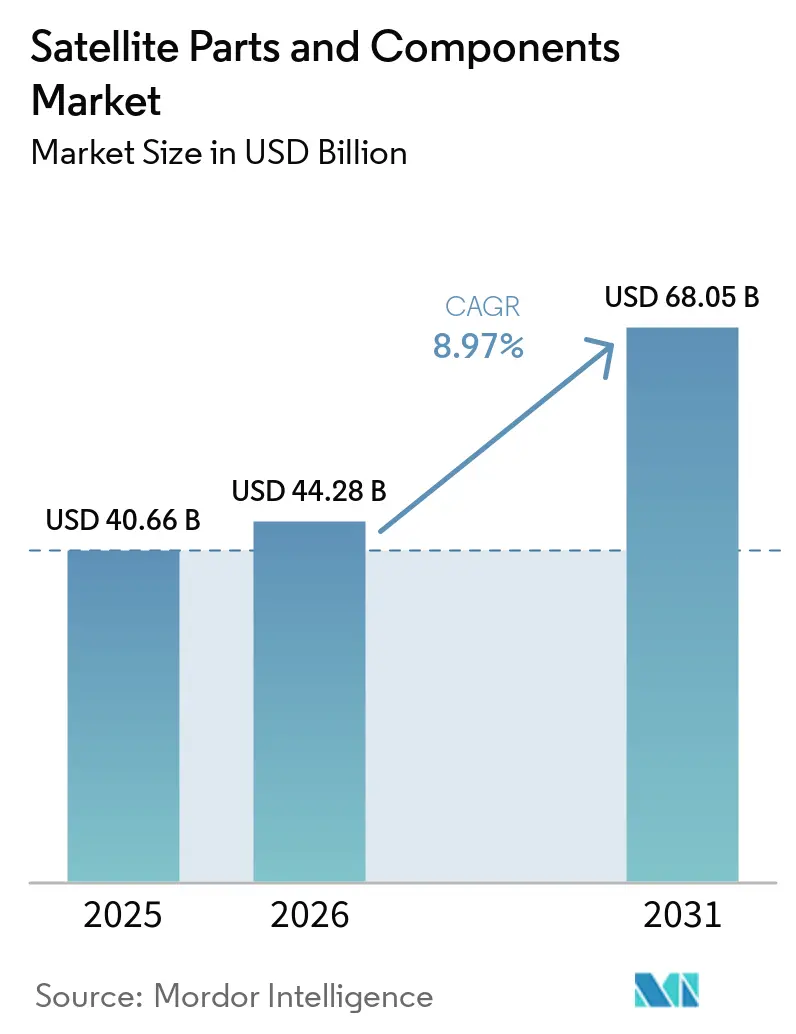

| Market Size (2026) | USD 44.28 Billion |

| Market Size (2031) | USD 68.05 Billion |

| Growth Rate (2026 - 2031) | 8.97% CAGR |

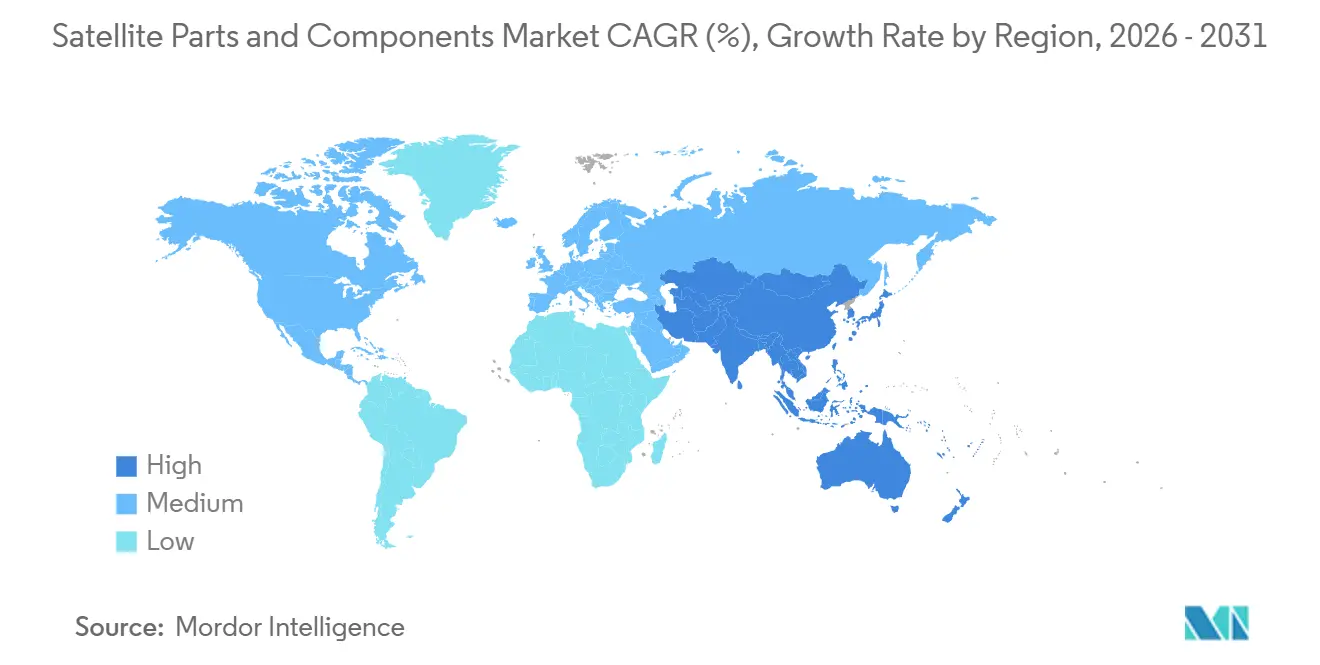

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Satellite Parts and Components Market Analysis by Mordor Intelligence

The satellite parts and components market size is expected to grow from USD 40.66 billion in 2025 to USD 44.28 billion in 2026, and is forecasted to reach USD 68.05 billion by 2031 at an 8.97% CAGR over 2026-2031. Growth reflects the acceleration of proliferated low Earth orbit (LEO) networks, the standardization of satellite platforms for serial production, and the adoption of COTS components across defense programs. Multi-vendor procurement for missile warning and tracking satellites is widening supplier participation and compressing unit economics across avionics, power, propulsion, and communications subsystems. Regulatory momentum on orbital debris mitigation is reshaping propulsion sizing and end-of-life design choices, strengthening demand for deorbit capabilities and autonomous guidance. Asia-Pacific policy actions, including Japan’s Space Strategy Fund, are anchoring long-term capacity build-out and component localization that raise competition against North American incumbents.

Key Report Takeaways

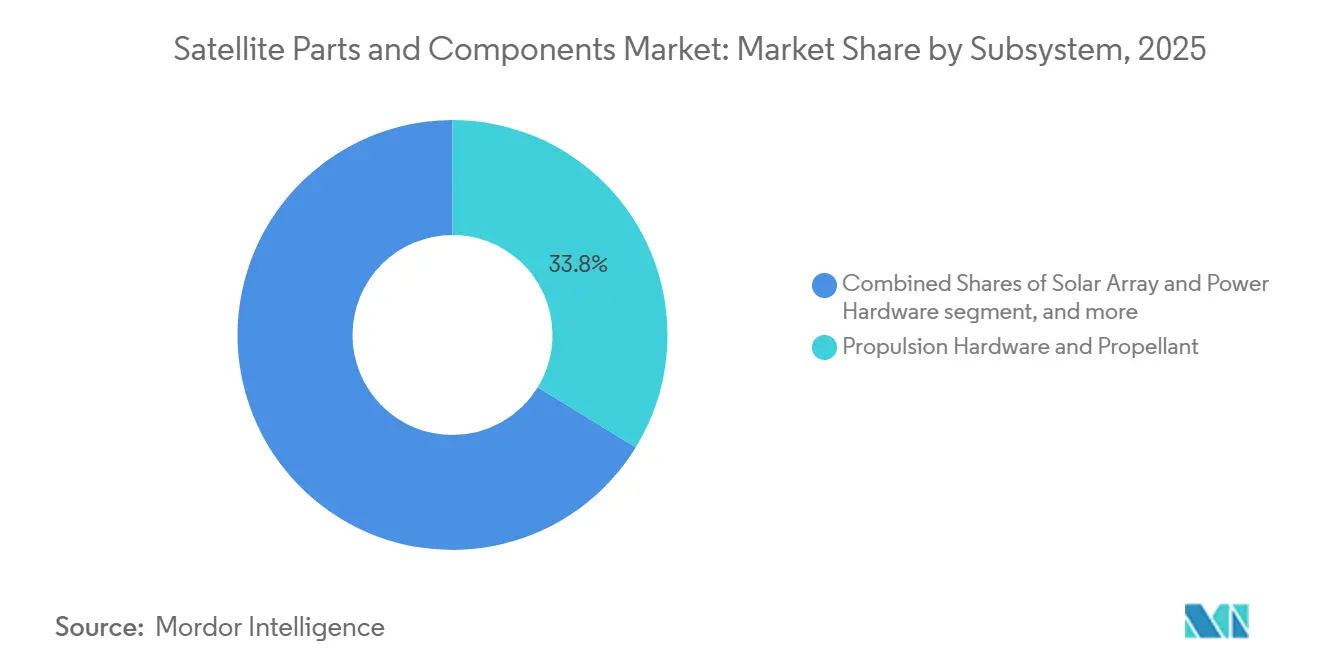

- By subsystem, propulsion hardware and propellant accounted for 33.76% in 2025 and are forecast to grow at a 10.22% CAGR through 2031.

- By component type, hardware dominated in 2025 with an 82.45% share, and software is projected to be the fastest-growing segment, with a 10.47% CAGR through 2031.

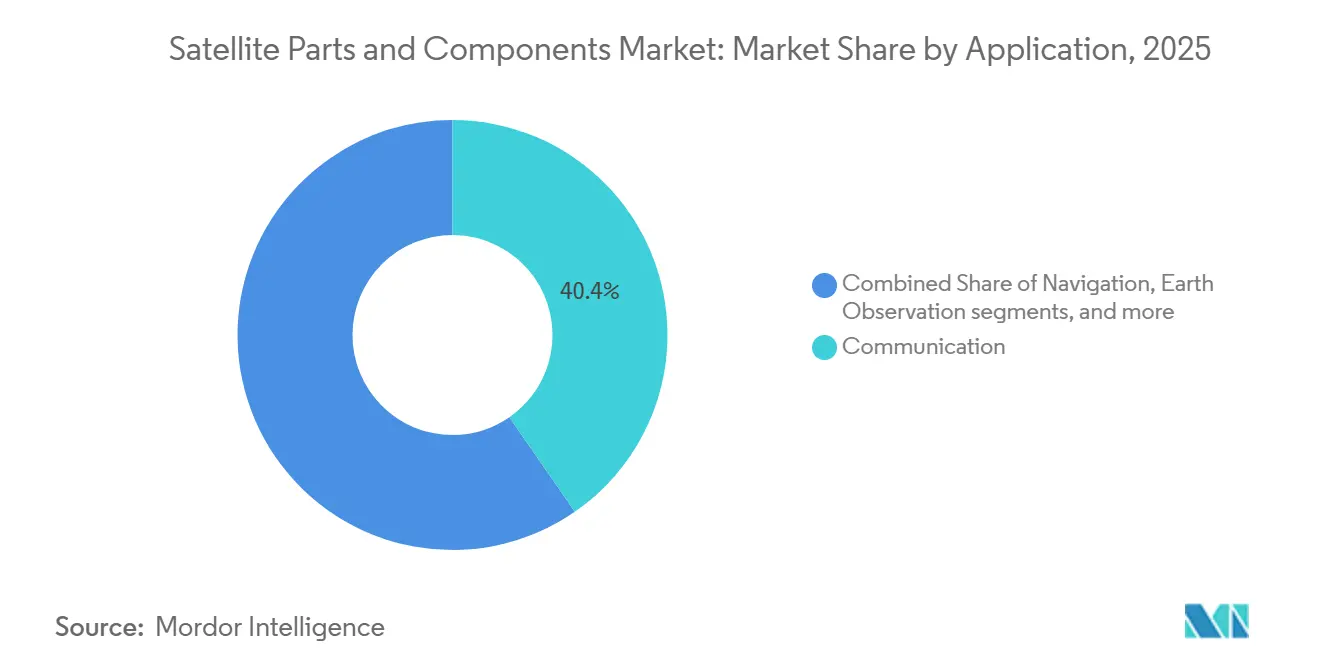

- By application, communication held a 40.37% share in 2025, and space observation is projected to grow with an 11.47% CAGR through 2031.

- By geography, North America led with a 39.54% share in 2025, and Asia-Pacific is forecast to grow at an 11.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Satellite Parts and Components Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid proliferation of LEO broadband constellations | +2.8% | Global, with concentration in US, Europe, China | Medium term (2-4 years) |

| Standardization and mass-manufacture of satellite buses | +1.9% | Global, spill-over from automotive/consumer electronics supply chains | Medium term (2-4 years) |

| Defense adoption of Commercial-Off-The-Shelf (COTS) components | +1.6% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| 3D printing of RF and structural parts | +1.2% | North America and EU, early gains in Bangalore and Singapore | Long term (≥ 4 years) |

| Optical inter-satellite link (OISL) design wins in small sats | +1.4% | Global, led by North America and China | Medium term (2-4 years) |

| Space-sustainability mandates driving demand for de-orbit kits | +0.8% | Global with strongest enforcement in US and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Proliferation of LEO Broadband Constellations

LEO broadband deployments are resetting build cadence and component standardization across the satellite parts and components market. Commercial operators are scaling production lines and embedding higher-throughput crosslinks, which lifts demand for phased arrays, electric propulsion, and radiation-tolerant compute. Amazon’s Project Kuiper reported early service demonstrations in 2026 and confirmed high-volume assembly with optical inter-satellite link capability, a signal that mission-critical components are entering a repeatable manufacturing regime.[1]Project Kuiper Communications, “Project Kuiper Service Launch and Satellite Update,” Amazon, aboutamazon.com Airbus disclosed a EUR 2.2 billion (USD 2.59 billion) award for 440 next-generation satellites that move more signal processing onboard, expanding the addressable market for space-qualified FPGAs and high-throughput digital processors. Regional programs add to the wave, with the G60 plan in Shanghai highlighting mass deployments that amplify demand for standardized buses and propulsion kits. The cumulative effect is a predictable, serial demand profile that enables tiered suppliers to invest in automation and quality systems suitable for aerospace tolerances.

Standardization and Mass-Manufacture of Satellite Buses

Manufacturers are consolidating part counts and tooling with modular bus templates and additive fabrication, compressing integration cycles in the satellite parts and components market. Boeing announced 3D-printed solar array substrates designed to cut composite build time by up to 6 months and reported delivering over 150,000 printed parts across its aerospace portfolio, demonstrating maturation from prototyping to production-grade flight hardware.[2]Investor Relations, “Boeing Sets Rapid Pace with 3D-Printed Solar Array Substrates,” Boeing, investors.boeing.com Japan’s Space Strategy Fund earmarked financing to lift Quality-Cost-Delivery (QCD) across key components such as solar cells, cover glass, and arrays, supporting domestic standardization that meets defense specifications without bespoke rework. As bus platforms converge on common interfaces, suppliers of structures, harnesses, and power modules can scale through flexible, semi-automated flow lines that reduce requalification costs. This pattern mirrors high-volume playbooks in adjacent sectors while maintaining the fundamentals of traceability and reliability for flight systems. Over time, standardization supports interchangeable subsystems, which smooths demand volatility and reduces working capital needs.

Defense Adoption of Commercial-Off-The-Shelf (COTS) Components

Defense procurement has shifted toward proliferated architectures that source from commercial bus and payload lines with targeted mission-specific adaptations. This trend recasts the demand outlook for the satellite parts and components market. The US Space Development Agency awarded USD 3.5 billion in December 2025 to four vendors for 72 Tracking Layer satellites, a deliberate multi-vendor approach that encourages price competition and platform reuse. This procurement philosophy draws in mid-tier and specialist suppliers and tilts component roadmaps toward scalable, repeatable builds with cyber-hardened overlays. NATO’s commercial space priorities have also placed flexibility and rapid contracting at the center of allied efforts, which further supports COTS infusion into secure payloads and ground systems. As a result, avionics, power, propulsion, and optical terminals that meet baseline military survivability are increasingly sourced from commercialized lines, with integration and crypto as the primary differentiators.

3-D Printing of RF and Structural Parts

Additive manufacturing is progressing from a design enabler to a lever for throughput and cost in the satellite parts and components market. Boeing’s production-grade printed substrates for solar arrays and the integration of over 1,000 additively manufactured RF elements per large spacecraft illustrate how lattice structures and consolidated assemblies reduce mass and part counts without compromising performance. NASA programs have validated additive techniques for propulsion components, providing the heritage data needed for more conservative space platforms to move from prototypes to flight units. As design teams exploit topology optimization, printed parts consolidate fasteners, ducts, and thermal pathways, streamlining inspections and reducing assembly labor. The additive value proposition aligns with serial bus production because repeatability and digital thread traceability aid in qualification and lot acceptance. Through the decade, broader use of printed RF hardware, structural panels, and thermal management elements is set to deepen as flight-proven parts accumulate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-rel buy-qualified component shortages and long lead times | -1.9% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Tariff and export-control risk on radiation-hardened semiconductors | -1.3% | Global, bifurcation across US-aligned and China-aligned supply chains | Medium term (2-4 years) |

| Orbital-debris liability raising insurance and design costs | -0.9% | Global with strongest impact on GEO missions | Long term (≥ 4 years) |

| Super-heavy-lift launch delay risk for next-gen large buses | -0.6% | Global, concentrated in US and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High-Rel Buy-Qualified Component Shortages and Long Lead Times

Specialized space-grade electronics and materials continue to face supply constraints, slowing assembly schedules and moderating near-term growth in the satellite parts and components market. Demand for advanced memory, packaging, and radiation-hardened devices competes with adjacent sectors, which limits surge capacity at foundries and module lines. Niche optical terminals, crypto devices, and certain propulsion components rely on a small number of qualified suppliers, so disruptions ripple through integration timelines. Prime contractors have responded by expanding integration and test space, which supports parallel workstreams and higher throughput once components arrive. Ground segment programs also emphasize cloud-native architectures and agile release cycles to keep mission schedules on track while flight hardware backlogs unwind. Over time, further standardization and dual-sourcing strategies are expected to reduce bottlenecks, but the near-term impact remains material for high-reliability builds.

Orbital-Debris Liability Raising Insurance and Design Costs

Growing debris density and stricter compliance regimes increase insurance scrutiny and design requirements, which add cost layers to flight hardware in the satellite parts and components market. Regulators in the US and Europe have cemented five-year deorbit standards for LEO missions, prompting more robust propulsion margins and reliable end-of-life autonomy.[3]Public Notice, “Space Innovation: Updating the FCC’s Space Station Licensing Rules,” Federal Communications Commission, fcc.gov Model-based risk assessments and debris environment statistics published by space agencies are informing operator decisions and underwriter evaluations. Collision-avoidance automation and protected propellant reserves are becoming standard, which increases component counts and integration complexity. As active removal demonstrations proceed under ESA programs, licensing regimes may incorporate such capabilities into large constellation approvals, further supporting demand for specialized mechanisms. These responses increase the burden on quality control and testing for propulsion and structures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Subsystem: Propulsion Thrusters Propel Electric and Chemical Innovation

Propulsion hardware and propellant commanded a 33.76% share in 2025 and are projected to grow at a 10.22% CAGR through 2031, making it the fastest-rising subsystem within the satellite parts and components market. Electric propulsion options such as Hall-effect and ion thrusters are gaining share in LEO constellations where continuous station-keeping and efficient orbital transfers are priorities. The requirement to meet end-of-life disposal timelines continues to nudge designs toward greater propellant reserves and more reliable attitude-control logic. Growth in optical crosslinks and mesh routing drives orbit-raising and phasing needs that align with electric propulsion profiles. Suppliers with combined portfolios in chemical and electric thrusters are focusing on flexible interfaces, enabling bus-level configurability across mission profiles. Integration of propulsion with bus avionics and fault-tolerant power architectures is improving system-level reliability as production runs lengthen and test data accumulates.

The propulsion segment’s trajectory is reinforced by sustainability mandates and proliferated architectures that demand precise end-of-life control. The FCC’s 2024 five-year deorbit standard codified propulsive disposal planning as a non-negotiable baseline for operators, with implications for sizing and redundancy of both chemical and electric thrusters. The satellite parts and components industry is also experimenting with new propellants and feed systems to raise specific impulse without sacrificing manufacturability. As serial production advances, procurement emphasizes components with proven radiation tolerance, long-life cathodes, and consistent qualification test results across lots. Production capacity expansions at leading integrators support parallel lines for different thruster classes, which lowers cycle times once buy-qualified parts are available. Over the forecast horizon, the satellite parts and components market is expected to see propulsion suppliers consolidate around scalable modules that serve both compliance and maneuverability needs.

By Component: Hardware Dominates While Software Surges in Value

Hardware held an 82.45% share in 2025 across RF front ends, power subsystems, bus avionics, propulsion units, sensors, and structures, reflecting the hardware-intensive nature of satellite builds. Software, with a 17.55% share in 2025, is the fastest-growing component, growing at a 10.47% CAGR, driven by the shift to software-defined payloads, in-orbit reconfigurability, and cloud-native ground segments. The satellite parts and components market benefits when software enables beam steering, dynamic bandwidth allocation, and payload flexibility without hardware swaps, thereby raising utilization rates throughout each spacecraft’s life. The move to DevSecOps in ground systems and iterative release cycles helps operators improve resilience and reduce operational overhead. Digital twins and model-based systems engineering are becoming standard in qualification and fault isolation, improving first-pass yield and reducing rework.

Hardware advances continue in arrays, batteries, and structural elements, supported by additive manufacturing and modular designs. Boeing’s work on printed solar array substrates and the broader use of additively manufactured RF components illustrate how design consolidation reduces part counts and lead times for complex assemblies. Power systems and arrays benefit from domestic component development in Japan, which targets radiation resistance and cost reductions aligned with high-volume production. As on-orbit servicing concepts mature, software will extend operational life and capability through updates, lowering lifetime cost per satellite. The satellite parts and components industry will see hardware suppliers forge closer ties with software vendors to enable seamless upgrades and in-orbit optimization. Together, these shifts maintain hardware’s large base while reinforcing software’s double-digit growth trajectory.

By Application: Communication Leads; Space Observation Accelerates

Communication applications accounted for 40.37% in 2025, supported by a mix of GEO broadcast, LEO broadband, and secure SATCOM services for both civil and defense customers. The investment focus is shifting to LEO and MEO constellations that offer lower latency, flexible bandwidth allocation, and resilient routing, thereby increasing demand for phased arrays, optical terminals, and reconfigurable digital payloads. Defense procurement continues to prioritize missile warning and secure transport layers, which sustains orders for bus avionics, crypto, and pointing systems. System integrators are pushing for compatibility with mesh architectures and optical crosslinks to reduce reliance on ground gateways and improve performance in contested environments. As communication architectures standardize, recurring ground upgrades and software-defined payload controls increase end-user flexibility and uptime.

Space observation is the fastest-growing application, with a 11.47% CAGR, as commercial and defense customers demand higher revisit rates, multi-sensor fusion, and real-time analytics. The satellite parts and components market benefits when imaging constellations deploy agile buses with high-precision attitude control, efficient electric propulsion, and robust downlink or crosslink capacity. On-board processing frameworks are reducing the need to downlink raw data by generating derived intelligence on orbit, which raises compute and memory requirements within qualified power envelopes. National programs in Europe continue to expand observation capacity for environmental and security missions, which keeps the component order pipeline steady. As optical and SAR sensors proliferate, suppliers of thermal control, structural, and precision pointing subsystems see consistent demand for stability and vibration isolation. Over the forecast period, observation growth complements communications leadership, broadening the component mix required across constellations.

Geography Analysis

North America led with 39.54% share in 2025, supported by defense and civil space programs that underpin consistent procurement of bus avionics, propulsion, power, and communications payloads. The US Space Development Agency’s Transport and Tracking Layers have awarded multi-vendor tranches for a proliferated LEO architecture, spreading orders across primes and specialist manufacturers while reinforcing serial production behaviors. Prime contractors have expanded integration and test capacity to support larger parallel workstreams, leading to a smoother transition from development to production. Ground segment modernization is integrating cloud-native approaches that enhance command and control for proliferated architectures. The regulatory environment emphasizes orbital debris compliance and technology controls, shaping component specifications and increasing the need for mission assurance in procurement. Suppliers in the region benefit from government-backed programs that maintain cadence across budget cycles.

Asia-Pacific is forecasted to grow fastest at 11.73% CAGR through 2031, propelled by constellation build-outs and government programs that emphasize domestic component capability. China’s large-scale LEO plans and regional manufacturing initiatives have increased the flow of standardized bus and subsystem orders, and public sector programs signal sustained capacity development. Japan’s Space Strategy Fund commits to domestic production of solar cells, cover glass, arrays, and related components, with quality and radiation-resilience targets that align with both commercial and defense missions. Regional launch providers and integrators continue to focus on small- and medium-class satellites that support modular component ecosystems. As supply chains localize, qualification and testing infrastructure within the region will expand, enabling faster time-to-fly for domestic builds. These moves position Asia-Pacific suppliers to compete for global orders as standards converge.

Europe maintains steady demand anchored by climate monitoring, secure communications, and sovereign constellation initiatives that reinforce ongoing investment in bus platforms and payloads. ESA’s Zero Debris Charter and active debris removal programs influence component sizing and end-of-life capabilities, supporting propulsion, guidance, and structural segments. European primes continue to streamline operations and pursue technology upgrades in additive manufacturing, digital payloads, and optical terminals to compete on cost and capability. Secure communications and defense-driven programs expand opportunities for suppliers of crypto, radiation-hardened electronics, and optical crosslinks. Overall, regional policy and agency-backed missions create durable demand for components while standardization pushes efficiency gains across the value chain.

Competitive Landscape

Competition is intensifying as multi-vendor defense awards and proliferated LEO architectures expand opportunities for both primes and specialist manufacturers in the satellite parts and components market. The US Space Development Agency awarded four companies a combined USD 3.5 billion for 72 Tracking Layer satellites in December 2025, reinforcing competitive sourcing for buses, payloads, and supporting components.[4]Newsroom, “Tracking Layer Contracts,” Lockheed Martin, news.lockheedmartin.com Hardware leaders are investing in repeatable integration capacity to meet serial delivery schedules for proliferated constellations. Ground system providers are moving to cloud-native architectures that scale with constellation sizes and enable faster updates. Together, these advances intensify competition on price, delivery speed, and reliability.

Prime contractors and specialized suppliers are also deploying additive manufacturing and modular designs to reduce lead times and validate flight units more quickly. Boeing’s 3D-printed solar array substrates and its broader adoption of printed RF components show how consolidated assemblies reduce part counts and tooling complexity in high-mix, low-volume production. Companies with software-defined payload capabilities are winning opportunities that rely on dynamic beamforming and in-orbit reconfiguration, elevating the roles of high-throughput compute and secure software stacks. Power and propulsion specialists continue to scale production of electric and chemical thrusters to meet deorbit mandates and maneuverability needs across constellations. Component suppliers who pair hardware innovations with software and testing infrastructure gain an edge in qualification and delivery cadence.

Corporate actions are reshaping competitive positioning as companies aim to focus on core aerospace and defense categories. Honeywell’s planned aerospace technologies spin-off by Q3 2026 highlights a portfolio simplification strategy aligned to growth in defense and space demand. Redwire is expanding into docking systems and other mission-critical mechanisms through new program wins, widening participation in human and cargo space station applications. European suppliers continue to support climate and security missions through sustained deliveries of observation satellites, which sustain demand for imaging payloads, thermal control, and structural components. The satellite parts and components market will continue to reward players that scale reliably and align roadmaps with proliferated architectures, orbital debris mitigation, and optical networking.

Satellite Parts and Components Industry Leaders

Lockheed Martin Corporation

Northrop Grumman Corporation

The Boeing Company

Airbus SE

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The US Space Force's Space Systems Command (SSC) awarded a USD 90 million contract to Rocket Lab Corporation to design, manufacture, integrate, and operate two geostationary (GEO) satellites hosting the Heimdall space domain awareness payload.

- December 2025: L3Harris Technologies, Inc. received a contract from the Space Development Agency (SDA) to manufacture 18 infrared satellites for the Tranche 3 Tracking Layer. The contract, valued at up to USD 843 million, encompasses ground software, operations, and sustainment functions.

- February 2025: Thales Alenia Space, a joint venture between Thales (67%) and Leonardo (33%), signed a contract with NIBE Space, a subsidiary of NIBE Limited, to supply a high-resolution optical satellite. This agreement marks the initial phase of NIBE's Earth Observation constellation project and aims to establish its first operational Earth observation capabilities in India.

Global Satellite Parts and Components Market Report Scope

Satellite parts and components comprise subsystems and specialized elements that constitute the spacecraft's bus and payload, enabling its operation in space. Major systems include solar arrays and power hardware, structures, harnesses, mechanisms, and other hardware and software systems.

The satellite parts and components market is segmented by subsystem, component, application, and geography. By subsystem, the market is segmented into solar arrays and power hardware; structures, harnesses, and mechanisms; propulsion hardware and propellant; and satellite bus and subsystems. By component, the market is divided into hardware and software. By application, the market is segmented into communication, navigation, earth observation, space observation, and others. The report also covers the market sizes and forecasts for the satellite parts and components market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Solar Array and Power Hardware |

| Structures, Harness and Mechanisms |

| Propulsion Hardware and Propellant |

| Satellite Bus and Subsystems |

| Hardware |

| Software |

| Communication |

| Navigation |

| Earth Observation |

| Space Observation |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Israel |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Subsystem | Solar Array and Power Hardware | ||

| Structures, Harness and Mechanisms | |||

| Propulsion Hardware and Propellant | |||

| Satellite Bus and Subsystems | |||

| By Component | Hardware | ||

| Software | |||

| By Application | Communication | ||

| Navigation | |||

| Earth Observation | |||

| Space Observation | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Israel | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.