Printed Electronics In Healthcare Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

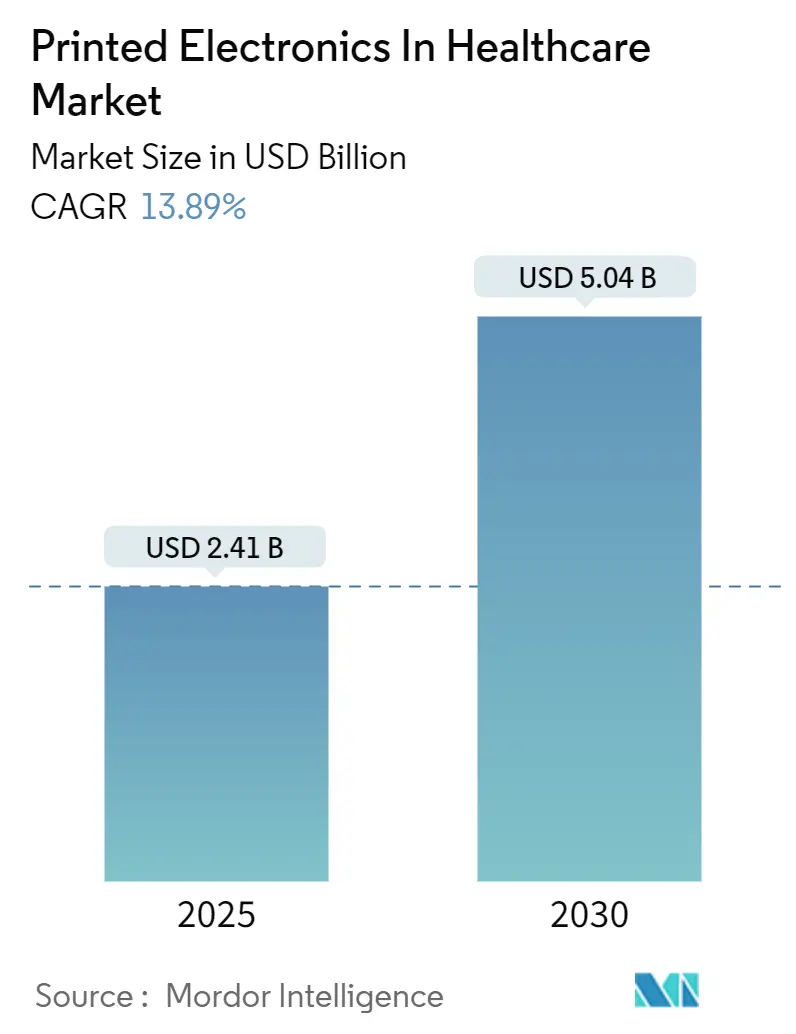

| Market Size (2025) | USD 2.41 Billion |

| Market Size (2030) | USD 5.04 Billion |

| Growth Rate (2025 - 2030) | 13.89% CAGR |

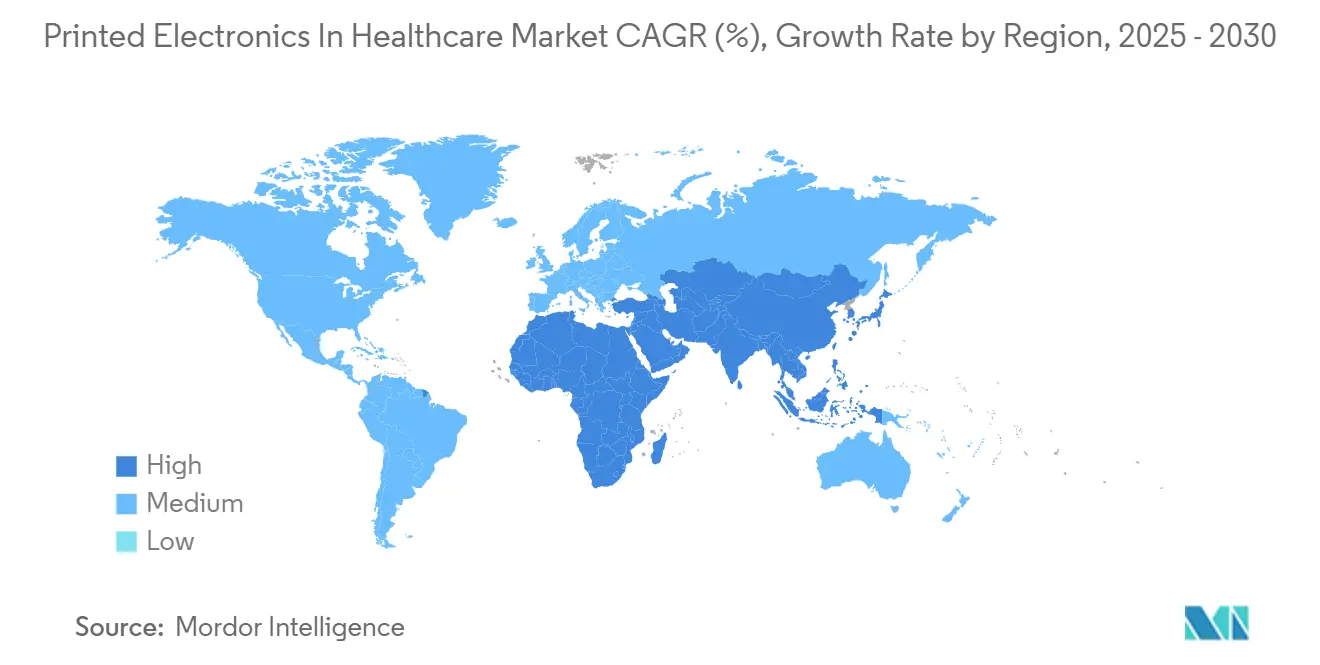

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

.webp)

Printed Electronics In Healthcare Market Analysis by Mordor Intelligence

The printed electronics market in healthcare is currently valued at USD 2.41 billion and is forecast to achieve USD 5.04 billion by 2030, reflecting a 13.89% CAGR. This vigorous expansion stems from the technology’s ability to deliver flexible, lightweight, and disposable medical devices at unit costs traditional silicon manufacturing cannot match.[1]PMC, “Biomedical Skin Patches with Microfluidic-Regulated 3D Bioprinting for Advanced Healthcare Applications,” pmc.ncbi.nlm.nih.gov Strong demand for remote patient-monitoring wearables, growth in smart pharmaceutical packaging, and rapid innovation in biocompatible conductive inks anchor near-term growth. North America’s early regulatory clarity and generous NIH grants accelerate commercialization pipelines, while Asia-Pacific’s push for point-of-care diagnostics widens the customer base. Meanwhile, breakthroughs in self-healing conductors and stretchable substrates promise fresh revenue streams as clinical adoption hurdles are cleared.

Key Report Takeaways

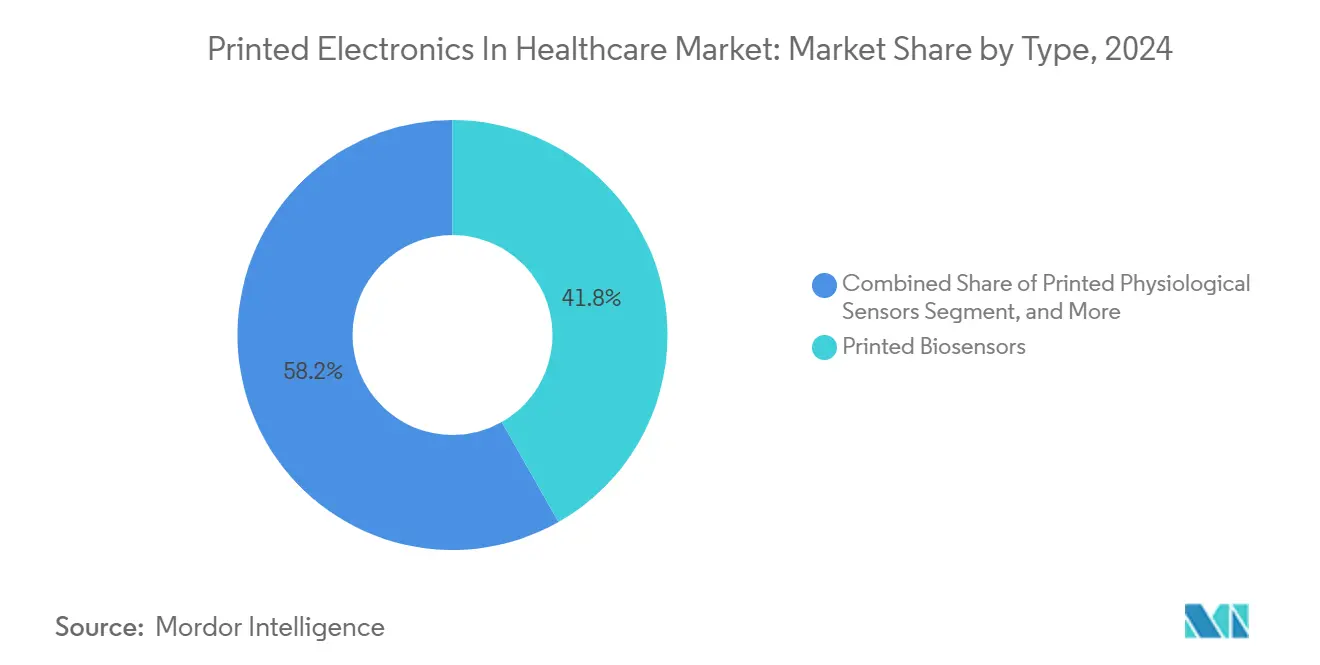

- By type, printed biosensors led with 41.8% of printed electronics market share in 2024; stretchable and flexible hybrid electronics is forecast to expand at 16.3% CAGR to 2030.

- By printing technology, screen printing commanded 52.9% share of the printed electronics market size in 2024; aerosol jet and 3D printing is advancing at a 14.7% CAGR through 2030.

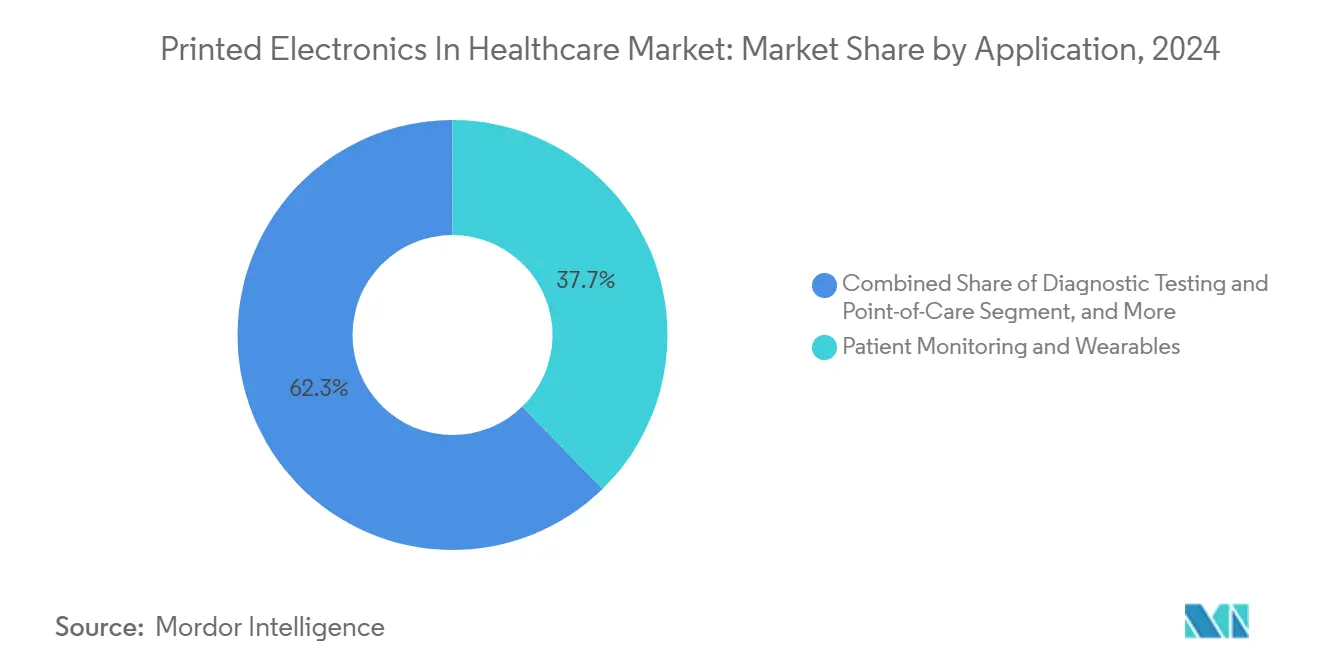

- By application, patient monitoring and wearables accounted for 37.7% share of the printed electronics market size in 2024; pharmaceutical packaging and anti-counterfeit solutions are projected to grow at 15.6% CAGR to 2030.

- By end-user, hospitals and clinics held 33.8% of printed electronics market share in 2024; home healthcare providers record the highest projected CAGR at 14.3% between 2025-2030.

- By geography, North America dominated with 40.8% revenue share in 2024; the Middle East and Africa region is set to rise at a 15.4% CAGR through 2030.

Global Printed Electronics In Healthcare Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid uptake of remote patient-monitoring wearable patches in United States homecare | +2.8% | North America, spillover to EU | Medium term (2-4 years) |

| EU Falsified Medicines Directive catalyzing smart pharma-packaging with printed RFID | +2.1% | Europe, adoption in APAC | Short term (≤2 years) |

| Surge in point-of-care disposable biosensors for infectious disease detection in Asia | +1.9% | APAC core, expanding to MEA | Medium term (2-4 years) |

| Chronic-disease burden driving demand for flexible printed electrodes in cardiology | +1.6% | Global | Long term (≥4 years) |

| Cold-chain integrity needs boosting printed temperature sensors for vaccines | +1.4% | Global, focus on emerging markets | Short term (≤2 years) |

| NIH and EU Horizon grants funding bio-compatible conductive-ink R&D | +1.2% | North America and EU | Long term (≥4 years) |

Source: Mordor Intelligence

Rapid Uptake of Remote Patient-Monitoring Wearable Patches in United States Homecare

Medicare’s broader reimbursement for telehealth, coupled with FDA clearance of skin-friendly glucose and cardiac patches, fuels wide deployment of printed sensors in the home-care channel. Hybrid microfluidic-regulated patches now capture multi-parameter vitals, handing care teams granular longitudinal data without clinic visits. U.S. systems report fewer readmissions and higher patient satisfaction, confirming tangible cost savings. Device makers scaling in this environment set a compelling precedent for EU and APAC health systems as they evaluate reimbursement frameworks.

EU Falsified Medicines Directive Catalyzing Smart Pharma-Packaging with Printed RFID

Full serialization under the EU Falsified Medicines Directive forces pharmaceutical producers to embed authentication features on every retail pack. Printed RFID and NFC tags, fabricated on high-speed flexographic lines, now satisfy both traceability and tamper evidence at unit cost levels acceptable to generic and branded manufacturers. Global drug firms adopting EU-compliant packaging extend the same solutions to APAC logistics hubs, creating a multiplier effect on demand for conductive inks optimized for paper and foil substrates.

Surge in Point-of-Care Disposable Biosensors for Infectious Disease Detection in Asia

Asia-Pacific governments are upgrading frontline diagnostic capacity to mitigate future outbreaks. Screen-printed lateral flow assays incorporating nanomaterial optical sensors deliver rapid antigen reads inside 15 minutes, eliminating central-lab bottlenecks.[2]MDPI, “Lateral Flow Assays for Viral Protein Detection with Nanomaterial-Based Optical Sensors,” mdpi.com Smartphone-linked readers layer AI analytics on top of raw signals, giving clinicians near-real-time epidemiological visibility. The scalable cost profile of printed test strips positions the technology as a mainstay in rural health deployments across India, Indonesia, and the Philippines.

Cold-Chain Integrity Needs Boosting Printed Temperature Sensors for Vaccines

Complex mRNA vaccine logistics spotlight gaps in end-to-end temperature control. Printed temperature-threshold indicators embedded on secondary packaging provide an unbroken thermal record at vial level, supporting pharmacovigilance audits and reducing spoilage. Fast-curing silver-polymer inks keep unit costs low enough for global health agencies scaling multi-million dose campaigns.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDA and EMA validation cycles delaying commercial roll-outs | -2.40% | North America & EU | Short term (≤ 2 years) |

| Heightened cybersecurity requirements for connected devices | -1.50% | North America & EU | Short term (≤ 2 years) |

| Sterilization compatibility issues of polymer substrates | -1.00% | Global | Medium term (2-4 years) |

| Biocompatibility risks & humidity-driven sensor degradation | -0.80% | Global | Medium term (2-4 years) |

Source: Mordor Intelligence

FDA and EMA Validation Cycles Delaying Commercial Roll-outs

Actual 510(k) reviews often stretch to 6-7 months, well beyond nominal timelines, as examiners request extra bench and clinical data on novel substrates.[3]Hardian Health, “How Long Does an FDA 510(k) Submission Actually Take?” hardianhealth.com De novo classifications lengthen approvals further, and the new European MDR imposes additional clinical performance studies, forcing dual submission tracks. Rising cybersecurity and AI documentation requirements add layers of testing cost, prompting some mid-cap firms to defer U.S. launches in favor of pilot deployments in MEA or South America.

Sterilization and Biocompatibility Challenges of Polymer Substrates

Ethylene-oxide and gamma sterilization can embrittle common medical-grade polymers, reducing sensor lifespan in ICU use cases. Alternative ozone cycles show promise yet require device-specific validation.[4]MDPI, “The Effects of Ozone Sterilization on the Chemical and Mechanical Properties of 3D-Printed Biocompatible PMMA,” mdpi.com Moisture-driven drift remains a key failure mode for tropical deployments, while antimicrobial additives complicate cytotoxicity profiles in chronic-wear devices. Progress in self-healing elastomers eases some concerns, but comprehensive ISO 10993 testing schedules still add six-plus months to many programs.

Segment Analysis

By Type: Biosensors Lead Innovation Wave

Printed biosensors held 41.8% of the printed electronics market in 2024. Glucose strips and continuous glucose monitors dominate the installed base, buoyed by over-the-counter U.S. approvals that destigmatize routine monitoring. Infectious disease assays remain a growth engine in APAC public-health tenders, while emerging pH and wound-monitor patches broaden clinical reach.

Stretchable and flexible hybrid electronics is projected to post a 16.3% CAGR, the fastest among types. Self-healing conductive meshes now survive repeated strain cycles without delamination, allowing week-long cardiac or neuro monitoring. Printed RFID labels for pharma packs add a second demand pillar, especially as global serialization mandates mature

Note: Segment shares of all individual segments available upon report purchase

By Printing Technology: Screen Printing Dominance Faces Innovation Pressure

Screen printing captured 52.9% of the printed electronics market in 2024 thanks to proven throughput and low per-unit costs for disposable electrodes. Mature process controls ease FDA filing, making it the default for high-volume biosensors.

Aerosol jet and 3D methods are growing at a 14.7% CAGR. Their ability to deposit conductive tracks inside 3D microfluidic channels has cut prototyping times from days to minutes. Early adopters in Switzerland and Singapore have demonstrated sub-100 µm channel fidelity at pilot scale, enabling rapid design iteration for lab-on-chip diagnostics.

By Application: Patient Monitoring Leads Market Transformation

Patient monitoring and wearables contributed 37.7% of printed electronics market revenue in 2024. Smart patches aggregating ECG, SpO₂, and temperature sensors send continuous streams to cloud dashboards, underpinning hospital-at-home models. Insurance payers cite lower acute care costs and higher adherence.

Pharmaceutical packaging and anti-counterfeit solutions will expand at 15.6% CAGR, the highest among applications. Digital display labels powered by printed batteries enable dynamic dosing instructions in clinical trials, while temperature-sensitive pigment layers verify cold-chain integrity in vaccine shipments. Combined, these features create a robust compliance toolkit for regulators and brand owners alike.

By End-user: Healthcare Providers Drive Adoption

Hospitals and clinics represented 33.8% of printed electronics market revenue in 2024, reflecting institutional buying power and preference for FDA-cleared devices. Bulk contracts for disposable ECG electrodes and wound sensors anchor this channel, with average contract cycles of three years.

Home healthcare services are set to grow 14.3% annually through 2030. Reimbursement expansions have lowered barriers for remote monitoring kits shipped directly to patients, often bundled as subscription platforms. Diagnostic labs and pharma firms form secondary demand pools for serialized packaging and point-of-care equipment, while universities supply a steady pipeline of patented IP.

Geography Analysis

North America posted 40.8% of global revenue in 2024, benefiting from FDA’s early digital-health frameworks and NIH funding streams that de-risk material R&D. Multicenter trials at Mayo Clinic and Cleveland Clinic validate remote monitoring endpoints, smoothing procurement approvals for regional hospital networks. Canadian research clusters in Ontario add specialized substrate expertise, further bolstering continental leadership.

Europe remains a strategic stronghold. The region’s pharmaceutical giants must comply with the Falsified Medicines Directive, locking in sustained demand for serialized smart tags. Germany’s precision-machinery heritage supports high-volume printing presses, while the United Kingdom channels venture funding into flexible IC startups. Public health authorities in France and Nordic nations augment uptake through preventive-care reimbursement for remote sensors.

The Middle East and Africa is forecast to deliver a 15.4% CAGR, the fastest worldwide. National health expansions in Saudi Arabia and the United Arab Emirates allocate budget lines for connected diagnostics, seeing printed electronics as a quick path to rural coverage without heavy infrastructure. South Africa’s regulatory agency aligns its device code to FDA classification, accelerating import approvals. This momentum signals a step-change in the region’s medical technology self-sufficiency.

Competitive Landscape

The printed electronics market in healthcare is moderately fragmented. Materials suppliers such as DuPont secure upstream control by acquiring molding specialists like Donatelle Plastics to integrate circuit substrates with medical housings. Device stalwarts including Abbott leverage large installed bases in diabetes care to cross-sell next-gen printed patches.

Startups chase white-space opportunities. Pragmatic Semiconductor’s USD 125 million Series C bankrolls low-cost flexible ICs for smart blister packs. Neuranics uses new magnetoresistive sensors to pursue neurologic monitoring niches. In orthopedics, Zimmer Biomet’s acquisition spree embeds sensors in revision implants, linking physical prosthetics with cloud analytics.

Strategic collaborations flourish. Imec and MIT co-develop miniaturized power management modules to shrink wearable form factors. Flex expands Dallas capacity to house quick-turn medical PCB lines, merging AI edge hardware with printed sensor arrays. Overall, firms combining materials IP, high-volume print know-how, and regulatory fluency command clear advantage.

Printed Electronics In Healthcare Industry Leaders

-

Jabil Inc.

-

Bebop Sensors Inc.

-

Sensing Tex S.L

-

E Ink Holdings Inc.

-

Flex Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Imec partnered with MIT’s Research Laboratory of Electronics to accelerate personalized healthcare through advanced printed electronics technologies.

- April 2025: Zimmer Biomet completed acquisition of Paragon 28, boosting foot-and-ankle offerings with smart implant features that rely on printed electronics.

- April 2025: Neuranics secured USD 8 million to advance TMR magnetic sensing technology for medical devices.

- March 2025: DuPont announced leadership for its upcoming electronics spin-off “Qnity,” targeting healthcare substrates and inks.

- March 2025: Zimmer Biomet received FDA clearance for registered Persona Revision trademarked SoluTion Femur knee implant with integrated printed electronics capabilities

- February 2025: Flex opened a 400,000 sq ft Dallas facility to boost AI-ready power systems production that incorporates printed components for medical clients.

Global Printed Electronics In Healthcare Market Report Scope

Printed electronics are electronic components/devices that can be manufactured through precision printing. Flexible circuits are printed on films and pliable materials for various healthcare industry applications using advanced printing techniques such as screen printing, flexography, offset lithography, gravure, and inkjet.

The printed electronics market in the healthcare industry is segmented by type (printed sensors, stretchable electronics, and printed RFID) and geography (North America, Europe, Asia-Pacific, and the Rest of the World). The study also provides a detailed analysis of the impact of COVID-19 on the market.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| By Type | Printed Biosensors | Glucose Sensors | ||

| Infectious-Disease Test Strips | ||||

| Other Biosensors | ||||

| Printed Physiological Sensors | ECG/EEG Electrodes | |||

| Temperature/pH Patches | ||||

| Printed RFID/NFC Labels | ||||

| Stretchable and Flexible Hybrid Electronics | ||||

| Printed Microfluidics | ||||

| Other Printed Components (Antennas, Heaters) | ||||

| By Printing Technology | Screen Printing | |||

| Inkjet Printing | ||||

| Gravure/Flexography | ||||

| Aerosol Jet and 3D Printing | ||||

| By Application | Patient Monitoring and Wearables | |||

| Diagnostic Testing and Point-of-Care | ||||

| Drug Delivery and Smart Patches | ||||

| Pharmaceutical Packaging and Anti-Counterfeit | ||||

| Medical Imaging and Therapeutic Devices | ||||

| Others | ||||

| By End-user | Hospitals and Clinics | |||

| Home Healthcare Providers | ||||

| Pharmaceutical and Biotech Companies | ||||

| Diagnostic Laboratories | ||||

| Academic and Research Institutes | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Nordics | ||||

| Rest of Europe | ||||

| South America | Brazil | |||

| Rest of South America | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South-East Asia | ||||

| Rest of Asia-Pacific | ||||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | ||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Rest of Africa | ||||

| Printed Biosensors | Glucose Sensors |

| Infectious-Disease Test Strips | |

| Other Biosensors | |

| Printed Physiological Sensors | ECG/EEG Electrodes |

| Temperature/pH Patches | |

| Printed RFID/NFC Labels | |

| Stretchable and Flexible Hybrid Electronics | |

| Printed Microfluidics | |

| Other Printed Components (Antennas, Heaters) |

| Screen Printing |

| Inkjet Printing |

| Gravure/Flexography |

| Aerosol Jet and 3D Printing |

| Patient Monitoring and Wearables |

| Diagnostic Testing and Point-of-Care |

| Drug Delivery and Smart Patches |

| Pharmaceutical Packaging and Anti-Counterfeit |

| Medical Imaging and Therapeutic Devices |

| Others |

| Hospitals and Clinics |

| Home Healthcare Providers |

| Pharmaceutical and Biotech Companies |

| Diagnostic Laboratories |

| Academic and Research Institutes |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the printed electronics market in healthcare?

The printed electronics market size stands at USD 2.41 billion in 2025 and is projected to reach USD 5.04 billion by 2030.

Which application area generates the most revenue today?

Patient monitoring and wearables accounted for 37.7% of global revenue in 2024, reflecting strong demand for remote care technologies.

Which region is expanding the fastest?

The Middle East and Africa region is forecast to grow at a 15.4% CAGR through 2030, driven by healthcare infrastructure investments and mobile diagnostics.

Why is screen printing still dominant in production?

Screen printing holds 52.9% market share because it offers proven scalability and regulatory familiarity, which keeps per-unit costs low for disposable sensors.

What is the main regulatory hurdle for new devices?

Lengthy FDA and EMA validation cycles, often extending beyond six months, delay the commercial roll-out of novel printed electronics.

Which segment shows the highest future growth potential?

Stretchable and flexible hybrid electronics is poised to expand at a 16.3% CAGR as self-healing materials enable next-generation wearable and implantable devices.

Page last updated on: July 7, 2025