Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.48 Billion |

| Market Size (2026) | USD 1.65 Billion |

| Market Size (2031) | USD 2.69 Billion |

| Growth Rate (2026 - 2031) | 10.25% CAGR |

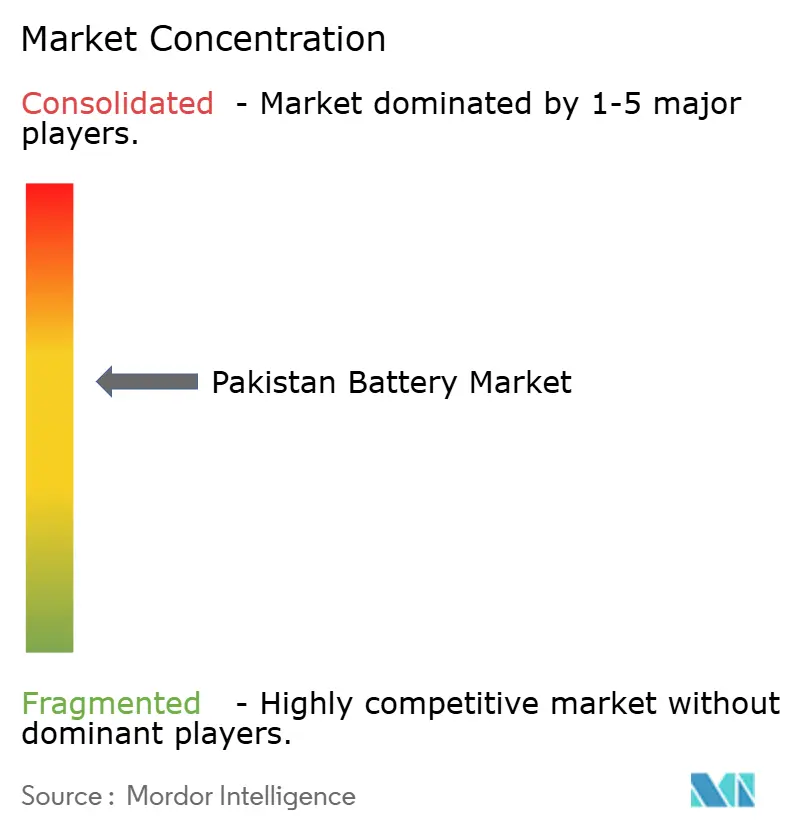

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Battery Market Analysis by Mordor Intelligence

The Pakistan Battery Market size is expected to grow from USD 1.48 billion in 2025 to USD 1.65 billion in 2026 and is forecast to reach USD 2.69 billion by 2031 at 10.25% CAGR over 2026-2031.

Rooftop solar capacity quadrupled ahead of the National Electric Power Regulatory Authority’s (NEPRA) February 2026 shift from net metering to net billing, triggering a surge in behind-the-meter storage demand.[1]National Electric Power Regulatory Authority, “Net Billing Regulations,” nepra.org.pk Simultaneously, the National EV Policy targets 30% electric-vehicle penetration by 2030 through cash incentives that are already stimulating lithium-ion uptake across two- and three-wheeler fleets.[2]Ministry of Industries & Production, “National EV Policy 2025-2030,” moip.gov.pk Data-center and telecom operators are moving from valve-regulated lead-acid units toward long-life lithium-ion UPS systems to curb diesel reliance and comply with carbon mandates.[3]Pakistan Telecommunication Authority, “Annual Report 2024,” pta.gov.pk At the other end of the scale, utility-scale battery energy storage remains constrained by circular-debt-driven payment delays that raise project-finance risk premiums.

Key Report Takeaways

- By type, secondary batteries held 87.0% of the Pakistan battery market share in 2025, and the same is projected to grow at 10.9% through 2031.

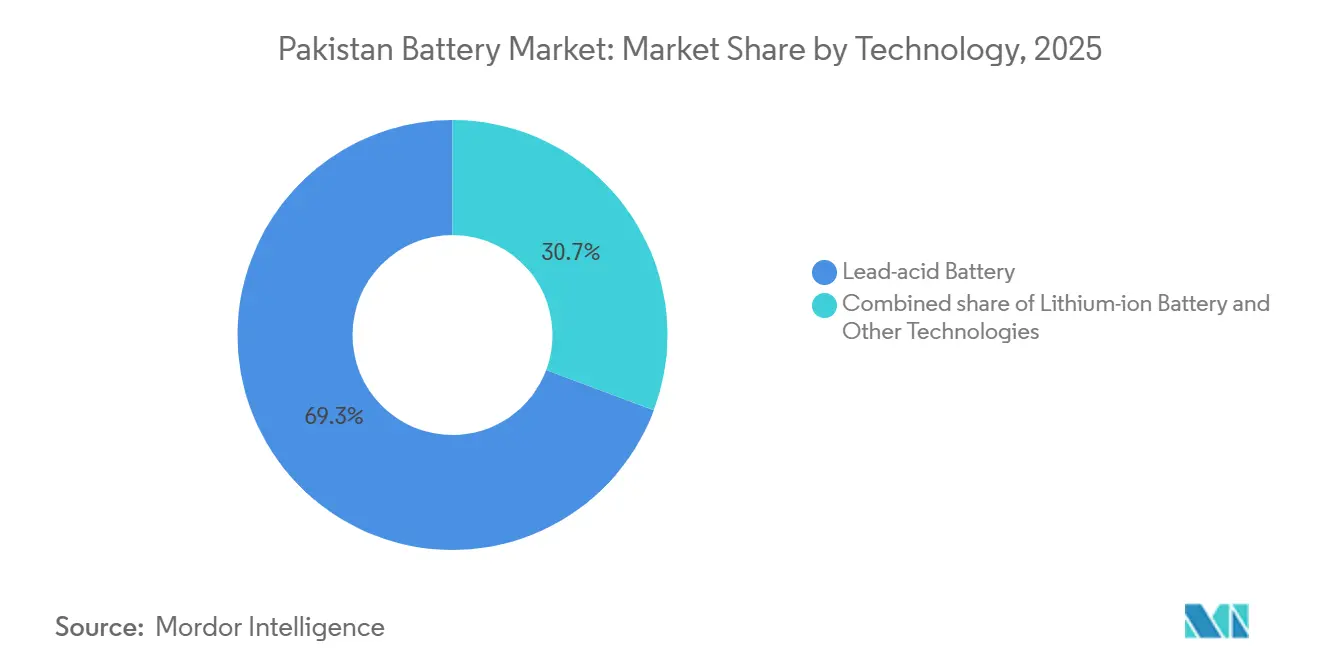

- By technology, the lead-acid battery segment accounted for 69.3% of the market, while the lithium-ion segment is projected to register a 14.0% CAGR through 2031.

- By form factor, cylindrical cells held 62.8% of the Pakistan battery market share in 2025, while pouch cells are projected to expand at a 15.1% CAGR to 2031.

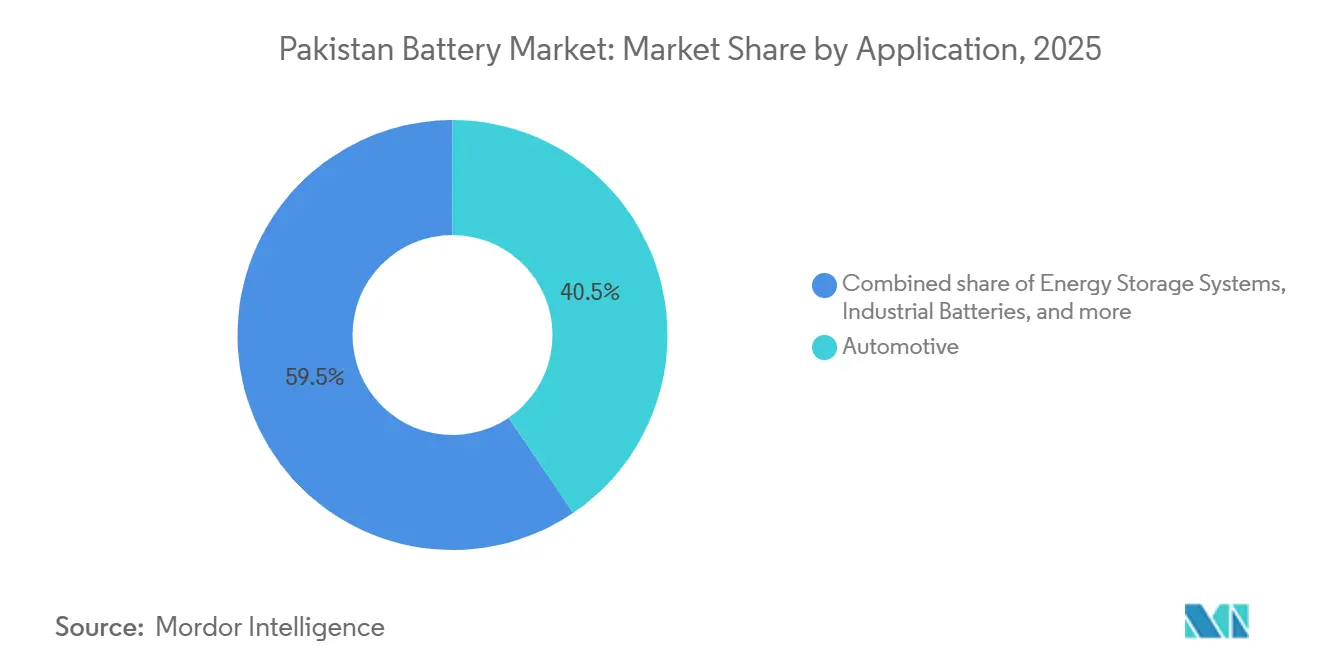

- By application, automotive accounted for 40.5% of the Pakistan battery market size in 2025 and is expected to advance at a 12.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Pakistan Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of rooftop solar-storage systems | +2.8% | Punjab & Sindh urban centers | Medium term (2-4 years) |

| National EV Policy (30% EV sales target) | +2.1% | Nationwide, led by Karachi-Lahore-Islamabad | Long term (≥ 4 years) |

| Data-center & telecom backup demand surge | +1.5% | Metro hubs | Short term (≤ 2 years) |

| Declining battery prices & local manufacturing push | +1.3% | Karachi & Lahore clusters | Medium term (2-4 years) |

| Night-time surplus power spurring utility-scale BESS | +0.9% | Grid-connected sites | Long term (≥ 4 years) |

| Duty-free raw-material incentive | +0.7% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Rooftop Solar-Storage Systems

NEPRA’s move to net billing cut sell-back tariffs by roughly 40%, so households now store daytime generation for evening use, reducing payback periods to 3-5 years despite a 48% surcharge on net-billed units.[4]National Electric Power Regulatory Authority, “Net Billing Regulations,” nepra.org.pk Distributed solar has reached a cumulative 17 GW, and battery imports are forecast to climb from 1.25 GWh in 2024 to 8.75 GWh by 2030. Lithium iron phosphate packs dominate because they tolerate Pakistan’s high ambient temperatures and deliver 6,000-plus cycles. Local vendors now offer modular systems scaling beyond 80 kWh, a configuration popular with textile mills hedging peak-tariff exposure. The same dynamic is encouraging small commercial sites in Faisalabad and Sialkot to deploy 100-500 kWh systems.

National EV Policy (30% EV Sales Target by 2030)

The policy earmarks Rs 9 billion in FY 2025-26 subsidies, PKR 50,000 per e-bike and PKR 200,000 per e-rickshaw, while imposing a 1-3% levy on internal-combustion sales to fund incentives. Fifty-six electric two-wheelers and nine three-wheelers have secured type approval, but assembly lines operate below capacity, signaling latent demand. BYD Pakistan expects EV sales to triple as its Karachi plant rolls out 25,000 units annually from mid-2026. Parallel motorway charging projects aim to ease range anxiety, though price premiums still limit passenger-car conversion. Local component sourcing requirements baked into the subsidy scheme are steering battery makers toward cell production rather than mere pack assembly.

Data-Center & Telecom Backup Demand Surge

Nationwide 5G rollout and hyperscale data-center projects raise the reliability bar. Tower counts exceed 70,000, and diesel costs have doubled since 2023, tilting the economics toward lithium-ion systems that cut total cost of ownership by up to 30% over a decade. UPS specifications now call for sub-10-millisecond switchover and N+1 modularity. Falling pack prices, USD 100 per kWh in 2025 compared with USD 140 in 2023, have narrowed the gap with VRLA to 1.5×, quickening adoption.

Declining Battery Prices & Local Manufacturing Push

January 2026 policy reforms provide duty-free raw-material quotas and have unlocked USD 558 million in Chinese investment commitments. Atom Power and HUBCO target vertical integration to cut landed costs 15-20% by localizing cathode processing and refining. Duty on imported finished packs remains 10%, creating a protective delta that incentivizes semi-knocked-down kit importation while domestic cell lines ramp up. Electricity rates, at PKR 16-20 per kWh for industry, still erode margin, so energy-efficiency retrofits form part of every new plant’s capital plan.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency volatility inflating imported components | -1.4% | Nationwide importers | Short term (≤ 2 years) |

| Weak recycling ecosystem & e-waste concerns | -0.8% | National, informal sector | Medium term (2-4 years) |

| Circular-debt delays in power-sector payments | -1.1% | National utility projects | Medium term (2-4 years) |

| Graphite supply-chain geopolitical risk | -0.6% | Import dependent | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility Inflating Imported Components

The rupee swung 3% against the USD during 2024, amplifying raw-material cost swings by up to 20% for lithium, cobalt, and separator film. Import-compression measures under the IMF program lengthened shipment lead times to six weeks, forcing assemblers to double safety stocks and absorb higher working-capital charges. A new customs valuation floor has closed avenues for creative invoicing, lifting effective landed costs 8-12% for aftermarket distributors.

Weak Recycling Ecosystem & E-Waste Concerns

Informal operators process around 90% of end-of-life batteries using rudimentary methods that leak lead and acid into the environment. Formal capacity is limited to two lead-acid smelters; there is still no lithium-ion recycler on Pakistani soil. Extended Producer Responsibility rules require 70% recovery by 2027, yet enforcement gaps persist, and valuable cobalt, nickel, and lithium worth USD 15-20 million a year are lost to landfill.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Secondary Batteries Anchor Rechargeable Demand

Secondary batteries dominated the Pakistan battery market with an 87.0% share in 2025 and are projected to expand at a 10.9% CAGR to 2031, driven by automotive SLI replacements, UPS systems, and a budding EV fleet. Lead-acid technology maintains cost leadership, particularly in regions where peak summer temperatures exceed 45 °C, while lithium-ion captures premium niches such as rooftop solar storage and telecom towers. Exide Pakistan and Atlas Battery jointly hold roughly 35% of this segment and continue to invest in local separator and grid-casting capacity to buffer currency volatility.

Lithium-ion penetration is accelerating as subsidies narrow the price gap and as local assemblers gain a 15-18% landed-cost advantage under the FY 2025 tariff schedule. Primary cells, serving low-drain devices, captured 13.0% share in 2025 and face a modest 6.2% CAGR; stringent EPR mandates may consolidate this sub-segment around multinationals able to finance compliant collection networks.

By Technology: Lithium-Ion Gains Despite Lead-Acid Incumbency

Lead-acid batteries held 69.3% of the Pakistan battery market share in 2025, thanks to a mature recycling loop that recovers up to 90% of lead content. However, lithium-ion is forecast to post a 14.0% CAGR on the back of EV incentives, telecom modernization, and rooftop-solar coupling. Sodium-ion and nickel-metal-hydride together comprise less than 5% and remain commercially marginal.

The Pakistan battery market size for lithium-ion packs used in two-wheelers is expected to reach USD 410 million by 2031, reflecting falling cathode costs and imported cell prices that have already dropped to USD 100 per kWh. Domestic cell projects announced by Atom Power and HUBCO could trim a further 10% off system costs once graphite and electrolyte processing localizes.

By Form Factor: Pouch Cells Surge in Consumer Electronics

Cylindrical formats constituted 62.8% of 2025 revenue, underpinned by 18650 and 21700 cells embedded in power tools and laptops. The Pakistan battery market size for pouch-cell configurations is projected to jump from USD 280 million in 2026 to USD 670 million in 2031, reflecting a 15.1% CAGR tied to smartphone, drone, and wearable form-factor requirements. Prismatic cells retain automotive relevance, especially in BYD’s Blade Battery packs now being localized in Karachi.

Manufacturers face a trade-off: cylindrical lines offer mature automation and yield reliability, while pouch cells deliver superior volumetric energy density but demand tighter humidity control during assembly. The National Lithium-Ion Battery Manufacturing Policy purposefully leaves form-factor choice to industry, but local incentives tilt in favor of configurations that maximize domestic content value.

By Application: Automotive Segment Leads EV Transition

Automotive uses absorbed 40.5% of 2025 revenue and are forecast to grow at a 12.5% CAGR on subsidy-supported two-wheelers and ride-hailing fleets. The Pakistan battery market size for automotive is set to exceed USD 1.3 billion by 2031. OEMs have begun passing the Energy Vehicle Adoption Levy onto ICE buyers, nudging price-sensitive consumers toward entry-level e-bikes priced below PKR 250,000.

Energy storage systems represent roughly a quarter of industry value and will expand at 11.8% CAGR as residential and commercial users respond to net-billing economics. Industrial motive-power and portable-electronics segments trail, growing at 8.3% and 9.1% respectively, yet provide a stable baseline demand that helps smooth factory utilization rates.

Geography Analysis

Punjab and Sindh together account for close to 75% of Pakistan's battery market demand, anchored by Karachi’s manufacturing and logistics hub and by Lahore’s automotive cluster. Karachi hosts BYD’s assembly line and Atom Power’s 100 MWh plant in development, catalyzing a battery corridor that mirrors India’s Pune–Bengaluru ecosystem. Punjab’s rooftop solar installations quadrupled in 2026, and post-billing-shift households have accelerated adoption of 5–10 kWh lithium-ion packs.

Khyber Pakhtunkhwa and Balochistan hold roughly 15% share, constrained by lower per-capita income and patchy grid connectivity. Nonetheless, both provinces appear in exploration programs targeting domestic graphite that could de-risk future supply chains. Micro-grid deployments in Gilgit-Baltistan and Azad Jammu & Kashmir rely on 5–20 kWh systems to bridge hydropower seasonality.

Cross-border trade remains China-centric: Pakistan imported USD 180 million of battery materials in 2024, and government policy now aims to boost exports to Australia and Africa via HUBCO’s planned 50,000-unit EV hub. Infrastructure investments, including 40 motorway fast chargers and BYD’s own branded network, will further entrench the Karachi-Lahore-Islamabad triangle as the epicenter of EV charging capacity.

Competitive Landscape

Legacy lead-acid incumbents, Exide Pakistan, Atlas Battery, and Phoenix Battery Industries collectively command around one-third of the Pakistan battery market and leverage nationwide dealer footprints and established recycling loops to defend SLI and UPS niches. Chinese entrants, led by BYD and CATL partnerships, are accelerating lithium-ion penetration in mobility and energy-storage segments that still make up less than 15% of 2025 revenue but will post mid-teens CAGR to 2031.

Atom Power originated Pakistan’s first locally assembled lithium-ion pack in December 2024 and targets 100 MWh assembly capacity by 2026, with a Phase 2 plan to add prismatic cell manufacturing that incorporates domestically purified graphite. HUBCO’s vertical-integration play seeks to control mining through vehicle assembly, echoing BYD’s Chinese strategy and potentially shaving 20% off delivered battery costs if local ore proves viable.

Competitive tactics revolve around localization. Duty-free raw-material quotas provide a 15-18% cost edge for registered manufacturers, squeezing margins for import-only distributors and hastening joint-venture discussions between legacy lead-acid firms and Chinese technology suppliers. Meanwhile, Inverex Power Solutions has carved out a high-margin niche in modular residential storage, bundling smart BMS features and banking on three-to-five-year paybacks to justify premium pricing.

Pakistan Battery Industry Leaders

Zhejiang Narada Power Source Co., Ltd.

Phoenix Battery Ltd.

Atlas Battery Limited

Exide Pakistan Limited.

Volta & Osaka Batteries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Pakistan has announced plans to establish its first lithium-ion battery manufacturing facility in the Korangi Industrial Area of Karachi. This initiative aligns with the proposed National Lithium-Ion Battery Manufacturing Policy 2026–2031, which seeks to reduce reliance on battery imports and enhance domestic energy storage manufacturing capabilities.

- June 2025: China’s XYZ introduced a 261 kWh immersion-cooled commercial battery designed to enhance fire safety and support high-power EV charging. While not directly targeting Pakistan, this technology could influence the development of standards for large-scale energy storage and safety in Pakistan’s growing battery industry as global adoption of commercial batteries continues to expand.

- March 2025: BYD unveiled its first integrated residential energy storage system, the Battery-Box HVE, which combines battery modules with hybrid inverters for flexible home energy storage. This advancement in residential battery storage reflects global trends that could inform the development of Pakistan’s nascent distributed energy storage market, contributing to the growth of the country’s battery industry.

Pakistan Battery Market Report Scope

A battery can be defined as an electrochemical device (consisting of one or more electrochemical cells) that can be charged with an electric current and discharged whenever required. Batteries are usually devices that are made up of multiple electrochemical cells that are connected to external inputs and outputs.

The Pakistan Battery Market Report is Segmented by Type (Primary Battery and Secondary Battery), Technology (Lead-acid Battery, Lithium-ion Battery, and Other Technologies (Ni-MH, Zinc-air, Sodium-ion, Solid-State Prototype)), Form Factor (Cylindrical, Prismatic, and Pouch), Application (Automotive (Passenger Electric Vehicles and Commercial Electric Vehicles), Energy Storage Systems (Utility-Scale and Commercial & Industrial), Industrial Batteries, Portable Electronics, and Others (Medical Devices, Defence, Marine)), and Geography (Pakistan). Market Forecasts are Provided in Terms of Value (USD).

By Type

| Primary Battery |

| Secondary Battery |

By Technology

| Lead-acid Battery |

| Lithium-ion Battery |

| Other Technologies (Ni-MH, Zinc-air, Sodium-ion, Solid-State Prototype) |

By Form Factor

| Cylindrical |

| Prismatic |

| Pouch |

By Application

| Automotive (Passenger Electric Vehicles and Commercial Electric Vehicles) |

| Energy Storage Systems (Utility-Scale and Commercial & Industrial) |

| Industrial Batteries |

| Portable Electronics |

| Others (Medical Devices, Defence, Marine) |

| By Type | Primary Battery |

| Secondary Battery | |

| By Technology | Lead-acid Battery |

| Lithium-ion Battery | |

| Other Technologies (Ni-MH, Zinc-air, Sodium-ion, Solid-State Prototype) | |

| By Form Factor | Cylindrical |

| Prismatic | |

| Pouch | |

| By Application | Automotive (Passenger Electric Vehicles and Commercial Electric Vehicles) |

| Energy Storage Systems (Utility-Scale and Commercial & Industrial) | |

| Industrial Batteries | |

| Portable Electronics | |

| Others (Medical Devices, Defence, Marine) |

Key Questions Answered in the Report

How large will Pakistan's battery demand be by 2031?

It is projected to reach USD 2.69 billion by 2031, growing at a 10.25% CAGR from the 2026 base.

Which battery chemistry is gaining ground fastest?

Lithium-ion is forecast to post a 14.0% CAGR through 2031, narrowing the gap with incumbent lead-acid systems.

What is the main driver behind residential storage uptake?

NEPRA's net-billing regime cuts solar feed-in tariffs, making batteries essential for self-consumption savings.

How is the government encouraging electric two-wheelers?

Subsidies of PKR 50,000 per e-bike and streamlined type approvals reduce upfront costs and speed market entry.

Does Pakistan recycle lithium-ion batteries locally?

No dedicated facility exists yet; the formal sector only covers 5-10% of overall end-of-life battery volumes.

What cost advantage do local assemblers enjoy over imports?

Duty-free raw-material quotas provide a 15-18% landed-cost edge versus finished-pack importers.

Page last updated on: