Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

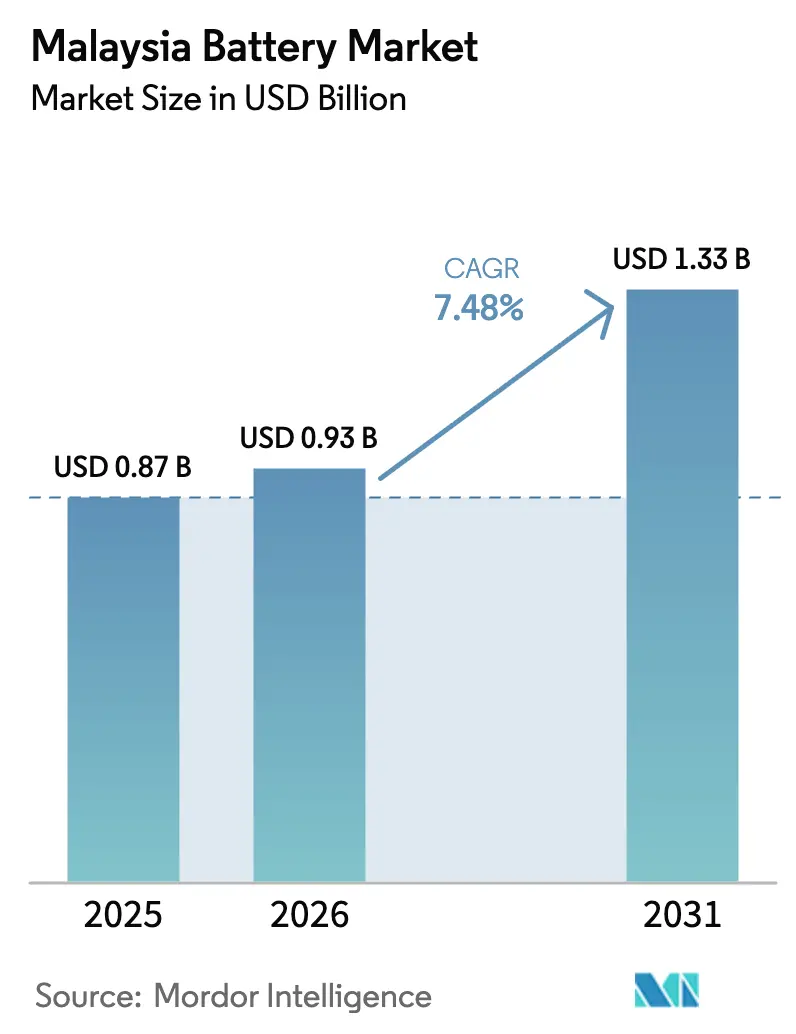

| Base Year Market Size (2025) | USD 0.87 Billion |

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.33 Billion |

| Growth Rate (2026 - 2031) | 7.48% CAGR |

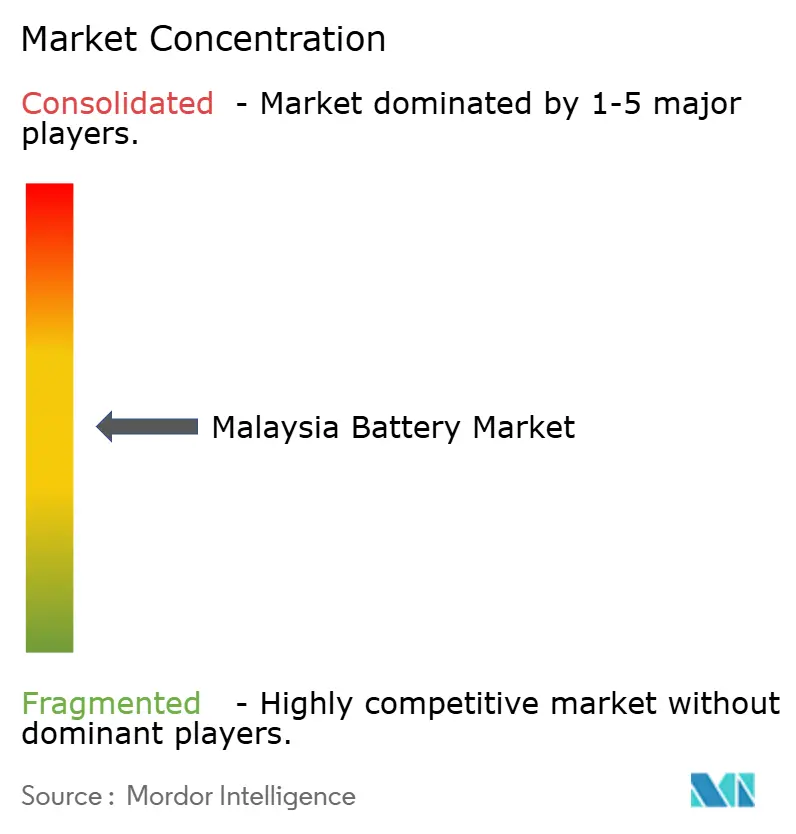

| Market Concentration | Medium |

Major Players/malaysia-battery-market---growth,-trends,-and-forecast-(2020---2025)_Companies_-_Malaysia_Battery.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Battery Market Analysis by Mordor Intelligence

The Malaysia Battery Market size is projected to expand from USD 0.87 billion in 2025 and USD 0.93 billion in 2026 to USD 1.33 billion by 2031, registering a CAGR of 7.48% between 2026 to 2031.

This trajectory stems from three structural shifts: mandatory battery energy storage adoption under the Solar ATAP framework that began in 2026, accelerating Chinese green-field cell manufacturing that leverages Malaysia’s tariff advantages, and rapid data-center buildouts that require high-reliability UPS solutions.[1]Malaysian Investment Development Authority, “Battery industry overview and incentives,” mida.gov.my Rising electric-vehicle (EV) registrations, grid-scale storage tenders, and foreign direct investment (FDI) inflows are rebalancing demand away from commodity lead-acid starting-lighting-ignition (SLI) units toward higher-value lithium-ion chemistries serving automotive, stationary, and industrial customers. Intensifying competition, together with overcapacity-driven price wars among Chinese manufacturers, exerts margin pressure on domestic assemblers but simultaneously widens downstream opportunities in pack integration, thermal management, and grid-service software. Malaysia’s dependence on imported lithium, cobalt, and nickel remains a supply-chain vulnerability, yet federal incentives under the National Energy Transition Roadmap encourage ecosystem buildout across Kedah, Johor, and Selangor, positioning the Malaysia battery market for multi-year growth.

Key Report Takeaways

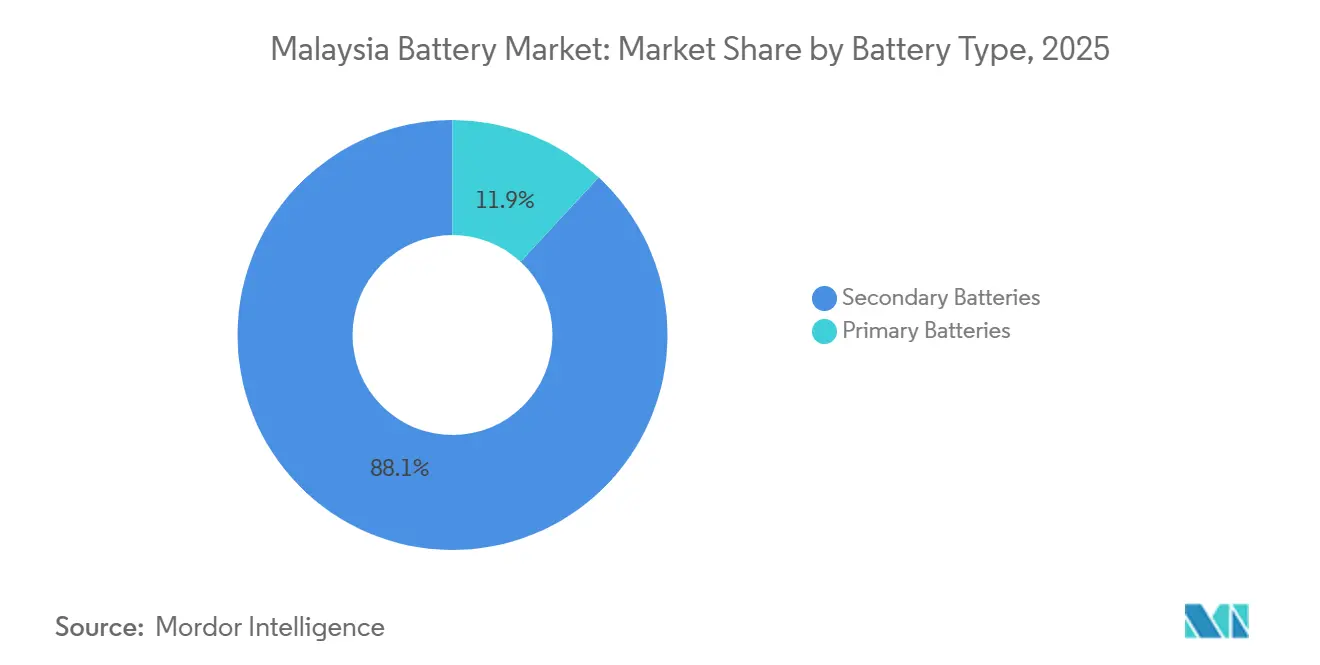

- By battery type, secondary (rechargeable) batteries captured 88.1% of Malaysia's battery market share in 2025 and are forecast to grow at a 7.9% CAGR through 2031.

- By technology, lead-acid commanded 41.5% of the Malaysia battery market size in 2025, while solid-state batteries are expected to register the fastest 11.3% CAGR over 2026-2031.

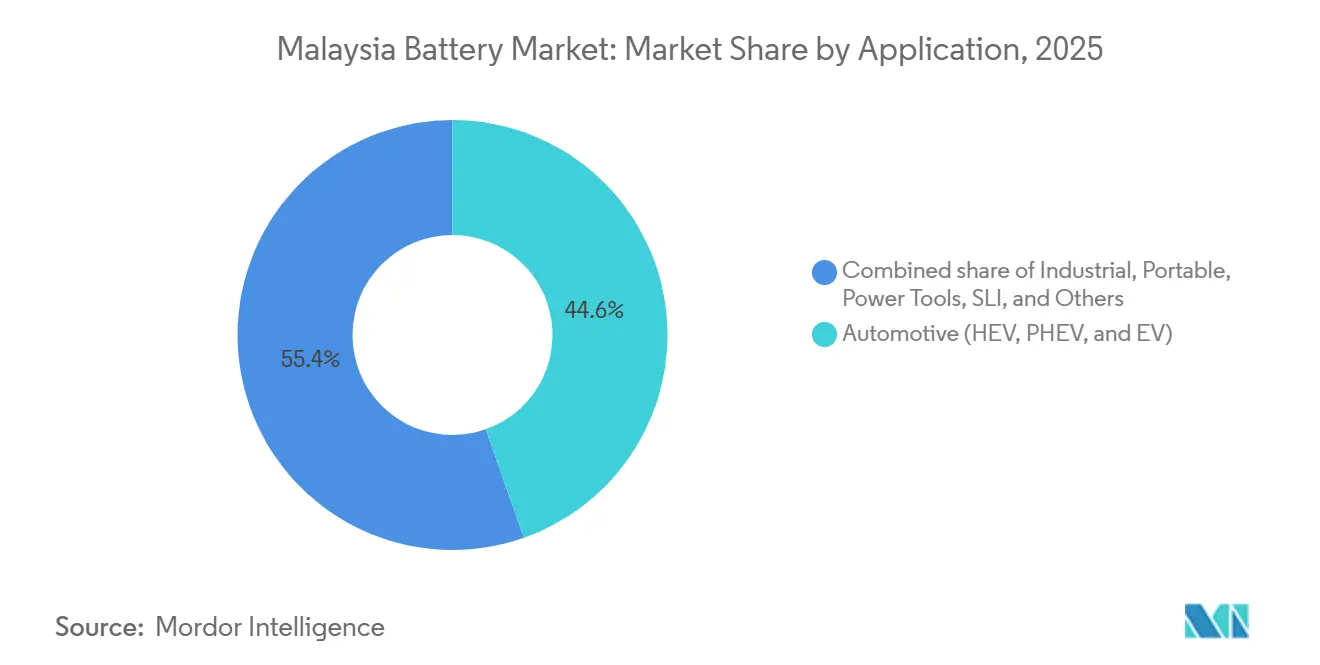

- By application, automotive batteries held 44.6% of Malaysia's battery market share in 2025, and are projected to log the highest 8.8% CAGR to 2031.

- By geography, Kedah leads manufacturing capacity with EVE Energy's combined 10-15 GWh ESS expansion, whereas Johor is the fastest-growing deployment cluster, supported by a five-fold data-center pipeline increase to 2029.

- Panasonic Energy Malaysia, Samsung SDI, and GS Yuasa collectively accounted for roughly 25% of 2025 shipments, while new Chinese entrants added more than 9 GWh of announced capacity, intensifying rivalry in the Malaysia battery market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining lithium-ion battery prices | +1.2% | Global, import cost benefits nationwide | Medium term (2-4 years) |

| National Energy Transition Roadmap incentives for ESS | +1.8% | Peninsular grid zones | Long term (≥ 4 years) |

| Expansion of Malaysia’s data-center industry | +1.0% | Johor, Selangor growth corridors | Short term (≤ 2 years) |

| Net Energy Metering 4.0 boosting residential storage | +0.9% | Urban rooftop segments | Medium term (2-4 years) |

| Rapid growth of e-moped & e-scooter market | +0.6% | Urban logistics hubs | Short term (≤ 2 years) |

| Southeast Asia battery-manufacturing FDI inflows | +1.5% | Kedah and Johor industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining Lithium-Ion Battery Prices

Global lithium-ion pack costs averaged USD 108 per kWh in 2025, down 8% year-on-year despite volatile raw-material inputs. Stationary storage packs fell to USD 70 per kWh, slashing levelized costs for solar-plus-storage projects in Malaysia's commercial and industrial (C&I) sector. While falling prices compress margins for domestic cell assemblers, they expand addressable use-cases in off-grid telecom towers, industrial microgrids, and behind-the-meter systems. China's USD 84 per kWh average, 48% lower than Europe's, amplifies competitive pressure on Malaysian producers that lack scale efficiencies.[2]Anu Bhambhani, “Battery Pack Prices Hit New Low in 2025,” TaiyangNews, taiyangnews.info The IEA foresees a further 40% global decline by 2030, implying future Malaysia battery market competitiveness will hinge more on system integration and software than on cell costs.[3]International Energy Agency, “Batteries and Secure Energy Transitions,” iea.org

National Energy Transition Roadmap Incentives for ESS

Malaysia’s roadmap targets 70% renewable capacity by 2050 and underwrites a 500 MW BESS roll-out by 2030. The Solar ATAP framework, live since January 2026, mandates storage integration for large-scale solar and community projects, while SELCO guidelines require batteries for rooftop systems above 72 kWp. Tenaga Nasional Berhad’s MyBEST tender for 400 MW/1,600 MWh signals a shift from pilots to bankable procurement, yet capacity-payment mechanisms remain undefined, tempering private capital appetite. Early grid projects in Sarawak and Sabah validate technical viability but underscore reliance on multilateral financing.

Expansion of Malaysia’s Data-Centre Industry

Google’s USD 2 billion and Microsoft’s USD 2.2 billion hyperscale commitments are driving megawatt-scale UPS demand. Each megawatt of IT load requires roughly 1.5-2 MWh of backup storage to achieve 99.995% uptime, catalyzing lithium-ion adoption over VRLA solutions. Gold Peak Technology’s USD 150 million Johor plant, slated for 2028 operations, targets this UPS niche, betting on lower lifecycle costs and higher energy density. The technology shift spawns a bifurcated replacement market: legacy VRLA suppliers defend installed bases, while lithium-ion specialists secure greenfield buildouts.

Net Energy Metering 4.0 Boosting Residential Storage

The Solar ATAP program supersedes Net Energy Metering 3.0 and explicitly permits behind-the-meter storage. High-income households in Klang Valley and Penang are early adopters of 5-10 kWh lithium-ion systems despite payback periods above seven years, whereas middle-income segments await financing innovations. Newly published SIRIM safety standards favor certified brands and raise barriers for uncertified imports. Absent subsidies, community storage models are gaining traction in newly planned townships, although regulatory clarity on virtual net metering is still evolving.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited domestic raw-material supply chain | -0.8% | Nationwide | Long term (≥ 4 years) |

| High upfront cost of stationary storage for households | -0.5% | Residential segments | Medium term (2-4 years) |

| Policy-continuity uncertainty in EV incentives | -0.7% | Automotive demand | Short term (≤ 2 years) |

| Influx of low-cost Chinese battery imports | -0.6% | Price-sensitive channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Domestic Raw-Material Supply Chain

Malaysia lacks lithium, cobalt, and nickel refining at battery-grade purity, forcing manufacturers to import precursor materials primarily from China, Australia, and Indonesia. Secondary lead stocks are plentiful but largely below 99.97% purity, limiting usefulness for valve-regulated lead-acid upgrades. Rising ESG compliance costs and dependence on volatile commodity markets heighten supply-chain risk and reduce cost competitiveness relative to Chinese imports.

High Upfront Cost of Stationary Storage for Households

Residential BESS units cost RM 20,000-25,000 (USD 4,500-5,600), translating to 7-10-year payback periods at Malaysia’s flat residential tariffs of RM 0.40-0.50 per kWh. Absence of grants or low-interest loans limits adoption to affluent early adopters. Although community storage models promise cost sharing, regulatory gaps on third-party ownership and revenue splitting constrain rollout.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeable Dominance Accelerates

Secondary batteries held 88.1% of Malaysia's battery market share in 2025 and are forecast to grow at a 7.9% CAGR, buoyed by EV uptake, grid-scale mandates, and industrial motive replacements. Primary batteries retain 11.9% share, confined to remote sensors and medical devices. The National Energy Transition Roadmap and Solar ATAP program anchor demand for rechargeable systems, while EVE Energy's CNY 8.654 billion Phase 2 ESS investment exemplifies the scale economics needed to serve domestic and export customers. Primary battery innovation focuses on shelf-life and eco-chemistry tweaks, underscoring a structural pivot toward rechargeables.

By Technology: Lead-Acid Incumbency Meets Solid-State Disruption

Lead-acid commanded 41.5% of the Malaysia battery market size in 2025, underpinned by aftermarket SLI demand and cost-sensitive industrial fleets. Solid-state batteries, though nascent, are expected to record the fastest 11.3% CAGR through 2031 as pilot lines target 390-560 Wh/kg energy densities. Lithium-ion chemistries continue to capture incremental demand, with Samsung SDI’s USD 1.3 billion Seremban Plant 2 producing PRiMX 21700 cells and evaluating 4680 formats for potential Tesla supply. NiMH holds residual presence in non-plug-in hybrids, while NaS and flow batteries remain in pilot phases.

By Application: Automotive Batteries Lead, Industrial Diversifies

Automotive batteries represented 44.6% of Malaysia's battery market share in 2025 and are projected to clock an 8.8% CAGR to 2031, contingent on post-2025 incentive clarity. Industrial stationary segments, backed by data-center UPS and grid BESS projects, form the fastest-expanding non-automotive category. Portable consumer electronics face commoditization, prompting producers to pivot toward higher-margin silicon-anode cells for wearables, as exemplified by Enovix's USD 1.2 billion facility.[4]Malaysian Investment Development Authority, “EVE Energy Phase 2 expansion details,” mida.gov.my Power-tool demand benefits from EVE Energy's 680 million-cell annual output, supplying global OEMs.

Geography Analysis

Peninsular Malaysia dominates manufacturing, with Kedah hosting EVE Energy’s twin-phase gigafactory and Shenzhen Senior Technology Material’s separator line. Johor attracts UPS-centric lithium-ion investments linked to hyperscale data centers, while Selangor remains the legacy hub for Panasonic and Samsung SDI. East Malaysia’s Sabah and Sarawak focus on grid-scale storage installations, such as the 60 MW/80 MWh Sejingkat BESS and the 100 MW/400 MWh Sungrow project, illustrating regional renewable integration needs. Perak’s ascendance as an EV assembly node through BYD’s 150-acre plant suggests future pack-integration spillovers. Geographic dispersion creates logistics inefficiencies as cells produced in Kedah and Johor are shipped to Borneo, adding up to 7% to landed project costs.

Competitive Landscape

The Malaysia battery market is moderately fragmented. Incumbent Japanese and South Korean firms leverage long-term OEM contracts, vertical integration, and certification pedigrees to defend market share. Chinese entrants deploy modular gigafactories, achieving record 16-month commissioning cycles that undercut traditional timelines. Domestic lead-acid players compete on distribution density but face import-driven price compression. Strategic moves in 2025 include Samsung SDI’s pilot run of 4680 cells, EVE Energy’s Phase 2 ESS expansion, and Gold Peak’s Johor UPS plant announcement. Second-life battery integrators and BMS developers represent emerging niches with lower capital intensity and potential for local value capture.

Malaysia Battery Industry Leaders

Panasonic Energy Malaysia Sdn Bhd

Samsung SDI Energy Malaysia Sdn Bhd

GS Yuasa Corporation

FIAMM Energy Technology SpA

Yokohama Batteries Sdn Bhd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: SIRIM issued safety guidelines for residential and commercial BESS, aligning with IEC 62619.

- August 2025: BYD confirmed a Perak assembly plant aimed at serving ASEAN EV demand.

- July 2025: EVE Energy announced a CNY 8.654 billion Phase 2 ESS expansion targeting 10-15 GWh capacity.

- February 2025: Shenzhen Senior Technology Material broke ground on a CNY 5 billion separator facility in Kulim.

Malaysia Battery Market Report Scope

A battery is a device that converts chemical energy contained within its active materials directly into electric energy, utilizing an electrochemical oxidation-reduction (redox) reaction. The Malaysian battery market report includes:

By Battery Type

| Primary Batteries |

| Secondary Batteries |

By Technology

| Lead-acid |

| Li-ion |

| Nickel-metal hydride |

| Nickel-cadmium |

| Sodium-sulfur |

| Solid-state |

| Flow Battery |

| Emerging chemistries |

By Application

| Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) |

| Portable (Consumer Electronics, etc.) |

| Power Tools |

| SLI |

| Other Applications |

| By Battery Type | Primary Batteries |

| Secondary Batteries | |

| By Technology | Lead-acid |

| Li-ion | |

| Nickel-metal hydride | |

| Nickel-cadmium | |

| Sodium-sulfur | |

| Solid-state | |

| Flow Battery | |

| Emerging chemistries | |

| By Application | Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) | |

| Portable (Consumer Electronics, etc.) | |

| Power Tools | |

| SLI | |

| Other Applications |

Key Questions Answered in the Report

What is the current value of the Malaysia battery market?

The market was valued at USD 0.93 billion in 2026 and is forecast to reach USD 1.33 billion by 2031.

How fast is the lithium-ion segment growing in Malaysia?

Lithium-ion demand is rising alongside EV sales and grid-scale projects, contributing to a 7.9% CAGR forecast for rechargeable batteries through 2031.

Which state hosts the largest battery manufacturing investments?

Kedah leads, anchored by EVE Energy's multi-phase gigafactory and Shenzhen Senior Technology Material's separator plant.

What policy changes shape stationary storage adoption?

The Solar ATAP framework effective in 2026 mandates BESS for large solar systems and introduces community storage requirements.

How will the expiry of EV tax incentives affect battery demand?

If duty exemptions lapse without replacement after December 2025, short-term EV and battery demand could dip, but local assembly incentives may cushion the impact.

Which companies dominate UPS batteries for data centers?

Gold Peak Technology, Samsung SDI, and GS Yuasa are leading suppliers, with new lithium-ion modules optimized for high-availability data-center architectures.

Page last updated on: