Office And Contact Center Headset Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.03 Billion |

| Market Size (2031) | USD 4.72 Billion |

| Growth Rate (2026 - 2031) | 9.27% CAGR |

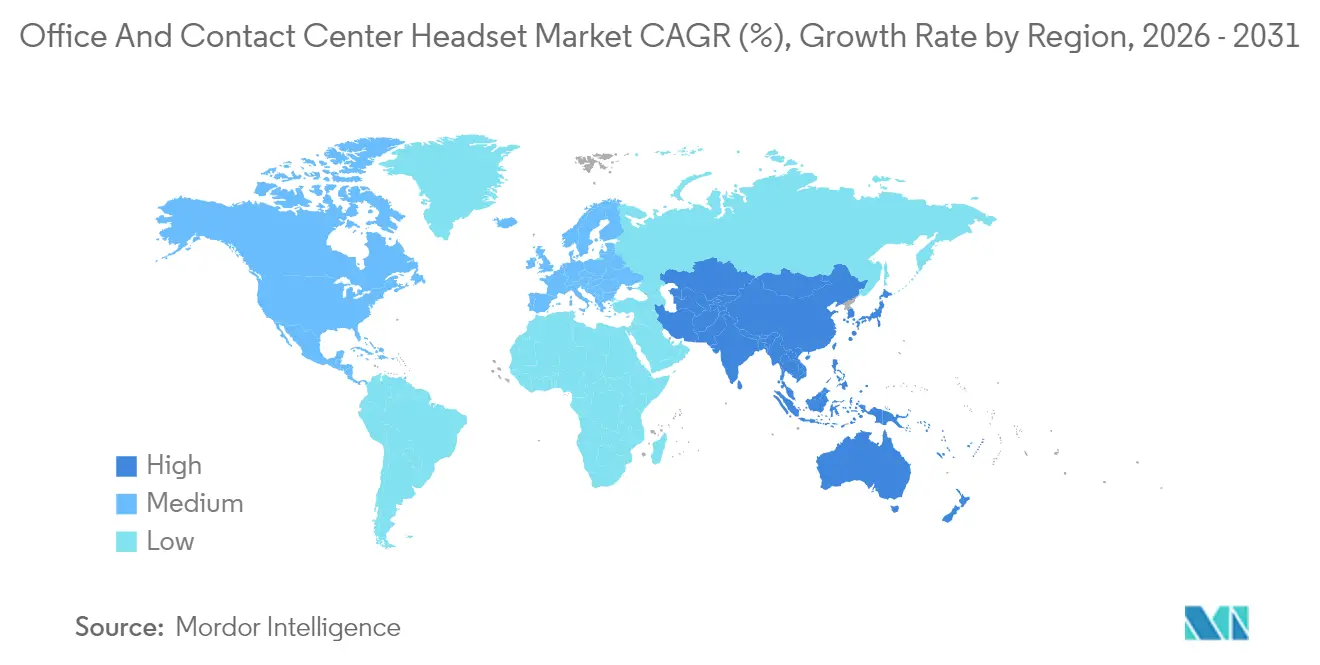

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Office And Contact Center Headset Market Analysis by Mordor Intelligence

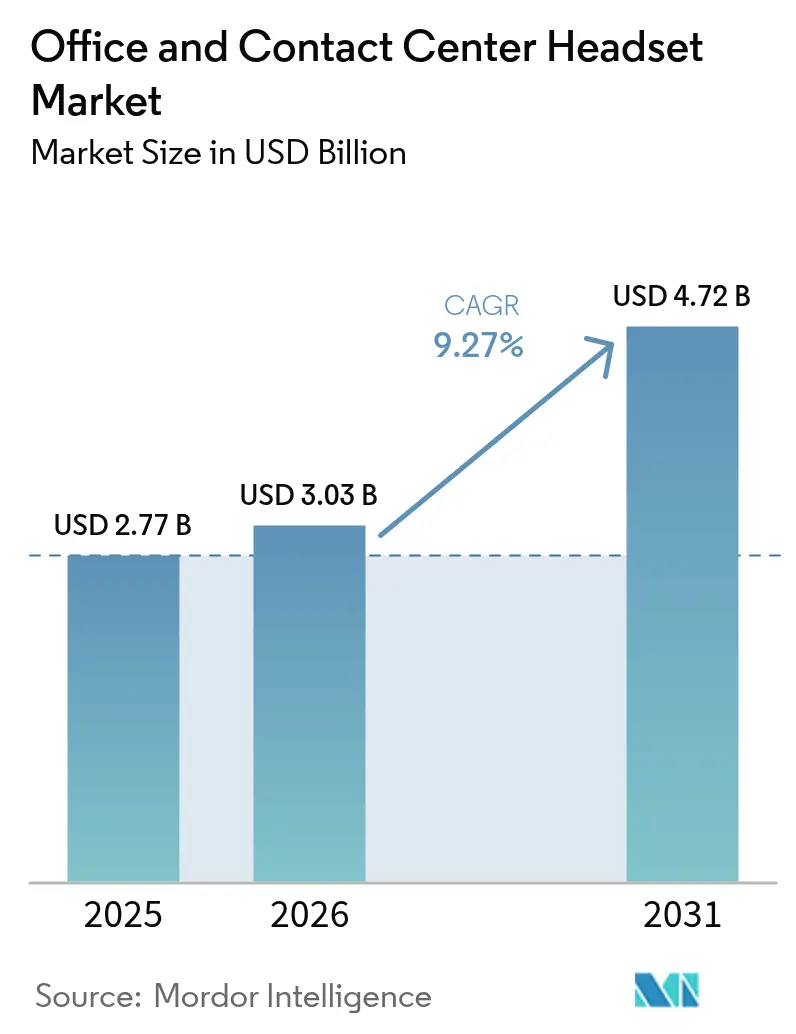

The office and contact center headset market size is expected to grow from USD 2.77 billion in 2025 to USD 3.03 billion in 2026 and is forecast to reach USD 4.72 billion by 2031 at 9.27% CAGR over 2026-2031. This momentum stems from the normalization of hybrid work, cloud-native contact center rollouts, and artificial intelligence-powered voice processing, which repositions headsets as strategic endpoints rather than low-cost consumables. Enterprises now embed telemetry from headsets into workforce analytics, lifting average selling prices while lengthening replacement cycles. Wireless connectivity is expanding as Bluetooth Low Energy lengthens battery life beyond 30 hours, and premium tiers gain ground because adaptive noise cancellation demonstrably trims call handling time. Competitive intensity is rising as certified low-cost Chinese OEMs undercut incumbents, while the migration to softphones trims multi-device attach rates and fuels differentiation through AI features. North America remains the revenue leader, but the Asia-Pacific region outpaces all others due to its dense business process outsourcing (BPO) labor pool and rapid cloud migration.

Key Report Takeaways

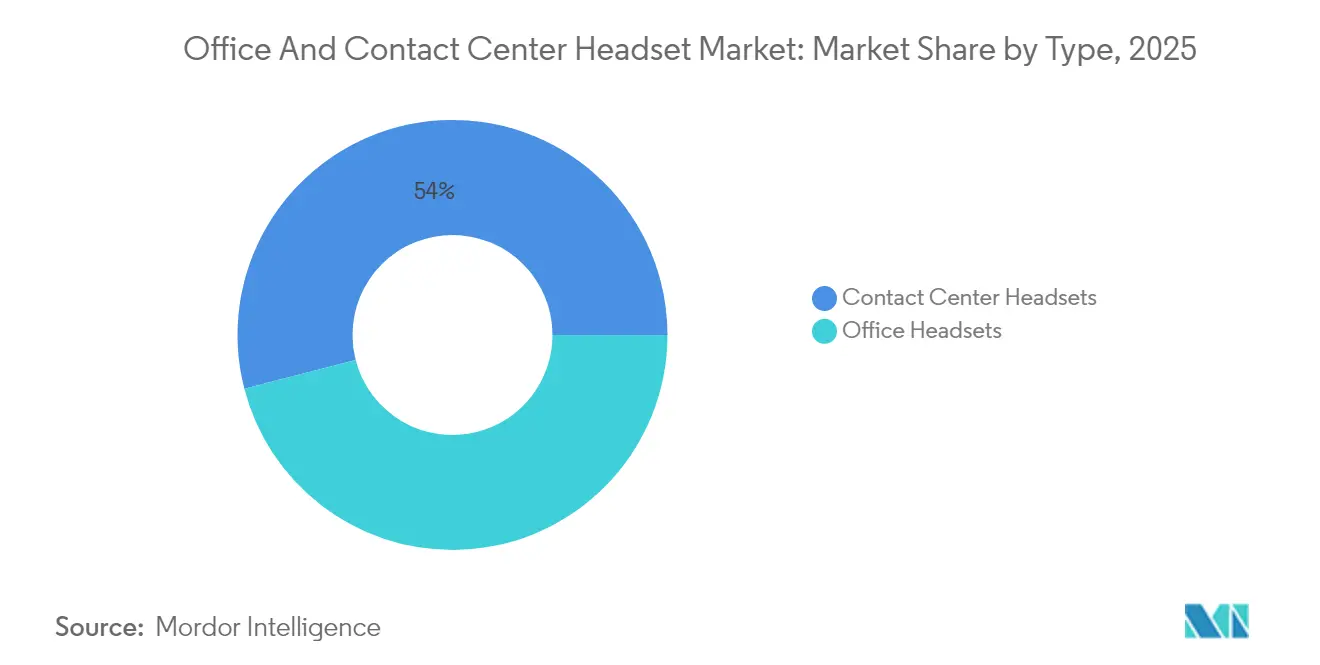

- By type, contact center headsets contributed 54.02% share of the office and contact center headset market size in 2025; office headsets are advancing at a 10.55% CAGR to 2031.

- By connectivity, wireless models controlled 63.55% share of the office and contact center headset market size in 2025 and are forecast to grow at a 10.96% CAGR to 2031.

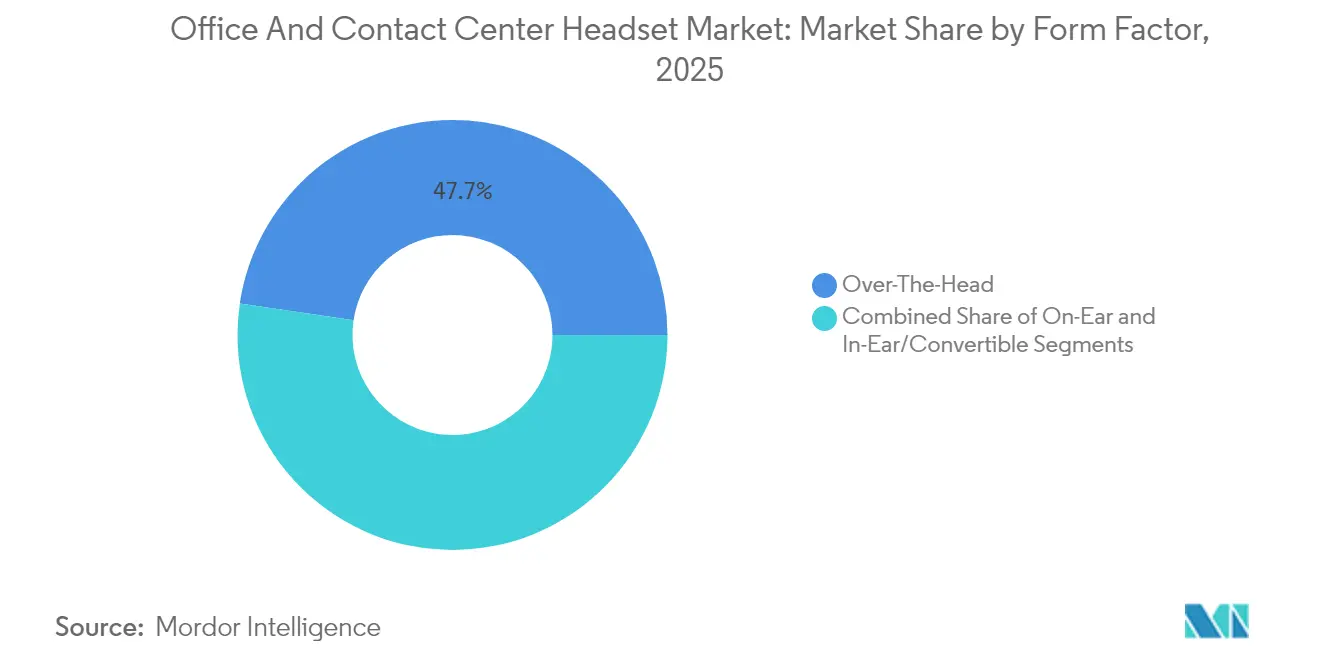

- By form factor, over-the-head designs held 47.66% share of the office and contact center headset market size in 2025, while in-ear and convertible options are expanding at 9.89% through 2031.

- By end-user sector, IT and telecom commanded 28.94% share of the office and contact center headset market size in 2025; healthcare is the fastest mover, growing at 11.08% CAGR through 2031.

- By price band, the USD 101-250 tier captured 41.35% share of the office and contact center headset market size in 2025; the above-USD 250 premium bracket is rising at 10.63% CAGR to 2031.

- By region, North America represented 34.18% share of the office and contact center headset market size in 2025, yet Asia-Pacific is set to grow at 10.35% CAGR on the back of its 5.44 million-agent BPO workforce.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Office And Contact Center Headset Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Growth of Remote and Hybrid Work Culture | +3.2% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Increasing Cloud-Based Contact Center Adoption | +2.8% | Global, Asia-Pacific Core with spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Advancements in Noise-Cancellation and Voice AI Algorithms | +2.4% | Global, early uptake in North America and Asia-Pacific | Medium term (2-4 years) |

| Expanding Adoption of Unified Communications Platforms in SMEs | +2.1% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Integration of Headset Telemetry Data into Workforce Analytics | +1.6% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Growing Sales Via Device-as-a-Service Procurement Models | +1.4% | North America and Europe, expanding into Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Growth of Remote and Hybrid Work Culture

Hybrid arrangements stabilized at 53% of the global labor force, and 16% work fully remote in 2024.[1]Owl Labs, “State of Hybrid Work 2024,” owllabs.com Employers now mandate certified headsets to ensure uniform call quality, especially in professional services and software development. Logitech reported that 68% of its enterprise customers require approved peripherals for all client-facing employees. Durability needs in home offices lengthen replacement cycles to as much as five years, yet higher build specifications raise unit pricing and, in turn, push the office and contact center headset market higher.

Increasing Cloud-Based Contact Center Adoption

Annual spending on cloud contact-center infrastructure reached USD 5.1 billion in 2024. Asia-Pacific leads migration: NASSCOM projects that 73% of India’s 4 million BPO agent seats will be cloud-based by 2026, up from 41% in 2024, NASSCOM.IN. Cloud architectures require IP-native headsets that integrate with Amazon Connect, Genesys Cloud, and Five9, creating pull-through demand for certified wireless devices across the office and contact center headset market.

Advancements in Noise-Cancellation and Voice AI Algorithms

University of Washington researchers demonstrated a semantic hearing system that improved signal-to-noise ratio by up to 4.62 dB in 2024. Chipmaker Airoha’s AB1595 Bluetooth system-on-chip features a neural processing unit for local echo suppression and voice activity detection, achieving a latency of under 20 milliseconds. These gains elevate premium headsets from accessories to cost-saving assets, as every 10-second reduction in average handle time saves approximately USD 1.2 million per 1,000 agents, accelerating the adoption of premium headsets across the office and contact center headset market.

Expanding Adoption of Unified Communications Platforms in SMEs

Microsoft Teams surpassed 320 million monthly active users in 2024, with small enterprises accounting for 62% of the incremental seats. Native device certification lowers support tickets and shortens onboarding, motivating SMEs to replace consumer earbuds with professional headsets. As unified-communications penetration rises, headset demand extends beyond Fortune 500 environments, making SMEs a core incremental buyer segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Consumer-Grade Earbuds Cannibalizing Professional Sales | -1.8% | Global, sharpest in North America and Western Europe | Short term (≤ 2 years) |

| Transition From Desk Phones to Softphones Reducing Multi-Device Attach Rates | -1.3% | North America and Europe, gradual in Asia-Pacific | Medium term (2-4 years) |

| Intensifying Price Pressure From Low-Cost Asian OEMs | -1.1% | Global, concentrated in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Increasing Cybersecurity Certification Costs for Enterprise Headsets | -0.7% | Regulated industries in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Consumer-Grade Earbuds Cannibalizing Professional Sales

Volume shipments of true-wireless earbuds create an employee perception that personal devices are sufficient for work calls. Enterprises counter by enforcing peripheral policies, yet sub-USD 100 price bands still lose share to earbuds that now match battery life and basic ANC. Vendors respond with enterprise-specific differentiators, such as busy lights and centralized firmware updates, to defend the office and contact center headset market.

Transition From Desk Phones to Softphones Reducing Multi-Device Attach Rates

Widespread softphone migration eliminates the need for headsets that pair with both desk phones and computers, reducing attachment rates for higher-priced models. Vendors are increasingly embedding AI transcription, telemetry, and extended warranties to maintain average selling prices and preserve their share in the office and contact center headset market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type – Office Headsets Gain Momentum in a Hybrid World

Office headsets are forecast to grow at 10.55% to 2031, narrowing the gap with contact center devices, which still account for over one-half of the revenue. Remote employees bring their own peripherals between hot desks and home offices, boosting demand for foldable, multi-point models such as the Logitech Zone Wireless. The office and contact center headset market size for the office segment is projected to grow the fastest, as telemetry dashboards help HR identify ergonomic or usage issues.

Contact center growth remains anchored in Asia-Pacific cloud migrations. Poly’s Voyager 4320 UC, at USD 249, addresses home-based agents who need 50-hour battery life and adaptive ANC. Premium, rugged units such as the EPOS IMPACT 1060 ANC, at EUR 549 (USD 586), satisfy 24-hour operations, extending life cycles to five years and stabilizing the office and contact center headset market share within large BPO facilities.

By Connectivity – Wireless Dominance Accelerates

Wireless devices controlled a 63.55% share in 2025 and are expected to expand at a 10.96% CAGR. Bluetooth 5.2 and LE Audio deliver over 30 hours of talk time, while DECT remains indispensable on sprawling contact center floors. The office and contact center headset market size for wireless offerings is expected to exceed USD 3.12 billion by 2031, as Teams and Zoom introduce native Bluetooth pairing, eliminating the need for proprietary dongles.

Wired products persist where Bluetooth is banned, notably on trading floors and in some government call centers. Audio-Technica’s BPHS1, priced at USD 199, offers XLR connectivity for analog backup lines, underscoring a resilient niche even as wireless technology scales globally.

By Form Factor – In-Ear Convertibles Lead Growth

In-ear and convertible designs are expected to grow at a rate of 9.89% due to commuting professionals who prefer pocket-sized gear. The Jabra Evolve2 Buds, priced at USD 279, combine IP57 sealing with eight-microphone ANC, underpinning expansion beyond offices into outdoor work settings. The office and contact center headset market share for over-the-head models still stands at 47.66% because contact centers value comfort and battery modularity.

On-ear hybrids appeal to executives who want to make spatial-audio video calls during travel. Bose QuietComfort Ultra, at USD 429, offers 24-hour autonomy and spatial awareness, ensuring senior staff remain engaged in negotiations without visual fatigue.

By End-User Industry – Healthcare Surges as Telemedicine Stabilizes

Telehealth has matured into mainstream care, driving demand for healthcare headsets at an 11.08% CAGR through 2031. Clinicians require HIPAA-compliant audio and busylights that signal consultations in shared living spaces. Noise-isolating microphones also improve behavioral-health outcomes because therapists rely on vocal cues.

IT and telecom retained 28.94% revenue in 2025 but is plateauing in North America and Europe. Asian shared-service centers help offset some saturation, and banks in the BFSI sector upgrade to AI-ready headsets that detect scripting violations in real-time, reinforcing compliance within the office and contact center headset market.

By Price Range – Premium Tier Expands on Productivity ROI

The above-USD 250 bracket grows at 10.63% as enterprises quantify time savings from advanced ANC and voice AI. The Jabra Evolve2 85, priced at USD 469, recovers its premium within one year by reducing support calls, while the EPOS IMPACT 1060 ANC offers a five-year service life that lowers total cost.

The USD 101-250 segment captures the highest unit share at 41.35%, driven by volume BPO rollouts that negotiate bulk discounts while still demanding certified gear. Sub-USD 100 devices face erosion from earbuds unless vendors add enterprise-specific firmware and telemetry to justify their procurement.

Geography Analysis

The Asia-Pacific region posts the fastest 10.35% CAGR, driven by India’s 4 million agents and the Philippines’ 1.44 million handler workforce, which processes 71% of global voice BPO interactions. NASSCOM values India’s BPO revenue at USD 49.87 billion in 2024, with cloud penetration expected to reach 73% by 2026, maintaining robust headset orders. Eastern Europe emerges as an auxiliary hub, with Poland, Romania, and Ukraine together employing over 700,000 agents and standardizing on IP headsets to service multilingual campaigns.

North America generated 34.18% of 2025 revenue through the early adoption of unified communications and the presence of dense Fortune 500 contact centers. Growth decelerates as replacement cycles stretch to five years, but the United States' next-generation 911 funding, a USD 442 million hardware allocation over seven years, sustains procurement for secure, VoIP-ready headsets. Canadian provinces follow similar modernization paths, tightening cybersecurity standards that favor certified vendors. Europe lags because legacy PSTN links persist in Germany and France, whereas the United Kingdom and the Nordics are migrating aggressively to cloud platforms. Latin America and Africa add volume through new multilingual BPO centers in Brazil and South Africa, leveraging labor cost advantages by adopting mid-range wireless models that balance budget and certification needs. Collectively, these regions propel the ongoing diversification of the office and contact center headset market.

Competitive Landscape

The major vendors, including Logitech, GN Store Nord (Jabra), HP (Poly), EPOS, and Sennheiser, captured a significant share of the 2024 revenue. Logitech and Jabra leverage preferred-vendor status inside Microsoft Teams and Zoom procurement portals, reinforcing ecosystem lock-in. Each offers management dashboards that integrate with ServiceNow to flag battery cycles and firmware versions, enabling predictive maintenance and just-in-time replacements.

Chinese OEMs erode pricing power by delivering Teams-certified headsets for USD 49-79. Yealink alone shipped more than 140 million cumulative units and generated CNY 4.2 billion (USD 580 million) in 2024, supported by ISO 9001 factories and distribution through Ingram Micro and TD Synnex.[3]Ingram Micro, “2024 Distribution Announcements,” ingrammicro.com Western incumbents respond by consolidating their assembly in Vietnam and India, while embedding AI analytics and on-device security to justify their premium positioning.

Emerging challengers include Sony and Samsung, which repurpose consumer earbud supply chains to offer multipoint pairing and busylights around 20-30% below established brands. Certification costs between USD 50,000 and USD 150,000 per model, along with six-to-twelve-month validation cycles, restrict smaller suppliers, effectively channeling market share toward capital-rich players and helping stabilize the office and contact center headset market.

Office And Contact Center Headset Industry Leaders

GN Store Nord A/S

HP Inc. (Poly Inc.)

Logitech International S.A.

EPOS Group A/S

Yealink Network Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: EPOS has unveiled its latest wireless headset, designed for office and call center workers seeking comfort, noise cancellation, and a degree of future-proofing due to the latest version of the Bluetooth wireless protocol. The EPOS Impact 500 is an on-ear Bluetooth headset, and it’s the latest model to join the Next IMPACT Generation of EPOS enterprise headsets.

- November 2025: Yealink entered a strategic partnership with Officeworks to supply a full range of professional business headsets across its network of 162 stores in Australia. This move makes Yealink's headsets available on the high street and online for the growing number of Australians working remotely or in hybrid environments.

- October 2025: Jabra announced that it had teamed up with Zoom to achieve new certifications for its professional headsets, underscoring their shared commitment to empowering both frontline and hybrid workers with communication tools that help them stay connected and productive in any environment.

- September 2025: Logitech introduced the Zone Wireless 2 ES and Zone Wired 2 headsets, designed for use in noisy offices. With AI-powered noise-canceling mics, hybrid active noise cancellation (ANC) that automatically adjusts to minimize background noise, and a gaming-inspired headstrap design for all-day comfort, the headsets turn open office clamor into quiet focus zones.

Global Office And Contact Center Headset Market Report Scope

Office and Contact Center Headsets facilitate clear, hands-free communication in bustling work environments. Equipped with boom mics and noise cancellation features, these headsets ensure superior sound quality for both agents and customers. They prioritize all-day comfort and offer versatile connectivity options, including PC, desk phone, and mobile. The outcome is a boost in productivity and a reduction in fatigue, benefiting both customer service roles and general office tasks.

The Global Office and Contact Center Headset Market Report is Segmented by Type (Office Headsets, and Contact Center Headsets), Connectivity (Wired, and Wireless), Form Factor (Over-The-Head, On-Ear, and In-Ear/Convertible), End-User Industry (BFSI, Government and Public Sector, Healthcare, IT and Telecom, and Others), Price Range (Sub-USD 100, USD 101-250, and Above USD 250), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Office Headsets |

| Contact Center Headsets |

| Wired |

| Wireless |

| Over-The-Head |

| On-Ear |

| In-Ear/Convertible |

| BFSI |

| Government and Public Sector |

| Healthcare |

| IT and Telecom |

| Others |

| Sub-USD 100 |

| USD 101-USD 250 |

| Above USD 250 |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Type | Office Headsets | ||

| Contact Center Headsets | |||

| By Connectivity | Wired | ||

| Wireless | |||

| By Form Factor | Over-The-Head | ||

| On-Ear | |||

| In-Ear/Convertible | |||

| By End-User Industry | BFSI | ||

| Government and Public Sector | |||

| Healthcare | |||

| IT and Telecom | |||

| Others | |||

| By Price Range | Sub-USD 100 | ||

| USD 101-USD 250 | |||

| Above USD 250 | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the office and contact center headset market?

The market stands at USD 3.03 billion in 2026 and is set to climb to USD 4.72 billion by 2031.

Which region is expected to grow the fastest through 2031?

Asia-Pacific will grow at a 10.35% CAGR, led by India and the Philippines with their large BPO workforces.

Why are premium headsets gaining share despite higher prices?

Enterprises quantify productivity gains from adaptive noise cancellation and voice AI, making payback periods shorter than one year.

How significant are wireless models in overall demand?

Wireless devices already hold 63.55% revenue share and will expand rapidly as Bluetooth LE and DECT technologies mature.

Which end-user sector shows the highest growth potential?

Healthcare leads with a 11.08% CAGR because telemedicine has become a sustained care channel.

What factors most threaten market growth?

Cannibalization by consumer earbuds and shrinking multi-device attach rates as desk phones disappear exert downward pressure on overall demand.

Page last updated on: