Oat Milk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.65 Billion |

| Market Size (2031) | USD 6.96 Billion |

| Growth Rate (2026 - 2031) | 13.78% CAGR |

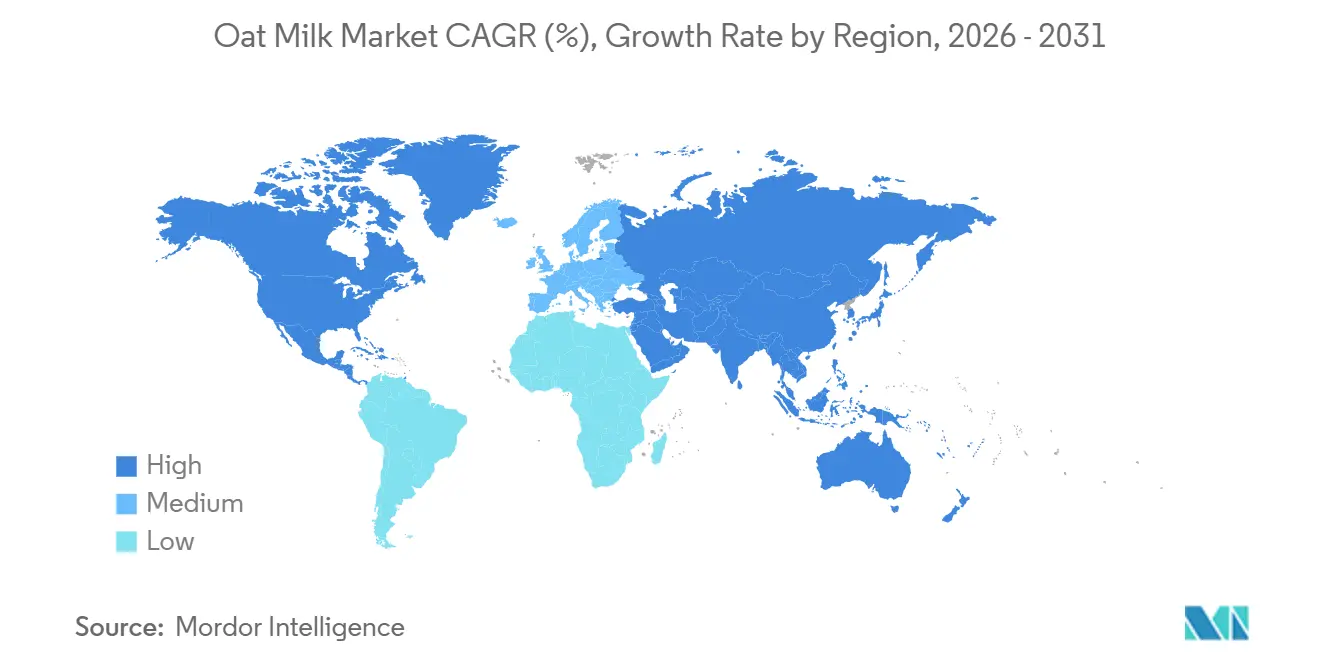

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oat Milk Market Analysis by Mordor Intelligence

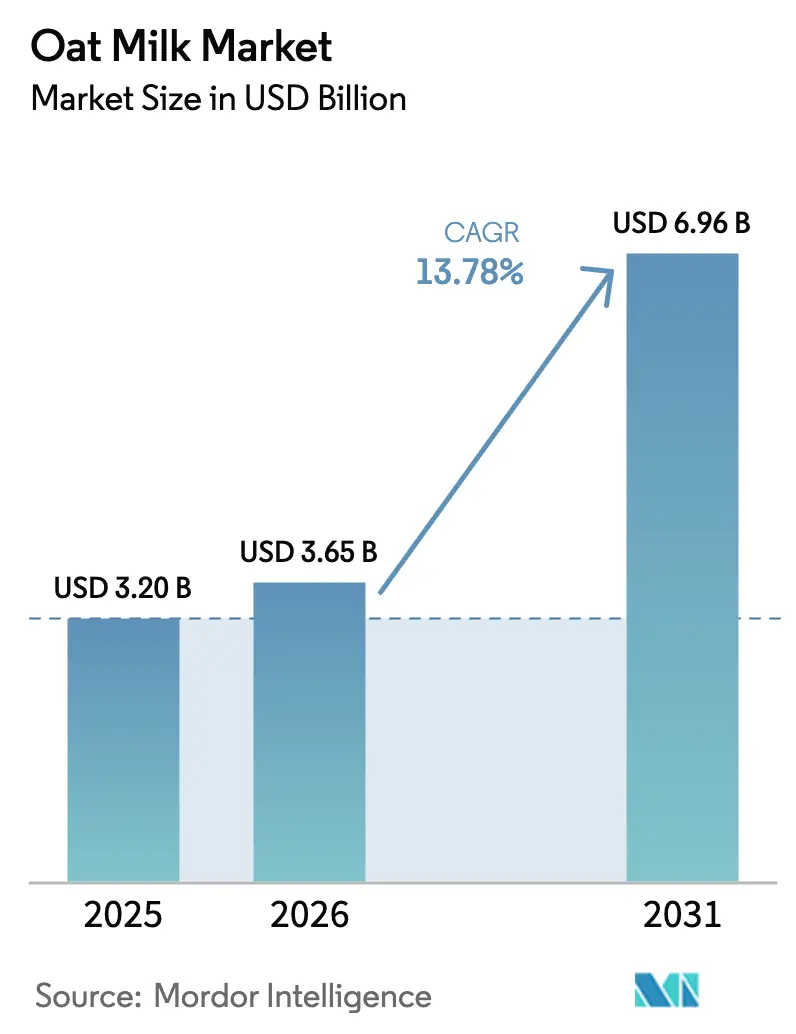

The oat milk market size is projected to expand from USD 3.20 billion in 2025 and USD 3.65 billion in 2026 to USD 6.96 billion by 2031, registering a CAGR of 13.78% between 2026 to 2031. Growing lactose intolerance, which affects roughly two-thirds of the global population, is creating a reliable demand floor for dairy-free beverages. At the same time, rising environmental awareness positions oat milk as a lower-carbon alternative to dairy, aided by life-cycle data showing 70% fewer greenhouse-gas emissions per liter. Coffee-shop adoption is accelerating because oat milk foams well for lattes, and foodservice listings often spill over into retail sales. Europe currently leads consumption, yet Asia-Pacific is the fastest-growing region, driven by urbanization, digital commerce, and high lactose intolerance. Regulatory guidance on fortification in the United Kingdom and stricter EFSA rules on contaminants are also nudging product reformulation toward nutrient-dense, premium offerings.

Key Report Takeaways

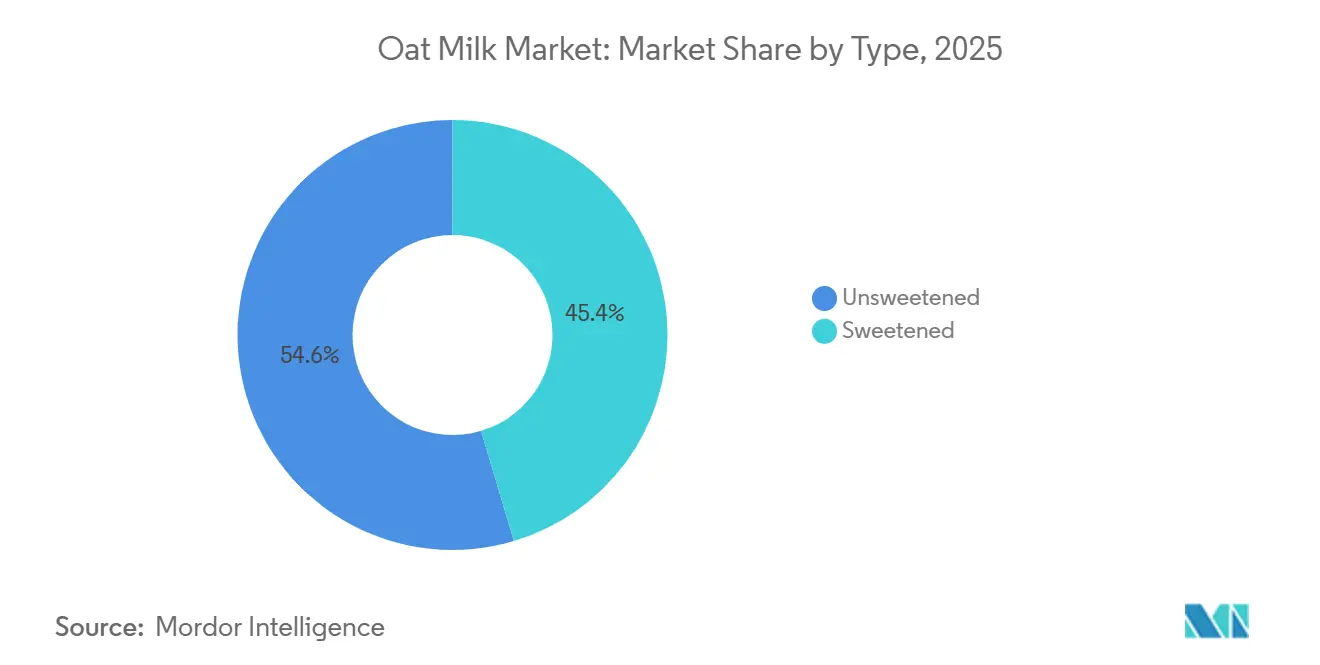

- By type, unsweetened captured 54.62% of the oat milk market share in 2025, while sweetened is projected to expand at a 15.97% CAGR through 2031.

- By flavour, unflavoured products held 67.96% of revenue in 2025, whereas flavoured alternatives are on track for a 15.32% CAGR to 2031.

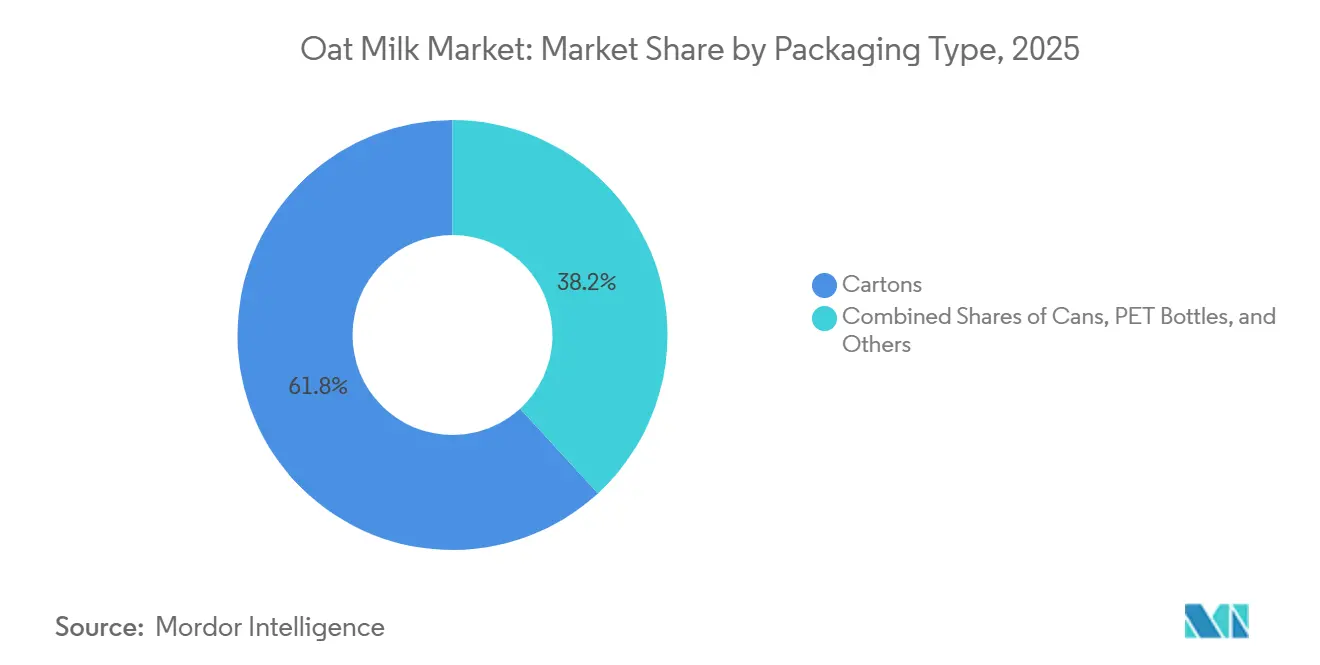

- By packaging, cartons led with 61.82% of sales in 2025, and cans are poised to rise at a 14.65% CAGR during 2026-2031.

- By distribution channel, off-trade outlets accounted for 93.69% of volume in 2025, while on-trade is forecast to grow at 14.83% through 2031.

- By geography, Europe led with 37.59% revenue share in 2025, and Asia-Pacific is projected to post a 15.13% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oat Milk Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of plant-based diets and flexitarian lifestyles | +3.5% | Global, with strongest momentum in North America and Europe | Medium term (2-4 years) |

| Rising prevalence of lactose intolerance and dairy sensitivities | +2.8% | Global, particularly acute in Asia-Pacific (70-90% prevalence) and parts of Africa | Long term (≥ 4 years) |

| Expansion of oat milk usage in coffee and foodservice channels | +2.2% | North America and Europe core, spillover to Asia-Pacific urban centers | Short term (≤ 2 years) |

| Product innovation and premiumization strategies | +1.9% | Europe and North America lead, Asia-Pacific following with localized flavors | Medium term (2-4 years) |

| Growth of functional and fortified oat milk products | +1.7% | Global, with regulatory push in Europe (EFSA) and UK (SACN) | Medium term (2-4 years) |

| Influence of health, wellness, and lifestyle marketing | +1.5% | Global, resonating strongly with millennial and Gen Z cohorts in urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Plant-Based Diets and Flexitarian Lifestyles

Flexitarian eating patterns, characterized by occasional meat consumption alongside predominantly plant-based meals, have become mainstream dietary strategies rather than niche preferences, with the OECD-FAO Agricultural Outlook 2024-2033 projecting global food consumption growth of 1.2% annually while highlighting rising consumer concerns about environmental sustainability and personal health[1]Source: OECD-FAO, “Agricultural Outlook 2024-2033,” OECD-ILIBRARY.ORG. Oat milk benefits disproportionately from this shift because its production requires 80% less land and generates 70% lower greenhouse gas emissions than dairy milk, positioning it as a credible climate-friendly alternative that does not require full dietary transformation, according to Oatly Sustainability Report 2024. Regulatory influence is emerging through voluntary carbon labeling schemes and government procurement guidelines in Scandinavia and the Netherlands that favor low-carbon food products, indirectly boosting oat milk adoption in institutional foodservice.

Rising Prevalence of Lactose Intolerance and Dairy Sensitivities

Approximately 65-68% of the global population exhibits some degree of lactose malabsorption after infancy, with prevalence exceeding 90% in parts of East Asia and 70-80% in South Asia, Africa, and the Middle East, creating a structural demand floor for lactose-free alternatives, according to the National Institutes of Health[2]Source: National Institutes of Health, “Lactose Intolerance,” NCBI.NLM.NIH.GOV. Oat milk's naturally creamy mouthfeel, derived from beta-glucan soluble fiber, delivers sensory satisfaction closer to dairy milk than almond or soy alternatives, reducing the perceived trade-off for lactose-intolerant consumers. The UK SACN/COT report in July 2025 noted that typical oat milk contains 0.6 grams of protein per 100 grams compared to 3.4 grams in cow's milk, prompting manufacturers to introduce protein-fortified variants with 3-5 grams per serving to address nutritional gaps. Regulatory frameworks in the European Union under Regulation 1169/2011 require clear allergen labeling, ensuring lactose-intolerant consumers can confidently identify suitable products, while FDA guidance in the United States permits "lactose-free" claims on plant-based beverages that meet compositional standards.

Expansion of Oat Milk Usage in Coffee and Foodservice Channels

Oat milk accounted for 33% of all alternative milk orders in coffee shops during 2024, surpassing almond and soy milk to become the dominant non-dairy option, according to transaction data from Square's coffee and snack shop network[3]Source: Square, “Oat Milk in Coffee Shops 2024,” SQUAREUP.COM. This leadership stems from oat milk's superior steaming and frothing properties, which baristas attribute to its higher fat content (typically 1.5-3%) and beta-glucan viscosity, which creates stable microfoam essential for latte art and texture. The Good Food Institute reported that oat milk represents 38% of plant-based milk dollar sales in U.S. foodservice channels, reflecting premium pricing power when bundled with specialty coffee beverages. SunOpta announced in October 2024 that its Dream Oatmilk Barista product expanded to 6,700 additional stores through a partnership with a large coffee chain, demonstrating how foodservice contracts drive volume at scale while building brand awareness that spills over into retail channels. Compliance with food safety standards such as HACCP and ISO 22000 is critical for foodservice suppliers, as institutional buyers require third-party certification to mitigate contamination risks.

Product Innovation and Premiumization Strategies

Manufacturers are differentiating through limited-edition flavors, barista-specific formulations, and functional claims that command 20-40% price premiums over baseline oat milk products. Danone launched Silk NextMilk in 2024, a proprietary blend designed to more closely replicate the taste and nutrition of dairy milk, targeting consumers who remain hesitant about plant-based alternatives due to perceived taste compromises. Oatly introduced a 100% British-grown oat sourcing commitment for its Barista range in October 2025, reducing the climate footprint by 7-13% and appealing to consumers who prioritize local agriculture and supply chain transparency. Tetra Pak's whole oat grain processing technology, launched in 2025, enables manufacturers to extract up to 25% more beverage from the same raw material input (10 liters from 1.1 kilograms of oats versus 8 liters with conventional methods), improving gross margins and supporting premium positioning through sustainability narratives. Regulatory compliance with novel food regulations under EFSA and FDA GRAS (Generally Recognized as Safe) determinations is essential for ingredient innovations, particularly for added proteins, fibers, and bioactive compounds.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and raw material costs | -1.8% | Global, most acute in regions with limited oat cultivation (South America, MEA) | Short term (≤ 2 years) |

| Volatility in oat supply and agricultural risks | -1.3% | North America and Europe primary, climate risks spillover globally | Medium term (2-4 years) |

| Allergen cross-contamination risks | -0.9% | Global, regulatory scrutiny highest in EU and North America | Long term (≥ 4 years) |

| Price sensitivity among consumers | -1.2% | Emerging markets (Asia-Pacific, South America, MEA) and price-conscious segments in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production and Raw Material Costs

Oat milk production requires specialized enzymatic hydrolysis to break down oat starches into fermentable sugars, high-pressure homogenization to achieve stable emulsions, and ultra-high-temperature (UHT) processing for shelf stability, resulting in capital expenditures that exceed those for conventional dairy processing. SunOpta's USD 26 million investment to expand its Modesto facility by 60% capacity illustrates the scale of infrastructure required, with the company adding 167,684 square feet of production space and creating 17 new jobs to support operations. Raw oat prices in the United States declined to USD 3.10-3.40 per bushel in 2024 from higher levels in 2023, yet remain subject to weather-driven volatility, with USDA reporting 2024 oat production at 67.8 million bushels and yields at a record 76.5 bushels per acre. Tetra Pak's whole oat processing technology, which raises oat solids from 15-16% to 30%, reduces electricity, water, and steam consumption per liter, offering a pathway to lower variable costs over time[4]Source: Tetra Pak, “Oat Beverage Processing Solutions,” TETRAPAK.COM. Regulatory compliance with FDA food safety modernization rules and EFSA contaminant limits adds incremental testing and documentation expenses that disproportionately burden smaller producers.

Volatility in Oat Supply and Agricultural Risks

Oat cultivation is concentrated in North America (the United States, Canada) and Northern Europe (Finland, Sweden, and Poland), exposing the supply chain to regional weather events, pest pressures, and agronomic challenges. The OECD-FAO Agricultural Outlook 2024-2033 highlights climate variability and trade policy risks as persistent threats to cereal production, with oats particularly vulnerable to spring frost and summer drought during critical growth stages. Oatly's October 2025 commitment to source 100% British-grown oats for its Barista range represents a strategic hedge against supply disruptions, though it also increases dependence on a single geographic region and exposes the company to UK-specific agricultural risks. Oatside's use of Australian oats for its Indonesian production facility diversifies sourcing but introduces currency and freight cost variability. Regulatory frameworks under USDA organic certification and EU Organic Regulation 2018/848 impose additional constraints on pesticide use and crop rotation, potentially limiting yield scalability for organic oat milk producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Unsweetened Variants Dominate, Sweetened Accelerates Through Indulgence

Unsweetened oat milk held 54.62% of the market in 2025, while sweetened oat milk is forecast to grow at 15.97% CAGR during 2026-2031, outpacing the unsweetened segment. Unsweetened products appeal to health-conscious consumers seeking clean-label formulations with minimal added sugars, aligning with dietary guidelines from the American Heart Association and WHO that recommend limiting free sugar intake to less than 10% of total energy consumption. The UK SACN/COT report noted that typical oat milk contains 3.5 grams of free sugars per 100 grams, derived from enzymatic breakdown of oat starches during processing, positioning unsweetened variants as lower-sugar alternatives to flavored dairy milk and sweetened plant-based competitors[5]Source: U.K. SACN/COT, “Plant-Based Drinks Benefit and Risk Assessment,” GOV.UK.

Sweetened oat milk's faster growth reflects manufacturers' introduction of indulgent flavors, vanilla, chocolate, strawberry, and matcha, that target younger demographics and drive trial through sensory appeal. Danone's Silk NextMilk launch in 2024 included both sweetened and unsweetened formulations, leveraging the brand's dairy milk heritage to bridge consumer preferences. Regulatory compliance with FDA food labeling requirements mandates clear disclosure of added sugars on Nutrition Facts panels, enabling informed consumer choice and supporting premiumization of low-sugar products.

By Flavour: Un-Flavoured Leads, Flavoured Gains Through Coffee and Dessert Applications

Unflavoured oat milk commanded 67.96% of the market in 2025, yet flavoured variants are expanding at 15.32% CAGR through 2031, driven by coffee shop collaborations and dessert-inspired limited editions. Unflavoured products serve as versatile ingredients for cooking, baking, and cereal applications, with neutral taste profiles that do not interfere with recipe flavors. Oatly's Barista Edition, formulated specifically for steaming and frothing in espresso-based beverages, exemplifies unflavoured oat milk's dominance in foodservice, where baristas prioritize texture and foam stability over flavor.

Flavoured oat milk's accelerated growth stems from product innovation in vanilla, chocolate, and seasonal flavours that directly compete with flavoured dairy milk and appeal to children and younger adults. Califia Farms' expansion into flavored oat milk, including cold-brew coffee-infused products, illustrates how manufacturers are blurring category boundaries to capture incremental occasions. SunOpta's Dream Oatmilk Barista, which expanded to 6,700 additional stores in October 2024, includes both unflavoured and vanilla-flavored options, reflecting retailer demand for portfolio breadth.

By Packaging Type: Cartons Prevail, Cans Surge on Portability and Premiumization

Cartons held 61.82% of packaging share in 2025, benefiting from established supply chains, consumer familiarity, and Tetra Pak's dominance in aseptic packaging technology, yet cans are growing at 14.65% CAGR through 2031, the fastest rate among all packaging formats. Cartons' leadership reflects their cost efficiency, recyclability, and compatibility with UHT processing that delivers 6-12 month shelf life without refrigeration, critical for retail distribution and export markets. Tetra Pak's whole oat processing lines, launched in 2025, integrate seamlessly with existing carton filling infrastructure, enabling manufacturers to adopt yield-enhancing technology without replacing packaging equipment.

Cans' rapid growth is driven by single-serve convenience, premium positioning in specialty coffee shops, and sustainability narratives around infinitely recyclable aluminum. Minor Figures, a UK-based oat milk brand targeting independent coffee shops, pioneered canned oat milk in Europe and has expanded distribution through its distinctive packaging and barista-focused marketing. PET bottles and other formats (glass, pouches) account for the remaining share, with glass bottles appealing to ultra-premium segments and pouches gaining traction in emerging markets where cost per serving is paramount.

By Distribution Channel: Off-Trade Dominates, On-Trade Accelerates Through Coffee Culture

Off-trade channels accounted for 93.69% of distribution in 2025, encompassing supermarkets, hypermarkets, convenience stores, specialist retailers, online retail, and warehouse clubs, while on-trade channels (restaurants, cafes, hotels) are forecast to grow at a 14.83% CAGR during 2026-2031. Off-trade's overwhelming dominance reflects household consumption patterns, with consumers purchasing oat milk for breakfast cereal, coffee at home, cooking, and baking. Supermarkets and hypermarkets account for the largest share of the off-trade, leveraging shelf space, promotional support, and private-label offerings to drive volume.

Online retail is expanding rapidly as subscription models from brands like Oatly and direct-to-consumer platforms reduce customer acquisition costs and enable personalized product recommendations. Specialist retailers, including natural food stores and organic grocers, command premium pricing and attract early adopters willing to pay for certified organic, non-GMO, and locally sourced products. On-trade's faster growth stems from oat milk's 33% share of alternative milk orders in coffee shops and 38% of plant-based milk dollar sales in foodservice, with barista-specific formulations commanding USD 0.50-1.00 upcharges per beverage. SunOpta's October 2024 expansion into 6,700 additional stores through a large coffee chain partnership exemplifies how on-trade contracts drive brand awareness that spills over into retail channels.

Geography Analysis

Europe held 37.59% of the global oat milk market in 2025, yet Asia-Pacific is forecast to grow at 15.13% CAGR during 2026-2031, the fastest rate among all regions, reflecting divergent maturity curves and consumption drivers. Europe's leadership stems from early adoption in Scandinavia, Germany, and the United Kingdom, where environmental consciousness, lactose intolerance prevalence, and strong coffee culture created fertile ground for oat milk penetration. Oatly's Swedish heritage and initial market development in Nordic countries established oat milk as a credible dairy alternative before global expansion, while Arla Foods' launch of Jörð oat milk in the UK in September 2022 demonstrated how incumbent dairy cooperatives are defending market share through plant-based diversification. The UK SACN/COT report in July 2025, which identified oat milk as the fastest-growing plant-based beverage in the UK and issued comprehensive nutritional recommendations, underscores regulatory attention to category development and consumer safety. Germany, the Netherlands, Sweden, and France exhibit high per capita consumption, supported by extensive retail distribution, foodservice penetration, and sustainability-oriented consumer preferences. EFSA's January 2025 novel food guidance, mandating rigorous allergenicity, mycotoxin, and heavy metal testing, raises compliance costs but also elevates quality standards and consumer confidence across the European market according to the EFSA.

Asia-Pacific's 15.13% CAGR reflects rapid urbanization, rising disposable incomes, and high lactose intolerance prevalence (70-90% in East and Southeast Asia), creating structural demand for dairy alternatives. Oatside, a Singapore-based oat milk producer backed by Temasek, raised USD 35 million in Series B funding in June 2024 and operates production facilities in Bandung, Indonesia, supplying 18 countries across the region with competitively priced products tailored to local taste preferences. The company's revenue tripled to over USD 50 million in 2023 and doubled again in 2024, though losses widened due to aggressive expansion and marketing investments, illustrating the trade-off between market share capture and near-term profitability. Oatly's closure of its Senoko, Singapore facility in December 2024, incurring USD 20-25 million in impairment charges, highlights the operational challenges of maintaining profitability in price-sensitive markets where local competitors enjoy cost advantages. China, Japan, Australia, India, and Indonesia represent the largest markets within Asia-Pacific, with China's plant-based beverage market benefiting from government nutrition campaigns and Japan's coffee shop culture driving barista-edition oat milk adoption. Australia's established dairy alternative market and domestic oat cultivation provide supply chain advantages, with Australian oats exported to Southeast Asian producers like Oatside.

North America held the second-largest regional share in 2025, with the United States, Canada, and Mexico exhibiting distinct consumption patterns shaped by retail concentration, foodservice penetration, and regulatory frameworks. SunOpta's USD 26 million Modesto facility expansion, completed in June 2024, increased U.S. oat milk production capacity by over 60% and positioned the company to serve leading brands, foodservice operators, and private label customers. Califia Farms, HP Hood's Planet Oat, and Campbell Soup's Pacific Foods dominate U.S. retail shelves, leveraging established distribution networks and brand equity to compete with Oatly and Chobani. Square's transaction data showing oat milk as 33% of alternative milk orders in U.S. coffee shops underscores foodservice's role in driving trial and brand awareness. Canada's market mirrors U.S. trends, with Earth's Own and Danone's Silk brand capturing significant share, while Mexico's emerging plant-based beverage market is constrained by lower disposable incomes and entrenched dairy consumption habits. South America and Middle East & Africa remain smaller markets in 2025 but offer long-term growth potential as urbanization, rising incomes, and exposure to global food trends increase receptivity to plant-based alternatives, though infrastructure gaps, price sensitivity, and limited oat cultivation present near-term headwinds.

Competitive Landscape

The global oat milk market exhibits moderate consolidation, as Oatly, Danone, Califia Farms, Campbell Soup, and Ecotone collectively hold significant share while regional challengers and private label offerings fragment the competitive landscape. Oatly's return to profitability in Q3 2025, with revenue of USD 222.8 million and adjusted EBITDA of USD 3.1 million, marks a strategic inflection point after years of losses following its 2021 IPO, validating the company's asset-light manufacturing strategy and operational restructuring. The closure of Oatly's Singapore facility in December 2024, incurring USD 20-25 million in impairment charges, reflects a broader industry trend toward regional manufacturing hubs that balance scale economies with proximity to demand centers. SunOpta's USD 26 million capacity expansion at its Modesto, California, facility, completed in June 2024, demonstrates how contract manufacturers are capturing value by serving multiple brands, foodservice operators, and private label customers through vertically integrated production and co-packing arrangements.

Danone's Silk NextMilk launch in 2024 leverages the company's dairy milk heritage and distribution muscle to bridge consumer preferences, while Califia Farms' flavored oat milk innovations and HP Hood's Planet Oat retail expansion illustrate how established beverage companies are defending share through portfolio diversification. White-space opportunities are emerging in functional and fortified oat milk products, with the UK SACN/COT report in July 2025 explicitly recommending enhanced fortification for children aged 1-5 years, creating a regulatory tailwind for protein-enriched, vitamin-fortified, and mineral-supplemented formulations. Regional disruptors like Oatside in Asia-Pacific, Minor Figures in Europe, and Earth's Own in Canada are gaining traction through localized sourcing, premium positioning, and barista-focused marketing that resonates with independent coffee shops and specialty retailers.

Tetra Pak's whole oat processing technology, which increases beverage yield by 25% and eliminates fiber waste, is enabling smaller producers to compete on cost and sustainability metrics, potentially fragmenting the market further as barriers to entry decline. Incumbent dairy cooperatives such as Arla Foods (Jörð) and Valio (Oddlygood) are entering the oat milk category to defend their retail shelf space and foodservice relationships, intensifying competition and accelerating innovation cycles. Compliance with FDA food safety modernization rules, EFSA novel food regulations, and ISO 22000 certification is becoming a competitive differentiator, as retailers and foodservice operators prioritize suppliers with robust quality management systems and third-party audits.

Oat Milk Industry Leaders

Califia Farms LLC

Campbell Soup Company

Danone SA

Ecotone

Oatly Group AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Moma Foods expanded its UK retail portfolio by launching four new oat milk products, diversifying its range with flavored, functional, and ready-to-drink (RTD) offerings. The lineup included Salted Maple & Hazelnut Oat Drink and Pistachio Oat Drink, both introduced to deliver café-style taste experiences without syrups, and Immunity Support Oat Drink, fortified with essential vitamins and minerals to target the growing functional beverage segment.

- July 2025: Oatly launched a new Matcha Latte Oat Drink in the United Kingdom. This ready-to-drink beverage combines sweet matcha flavor with a hint of vanilla, blended into Oatly’s signature creamy oat base. It was available in one-liter cartons, initially released at Sainsbury’s, followed by Morrisons and Ocado

- June 2025: Indian dairy and grocery brand Country Delight expanded into the plant-based drink segment by launching its all-new Oats Beverage. The product is made from high-quality Australian oats and is free from chemical additives, preservatives, added sugars, soy, and nuts.

- June 2025: Oatly launched new product variations in North America, introducing Unsweetened and Super Basic OatMilks to expand its beverage portfolio. The products are claimed to be clean-label and plant-based.

Global Oat Milk Market Report Scope

Oat milk is a plant-based, dairy-free beverage made by blending oats with water and then straining the mixture to create a smooth, milk-like liquid. The report segments the market by product type, flavor, packaging type, distribution channel, and geography to provide a structured, in-depth evaluation. By type, the market is divided into sweetened and unsweetened oat milk. By flavor, the study distinguishes between flavoured and unflavoured variants. By packaging type, the report analyzes PET bottles, cans, cartons, and other packaging formats. By distribution channel, the market is divided into on-trade and off-trade segments. The on-trade segment evaluates consumption through cafés, restaurants, and foodservice establishments, while the off-trade segment covers retail sales through supermarkets and hypermarkets, convenience stores, specialist retailers, online retail, and other channels such as warehouse clubs and gas stations. Geographically, the report covers North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The study evaluates key developments influencing the market during the forecast period, with detailed market sizing and projections presented in both value and volume terms.

| Sweetened Oat Milk |

| Unsweetened Oat Milk |

| Flavoured |

| Un-flavoured |

| PET Bottles |

| Cans |

| Cartons |

| Others |

| On-trade | |

| Off-trade | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Specialist Retailers | |

| Online Retail | |

| Others (Warehouse clubs, gas stations, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Type | Sweetened Oat Milk | |

| Unsweetened Oat Milk | ||

| Flavour | Flavoured | |

| Un-flavoured | ||

| Packaging Type | PET Bottles | |

| Cans | ||

| Cartons | ||

| Others | ||

| Distribution Channel | On-trade | |

| Off-trade | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Specialist Retailers | ||

| Online Retail | ||

| Others (Warehouse clubs, gas stations, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Market Definition

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms