Maleic Anhydride Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

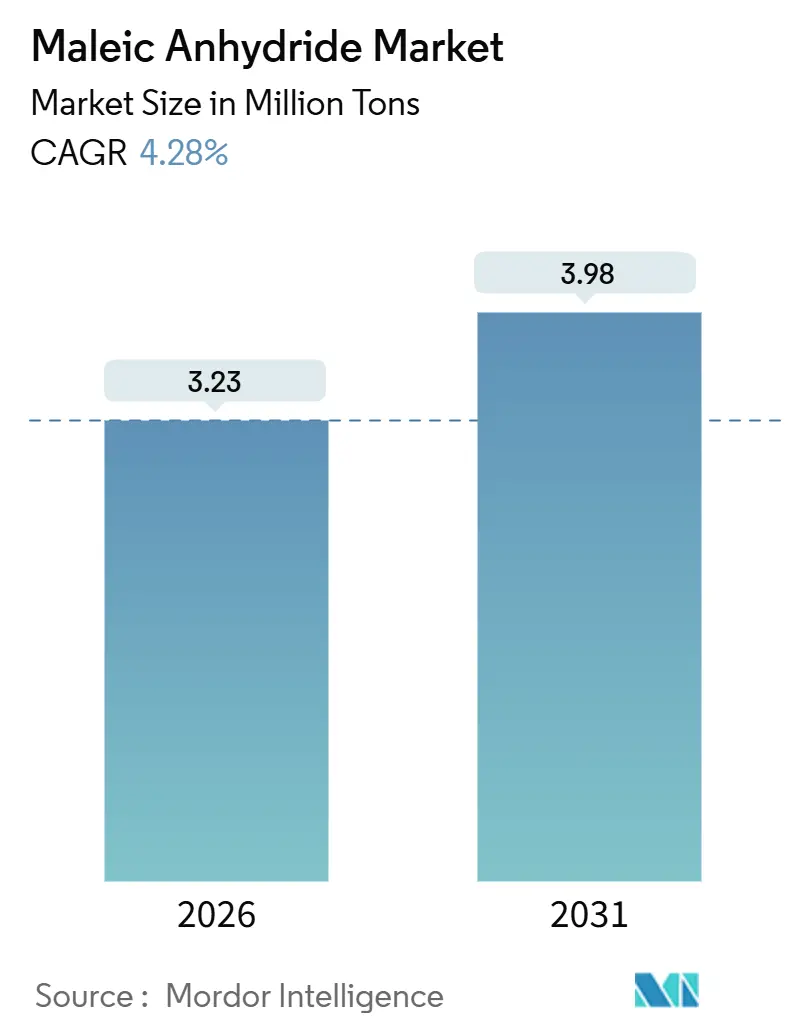

| Market Volume (2026) | 3.23 Million tons |

| Market Volume (2031) | 3.98 Million tons |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

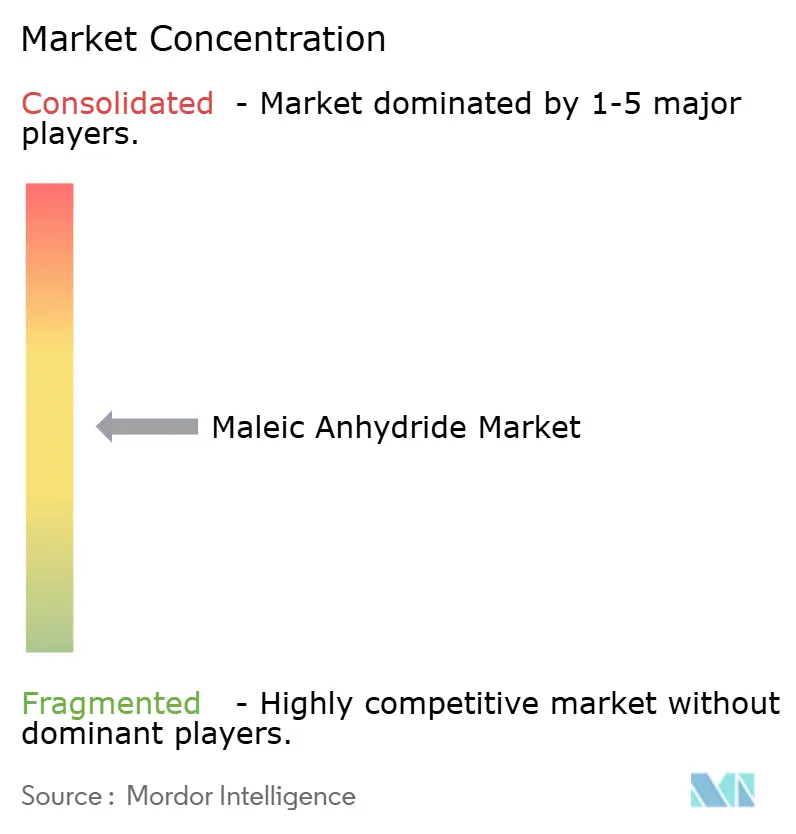

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Maleic Anhydride Market Analysis by Mordor Intelligence

The Maleic Anhydride Market size is estimated at 3.23 million tons in 2026, and is expected to reach 3.98 million tons by 2031, at a CAGR of 4.28% during the forecast period (2026-2031). This growth rests on Asia-Pacific capacity additions, accelerating recycled-PET composite adoption, and the steady pivot from benzene to n-butane feedstock. New Chinese plants boosted global nameplate by 1.46 million tons in 2024, creating oversupply that squeezed margins, especially in Europe and South America. Western producers responded by shutting or mothballing older benzene units, while integrated resin manufacturers in North America and Southeast Asia are embracing molten supply to lower logistics costs. Regulatory drivers—EU circular-economy rules and stricter OECD benzene-emission caps—continue to push production toward low-emission processes and higher-value derivative grades. Competitive intensity is therefore highest in the commodity flake trade, whereas specialty copolymers and high-purity molten grades offer margin resilience.

Key Report Takeaways

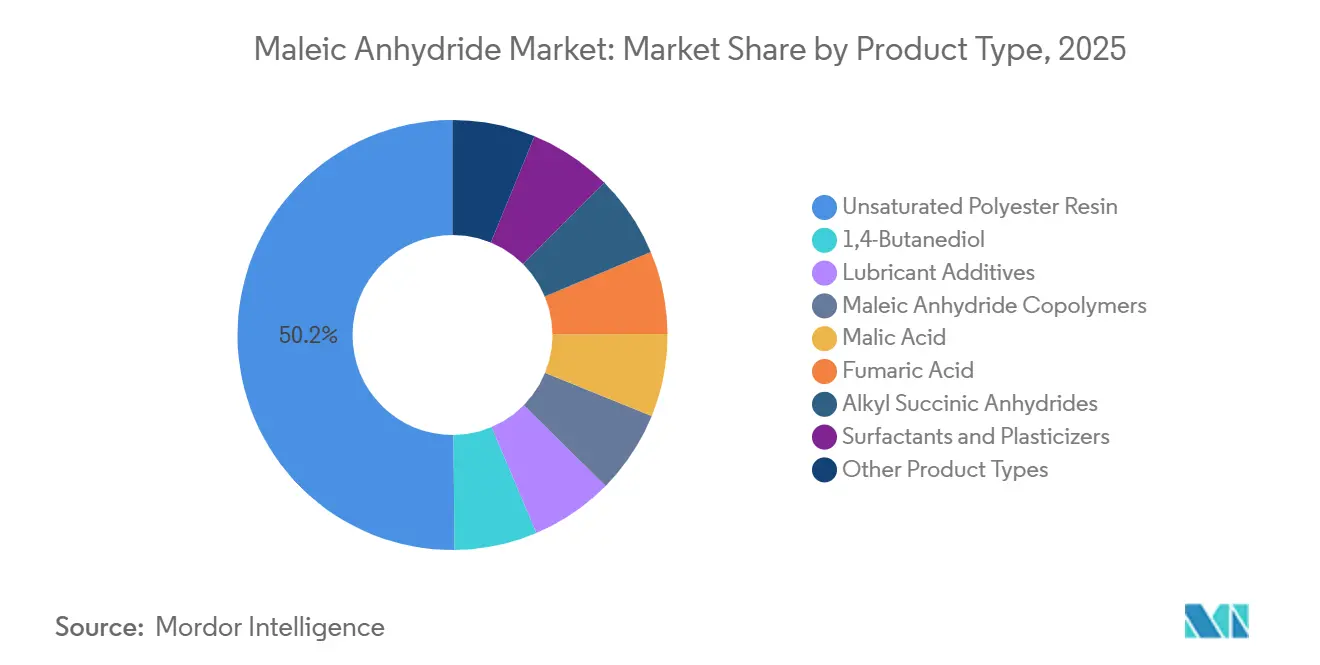

- By product type, unsaturated polyester resin captured 50.15% of the maleic anhydride market share in 2025 and is forecast to expand at a 4.98% CAGR between 2026-2031.

- By raw material, the n-butane route commanded 70.45% share of the maleic anhydride market size in 2025, and the benzene-based route is projected to expand at a 4.72% CAGR through 2031.

- By physical form, the solid form commanded 60.78% share of the maleic anhydride market size in 2025, and molten grade volume is advancing at a 4.93% CAGR, outpacing solid flake/prill growth.

- By end-user industry, construction accounted for 62.23% of the maleic anhydride market size in 2025 and is forecast to expand at a 4.78% CAGR to 2031.

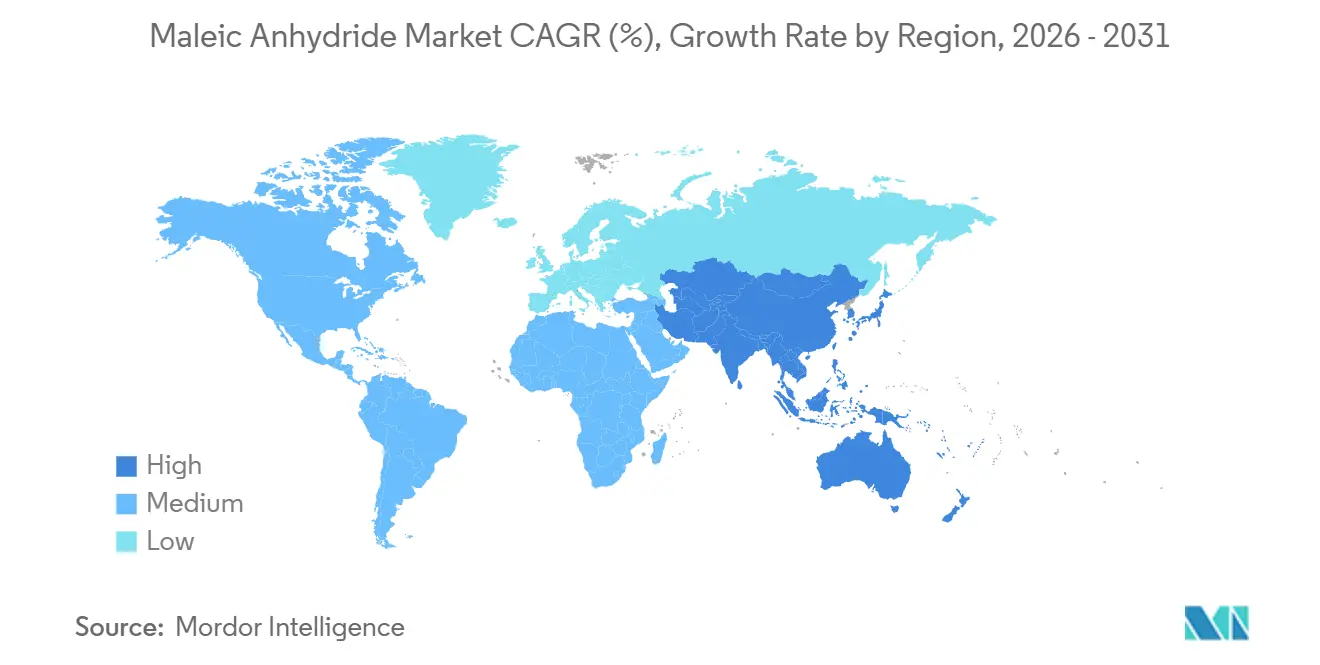

- By geography, Asia-Pacific captured 69.45% of the maleic anhydride market share in 2025 and is advancing at a 4.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Maleic Anhydride Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging adoption of recycled-PET UPR in European construction | +0.8% | Europe (EU-27), with early adoption in Germany, France, Netherlands | Medium term (2–4 years) |

| Capacity additions of n-butane plants lowering feedstock cost | +1.2% | Global, with strongest effect in North America (Gulf Coast), Middle East (Saudi Arabia, Oman), Asia-Pacific (China coastal provinces) | Short term (≤ 2 years) |

| Lightweight SMC panels for EVs boosting UPR demand in North America | +0.6% | North America (United States, Mexico), spill-over to Europe | Medium term (2–4 years) |

| Rising 1,4-BDO demand for spandex and PBT in Asia | +0.9% | Asia-Pacific core (China, India, Vietnam, Indonesia), spill-over to Middle East textile hubs | Medium term (2–4 years) |

| Bio-based succinic-acid copolymers unlocking premium margins | +0.4% | Global, with early commercialization in Japan, Europe (Germany, Netherlands), North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of Recycled-PET UPR in European Construction

In response to EU Regulation 2022/1616, which mandates recycled content in plastics, and the 2024 Ecodesign Regulation, requiring digital product passports to certify circular attributes, European composite producers are taking proactive steps[1]European Union, “Regulation 2022/1616,” eur-lex.europa.eu. They are blending post-consumer PET with maleic-anhydride-modified unsaturated polyester resin. This strategy not only helps them secure green-building credits but also enables a reduction in embodied carbon. Countries like Germany, France, and the Netherlands are leading the charge, channeling their UPR demand into these eco-friendly blends. With passport obligations set to take effect in July 2026, the adoption of these practices is poised to accelerate, solidifying maleic anhydride’s pivotal role as a compatibilizer in the realm of low-carbon construction composites.

Capacity Additions of N-Butane Plants Lowering Feedstock Cost

In 2024, n-butane oxidation dominated with a commanding share of global capacity. Notably, new facilities in China and Oman, leveraging cutting-edge vanadium-phosphate and tri-leaf catalysts, are achieving high yields[2]BASF SE, “Factbook 2024,” basf.com. These advancements not only enhance productivity but also mitigate benzene emissions, allowing these facilities to dodge EPA NESHAP compliance costs. Furthermore, feedstock dynamics tilt in favor of butane, while producers in the Asia-Pacific region paid less for butane than for benzene. This pronounced cost disparity is fueling a surge in conversions and greenfield projects across three continents, solidifying the n-butane route's competitive advantage.

Lightweight SMC Panels for EVs Boosting UPR Demand in North America

In 2025, North American electric vehicle (EV) production surged, marking a robust year-on-year growth. OEMs are now turning to sheet-molding-compound battery enclosures, utilizing unsaturated polyester resin (UPR) and maleic anhydride for each vehicle. The USMCA's local-content regulations are pushing for domestic resin production. This is underscored by the launch of new facilities in Illinois and West Virginia, both of which became operational in 2024. With the rising popularity of gigacasting, the appetite for flame-retardant SMC grades, known for their superior wet-out properties, is set to eclipse the growth of traditional automotive composites, leading to an uptick in regional maleic anhydride consumption.

Rising 1,4-BDO Demand for Spandex and PBT in Asia

Asian textile and electronics clusters are utilizing 1,4-BDO to produce spandex and PBT. By continuously hydrogenating maleic anhydride to BDO at 190 °C, a high yield is achieved. This success has spurred integrated investments, such as BASF’s Zhanjiang Verbund, which is set to commence downstream oxo-C4 units in 2025. China, India, and Vietnam have collectively boosted their PBT capacity, and spandex fiber production has also increased. With a captive BDO supply, producers are insulated from the volatile commodity prices of maleic anhydride, allowing them to command a premium on high-purity grades.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global oversupply driven by new Chinese capacities | -1.1% | Global, with most acute margin pressure in Asia-Pacific, Europe, and Latin America | Short term (≤ 2 years) |

| Stricter OECD benzene-emission caps raising compliance cost | -0.5% | OECD countries (North America, Europe, Japan, South Korea), with benzene-route plants most affected | Medium term (2–4 years) |

| ICE phase-out curbing lube-oil-additive derivatives | -0.3% | Europe (EU-27), North America (United States, Canada), with gradual impact in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Oversupply Driven by New Chinese Capacities

In 2024, China unveiled new capacity, spearheaded by Hengli's complex, pushing China's global output share past the 70% mark. Ex-works prices plummeted, a stark contrast to North America's spot prices, igniting a surge in exports. Meanwhile, utilization rates dipped. Western players, grappling with elevated fixed costs, began shuttering plants: Huntsman ceased operations at its Moers facility in mid-2025, and Nan Ya put its Taiwan site on hold in late 2024. In a bid to navigate these challenges, industry incumbents are now focusing on high-purity molten supplies and specialty copolymers, areas where competition from China remains limited.

Stricter OECD Benzene-Emission Caps Raising Compliance Cost

In response to EPA NESHAP and similar EU regulations, which impose benzene limits, units utilizing the benzene route have been compelled to adopt oxidizers and implement continuous monitoring. These measures have escalated operating costs and incurred significant capital expenditure. Consequently, this financial burden has led Huntsman and Nan Ya to shutter their plants and has dissuaded the establishment of new benzene-based facilities. Reflecting this trend, every capacity announced post-2024—including Hengli in China, ABP in Oman, and Indian Oil’s proposed unit in Panipat—has pivoted to n-butane oxidation, signaling a pronounced shift away from benzene technology.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Unsaturated Polyester Resin Dominance Reflects Construction and EV Composites Momentum

Unsaturated polyester resin secured 50.15% of the maleic anhydride market share in 2025 and is tracking a 4.98% CAGR to 2031, ahead of the overall market. European regulations are pushing for the use of recycled-PET blends. In North America, electric vehicle (EV) battery enclosures are utilizing maleic anhydride for each vehicle. These applications act as a buffer, shielding volumes from the cyclical downturns often seen in commodity resins. Demand for 1,4-BDO is on an annual growth trajectory, driven by investments in spandex and PBT across Asia. While the usage of lubricant additives has seen a decline as combustion engines wane, maleic anhydride copolymers are thriving. These copolymers, utilized in water treatment and bio-based packaging, are helping to mitigate the downturn in lubricants. Additionally, fumaric and malic acid derivatives are witnessing steady annual growth, primarily fueled by their use as beverage acidulants.

Specialty products, despite their lower volumes, command significant margins. For instance, bio-based succinic-acid copolymers are achieving impressive premiums in the premium packaging sector. Producers are strategically tapping into these niche markets to navigate the challenges of oversupply. Notably, Japanese research and development is making strides, focusing on the furfural-route maleic anhydride and its downstream green copolymers. This dual landscape not only solidifies unsaturated polyester's central role in the maleic anhydride market's revenue but also highlights the diversification of profit pools through its derivatives.

By Raw Material: N-Butane Route Ascendancy Driven by Yield, Cost, and Regulatory Advantages

The n-butane route dominated 70.45% of production in 2025 and is projected to grow faster than the overall maleic anhydride market. Butane oxidation eliminates benzene emissions and captures co-product hydrogen, delivering lower cash costs and simpler permitting. BASF's tri-leaf catalyst boosts yield and reduces reactor pressure drop, translating to significant savings, especially with energy being the second-largest variable cost.

Benzene-based production, though declining in share, is forecast to grow at a 4.72% CAGR through 2031, faster than the overall market, because surviving benzene-route plants are concentrated in integrated petrochemical complexes where benzene is a low-cost byproduct of naphtha cracking and where producers have already amortized compliance investments. Surviving benzene units remain competitive only where benzene is an internal cracker by-product, for example, Huntsman’s U.S. Gulf Coast sites co-located with UPR reactors. Even there, continued operation hinges on already-amortized scrubbers.

By Physical Form: Molten Grade Gains Traction as Integrated Producers Co-Locate

Solid forms (flake and prill) accounted for 60.78% of the 2025 volume because they store and ship easily across oceans. Molten supply, though smaller, is climbing at 4.93% CAGR thanks to integrated resin complexes in Illinois,

In Kuantan and Yantai, heated pipelines and railcars have managed to reduce energy consumption in packaging and re-melting. This reduction is particularly significant given that carbon pricing in Europe is projected to increase. Molten distribution has an economic radius, leading to a concentration of uptake in areas where UPR plants are adjacent to maleic anhydride reactors. Europe, however, is falling behind. The continent's fragmented resin plants find it uneconomical to invest in dedicated hot-tank logistics, resulting in a dominance of flakes in EU trade.

By End-User Industry: Construction Leads, but Automotive and Electronics Diversify Demand

Construction consumed 62.23% of the maleic anhydride market size in 2025 and is growing at a 4.78% CAGR to 2031. India's infrastructure initiatives and the EU's push for a circular economy are fueling this growth. The automotive sector is reaping the rewards of a surge in demand for EV-driven composites and parts, thanks to the USMCA regulations. In the electronics realm, there's notable growth largely driven by the demand for connectors and sensor housings, specifically those made from PBT sourced from BDO. While the food and beverage and specialty chemicals sectors collectively represent a smaller portion of the market, they are witnessing stable growth, bolstered by regulations. This stability helps insulate overall demand from the declining trend of oil additives in ICE lubricants.

Geography Analysis

Asia-Pacific held 69.45% of global volume in 2025 and advances at a 4.66% CAGR to 2031. Hengli alone boosts China's output, but with utilization rates lingering around 70%, export pressures remain pronounced. Indian Oil's project in Panipat signals India's pivot from a 70% reliance on imports to a stride towards self-sufficiency. Meanwhile, Japan and South Korea are channeling efforts into high-purity and bio-based research and development, setting the stage for a commercial leap into furfural routes after 2028.

North America is on a growth trajectory, buoyed by EV production and USMCA content stipulations. New butane facilities in Illinois and West Virginia are dedicated to in-house resin production, and Gulf Coast benzene units operate solely where scrubbers have seen their depreciation. Selling prices in the region often surpass Chinese exports, underscoring the logistics and purity premiums commanded.

Europe, holding a share of demand, is expanding at a more tempered pace, grappling with energy-price challenges and stringent benzene-emission regulations. However, Europe's surge in recycled-PET composites and the impending rollout of digital passports provide a cushion for the maleic anhydride market against the influx of Asian imports. South America and the MEA region see strategic investments like ABP's plant in Oman, which capitalizes on affordable butane to cater to the resin markets in Africa and the Middle East that have long been underserved.

Competitive Landscape

The maleic anhydride market is moderately fragmented. Chinese oversupply has forced Western exits. Survivors pivot to value-added niches. BASF’s Zhanjiang Verbund integrates a steam cracker, a maleic anhydride unit, and downstream oxo-C4 units to capture integrated margins. Regionally, PETRONAS Chemicals bought BASF’s 113 kt Kuantan plant to supply ASEAN molten demand, and ABP’s Oman unit serves Middle East composites. Indian Oil’s Panipat plant will mitigate India’s import reliance and supply its growing construction segment. Technology leadership - tri-leaf catalysts, AI controls, and molten logistics - defines cost positions, and the pivot to specialty copolymers and bio-based derivatives differentiates margin performance in an otherwise oversupplied maleic anhydride market.

Maleic Anhydride Industry Leaders

Polynt S.p.A.

Huntsman International LLC

Mitsubishi Chemical Group Corporation

INEOS AG

Wanhua

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: TCL Specialties USA has completed Phase I of its USD 200 million plant in New Martinsville, West Virginia, increasing its maleic anhydride production capacity by 40,000 tons per year. This expansion is expected to strengthen the supply chain and meet the growing demand in the maleic anhydride market.

- August 2024: BASF and UPC Technology have signed a memorandum of understanding (MoU) to establish a long-term collaboration on maleic anhydride catalysts and implement carbon-reduction initiatives. This partnership is expected to drive innovation and sustainability in the maleic anhydride market, enhancing its growth potential.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the maleic anhydride market as all newly produced solid and molten grades obtained mainly through n-butane or benzene oxidation and then sold for downstream uses such as unsaturated polyester resins, 1,4-butanediol, lubricant additives, copolymers, and various specialty acids.

Scope exclusion: Internal captive consumption that never enters merchant trade is left outside our sizing.

Segmentation Overview

- By Product Type

- Unsaturated Polyester Resin

- 1,4-Butanediol

- Lubricant Additives

- Maleic Anhydride Copolymers

- Malic Acid

- Fumaric Acid

- Alkyl Succinic Anhydrides

- Surfactants and Plasticizers

- Other Product Types

- By Raw Material

- N-Butane

- Benzene

- By Physical Form

- Solid (Flake / Prill)

- Molten

- By End-user Industry

- Construction

- Automobile

- Electronics

- Food and Beverage

- Oil Products

- Personal Care

- Pharmaceuticals

- Agriculture

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Structured calls with producers, resin formulators, composite part fabricators, regional chemical distributors, and trade-association technologists let us check shipment trends, typical contract prices, feedstock switches, and inventory cycles across Asia, North America, Europe, and the Middle East. Insights from these interviews validate secondary signals and fine-tune model assumptions on operating rates and end-user substitution tendencies.

Desk Research

We start with trade and production snapshots from public statistics issued by entities such as UN Comtrade, U.S. Energy Information Administration, Eurostat PRODCOM, and China Customs, which help our team align export-import flows with declared plant capacities. Macroeconomic cues, OECD construction spending, OICA vehicle output, and World Bank polymer indices guide demand pool calibration. Company 10-Ks, investor decks, and major plant environmental filings close early data gaps. When deeper corporate intelligence is essential, Mordor analysts access paid datasets like D&B Hoovers for revenue splits and Dow Jones Factiva for timely shutdown or expansion alerts. This list is illustrative; many other secondary sources are routinely consulted.

Market-Sizing & Forecasting

We apply a top-down and bottom-up blend: global production capacity, utilization, and net trade reconstruct apparent consumption, which is then cross-checked with sampled average selling price × volume roll-ups from key suppliers. Variables such as n-butane price spreads over benzene, quarterly UPR off-take ratios, residential floor-space completions, and automotive sheet-molding compound penetration drive our multivariate regression forecast. Where bottom-up invoices are partial, regional growth factors derived from construction permits and vehicle build statistics bridge remaining gaps before final reconciliation.

Data Validation & Update Cycle

Our model passes two internal review loops that flag outliers against historical series and peer metrics. Updates occur annually, with interim refreshes triggered by capacity additions, feedstock shocks, or regulatory swings, ensuring clients receive an up-to-date baseline before every delivery.

Why Mordor's Maleic Anhydride Baseline Commands Reliability

Published figures often diverge because providers pick different unit bases, treat captive output differently, or refresh on uneven schedules. We, at Mordor Intelligence, report the full merchant market tonnage and revisit drivers every year, which lowers revision risk for users.

Key gap drivers include differing inclusion of captive BDO-integrated output, currency conversion dates, assumed average selling prices, and whether benzene-based units running at low rates are counted as 'available' supply.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 3.18 million tons (2025, volume) | Mordor Intelligence | - |

| USD 4.57 billion (2024) | Global Consultancy A | Uses value, applies fixed ASPs, counts captive output as sold |

| USD 3.36 billion (2025) | Industry Publishing B | Omits idle Chinese capacity, older forecast refresh cadence |

In sum, our disciplined scope selection, verified operating-rate inputs, and annual refresh give decision-makers a balanced, transparent baseline that can be replicated with clear steps. Mordor analysts size 2025 demand at 3.18 million tons. Global Consultancy A places 2024 value at USD 4.57 billion. Industry Publishing B estimates 2025 value at USD 3.36 billion.

Key Questions Answered in the Report

What is the forecast size of the maleic anhydride market in 2031?

Global volume is projected to reach 3.98 million tons by 2031, expanding at a 4.28% CAGR from 3.23 million tons in 2026.

Why is the n-butane route gaining share over the benzene route?

N-butane oxidation offers higher yields, lower feedstock cost, and avoids benzene-emission compliance expenses, leading to a 70.45% share in 2025.

How does EV production influence maleic anhydride demand?

In North America, as EV output rises, so does the regional consumption of sheet-molding-compound panels, which each EV utilizes with maleic anhydride.

Which region adds the most new capacity?

In 2024, China emerged as the leading contributor to global capacity expansion, primarily driven by Hengli's unit.

What strategic shift are incumbents making to protect margins?

Producers focus on specialty copolymers, molten supply, and bio-based derivatives that command price premiums over commodity grades.

Page last updated on: