Laundry Drying Cabinets Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

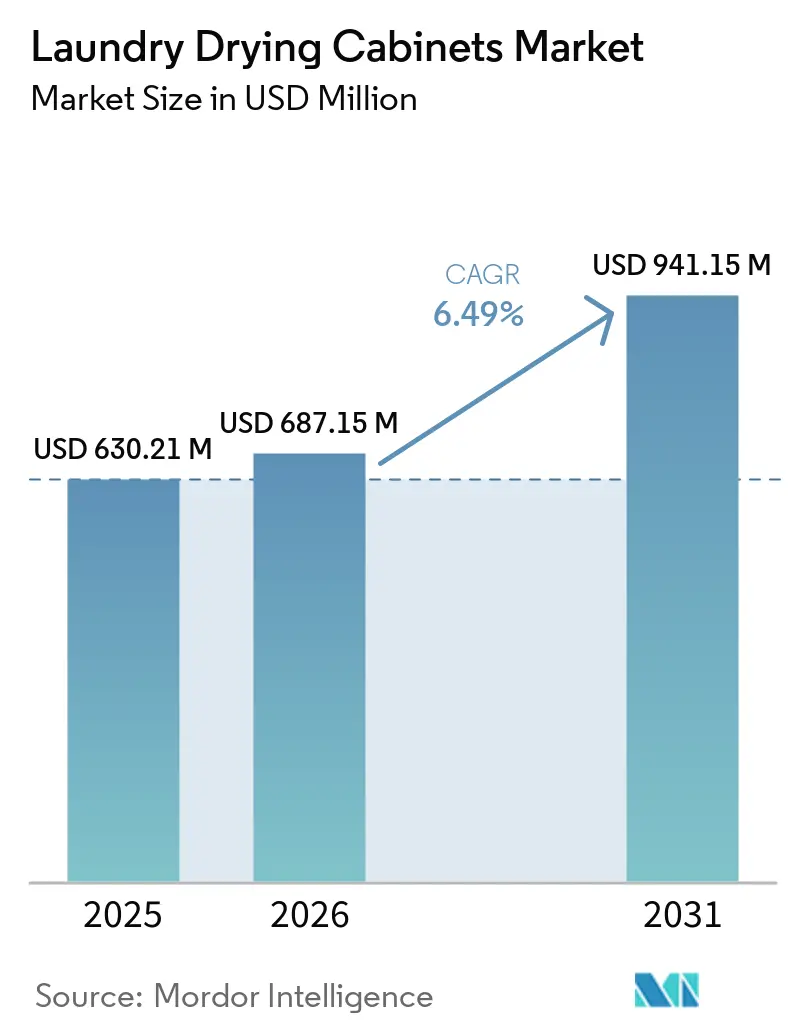

| Market Size (2026) | USD 687.15 Million |

| Market Size (2031) | USD 941.15 Million |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laundry Drying Cabinets Market Analysis by Mordor Intelligence

The laundry drying cabinets market size is expected to increase from USD 630.21 million in 2025 to USD 687.15 million in 2026 and reach USD 941.15 million by 2031, growing at a CAGR of 6.49% over 2026-2031. While the broader laundry appliances segment is growing faster, this category's slower pace underscores its niche role and also highlights its steady advancement, especially as energy-efficiency standards expand globally. Within the laundry drying cabinets market, heat pump models that cut energy use near 40% versus vented systems are shaping both commercial replacement decisions and residential upgrades in compact homes that favor ventless, integrated installations. Standard updates for firefighter PPE care and more hospital and hotel on-premise laundry capacity strengthen institutional demand that values gentle drying and throughput efficiency [1]NFPA, “NFPA 1850 Standard,” National Fire Protection Association, nfpa.org. Regional dynamics amplify competition, with Europe ahead in installed base and Asia-Pacific gaining on premium garment-care awareness and expanding distribution reach by leading OEMs. Channel mix is also evolving as digital journeys improve product discovery and technical education for first-time buyers while showrooms continue to influence decisions through live demonstrations of quiet, ventless operation.

Key Report Takeaways

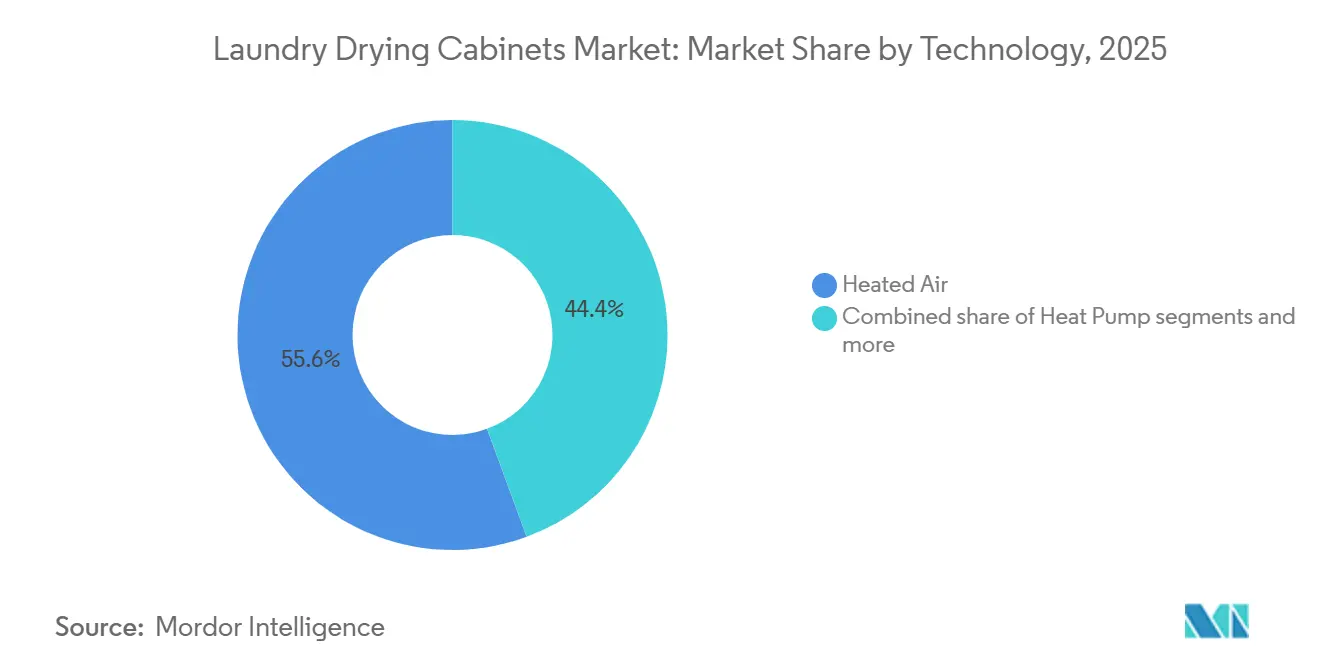

- By technology, heated-air cabinets led with 55.61% of the laundry drying cabinets market share in 2025, while heat pump variants are projected to grow at 7.52% CAGR through 2031.

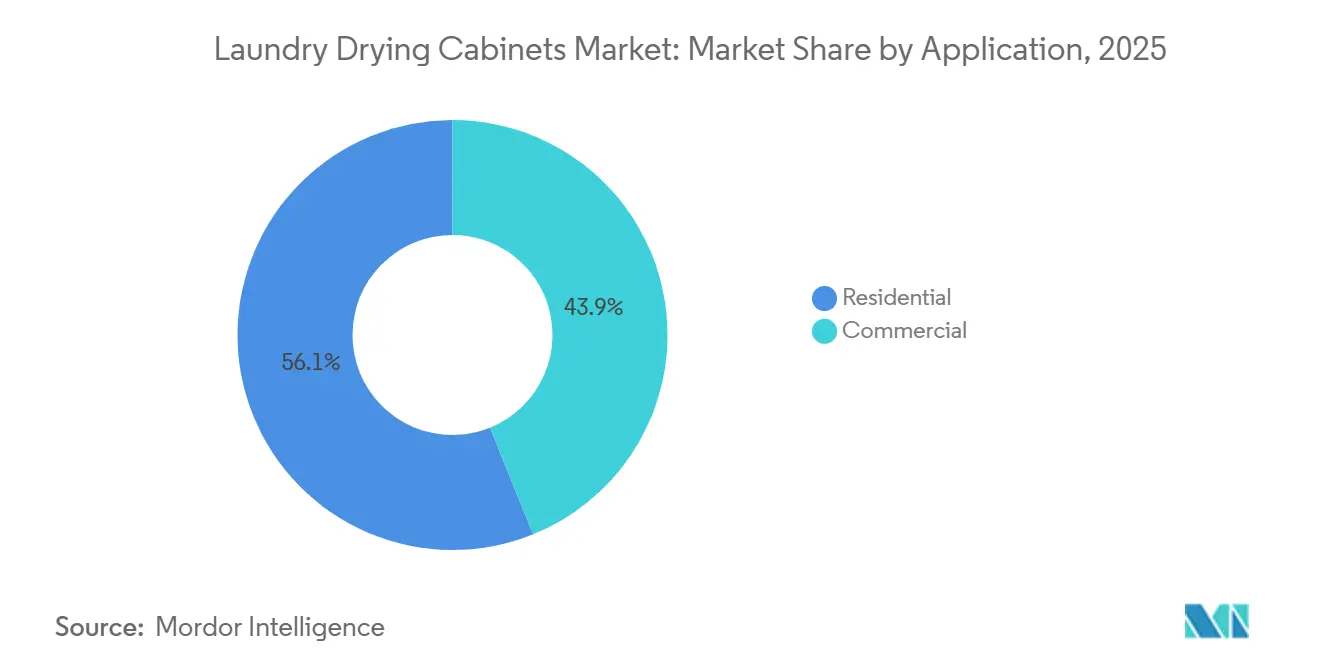

- By application, residential accounted for a 56.12% share in 2025, and commercial and industrial installations are forecast to expand at an 8.65% CAGR through 2031.

- By installation type, freestanding units captured 63.23% in 2025, and built-in or wall-mounted formats are set to advance at 7.67% CAGR over 2026-2031.

- By distribution channel, offline retail represented 71.43% of 2025 sales, with online channels growing at 9.52% annually.

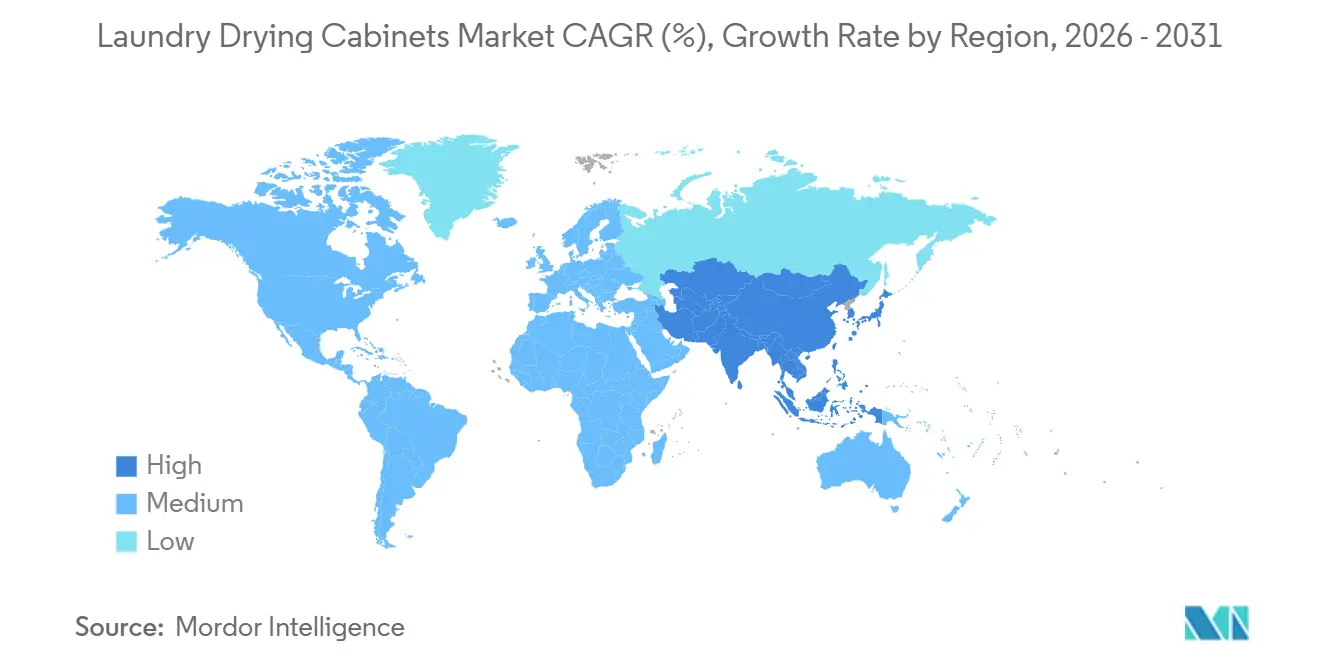

- By geography, Europe commanded 44.41% of 2025 revenue, and Asia-Pacific is expected to post the fastest growth at 10.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laundry Drying Cabinets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficiency mandates favor heat-pump cabinets | + 1.8% | Europe, North America, and early Asia-Pacific adopters | Medium term (2-4 years) |

| Growth in professional laundry, hospitality, healthcare, and PPE care | + 1.5% | Global, concentrated in North America, GCC, and core Asia-Pacific | Long term (≥ 4 years) |

| Urban compact living boosts built-in/wall-mounted adoption | + 1.2% | Asia-Pacific megacities, Europe historic zones, and select South America cities. | Medium term (2-4 years) |

| E-commerce expands retail reach and product discovery | + 0.8% | National, with early gains across North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Fire and rescue PPE standards require gentle, cabinet drying | + 0.7% | North America, Europe, with spill-over to ANZ and GCC | Long term (≥ 4 years) |

| Dehumidifier-tech cabinets address no-vent and IAQ needs | + 0.5% | Asia-Pacific high-humidity zones and tropical markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficiency Mandates Favor Heat-Pump Cabinets

The European Union’s ecodesign framework, taking effect in mid-2025, raises the bar on dryer energy performance, which benefits heat pump drying cabinets because they deliver A-to-C label outcomes without external venting and with lower wattage draw in real-world use [2]Energimyndigheten, “EU Ecodesign and Energy Labeling Updates,” Swedish Energy Agency, energimyndigheten.se. Commercial buyers are moving toward heat pump replacements as models such as PODAB’s ProLine TS63 HP demonstrate low kWh per cycle at relevant capacities, a combination that reduces operating costs while supporting longevity targets for high-duty laundry rooms. Targeted stimulus continues to shape payback math for hotels and restaurants, with national programs in Europe offsetting capital outlays per kilogram of cabinet capacity and improving the affordability of first-time heat pump deployments. In North America, electrification rebates encourage ventless and efficient laundry solutions in multifamily settings where space and building codes limit ducted installs, which supports steady adoption of cabinet formats where tumble dryers are less practical. Refrigerant policy is accelerating the shift to R290 propane systems in heat pump cabinets, and suppliers highlight significant CO₂ emission reductions against legacy refrigerants as well as simpler compressor architectures that help narrow retail price gaps. Across the laundry drying cabinets market, these regulatory and cost-of-ownership forces collectively underpin the technology mix shift toward heat pump designs over the forecast horizon.

Growth in Professional Laundry, Hospitality, Healthcare, and PPE Care

Institutional buyers are scaling cabinet fleets to align with higher throughput targets and stricter textile-care protocols in hospitals, hotels, and multi-tenant properties, and they often bundle predictive maintenance through OEM connectivity to raise uptime and reduce service costs. Commercial growth outpaces residential, supported by lodging operators and co-living brands that value ventless placement flexibility, fabric protection, and lower energy budgets per kilogram dried in daily operations. Energy-optimized hotel programs reference platforms such as Electrolux Professional Line 6000, which offers auto-stop drying at defined moisture thresholds and competitive cycle times at low kWh per kilogram that improve linen-turnaround efficiency. Healthcare laundry rooms have sustained higher PPE volumes than pre-pandemic baselines and report better textile longevity when cabinets are used at controlled temperatures rather than mechanical tumbling, which aligns with the need to preserve coatings and structural integrity through repeated cleaning cycles. Fire-service operations underscore the case for cabinet drying due to post-wash temperature limits and the absence of mechanical abrasion, and specialized units from Rescue Intellitech and others support interior and exterior drying of turnout gear within safe heat thresholds. As OEMs expand telemetry and fleet-management features into these commercial workflows, buyers benefit from shorter repair windows and more predictable service schedules across multi-site deployments.

Urban Compact Living Boosts Built-in/Wall-Mounted Adoption

Developers and homeowners in dense urban cores favor ventless, integrated cabinets that fit constrained footprints and operate at low noise levels suitable for studios and small apartments. Product design is evolving to serve this need, with slim heat pump models that fit 600 mm-width cabinetries, offer long hanging lengths within narrow frames, and use R290 refrigerant to reduce environmental impact while keeping sound levels in a typical conversation range. Built-in and wall-mounted formats have become the default choice in many renovation projects where ducting is restricted, and closed-loop airflow makes these configurations attractive in utility closets, bathrooms, and kitchens with limited mechanical access. Wet-zone safety and ingress protection criteria are common in kitchen and bath placements, and Nordic-origin cabinets incorporate relevant protections across IP and electrical classes to support flexible installation. As more residential projects target all-electric mechanical systems for sustainability goals, ventless cabinets fit well with induction cooktops and heat pump HVAC, reinforcing a smooth shift from gas-powered laundry and eliminating duct penetrations. These factors collectively lift the built-in and wall-mounted share within the laundry drying cabinets market as urbanization patterns continue.

E-Commerce Expands Retail Reach and Product Discovery

Direct-to-consumer and multi-brand web stores now feature deeper product education than legacy retail displays, and buyers engage with cabinet-specific visuals and specification comparisons that simplify first-time category evaluation. Service bundling improves digital conversion in markets where installers and parts networks are sparse, as seen in NIMO Droogkasten’s annual preventive maintenance package, priced at USD 108.9 (EUR 99), which helps sustain performance and drive repeat relationships over time. European Union energy labeling rules also introduce scanning and QR code workflows for retail, and EPREL-linked pages allow shoppers to verify performance data on their phones before purchase, making attributes such as energy class and noise more transparent online and in-store. Showrooms continue to play a role by demonstrating quiet operation and ventless setup, helping explain differences versus tumble dryers in a format that highlights fabric care and placement flexibility. As brands refine omnichannel journeys and standardize merchandising, the laundry drying cabinets market benefits from wider awareness and more consistent category positioning across geographies. The net effect is a more balanced channel mix with growing online discovery and strong offline influence at the point of demonstration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront prices for advanced models | - 0.9% | Global, with acute pressure in price-sensitive markets | Medium term (2-4 years) |

| Low awareness vs. tumble dryers outside Nordic markets | - 0.6% | North America, many Asia-Pacific and South American countries | Long term (≥ 4 years) |

| Vented installs constrained by exhaust/space requirements | - 0.4% | Europe, Asia-Pacific dense cores, older North American stock | Medium term (2-4 years) |

| Gentle/dehumidifier cabinets have longer cycle times | - 0.3% | Global, especially throughput-driven commercial sites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Prices for Advanced (Heat-Pump/IoT) Models

Retail premiums for heat pump cabinets remain meaningful versus conventional heated-air options, which slows adoption in cost-sensitive households and smaller commercial sites even when lifetime energy savings are favorable. Nordic distributors illustrate the pricing framework with installed heat pump models offered through monthly financing that spreads capital outlays over multi-year terms, making total cost more manageable for small operators [3]Berg & Dahl, “Electrolux Line 6000 Pricing and Financing,” Berg & Dahl, berg-dahl.no. Connectivity boxes, fleet dashboards, and sensor-based auto-stop programs add value to commercial buyers but can raise list prices for residential shoppers who may not need usage analytics. OEMs emphasize durability, long component lifespans, and rebuildable heat pump modules that target 20 years or more of service, positioning cabinets as investment-grade assets rather than short-cycle consumer appliances. As refrigerant changes simplify compressor assemblies and volumes scale, manufacturers expect smaller differentials versus heated-air units, which could improve conversion rates during the replacement cycle. Until then, the laundry drying cabinets market continues to face upfront price friction in markets without strong subsidies or financing penetration.

Low Awareness vs. Tumble Dryers Outside Nordic Markets

Category awareness trails tumble dryers in many regions, and retail displays still devote much more space to conventional drum-based systems, which can limit exposure and salesperson familiarity with cabinet-specific benefits. In contrast, Nordic multi-family residences have normalized cabinet use in shared laundry rooms and apartment installations, which sustains a consistent replacement base and higher confidence in cabinet drying for delicate textiles. OEMs and resellers respond with step-by-step explainers, configuration visuals, and lifecycle-cost comparisons that clarify energy and fabric-care advantages for first-time buyers. Community and builder partnerships also help normalize cabinets in new projects, as seen in markets where developers integrate ventless solutions to meet electric-only design goals and low-noise requirements. The broadening of content, demos, and service offers contributes to incremental progress, yet closing the awareness gap remains a multi-year task for the laundry drying cabinets market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Heat Pumps Ascend as R290 Costs Converge

Heated-air cabinets held 55.61% of the global base in 2025, while heat pump variants are projected to expand at 7.52% CAGR through 2031 as buyers prioritize energy performance and ventless flexibility in the laundry drying cabinets market. Energy per cycle on modern heat pump models, such as PODAB’s TS series, compares favorably against heated-air equivalents, which supports retrofit decisions in commercial rooms where electricity use per kilogram adds up across shifts [4]PODAB, “TS-Series Heat Pump Specifications,” PODAB, podab.com. Dehumidifier cabinets present a niche for overnight residential drying and for apartments that want combined laundry and air-quality benefits, although their longer cycles limit broad commercial appeal. Refrigerant policy has guided the transition toward R290 propane compressors across heat pump portfolios, and OEM disclosures cite material CO₂ reductions and simpler circuits that help narrow cost differentials with heated-air designs. Slim, quiet heat pump cabinets designed for integrated kitchens or bath closets are gaining share in urban renovations, and they strengthen the category’s fit for sound-sensitive residences.

As a result, the technology mix continues to tilt toward heat pumps as the preferred all-rounder in the laundry drying cabinets market, with heated-air cabinets retained where cycle speed dominates buying criteria, such as hotel linen programs with tight shift rotations. Dehumidifier units retain clear use cases in tropical or temperate markets for plug-and-play installs and indoor humidity control, even if their capacity range is smaller than heat pump alternatives. Regulatory changes in Europe steer shoppers who search for ventless dryers toward cabinet categories that deliver gentler treatment of fabrics at lower wattage than many washer-dryer combos, which creates halo effects in adjacent appliance aisles. The net effect lifts the technology profile of the laundry drying cabinets market and sets a multi-year path for broader R290 adoption across price points.

By Installation Type: Built-in Gains Mirror Micro-Apartment Surge

Freestanding cabinets accounted for 63.23% of the installed base in 2025, reflecting legacy laundry-room layouts and mobility needs in rental markets that still dominate absolute volumes in the laundry drying cabinets market. Built-in and wall-mounted formats are projected to grow at 7.67% CAGR, helped by compact kitchens and bathrooms where ventless, quiet cabinets allow integration without ducting or structural changes. Configurations with reversible racks and adjustable feet make semi-permanent installs more practical for co-living properties that turn tenants frequently while keeping shared amenities intact. Premium towers and large apartments incorporate cabinets behind wardrobe doors to keep aesthetics clean and to avoid transferring wear to delicate garments that suffer in drum-based dryers.

In commercial and public-safety settings, open-front designs enable quick hanging of gear without door actuation, which reduces contamination risk between cycles and speeds handling during busy shifts. As OEMs expand connectivity and reduce mean time to repair with remote diagnostics, the case for fixed installations in managed properties improves and lowers the total cost of ownership across multi-site portfolios. Safety and ingress-protection features support installation in wet zones, broadening placement options and simplifying renovation planning when dedicated utility space is limited. These installation trends keep the laundry drying cabinets market aligned with urban living patterns and the operational realities of institutional laundry rooms.

By Application: Commercial Propelled by Co-Living and PPE Protocols

Residential applications held 56.12% of the 2025 volume, while commercial and industrial uses are on track to expand at 8.65% CAGR through 2031, supported by hospitality, healthcare, PPE protocols, and shared amenities in co-living developments in the laundry drying cabinets market. Hotels and resorts adopt cabinet drying to preserve linens and uniforms while controlling energy per kilogram, and features such as auto-stop at target dryness points limit over-drying in daily operations. Fire departments and industrial safety teams deploy specialized cabinets for turnout gear and flame-resistant clothing that require non-mechanical drying and safe, compliant temperature limits. In hospitals and clinics, cabinet drying preserves coatings and fabric structure across repeated cleanings, which helps extend PPE lifespan compared with repeated tumbling.

Residential adoption is strongest in urban settings where compact footprints and quiet, ventless operation enable placement in closets and small bathrooms, and where e-commerce content now provides the education needed to compare cabinets versus tumble options. Growth in smart fleet management and connectivity is pronounced in commercial fleets, which favor remote diagnostics, service alerts, and program control across many locations. With subsidies for efficient equipment and rising cost-of-energy awareness, the commercial case continues to strengthen for cabinets that keep textiles functional and minimize downtime due to wear or maintenance. This pattern supports steady gains in the laundry drying cabinets market across institutional end users through 2031.

By Distribution Channel: Offline Anchors as Online Gains Share

Offline channels accounted for 71.43% of 2025-unit sales, supported by appliance showrooms where buyers see and hear cabinets in action and evaluate ventless setups alongside washers and traditional dryers in the laundry drying cabinets market. Online channels are growing at 9.52% annually, led by deeper product explainers, visualizations, and solution bundles that include installation or maintenance plans for first-time cabinet buyers. Direct service offerings have improved conversion in select markets, with NIMO Droogkasten’s annual preventive package listed at USD 108.9 (EUR 99). EPREL-linked QR codes tied to European Union energy labeling allow quick scans for verified performance figures, which makes it easier to compare sound levels, energy classes, and program options on mobile devices.

Commercial deals often run through direct OEM sales to bundle connectivity, program libraries, and accessories tailored for sectors like hospitality or firefighting, which avoids retail markups and keeps service plans unified. Retail financers and distributors are extending leasing to align with expected equipment lifespans, as seen in Nordic channels that support multi-year cabinet financing for operators that prefer predictable monthly costs. Showrooms demonstrate quiet operation and gentle airflow programs that differentiate cabinets from drum dryers, while digital channels supplement discovery and specification checks. As brands standardize omnichannel journeys, the laundry drying cabinets market benefits from consistent education and better fit-for-purpose product selection across buyer types.

Geography Analysis

Europe held 44.41% of 2025 revenue and remains the anchor region due to long-standing cabinet adoption in multi-dwelling buildings and strong compliance orientation around refrigerants and energy labeling in the laundry drying cabinets market. Policy momentum that favors efficient, ventless solutions strengthens heat pump cabinets across replacement cycles, and OEMs have adapted cabinets to meet noise, ingress, and refrigerant criteria across European codes. Nordic-origin models set performance references for IP ratings, airflow uniformity, and closed-loop operation, which sustain durable installed bases and long service lifespans. As post-2025 assortments re-balance toward heat pumps in adjacent dryer categories, cabinets gain from shoppers seeking gentler, quieter, and ventless garment care.

Asia-Pacific is the fastest-growing region at 10.41% CAGR through 2031, propelled by premium garment-care awareness and rising penetration of ventless laundry solutions in tier-1 and tier-2 urban markets that value space efficiency. OEM distribution has expanded through regional partners to improve availability and service, and portfolios include compact, low-noise cabinets designed for apartments and condominiums. In parallel, public-safety and industrial segments in mature Asia-Pacific markets are adopting cabinet solutions aligned with temperature limits and non-mechanical drying to protect specialized textiles, which brings commercial momentum to the region. The interplay between dense living, energy-conscious consumers, and ventless installation supports a favorable trajectory for the laundry drying cabinets market in Asia-Pacific.

North America is growing from a lower installed base and is influenced by policy incentives for efficient electric appliances, tighter multifamily codes, and standards-driven PPE care in fire and industrial applications. The revision of NFPA guidance around post-wash temperature limits and the need for gentle handling favor cabinet adoption in emergency services and utilities, as cabinets eliminate mechanical abrasion and help protect gear longevity. Manufacturers are refreshing North American lineups with heat pump cabinets that include auto-stop, humidity tracking, and standardized accessories for gloves, boots, and PPE, which broadens use cases beyond general household drying. Distributor and retailer participation has increased as online and in-store merchandising improves, making the laundry drying cabinets market more visible to mainstream buyers across the United States and Canada.

Oceania features complementary momentum driven by premium laundry positioning and the expansion of cabinet solutions into commercial venues that serve outdoor apparel, tourism, and safety wear, matched by local parts support. In select European and Nordic markets, retail partners have improved delivery and install lead times for flagship models, and price transparency across web listings helps buyers plan upgrades. Distributors across Benelux and nearby markets stock a tiered range of cabinets that address both residential and professional needs, which makes conversion easier for first-time category entrants. Across regions, the laundry drying cabinets market benefits from policy alignment, ventless installation advantages, and increasingly robust service ecosystems.

Competitive Landscape

The laundry drying cabinets market features a focused group of global and regional OEMs that compete across residential, commercial, and specialist safety applications, with Europe-origin brands prominent in heat pump engineering and long-life cabinet construction. Electrolux Professional, PODAB, NIMO, Miele Professional, and Primus anchor many portfolios, and their product lines emphasize durability, modular serviceability, and compliance with noise and ingress criteria for flexible placement. Challenger brands from Asia compete on price in residential channels, while incumbents stress 20-year design lives, rebuildable pump modules, and extended warranties that lower ownership costs for commercial fleets. No single firm dominates across all use cases and geographies, and product differentiation often rests on safety certifications, accessories for sector-specific garments, and service-network breadth.

Technical roadmaps are consolidating around R290 refrigerants, humidity-tracking auto-stop, and connectivity that delivers fleet diagnostics and remote program updates to large customers. At the same time, leading laundry brands invest in fabric-care research that informs airflow patterns, rack geometry, and temperature controls that reduce textile wear, even as advanced drum-based dryers maintain separate innovation tracks for motion control and materials. OEMs also target accessory ecosystems for gloves, boots, and PPE, which broaden the functional scope of cabinets and facilitate standard operating procedures in safety-critical environments. The combination of energy performance, textile protection, and fleet management features remains central to competitive strategies within the laundry drying cabinets market.

Growth opportunities center on retrofit paths from vented to closed-loop operation, compact form factors for small balconies and utility closets, and antimicrobial solutions that extend the usable life of uniforms and PPE when compared with tumble drying. Dehumidifier cabinets also pressure incumbent narratives on efficiency for small residential loads, which has prompted R&D into hybrid architectures that target shorter cycles while preserving low energy use. Connectivity is more prevalent in commercial fleets than in households, but as service ecosystems mature, residential features may expand to include more diagnostics and guided maintenance. Compliance leadership around NFPA standards and ATEX classifications provides a moat in contracts with fire, petrochemical, and utilities customers, and favors brands with proven testing and certification processes.

Laundry Drying Cabinets Industry Leaders

Electrolux Professional

Nimo (Nimoverken AB)

ASKO Appliances (Hisense)

Primus (Alliance Laundry Systems)

PODAB AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: PODAB listed the PrimeLine TS4 VP and ProLine TF9 VP on its Swedish website, featuring compact 4 kg and 10 kg heat pump cabinets optimized for energy efficiency and small laundry rooms.

- February 2026: Hedins VVS listed the NIMO Easy Dryer 1900 BOD at USD 888.9 (SEK 9,346) and the NIMO Sensor Dryer 1900 at USD 1,035.8 (SEK 10,903) and promoted fast shipping and installation services for cabinet buyers.

- January 2026: Electrolux Professional launched updated Line 6000 heat pump drying cabinets, including the DC6-10HP at 2.6 kWh per 10 kg load with auto-stop programs, and Nordic distributor Berg & Dahl listed pricing at USD 5,605 (NOK 59,000) using an average 2026 exchange rate for clarity.

- December 2025: NIMO introduced the Passad DC 60 heat pump drying cabinet using R290 refrigerant, operating near 55°C with low sound output and a ventless closed-loop design.

Global Laundry Drying Cabinets Market Report Scope

| Heated Air |

| Heat Pump |

| Dehumidifier |

| Freestanding |

| Built-in / Wall-Mounted |

| Open-Front |

| Residential |

| Commercial |

| Industrial |

| B2C/Retail | Multi-brand Stores (big box retailers, department stores, electronics chain, home improvement centers) |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B/Directly from the Manufacturers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Technology | Heated Air | |

| Heat Pump | ||

| Dehumidifier | ||

| By Installation Type | Freestanding | |

| Built-in / Wall-Mounted | ||

| Open-Front | ||

| By Application | Residential | |

| Commercial | ||

| Industrial | ||

| By Distribution Channel | B2C/Retail | Multi-brand Stores (big box retailers, department stores, electronics chain, home improvement centers) |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Directly from the Manufacturers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size and growth rate of the laundry drying cabinets market to 2031?

The laundry drying cabinets market size is expected to reach USD 941.15 million by 2031, growing at a 6.49% CAGR over 2026-2031.

Which technology is set to grow fastest in laundry drying cabinets?

Heat pump cabinets are forecast to post a 7.52% CAGR through 2031 as efficiency and ventless installation drive upgrades in both residential and commercial use.

Which regions lead and grow fastest in laundry drying cabinets?

Europe led with 44.41% of 2025 revenue, while Asia-Pacific is the fastest-growing region at 10.41% CAGR through 2031.

How are standards influencing cabinet adoption in emergency services?

NFPA 1850 guidance on post-wash temperature limits reinforces cabinet drying for turnout gear, promoting gentle drying and compliance in fire-service workflows.

What is the main barrier to broader cabinet adoption outside Europe?

Upfront price premiums for advanced heat pump and connected models, plus lower category awareness versus tumble dryers, remain the major hurdles in many regions.

Which applications are driving commercial demand for cabinets?

Hospitality, healthcare PPE care, and fire-service PPE programs are key growth vectors due to fabric-care needs, ventless placement, and standards compliance.

Page last updated on: