Implantable Loop Recorders Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

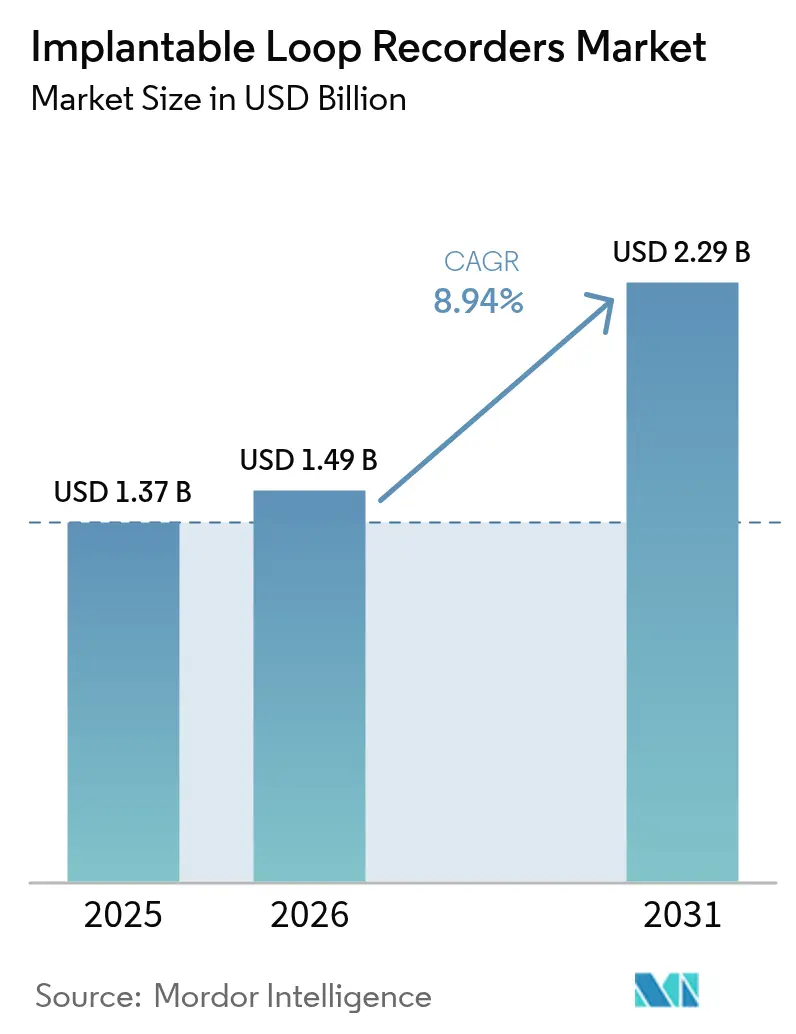

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 8.94% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

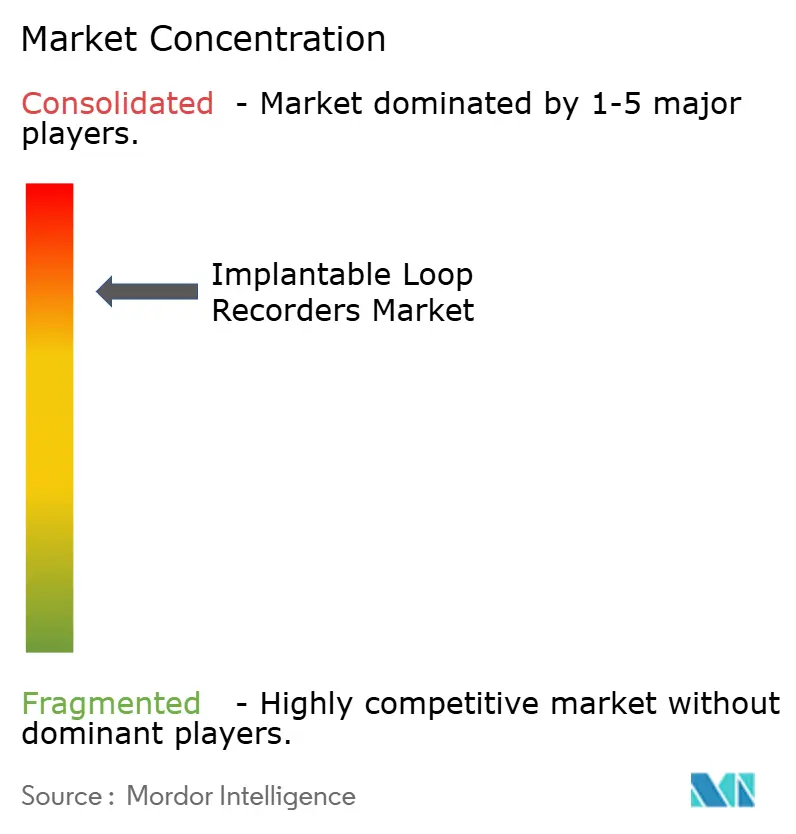

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Implantable Loop Recorders Market Analysis by Mordor Intelligence

The implantable loop recorder market size is expected to grow from USD 1.37 billion in 2025 to USD 1.49 billion in 2026 and is forecasted to reach USD 2.29 billion by 2031 at 8.94% CAGR over 2026-2031. Accelerated growth follows rising cardiovascular disease prevalence, rapid device miniaturization, and the widening of reimbursement policies that encourage long-term rhythm surveillance in outpatient and inpatient pathways. Uptake is strongest where cryptogenic stroke monitoring reveals atrial fibrillation in 28.2% of patients within 36 months, prompting earlier anticoagulation. Hospitals rely on proven clinical utility, yet demand is quickly shifting toward remote models as Bluetooth telemetry removes the need for bedside monitors. Competitive intensity rises as Medtronic, Abbott, and Boston Scientific introduce six-year battery designs, AI-driven arrhythmia analytics, and frictionless cloud connectivity.

Key Report Takeaways

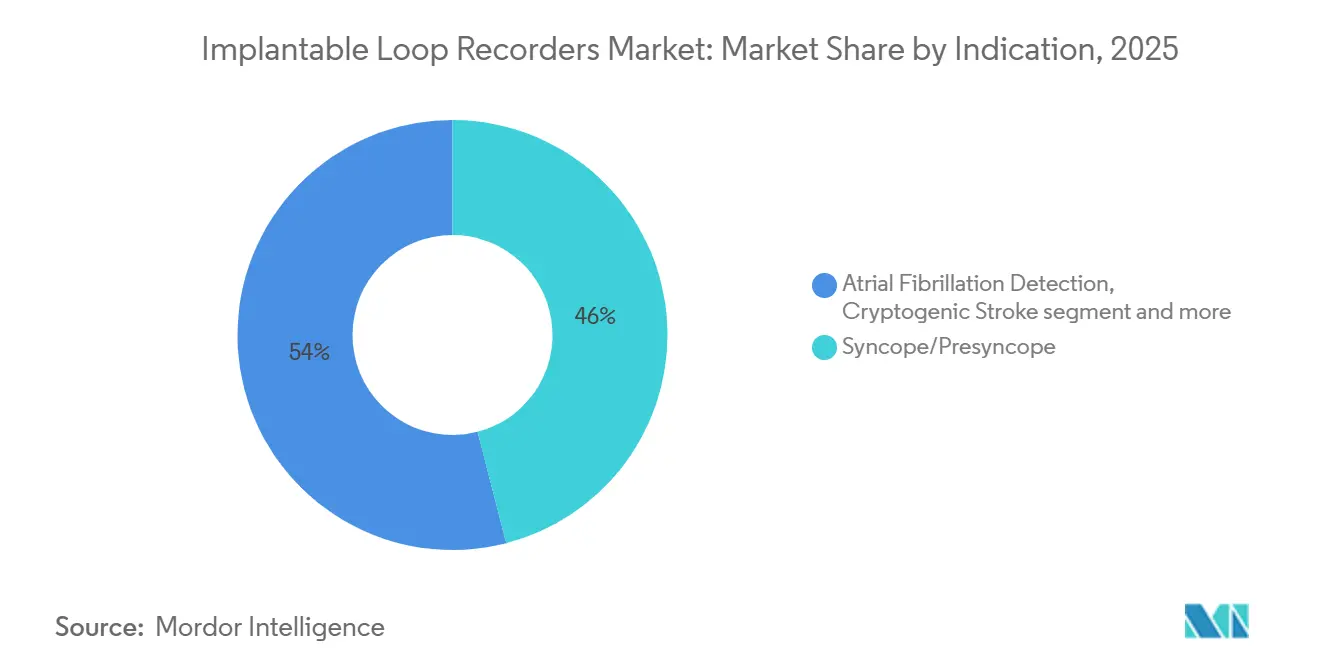

- By indication, syncope/presyncope held 45.98% of the implantable loop recorder market share in 2025; cryptogenic stroke is poised for the fastest expansion at a 10.59% CAGR through 2031.

- By end-user, hospitals commanded 62.83% revenue in 2025, while home-based and remote monitoring programs are forecast to grow at 10.97% CAGR to 2031.

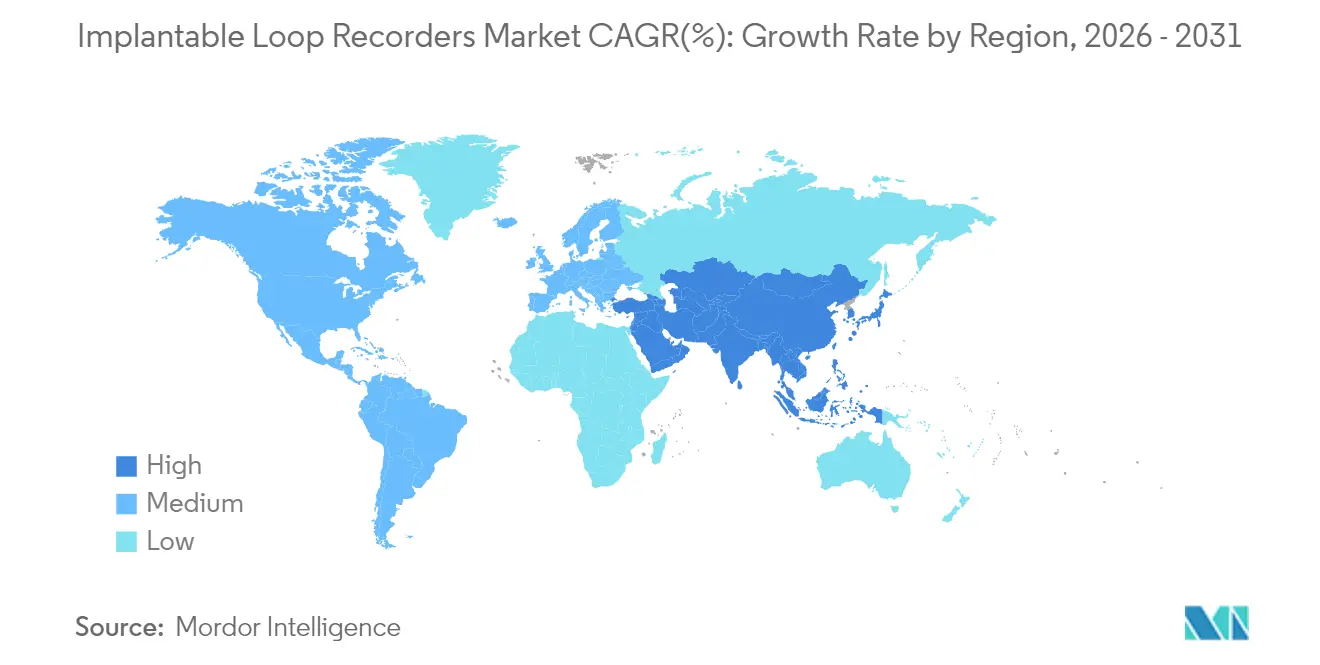

- By geography, North America contributed 46.92% of 2025 sales, whereas Asia-Pacific is projected to climb at 10.62% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Implantable Loop Recorders Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Atrial Fibrillation & Cryptogenic Stroke | +2.80% | Global, with higher impact in aging populations of North America & Europe | Medium term (2-4 years) |

| Growing Preference for Long-Term Ambulatory Rhythm Monitoring | +2.10% | Global, particularly strong in developed markets | Short term (≤ 2 years) |

| Technological Advances in Miniaturization & Bluetooth Telemetry | +1.90% | Global, led by innovation hubs in US, EU, Japan | Medium term (2-4 years) |

| Favorable Reimbursement Expansions in the US & EU | +1.50% | North America & Europe primarily | Short term (≤ 2 years) |

| AI-Enabled Predictive Analytics for Asymptomatic Arrhythmia | +1.20% | Developed markets initially, expanding globally | Long term (≥ 4 years) |

| CMS Bundled Stroke Payment Pushing Hospitals Toward IRLs | +0.80% | United States primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Atrial Fibrillation & Cryptogenic Stroke

Expanding lifetime risk of atrial fibrillation from 24.2% to 30.9% across developed regions intensifies demand for prolonged cardiac surveillance[1]Source: Marios Vizirianakis, “Temporal Trends in Lifetime Risks of Atrial Fibrillation,” BMJ, bmj.com . Implantable loop recorders detect previously hidden atrial fibrillation in 19.5% of cryptogenic stroke cases within national registries, enabling earlier secondary prevention through anticoagulation. Traditional 24-hour Holter studies miss many paroxysmal events, whereas median detection emerges 7.9 months after device insertion, underscoring the clinical value of continuous monitoring. As a result, neurologists increasingly collaborate with electrophysiologists to implant recorders in stroke units before discharge to curtail recurrent events. This epidemiological momentum underpins long-run adoption across both hospital and outpatient settings.

Growing Preference for Long-Term Ambulatory Rhythm Monitoring

Diagnostic yield rises markedly when cardiac surveillance extends from 24 hours to 7 days, amplifying premature ventricular contraction quantification accuracy. Extended monitoring devices now represent 40% of connected cardiac monitors in US clinics, while mobile telemetry contributes another 20%, indicating significant displacement of brief Holter studies. Physicians value higher arrhythmia detection in low-symptom patients, which translates into earlier therapy initiation and fewer unplanned admissions. Health systems also document economic benefits through reduced duplicate testing and shorter diagnostic journeys. These advantages align with payer incentives that reimburse single-procedure implant and multi-year data review, accelerating the transition toward continuous monitoring modalities.

Technological Advances in Miniaturization & Bluetooth Telemetry

Recent design innovations shrink implantable loop recorders to sub-3 cm profiles while extending battery life up to six years. Bluetooth Low Energy links enable real-time data export to smartphones, eliminating bedside transmitters and encouraging higher patient adherence. Motion-tolerant sensor arrays capture clear signals during exercise, overcoming prior diagnostic gaps in ambulatory settings . These improvements foster day-one activation, streamlined follow-up, and quicker clinical interventions. They also open pathways for home-based programs that rely on fast cloud uploads and automated triage dashboards, reducing staff burden in electrophysiology clinics.

AI-Enabled Predictive Analytics for Asymptomatic Arrhythmia

Deep-learning algorithms now reach 96.2% sensitivity and 94.5% specificity in atrial fibrillation detection by merging surface ECG traces with intracardiac electrograms. Predictive models forecast arrhythmia onset nearly 31 minutes in advance with 83% accuracy, giving clinicians a therapeutic window to adjust medication or schedule urgent review. AI also curtails false-positive alerts from 75% in legacy devices to 18% in next-generation platforms, trimming time spent on unnecessary reviews. Cloud-based pattern recognition integrates with hospital electronic record systems, creating a closed feedback loop in which device data informs immediate care plans. This shift from reactive to proactive arrhythmia management strengthens the implantable loop recorder market’s clinical value proposition.

Restraints Impact Analysis of Implantable Loop Recorders Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device & Implantation Costs | -1.80% | Global, particularly acute in emerging markets | Medium term (2-4 years) |

| Risk of Infection, Pocket Erosion & False-Positive Alerts | -1.20% | Global | Short term (≤ 2 years) |

| Data-Management Burden on Electrophysiology Clinics | -0.90% | Developed markets with high device penetration | Medium term (2-4 years) |

| Increasing Cybersecurity / Patient-Privacy Concerns | -0.70% | Global, heightened in regulated markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Device & Implantation Costs

Procedure fees remain a prominent barrier, with Australian reimbursement schedules listing AUD 175.75 (USD 117.8) for insertion alone, while device prices range from USD 11,329 upward for AI-enabled systems. Budget pressures intensify as US physician fee schedules project 2.93% rate cuts in 2025, squeezing hospital margins [2]Source: Centers for Medicare & Medicaid Services, “Medicare Physician Fee Schedule Final Rule 2025,” cms.gov . Many emerging markets allocate scarce cardiac funds to basic revascularization, leaving limited capacity for premium recorders despite rising cardiovascular incidence. Vendors attempt to counter pricing sensitivity through leasing models and performance-based contracts but affordability hurdles still temper adoption pace outside high-income regions.

Data-Management Burden on Electrophysiology Clinics

Although AI reduces noise, remote monitoring still generates large alert volumes that demand clinician review. Historically, three-quarters of notifications were false positives, burdening staff with time-consuming triage. Recent firmware updates cut that share to 18% yet clinics must invest in dedicated personnel for data oversight, patient counseling, and follow-up scheduling. Smaller practices, especially in rural areas, report workflow strain when expanding beyond a few dozen devices. Without scalable informatics support, some facilities hesitate to broaden implantation programs, moderating the implantable loop recorder market’s near-term uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Implantable Loop Recorders Market Segment Analysis

By Indication:

Syncope Leadership and Stroke Prevention UpswingSyncope/Presyncope retained 45.98% of the implantable loop recorder market share in 2025, driven by its high diagnostic yield over conventional tilt-table or Holter tests. Physicians consider continuous rhythm capture the gold standard when unexplained fainting threatens driving privileges or occupational safety. Implant data reveal actionable arrhythmias in up to 33% of syncope cases within 12 months, enabling pacemaker or ablation interventions that cut readmissions. The implantable loop recorder market size for syncope applications is projected to advance steadily as aging populations raise incidence of neuro-cardiogenic events.

Cryptogenic Stroke is advancing at a 10.59% CAGR, outpacing other indications through compelling evidence that 28.2% of implanted patients experience covert atrial fibrillation within three years. Stroke specialists increasingly embed recorders during index admission to accelerate anticoagulation decisions, a practice supported by updated neurology guidelines. Payers acknowledge cost offsets from avoided recurrent strokes, facilitating broader coverage. Over the forecast horizon, stroke-led growth will continue to elevate total implant volumes, narrowing the share gap with syncope.

Atrial Fibrillation Detection outside the stroke setting remains a sizeable niche where recorders confirm symptomatic palpitations when surface ECG fails. Post-procedure monitoring after pulmonary vein isolation also leverages multi-year visibility to gauge ablation success. Palpitations & Other Arrhythmias benefit from extended capture of ventricular ectopy and inherited rhythm disorders in younger cohorts who reject bulky external devices. Collectively, evolving evidence keeps all indications in positive territory, sustaining balanced portfolio demand for manufacturers.

By End-User:

Hospital Dominance and Rapid Home-Care ExpansionHospitals supplied 62.83% of 2025 implant volumes owing to in-house electrophysiology labs, anesthesia support, and immediate post-operative observation capacity. The implantable loop recorder market size for hospitals remains sizable as complex comorbid patients often require inpatient workflows. Teaching centers also run device clinics that aggregate large data sets for AI training, reinforcing centralized implantation models.

Home-based & Remote Monitoring Programs are projected to grow 10.97% CAGR through 2031, the fastest among end-users. Bluetooth telemetry and smartphone apps allow same-day discharge with automatic cloud uploads, reducing travel for elderly or rural patients. Health systems view home pathways as levers to lower emergency department visits while preserving clinical vigilance. Cardiac Centers & Clinics maintain moderate growth by specializing in arrhythmia-only services, ensuring prompt implantation within outpatient settings. Ambulatory Surgical Centers see upticks in procedure volume where payers incentivize same-day surgery, yet they rely on downstream remote monitoring networks to close the loop. Together, diversified care settings increase total channel availability and smooth device access across demographic segments.

Geography Analysis

North America Implantable Loop Recorders Market

North America accounted for 46.92% of worldwide revenue in 2025, supported by Medicare National Coverage Determinations that reimburse implants across syncope, stroke, and atrial fibrillation indications . Extensive cardiology infrastructure, high public awareness, and broad telehealth acceptance sustain volume growth. Purchasing consortia negotiate bulk pricing, but the implantable loop recorder market remains value-oriented due to outcome-based payment incentives that reward stroke avoidance and readmission reduction.

Europe Implantable Loop Recorders Market

Europe maintains consistent expansion through universal healthcare systems that emphasize preventive cardiology. Germany, the United Kingdom, and France anchor regional demand with large electrophysiology capacities and harmonized device approvals under MDR. Cross-country initiatives share registry data, accelerating evidence generation and standardizing care protocols. Southern and Eastern European states adopt implantable recorders more gradually as reimbursement parity evolves, but overall penetration keeps rising alongside aging demographics.

APAC, South America and MEA Implantable Loop Recorders Market

Asia-Pacific shows the highest trajectory with a 10.62% CAGR through 2031. Urban hospitals in China and Japan rapidly integrate miniaturized recorders into stroke units, leveraging national policies that prioritize non-communicable disease management. India’s tier-one cities display growing adoption among middle-class consumers seeking private cardiology services. Government insurance schemes in several Southeast Asian nations commence pilot reimbursements, encouraging broader clinical use. Despite heterogeneous health financing and physician distribution, cumulative regional demand scales quickly, reflecting large patient bases and escalating cardiovascular disease prevalence. South America and the Middle East & Africa observe early-stage uptake where tertiary centers spearhead technology introduction, yet economic and infrastructure constraints temper near-term share.

Competitive Landscape

The implantable loop recorder market is moderately concentrated. Medtronic, Abbott, and Boston Scientific hold prominent positions through established product lines, deep clinical trial portfolios, and global sales coverage. Medtronic’s Reveal LINQ platform benefits from long-standing physician familiarity and a robust support ecosystem. Abbott’s six-year Assert-IQ launch elevates battery life standards and leverages smartphone connectivity to differentiate usability. Boston Scientific capitalizes on mCRM integration, combining insertable monitors with leadless pacing and defibrillation for a holistic rhythm-management suite

Strategic competition centers on extending longevity, cutting alert noise, and embedding AI algorithms that predict arrhythmia onset. Vendors invest in algorithmic refinements that compress false-positive rates while flagging actionable events for immediate intervention. Partnerships with cloud analytics firms accelerate data-driven services that sell alongside hardware. Emerging participants such as iRhythm Technologies and Angel Medical Systems focus on specialized ambulatory solutions or ischemia-detection implants, carving out niche segments within the broader implantable loop recorder industry.

Regulatory milestones shape positioning. CE Mark approvals for dual-chamber leadless pacemaker systems and FDA breakthroughs in pulsed-field ablation create cross-selling synergies for companies offering full cardiac portfolios. Intellectual-property barriers around telemetry encryption and firmware updates add defensibility for incumbents as cybersecurity standards tighten. Over the forecast window, scale economies, integrated platforms, and evidence-rich datasets will dictate share retention, while nimble entrants push innovation on sensor miniaturization and predictive analytics

Implantable Loop Recorders Industry Leaders

Abbott

Medtronic

BIOTRONIK

Boston Scientific Corporation

Vectorious

- *Disclaimer: Major Players sorted in no particular order

Implantable Loop Recorders Market Companies Covered in this Report

- Medtronic

- Abbott Laboratories

- BIOTRONIK

- Boston Scientific

- Angel Medical Systems

- iRhythm Technologies

- MicroPort

- Vectorious Medical

- LivaNova

- Koninklijke Philips

- Bardy Diagnostics

- Eko Devices

Recent Industry Developments in Implantable Loop Recorders Market

- April 2025: Abbott launched the ASCEND CSP pivotal trial evaluating a conduction-system pacing ICD lead

- March 2024: Abbott received CE Mark for the Assert-IQ insertable cardiac monitor featuring six-year battery life and advanced Bluetooth connectivity.

- January 2024: Medtronic secured CE Mark for Micra AV2 and VR2 leadless pacemakers with 40% longer battery expectancy, targeting 16-17 years of service.

Implantable Loop Recorders Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the implantable loop recorders market as the global sales value of single-lead, subcutaneously inserted ECG devices that archive and wirelessly transmit rhythm data for at least twelve months, helping clinicians investigate unexplained syncope, detect atrial fibrillation, monitor cryptogenic stroke cases, and track other intermittent arrhythmias.

Scope Exclusion: We leave out external or wearable event recorders, mobile cardiac-telemetry patches, and related accessories.

Segments Covered in This Report

- By Indication

- Syncope/Presyncope

- Atrial Fibrillation Detection

- Cryptogenic Stroke

- Palpitations & Other Arrhythmias

- By End-User

- Hospitals

- Cardiac Centers & Clinics

- Ambulatory Surgical Centers (ASCs)

- Home-based & Remote Monitoring Programs

- By Region

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We spoke with cardiologists, electrophysiologists, distributor buyers, and reimbursement advisors across North America, Europe, and Asia-Pacific. Their insights confirmed the shift toward miniaturized Bluetooth-ready models, validated real-world price erosion, and clarified average implantation rates in secondary-care centers.

Desk Research

Mordor analysts first mapped disease prevalence through open cardiac registers from the World Health Organization, the American Heart Association, and the European Heart Rhythm Association. They then paired those findings with procedure volumes visible in FDA PMA summaries, peer-reviewed epidemiology papers, and national hospital procurement dashboards. We next mined import-export codes for implantable cardiac monitors across twenty customs jurisdictions to sense shipment momentum and cross-checked average selling prices against company 10-Ks, investor decks, and product recall notices.

To sharpen revenue splits, our team drew on paid intelligence feeds from D&B Hoovers and Dow Jones Factiva, while guideline updates and tender notices were scanned to flag sudden demand swings. The sources noted are illustrative; many additional materials supported data checks.

Market-Sizing & Forecasting

Our model begins with a top-down prevalence-to-treated-patient pool built on syncope incidence, atrial-fibrillation rates, monitoring-guideline uptake, and reimbursement penetration. Bottom-up spot checks sampled average price multiplied by unit volumes extracted from hospital tenders and supplier disclosures help anchor totals and close data gaps. A multivariate regression blending aging population curves, remote monitoring adoption, reimbursement latitude, and device miniaturization indices projects demand to 2030, with scenario tests for price compression and battery breakthroughs.

Data Validation & Update Cycle

Outputs pass anomaly and variance screens before senior review. We refresh the model each year, with interim reruns triggered by major product approvals, safety alerts, or tariff shifts, ensuring clients receive the latest calibrated view.

How Mordor Intelligence's Implantable Loop Recorders Market Size Compares to Other Published Estimates

Published estimates often diverge because studies mix device classes, rely on list prices, or refresh less often. Key gap drivers include inclusion of external recorders, shipment-only modeling, currency inconsistencies, and conservative remote monitoring assumptions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.37 B (2025) | Mordor Intelligence | - |

| USD 1.55 B (2024) | Global Consultancy A | Includes external recorders and list prices |

| USD 1.60 B (2024) | Trade Journal B | Shipment-led model, no currency normalization |

| USD 1.27 B (2024) | Regional Consultancy C | Excludes remote monitoring programs, conservative uptake |

These contrasts show how our disciplined scope selection, dual-lens modeling, and annual refresh deliver a balanced, transparent baseline decision-makers can rely on.

Key Questions Answered in the Report

What is the current implantable loop recorder market size and growth outlook?

The implantable loop recorder market is USD 1.49 billion in 2026 and is projected to reach USD 2.29 billion by 2031 at a 8.94% CAGR.

Which indication dominates the market today?

Syncope/presyncope commands 45.98% of global revenue, reflecting extensive clinical adoption for unexplained fainting evaluation.

What segment is expanding the fastest?

Cryptogenic stroke monitoring shows the highest momentum, advancing at a 10.59% CAGR as it detects covert atrial fibrillation in nearly one-third of patients within three years.

How long can modern devices monitor cardiac rhythms?

Leading systems now provide continuous surveillance for up to six years, doubling the three-year benchmark of earlier generations.

Which regions display the highest future growth?

Asia-Pacific is forecasted to grow at 10.62% CAGR through 2031, while North America remains the largest market with 46.92% share.

Page last updated on: