Healthcare Operational Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

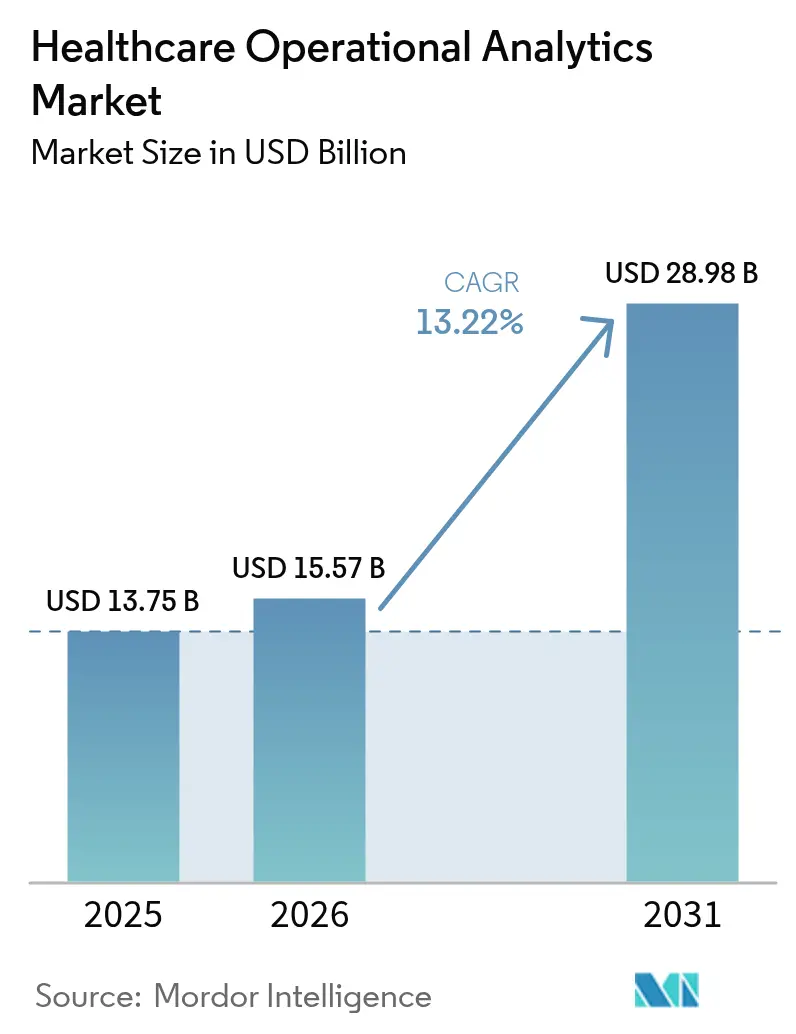

| Market Size (2026) | USD 15.57 Billion |

| Market Size (2031) | USD 28.98 Billion |

| Growth Rate (2026 - 2031) | 13.22% CAGR |

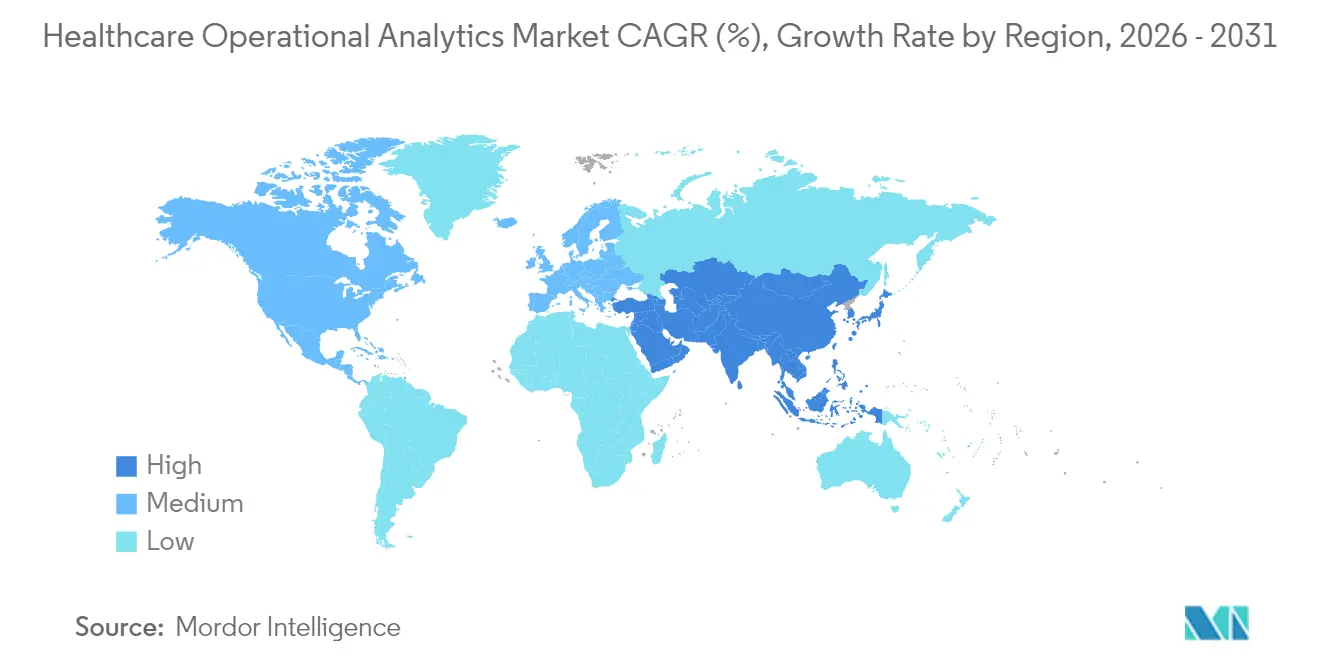

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

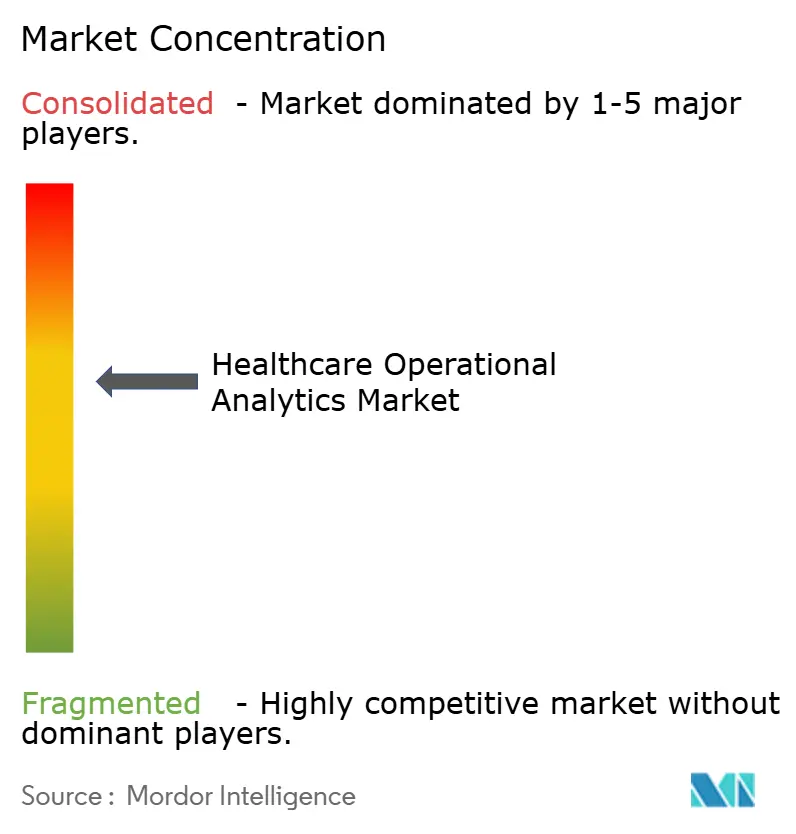

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Healthcare Operational Analytics Market Analysis by Mordor Intelligence

The healthcare operational analytics market size in 2026 is estimated at USD 15.57 billion, growing from 2025 value of USD 13.75 billion with 2031 projections showing USD 28.98 billion, growing at 13.22% CAGR over 2026-2031. Accelerated transition to value-based payment, surging volumes of electronic health-record data, and persistent cost-containment mandates keep adoption momentum high across payers and providers. Cloud-native platforms shorten deployment cycles, enabling real-time insights without large capital outlays, while workforce shortages heighten demand for predictive staffing tools that safeguard care quality despite lean clinical rosters. Vendors are broadening portfolios through M&A and strategic partnerships that embed artificial intelligence into everyday workflows, and venture capital is flowing toward Asia-Pacific start-ups that address foundational digital-health gaps. Taken together, these forces support sustained double-digit expansion of the healthcare operational analytics market through the end of the decade.

Key Report Takeaways

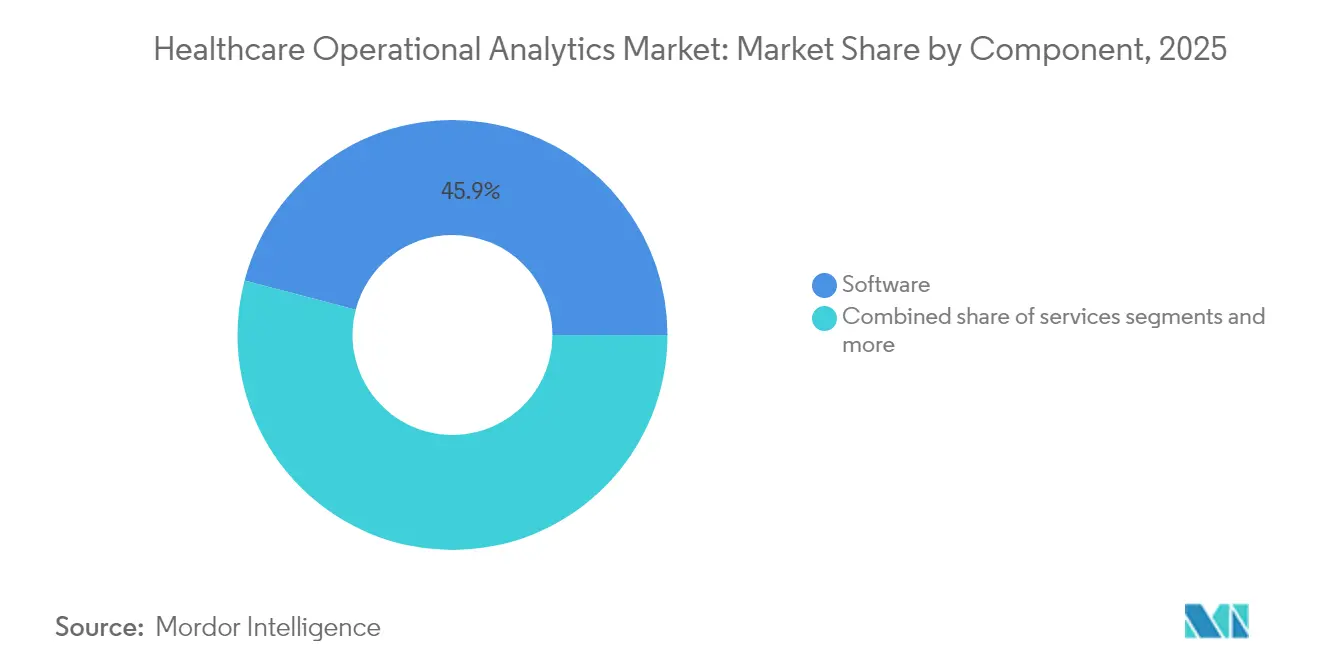

- By component, Software commanded 45.92% of the healthcare operational analytics market share in 2025; Services is projected to expand at a 14.05% CAGR through 2031.

- By deployment mode, Cloud-based platforms captured 56.78% of the healthcare operational analytics market size in 2025 and are advancing at a 13.41% CAGR to 2031.

- By application, Financial & Revenue-Cycle Management held 63.10% share of the healthcare operational analytics market size in 2025, whereas Workforce Management is tracking the fastest 13.78% CAGR through 2031.

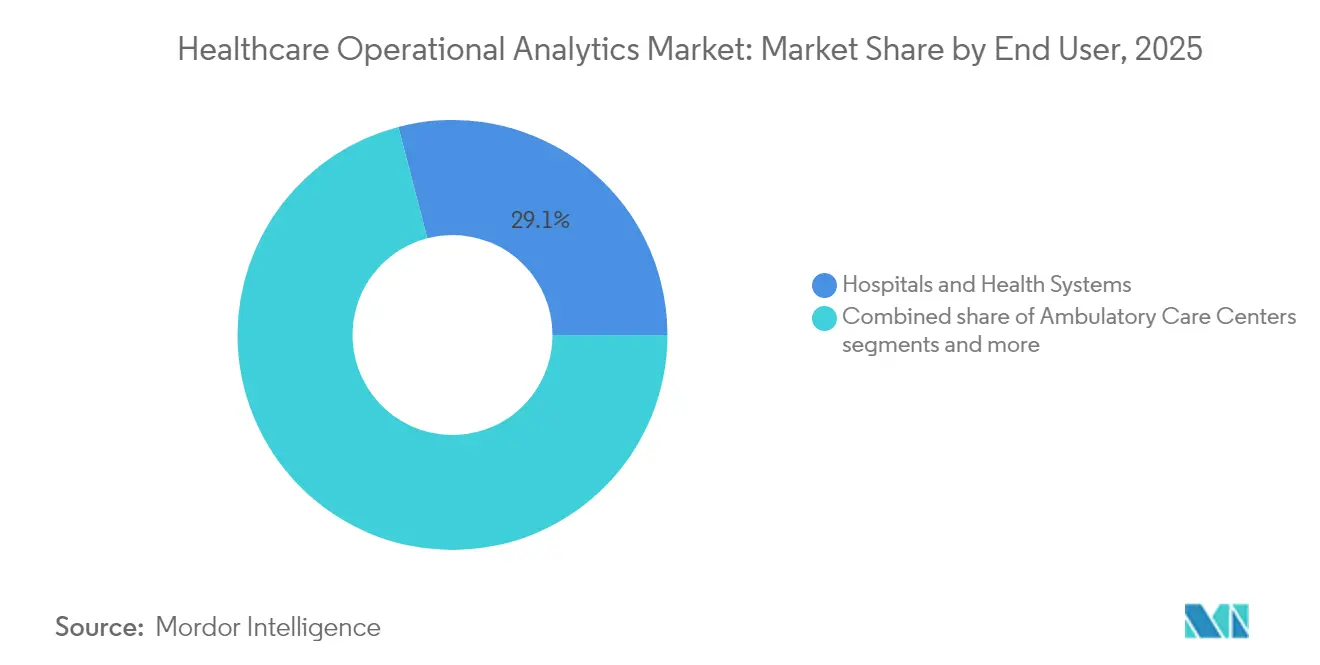

- By end user, Hospitals & Health Systems accounted for 29.05% of the healthcare operational analytics market share in 2025; Ambulatory Care Centers are growing at a 14.37% CAGR between 2026-2031.

- By geography, North America led with 37.75% of the healthcare operational analytics market size in 2025, while Asia-Pacific is accelerating at a 13.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Operational Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Value-based-care cost-containment push | +3.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Data deluge from EHR digitization | +2.8% | Global, with highest impact in North America | Short term (≤ 2 years) |

| Hospital efficiency needs amid staffing gaps | +2.5% | Global, acute in North America & EU | Short term (≤ 2 years) |

| Shift to cloud-native analytics platforms | +2.1% | Global, led by North America & EU | Medium term (2-4 years) |

| RTLS-enabled real-time throughput insights | +1.4% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Predictive maintenance for equipment uptime | +1.0% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Value-based-care cost-containment push

Centers for Medicare & Medicaid Services finalized 97 quality measures for program year 2025, compelling providers to embed analytics into reimbursement workflows and strengthening the growth outlook for the healthcare operational analytics market [1]Centers for Medicare & Medicaid Services, "2025 Quality Rating System Measure Technical Specifications," cms.gov. Early adopters have reported savings of USD 45 million across five years after linking outcome dashboards to bundled-payment contracts. Financial incentives in the Medicare Shared Savings Program secure long-term demand irrespective of macroeconomic cycles [2]Centers for Medicare & Medicaid Services, "Medicare Shared Savings Program Continues to Deliver Meaningful Savings and High-Quality Health Care," cms.gov. As Medicare aims for universal value-based coverage by 2030, analytics platforms become infrastructure rather than optional upgrades. Competitive differentiation now hinges on the precision and timeliness of cost-quality insights delivered to clinical teams.

Data deluge from EHR digitization

Nearly half of the data stored in hospital systems remains unused for decision-making even though 95% of executives believe better use would raise clinician productivity. EHR adoption has created mixed data types-structured codes, unstructured notes, imaging metadata that exceed the capability of legacy business-intelligence tools. The healthcare operational analytics market responds with scalable machine-learning engines compliant with HIPAA and GDPR, unlocking value from long-tail clinical variables. Data-quality, provenance, and governance modules are bundled into modern solutions to reduce compliance workloads. As interoperability frameworks mature, cross-provider longitudinal datasets fuel population-health risk models that enhance preventive-care outreach.

Hospital efficiency needs amid staffing gaps

A projected shortage of 1.1 million nurses by 2030 is forcing hospitals to shift from reactive scheduling to predictive labor-management strategies. Mercy Health cut contingent labor spending by USD 30.7 million in 2023 after deploying AI scheduling that increased shift-fill rates to 86%. [3]Mercy, "AI-Powered Workforce Tool Saved Mercy USD 30 Million in 2023," mercy.net Predictive census models using recent admission patterns achieve 3.7% forecast error, enabling just-in-time staffing and reducing overtime. Workflow engines integrated with the healthcare operational analytics market also guide float-pool redeployments, boosting nurse satisfaction and retention. Continuous monitoring of capacity, acuity, and skill mix aligns clinical resources with real-time demand, protecting margins in a flat reimbursement environment.

Shift to cloud-native analytics platforms

Healthcare organizations spend an average USD 38 million per year on cloud services yet consume only 44% of reserved capacity, leaving headroom to migrate analytics workloads without additional contracts. Public-cloud environments simplify high-performance compute access for deep-learning models, slashing hardware refresh cycles. Early Epic workloads on Amazon Web Services deliver higher satisfaction scores regarding scalability compared with on-premise installations. Federated delivery models distribute data-science sandboxes to clinical teams while central governance maintains security posture. Consistent patching and automated backups mitigate ransomware risk, a rising board-level concern.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High legacy integration costs | -2.1% | Global, most acute in North America & EU | Medium term (2-4 years) |

| Data-privacy & security compliance burden | -1.8% | Global, with varying regional requirements | Short term (≤ 2 years) |

| Operations-analytics talent shortage | -1.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Clinical-workflow disruption resistance | -1.2% | Global, cultural variations by region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High legacy integration costs

Case studies show multimillion-dollar variances when migrating historical data into new analytic environments, with scarce benchmarks for CIO planning. Parallel run periods inflate operating budgets and extend payback periods, causing some mid-tier hospitals to defer analytics upgrades that rely on modern EHR architectures. Vendors in the healthcare operational analytics market now package conversion accelerators using FHIR and bulk-export tooling to ease pain points, yet budgetary hesitation persists.

Data-privacy & security compliance burden

HIPAA fines range from USD 141 to over USD 2 million per incident, and the forthcoming EU AI Act classifies most clinical algorithms as high-risk applications. Hospitals must fund encryption, audit logging, and bias-monitoring processes before go-live, raising total cost of ownership. Smaller providers struggle with documentation overhead, slowing healthcare operational analytics market penetration until external managed-service options mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Drive Implementation Success

Services revenue, though smaller than software, is poised to grow at a 14.05% CAGR because implementation expertise determines return on analytics investments. Hospital groups purchasing enterprise licenses often realize value only after consulting teams align dashboards with clinical workflows and build FHIR pipelines from ancillary systems. McKinsey found that holistic revenue-cycle automation programs combining leadership coaching, process redesign, and data-science support accelerate margin gains.

Software still represents 45.92% of the healthcare operational analytics market share due to embedded EHR modules and subscription contracts. However, consumption models now bundle managed services, blurring lines between license and support revenue. Hardware remains niche, limited to high-security edge appliances protecting imaging archives or military treatment facilities. Overall, the healthcare operational analytics market sees services as the catalyst for sustainable software usage and continuous-improvement cycles.

By Deployment Mode: Cloud Dominance Accelerates

Cloud deployments held 56.78% share of the healthcare operational analytics market in 2025 and post the fastest 13.41% CAGR through 2031. Organizations migrating Epic workloads reported smoother monthly update cycles and more predictable cost structures versus on-premise environments. Hybrid models persist where imaging archives or genomic datasets must remain on local servers, but containerization eases workload portability.

Cost optimization is the next frontier, with many health systems over-provisioned on reserved instances. Rightsizing initiatives unlock funds for advanced AI projects, reinforcing cloud momentum inside the healthcare operational analytics market. On-premise deployments survive primarily in single-facility hospitals or defense installations with strict data-sovereignty mandates.

By End User: Ambulatory Care Centers Lead Growth

Hospitals & Health Systems held 29.05% healthcare operational analytics market share in 2025 given their scale and mandated reporting. Ambulatory Care Centers expand fastest at 14.37% CAGR as outpatient procedure volume is forecast to rise 21% to 44 million cases by 2034.

ASC operators prioritize lightweight scheduling, implant cost-tracking, and payer-contract analytics delivered via cloud SaaS. Private-equity ownership promotes standardized dashboards across geographically dispersed sites, driving incremental demand within the healthcare operational analytics market. Payers also deploy self-service portals that allow physicians to monitor quality and cost metrics tied to bundled-payment incentives.

By Application: Workforce Management Emerges as Growth Leader

Financial & Revenue-Cycle Management continues to dominate with 63.10% healthcare operational analytics market size in 2025 as hospitals chase denial reduction and cash acceleration. Yet Workforce Management grows fastest at 13.78% CAGR, reflecting acute staffing shortages. AI scheduling engines raised nurse satisfaction scores by 12 points at one large academic center after empowering clinicians with self-service rosters.

Supply-Chain modules gain traction amid inflationary pressure on medical supplies, and Patient Care & Performance dashboards link sepsis alerts to operational capacity metrics. Risk & Compliance solutions monitor algorithm bias and safety events, becoming integral features rather than bolt-ons. These diverse applications broaden the healthcare operational analytics market addressable revenue.

Geography Analysis

North America remains the largest region with 37.75% of healthcare operational analytics market size, benefiting from mature interoperability mandates. CMS rules linking payment to digital-quality reporting sustain purchasing even amid tight margins. However, integration costs and cyber-security spending absorb budgets, leading to selective feature rollouts instead of enterprise-wide deployments.

Asia-Pacific posts the highest 13.92% CAGR, catalyzed by demographic aging, rising consumer expectations, and government cloud-first strategies. The region’s digital-health market could unlock USD 100 billion in value by 2025, prompting hospitals to leapfrog legacy systems and install cloud analytics from day one. IDC forecasts 28.9% AI spending growth through 2027, with healthcare a top vertical.

Europe shows steady uptake as GDPR and soon-to-be-effective AI regulations elevate data-privacy governance. Providers invest in consent-management dashboards and zero-trust architectures. South America and Middle East & Africa represent emerging pockets where mobile penetration and public-sector funding begin to seed analytics pilot programs, expanding the global healthcare operational analytics market footprint.

Competitive Landscape

The healthcare operational analytics market exhibits moderate concentration. Epic increased its U.S. acute-care market share to 42.3% in 2024, far ahead of Oracle Health at 22.9% after client attrition. Epic’s integrated Cogito suite leverages a unified data model, while Oracle emphasizes voice-enabled workflows and embedded AI.

Philips deepens analytics reach via collaborations with Mass General Brigham to build real-time data ecosystems that fuse device telemetry with EHR feeds. Niche vendors focus on RTLS, predictive maintenance, and revenue-cycle automation. Black Book surveys show 96% of CFOs tracking automation tools for charge-capture accuracy.

Strategic M&A persists, illustrated by Oracle’s USD 28.4 billion Cerner deal that aims to create end-to-end cloud platforms yet risks integration setbacks. Private-equity roll-ups in ASC analytics target scheduling, supply chain, and clinician performance niches. Interoperability, user experience, and measurable ROI remain decisive purchase criteria for healthcare operational analytics market buyers.

Healthcare Operational Analytics Industry Leaders

-

Oracle Corporation (Cerner Corporation)

-

MERATIVE (IBM Watson)

-

Veradigm LLC (Allscripts Healthcare Solutions, Inc.)

-

McKesson Corporation

-

UnitedHealth Group Incorporated (OptumInsight)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Milliman MedInsight launched the MedInsight Innovation Portal, an advanced iteration of its Data Science Portal (DSP). Tailored for healthcare organizations facing growing complexities, the MedInsight Innovation Portal offers enhanced capabilities, user-friendly workflows, and cloud services, all aimed at fostering innovation, speeding up analytics, and bolstering data-driven decisions

- April 2025: MedeAnalytics, launched Health Fabric on the Snowflake AI Data Cloud. This integration allows organizations to unify diverse data sources and enhance their current infrastructure. Health Fabric serves as a comprehensive platform for analytics, speeding up insights and improving patient outcomes

- February 2025: Philips and Mass General Brigham announced a collaboration to integrate live healthcare data with AI for continuous cardiac monitoring

- April 2024: Baker McKenzie reported rising private-equity investment in Asia-Pacific healthcare analytics ventures

Global Healthcare Operational Analytics Market Report Scope

As per the scope of the report, analytics helps an organization through the systematic use of technologies, methods, and data to derive insights and to enable fact-based decision-making for planning, management, operational activities, measurement, and learning. With the availability of large data sets in the healthcare industry, it has become necessary for companies to be equipped with operational analytics tools to use data efficiently.

The healthcare operational analytics market is segmented by type (supply chain analytics, human resource analytics, and strategic analytics), component (software, hardware, and services), deployment (on-premise, web and cloud-based), end user (hospitals and clinics, pharmaceutical and biotechnology companies, and other end users) and geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally.

The report offers the value (in USD) for the above segments.

| Software |

| Hardware |

| Services |

| Cloud-based |

| On-premise |

| Hybrid |

| Supply Chain & Inventory Management |

| Workforce Management |

| Financial & Revenue-Cycle Management |

| Patient Care & Performance Management |

| Risk & Compliance Management |

| Others |

| Hospitals & Health Systems |

| Payers |

| Ambulatory Care Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Component | Software | |

| Hardware | ||

| Services | ||

| By Deployment Mode | Cloud-based | |

| On-premise | ||

| Hybrid | ||

| By Application | Supply Chain & Inventory Management | |

| Workforce Management | ||

| Financial & Revenue-Cycle Management | ||

| Patient Care & Performance Management | ||

| Risk & Compliance Management | ||

| Others | ||

| By End User | Hospitals & Health Systems | |

| Payers | ||

| Ambulatory Care Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the healthcare operational analytics market by 2031?

The market is forecast to reach USD 28.98 billion by 2031.

How fast is the healthcare operational analytics market expected to grow?

It is projected to expand at a 13.22% CAGR between 2026 and 2031.

Which deployment model leads adoption in healthcare analytics?

Cloud-based platforms held 56.78% share in 2025 and show the fastest growth to 2031.

Why are ambulatory care centers investing heavily in analytics?

Procedure migration to outpatient settings and the need for cost-efficient scheduling drive a 14.37% CAGR in analytics adoption among ASCs.

What is the biggest restraint on analytics adoption for hospitals?

High integration costs when linking modern analytics tools with legacy EHR systems remain the primary hurdle.

Page last updated on: