Healthcare 3D Printing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

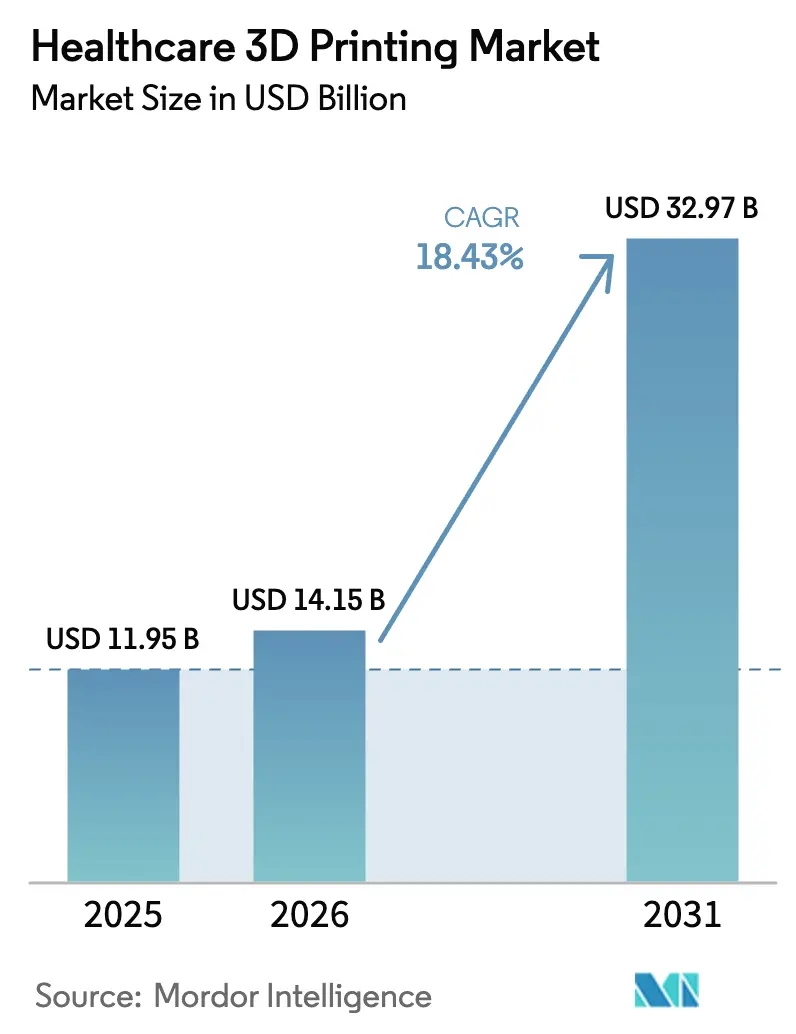

| Market Size (2026) | USD 14.15 Billion |

| Market Size (2031) | USD 32.97 Billion |

| Growth Rate (2026 - 2031) | 18.43% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare 3D Printing Market Analysis by Mordor Intelligence

The healthcare 3D printing market size is projected to expand from USD 11.95 billion in 2025 and USD 14.15 billion in 2026 to USD 32.97 billion by 2031, registering a CAGR of 18.43% between 2026 to 2031. Hospitals are shifting from outsourced prototyping to in-house fabrication of patient-specific guides and anatomical models, compressing pre-operative planning cycles from weeks to days. Regulatory clarity, particularly the U.S. Food and Drug Administration’s additive manufacturing guidance, reduces approval risk, which in turn encourages capital investment. Stereo lithography leads adoption because its sub-50-micron resolution supports dental and craniofacial work, while electron-beam melting (EBM) grows fastest as orthopedic suppliers scale titanium-alloy implant production. Material innovation, particularly cell-laden hydrogels, propels bioprinting beyond proof-of-concept and into drug-screening workflows. Consolidation favors vertically integrated players that own powder supply chains and design-automation software, strengthening competitive moats and insulating margins against commodity volatility.

Key Report Takeaways

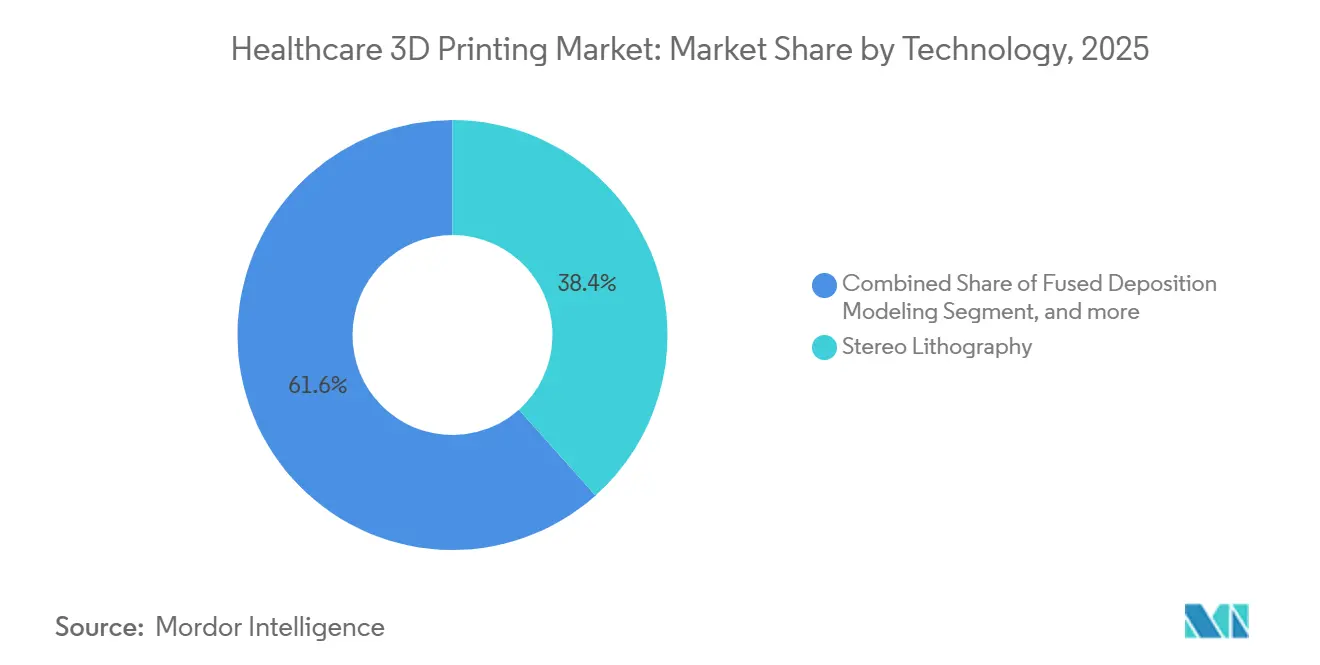

- By technology, stereo lithography led the healthcare 3D printing market with 38.42% of the market share in 2025; electron-beam melting is projected to expand at a 20.43% CAGR through 2031.

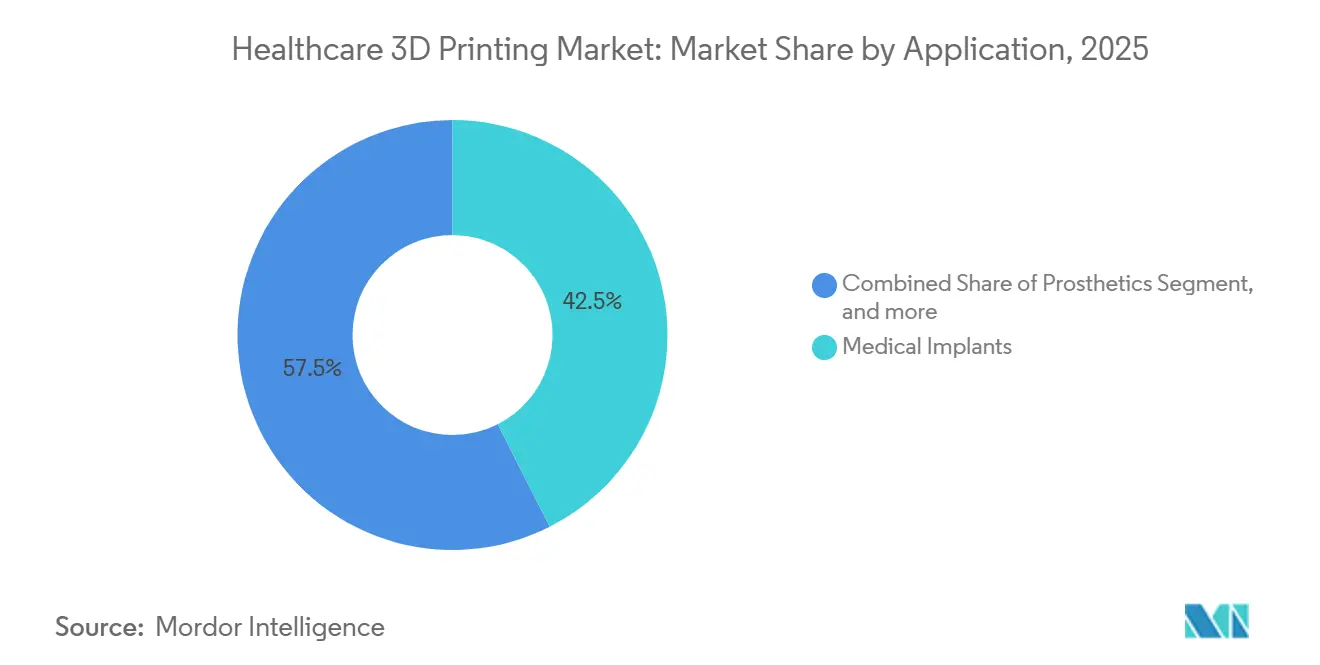

- By application, medical implants captured 42.53% of the healthcare 3D printing market size in 2025, while tissue engineering & bioprinting is advancing at a 20.67% CAGR through 2031.

- By material, metals & alloys accounted for 45.34% of the healthcare 3D printing market size in 2025; biomaterials/bio-inks are projected to record the highest CAGR at 20.11% through 2031.

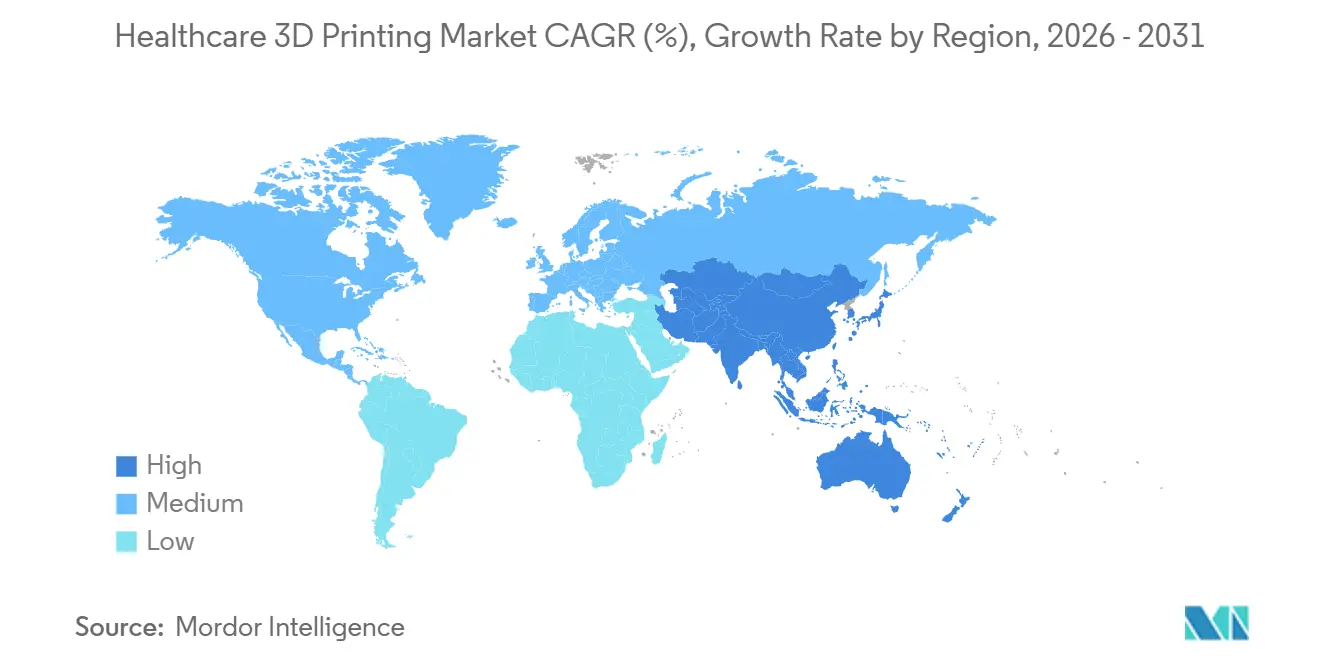

- By geography, North America retained 40.43% of the 2025 revenue, whereas the Asia-Pacific region is expected to grow at a 19.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare 3D Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in additive-manufacturing precision & speed | +4.2% | Global, early in North America & Europe | Medium term (2-4 years) |

| Expanding clinical indications across orthopedics, dental & tissue engineering | +3.8% | Global, strongest in North America & Asia-Pacific | Long term (≥4 years) |

| Growing acceptance of patient-specific implants & prosthetics | +3.5% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Hospital-based point-of-care labs reducing surgical lead times | +2.9% | North America, select European sites, emerging in APAC | Short term (≤2 years) |

| AI-driven automated design optimization | +2.1% | North America, Europe, Japan | Medium term (2-4 years) |

| Reimbursement codes for 3D-printed anatomical models | +1.8% | United States, Germany, Japan | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Advancements In Additive Manufacturing: Precision and Speed

Electron-beam systems now densify titanium lattices in single-digit-hour build cycles, enabling same-week delivery of patient-specific spinal cages. Multi-laser configurations double throughput without sacrificing dimensional tolerances, so batch production of 50–100 cranial plates becomes cost-competitive. Surface-finish gains reduce polishing, which formerly consumed 20%–30% of total production time. Lower per-part cost allows hospitals to match pricing on machined alternatives while retaining customization advantages. Such efficiencies collectively add roughly 4.2 percentage points to the sector’s forecast CAGR.

Expanding Clinical Indications Across Orthopedics, Dental, and Tissue Engineering

Dental labs produce clear-aligner molds in under 48 hours, displacing thermoforming workflows that took 10 days. Bioprinted vascularized constructs now remain viable for multi-week toxicology tests, meeting pharmaceutical screening thresholds. The FDA’s draft guidance on bioprinted tissues clarifies sterility and potency requirements, reducing filing uncertainty. As evidence accrues and reimbursement codes broaden, adoption will spread from tertiary centers to community hospitals. These factors collectively lift the CAGR contribution by 3.8 percentage points.

Growing Acceptance of Patient-Specific Implants and Prosthetics

Clinical data show custom implants cut revision rates and operating-room time, lowering overall cost of care. Prosthetic sockets with lattice structures distribute pressure evenly, resulting in improved comfort scores in peer-reviewed trials. Insurance parity encourages hospitals to order custom devices because reimbursement matches prefabricated alternatives[1]Centers for Medicare & Medicaid Services, “CY 2025 Physician Fee Schedule Final Rule,” cms.gov. German and Japanese payers have issued similar coverage, bolstering global diffusion. Acceptance adds 3.5 percentage points to forecast growth.

Hospital-Based Point-of-Care 3D Printing Labs Reducing Surgical Lead Times

Academic centers with on-site printers reduce model-delivery time from weeks to days; surgeons can iterate and guide the same day, which is impossible with distant service bureaus. Automated DICOM-to-print software cuts segmentation to under 30 minutes, lowering skill barriers. The FDA considers single-patient hospital prints as physician-directed, exempting them from pre-market review. Resulting time savings and scheduling flexibility raise procedure volume, contributing 2.9 percentage points to CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory approval pathways | −2.3% | Global, acute in North America & Europe | Medium term (2-4 years) |

| Skilled workforce shortage | −1.8% | Global, pronounced in emerging APAC | Long term (≥4 years) |

| Non-standardized sterilization for porous implants | −1.5% | Global, regulatory gaps in APAC & MEA | Medium term (2-4 years) |

| Raw-material supply volatility | −1.2% | Global, supply centered in Europe & North America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Approval Pathways for 3D-Printed Medical Devices

Process variability complicates validation, extending FDA 510(k) timelines by several months and necessitating costly powder characterization tests. Under Europe’s MDR, manufacturers must prove equivalence with machined predicates that lack porous architectures, inflating evidence requirements. Consulting fees can exceed USD 500,000 per device submission, deterring startups. ISO/ASTM standards harmonize terminology yet remain voluntary, so firms juggle fragmented regional rules. These factors reduce CAGR by 2.3 percentage points.

Shortage of Skilled Additive Manufacturing Workforce in Healthcare

Fewer than 30 universities offer curricula that combine ISO 13485 and hands-on printer operation, thereby limiting the talent supply. Hospitals rely on OEM service contracts, which raise operating costs and hinder in-house innovation. APAC growth intensifies shortages; Indian firms report additive-manufacturing vacancy rates above 25%. Certification bodies have launched fast-track courses, but equipment and instructor scarcity hinder their scale. Workforce gaps subtract 1.8 percentage points from forecast growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Resolution And Material Compatibility Drive Adoption

Stereo lithography contributed 38.42% of 2025 revenue, underscoring its dominance within the healthcare 3D printing market. Ultra-fine layers below 25 microns provide the smooth surfaces required for clear aligners and craniofacial models, while biocompatible photopolymers simplify FDA material submissions[2]U.S. Food and Drug Administration, “Premarket Notification Database,” fda.gov. EBM adoption accelerates at a 20.43% CAGR because it fuses high-melting-point titanium without residual porosity, essential for load-bearing hip stems.

Fused deposition modeling retains appeal for budget-sensitive anatomical models, whereas selective laser sintering satisfies dental and hearing-aid niches by pairing nylon powders with autoclave stability. PolyJet’s multi-material capability simulates cartilage versus bone in surgical rehearsals, and binder-jet ceramics supply bioactive scaffolds. Laminated-object manufacturing wanes as resin and powder systems match its economics with higher precision. Technologies that embed closed-loop melt-pool monitoring address FDA expectations for process validation, directing hospitals toward vendors offering turnkey compliance.

By Application: Implants Dominate, Bioprinting Gains Momentum

Medical implants accounted for 42.53% of 2025 application revenue, underscoring their dominance in the healthcare 3D printing market. Surgeons value pre-contoured titanium acetabular cups that cut fitting time, while dental zirconia crowns fabricated via powder-bed fusion fetch premium pricing. Tissue engineering and bioprinting, although still in their early stages, are expected to log a 20.67% CAGR as vascularized constructs address pharma’s need for human-relevant toxicology models.

Procedural reimbursement for surgical guides led to a rapid uptake, with hospitals printing models for 15%–20% of complex cases. Prosthetics benefit from lattice sockets that reduce skin-pressure hotspots, enhancing patient satisfaction. Wearable devices remain nascent, but they could expand once flexible filaments clear the biocompatibility hurdles. Implant design advances focus on graded porosity that encourages bone ingrowth and mitigates stress shielding, features unattainable in machined components.

By Material: Metals Lead, Bio-Inks Show Highest Growth Potential

Metals & alloys accounted for 45.34% of the 2025 material revenue, the largest share of the healthcare 3D printing market size for materials. Titanium alloy’s osteoconductivity underpins orthopedic dominance, while cobalt-chromium resists wear in articulating joints. Biomaterials and bio-inks are expected to post a 20.11% CAGR, with alginate-gelatin hydrogels demonstrating>85% post-print cell viability in preclinical studies.

Polymers and photopolymers meet the demands of dental and prosthetic applications with sterilizable methacrylate resins and polyamide-12. Ceramic scaffolds account for less than 10% of sales but attract niche demand for bioactive bone substitutes. Supply-chain risk remains: single-source polyamide-12 outages disrupt printer utilization rates, motivating device firms to dual-source materials. Metal powder innovation prioritizes spherical morphology to improve flow and fatigue life, while polymer vendors pursue antimicrobial additives to fight post-operative infection.

Geography Analysis

North America contributed 40.43% of the 2025 revenue, the largest regional share of the healthcare 3D printing market. The FDA’s additive-manufacturing guidance, coupled with CMS reimbursement for anatomical models, propels adoption across academic and community hospitals. Canada follows similar regulatory contours, yet provincial reimbursement heterogeneity tempers uniform uptake. Mexico utilizes duty-free zones to attract dental device contract manufacturing for export to the United States.

The Asia-Pacific region is expected to grow at a 19.54% CAGR through 2031, as China, Japan, and South Korea implement national additive manufacturing strategies. China scaled domestic powder output and expedited device approvals, reducing dependence on imports[3]National Medical Products Administration of China, “Guideline for Additively Manufactured Implants,” nmpa.gov.cn. Japan’s PMDA introduced fast-track pathways, and public insurers now cover patient-specific titanium implants. South Korean research centers are focusing on vascularized bioprinting to conduct clinical trials within five years. India positions itself as an orthopedic export hub but faces workforce constraints.

Europe held a mid-20s share in 2025. German insurers reimburse surgical guides, spurring equipment orders; the United Kingdom’s NHS pilots centralized 3D printing hubs to pool demand. France shortened customs implant reviews under its ANSM agency. The Middle East and Africa remain sub-10% share: the UAE’s free zones host orthopedic startups, whereas broader regional adoption lags due to reimbursement gaps. South America captures a low single-digit share, with Brazil approving primarily dental devices; tariffs inflate equipment costs.

Competitive Landscape

The healthcare 3D printing market is moderately concentrated, with the top five suppliers accounting for roughly 35% of the 2025 revenue. Orthopedic giants such as Zimmer Biomet and Stryker vertically integrate by acquiring powder manufacturers, securing feedstock quality and margin stability. EOS and 3D Systems differentiate with closed-loop melt-pool monitoring that satisfies FDA validation criteria, while Stratasys monetizes design-automation software through subscription models.

Startups exploit white spaces in bioprinting and ceramic scaffolds. Organovo and CELLINK pursue vascularized liver constructs for pharma toxicology before pivoting to therapeutic grafts. Partnership deals proliferate: software vendors embed generative design engines directly into printer controllers, sharing royalties on medical machines sold. Capital budgets under USD 100,000 favor compact printers tailored for dental labs and hospital point-of-care units, a niche populated by Formlabs and Carbon. ISO 13485 certification and FDA registration serve as acquisition filters; large corporates buy compliance infrastructure rather than build it.

Recent litigation trends show patent enforcement around lattice-optimization algorithms, signaling the strategic importance of design IP. Powder suppliers enter into long-term agreements with implant manufacturers to secure predictable demand and hedge against fluctuations in commodity prices. The competitive focus is shifting from printer price to turnkey workflow ownership, which bundles hardware, software, materials, and quality documentation templates.

Healthcare 3D Printing Industry Leaders

Nanoscribe GmbH & Co. KG

Stratasys Ltd

3D Systems Inc.

EOS GmbH

Renishaw PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Stratasys Ltd. made its RadioMatrix radiopaque 3D printing material fully available for commercial use in the United States. This development follows earlier limited deployments of the material. It now allows healthcare providers, device manufacturers, and research institutions nationwide to access and utilize it for medical imaging and training.

- November 2025: Lynxter has expanded its S300X ecosystem by adding two new modules: the NEST – GEL and NEST – POWDER, developed in collaboration with 3Deus Dynamics. These modules enhance the capabilities of the S300X for silicone 3D printing of thin-walled parts. The new solutions offer a clean, solvent-free process suitable for industrial, medical, and research applications.

- December 2024: Materialise, a prominent player in medical 3D printing and planning solutions, has introduced its fully integrated Materialise Mimics platform. The platform aims to improve efficiency in advanced 3D planning and personalized device creation. This development enhances accessible patient care for medical device companies and hospitals worldwide.

Global Healthcare 3D Printing Market Report Scope

As per scope of the report, healthcare 3D printing involves creating medical devices, implants, and anatomical models using 3D printing technology. It enables personalized treatments and precise surgical planning tailored to individual patients. This innovation enhances outcomes and reduces costs in healthcare.

The Healthcare 3D Printing Market is Segmented by Technology (Stereo Lithography, Fused Deposition Modeling, Selective Laser Sintering, Electron Beam Melting, PolyJet/MultiJet, Binder Jetting, and Laminated Object Manufacturing), Application (Medical Implants, Prosthetics, Surgical Guides & Anatomical Models, Tissue Engineering & Bioprinting, and Wearable Devices), Material (Metals & Alloys, Polymers & Photopolymers, Ceramics & Bioceramics, and Biomaterials/Bio-Inks), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Stereo Lithography |

| Fused Deposition Modeling |

| Selective Laser Sintering |

| Electron Beam Melting |

| PolyJet / MultiJet |

| Binder Jetting |

| Laminated Object Manufacturing |

| Medical Implants |

| Prosthetics |

| Surgical Guides & Anatomical Models |

| Tissue Engineering & Bioprinting |

| Wearable Devices |

| Metals & Alloys |

| Polymers & Photopolymers |

| Ceramics & Bioceramics |

| Biomaterials / Bio-Inks |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East And Africa | GCC |

| South Africa | |

| Rest Of Middle East And Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Technology | Stereo Lithography | |

| Fused Deposition Modeling | ||

| Selective Laser Sintering | ||

| Electron Beam Melting | ||

| PolyJet / MultiJet | ||

| Binder Jetting | ||

| Laminated Object Manufacturing | ||

| By Application | Medical Implants | |

| Prosthetics | ||

| Surgical Guides & Anatomical Models | ||

| Tissue Engineering & Bioprinting | ||

| Wearable Devices | ||

| By Material | Metals & Alloys | |

| Polymers & Photopolymers | ||

| Ceramics & Bioceramics | ||

| Biomaterials / Bio-Inks | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East And Africa | GCC | |

| South Africa | ||

| Rest Of Middle East And Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is the healthcare 3D printing market in 2026?

It is valued at USD 14.15 billion, with an 18.43% CAGR projected through 2031.

Which technology leads current revenues?

Stereo lithography holds 38.42% of 2025 revenue due to high resolution and biocompatible resins.

What is the fastest-growing regional segment?

Asia-Pacific is forecast to expand at 19.54% CAGR through 2031 as China, Japan and South Korea scale capacity.

Why are titanium powders critical?

Titanium's biocompatibility and strength make it indispensable for load-bearing implants, giving metals 45.34% of 2025 material revenue.

How do reimbursement policies impact adoption?

CMS and other insurers now reimburse anatomical models and custom implants, turning 3D printing into a revenue-neutral or cost-saving option for hospitals.

Page last updated on: