Fraud Detection and Prevention (FDP) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

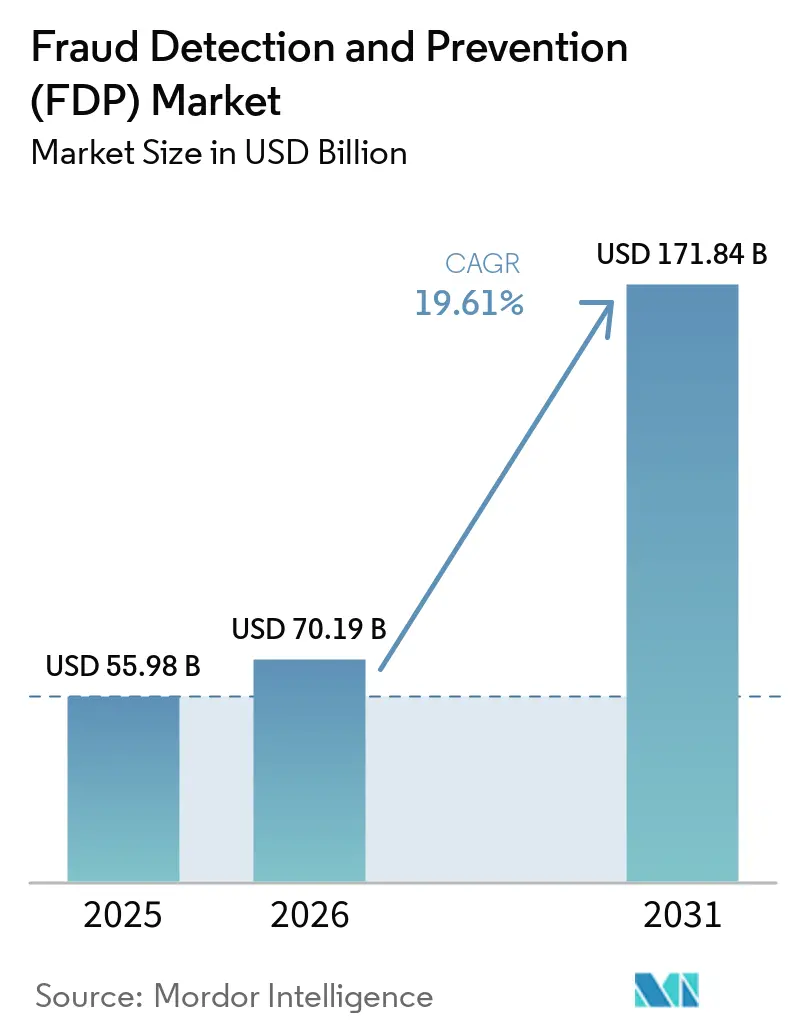

| Market Size (2026) | USD 70.19 Billion |

| Market Size (2031) | USD 171.84 Billion |

| Growth Rate (2026 - 2031) | 19.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fraud Detection and Prevention (FDP) Market Analysis by Mordor Intelligence

The fraud detection and prevention market size is expected to increase from USD 55.98 billion in 2025 to USD 70.19 billion in 2026 and reach USD 171.84 billion by 2031, growing at a CAGR of 19.61% over 2026-2031. Rising digital-payment adoption, tighter global compliance mandates, and generative-AI-driven identity fraud are converging to expand both attack surfaces and spending on adaptive defenses. Institutions are shifting budgets from rule engines to self-learning models that ingest billions of data points in real time, while open-banking rails shorten fraud-detection windows to milliseconds. Regional payment initiatives such as Pix in Brazil and the Unified Payments Interface in India amplify transaction flow, forcing banks and merchants to upgrade analytics pipelines. Vendor competition is intensifying as payment networks embed risk scoring within authorization flows and fintech specialists train sector-specific models that outperform generalist platforms.

Key Report Takeaways

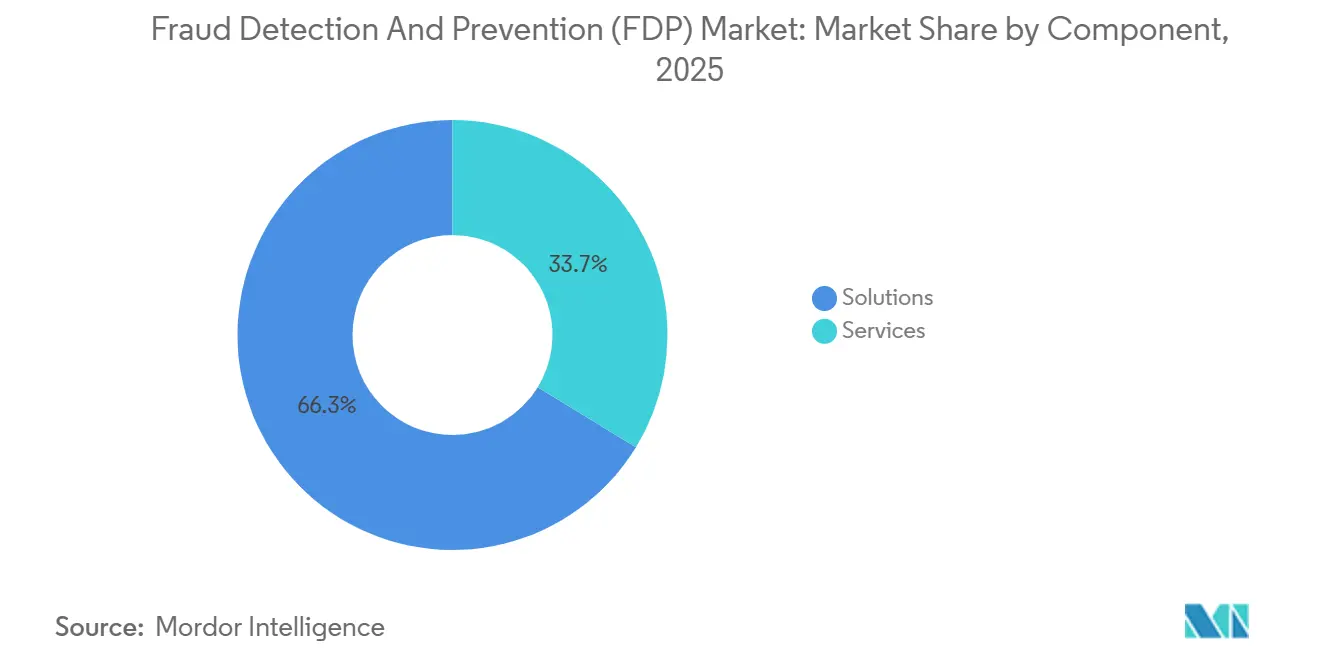

- By component, solutions led with 66.26% of the fraud detection and prevention market share in 2025, while services are advancing at a 19.97% CAGR through 2031.

- By deployment mode, cloud accounted for 63.82% of the fraud detection and prevention market revenue in 2025 and is projected to expand at a 19.95% CAGR through 2031.

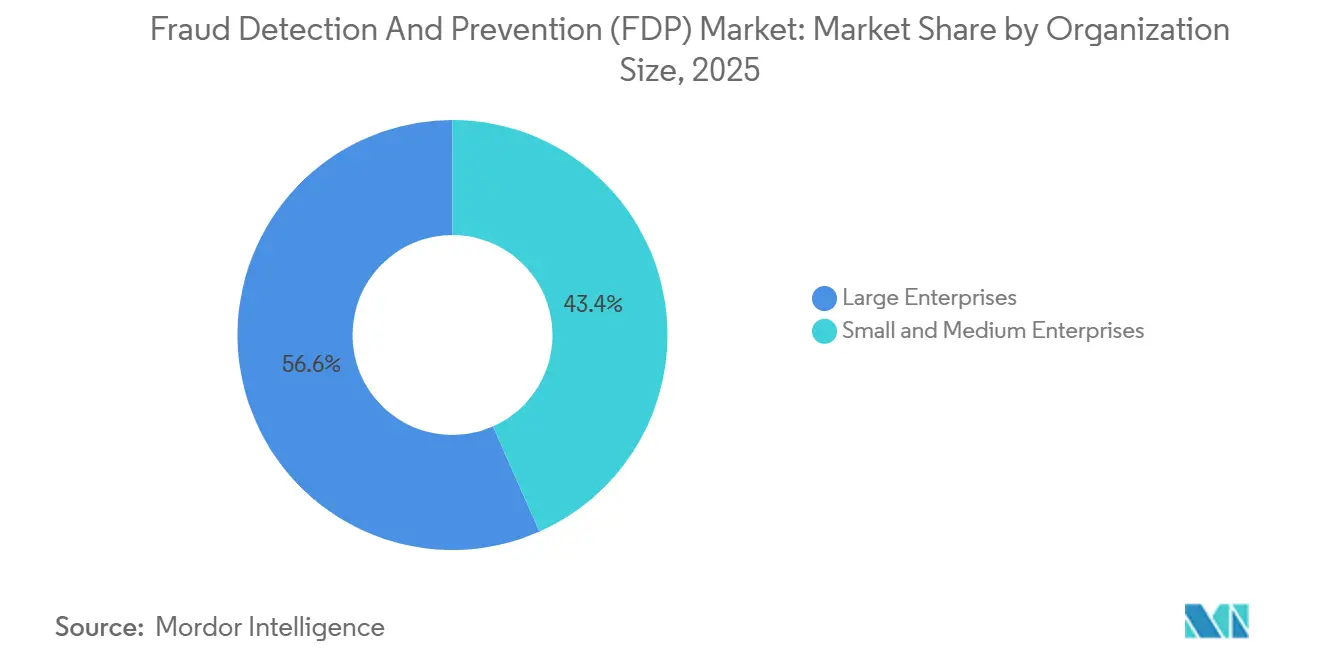

- By organization size, large enterprises captured 56.64% of 2025 spending, whereas small and medium enterprises are growing at a 19.92% CAGR to 2031.

- By end-user industry, BFSI commanded 26.15% of 2025 revenue, and retail and e-commerce is the fastest-growing vertical at a 21.18% CAGR through 2031.

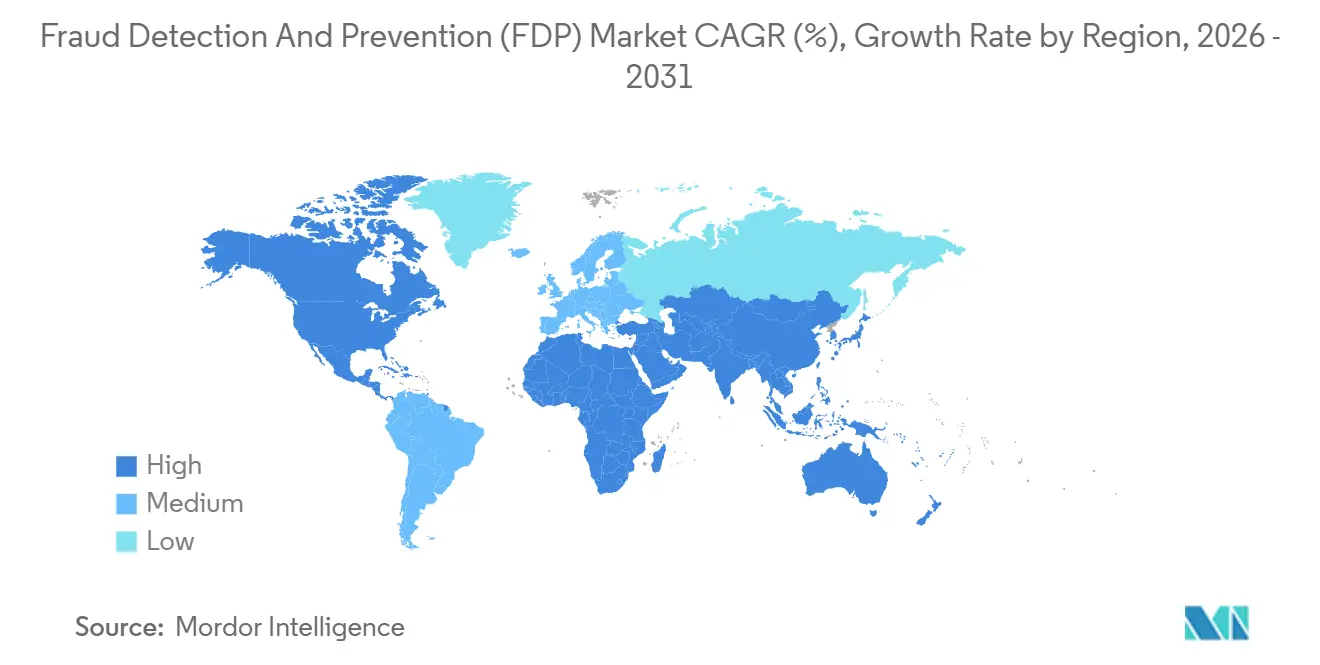

- By geography, North America accounted for 31.87% of the 2025 revenue in the fraud detection and prevention market, while Asia-Pacific is forecast to record a 20.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fraud Detection and Prevention (FDP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Digital Payments and E-Commerce Transaction Volumes | +4.8% | Global with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Stringent Regulatory Compliance for AML and PSD2 SCA | +4.2% | Europe and North America, extending to Middle East and Asia-Pacific | Short term (≤ 2 years) |

| AI and Machine Learning Models Increasing Real-Time Detection Accuracy | +3.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Tokenization and EMV 3-D Secure 2.3 Adoption Reducing Card-Not-Present Fraud | +2.7% | Global with early gains in Europe and North America | Short term (≤ 2 years) |

| Proliferation of Open Banking and Instant-Payment Rails Creating New Fraud Vectors | +2.4% | Europe and Asia-Pacific core, spill-over to South America | Medium term (2-4 years) |

| Generative AI Deepfake and Synthetic Identity Attacks Pushing Adaptive FDP Investments | +2.1% | Global with highest impact in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Digital Payments And E-Commerce Transaction Volumes

Card-not-present transactions account for the majority of global fraud losses as consumers shift to online channels where physical security features are absent. The European Central Bank reported that card-not-present fraud accounted for 79% of total card fraud in 2024. India’s Unified Payments Interface processed 16.73 billion transactions in December 2025 alone, a 45% year-over-year increase that strained batch-oriented legacy systems. Cross-border e-commerce complicates detection because region-specific risk patterns rarely generalize, compelling vendors to maintain localized models. Merchants are adopting passive biometrics to balance fraud control and customer friction, and payment facilitators aggregate network intelligence so even small sellers benefit from consortium-wide signals.

Stringent Regulatory Compliance For AML And PSD2 SCA

Successive rulemakings are mandating multi-factor authentication, continuous monitoring, and auditable workflows. The European Banking Authority’s tightened Strong Customer Authentication exemptions in 2024 narrowed frictionless-payment thresholds, prompting issuers to deploy risk-based engines. Proposed Payment Services Directive 3, which is circulating in 2025, would extend liability for authorized push-payment fraud to sending banks, shifting detection to the initiation layer. In the United States, FinCEN’s beneficial-ownership rule requires verification of control structures, driving interest in graph-database analytics. Multinational institutions must reconcile divergent data-residency obligations, leading to federated learning approaches that keep training data within national borders while sharing model weights.

AI And Machine Learning Models Increasing Real-Time Detection Accuracy

Graph neural networks and transformer ensembles uncover non-linear links among cards, devices, and merchants that static rules miss. The Bank of England’s Project Hertha generates synthetic transaction sets so regional banks can train without exposing live customer data.[1]Bank of England, “Project Hertha: Synthetic Data for Financial Stability,” BANKOFENGLAND.CO.UK Visa processed 8.6 billion tokenized transactions in H1 2025, feeding dynamic features into its real-time models. Vendors now retrain weekly to counter adversarial input manipulations that subtly shift feature distributions. Compute elasticity from cloud providers lets mid-tier banks run resource-intensive deep-learning pipelines once reserved for tier-one institutions.

Tokenization And EMV 3-D Secure 2.3 Adoption Reducing Card-Not-Present Fraud

Tokenization replaces static PANs with ephemeral identifiers, while EMV 3-D Secure 2.3 embeds rich risk data to enable issuers to silently approve low-risk transactions. EMVCo recorded more than 10 billion 3-D Secure 2 authentications worldwide in 2024, a 40% rise over 2023.[2]EMVCo, “EMV 3-D Secure Deployment Statistics,” EMVCO.COM Visa’s Scam Disruption consortium shares tokenized risk scores in real time, allowing members to invalidate compromised tokens before reuse.[3]Visa, “Fiscal 2025 Second Quarter Financial Results,” INVESTOR.VISA.COM Provisioning remains the weak link, as threat actors hijack wallet onboarding to attach stolen credentials, accounting for 18% of card-not-present fraud in 2024, according to industry estimates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High False-Positive Rates Undermining Customer Experience | -2.8% | Global with acute impact in North America and Europe | Short term (≤ 2 years) |

| Integration Complexity With Fragmented Legacy Core Systems | -2.3% | Global concentrated in North America and Europe | Medium term (2-4 years) |

| Scarcity Of Labeled Fraud Datasets For Advanced ML Training | -1.6% | Global | Long term (≥ 4 years) |

| Data-Sharing Constraints Imposed By GDPR And CCPA | -1.4% | Europe, North America extending to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High False-Positive Rates Undermining Customer Experience

Legacy rules still misclassify legitimate orders at double-digit rates, generating operational cost and lifetime-value erosion that sometimes exceed direct fraud losses. Manual reviews can cost USD 10-15 per flagged transaction, burdening merchants with thin margins. Behavioral biometrics that capture keystroke cadence and device-tilt angles promise to cut false positives below 3%, yet deployment lags because many consent frameworks treat continuous behavior capture as sensitive personal data. Cross-border orders suffer most, since unfamiliar IP geographies trip velocity checks, leading to cart abandonment and reputational damage.

Integration Complexity With Fragmented Legacy Core Systems

Mainframe-based payment cores use proprietary data formats and nightly batch cycles, complicating data-stream capture for real-time fraud scoring. Tier-one banks report 18-36-month rollouts and budgets topping USD 50 million when refactoring interfaces. Middleware hubs introduce latency and new failure modes, while divergent message schemas consume half of implementation resources. API-standardization programs such as the Berlin Group’s NextGenPSD2 and the Financial Data Exchange reduce friction, but uneven adoption forces vendors to maintain multiple connectors, inflating total cost of ownership.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Rise As Continuous Model Tuning Outpaces One-Time Licensing

The fraud detection and prevention market size for solutions reached its highest level in 2025, capturing 66.26% of platforms, authentication gateways, and reporting dashboards delivered rapid ROI. Yet services, including managed detection, model validation, and regulatory advisory, are expanding faster than packaged software. Institutions are learning that adaptive fraud defense is an ongoing process requiring weekly model refreshes and ever-evolving compliance mapping. Specialist consultancies now bundle data-science talent with SaaS dashboards so banks can outsource feature engineering without ceding strategic oversight. Reporting and visualization modules that once sat on the sidelines are gaining board-level attention because real-time exposure metrics influence capital-allocation decisions. Consolidation of fraud detection with identity verification blurs component boundaries, enabling unified risk scoring across the customer lifecycle.

Longer term, commoditization pressures solutions vendors to differentiate through proprietary data networks and low-latency inference. IBM’s 2025 expansion of consumption-priced fraud detection as a service illustrates how pay-as-you-go models align costs with actual transaction risk. Workflow orchestration that prioritizes alerts based on financial risk and regulatory severity is becoming table stakes. Institutions now allocate 30-40% of their fraud-prevention budget to external services, reinforcing the shift from capex technology purchases to opex partnerships focused on measurable loss-reduction outcomes.

By Deployment Mode: Elastic Cloud Capacity Accelerates Model Training Cycles

Cloud captured 63.82% of 2025 revenue, growing around 19.95% through 2031, as elastic compute lets fraud teams spin up GPU clusters for graph neural network training on demand. Real-time scaling means weekly model redeployments are complete without downtime, and security certifications from major hyperscalers satisfy most supervisory expectations. On-premises installations persist where data-sovereignty statutes prohibit cross-border transfer or where recent datacenter investments remain on depreciation schedules. Hybrid architectures, which score high-risk transactions locally while pooling de-identified aggregates in cloud data lakes, reconcile residency rules with machine-learning efficiency. The European Banking Authority clarified in 2024 that cloud outsourcing does not transfer accountability, giving risk committees confidence to migrate critical workloads.

Multi-cloud strategies gain traction among global banks keen to avoid single-vendor lock-in and to distribute compute across regions for resilience. Still, divergent toolchains complicate data synchronization, and model version drift can lead to inconsistent decisions across channels. Google Cloud’s virtual-private-cloud deployment pattern, adopted by several mid-tier U.S. banks in late 2025, shows regulators can be convinced when customers retain encryption-key control.

By Organization Size: SMEs Close The Capability Gap Through Embedded Fraud Scoring

Large enterprises retained 56.64% of their 2025 spend due to higher transaction volumes and stringent compliance audits, while small and medium enterprises now have access to enterprise-grade analytics embedded in acquiring platforms. Payment facilitators such as Stripe and Square supply network-effect intelligence so a single compromise on one merchant uplifts risk thresholds globally. Consumption-based pricing eliminates large upfront fees, which are critical for businesses with variable monthly volumes. The fraud detection and prevention market share differential narrows as SMEs integrate out-of-the-box behavioral analytics for account takeover detection, previously restricted to banks with in-house data science teams.

Nonetheless, social engineering attacks and business email compromise schemes disproportionately affect SMEs without layered approval workflows. Regulators increasingly highlight the exposure of embedded-finance platforms that extend credit or payments under their own brands, forcing small retailers to assume risk-management responsibilities that banks traditionally held. Large enterprises, meanwhile, shift toward insider-threat analytics and third-party risk scoring to address vulnerabilities arising from complex supply chains.

By End-User Industry: BFSI Sustains Lead While Retail Growth Slows Amid Saturation

The banking, financial services, and insurance sector captured the largest fraud detection and prevention market share at 26.15% in 2025as regulators continued to tighten anti-money-laundering, insurance fraud detection, and real-time payment rules, making continuous transaction monitoring non-negotiable for every tier-one institution. Mandatory customer due diligence checks, instant settlement rails, and liability shifts under evolving U.S. and European legislation keep capital flowing toward graph analytics, case management automation, and insider threat modules. Incumbent banks now push fraud scoring out to the customer-edge, incorporating behavioral biometrics into mobile apps so risk decisions arrive within 50 milliseconds of a tap, while insurers deploy anomaly detection to flag staged-accident and premium-evasion schemes.

Retail and e-commerce accounted for 21.18% of the 2025 fraud detection and prevention market, reflecting both the sheer volume of card-not-present transactions and the continuing shift toward marketplace models that expose sellers to third-party risk. Growth is slower than in other verticals because basic payment-gateway filters are already ubiquitous, yet investment persists as merchants battle loyalty-point fraud, promo-code abuse, and refund manipulation that evade rule engines tuned only for outright payment theft. Large platforms enrich device fingerprints with geolocation telemetry to lower false positives without adding checkout friction, while small sellers rely on embedded risk scoring offered by payment facilitators.

Geography Analysis

North America generated 31.87% of global revenue in 2025 as high digital-payment penetration and robust compliance frameworks kept spending elevated. The U.S. Federal Trade Commission logged USD 10 billion in consumer fraud losses in 2023, reinforcing board-level urgency for improved controls. Real-time rails such as the Real-Time Rail in Canada and FedNow in the United States are shortening settlement windows, forcing banks to reduce model-scoring latency to sub-second levels. Regulatory scrutiny intensifies around third-party service providers, compelling financial institutions to audit vendor models for explainability and bias.

Asia-Pacific is the fastest-growing region, projected to post a 20.43% CAGR as India, China, Australia, and Japan modernize payments infrastructure. India’s UPI handled 16.73 billion transactions in December 2025, catalyzing Reserve Bank mandates for additional authentication on high-ticket transfers RBI.ORG.IN. China’s digital-yuan pilots expand cashless ecosystems to rural counties, adding novel fraud vectors such as identity spoofing in offline wallets. Japan’s revised AML guidelines emphasize continuous monitoring over rule-based checks, stimulating demand for AI platforms such as. Australia’s New Payments Platform processed 1.2 billion instant transfers in 2024, exposing gaps in fraud-analytics stacks built for batch ACH files.

Europe maintains significant share on the strength of PSD2 Strong Customer Authentication mandates, yet card-not-present losses still reached EUR 4.2 billion (USD 4.5 billion) in 2024. Fragmented interpretations across 27 member states complicate multinational rollouts, prompting banks to deploy configurable policy engines capable of local overrides. South America gains momentum as Brazil’s Pix clocked 42 billion transactions in 2024, leading the Central Bank to impose transaction caps and nightly cooling-off periods. The Middle East and Africa regions accelerate adoption of mobile-money fraud analytics to protect unbanked populations joining digital ecosystems.

Competitive Landscape

The fraud detection and prevention market is moderately fragmented, with enterprise software giants, payment network operators, fintech innovators, and consulting players. SAP, Oracle, and IBM cross-sell fraud modules into their existing ERP or core-banking footprints, leveraging entrenched customer relationships but sometimes delivering generic functionality that requires costly tuning. Visa and Mastercard embed scoring in the authorization layer, giving them immediate access to network-wide telemetry yet limiting their horizon to card-based flows. Fintech specialists such as Feedzai, Riskified, and Kount train domain-specific models on proprietary consortium data, winning mid-market merchants seeking rapid integration and consumption pricing.

Consolidation is accelerating as vendors strive to offer platforms that cover identity proofing, transaction monitoring, alert management, and compliance reporting. Worldpay’s 2024 acquisition of Ravelin integrates machine-learning decisioning directly into acquiring rails. Experian’s 2025 purchase of KYC360 merges sanctions screening with identity verification for a single-pane-of-glass approach. Remaining mid-tier suppliers lacking proprietary data or regulatory expertise face margin compression and acquisition pressure. White-space entrants target niches like deepfake voice detection and fraud analytics for decentralized-finance protocols, leveraging agile development cycles and cloud-native pipelines to out-innovate incumbents.

Technology differentiation hinges increasingly on data access. Payment-gateway operators and identity providers hold structural advantages because they generate continuous labeled transaction streams. Pure-software vendors counter by forming collaborative data-sharing consortia that anonymize telemetry while retaining predictive value. Regulatory interest in model governance favors suppliers that expose explainability dashboards, versioning controls, and lineage tracking to compliance officers.

Fraud Detection and Prevention (FDP) Industry Leaders

SAP SE

IBM Corporation

SAS Institute Inc.

ACI Worldwide Inc.

Fiserv Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Visa expanded its Scam Disruption initiative to 15 additional Asia-Pacific and South America markets, enabling real-time sharing of tokenized fraud intelligence among issuers and acquirers.

- January 2026: Mastercard launched an account-to-account payment service in North America using tokenized credentials to compete with domestic real-time rails.

- December 2025: Fiserv partnered with Google Cloud to deliver anti-money-laundering AI within customer-controlled virtual private clouds, easing data-residency concerns.

- November 2025: IBM broadened its fraud detection as a service to include regulatory reporting and case management under a consumption-based model.

- October 2025: FICO introduced a deepfake voice-detection module that analyzes acoustic anomalies to counter voice-cloning attacks.

Global Fraud Detection and Prevention (FDP) Market Report Scope

The Fraud Detection and Prevention Market Report is Segmented by Component (Solutions including Fraud Analytics, Authentication, Reporting, Visualization, and Other Components; Services), Deployment Mode (Cloud, On-premises), Organization Size (Small and Medium Enterprises, Large Enterprises), End-user Industry (BFSI, Retail and E-Commerce, IT and Telecom, Healthcare, Energy and Utilities, Manufacturing, Government and Public Sector, Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Fraud Analytics |

| Authentication | |

| Reporting | |

| Visualization | |

| Other Components | |

| Services |

| Cloud |

| On-premises |

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| Retail and E-Commerce |

| IT and Telecom |

| Healthcare |

| Energy and Utilities |

| Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component | Solutions | Fraud Analytics |

| Authentication | ||

| Reporting | ||

| Visualization | ||

| Other Components | ||

| Services | ||

| By Deployment Mode | Cloud | |

| On-premises | ||

| By Organization Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-user Industry | BFSI | |

| Retail and E-Commerce | ||

| IT and Telecom | ||

| Healthcare | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the fraud detection and prevention market in 2026?

It stands at USD 70.19 billion, up from USD 55.98 billion in 2025.

What is the forecast CAGR for fraud-prevention spending through 2031?

Spending is projected to grow at a 19.61% CAGR between 2026 and 2031.

Which component is growing fastest?

Services, driven by demand for managed model tuning and regulatory reporting, are expanding at a 19.97% CAGR.

Why is Asia-Pacific the fastest-growing region?

Rapid digital-payment adoption and instant-payment rails such as UPI and Pix necessitate real-time analytics, yielding a projected 20.43% CAGR.

What challenge do legacy systems pose to banks?

Fragmented mainframe cores prolong integration timelines to as long as 36 months, increasing deployment costs and delaying ROI.

How are payment networks addressing emerging fraud vectors?

Visa and Mastercard are embedding real-time risk scoring and consortium-based intelligence sharing to block compromised credentials across markets.

Page last updated on: