Epoxy Tooling Board Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

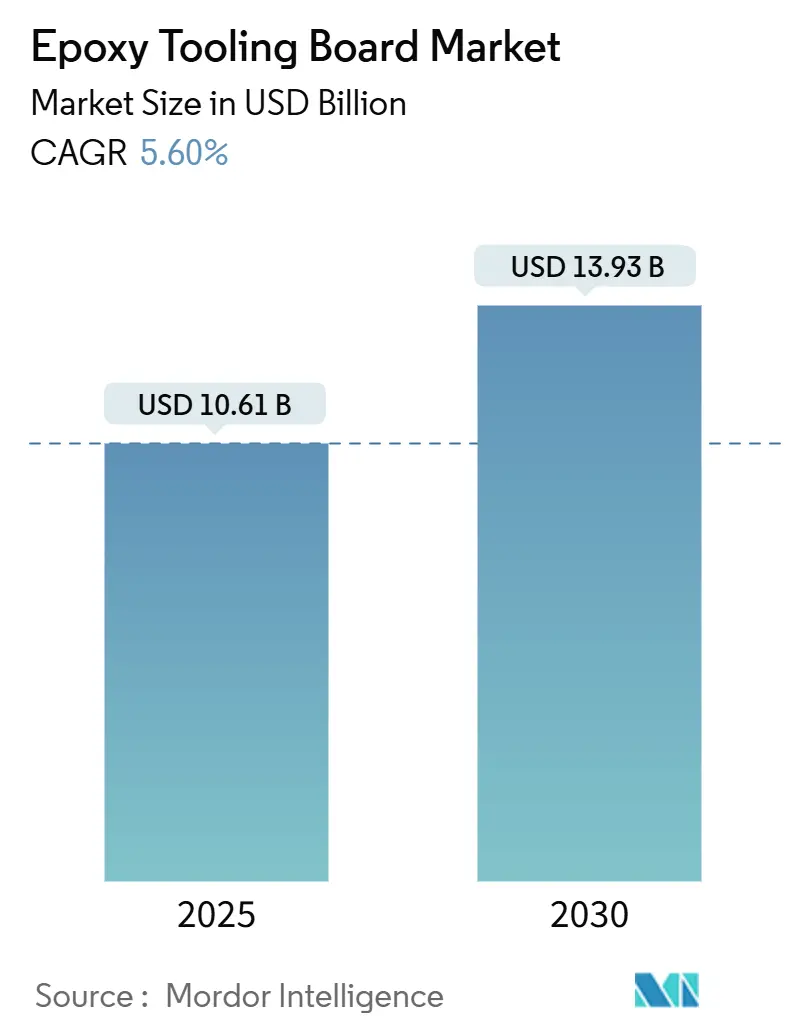

| Market Size (2025) | USD 10.61 Billion |

| Market Size (2030) | USD 13.93 Billion |

| Growth Rate (2025 - 2030) | 5.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Epoxy Tooling Board Market Analysis by Mordor Intelligence

The Epoxy Tooling Board Market size is estimated at USD 10.61 billion in 2025, and is expected to reach USD 13.93 billion by 2030, at a CAGR of 5.60% during the forecast period (2025-2030). Rising demand for recyclable carbon-fiber components in aerospace programs, together with stricter sustainability mandates across advanced manufacturing, underpins consistent volume growth. Robust temperature resistance above 180°C, improved machinability and tight dimensional tolerance are rapidly becoming baseline purchase requirements, prompting suppliers to refine resin chemistries and filler systems. The wind sector’s shift toward 100-meter-plus blades, expanding rapid-prototyping adoption in Chinese automotive plants and the emergence of bio-based epoxies are broadening the end-use profile, allowing new premium-priced grades to command healthy margins. At the same time, antidumping tariffs on Asian epoxy resins and volatile bisphenol-A pricing are forcing both formulators and buyers to diversify raw-material strategies and accelerate testing of bio-based or recycled feedstocks. Competitive intensity remains moderate, but innovation cycles are shortening as tooling producers contend with ever-higher service-temperature expectations and digital-manufacturing workflows.

Key Report Takeaways

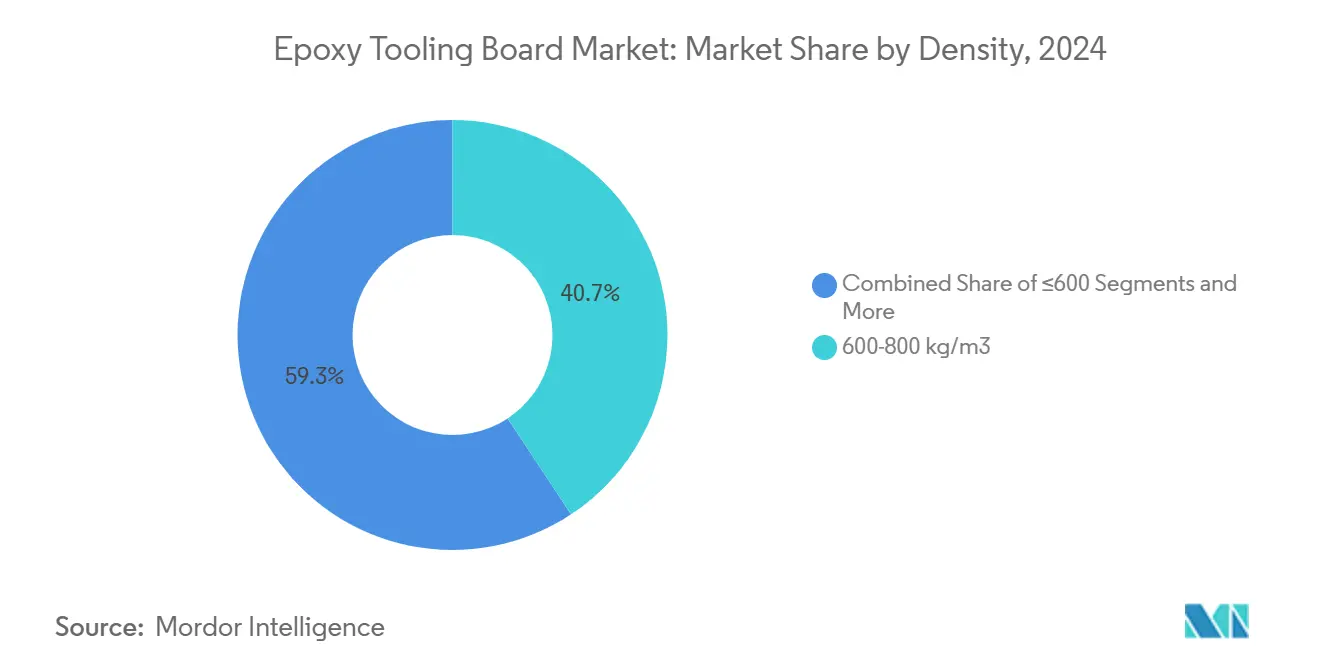

- By density, 600-800 kg/m³ boards captured 40.67% of 2024 revenue; ultra-high-density grades above 1,000 kg/m³ will expand at a 7.95% CAGR to 2030.

- By service temperature, 130-180°C products accounted for 46.54% of the Epoxy tooling board market size in 2024; boards rated above 180°C are set to grow at 9.10% CAGR.

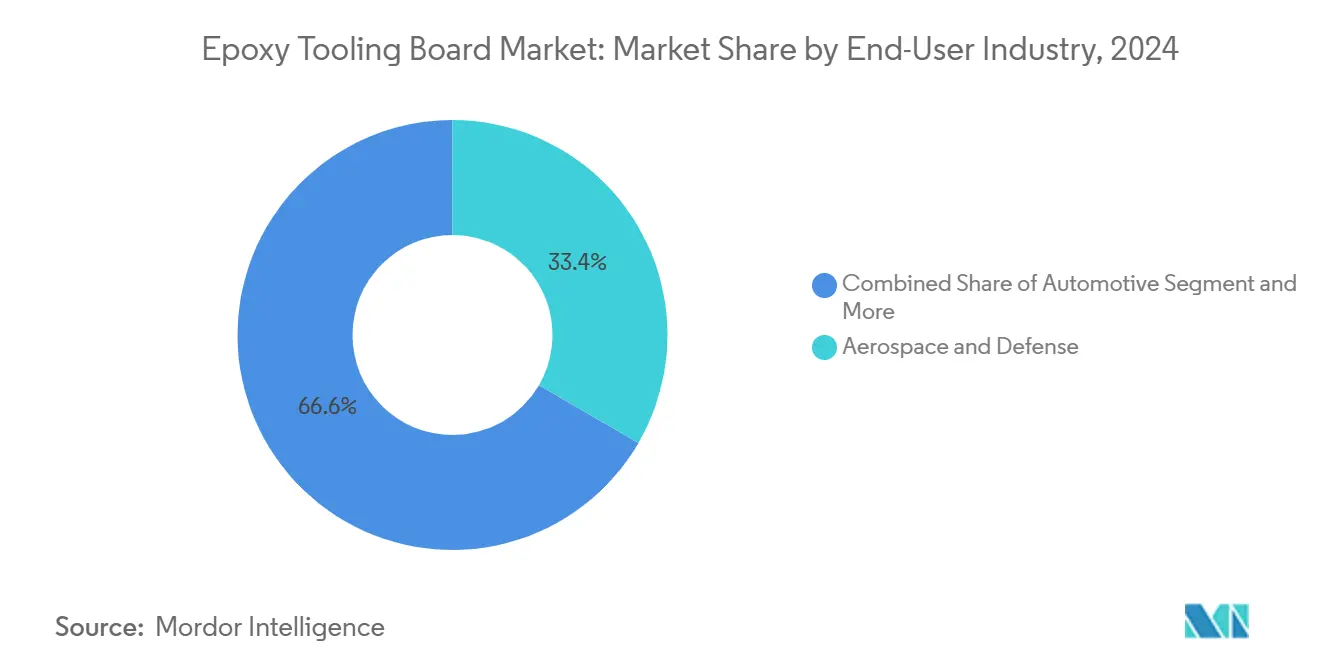

- By end-use industry, aerospace & defense led with 33.35% of the Epoxy tooling board market share in 2024, while wind energy is projected to record the fastest 10.70% CAGR through 2030.

- By distribution channel, direct OEM sales controlled 67.87% of 2024 revenue, whereas authorized distributors are forecast to rise at a 6.55% CAGR.

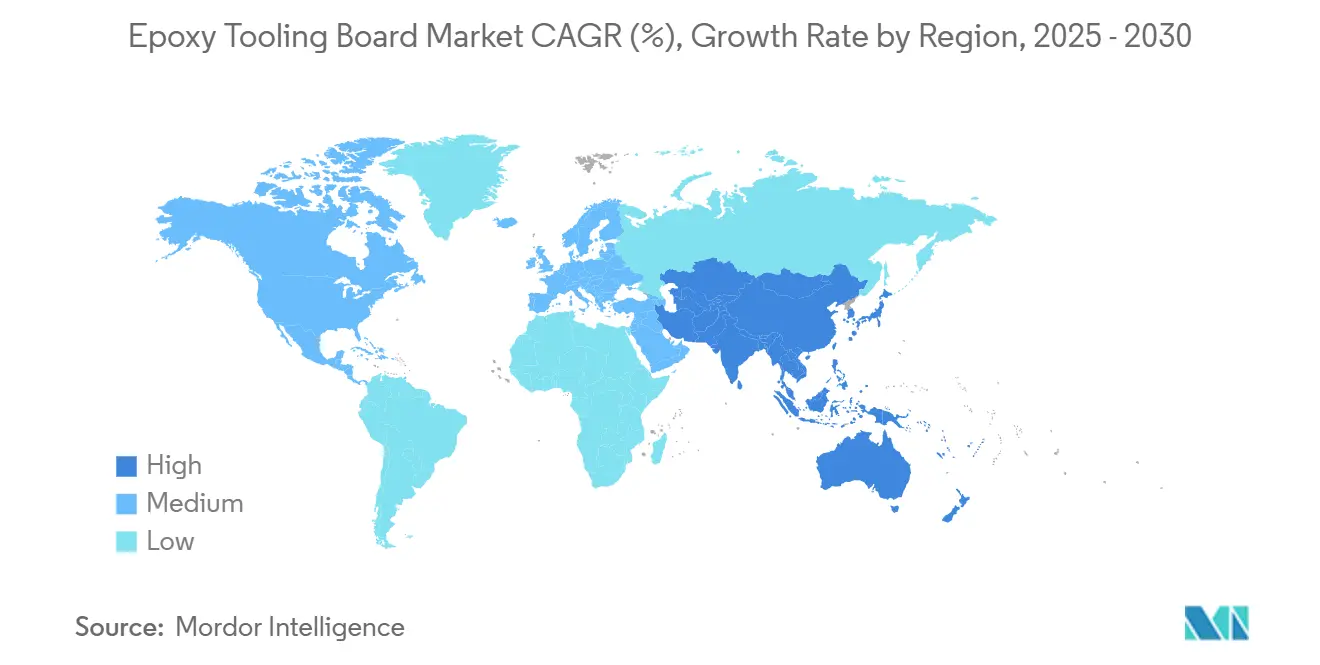

- By geography, North America held 37.78% of 2024 sales, yet Asia-Pacific will post the highest 10.60% CAGR through 2030.

Global Epoxy Tooling Board Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased Demand for Bio-based Epoxy Systems in Aerospace Tooling | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rapid Prototyping Adoption in Chinese Automotive Sector | +0.8% | APAC core, spill-over to global automotive supply chains | Short term (≤ 2 years) |

| Surging Wind-Blade Lengths Driving Large-Scale Master Models | +0.6% | Global, with emphasis on North America, Europe, APAC | Long term (≥ 4 years) |

| European Shift Toward Closed-Mould Composite Fabrication | +0.4% | Europe primary, with adoption spreading to North America | Medium term (2-4 years) |

| Localization of Aircraft MRO in MEA | +0.3% | Middle East & Africa, with regional supply chain benefits | Long term (≥ 4 years) |

| USA Government Tax Incentives for On-Site Wind Turbine Manufacturing | +0.2% | United States, with indirect global supply chain effects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Bio-based Epoxy Systems Transform Aerospace Tooling Economics

Plant-derived epoxies reduce greenhouse-gas footprints by 20–40% while allowing room-temperature carbon-fiber recycling, a capability now validated on production-scale wing-skin tools[1]David Hart, "Plant-Derived Epoxy Resins Enable Recyclable Carbon- Fiber Composites," National Renewable Energy Laboratory, nrel.gov. Sicomin’s GreenPoxy series has seized roughly half of the specialist bio-based segment, demonstrating that glycerol-origin resins can match petro-based performance without cost penalties. The 12% CAGR enjoyed by bio-formulations is realigning procurement policies at leading airframe builders, who increasingly require evidence of end-of-life recyclability alongside 180°C service limits. Tooling suppliers that document life-cycle savings are securing preferred-supplier status, buffering margin pressure, and differentiating against commodity boards.

Chinese Automotive Rapid Prototyping Accelerates Tooling Demand

Automakers in China now collapse mold-fabrication lead times from 16 weeks to under a month by integrating large-format additive printing with epoxy-board finishing, cutting EV concept-cycle costs by nearly 60%. Hybrid tooling methods pair 3D-printed skeletal forms with high-temperature boards for face-skins, preserving surface quality while reducing waste. The model is scaling outward to global tier-1 suppliers that serve transnational OEMs, lifting international demand for mid-density grades that balance machinability and heat resistance.

Wind-turbine Blade Scaling Demands Advanced Master Models

Next-generation blades exceed 100 m and require molds capable of multi-zone heating to assure resin cure uniformity. Direct-printed carbon-fiber molds from Oak Ridge National Laboratory have trimmed typical blade-tool costs from USD 1 million to roughly USD 700,000 while improving cycle accuracy[2]Brian Post, "Large-Scale Additive Manufacturing for Wind-Blade Molds," Oak Ridge National Laboratory, ornl.gov. These economics underpin the double-digit growth of ultra-high-density boards used for master plugs, as they preserve dimensional fidelity under differential thermal loading during long cure cycles.

European Closed-mould Fabrication Reshapes Manufacturing Standards

Compression-molding and RTM lines across Germany, France and the Nordics are shifting toward closed-tool processes to cut VOC emissions by over 90% relative to open-mould lay-ups. The regulatory environment now rewards operators adopting low-emission tooling, spurring demand for boards that hold gloss and flatness at pressures above 6 bar. Epoxy tooling board market suppliers aligning with EN 16516 emissions norms are gaining share in transportation and consumer-durables programs.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Bisphenol-A Prices Impacting Resin Cost Structure | -0.5% | Global, with acute impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Limited Recyclability Versus Thermoplastic Tooling Plates | -0.3% | Europe & North America, driven by regulatory pressures | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Bisphenol-A Price Volatility Disrupts Supply-chain Economics

April 2024 antidumping duties on Chinese, Indian, South Korean, Taiwanese and Thai epoxy resins shifted global BPA trade flows, inflating spot costs by up to 30% during the second half of 2024[3]U.S. International Trade Commission, “Epoxy Resin From China, India, South Korea, Taiwan, and Thailand: Antidumping Investigation," usitc.gov. Tooling board formulators mitigated exposure through dual-sourcing strategies and accelerated qualification of castor-oil-based epoxies. Nevertheless, price swings complicate long-term quoting, pushing OEMs to seek index-linked contracts or stockpiling agreements to stabilize program budgets.

Recyclability Limitations Challenge Sustainability Mandates

Thermoset cross-linking historically barred mechanical recycling, placing epoxy boards at a disadvantage against thermoplastic plates that can be reheated and reshaped. Vitrimeric chemistries now permit bond-exchange reprocessing, but industrial uptake remains nascent. European buyers tasked with achieving 2030 circular-economy targets are scrutinizing end-of-life disposal routes; suppliers offering chemical-recycling take-back schemes are better positioned to comply with extended producer-responsibility rules.

Segment Analysis

By Density: Ultra-high-density Boards Drive Performance Evolution

Ultra-high-density grades above 1,000 kg/m³ generated the fastest 7.95% CAGR outlook thanks to their superior compressive strength and minimal CTE drift at 180°C autoclave settings. In 2024, medium-density 600–800 kg/m³ products still led revenue with 40.7% share, reflecting widespread use in automotive and marine prototypes where cost sensitivity outweighs ultimate heat performance. Gradient-density structures—dense skins over lighter cores—now optimize material usage without sacrificing edge-machinability, a feature increasingly requested by European wind-mold builders.

Enhanced filler technologies and nano-silica dispersion allow ultra-high-density boards to retain machinability, avoiding tool wear issues once endemic to heavy mineral-filled panels. Aerospace OEMs report dimensional drift under 0.02 mm across 2 m spans after 10 thermal cycles, a critical metric for fuselage-section bonding jigs. Cost, while higher, is offset by tool longevity extending beyond 300 cure cycles, reducing lifetime part cost. Low-density boards under 600 kg/m³ continue to carve a niche in pattern-making for furniture or sports goods, where weight reduction simplifies handling and installation.

Note: Segment shares of all individual segments available upon report purchase

By Service Temperature Rating: High-temperature Applications Accelerate Growth

Boards rated 130–180°C maintained 46.6% of 2024 revenue thanks to compatibility with standard aerospace pre-preg cures. Yet the more than 180°C cohort will expand 9.10% annually as next-generation airframe and eVTOL programs cure at 190–200°C to maximize Tg of matrix resins. The Epoxy tooling board market size for high-temperature boards is projected to reach USD 3.9 billion by 2030, reflecting greater tooling volume per aircraft.

Achieving Tg more than 190°C without brittleness required novel cycloaliphatic hardeners and nanoparticulate ceramic fillers, ensuring coefficient-of-thermal-expansion alignment with carbon composite parts. Multi-zone infrared heating cavities paired with distributed thermocouples mitigate thermal gradients across 8-meter wing-skin molds, preserving surface accuracies within ±0.05 mm. Conversely, sub-130°C boards hold steady demand for concept vehicles and consumer-electronics casings, where epoxy tooling board market buyers prioritize rapid machining over high heat.

By End-User Industry: Wind Energy Disrupts Traditional Aerospace Dominance

Aerospace & defense captured 33.4% of 2024 revenue, but wind-energy applications are accelerating at 10.70% CAGR as blade lengths climb and regional localization rules spread. Offshore projects in the United States, United Kingdom, and Taiwan require nacelle-cover and spar-cap molds delivered within 20-week EPC windows, favoring suppliers able to combine 3-axis CNC surfacing with additive sub-structures. Wind energy’s expanding share is narrowing annual volume swings that once correlated solely with aircraft production cycles, stabilizing plant utilization rates for board converters.

Automotive programs centered on battery-electric vehicle enclosures and Class-A exterior panels are adopting mid-density boards for low-pressure compression mould tools, supporting 4–6% yearly volume growth. Marine, railway, and industrial machinery remain niche but profitable segments demanding exceptional corrosion and dimensional stability in humid operating environments. The Epoxy tooling board industry, therefore, benefits from risk diversification across multiple clean-transport vectors, lessening exposure to aeronautical order volatility.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Direct-sales Dominance Faces Distributor Growth

Direct OEM relationships accounted for 67.9% of 2024 turnover as complex applications required close technical collaboration. However, authorized distributors are forecast to outpace at a 6.55% CAGR, extending geographic reach into Southeast Asia, Eastern Europe, and Latin America, where smaller mold shops value local inventory and on-call process advice. E-commerce portals specializing in composites have begun offering cut-to-size board blanks with 72-hour delivery, broadening access for design houses and academic R&D labs.

Global tier-one tooling suppliers now pair web-based selection software with distributor service centers, allowing engineers to simulate deflection and thermal profiles before purchasing a board format. That digital convenience shortens sales cycles but pushes producers to maintain broader SKU ranges, challenging production planning. Meanwhile, direct-sales teams concentrate on high-touch programs such as space-launch structures and hypersonic test hardware, reinforcing premium positioning and safeguarding application data.

Geography Analysis

North America retained 37.8% of 2024 revenue, underpinned by integrated aerospace supply chains and federal incentives that reward domestic wind-turbine nacelle and blade production[4]Federal Aviation Administration, "Advanced Composites Manufacturing Roadmap 2025," faa.gov. United States composite clusters in Washington, Kansas and Alabama anchor demand for ultra-high-temperature boards, while Canada’s Quebec corridor leverages hydroelectric power to lower embodied energy in tool manufacture. Skilled-labor shortages, however, are prompting heavier reliance on automation, elevating demand for precision-machinable board slabs shipped pre-squared and stress-relieved.

Asia-Pacific is the fastest-growing region at 10.60% CAGR on the back of China’s EV platform proliferation, India’s passenger-aircraft-component ambitions, and Japan’s carbon-fiber competency. Government-backed prototyping hubs in Guangzhou, Shanghai, and Pune subsidize mold-shop upgrades that specify higher-density grades, lifting regional price realization. ASEAN nations such as Vietnam and Indonesia attract relocation of marine and furniture composite production, magnifying mid-density board imports and stimulating distributor network expansion.

Europe remains technologically mature but environmentally exacting, prioritizing closed-mould processes that mandate low-emission boards able to withstand higher consolidation pressures. Germany’s automotive giants demand boards machined to Ra 0.8 µm finishing for Class-A outer panels, while Denmark’s offshore-wind OEMs specify gradient-density plugs to minimize thermal lag during 10-hour gel cycles. Tightened waste-disposal directives push suppliers to adopt take-back and chemical-recycling pilots, positioning compliant grades for premium pricing over legacy petro-based boards.

Competitive Landscape

The Epoxy tooling board market features moderate fragmentation. RAMPF Tooling Solutions leverages vertically integrated polyaddition chemistry and multi-plant machining centers to serve aerospace and motorsport customers from Germany and the United States. Trelleborg AB differentiates through low-void, high-compressive-strength plate technology for wind-blade spar-cap molds, backed by onsite technical audits. Huntsman Corporation’s RenShape series benefits from global logistics capacity and ongoing R&D into vitrimeric epoxies that promise recyclability without tooling-temperature compromise.

Strategic alliances accelerate innovation cycles. Airtech Advanced Materials Group and Ascent Aerospace signed an exclusive material-supply pact in 2024 to streamline large-format additive-tooling adoption in fuselage panel applications. Gurit, traditionally strong in structural foam, now cross-sells compatible epoxy boards with glass-skinning systems for wind master plugs, bundling material kits to simplify procurement. Smaller specialists—Alchemie, Curbell Plastics, and OBO Tooling—capture regional niches by offering inventory-on-demand and bespoke machinability additives, often under private-label agreements.

Raw-material disruption is reshaping competitive cost structures. Companies with bio-based formulations partially insulated from BPA swings are winning long-term supply awards with European OEMs. Conversely, formulators reliant on imported bisphenol-A face margin compression until hedging strategies or alternative feedstocks mature. Digital-manufacturing compatibility, especially the ability to validate board behavior in finite-element simulations, is emerging as a new bid-qualification criterion among aerospace primes. Companies investing in material-database integration with major CAD/CAE suites are therefore capturing higher-value programs.

Epoxy Tooling Board Industry Leaders

-

Trelleborg AB

-

RAMPF Tooling Solutions

-

Huntsman Corporation

-

Base Group

-

Curbell Plastics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Norco Composites doubled its CNC and kit-cutting floor to 16,000 sq ft and installed advanced routers and waterjets to meet rising demand for precision-machined epoxy-board components.

- December 2024: Norco added a 6-axis 3D printer and subtractive 5-axis machining line, enabling rapid prototype tooling for marine, aerospace and automotive parts while reducing waste through near-net-shape printing.

- September 2024: Airtech Advanced Materials Group and Ascent Aerospace entered an exclusive supply agreement for large-format additive-manufacturing tooling in aerospace programs.

- July 2024: Lyons Industries deployed a Massivit 10000 printer to slash fiberglass-mold lead times from 16 weeks to 3–4 weeks for bath-ware components.

Global Epoxy Tooling Board Market Report Scope

| Less than 600 kg /m³ |

| 600–800 kg /m³ |

| 800–1000 kg /m³ |

| More than 1 000 kg /m³ |

| Less than 130 °C |

| 130–180 °C |

| More than 180 °C |

| Aerospace & Defense |

| Automotive |

| Marine |

| Wind Energy |

| Railway |

| Industrial Equipment |

| Others (Medical Devices, Consumer Products, etc.) |

| Direct Sales (OEMs) |

| Authorized Distributors |

| Others (Online Technical Distributors, Third-Party Service providers, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Density | Less than 600 kg /m³ | |

| 600–800 kg /m³ | ||

| 800–1000 kg /m³ | ||

| More than 1 000 kg /m³ | ||

| By Service Temperature Rating | Less than 130 °C | |

| 130–180 °C | ||

| More than 180 °C | ||

| By End-Use Industry | Aerospace & Defense | |

| Automotive | ||

| Marine | ||

| Wind Energy | ||

| Railway | ||

| Industrial Equipment | ||

| Others (Medical Devices, Consumer Products, etc.) | ||

| By Distribution Channel | Direct Sales (OEMs) | |

| Authorized Distributors | ||

| Others (Online Technical Distributors, Third-Party Service providers, etc.) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Epoxy tooling board market?

The market stands at USD 10.61 billion in 2025 and is forecast to grow to USD 13.93 billion by 2030 at a 5.60% CAGR.

Which end-use industry is expanding fastest?

Wind energy applications are posting the quickest growth, advancing at 10.70% CAGR as blade lengths exceed 100 m and require sophisticated large-scale molds.

Why are bio-based epoxies gaining traction in tooling applications?

Plant-derived resins cut greenhouse-gas emissions by up to 40% and enable recyclable carbon-fiber composites, helping aerospace OEMs satisfy sustainability mandates without sacrificing 180 °C service temperatures.

How will antidumping duties influence supply chains?

US tariffs on Asian epoxy resins are inflating bisphenol-A costs and motivating board formulators to diversify feedstocks toward bio-based alternatives to stabilize pricing and ensure availability.