Diodes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

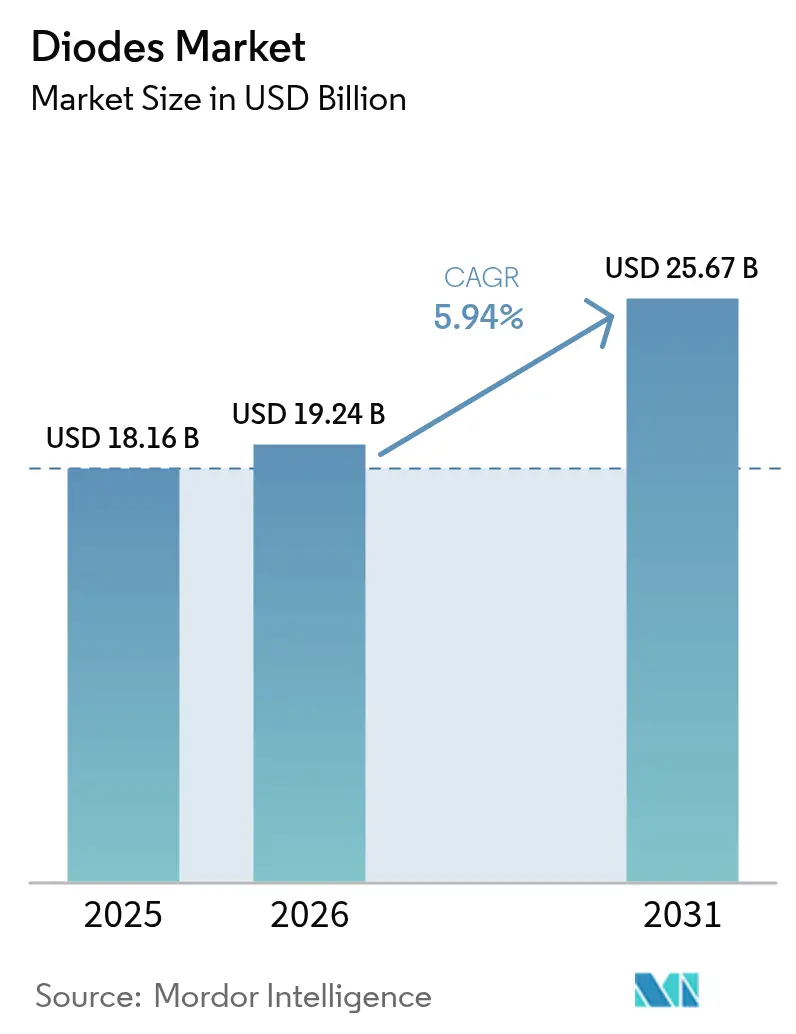

| Market Size (2026) | USD 19.24 Billion |

| Market Size (2031) | USD 25.67 Billion |

| Growth Rate (2026 - 2031) | 5.94% CAGR |

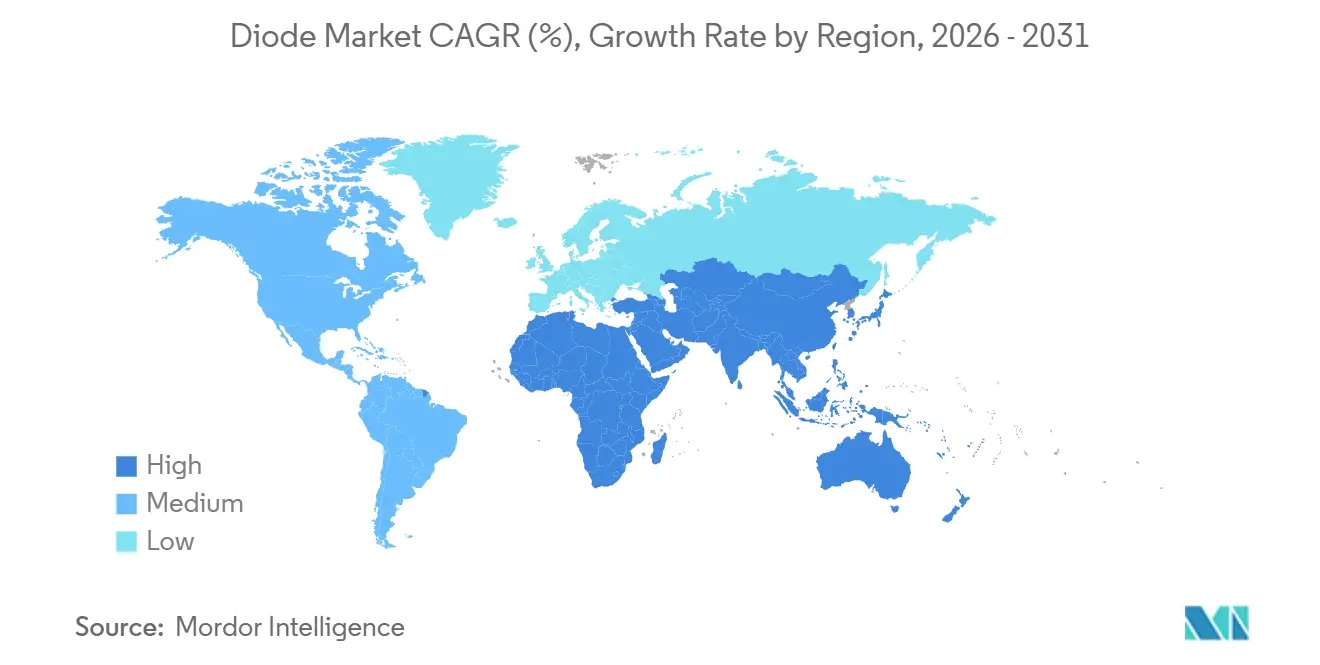

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Diodes Market Analysis by Mordor Intelligence

The diodes market size is projected to expand from USD 18.16 billion in 2025 to USD 19.24 billion in 2026 and reach USD 25.67 billion by 2031, registering a 5.94% CAGR from 2026 to 2031. Sovereign incentives to localize semiconductor fabs, rapid electrification in automotive and industrial systems, and the proliferation of edge-computing devices that demand faster switching and tighter voltage regulation are steering growth. Product-mix shifts toward wide-bandgap materials are lifting average selling prices even as volumes rise. Concurrently, onshore gallium nitride capacity additions under the CHIPS and Science Acts are compressing lead times for power-diode modules, while global 5G rollouts continue to enrich diode content per radio. Regulatory frameworks such as the European Union’s WEEE Directive are shortening replacement cycles for consumer electronics, indirectly supporting unit volumes.

Key Report Takeaways

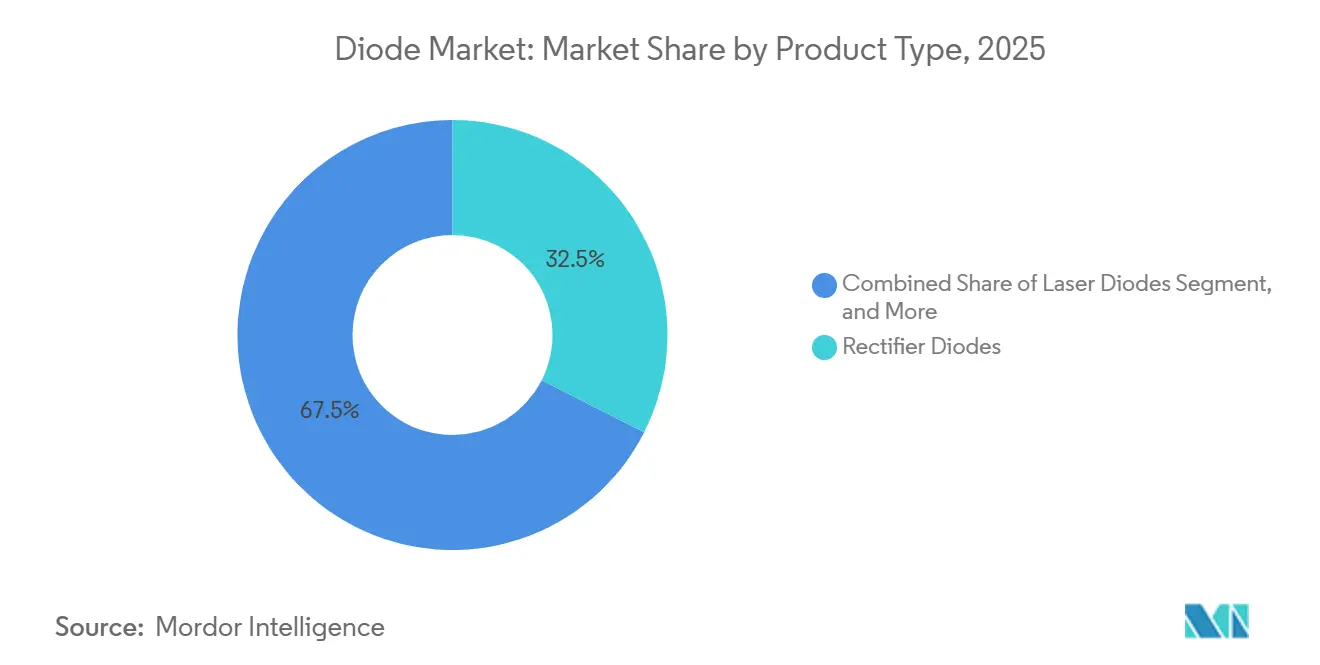

- By product type, rectifier diodes led with a 32.46% revenue share in 2025, whereas laser diodes are advancing at a 7.54% CAGR to 2031.

- By material, silicon accounted for 66.42% of the diodes market share in 2025, while gallium-nitride devices are projected to grow at a 6.91% CAGR through 2031.

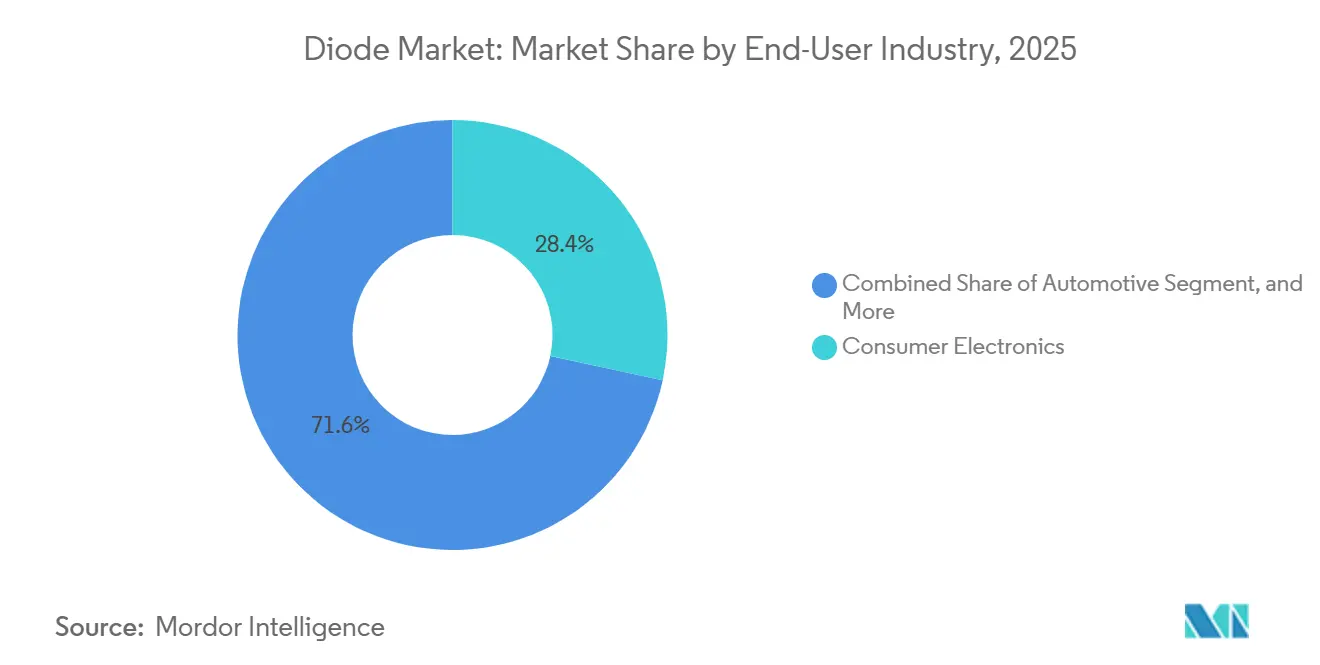

- By end-user, automotive electrification is posting the highest CAGR of 7.59% during 2026-2031, overtaking the 28.37% share held by consumer electronics in 2025.

- By mounting package, surface-mount devices secured 48.91% of the diodes market share in 2025, and flip-chip packages are on course for a 6.77% CAGR through 2031.

- By geography, Asia-Pacific accounted for 47.34% of 2025 sales; however, the Middle East and Africa is forecast to grow at a 6.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Diodes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitization of Consumer Electronics Ecosystems | +1.2% | Global, with concentration in Asia-Pacific manufacturing hubs (China, South Korea, Vietnam) | Medium term (2–4 years) |

| Acceleration of EV Production and On-Board Chargers | +1.5% | Global, early gains in China, Europe, North America; spillover to India and Southeast Asia | Medium term (2–4 years) |

| 5G Roll-Out Driving Demand for RF and Microwave Diodes | +0.9% | North America and Europe for infrastructure; Asia-Pacific for handset integration | Short term (≤2 years) |

| Data-Center Efficiency Mandates Boosting Power Diodes | +1.1% | North America and Europe for hyperscale facilities; Asia-Pacific for edge deployments | Short term (≤2 years) |

| Regulatory Tailwinds for GaN-on-Si High-Voltage Diodes | +0.8% | United States (CHIPS Act), European Union (Chips Act), Japan (economic security subsidies) | Long term (≥4 years) |

| E-Waste Recycling Laws Increasing Replacement Rates | +0.4% | European Union (WEEE Directive), select Asian markets (Japan, South Korea) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Digitization of Consumer Electronics Ecosystems

Smartphones and wearables embed ever-denser power-management ICs that combine multiple diode functions onto a single substrate, reducing board area and lowering assembly spend.[1]Microchip Technology, “Power Management IC Trends,” microchip.com Schottky and small-signal diodes rated below 1 A but switching in nanoseconds, protect always-on sensors and wireless-charging coils. Edge-AI accelerators raise thermal design power envelopes, forcing OEMs to adopt transient-voltage-suppressor diodes with higher energy ratings. Portfolios are therefore bifurcating into ultra-miniature devices for tight spaces and ruggedized variants for compute-heavy subsystems, both priced at premiums to legacy discretes. Growth is magnified as USB4 and Thunderbolt 5 interfaces deliver up to 240 W of power, increasing the protection-diode content per port.

Acceleration of EV Production and on-Board Chargers

Global electric-vehicle sales surpassed 14 million units in 2024, and 800-V architectures are halving charging times, which mandates silicon-carbide Schottky diodes in power-factor-correction stages.[2]International Energy Agency, “Global EV Outlook 2024,” iea.org Automakers are embedding laser diodes in solid-state LiDAR, with in-vehicle revenue forecast to reach USD 11.9 billion by 2032. Junction-temperature ceilings now exceed 175 °C, favoring wide-bandgap chemistries. Dual growth vectors emerge: high-voltage power conversion and laser-based sensing, each requiring distinct diode chemistries and packages. Government tax credits on zero-emission vehicles accelerate platform launches, further boosting the diodes market.

5G Roll-Out Driving Demand for RF and Microwave Diodes

Operators deployed more than 2 million 5 G base stations in 2024, each macro cell integrating up to 128 antenna elements that use PIN diodes for transmit-receive switching and varactor diodes for beam steering.[3]Ericsson, “5 G Infrastructure Deployment,” ericsson.com Millimeter-wave adoption above 24 GHz is exposing insertion-loss limits in legacy gallium-arsenide PIN diodes, prompting trials of indium-phosphide alternatives with 0.3 dB lower loss at 28 GHz. Handsets integrate multiple RF front-end modules embedding Schottky detector diodes for envelope tracking. Overall, diode content per radio rises by 30-40% compared with 4G, and this trend will compound as small-cell and private networks proliferate. Spectrum auctions scheduled through 2027 keep the deployment pipeline full, locking in visibility into demand.

Data-Center Efficiency Mandates Boosting Power Diodes

Hyperscale operators target power-usage-effectiveness below 1.15; server supplies are moving from 80 PLUS Titanium to synchronous rectification with silicon-carbide Schottky diodes to shave 1-2 percentage points of conduction losses. Liquid-cooled AI clusters are adopting 48 V rack distribution, requiring high-current rectifiers rated at 100 A or higher. The U.S. Department of Energy’s wide-bandgap roadmap projects 99% converter efficiency, an annual 20 TWh saving opportunity. Operators refresh power modules every 3-4 years, down from the historical 5-7, quickening diode replacement cycles. Public carbon-neutrality pledges further institutionalize this upgrade cadence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Price Volatility (Si, GaAs, GaN) | -0.7% | Global, acute in regions dependent on Chinese gallium exports (North America, Europe) | Short term (≤2 years) |

| Supply Chain Fragmentation amid Geopolitical Trade Restrictions | -0.5% | United States, China, European Union (export controls, tariffs, entity lists) | Long term (≥4 years) |

| Thermal Limitations in High-Current Packages | -0.4% | Global, particularly in automotive and industrial high-power applications | Medium term (2–4 years) |

| Patent Congestion in WBG Semiconductor Processes | -0.3% | Global, concentrated in United States, Europe, Japan, South Korea (litigation hotspots) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Si, GaAs, GaN)

China commands 98% of gallium refining, and its 2024 export license regime doubled spot prices within months. Gallium-arsenide wafer costs climbed 15-20% YoY in 2024, squeezing RF-diode margins for suppliers without offtake hedges. The European Union awarded a Greek startup a contract to build a 500-tpa gallium plant, yet it would still serve only under 5% of global demand. Silicon-carbide wafer lead times remain 26-30 weeks despite expansions by Wolfspeed and ROHM. Until diversified sources mature, procurement risk tempers diodes market expansion.

Thermal Limitations in High-Current Packages

Diodes above 50 A can exceed 150 °C junction temperatures; epoxy-molded packages with 1.5-2.0 K/W thermal resistance necessitate bulky heat sinks that offset the size benefits of wide-bandgap devices. Flip-chip or direct-bonded-copper packages lower resistance to 0.5-0.8 K/W but cost 40-60% more. Automotive designers investigate double-sided cooling and embedded-die boards, adding up to USD 1 million in non-recurring engineering per platform. Standardized thermal interfaces have yet to emerge, confining these premium modules to high-end EV and industrial drives and slowing mass-market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Laser Diodes Propel Autonomous Sensing

Rectifier products captured 32.46% of the diodes market share in 2025, supported by almost universal AC-DC conversion needs across consumer electronics and industrial power supplies. Laser devices, although smaller in volume, are forecast to expand at a 7.54% CAGR through 2031 as solid-state LiDAR gains favor in passenger vehicles and telecom operators upgrade long-haul fiber backbones. Schottky units continue to migrate into 800-V electric-vehicle platforms for their low forward-voltage drop, while Zener references remain staples in battery-management circuits that guard analog-to-digital converters from overvoltage events. Small-signal diodes dominate switching roles under 1 A, and transient-voltage-suppressor parts are proliferating in high-speed USB-C and Thunderbolt ports, each of which now handles up to 240 W of bidirectional power. RF and microwave variants underpin 5G radio front ends, enabling beam-forming arrays to toggle thousands of times per second with minimal insertion loss.

The laser slice of the diodes market size is set to widen as automakers favor 905-nm edge-emitting and 940-nm vertical-cavity surface-emitting devices that balance range with eye safety. Content per vehicle will also rise because next-generation headlamps bundle dozens of laser pixels to enable adaptive high-beam patterns. On the rectifier side, renewable-energy inverter makers are switching from 600-V silicon to 1,200-V silicon-carbide parts, slightly tempering demand for mainstream silicon diodes but creating a premium sub-segment. Suppliers able to co-package multiple diode functions, rectification, voltage clamping, and ESD protection into a single outline are commanding higher average selling prices. Overall, the product mix shift is expected to lift blended margins, even in moderate unit growth environments.

By Material Type: Gallium Nitride Gains Traction

Silicon maintained a 66.42% foothold in 2025, translating into the largest diodes market share, thanks to decades of yield optimization that have kept the cost per ampere under USD 0.01. Wide-bandgap gallium-nitride devices, however, are forecast to post a 6.91% CAGR through 2031 as hyperscale data-center operators target 99% conversion efficiency and automotive engineers chase cooler on-board chargers. Silicon-carbide alternatives are rising at a comparable 6.5% CAGR, buoyed by solar inverters and traction drives that require 1,200-V blocking capability. Gallium arsenide remains the incumbent for RF and microwave diodes in 5G base stations, though indium phosphide pilots threaten its dominance in millimeter-wave applications. Experimental substrates such as diamond and aluminum nitride still sit below 1% but attract R&D investment for post-2030 deployment.

The gallium-nitride slice of the diodes market will expand faster in North America and Europe, where CHIPS-funded fabs shorten lead times and reduce supply-chain risk. Silicon, though slower, retains an indispensable role in safety-critical analog circuits that require proven long-term reliability and established IEC 60747 compliance. Silicon-carbide output is climbing on larger 200-mm wafers, narrowing cost gaps and making the material viable for mid-tier EVs. Meanwhile, gallium-arsenide vendors face price headwinds from gallium export restrictions, prompting them to pursue long-term supply contracts. Each chemistry, therefore, occupies a well-defined performance-versus-cost niche, giving multilayer boards a wider palette of diode options.

By End-User Industry: Automotive Electrification Accelerates

Consumer electronics accounted for 28.37% of 2025 demand, fueled by diode proliferation in smartphones, tablets, and wearables that integrate increasingly power-dense management ICs. Automotive applications, however, are on pace for a 7.59% CAGR to 2031, making them the fastest-growing vertical as electric-vehicle volumes rise and advanced driver-assistance systems embed laser-based sensing. Communications infrastructure is expected to post a 6.2% CAGR on the back of 5G densification, with each macro cell housing up to 128 PIN and varactor diodes for beam steering. Defense and aerospace buyers, although limited in unit volume, pay premiums for radiation-hardened devices, while computer peripherals and industrial automation maintain solid mid-single-digit trajectories. LED-based lighting, as it shifts to micro-LEDs, continues to require tight current regulation to sustain small-signal diode volumes.

Automotive’s share of the diodes market size will climb as every new battery-electric vehicle contains 50–100 power diodes across traction inverters, DC-DC converters, and on-board chargers. Battery cell gigafactories in Canada, Germany, and Japan are leaning on silicon-carbide Schottky diodes to curb thermal runaway risks, lifting demand for devices rated above 175 °C. In communications, low-earth-orbit satellite constellations require gallium-nitride microwave diodes that withstand temperature cycling from –150 °C to +120 °C, extending supplier reach beyond terrestrial networks. Consumer electronics will stabilize as smartphone unit growth flattens, but wireless-charging coils and always-on sensors will nudge diode content per handset higher. Altogether, shifting end-user priorities are reshaping order books toward higher-value but lower-volume automotive and infrastructure segments.

By Mounting Package: Flip-Chip Gains Momentum

Surface-mount outlines commanded 48.91% of 2025 revenue by aligning with automated pick-and-place assembly and JEDEC-standard footprints. Flip-chip packages, although with only a mid-single-digit share today, are forecast to grow at a 6.77% CAGR through 2031 as smartphone and wearable designers pursue profiles under 0.5 mm and thermal resistance below 1 K/W. Through-hole formats slip toward 22% as legacy industrial boards refresh to surface-mount, while chip-scale packages rise at 6.1% thanks to RF front-end modules and battery-powered IoT devices. Direct-bonded-copper options are also gaining in 48-V automotive systems, offering superior heat spreading at modest area penalties.

Flip-chip’s share of the diodes market will grow fastest in consumer electronics, where board area is at a premium and single-digit Kelvin-per-watt performance is mandatory for high-refresh-rate displays. In automotive zones, double-sided cooling substrates paired with flip-chip diodes slash cooler mass by 30%, offsetting the higher component cost. Chip-scale units thrive in 5G handsets because their perimeter solder pads let antenna modules shrink without sacrificing RF integrity. Surface-mount will still dominate industrial retrofits that favor proven reliability over incremental miniaturization, while through-hole will remain entrenched in harsh-environment applications that require extra mechanical robustness. The packaging landscape, therefore, fragments along end-use and thermal-budget lines, giving contract manufacturers an ever-broader toolkit to optimize performance and cost.

Geography Analysis

Asia-Pacific accounted for 47.34% of the diodes market share in 2025 and is projected to post a 5.7% CAGR through 2031, anchored by China’s surge in electric-vehicle manufacturing and Japan’s accelerating demand for silicon-carbide power devices. Factory-incentive programs in India and capacity diversification into Vietnam, Thailand, and Malaysia are broadening regional supply, while South Korea’s sub-5 nm fabs are driving extra electrostatic-discharge protection content. Content per unit is also rising because consumer-electronics brands are adding wireless-charging coils and always-on sensors, each requiring multiple transient-voltage-suppressor diodes.

North America accounted for roughly 24% of the 2025 diodes market and is set to expand at a 5.5% CAGR as CHIPS Act funding cuts gallium-nitride lead times and hyperscale data-center operators replace legacy silicon rectifiers with wide-bandgap alternatives. Canada’s new battery-cell plants are integrating silicon-carbide Schottky diodes rated at 175 °C, and Mexico’s auto-electronics corridor is embedding high-current TVS devices in wiring harnesses. Europe captured a 19% share in 2025 and should climb at a 5.3% CAGR, propelled by EUR 43 billion in Chips Act subsidies that underwrite new gallium-nitride pilot lines in France and silicon-carbide fabs in Germany.

The Middle East and Africa secured 6% of global revenue in 2025 and are forecast to deliver the fastest CAGR of 6.96% to 2031, fueled by sovereign artificial-intelligence data centers in Saudi Arabia and the United Arab Emirates, whose 100 MW GPU clusters demand ultra-efficient rectification. South Africa’s solar-inverter boom is adopting silicon-carbide diodes to raise grid-tied efficiency, while Egypt’s contract assemblers are adding flip-chip lines that shorten regional lead times. South America, at 4% share in 2025, is likely to grow 5.4% annually as Brazil and Argentina scale up electric-bus production and industrial-automation retrofits, though currency volatility keeps capex cycles cautious.

Competitive Landscape

The five largest vendors, Infineon Technologies, STMicroelectronics, Vishay Intertechnology, Diodes Incorporated, and onsemi, collectively accounted for about 35–40% of 2025 revenue, confirming a moderately fragmented structure in which regional specialists and fabless wide-bandgap entrants can still gain design wins. Scale advantages let the leaders internalize epitaxy, assembly, and test, driving cost per ampere to sub-cent levels in high-volume silicon lines. New entrants counter by focusing on gallium nitride or silicon carbide niches where efficiency gains justify price premiums.

Strategic investment remained brisk: Infineon is spending USD 5.5 billion on a Dresden fab that will co-package silicon-carbide diodes with gate drivers, while STMicroelectronics is allocating EUR 5 billion to expand Catania capacity for 300-mm silicon-carbide wafers. Wolfspeed’s USD 750 million Mohawk Valley expansion targets 200-mm substrates, and GlobalFoundries has earmarked USD 95 million of CHIPS funds to lift gallium-nitride output in Vermont. Fabless innovators such as Navitas and GaN Systems license IP to foundries, compressing product-refresh cycles and sidestepping multi-billion-dollar capex.

Cross-licensing agreements among Infineon, Wolfspeed, and ROHM have eased patent congestion, accelerating technology diffusion to tier-2 suppliers. Quality standards ISO 9001 and IATF 16949 continue to favor incumbents with robust automotive track records, yet generous subsidies under the CHIPS and Science Act and the European Union Chips Act are lowering entry barriers for startups and university spin-offs. Overall, customer preference for higher efficiency and faster switching is gradually shifting revenue toward wide-bandgap specialists, even as entrenched silicon lines defend price-sensitive segments.

Diodes Industry Leaders

Alpha and Omega Semiconductor Ltd.

Central Semiconductor Corp.

Wolfspeed Inc.

Diodes Incorporated

GlobalFoundries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Wolfspeed announced a USD 750 million expansion of its Mohawk Valley fab in New York to produce 200-mm silicon-carbide wafers for automotive and industrial modules, with output slated for H2 2027.

- December 2025: STMicroelectronics committed EUR 5 billion (USD 5.5 billion) to expand its Catania facility, adding 300-mm silicon-carbide epitaxy and 200-mm gallium-nitride lines for European automotive clients, first wafers scheduled for Q3 2027.

- November 2025: Infineon Technologies acquired GaN Systems for USD 830 million, integrating gallium-nitride IP and broadening its power-diode catalog for data-center and EV uses.

- October 2025: Renesas Electronics invested USD 1.2 billion in its Kofu plant to double silicon-carbide diode capacity aimed at Japanese and North American EV inverters.

Global Diodes Market Report Scope

The Diodes Market Report is Segmented by Product Type (Schottky Diodes, Zener Diodes, Rectifier Diodes, Laser Diodes, Small-Signal Diodes, Electrostatic Discharge Protection Diodes, Transient Voltage Suppressor Diodes, RF and Microwave Diodes), Material Type (Silicon Diodes, Silicon Carbide Diodes, Gallium Nitride Diodes, Gallium Arsenide Diodes, Other Material Types), End-User Industry (Communications, Consumer Electronics, Automotive, Defense and Aerospace, Computer and Peripherals, Industrial, Lighting, Other End-User Industries), Mounting Package (Through-Hole, Surface-Mount, Chip-Scale Package, Flip-Chip), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Schottky Diodes |

| Zener Diodes |

| Rectifier Diodes |

| Laser Diodes |

| Small-Signal Diodes |

| Electrostatic Discharge Protection Diodes |

| Transient Voltage Suppressor Diodes |

| RF and Microwave Diodes |

| Silicon Diodes |

| Silicon Carbide Diodes |

| Gallium Nitride Diodes |

| Gallium Arsenide Diodes |

| Other Material Types |

| Communications |

| Consumer Electronics |

| Automotive |

| Defense and Aerospace |

| Computer and Peripherals |

| Industrial |

| Lighting |

| Other End-User Industries |

| Through-Hole |

| Surface-Mount |

| Chip-Scale Package |

| Flip-Chip |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Schottky Diodes | ||

| Zener Diodes | |||

| Rectifier Diodes | |||

| Laser Diodes | |||

| Small-Signal Diodes | |||

| Electrostatic Discharge Protection Diodes | |||

| Transient Voltage Suppressor Diodes | |||

| RF and Microwave Diodes | |||

| By Material Type | Silicon Diodes | ||

| Silicon Carbide Diodes | |||

| Gallium Nitride Diodes | |||

| Gallium Arsenide Diodes | |||

| Other Material Types | |||

| By End-User Industry | Communications | ||

| Consumer Electronics | |||

| Automotive | |||

| Defense and Aerospace | |||

| Computer and Peripherals | |||

| Industrial | |||

| Lighting | |||

| Other End-User Industries | |||

| By Mounting Package | Through-Hole | ||

| Surface-Mount | |||

| Chip-Scale Package | |||

| Flip-Chip | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the global diode market?

The diode market size reached USD 18.16 billion in 2025 and is projected to hit USD 19.24 billion in 2026.

How fast is the automotive sector growing in diode demand?

Automotive applications are forecast to expand diode consumption at a 7.59% CAGR between 2026 and 2031.

Which material platform is gaining the most traction?

Gallium-nitride diodes are advancing at a 6.91% CAGR, the fastest among material types.

Which region will see the quickest diode market growth?

Middle East and Africa is expected to post a 6.96% CAGR through 2031, outpacing all other regions.

What packaging format is growing fastest for diodes?

Flip-chip packages are set for a 6.77% CAGR as designers chase ultra-low-profile assemblies.

Who are the leading companies in the diode space?

Infineon Technologies, STMicroelectronics, Vishay Intertechnology, Diodes Incorporated, and onsemi collectively hold about 35-40% of global revenue.

Page last updated on: