Market Overview

| Study Period | 2019 - 2030 |

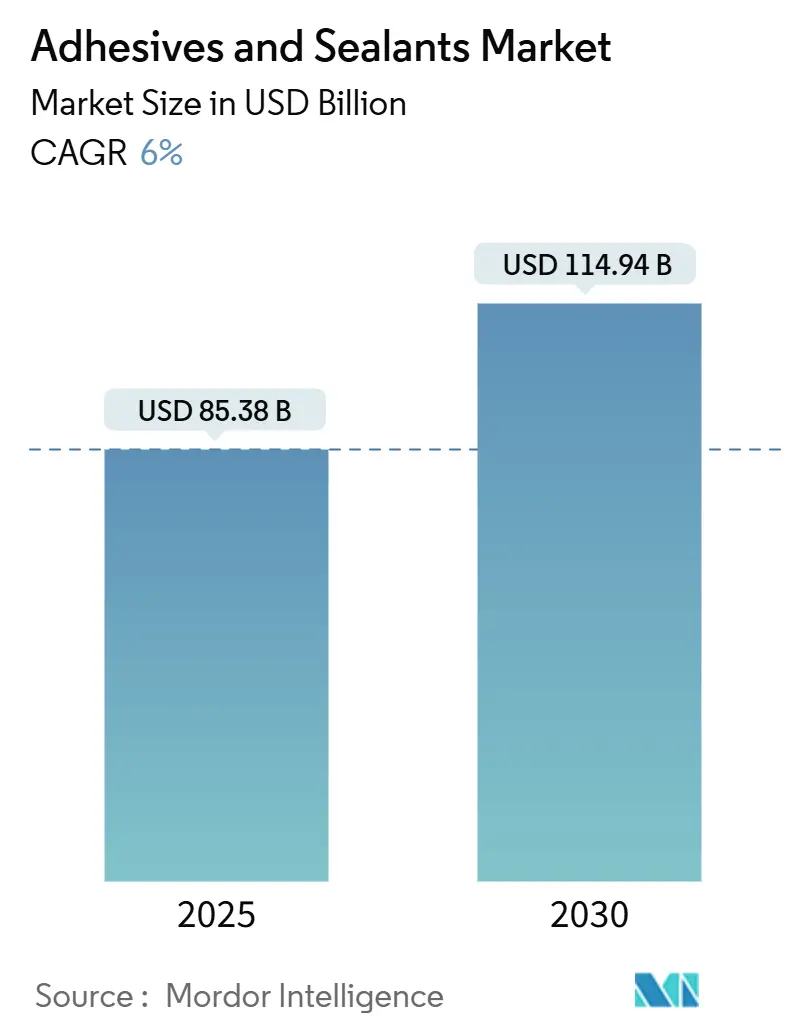

| Market Size (2025) | USD 85.38 Billion |

| Market Size (2030) | USD 114.94 Billion |

| Growth Rate (2025 - 2030) | 6.00% CAGR |

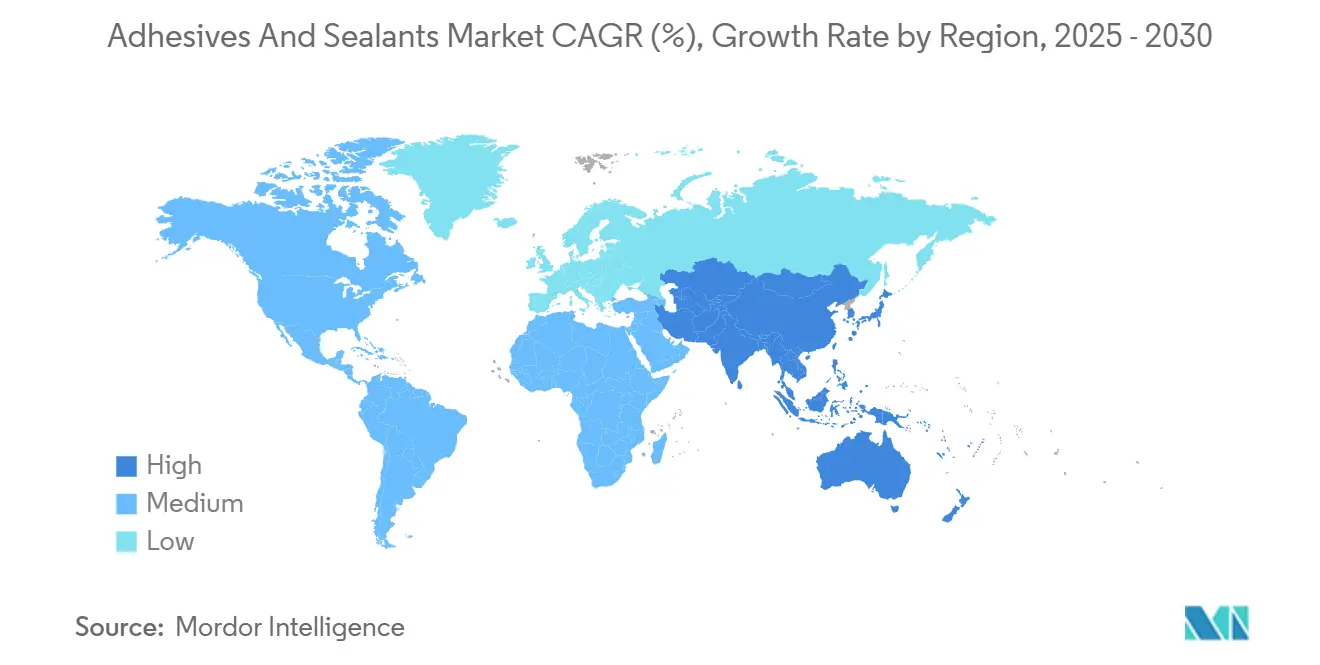

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Adhesives And Sealants Market Analysis by Mordor Intelligence

The Adhesives And Sealants Market size is estimated at USD 85.38 billion in 2025, and is expected to reach USD 114.94 billion by 2030, at a CAGR of 6% during the forecast period (2025-2030). Strong gains stem from rising demand for high-performance bonding solutions that support light-weighting in vehicles, automated e-commerce packaging, and modular construction. Regulatory pressure for lower-emission chemistries, especially under the EU Green Deal, is accelerating the shift toward bio-based and low-VOC formulations. Asia-Pacific remains the growth engine, supported by industrial expansion and infrastructure spending, while North America and Europe focus on technology upgrades that meet strict sustainability rules. Supply chain fragility for isocyanates and acrylic monomers continues to influence pricing, prompting producers to diversify feedstocks and invest in bio-based routes. Competitive dynamics are increasingly shaped by silicone and reactive technologies, which promise superior durability, higher temperature resistance, and improved processing speeds.

Key Report Takeaways

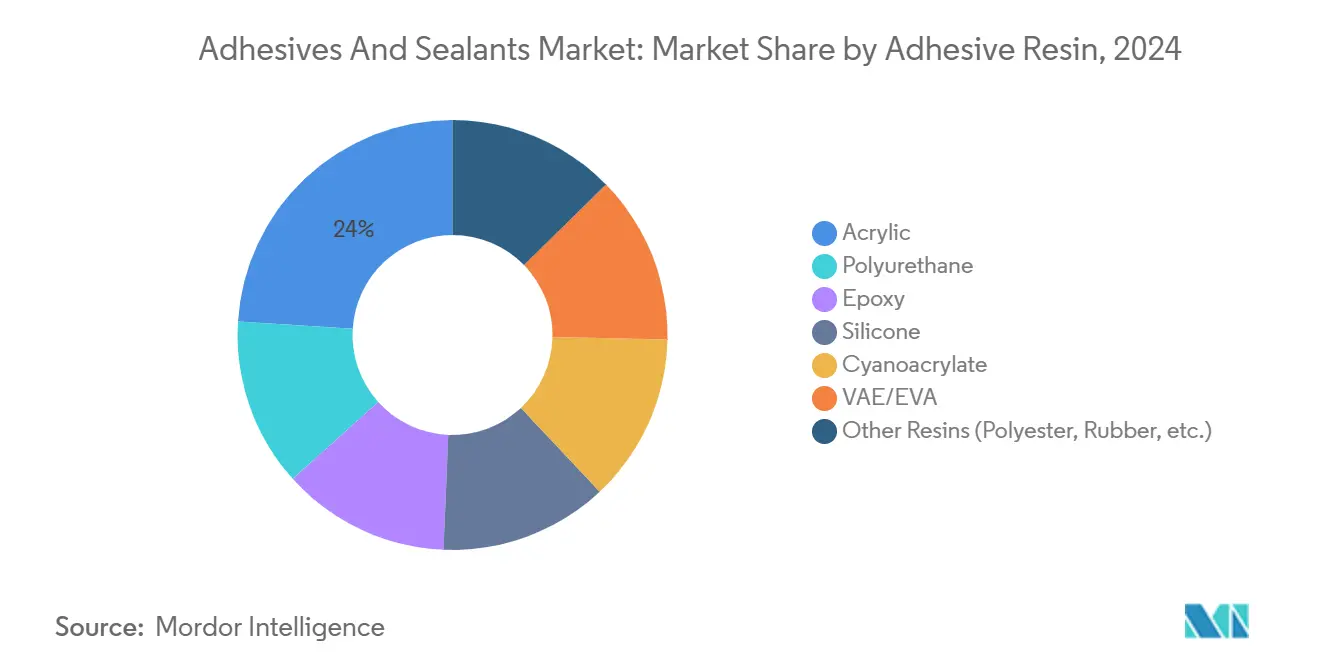

- By resin, acrylics held 24% of the adhesives and sealants market in 2024, while silicone resins are expected to expand at 8.50% CAGR over 2025-2030.

- By technology, water-based solutions accounted for 42% revenue in 2024; reactive systems are forecast to post the fastest 8.20% CAGR to 2030.

- By sealant resin, silicone captured 45% revenue in 2024; polyurethane sealants are on track for a 5.70% CAGR over the outlook.

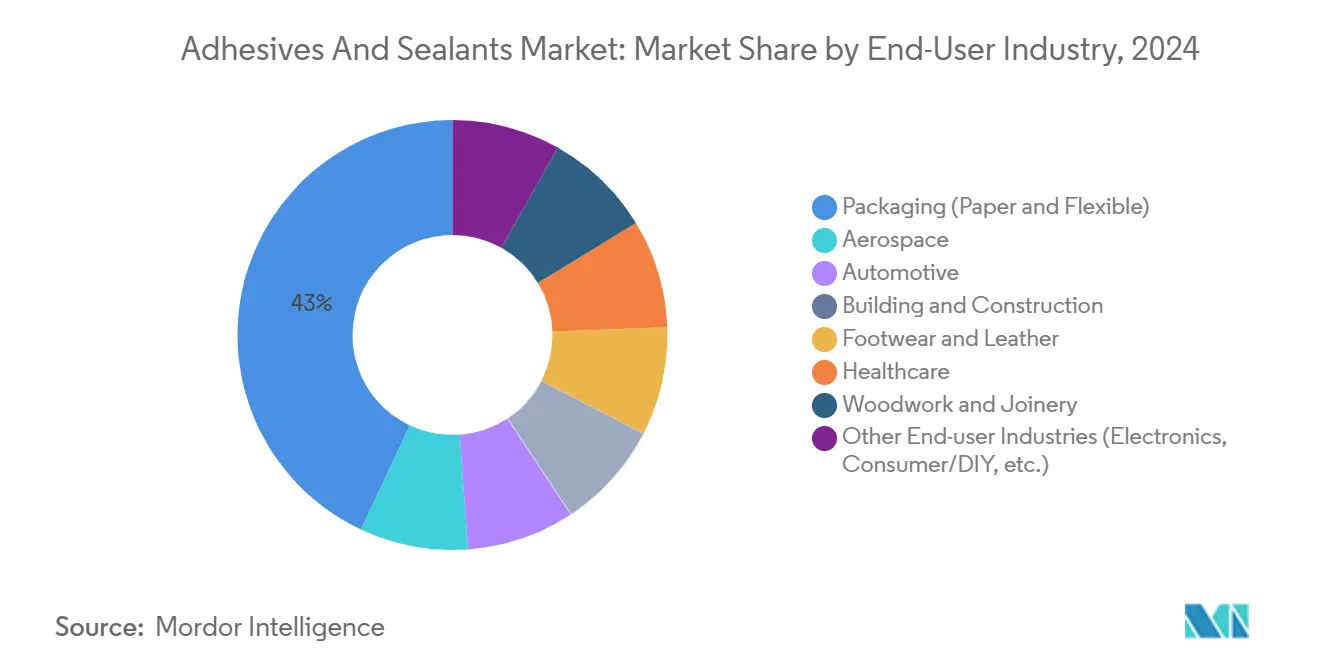

- By end-user, packaging led with 43% of the adhesives and sealants market share in 2024; building and construction is projected to grow at 6.50% CAGR through 2030.

- By geography, Asia-Pacific commanded a 37% adhesives and sealants market share in 2024 and is growing at 6.60% CAGR.

Global Adhesives And Sealants Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Lightweight Multi-material Vehicle Assemblies Boosting Structural Adhesive Uptake | +1.40% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Explosive Growth of E-commerce Requiring High-Performance Packaging Adhesive Solutions Globally | +1.10% | Global | Short term (≤ 2 years) |

| Rapid Expansion of Modular & Prefabricated Construction Methods in Asia-Pacific | +0.90% | Asia-Pacific | Medium term (2-4 years) |

| EU Green Deal & Global Regulatory Push Accelerating Bio-based, Low-VOC Adhesives | +1.20% | Europe, North America | Long term (≥ 4 years) |

| Healthcare Wearables Adoption Driving Medical-grade Reactive Hot-Melt Adhesives | +0.60% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

Source: Mordor Intelligence

Surge in Lightweight Multi-material Vehicle Assemblies Boosting Structural Adhesive Uptake

Electric-vehicle makers are replacing welds and rivets with structural adhesives to save weight, improve crash performance, and enable joining of aluminum, composites, and high-strength steel[1]“Structural Bonding,” Sika, automotive.sika.com . Adhesives also secure battery housings, where they manage heat and provide electrical insulation. Thermal interface materials inside packs prevent runaway and extend battery life, creating a specialized niche within the adhesives and sealants market. Automakers expect bonding technologies to remain dimensionally stable across wide temperature swings and resist fluid exposure for the entire vehicle lifespan. Such stringent requirements are pushing formulators toward reactive polyurethane hot-melts and modified epoxies that combine strength with flexibility. Growing EV penetration therefore acts as a structural demand catalyst for the adhesives and sealants market.

Explosive Growth of E-commerce Requiring High-Performance Packaging Adhesive Solutions Globally

Direct-to-consumer shipping exposes cartons to vibration, humidity, and temperature extremes, prompting brand owners to adopt high-tack hot-melt and water-based systems that keep packages sealed throughout complex logistics chains. Packaging represents 43% of the adhesives and sealants market and continues to expand as e-commerce volumes rise. Sustainability standards now require adhesives compatible with recycling streams; Henkel and Packsize introduced Eco-Pax, a bio-based hot-melt that can cut greenhouse gas emissions by 32% per 340 million boxes produced annually. Automated case-erection lines also demand low-viscosity grades that flow at reduced temperatures to save energy. Innovation in this driver underpins steady volume growth in the adhesives and sealants market.

Rapid Expansion of Modular & Prefabricated Construction Methods in Asia-Pacific

Urbanization and labor shortages are accelerating prefabrication, which relies on fast-curing adhesives for factory-built wall panels, façade elements, and flooring systems. Building and construction is the fastest-growing end-use at 6.50% CAGR, and silicone-based products dominate exterior joints due to superior UV and moisture resistance. Polyurethane and hybrid sealants bond dissimilar materials like glass fiber reinforced concrete and engineered timber, providing structural integrity during transport and installation. As governments in China, India, and Southeast Asia fund large housing schemes, demand for resilient bonding solutions increases in tandem. This development strengthens regional consumption within the adhesives and sealants market.

EU Green Deal & Global Regulatory Push Accelerating Bio-based, Low-VOC Adhesives

The forthcoming 2025 REACH revision will introduce stricter chemical rules, including PFAS bans and essential-use criteria that compel manufacturers to reformulate. Formaldehyde emission limits effective August 2026 further squeeze solvent-borne chemistries[2]Publications Office of the EU, “Commission Regulation (EU) 2023/1464,” eur-lex.europa.eu . Producers answer with starch, lignin, and captured-CO₂-based polymers, as shown by Henkel and Celanese’s carbon-reuse partnership. Bio-based silicone sealants certified under REDcert2, such as ELASTOSIL eco, also illustrate regulatory-driven innovation. Compliance costs are significant, yet early movers gain competitive advantage, reinforcing sustainability as a core growth driver for the adhesives and sealants market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Isocyanate & Acrylic Monomer Supply Chains Creating Cost Pressures | -0.80% | Global | Short term (≤ 2 years) |

| Stringent Environmental Regulations Regarding VOC Emissions | -0.60% | North America, Europe | Medium term (2-4 years) |

| Low Substitution Cost of Mechanical Fasteners in Emerging Markets Limiting Penetration | -0.40% | Latin America, Africa, South-East Asia | Short term (≤ 2 years) |

Source: Mordor Intelligence

Volatile Isocyanate & Acrylic Monomer Supply Chains Creating Cost Pressures

New EU rules require special training for anyone handling polyurethane systems with greater than 0.1% free isocyanate, adding administrative cost and limiting smaller converters’ access. Parallel tightness in acrylic acid supply elevates price volatility, prompting end users to renegotiate contracts quarterly. Producers hedge by localizing feedstock procurement and adopting bio-routes from vegetable oils, yet these measures involve capital outlays that weigh on margins. Sudden spikes in raw-material indices ripple through downstream prices, delaying project approvals in construction and automotive. The adhesives and sealants market must therefore navigate cost inflation while maintaining performance, a balancing act that tempers the growth outlook.

Stringent Environmental Regulations Regarding VOC Emissions

The District of Columbia caps VOC content in a wide range of adhesive categories, mirroring similar rules across U.S. states[3]Hal, “VOC Emissions Reduction,” epa.gov . Green Seal’s 2025 prohibition of PFAS in adhesives tightens compliance further, forcing reformulation and added testing expense. Solvent-borne products, valued for fast-setting and high-strength attributes, face declining acceptance in favor of water-borne or reactive alternatives. Manufacturers invest in R&D to retain performance without exceeding emission thresholds, yet technology transitions take time and resources. These constraints moderate demand expansion for solvent-heavy lines, placing a structural cap on part of the adhesives and sealants market.

Segment Analysis

By Adhesive Resin: Acrylic Dominance Challenged by Silicone Innovation

Acrylic resins generated 24% of the adhesives and sealants market revenue in 2024, favored for broad substrate compatibility and moderate cost. Nevertheless, silicone’s 8.50% CAGR over 2025-2030 signals a pivot toward high-temperature, weather-resistant applications, notably in automotive electronics and building facades. Performance differentiation drives this shift. Silicone adhesives retain elasticity from −50 °C to 200 °C, remain electrically insulating, and resist UV degradation, making them fit for LED assemblies and 5G antenna modules. Acrylics respond with next-generation formulations that cure faster and bond low-surface-energy plastics through functional monomer modifications. Polyurethane remains the choice for structural joints exposed to dynamic loads, while cyanoacrylates serve precision medical and consumer electronics uses. Bio-based epoxies produced from glycerol and lignin showcase early-stage potential, signaling a gradual decarbonization of the adhesives and sealants industry.

Note: Segment shares of all individual segments available upon report purchase

By Adhesive Technology: Water-based Solutions Lead Environmental Transition

Water-based systems held 42% revenue in 2024, aided by compliance with regional VOC caps and robust adhesion on porous substrates. They dominate corrugated box sealing, label lamination, and furniture assembly, all critical subsegments of the adhesives and sealants market. Product advances in polymer dispersion lower drying times, addressing historical speed constraints on automated lines.

Reactive technologies deliver the fastest 8.20% CAGR because they crosslink into thermoset networks, achieving structural strength once considered exclusive to epoxies. Reactive polyurethane hot-melts supply instant green strength plus final chemical bonding after moisture exposure, reducing assembly time for appliance and transportation manufacturers. UV-cured acrylates address electronics and medical devices where solvent elimination and rapid throughput are essential. Solvent-borne and rubber-based systems persist in niche uses, such as automotive interior trim and footwear, where their unique balance of tack and peel strength offsets regulatory hurdles.

By Sealant Resin: Silicone’s Versatility Drives Market Leadership

Silicone sealants captured 45% revenue in 2024 through unrivaled flexibility and 25-year durability, especially in exterior glazing, curtain walls, and solar module framing. New carbon-balanced offerings, including ELASTOSIL eco, substitute conventional methanol with plant-based biomethanol and lower cradle-to-gate emissions by up to 40%. Polyurethane sealants follow with a 5.70% CAGR, propelled by expansion-joint applications in highways and rail. Acrylic latex sealants cater to interior finishing where paintability and low shrinkage are valued. Hybrid silane-terminated polyether chemistries blend silicone flexibility with polyurethane toughness, rising quickly in transportation and renewable-energy structures. Tightening LEED and BREEAM criteria on VOC emissions further favor low-odor formulations, directing a sizable portion of future spending toward greener sealant chemistries within the broader adhesives and sealants market.

By End-user Industry: Packaging Dominance Reflects E-commerce Revolution

Packaging retained a 43% adhesives and sealants market share in 2024, supported by omnichannel retail growth and the drive for tamper-evident closures. Formulators are commercializing hot-melts like Tecbond 214B, the first fully certified biodegradable grade made with 44% bio-content.

Building and construction will post the fastest 6.50% CAGR as green building codes mandate durable, low-emission bonding solutions. Automotive electrification demands thermal-conductive adhesives for battery assemblies, while the healthcare segment looks to reactive hot-melts that replace sutures and staples in wound closure. Footwear, woodworking, and electronics round out demand, each requiring tailored chemistries to balance flexibility, speed, and environmental profile.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific generated 37% of global revenue in 2024 and is growing at 6.60% CAGR, driven by infrastructure megaprojects and the relocation of electronics supply chains into ASEAN nations. China continues large-scale high-speed rail and renewable-energy investments, stimulating demand for structural sealants and wind blade bonding systems. India’s USD 1.4 trillion National Infrastructure Pipeline channels adhesive consumption into roads, airports, and affordable housing. Electronics manufacturing in Vietnam and South Korea deepens regional requirements for low-void, high-thermal-conductivity adhesives used in semiconductors and display panels. Silicone products benefit most, given relentless pursuit of temperature stability in these sectors, ensuring Asia-Pacific retains primacy within the adhesives and sealants market.

North America represents a mature arena emphasizing technology differentiation and rapid regulatory alignment. U.S. electric-vehicle output surpassed 1 million units in 2024, raising consumption of structural, crash-durable adhesives for battery packs and body-in-white assemblies. Federal funding for bridges and broadband further elevates demand for civil-engineering sealants that remain flexible under extreme climates. Canadian wood-frame construction accelerates adoption of polyurethane adhesives that improve energy efficiency through airtight assemblies. The adhesives and sealants market shows steady mid-single-digit growth as producers offer drop-in water-borne alternatives conforming to CARB and EPA VOC limits.

Europe is shaped by the EU Green Deal’s call for carbon-neutral products by 2050. Manufacturers accelerate the transition to lignin-based phenolic alternatives and bio-renewable epoxies to retain market access. German and Nordic prefabrication plants rely on certified low-VOC adhesives in cross-laminated timber modules, reinforcing silicone demand for window and façade sealing. The adhesives and sealants market in Europe benefits from stringent quality expectations, though compliance costs lower EBIT margins. Eastern European vehicle plants broaden production footprints, amplifying regional adhesive requirements.

South America remains a small but vibrant arena. Brazil’s housing deficit spurs government-funded social programs that channel silicone and acrylic sealants into low-cost housing. Argentina’s agricultural packaging sector benefits from hot-melt upgrades to address prolonged storage and export routes. Chilean miners apply hybrid sealants that withstand acid exposure, adding niche growth pockets inside the adhesives and sealants market.

The Middle East & Africa lean on infrastructure ambitions such as Saudi Arabia’s NEOM city and Nigeria’s Lagos-Ibadan railway. Harsh climates reward silicone and polysulfide sealants with elevated UV and sand-abrasion resistance. Import substitution policies in the Gulf encourage local adhesive plants, reducing freight costs and delivery times. Overall, diverse climatic and regulatory landscapes shape differentiated product lineups for regional players in the adhesives and sealants market.

Competitive Landscape

The adhesives and sealants exhibits highly fragmented concentration. The top 10 players hold less than 45% of global revenue. Henkel’s Adhesive Technologies unit posted EUR 10.79 billion sales in 2023 and EUR 5.48 billion during H1 2024, powered by customer-centric formulations and sustainability branding. H.B. Fuller expanded into wound-closure and tissue-bonding through Medifill and GEM acquisitions in December 2024, strengthening exposure to the fast-growing medical segment.

Strategic alliances target low-carbon innovation. Henkel and Covestro co-develop polyurethane encapsulants using renewable polyols, seeking to shrink construction’s 40% global emissions contribution. Similarly, Celanese supplies captured-CO₂-based acetic acid to Henkel for bio-adhesives that reduce fossil content by 20%. Smaller specialists carve high-margin niches: DELO invests 15% of revenue in R&D, focusing on optical-grade adhesives for camera modules.

Mergers and acquisitions remains active. Saint-Gobain agreed to acquire Dubai-based Fosroc, enhancing construction chemical portfolios in the Middle East. Private equity interest persists, evidenced by Onex acquiring a majority stake in cartridge manufacturer Fischbach, signaling confidence in infrastructure-related sealant demand. Collectively, these moves model a landscape where scale, sustainability, and specialization co-exist in shaping the adhesives and sealants market.

Adhesives And Sealants Industry Leaders

-

Henkel AG & Co. KGaA

-

3M

-

Sika AG

-

H.B. Fuller Company

-

Arkema S.A. (Bostik)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2024: H.B. Fuller has strengthened its portfolio of medical-grade cyanoacrylates and tissue adhesives through the acquisition of Medifill Ltd. and an agreement to acquire GEM S.r.l. This strategic expansion is poised to enhance its competitiveness in the adhesives and sealants market by meeting the rising demand for innovative solutions.

- November 2024: Henkel and Celanese have partnered to develop adhesives using captured CO2, broadening the availability of carbon-negative bonding solutions. This collaboration is expected to drive innovation and sustainability in the adhesives and sealants market, aligning with the growing demand for eco-friendly products.

Global Adhesives And Sealants Market Report Scope

Adhesives are substances that join or bond two or more surfaces together by sticking to them. They are a type of material that provides cohesion between different substrates, creating a durable and often permanent bond. Adhesives are used in various applications, from everyday household use to industrial and technological processes.

Sealants are materials used to fill, seal, or close gaps and joints to prevent the passage of liquids or gases. They are designed to provide a barrier against moisture, air, dust, and other environmental elements. Sealants are commonly used in construction, automotive, aerospace, and other industries to create airtight and watertight seals and provide insulation and protection.

The adhesives and sealants market is segmented by adhesive resin, adhesives technology, sealant resin, end-user industry, and geography. By adhesive resin, the market is segmented into polyurethane, epoxy, acrylic, silicone, cyanoacrylate, VAE/EVA, and other resins (polyester, rubber, etc.). By adhesives technology, the market is segmented into solvent-borne, reactive, hot melt, UV-cured, and water-borne adhesives. The market is segmented into silicone, polyurethane, acrylic, epoxy, and other resins (bituminous, polysulfide, UV-curable, etc.) by sealant resin. By end-user industry, the market is segmented into aerospace, automotive, building and construction, footwear and leather, healthcare, packaging, woodwork and joinery, and other end-user industries (electronics, consumer/DIY, etc.). The report also covers the market size and forecasts for the adhesives and sealants market in 27 major countries across the major regions. The report offers the market size in value terms in USD for all the abovementioned segments.

| By Adhesive Resin | Polyurethane | ||

| Epoxy | |||

| Acrylic | |||

| Silicone | |||

| Cyanoacrylate | |||

| VAE / EVA | |||

| Other Resins (Polyester, Rubber, etc.) | |||

| By Adhesive Technology | Solvent-borne | ||

| Reactive | |||

| Hot Melt | |||

| UV-cured | |||

| Water-borne | |||

| By Sealant Resin | Silicone | ||

| Polyurethane | |||

| Acrylic | |||

| Epoxy | |||

| Other Resins (Bituminous, Polysulfide UV-curable, etc.) | |||

| By End-user Industry | Aerospace | ||

| Automotive | |||

| Building and Construction | |||

| Footwear and Leather | |||

| Healthcare | |||

| Packaging (Paper and Flexible) | |||

| Woodwork and Joinery | |||

| Other End-user Industries (Electronics, Consumer/DIY, etc.) | |||

| By Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Indonesia | |||

| Malaysia | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Turkey | |||

| Nordic Countries | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Qatar | |||

| Egypt | |||

| South Africa | |||

| Algeria | |||

| Rest of Middle and Africa | |||

By Adhesive Resin

| Polyurethane |

| Epoxy |

| Acrylic |

| Silicone |

| Cyanoacrylate |

| VAE / EVA |

| Other Resins (Polyester, Rubber, etc.) |

By Adhesive Technology

| Solvent-borne |

| Reactive |

| Hot Melt |

| UV-cured |

| Water-borne |

By Sealant Resin

| Silicone |

| Polyurethane |

| Acrylic |

| Epoxy |

| Other Resins (Bituminous, Polysulfide UV-curable, etc.) |

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging (Paper and Flexible) |

| Woodwork and Joinery |

| Other End-user Industries (Electronics, Consumer/DIY, etc.) |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Turkey | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| South Africa | |

| Algeria | |

| Rest of Middle and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the adhesives and sealants market?

The adhesives and sealants market is valued at USD 85.38 billion in 2025 and is projected to reach USD 114.94 billion by 2030.

Which region shows the fastest growth in the adhesives and sealants market?

Asia-Pacific leads with a 37% revenue share in 2024 and a forecast 6.60% CAGR, driven by industrial and infrastructure expansion.

Which end-user industry dominates market demand?

Packaging commands 43% of 2024 revenue due to rising e-commerce volumes and demand for sustainable sealing solutions.

What technology segment is growing the fastest?

Reactive adhesive technologies are expected to register an 8.20% CAGR between 2025 and 2030, outpacing other chemistries.

How are regulations affecting product development?

Stricter EU and U.S. VOC and PFAS limits push manufacturers toward bio-based, low-emission formulations, reshaping R&D priorities.

Who are the key players in the adhesives and sealants market?

Henkel AG & Co. KGaA, 3M, Sika AG, H.B. Fuller Company, and Arkema are the key players in the adhesives and sealants market.

Page last updated on: July 3, 2025