Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.48 Billion |

| Market Size (2026) | USD 1.57 Billion |

| Market Size (2031) | USD 2.07 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Adhesives Market Analysis by Mordor Intelligence

The Canada Adhesives Market size is projected to expand from USD 1.48 billion in 2025 and USD 1.57 billion in 2026 to USD 2.07 billion by 2031, registering a CAGR of 5.78% between 2026 to 2031. Federal clean-fuel mandates and evolving industry trends are reshaping demand in the Canada adhesives market. The shift from solvent-borne chemistries, growth in mass-timber construction, and vehicle electrification are driving changes. Hot-melt and reactive systems are replacing legacy solvents due to advancements in e-commerce fulfillment and sawmill automation. Electric-vehicle assembly in Ontario and Quebec is increasing adhesive usage, particularly high-strength polyurethane and epoxy formulations. Policy changes, including federal VOC limits effective January 2024 and the EU’s Carbon Border Adjustment Mechanism, highlight the strategic importance of domestic resin integration. Despite moderate competitive intensity, multinationals like Henkel, H.B. Fuller, Sika, 3M, Dow, BASF, RPM, and Arkema hold local assets but lack a dominant market share across all end-use channels.

Key Report Takeaways

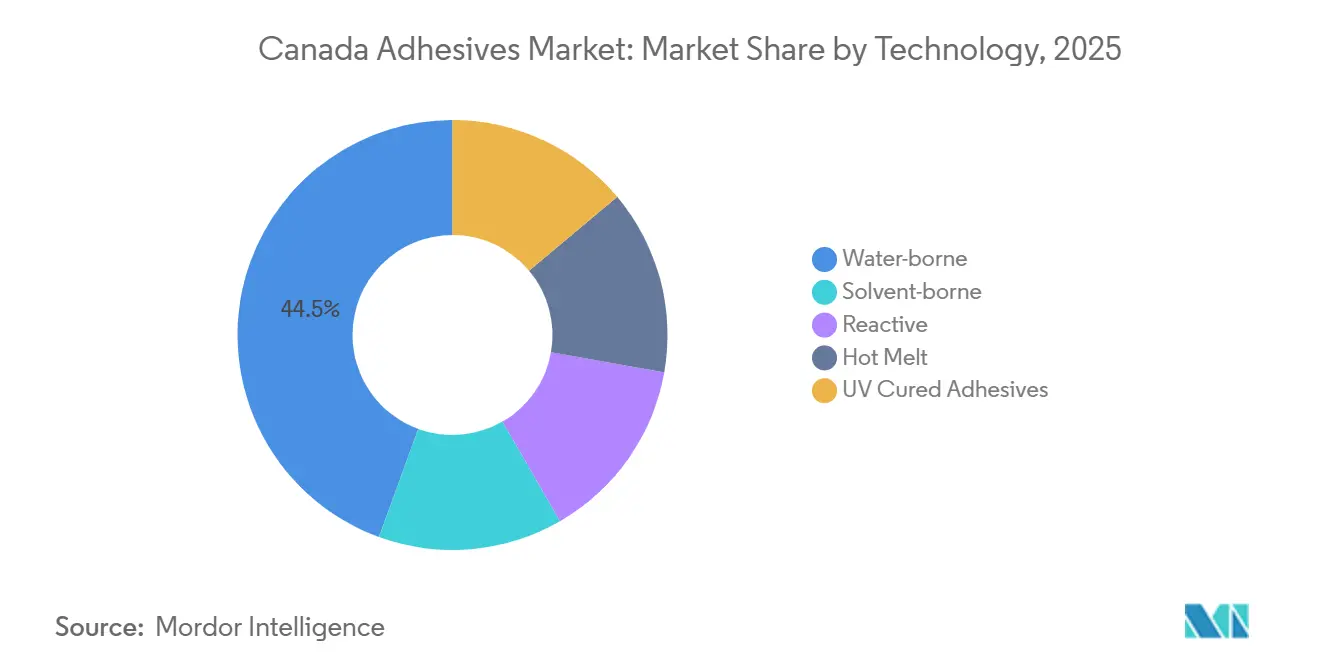

- By technology, water-borne systems commanded 44.46% of Canada Adhesives market share in 2025, yet hot-melt volumes are advancing at a 6.48% CAGR to 2031.

- By resin, acrylics led with 32.25% revenue share of the Canada Adhesives market size in 2025, while VAE/EVA resins are forecast to expand at a 6.23% CAGR through 2031.

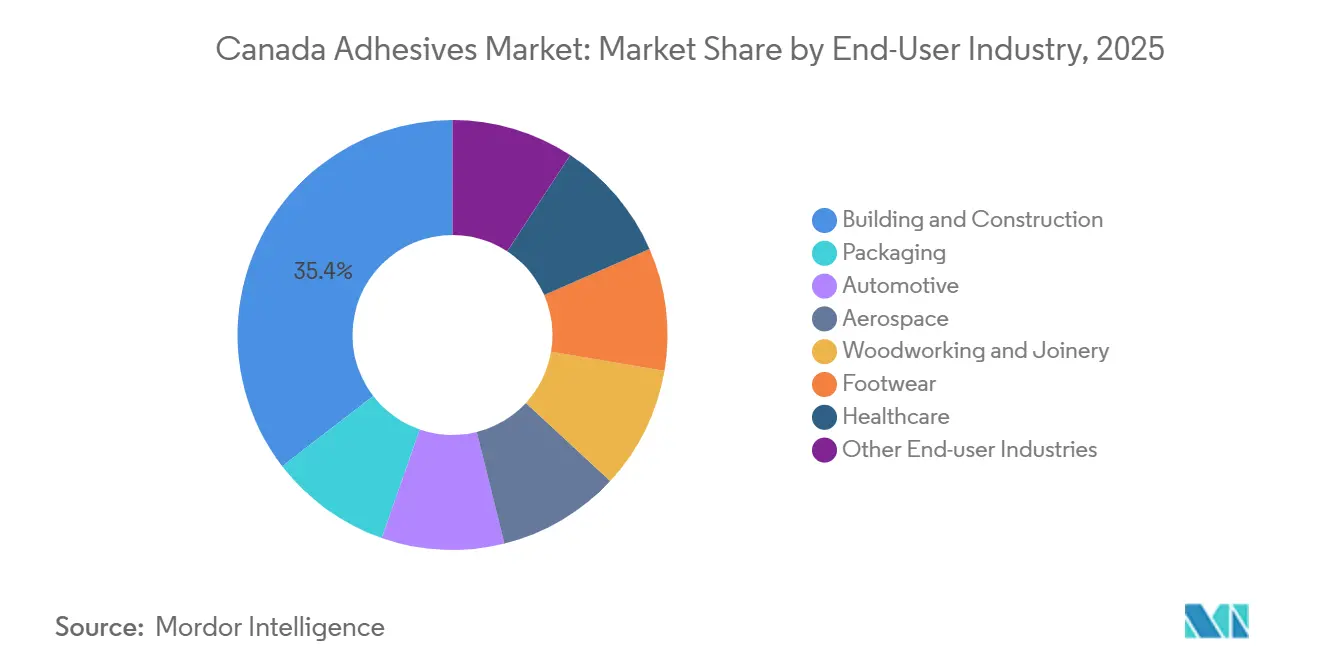

- By end-user, building and construction accounted for 35.44% of Canada Adhesives market share in 2025; automotive is poised to grow fastest at 6.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive e-commerce raises hot-melt usage in corrugated packaging | +1.2% | National, with concentration in Ontario and Quebec distribution hubs | Medium term (2-4 years) |

| EV assembly lines adopt lightweight structural bonding solutions | +1.4% | Ontario and Quebec automotive corridors | Medium term (2-4 years) |

| Hybrid-timber high-rises drive demand for specialty structural glues | +0.9% | British Columbia, Ontario, Quebec urban centers | Long term (≥ 4 years) |

| Clean Fuel Regulations spur bio-based adhesive feedstocks | +0.6% | National, with early adoption in British Columbia and Quebec | Long term (≥ 4 years) |

| Sawmill automation boosts low-temperature hot-melt consumption | +0.7% | British Columbia, Quebec, Ontario forestry regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive E-Commerce Raises Hot-Melt Usage in Corrugated Packaging

Canadian corrugated converters increasingly specify metallocene and low-temperature hot-melt adhesives that run clean at throughputs above 100 cases per minute, a shift that mirrors rapid e-commerce warehouse expansion in Ontario and Quebec[1]Hotmelt.com Editorial Team, “H.B. Fuller HL-0765 Product Sheet,” hotmelt.com. Plant-based alternatives have replaced polyvinyl acetate on 40% of new box lines commissioned since 2024, driven by brand-owner mandates for fiber-tear bonds on high-recycled-content liners. Exemption of hot-melt chemistries from VOC caps eliminates drying infrastructure costs, further tilting capital budgets toward these systems. AJ Adhesives reports that 225-275°F formulations cut energy use by 20% compared with conventional EVA blends, an added benefit as electricity tariffs rise in Quebec. Robotic case-sealing cells also require narrow viscosity windows, which metallocene grades provide more consistently than legacy EVA systems.

EV Assembly Lines Adopt Lightweight Structural Bonding Solutions

Honda’s CAD 15 billion (USD 10.74 billion) commitment to Ontario EV production, targeting 240,000 units annually by 2028, is accelerating demand for high-strength polyurethane and epoxy adhesives that bond aluminum, magnesium, and advanced high-strength steels without thermal distortion. Martinrea International validated a 12% mass reduction in aluminum subframes joined with adhesive and rivets, demonstrating structural integrity without resistance welding. H.B. Fuller’s UR4515GF two-component polyurethane offers 19 MPa (megapascal) shear strength on abraded aluminum and is optimized for automated dispensing, aligning with EV plants now deploying robotically applied continuous beads. Henkel’s USD 30 million expansion at Brandon, South Dakota, adds thermal-management adhesive capacity and shortens lead times for Canadian battery-module producers[2]Henkel North America, “Henkel Expands Brandon Plant to Support EV Growth,” henkel.com.

Hybrid-Timber High-Rises Drive Demand for Specialty Structural Glues

British Columbia amended its building code to permit 18-story wood-frame structures, unlocking a pipeline of more than 750 mass-timber projects totaling 2.9 million m². These projects demand formaldehyde-free adhesives that meet 2-hour fire-resistance ratings and cure at ambient temperature. FPInnovations and Université Laval showcased lignin-based formulations replacing up to 50% of phenol-formaldehyde resin while reducing VOC emissions by 40%, a milestone now migrating to commercial production at Uniboard’s Val-d’Or facility. However, creep performance under sustained load still necessitates epoxy or polyurethane systems with glass-transition temperatures above 80°C to maintain floor-panel rigidity, especially in hybrid concrete-timber slabs approved for Vancouver towers.

Clean Fuel Regulations Spur Bio-Based Adhesive Feedstocks

Canada’s Clean Fuel Regulations award lifecycle-carbon credits for bio-based content, creating a revenue stream when lignin replaces petroleum-derived phenol in structural wood adhesives. Tafisa and Uniboard have achieved cost parity by integrating onsite lignin extraction from kraft pulp waste, lowering adhesive carbon intensity by up to 35% versus conventional systems. The policy disincentivizes high-carbon epoxy and polyurethane intermediates such as epichlorohydrin and MDI, and pushes formulators to lock in forestry-sector coproducts before supply tightens. Arkema’s USD 20 million PVDF capacity expansion at Calvert City, Kentucky, scheduled for mid-2026, positions the company to market lower-carbon fluorinated precursors once demand spikes from packaging converters and lithium-ion battery lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC caps curtail solvent-borne technologies | -0.80% | National, with stricter enforcement in Quebec and British Columbia | Short term (≤ 2 years) |

| Skilled trades shortage slows adoption of advanced application methods | -0.60% | Ontario and Alberta manufacturing corridors | Medium term (2-4 years) |

| Carbon-border adjustment raises imported raw-material costs | -0.50% | National, with higher impact on epoxy and polyurethane formulators reliant on imported precursors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC Caps Curtail Solvent-Borne Technologies

Federal limits, effective January 2024, cap VOC content for acoustical sealants at 10% and structural waterproofing at 7%, immediately squeezing solvent-borne formulations. Compliance costs reach CAD 29.7 million (USD 21.26 million) for Canadian producers, a burden that pushes smaller regional formulators to exit categories such as contact adhesives historically favored for upholstery and footwear. While hot-melt and 100%-solids reactive systems are exempt, cold-weather construction in Alberta and Saskatchewan still relies on solvent-borne products that cure rapidly below freezing. Absence of suitable water-borne or reactive substitutes forces contractors either to delay winter work or import niche products at higher cost. Cabot Corporation’s Sarnia, Ontario silica plant faces new sulfur-dioxide controls by 2028, a factor that may lift rheology-modifier pricing embedded in sealant formulations.

Skilled Trades Shortage Slows Adoption of Advanced Application Methods

The Ontario Skills Development Fund invested CAD 260 million (USD 186.08 million)across 1,000 projects, yet applicants certified to program robotic dispensers remain scarce. Two-component mix-ratio control, UV-lamp calibration, and real-time viscosity monitoring demand new competencies that community-college programs have been slow to address. Henkel is expanding its Canadian technical-service teams to backstop customers lacking in-house expertise, but until labor pipelines strengthen, commissioning of adhesive-intensive EV battery and flexible-packaging lines continues to miss schedule milestones. Electronics subcontractors report six-to-nine-month lags in hiring technicians versed in jet-dispensing of UV-curable resins, constraining domestic assembly for high-reliability medical devices and telecom modules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Hot-Melt Gains on Packaging Automation

Water-borne systems retain the largest slice at 44.46% share, but freeze-thaw instability in unheated Western Canadian warehouses slows adoption in winter packaging lines. The market share of hot-melt adhesives is forecast to expand at 6.48% CAGR during the forecast period (2026-2031), supported by robotic case sealers that eliminate drying tunnels and trim energy use. Low-temperature metallocene grades now dominate new corrugated installations, reducing charring and extending hose life. Reactive systems, notably PUR and epoxy, win share inside EV body-in-white and aerospace composites because continuous bead application speeds assembly while preserving joint integrity. UV-curable chemistries remain niche at less than 2% of Canada Adhesives market, yet their instant-cure profile offers throughput advantages for medical device and electronics producers that cannot afford multi-day room-temperature cures.

Second-generation low-viscosity hot-melts running at 225-275°F cut energy consumption by nearly 20 % versus traditional EVA blends, helping converters manage electricity surcharges in Quebec. Conversely, solvent-borne grades declined 190 basis points in share in 2025 alone because of VOC caps on 130 product categories. Some contact adhesive users migrated to water-borne acrylics, but others still test newer reactive polyurethane systems that offer open time control via catalyst selection. Overall, technology substitution continues to compress legacy solvent demand and reshapes plant capital layouts to favor enclosed melters and robot-guided applicators.

By Resin: VAE/EVA Captures Flexible Packaging Shift

Acrylics led with 32.25% of Canada Adhesives market share in 2025, anchored in construction sealants and pressure-sensitive labels. Yet VAE/EVA copolymers are pacing ahead at a 6.23% CAGR, buoyed by mono-material pouch designs that require low-migration, FDA-compliant bonds. Polyurethanes remain indispensable for structural automotive joints where impact and peel resistance trump price. Epoxy systems, though smaller in tonnage, retain high value in aerospace interiors and wind-blade bonding, but environmental scrutiny of bisphenol-A has jump-started research into lignin-based epoxy precursors. Cyanoacrylate and silicone chemistries occupy specialty niches in healthcare and electronics, making them less sensitive to commodity monomer swings.

Dow’s USD 6.5 billion Path2Zero ethylene cracker, starting in 2027, secures a local supply of VAE/EVA backbones, tilting bargaining power away from independent formulators. BASF lifted butyl-acrylate prices by USD 0.03/lb in April 2026, exposing water-borne formulators to feedstock inflation they struggle to pass through to price-sensitive packaging accounts. Henkel’s January 2026 acquisition of ATP Adhesive Systems adds EUR 270 million of water-based tape capacity, signaling a bet that acrylic emulsions for electronics and automotive interiors will sustain premium pricing where 3M and Avery Dennison have entrenched positions.

By End-User Industry: Automotive Outpaces on Lightweighting Mandates

Building and construction represented 35.44% of Canada Adhesives market size in 2025, fueled by mass-timber high-rises and renovation of multi-family housing stock. Growth, however, is moderating because skilled-trades shortages delay project starts. Automotive demand, by contrast, is forecast to grow 6.36% CAGR during the forecast period (2026-2031) as EV platforms nearly double adhesive kilograms per vehicle. Each Honda EV rolling out of Ontario will require an estimated 18-22 kg of structural and thermal management adhesives, compared with 8-12 kg for internal combustion vehicles. Packaging's market share is driven by e-commerce and brand owners' targets on recyclable laminates. Aerospace and wind energy remain high-margin, low-volume segments, whereas woodworking, healthcare, and footwear together hold substantially less share, but each shows resilient, regulated demand for low-VOC or biocompatible formulations.

Honda’s investment lifts regional tier-one suppliers such as Martinrea, which validated adhesive-riveted aluminum subframes with a 12 % mass reduction. Building codes in British Columbia that now allow 18-story wood-frame towers further enlarge structural adhesive opportunity, although fire testing for new lignin systems is still under way. Packaging converters focus on compostable laminations, for which H.B. Fuller’s Flextra solutions enable food-contaminated films to enter industrial composting streams, satisfying organics-diversion mandates in British Columbia and Quebec.

Geography Analysis

In 2025, Ontario and Quebec accounted for over half of Canada's adhesive market, driven by strong automotive, packaging, and construction sectors. Ontario, boasting the nation's highest concentration of electric vehicle (EV) assembly, consumes structural polyurethane and epoxy at rates surpassing the national average. In Quebec, converters are increasingly adopting low-temperature hot-melts, owing to competitive electricity rates that support high-speed production lines and reduce downtime. Quebec also sees the strictest enforcement of federal VOC regulations, pushing the industry towards water-borne acrylics, especially for interior construction and pressure-sensitive tapes.

British Columbia's market share is expanding at a pace outstripping the national average, buoyed by permitting for mass timber structures up to 18 stories. With its robust forestry base, British Columbia positions local manufacturers close to lignin feedstocks, spurring an early shift towards bio-based structural glues. Meanwhile, Alberta and Saskatchewan's market share is bolstered by energy infrastructure projects and a reliance on solvent-borne adhesives for winter roofing. Although stringent environmental regulations on sulfur dioxide emissions at petrochemical facilities might slightly elevate raw material costs for local formulators, the impact is softened by the provinces' lower population density and reduced construction intensity.

While Atlantic Canada remains the smallest player in the market, it serves as an experimental ground for marine-grade sealants, particularly in offshore wind projects and fisheries infrastructure. Given the region's higher logistics costs, there's a preference for shipping hot-melt blocks and reactive cartridges, which avoid hazardous-material surcharges. In summary, the dynamics of Canada's adhesive market are shaped by local policies, proximity to feedstocks, and the prevailing end-use industries, underscoring the importance of geographic demand profiles.

Competitive Landscape

The Canada Adhesives market is moderately consolidated. White spaces remain. Lignin-based structural adhesives for mass-timber panels have proven lab feasibility but lack third-party certification for 2-hour fire ratings, creating an entry lane for companies able to fund scale-up and testing. Customized hot-melt blends that maximize fiber-tear on 100% recycled corrugated offer differentiation where large multinationals maintain standardized portfolios. Overall, multinationals continue to bulk up via acquisitions, but regional specialists hold defensible niches in customer-specific formulations and rapid turnaround production.

Canada Adhesives Industry Leaders

3M

H.B. Fuller Company

Henkel AG & Co. KGaA

Sika AG

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Parker Lord unveiled CHEMLOK NX-100, an eco-friendly covercoat adhesive designed to bond elastomers to various substrates. The product is available across Canada, the United States, and Mexico.

- October 2025: With a USD 70 million investment, ATP Adhesives inaugurated ATP North America, a venture aimed at catering to manufacturers in the United States and Canada. The new entity focuses on solvent-free adhesive technologies and boasts local product-development capabilities.

Canada Adhesives Market Report Scope

Adhesives, including glue, cement, and paste, bond two surfaces together, preventing their separation. Available in forms like liquid, paste, or tape, these substances are defined by their stickiness, allowing them to adhere to materials such as wood, metal, or skin.

The Canada Adhesives Market is segmented by technology, resin, and end-user industry. By Technology, the market is segmented into water-borne, solvent-borne, reactive, hot melt, and UV-cured adhesives. By Resin, the market is segmented into polyurethane, epoxy, acrylic, cyanoacrylate, VAE/EVA, silicone, and other resins. By End-user Industry, the market is segmented into building and construction, packaging, automotive, aerospace, woodworking and joinery, footwear, healthcare, and other end-user industries. The market sizes and forecasts are provided in terms of value (USD).

By Technology

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot Melt |

| UV Cured Adhesives |

By Resin

| Polyurethane |

| Epoxy |

| Acrylic |

| Cyanoacrylate |

| VAE/EVA |

| Silicone |

| Other Resins |

By End-User Industry

| Building and Construction |

| Packaging |

| Automotive |

| Aerospace |

| Woodworking and Joinery |

| Footwear |

| Healthcare |

| Other End-user Industries |

| By Technology | Water-borne |

| Solvent-borne | |

| Reactive | |

| Hot Melt | |

| UV Cured Adhesives | |

| By Resin | Polyurethane |

| Epoxy | |

| Acrylic | |

| Cyanoacrylate | |

| VAE/EVA | |

| Silicone | |

| Other Resins | |

| By End-User Industry | Building and Construction |

| Packaging | |

| Automotive | |

| Aerospace | |

| Woodworking and Joinery | |

| Footwear | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms