4K Display Resolution Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

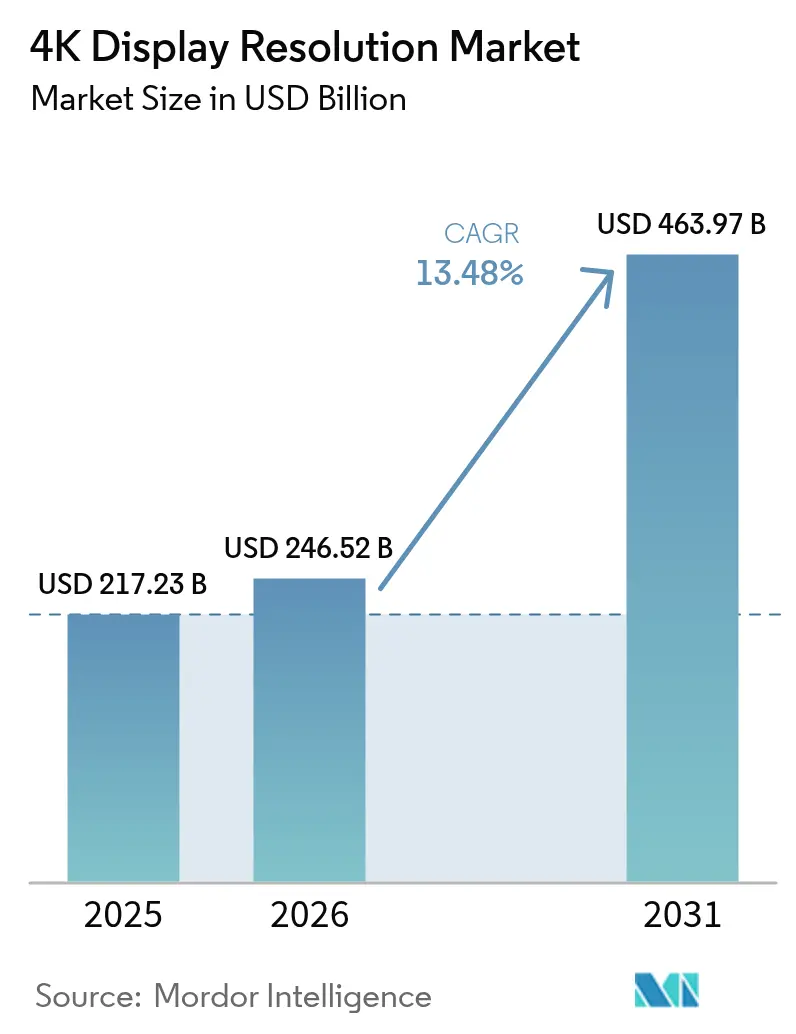

| Market Size (2026) | USD 246.52 Billion |

| Market Size (2031) | USD 463.97 Billion |

| Growth Rate (2026 - 2031) | 13.48% CAGR |

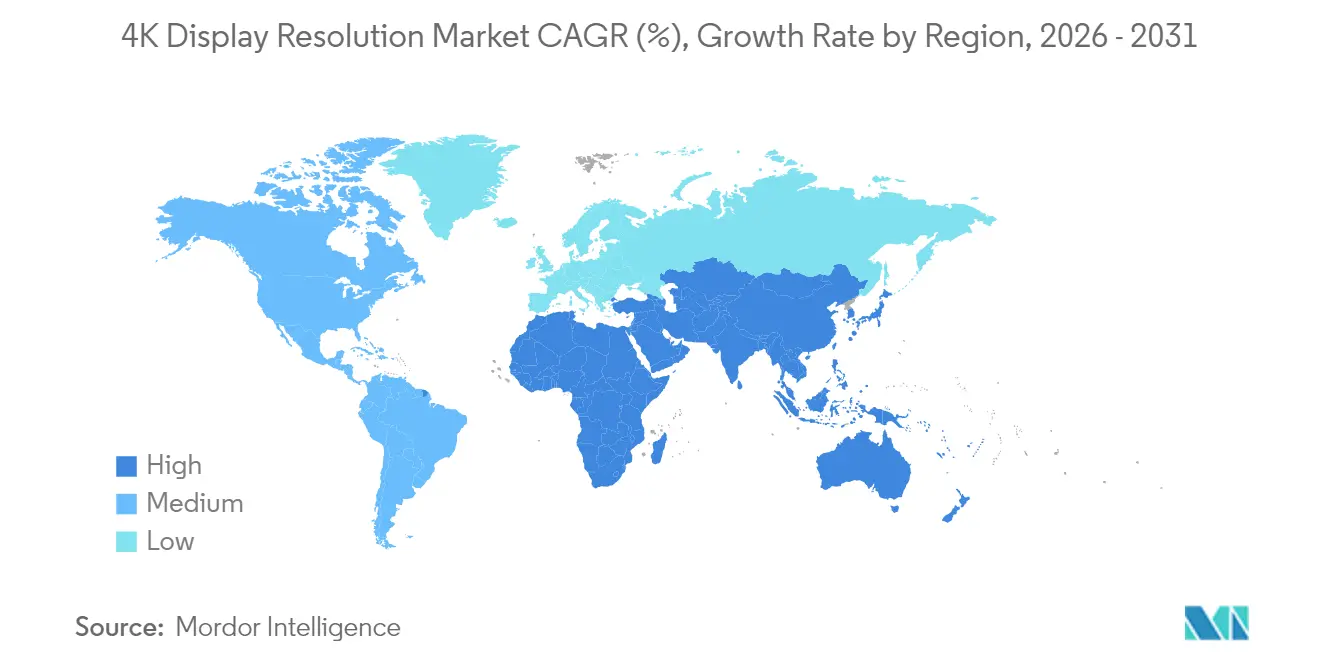

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

4K Display Resolution Market Analysis by Mordor Intelligence

The 4K display resolution market size was valued at USD 217.23 billion in 2025 and estimated to grow from USD 246.52 billion in 2026 to reach USD 463.97 billion by 2031, at a CAGR of 13.48% during the forecast period (2026-2031). Fast-declining panel costs, a richer supply of native 4K streaming content, and expanding corporate use cases are allowing the technology to move from premium positioning into mass adoption. Asia Pacific’s manufacturing scale keeps average selling prices low while the region’s consumers display a marked preference for larger screens. Hybrid-work demand and immersive gaming are further tightening refresh cycles, encouraging brands to launch increasingly specialized models. At the same time, supply chain risks around chipsets and evolving energy-efficiency rules in Europe urge vendors to diversify component sourcing and accelerate R&D in low-power backlighting.

Key Report Takeaways

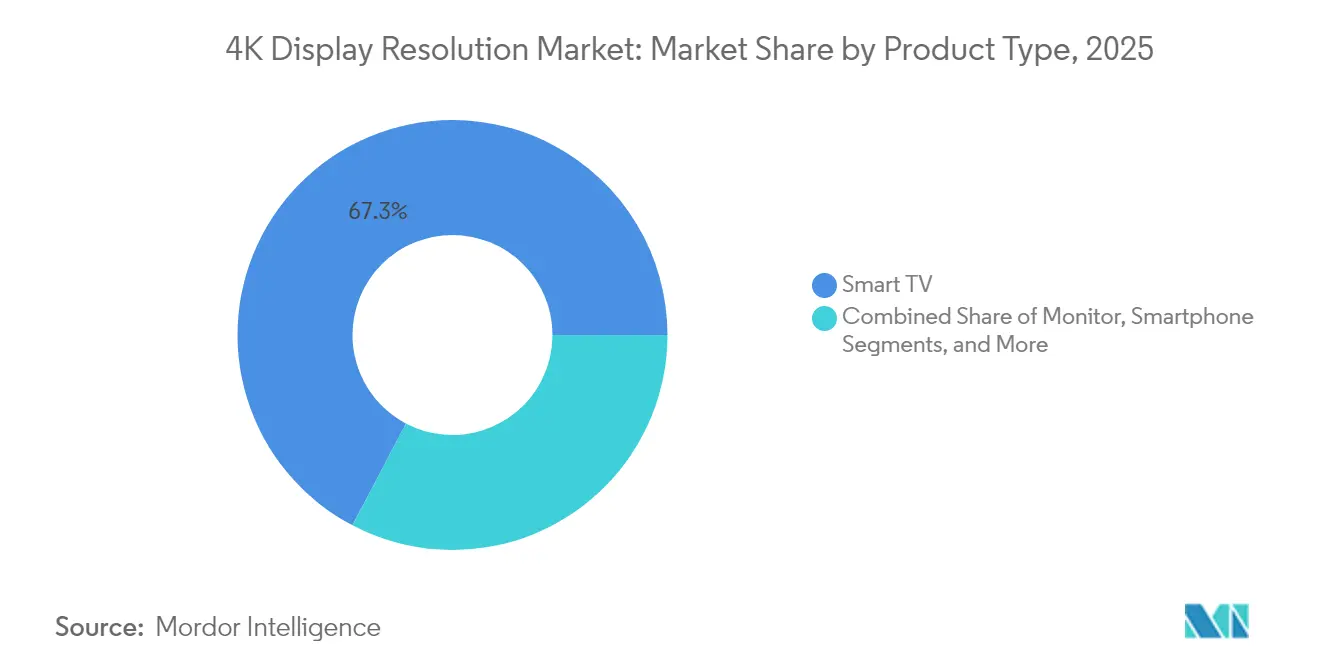

- By product category, smart TVs led with 67.30% revenue share in 2025; gaming monitors are projected to expand at a 13.84% CAGR through 2031.

- By panel technology, LCD held 70.40% of the 4K display resolution market share in 2025, whereas OLED is forecast to advance at a 16.25% CAGR to 2031.

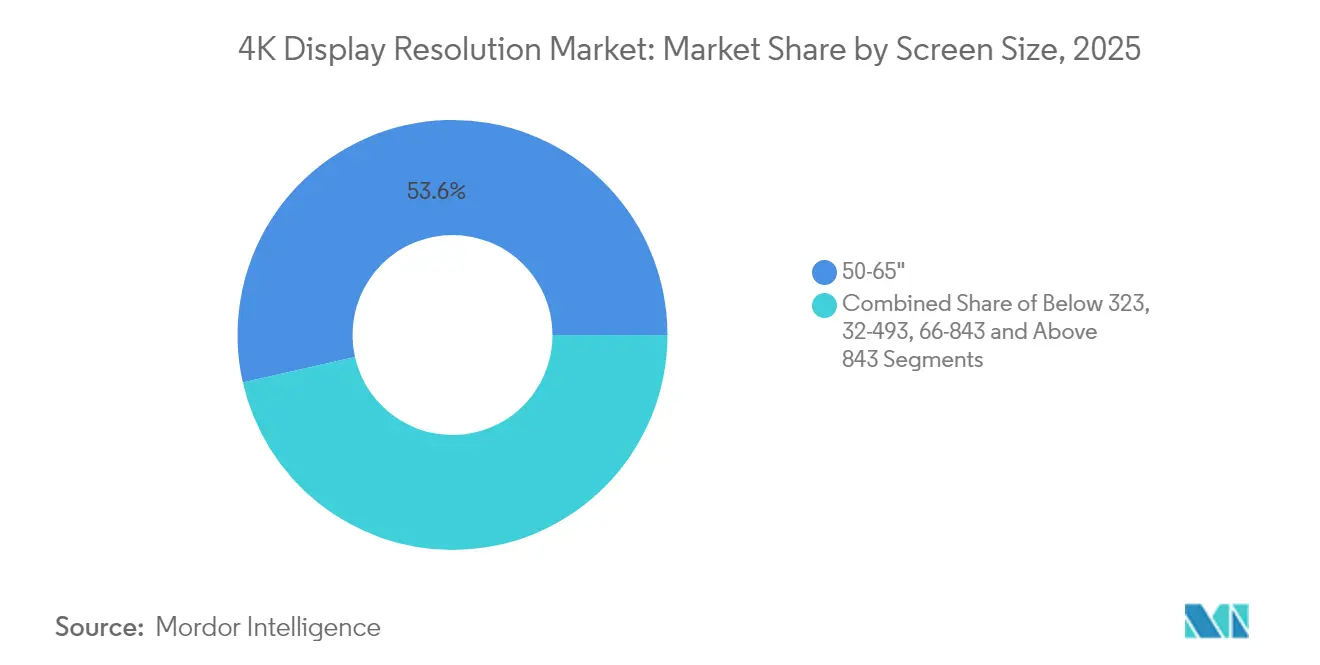

- By screen size, the 50–65″ bracket accounted for 53.55% of the 4K display resolution market size in 2025; displays above 65″ are expected to grow at 15.35% CAGR between 2026 and 2031.

- By end-user vertical, consumer electronics held 75.25% share of the 4K display resolution market size in 2025, while healthcare displays are set to rise at 13.05% CAGR over the same period.

- By geography, Asia Pacific captured 45.60% revenue share in 2025; the Middle East is predicted to record the fastest regional CAGR at 13.62% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 4K Display Resolution Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid OTT-led uptake of 4K streaming | +3.2% | North America, Europe | Medium term (2-4 years) |

| Panel subsidies and capacity expansion | +2.8% | Asia Pacific, Global supply chain | Short term (≤ 2 years) |

| Esports demand for 4K/144 Hz gaming monitors | +1.7% | Europe, North America, East Asia | Medium term (2-4 years) |

| Adoption of 4K surgical and diagnostic displays | +1.5% | North America, Japan, Western Europe | Long term (≥ 4 years) |

| Hybrid-work LED videowalls in GCC | +1.2% | Middle East, GCC countries | Medium term (2-4 years) |

| Mini-LED yield-driven price erosion | +1.9% | Global, initial impact in Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid OTT-led Uptake of 4K Streaming in North America

Streaming platforms delivered more than 60% of their new content in 4K during 2024, setting a stronger pull for compatible screens in household upgrades. Bandwidth gains from Wi-Fi 7, which supports data rates up to 46 Gbit/s, remove the previous bottlenecks that limited mainstream 4K adoption. Millimeter-wave rollouts, with Japan targeting 50,000 base stations by 2027, add further capacity that benefits cross-border content providers. The result is a steeper replacement cycle for television sets and monitors, with streaming services shaping feature roadmaps around HDR performance and wider color gamuts. Brands that synchronize panel launches with blockbuster content premieres are capturing early-adopter interest ahead of key sales quarters.

Panel Subsidies and Capacity Expansion in China and South Korea

Government incentives trimmed capital costs for new LCD and QD-OLED lines, enabling firms such as BOE Technology and Samsung Display to run plants at high utilization. Samsung Display plans to raise QD-OLED monitor panel shipments by 50% to 1.43 million units in 2025, giving OEM partners more scope to refresh premium catalogs. Economies of scale flowing from these investments support competitive pricing in the 50-65″ mainstream sweet spot, while yield-driven cost erosion in Mini-LED backlights widens adoption in mid-tier models. The subsidy-induced volume surge is already filtering through global supply chains, lowering bill-of-materials outlays for downstream assemblers.

Esports Demand for 4K/144 Hz Gaming Monitors in Europe

Professional esports leagues specified 4K/144 Hz displays as the baseline for tournament stages in 2024, creating a halo effect for consumer models. Samsung retained a 21.0% share in the global gaming monitor market and announced the Odyssey OLED G6 with a 500 Hz refresh rate for a late 2025 release.[1]Samsung Electronics, “Samsung Electronics Ranked No. 1 in Global Gaming Monitor Market for Six Consecutive Years,” news.samsung.com MSI’s CES-honored MPG 272URX QD-OLED display, the first 27″ 4K 240 Hz unit with DP 2.1, underscores the rapid spec evolution. Brand differentiation now centers on higher peak brightness, tandem OLED stacks, and advanced cooling to mitigate burn-in, allowing vendors to command premium ASPs in Europe’s enthusiast segment.

Adoption of 4K Surgical and Diagnostic Displays in U.S. and Japan

Operating rooms embraced 4K screens for endoscopy and microscopic surgery, leveraging their four-fold pixel density over Full HD to reveal finer anatomical structures. Sony’s LMD-32M1MD Mini-LED monitor, with over 1,850 cd/m² peak brightness and VESA HDR1000 certification, illustrates the required luminance ceiling for glare-prone theaters.[2]Sony, “Introducing the LMD-32M1MD: Sony’s Advanced 4K Mini-LED Medical Monitor,” pro.sony U.S. and Japanese regulatory frameworks favor devices that meet DICOM grayscale accuracy, spurring OEMs to invest in factory calibration workflows. Hospital procurement cycles are longer than consumer refresh rates, yet margins remain protective, shielding suppliers from price attrition in mainstream TV categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HDMI 2.1 chipset shortages 2024-25 | -1.4% | Global, higher in North America and Europe | Short term (≤ 2 years) |

| EU Eco-design rules for >65″ TVs | -0.9% | European Union, spillover to global manufacturing | Medium term (2-4 years) |

| Limited 4K broadcast spectrum in Africa | -0.4% | Sub-Saharan Africa | Long term (≥ 4 years) |

| Premium 8K cannibalization in East Asia | -0.7% | Japan, South Korea, high-income urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

HDMI 2.1 Chipset Shortages 2024-25

Constrained wafer starts at leading foundries have a limited supply of HDMI 2.1 retimer and switch ICs, delaying volume shipments of flagship gaming monitors and high-end TVs. Himax Technologies reported that 82.9% of 2024 revenue came from display driver ICs, underscoring dependence on a narrow component pool.[3]Himax Technologies, “Himax Technologies, Inc. Form 20-F FY 2024,” sec.gov Vendors redirected scarce chipsets to models with higher gross margins, creating temporary stockouts in mid-tier SKUs. The scarcity also accelerated DisplayPort 2.1 adoption, as seen in MSI’s new QD-OLED monitor, signaling possible long-term interface diversification even after supply normalizes.

EU Eco-design Rules Raising Compliance Costs for >65″ TVs

The European Commission’s public consultation on improving energy labels and reparability for electronic displays signals tighter rules beyond 2025. Larger panels face steeper efficiency thresholds, pushing brands to add Mini-LED dimming zones or switch to more efficient OLED matrices. Engineering changes, certification fees, and redesign of retail packaging inflate total landed costs, driving some manufacturers to favor sub-65″ models for Europe. These regulatory headwinds may reallocate R&D budgets toward low-power backlighting and recyclable chassis materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gaming Monitors Redefine Performance Standards

Gaming monitors accounted for a 13.84% CAGR forecast between 2026 and 2031, the fastest trajectory within the 4K display resolution market. Samsung upheld a 21.0% global share in 2024, while its 34.6% slice of the OLED sub-segment confirmed a first-mover advantage in emerging QD-OLED stacks. The segment thrives on esports sponsorship visibility, frequent model refreshes, and the synergy with powerful GPUs such as NVIDIA GeForce RTX 4090 that unlocked stable 4K/144 Hz gameplay. Monitor brands elevate specifications with higher peak brightness, tandem OLED layers, and DisplayPort 2.1 input to differentiate premium SKUs. Profitability remains thicker than mainstream TVs because enthusiast buyers value response time, HDR contrast, and color coverage.

Smart TVs preserved leadership with a 67.30% revenue share in 2025, supported by wide 4K streaming content libraries and falling BOM costs. Corporate video walls and digital signage screens gained importance as hybrid-work hubs required wide viewing angles and high pixel density. Medical displays formed a high-margin niche, with 4K surgical monitors like Sony’s LMD-32M1MD achieving VESA HDR1000 compliance for operating theaters. Smartphones and tablets with native 4K remain limited to creator-focused uses because energy draw offsets mobile benefits. Overall, consumer appetite for richer entertainment and workplace collaboration sustains multi-segment momentum within the 4K display resolution market.

By Panel Technology: OLED Challenges LCD Dominance

OLED panels are projected to expand at a 16.25% CAGR, the swiftest run in the 4K display resolution market. Samsung Display’s plan to ship 1.43 million QD-OLED monitor panels in 2025 exemplifies the capacity scaling that propels wider use beyond flagship TVs. Superior contrast, pixel-level dimming, and the introduction of tandem OLED stacks now reach gaming monitors, encouraging ASP premiums. LG’s 2025 G5 TV, with a 165 Hz native refresh and Micro Lens Array optics, underscores the continued pace of OLED R&D.

LCD technology retained 70.40% share in 2025 because of vast installed tooling, mature supply chains, and cost competitiveness for mid-range sets. Mini-LED backlighting adds local dimming and higher luminance, bridging performance gaps with OLED at a lower cost. Sony’s HDR1000-rated surgical monitor demonstrates Mini-LED influence in specialty verticals. Micro-LED remains confined to ultra-large formats, evidenced by Hisense’s 136-inch showpiece, until manufacturing yields improve. The coexistence of multiple panel types ensures that each application - gaming, signage, healthcare - receives an optimal balance of cost, brightness, and longevity within the expanding 4K display resolution market.

By Screen Size: Larger Displays Capture Premium Market

The above-65″ class is forecast to climb at 15.35% CAGR, the fastest pace in the 4K display resolution market. Cheaper large panels and immersive home-cinema demand catalyzed the release of TCL’s 100-inch P715 quantum dot TV for Asia Pacific households. Brand portfolios give priority to slimmer bezels and high dynamic range to justify premium tickets despite energy-efficiency hurdles in Europe.

The 50–65″ bracket, responsible for 53.55% of revenue in 2025, remains the universal sweet spot where living-room space, price, and 4K pixel density align. Yield gains in Taiwan’s Mini-LED lines trimmed BOM costs, helping this size hold center ground in the 4K display resolution market. Sets below 49″ serve desktop, hospitality, and secondary-room placements, while ultra-large 66-84″ screens penetrate boardrooms and education halls where group visibility ranks high. Regional taste diverges, with North America favoring bigger footprints than Europe or East Asia, compelling brands to customize model mixes by channel.

By End-user Vertical: Healthcare Applications Drive Innovation

The healthcare segment is on track for 13.05% CAGR through 2031, outpacing every other vertical in the 4K display resolution market. Surgical suites adopted 4K monitors for minimally invasive procedures that rely on razor-sharp imagery. Sony’s workflow solutions combine 4K acquisition, recording, and routing to support integrated operating rooms. Winmate’s M320TF-SDI display adds 12G-SDI connectivity for latency-free transfers, addressing stringent hospital standards.

Consumer electronics still delivered 75.25% of 2025 revenue thanks to smart TVs and console gaming. Esports arenas and gaming cafés specify high-refresh 4K screens that double as event showcases. Corporate and education users pursue pixel-dense collaboration boards for hybrid meetings, while retail signage exploits 4K clarity to overcome glare in bright venues. Aerospace and defense remain specialized niches, demanding ruggedized 4K panels that withstand vibration and extreme temperatures. Each vertical’s nuanced requirements deepen product segmentation inside the broader 4K display resolution market.

Geography Analysis

Asia Pacific generated 45.60% of 2025 revenue, cementing its position as the largest territory in the 4K display resolution market. China’s subsidies enabled swift capacity ramps, while South Korea’s OLED leadership supplied high-margin panels globally. Japan’s goal of installing 50,000 millimeter-wave bases by 2027 reinforces the regional network backbone supporting 4K streaming uptake. India and Southeast Asia entered a new adoption phase as falling ASPs aligned with rising discretionary income, unlocking large untapped volumes.

The Middle East is forecast to post the highest CAGR at 13.62% between 2026 and 2031. GCC corporations rolled out 4K video walls to enhance hybrid collaboration, boosting demand for fine-pixel-pitch LED assemblies. Sony Middle East and Africa reported notable sales gains and aims to release the INZONE M9 4K monitor within 2025, reflecting the region’s appetite for premium displays. Online channels have already captured 20% of regional TV sales, prompting brands to fine-tune e-commerce logistics.

North America’s mature installed base still grew on the back of fast OTT content adoption and a robust gaming monitor upgrade cycle. Healthcare institutions expanded to 4K diagnostic suites, widening a lucrative sub-segment less exposed to price wars. Europe faced a dual narrative: tech-savvy consumers embraced larger OLED sets while stricter Eco-design norms raised compliance costs for panels over 65″, nudging suppliers toward energy-efficient Mini-LED designs. Latin America and Africa remained emergent frontiers; limited 4K broadcast spectrum in parts of Sub-Saharan Africa tempered growth, though rising broadband coverage signals future upside.

Regulatory Landscape

Energy-efficiency and product-definition rules remain the most visible cross-border constraints on 4K displays. In the European Union, Commission Regulation (EU) 2019/2021 (ecodesign for electronic displays) and Delegated Regulation (EU) 2019/2013 (energy labelling) shape hardware design choices for large-screen 4K TVs, reinforcing industry moves toward lower-power backlighting (Mini-LED dimming zones) and more efficient OLED matrices as screen sizes expand.

Trade and IP enforcement can also affect supply availability for LCD-based 4K products. The U.S. International Trade Commission continued to process Section 337 investigations tied to LCD display supply chains, including a June 2026 notice related to glass substrates for liquid crystal displays naming multiple major electronics brands, and a prior April 2024 final initial determination in a separate Section 337 matter involving LCD digital displays. In China, the National Radio and Television Administration issued GY/T 399-2024 defining technical requirements and measurement methods for 4K UHD set-top boxes across satellite, cable, and IPTV platforms, supporting interoperability and compliance testing for 4K delivery devices.

Value Chain Analysis

The value chain starts with upstream materials and equipment (glass substrates, polarizers, backlight units, OLED emissive materials), then moves into panel fabrication (LCD, OLED, Mini-LED, Micro-LED) led by large Asia-based manufacturers. It is followed by driver ICs and interface chips (for HDMI 2.1/DisplayPort 2.1), module assembly, and final OEM integration into smart TVs, monitors, signage/videowalls, and specialty vertical devices such as medical displays. Downstream routes split between consumer retail and e-commerce, and B2B channels such as system integrators for corporate and education video walls and hospitals, where calibration, mounting, and after-sales service are material differentiators.

Recent supply dynamics show both concentration and chokepoints. Omdia reported that panel makers ran higher utilization in early 2025 and then shifted toward production-to-order to manage inventory amid tariff uncertainty. At the same time, component disruptions such as polarizer supply issues and an ongoing dependence on a narrow pool of high-end display driver IC and interface silicon suppliers constrained shipments of flagship 4K products. At the technology frontier, partnerships broaden the ecosystem beyond traditional TV and monitor supply chains, including July 2026 collaboration between Samsung Display and Tencent on specialized gaming displays for China, and June 2026 joint development work by EssilorLuxottica and Applied Materials on AR optics and waveguides that can pull advanced microdisplay and high-resolution module capabilities into adjacent display form factors.

Competitive Landscape

The 4K display resolution market is moderately consolidated, dominated by vertically integrated panel makers that leverage scale for cost leadership and R&D heft. Samsung Electronics, LG Display, and BOE Technology retained pole positions by combining in-house semiconductor, panel, and final assembly capabilities. Samsung’s 21.0% stake in global gaming monitors and 34.6% share of OLED monitors highlight its grip on fast-growing niches. LG pursued Micro Lens Array optics to raise OLED brightness, protecting its premium TV franchise.

Component specialists such as Valens Semiconductor see a serviceable available market topping USD 9 billion by 2026 for high-speed connectivity chips, illustrating how ecosystem players profit from bandwidth-hungry content pipelines.[7]Valens Semiconductor, “Form F-1,” sec.gov SHENZHEN ANWELL INDUSTRY collaborates with tier-one brands on LED walls, filling application gaps outside mainstream consumer displays. In medical imaging, firms like Sony and Winmate differentiate through regulatory certifications and localized after-sales networks, capturing resilient margins.

Strategic moves increasingly revolve around panel innovations - tandem OLED stacks, higher frame-rate controllers, and power-saving backlights - rather than pure price cuts. Partnerships across software, mounting hardware, and cloud services add recurring revenue streams and create sticky customer relationships. As supply chains diversify to mitigate chipset shortages, competitors with strong supplier contracts are poised to retain share, while late adopters risk margin compression.

4K Display Resolution Industry Leaders

Sony Corporation

LG Display Co. Ltd

Samsung Electronics Co. Ltd

Toshiba Corporation

Sharp Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace sits in regulated, high-margin verticals where 4K resolution is tied to workflow outcomes and compliance rather than entertainment upgrades. Medical and surgical visualization is one such lane. The segment already has product proof points such as Sony's LMD-32M1MD 4K Mini-LED monitor with VESA HDR1000 certification, and vendors are expanding roadmaps, including TSD initiating full development of a 4K MiniLED surgical display in April 2026. These use cases favor suppliers that can pair 4K panels with factory calibration, high-luminance performance, and medical-grade system integration.

Another opportunity lies in performance-led 4K monitors, where interface and refresh-rate innovation supports replacement decisions and higher-price SKUs. The industry is moving beyond baseline 4K into ultra-high refresh 4K panels and alternative I/O paths when certain chipsets are constrained, illustrated by the shift toward DisplayPort 2.1 in new gaming monitors and Samsung Display announcing a 360 Hz 4K QD-OLED monitor panel with mass production slated for H2 2026. In parallel, EU ecodesign and energy-label compliance for electronic displays keeps power-optimized backlighting, efficient OLED architectures, and materials choices central to product planning, creating demand for component suppliers that reduce watts-per-nit without sacrificing HDR brightness in larger screen sizes.

Recent Industry Developments

- July 2026: Toshiba TV expanded the international rollout of its Z870 4K MiniLED series, positioning 144 Hz refresh as a mainstream premium feature across more geographies. Broader availability of high-refresh MiniLED TVs increases competitive pressure on established premium LCD and entry OLED tiers, especially in larger screen sizes.

- June 2026: EssilorLuxottica and Applied Materials announced joint development work on AR optics and waveguides that can pull advanced microdisplay and high-resolution module capabilities into adjacent display form factors. The collaboration signals cross-domain acceleration for AR/VR enabled displays and could expand applications beyond traditional screens.

- May 2026: Samsung Display announced development of a 360 Hz 4K QD-OLED monitor panel with dual-mode operation and scheduled mass production for H2 2026. This lifts the performance ceiling for 4K gaming monitors and provides OEM partners a new panel option for differentiated, high-ASP flagship models.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues linked to 4K display resolution panels and related display modules that are integrated into end devices such as monitors, smart TVs, and smartphones, tracked across major regions in current US dollars.

Scope exclusions: Finished end products (for example, complete 4K UHD or 4K OLED TVs sold as consumer electronics) are not counted when the price mainly reflects the whole device rather than the 4K display panel value.

Segmentation Overview

- By Product Type

- Smart TV

- Monitor

- Smartphone

- Tablet

- Laptop

- Digital Signage/Videowall

- Projection Screen

- Head-Mounted Display (HMD)

- Medical Display

- Others

- By Panel Technology

- LCD (IPS/VA/TN)

- OLED

- Mini-LED

- Micro-LED

- Others

- By Screen Size

- Below 32 inch

- 32-49 inch

- 50-65 inch

- 66-84 inch

- Above 84 inch

- By End-user Vertical

- Consumer Electronics (Household)

- Gaming and Esports Venues

- Business and Education

- Retail and Advertisement

- Media and Entertainment Production

- Healthcare

- Aerospace and Defence

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics (Denmark, Sweden, Norway, Finland)

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Southeast Asia

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the demand and supply context that a panel-driven market needs, then narrowing it down to what is truly 4K. We used public sources such as ITU and ISO publications for resolution standards, UN Comtrade for trade flows that indicate where electronics move, World Bank indicators for income and device affordability trends, and sources like OECD/IEA for power and efficiency context that can influence replacement cycles.

To keep assumptions realistic, we also reviewed company annual reports and earnings decks for display and device makers, investor presentations for shipment and mix commentary, and reputable press coverage of panel capacity changes and pricing pressure. In addition, we used a paid subscription for company financials and news intelligence, and a paid patent database to check whether 4K adoption is supported by product roadmaps rather than only marketing statements. These desk sources are illustrative, and we also relied on other references to collect inputs, validate them, and clarify open questions during the work.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions, especially around what portion of device shipments actually carries a 4K panel and how pricing has moved by screen size and panel type. We spoke with a mix of display ecosystem participants and large-volume buyers, then used follow-up questions to reconcile differences in regional adoption patterns and in how 4K is defined across products.

The final model assumptions were adjusted only after consistent inputs were received across multiple respondent groups, and after we checked that the implied panel value per device stayed within practical ranges for each end device type.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 42% |

| Mid tier: 55% | Functional/Unit leaders: 43% | EMEA: 36% |

| Smaller Players: 17% | Managers: 44% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where device shipment baselines and category demand signals are translated into a 4K panel value pool through adoption rates and average panel value assumptions, and then mapped by region. Once the total was formed, we corroborated it with selective bottom-up checks such as sampled ASP x estimated 4K unit volumes for monitors, smart TVs, and smartphones, followed by channel and panel-mix sanity checks.

Key inputs used in the model included the mix shift toward 4K-capable devices, 4K panel pricing movement by screen size, panel technology mix (for example LCD versus OLED where relevant), content availability signals that influence upgrades, and regional replacement cycles tied to income and usage intensity. Where bottom-up data was thin in smaller device categories, gaps were handled by applying conservative adoption bands validated in interviews, then rechecking that the implied totals stayed consistent with known shipment and capacity direction.

For forecasting, scenario analysis was used with a base case anchored to consensus views gathered in primary discussions, then stress-tested for panel price erosion and faster adoption in gaming and work-from-home setups. The forecast was not treated as a straight line, since pricing and mix changes can shift revenue differently than unit growth in a 4K-led market.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, then variance checks at the product and regional level before the final numbers were signed off. If a segment total implied an unrealistic 4K share or an abrupt ASP jump, the assumptions were revisited and, when needed, respondents were re-contacted to confirm what changed and why.

Each report is refreshed on an annual cycle, and interim updates are made when a material event occurs (for example, a sharp panel price swing or a capacity disruption). Before delivery, a final analyst pass is completed so the published view reflects the latest available data and any late-breaking market shifts.

Mordor Intelligence's Global 4k Display Resolution Market Market Sizing Compared With Other Published Estimates

Published values for the 4K display resolution market do not always match because researchers often count different items and then apply different price and adoption logic. The biggest swings usually come from whether the figure represents only the 4K panel value inside devices or the full finished device revenue, and also from how quickly 4K penetration is assumed to rise in smartphones and TVs.

Shipment mix checks and panel-value-per-device sanity tests are the evidence gates that keep Mordor Intelligence's 2026 estimate tied to 4K display panel economics rather than full end-product pricing. When a study combines 4K finished-device sales with panel scope, or uses aggressive adoption curves without cross-checking implied ASPs, the market total can land far above or below what the device and panel signals support.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 246.52 B (2026) | |

| Global Consultancy A | USD 159.60 B (2025) | Uses a different base year and a broader definition of 4K resolution formats, and the sizing frame appears to mix multiple 4K use cases without clearly separating panel value from device-level revenue. |

| Industry Publisher B | USD 213.00 B (2025) | Includes a wider product set (such as cameras and projectors) and applies a higher long-range growth trajectory, which can inflate the total if 4K penetration and ASP paths are not rechecked against device shipment reality. |

Looking across the three figures, most of the spread is explained by scope boundaries and the year used for the starting point, followed by how adoption and ASP progression are handled across devices. Our approach stays repeatable because it links revenue to observable shipment and mix signals, then uses interview-based checkpoints to keep assumptions practical.

Key Questions Answered in the Report

What is the current size of the 4K display resolution market?

The market stood at USD 246.52 billion in 2026 and is forecast to rise to USD 463.97 billion by 2031.

Which segment is expanding the fastest within the 4K display resolution market?

Gaming monitors are projected to grow at a 13.84% CAGR from 2026 to 2031, driven by esports standardization of 4K/144 Hz specifications

Why are OLED panels gaining share against LCD in 4K displays?

OLED offers pixel-level dimming, superior contrast, and higher refresh scalability, and production capacity is increasing, supporting a 16.25% CAGR through 2031.

How do EU Eco-design rules affect large 4K televisions?

Upcoming efficiency standards raise compliance costs for sets over 65″, prompting manufacturers to adopt Mini-LED or power-optimized OLED architectures for the European market.

Page last updated on: