Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

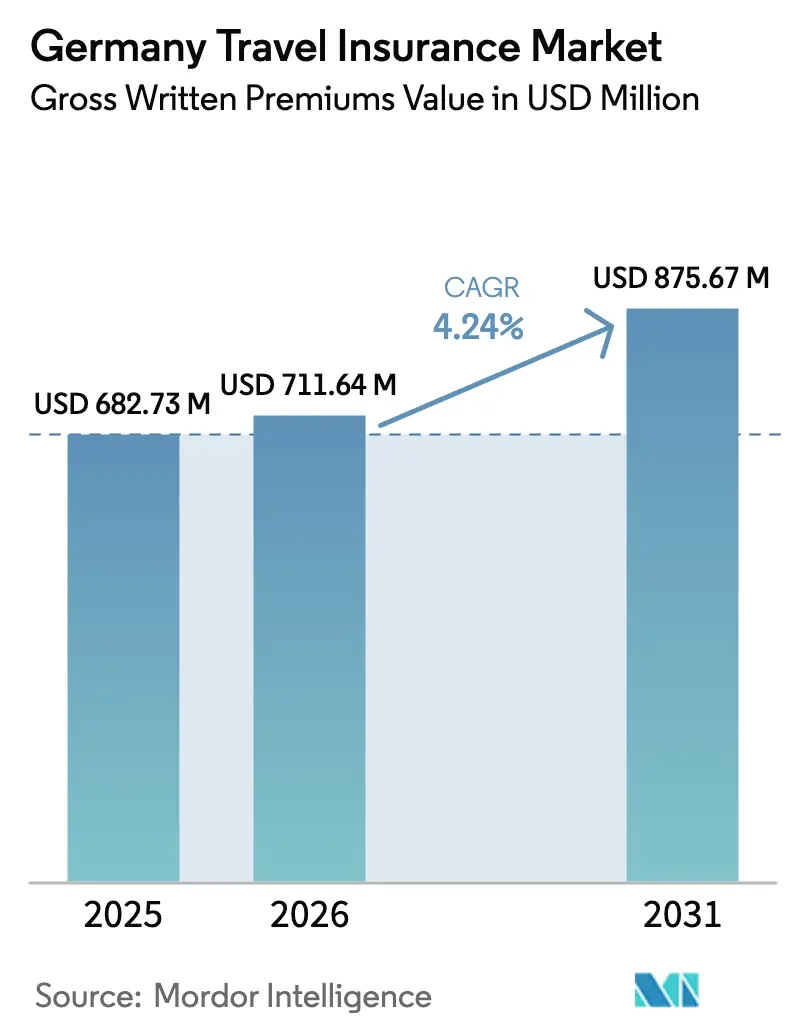

| Base Year Market Size (2025) | USD 682.73 Million |

| Market Size (2026) | USD 711.64 Million |

| Market Size (2031) | USD 875.67 Million |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

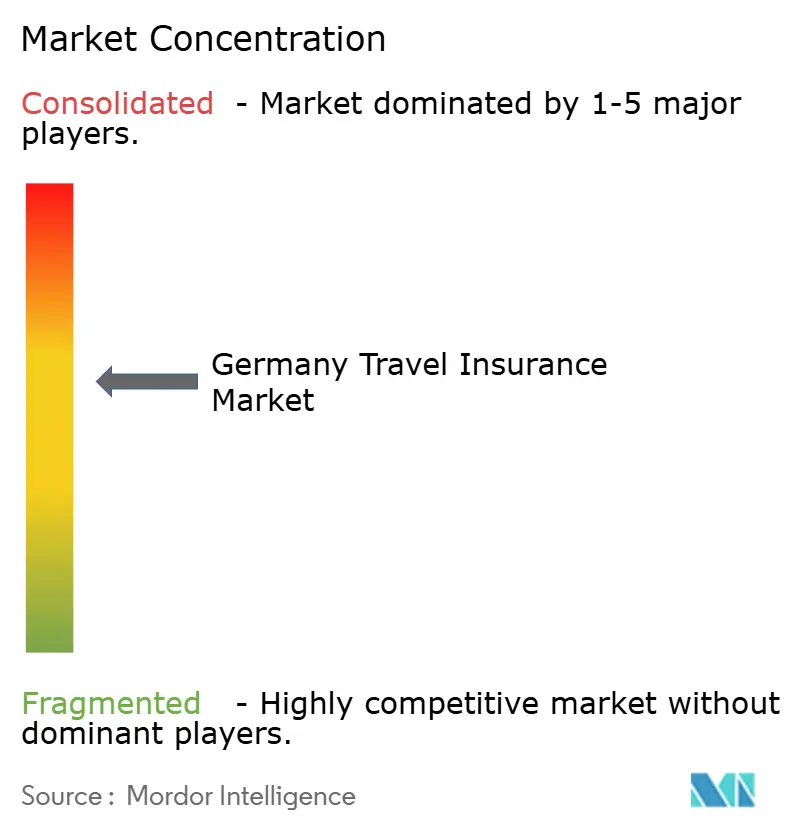

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Travel Insurance Market Analysis by Mordor Intelligence

The Germany Travel Insurance Market size in terms of gross written premiums value is projected to be USD 682.73 million in 2025, USD 711.64 million in 2026, and reach USD 875.67 million by 2031, growing at a CAGR of 4.24% from 2026 to 2031.

German residents completed 67.7 million vacations of five days or longer in 2025, and 77.8% of those trips were abroad, which sustains a consistent base for medical and trip protection purchases that reinforce the Germany travel insurance market. Average spending per trip stands at USD 758 and remains near the top of the European Union, signaling that coverage limits and assistance networks need to match higher-ticket itineraries. Statutory GKV coverage through the European Health Insurance Card does not include medical repatriation or many non-emergency services abroad, which keeps private travel health and assistance covers central to the Germany travel insurance market. Embedded offerings at the point of booking, such as airline and telecom bundles, are gaining traction and are shaping consumer expectations for simplified enrollment and rapid claims experiences within the Germany travel insurance market. Parametric solutions for flight delays, baggage issues, and weather events are expanding use cases for small, instant payouts, which improve perceived value in the Germany travel insurance market, where climate disruption and operational delays remain front of mind.

Key Report Takeaways

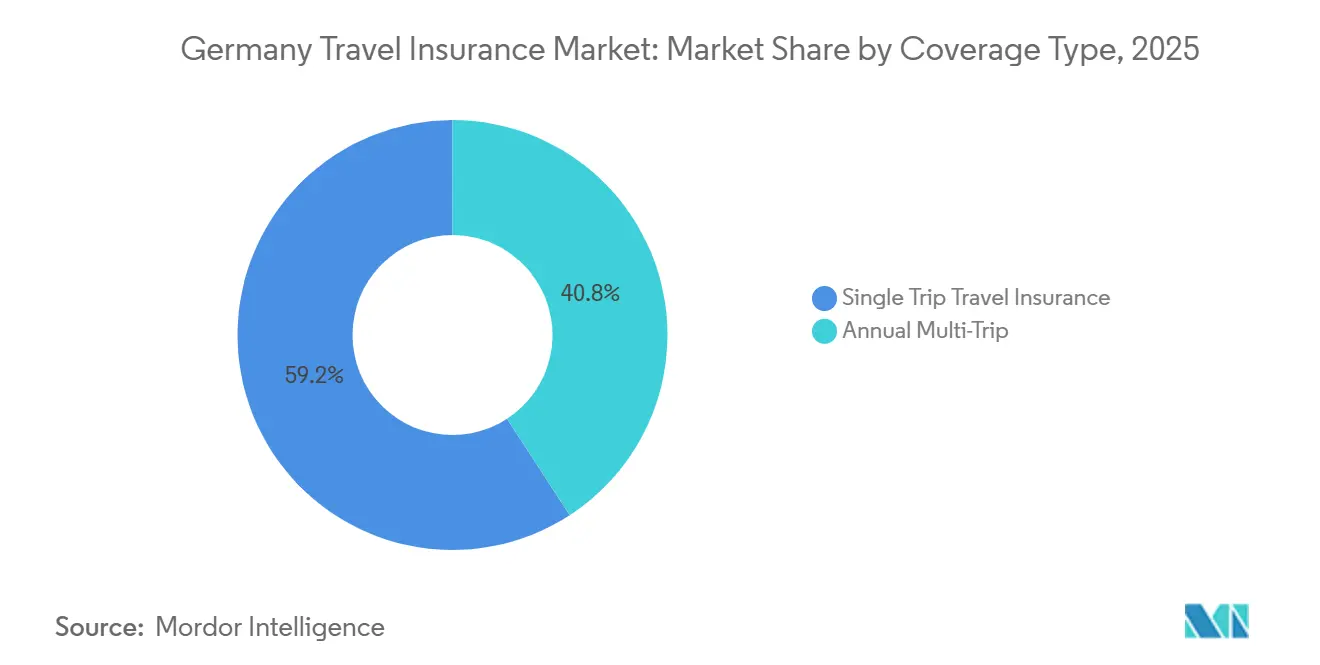

- By coverage type, single-trip policies held 59.18% of the Germany travel insurance market share in 2025; annual multi-trip plans are on track for a 12.74% CAGR through 2031.

- By end user, family travelers captured 39.96% of the Germany travel insurance market size in 2025, while education travelers are set to grow at a 14.86% CAGR over 2026-2031.

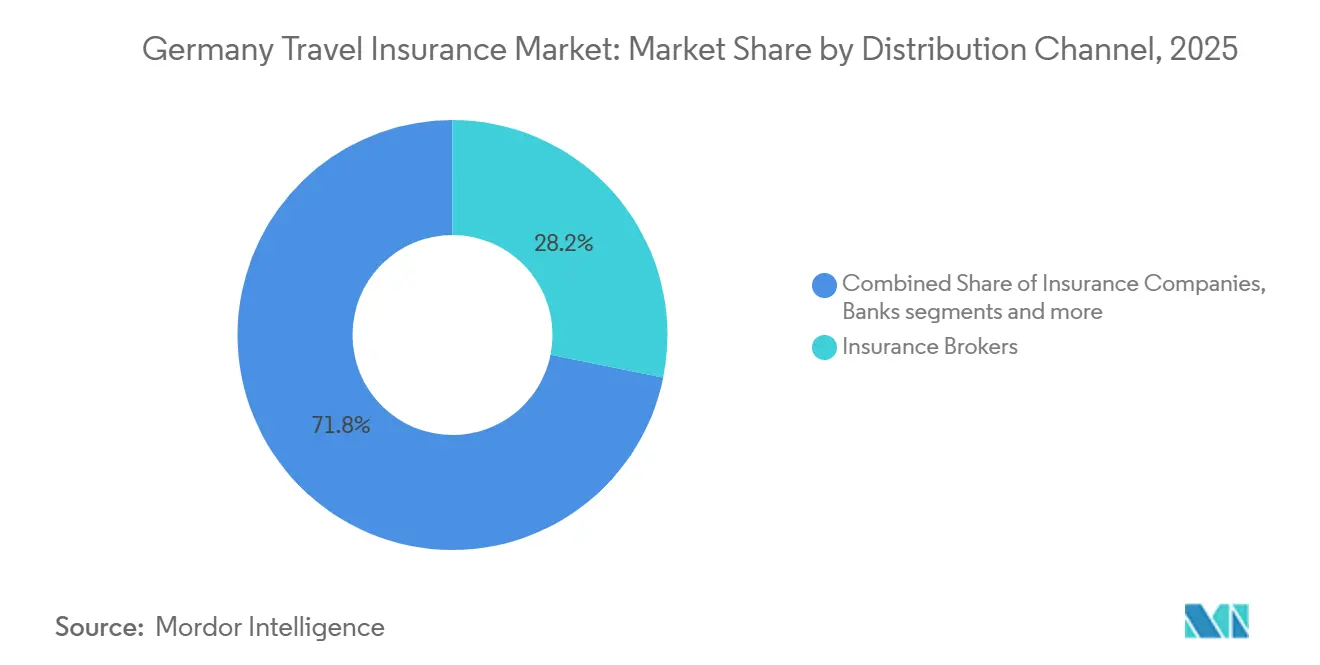

- By distribution, brokers commanded 28.17% of the Germany travel insurance market; aggregator platforms are projected to advance at a 18.42% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Travel Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outbound travel rebound and higher spend among German residents | 1.20% | Global, concentrated in Mediterranean & long-haul sun destinations | Medium term (2-4 years) |

| Business travel revival lifting annual multi-trip uptake | 0.80% | Global, with early gains in European corridors and North America | Short term (≤ 2 years) |

| GKV/EHIC coverage gaps driving private travel health purchase | 0.90% | EU/EEA for EHIC gaps; global for repatriation need | Long term (≥ 4 years) |

| Embedded distribution via OTAs, airlines, and neobanks | 0.70% | National, with early adoption in urban centers (Berlin, Munich, Frankfurt) | Medium term (2-4 years) |

| Climate-disruption risk repricing and parametric protection | 0.50% | Global, acute in Mediterranean, Alpine, and long-haul destinations prone to wildfires, floods, extreme weather | Medium term (2-4 years) |

| IDD-driven transparency shifting sales toward specialist/digital advice | 0.30% | National, concentrated in digitally-savvy demographics and urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Outbound Travel Rebound and Higher Spend Among German Residents

German travelers sustained a large outbound footprint in 2025 with 67.7 million vacations of at least five days and 77.8% of those trips taken abroad, which increases exposure to cross-border health costs and disruption risk[1]Deutscher Reiseverband, “Zahlen und Fakten 2026,” Deutscher Reiseverband, drv.de. Average spending per trip at USD 758 keeps coverage adequacy top of mind for families and longer-duration holidays, and it supports stronger demand for higher-sum-insured options in the Germany travel insurance market[2]Eurostat, “Tourism Statistics, Expenditure,” European Commission, ec.europa.eu. Spain, Turkey, and Italy remained leading destinations for long vacations in 2025, which aligns product design with well-trodden corridors and assistance networks across Southern Europe. The share of flights as the main mode of transport stayed high in 2025, which elevates the value of flight disruption, baggage, and medical emergency riders for outbound travel within the Germany travel insurance market. A rising share of consumers now factor weather and natural disaster risk into destination choice, which sustains interest in flexible cancellation and parametric add-ons that pay quickly for validated events.

GKV and EHIC Coverage Gaps Driving Private Travel Health Purchase

Germany’s statutory health insurance provides emergency care access in EU and EEA countries through the European Health Insurance Card, yet it does not cover medical repatriation, and it may not match the service level of private facilities abroad, which pushes many households to buy dedicated travel health cover. Consumers who travel beyond the EHIC area face full exposure for out-of-network costs and transport back to Germany, so the Germany travel insurance market benefits from steady demand for comprehensive medical assistance and evacuation benefits. Private health insurance policies sometimes include broader global benefits, though many tariffs still limit duration or define repatriation thresholds narrowly, which leaves travelers reliant on standalone travel health plans when taking longer or higher-risk trips. Insurers in Germany reported robust growth in travel health lines, underscoring a clear shift toward treating medical assistance and evacuation as non-discretionary for households that take international vacations. Consumer education from regulators and associations has highlighted the limitations of statutory coverage abroad, which reinforces consistent purchase behavior in the Germany travel insurance market when trips include countries outside the EHIC framework.

Aging Population Driving Senior-Specific Policies

Embedded insurance at the point of booking is reshaping how policies are discovered and purchased in the Germany travel insurance market, with mobile and partner channels improving attach rates for commodity covers such as international health and basic disruption riders. ERGO’s collaboration with O2 Telefónica added a travel health component to a monthly subscription, which reduces friction by integrating insurance in the telecom bill for millions of eligible customers. Berlin Direkt Versicherung launched parametric flight disruption and lost luggage features through Blink Parametric, enabling automatic alerts and instant cash or lounge benefits when delays or baggage issues are validated by external data feeds. Parametric travel covers from Baloise for weather and delays showcase a broader move toward predetermined triggers that pay small amounts fast, which improves perceived value among digital-first buyers in the Germany travel insurance market. Regulatory guardrails under the Insurance Distribution Directive allow ancillary intermediaries to distribute simple insurance products if they meet disclosure and professional requirements, which enables embedded partnerships to scale within a compliant framework in Germany.

Climate Disruption Risk Repricing and Parametric Protection

More intense wildfires, floods, and heat events across common holiday destinations are elevating disruption and cancellation risk, so insurers are refining pricing and deploying targeted covers in the Germany travel insurance market. Parametric modules for weather, flight delays, and baggage provide transparent triggers and faster payouts, which reduce operational costs and enhance customer satisfaction during peak travel seasons. Real-time data sources allow instant decisions that bypass manual claims, as shown by Blink’s integrations that switch on lounge access or cash as soon as delay conditions are met[3]Blink Parametric, “Partners With Berlin Direkt Versicherung,” Blink Parametric, blinkparametric.com. Reinsurers are expanding parametric capacity across climate perils, which supports product innovation and risk transfer within the Germany travel insurance market. As travelers weigh destination risk more explicitly, these modular solutions help right-size limits and premiums while preserving clarity around what events are covered and how fast payouts arrive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin compression from comparison portals and commission transparency | -0.40% | National, acute in online-savvy demographics | Short term (≤ 2 years) |

| Medical cost inflation in key destinations pressuring premiums | -0.30% | Global, most acute in United States, Switzerland, Australia, and Japan | Medium term (2-4 years) |

| EU261 overlap reducing perceived need for trip disruption cover | -0.20% | EU/EEA flight routes | Long term (≥ 4 years) |

| Bundled bank/credit card cover cannibalizing stand-alone policies | -0.20% | National, concentrated in affluent segments holding premium credit cards | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Margin Compression from Comparison Portals and Commission Transparency

IDD remuneration disclosures have made commission structures more visible, which narrows pricing headroom for intermediated single-trip products and deepens price-based competition in the Germany travel insurance market. Standardized consumer testing, including Stiftung Warentest ratings of leading tariffs, pushes carriers toward similar product configurations, which increases comparability and encourages shoppers to select the lowest premium once baseline cover quality is confirmed. Large digital platforms can direct high-intent traffic to comparison pages, which reduces the volume of direct-originated policies on insurer websites in the Germany travel insurance market. Carriers respond by emphasizing service metrics such as claims turnaround and 24x7 assistance access, and by sharpening embedded partnerships where attach rates are strongest at the point of booking. The shift favors scale players and specialist brands that can sustain digital marketing and compliance costs while maintaining responsiveness for brokers and travel distributors in the Germany travel insurance market.

Medical Cost Inflation in Key Destinations Pressuring Premiums

Outside the EHIC zone, travelers face hospital and emergency transport bills that can quickly climb into high five figures, which reinforces the need for comprehensive medical and evacuation benefits in the Germany travel insurance market[4]InformedHealth.org, “Health Insurance in Germany,” IQWiG, ncbi.nlm.nih.gov. Even within the EHIC area, public-system access may involve co-payments or service constraints that do not mirror German standards, which increases the appeal of private travel health cover for faster access and broader reimbursement. Insurers report strong growth in travel health lines, which is consistent with rising claim severities and a broader consumer focus on medical readiness during international travel. Premium adjustments reflect both destination-level treatment inflation and currency effects on assistance costs, which requires careful communication to preserve trust while explaining coverage value in the Germany travel insurance market. Clear disclosures on what constitutes a medically necessary evacuation and what limits apply help align expectations and reduce disputes at claim time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage Type: Multi-Trip Outpaces Despite Single-Trip Dominance

Single-trip policies commanded 59.18% of the Germany travel insurance market share in 2025 as households prioritized per-journey coverage for short breaks and long holidays, while annual multi-trip plans are projected to scale rapidly on the back of frequent travelers and corporate buyers. The Germany travel insurance market benefits from varied trip patterns, and the prevalence of outbound vacations to nearby European destinations supports single-trip purchases for one-off family holidays and city weekends. Multi-trip policies expand the addressable base as travelers plan multiple journeys in a year and seek the convenience of one policy for all travel within defined trip-duration limits, which fits well with repeat travel to Spain, Italy, and Turkey. Carriers have updated product design to keep pace with demand, including broader cancellation reasons and higher insured sums for premium lines in the Germany travel insurance market. Consumer-upgrade paths now include parametric modules for delay and baggage, which complement both single-trip and multi-trip structures and help reduce friction at claim time.

Annual multi-trip products are projected to grow at a 12.74% CAGR through 2031, which reflects higher-frequency travel behavior among working professionals and retirees who take multiple short trips each year. The Germany travel insurance market size for annual multi-trip policies is projected to expand at a 12.74% CAGR between 2026 and 2031 as travelers trade per-trip optimization for year-round certainty and streamlined administration. Assistance networks and rapid claims handling remain decisive differentiators for multi-trip buyers who expect responsive support when disruptions occur across any journey in policy scope. Insurers are aligning plan features with the most common travel windows and durations, and they continue to emphasize clear disclosures on maximum trip length and exclusions under current regulatory expectations in the Germany travel insurance market.

By End User: Education Travelers Surge While Families Anchor Premiums

Family travelers held 39.96% of the Germany travel insurance market share in 2025, supported by the country’s strong package-tour culture and continued preference for insuring longer vacations that include children and older relatives. The segment’s steady base gives carriers a clear target for bundle design that pairs cancellation and health benefits with baggage and assistance, which helps minimize interruptions during school breaks and peak summer windows. Families often prioritize broad medical coverage in the EHIC area and beyond, and they place value on 24x7 assistance with multilingual support in the Germany travel insurance market. Specialist brands have earned strong consumer trust through independent testing, which raises the likelihood of purchase during tour-operator checkout or through travel advisers who curate family plans.

Education travelers are the fastest-growing end user at a projected 14.86% CAGR to 2031, as students and exchange participants require comprehensive international health and assistance for long stays abroad. The Germany travel insurance market size for education travelers is projected to rise at a 14.86% CAGR as tariffs tailored to younger demographics include extended medical cover, liability protection where applicable, and sport or study-related extensions. These products often include longer policy terms and flexible start dates that match academic calendars, and they emphasize clear wording on pre-existing conditions and permitted activities in the Germany travel insurance market. The result is a consistent pipeline of long-stay customers whose policy needs differ from leisure travelers and whose purchase decisions hinge on transparent benefits and recognized brand credibility.

By Distribution Channel: Embedded and Aggregator Growth While Brokers Retain Complex Cases

Insurance brokers held 28.17% of distribution in 2025 as affluent households and complex itineraries relied on curated combinations of cancellation, medical, and baggage benefits with tailored sums insured in the Germany travel insurance market. Brokers maintain strength where product selection and claims support matter most, and they continue to partner with leading carriers that demonstrate fast service and clear documentation under IDD standards. Embedded distribution rose through partnerships with mobile, airline, and OTA platforms that present insurance at checkout, as seen with O2 Telefónica and ERGO’s launch of a travel health subscription that integrates into monthly billing workflows. Parametric integrations improve user experience for digital channels, which helps position aggregators and direct platforms to serve simple needs quickly in the Germany travel insurance market.

Insurance aggregators are projected to post the fastest channel growth through 2031, while brokers continue to own higher-value and multi-trip placements that benefit from tailored advice. Direct channels remain important for brand-loyal customers, and insurers are investing in self-service apps and digital claims that reduce friction and support cross-border assistance in the Germany travel insurance market. Compliance with IDD requires clear disclosure of remuneration and target-market suitability, which maintains a level playing field as embedded and aggregator flows expand. The combined effect is a hybrid distribution landscape where embedded and comparison channels capture commodity needs while brokers and bancassurance focus on longer stays, families, and business travelers within the Germany travel insurance market.

Geography Analysis

Outbound European destinations continue to anchor demand, with 77.8% of long vacations taken abroad in 2025 and a concentration in Spain, Turkey, and Italy that aligns with established assistance networks for the Germany travel insurance market. EHIC-based access to emergency care in EU and EEA countries reduces first-line medical exposure but not repatriation or private facility costs, so comprehensive travel health policies remain essential for families and older travelers. Summer heat events and wildfires in Mediterranean destinations have reinforced the role of cancellation and disruption riders, which support coverage uptake during the peak holiday calendar in the Germany travel insurance market. Carriers emphasize clear wording for destinations under travel advisories and conditions that may void or modify benefits, which helps reduce disputes and aligns expectations ahead of departure.

Intercontinental trips to North America, North Africa, and Asia have a disproportionate impact on risk and pricing because treatment and evacuation costs can be significantly higher outside the EHIC area, and policy buyers respond by selecting greater medical limits in the Germany travel insurance market. Popular long-haul itineraries require robust 24x7 assistance and clear repatriation triggers to manage clinical decisions and logistics, and they benefit from carriers with global networks and digital claims features. Parametric options are gaining relevance for long-haul flight delays due to operational complexity at major hubs, where automatic benefits reduce stress and spending during unplanned waiting periods. As travel patterns stabilize in 2026, insurers continue to refine destination-specific pricing and benefit design to accommodate varying standards of care and claims pathways across regions in the Germany travel insurance market.

Domestic travel accounts for a smaller share of long vacations, yet higher-value bookings for wellness or resort stays still create cancellation exposure that supports selective policy uptake within Germany. Product messaging for domestic-only policies emphasizes cancellation, trip interruption, and baggage benefits rather than medical cover because GKV applies fully inside national borders. Distributors tailor offers to school holidays and public long-weekend patterns, which contributes to predictable seasonal spikes in the Germany travel insurance market. Clear disclosures on covered reasons and documentation standards for cancellations help families and older travelers align purchase decisions with trip budgets and refund policies across German destinations.

Competitive Landscape

Market leadership in the Germany travel insurance market remains with established carriers that pair multi-decade distribution relationships with product refreshes and stronger digital servicing. HanseMerkur extended major distribution partnerships into 2025, and broadened cancellation features for premium lines to match higher trip values. ERGO demonstrated embedded momentum through its O2 Telefónica launch, which gives access to one of the country’s largest mobile customer bases for subscription-style travel health in the Germany travel insurance market. Allianz Partners expanded digital front doors for customers with its Allyz app, reinforcing always-on assistance and easy access to benefits for cross-border travelers.

Zurich strengthened its global position by acquiring AIG’s personal travel insurance and assistance business and integrating it with Cover-More, which expands scale and positions the group to compete more actively for OTA and airline partnerships that influence the Germany travel insurance market. Würzburger Versicherungs-AG’s TravelSecure brand won top ratings from Stiftung Warentest in January 2026 for 156 tariff variants, signaling strong consumer trust that supports broker and direct channel growth. Berlin Direkt Versicherung advanced instant-payout capabilities through Blink Parametric, which validates events from external data feeds and automates either lounge access or cash options, reflecting the industry’s shift toward low-friction claims in the Germany travel insurance market. Union Reiseversicherung continued to enhance product breadth in early 2025 with new modules and higher insured sums, signaling a focus on value features that match rising trip budgets.

Competitive focus centers on three levers that define share gains in the Germany travel insurance market. First, travel distribution depth through tour operators and agencies remains pivotal because it places offers at the point of booking and elevates attach rates for cancellation and medical bundles. Second, embedded partnerships with mobile, airline, and OTA ecosystems open acquisition pathways for commodity policies where simplicity drives conversion, and brand switching is common. Third, product and service differentiation through parametrics and app-based claims sets new expectations for speed, which resonates with digital-native demographics now booking more short trips each year. Regulatory oversight under IDD keeps sales practices and disclosures consistent across channels, which stabilizes the competitive field and rewards brands that combine compliance strength with user-friendly experiences in the Germany travel insurance market.

Germany Travel Insurance Industry Leaders

Allianz Partners

HanseMerkur

ERGO Reiseversicherung

AXA Partners

Europ Assistance

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Würzburger Versicherungs-AG's TravelSecure brand received "SEHR GUT" (1.2) ratings from Stiftung Warentest (Finanztest 01/2026) for 156 tariff variants of travel cancellation insurance and was awarded "Testsieger" for single and family policies.

- March 2025: Allianz joined a consortium to acquire Viridium Group for EUR 3.5 billion (USD 3.85 billion), enlarging its run-off portfolio.

- March 2025: Union Reiseversicherung introduced a new baggage module in Q2 2025, offering sums insured of USD 3,120 for individuals and USD 6,240 for families. The module can be booked standalone or as an add-on to travel cancellation, international health, and travel packages.

- December 2025: ERGO Reiseversicherung announced a strategic alliance with Lifecard Travel Assistance (LTA), a specialist insurer. The collaboration focused on developing novel travel insurance products and expediting the introduction of fresh innovations in the sector.

Germany Travel Insurance Market Report Scope

Travel insurance is defined as a sector within the insurance industry that provides financial protection and assistance to travelers, specifically addressing the needs of German residents who travel domestically and internationally.

The German travel insurance market is segmented by coverage type, distribution channel, and end-user. By coverage type, the market is segmented into single-trip travel insurance and annual multi-trip travel insurance. By end user, the market is segmented into senior citizens, education travelers, business travelers, family travelers, and other end users. By distribution channel, the market is segmented into insurance intermediaries, insurance companies, banks, insurance brokers, and insurance aggregators. The report offers market size and forecasts in terms of value (USD) for all the above segments.

By Coverage Type

| Single Trip |

| Annual Multi-Trip |

By End User

| Senior Citizens |

| Education Travelers |

| Business Travelers |

| Family Travelers |

| Other End-Users |

By Distribution Channel

| Insurance Intermediaries |

| Insurance Companies |

| Banks |

| Insurance Brokers |

| Insurance Aggregators |

| By Coverage Type | Single Trip |

| Annual Multi-Trip | |

| By End User | Senior Citizens |

| Education Travelers | |

| Business Travelers | |

| Family Travelers | |

| Other End-Users | |

| By Distribution Channel | Insurance Intermediaries |

| Insurance Companies | |

| Banks | |

| Insurance Brokers | |

| Insurance Aggregators |

Key Questions Answered in the Report

What is the Germany travel insurance market growth outlook to 2031?

The Germany travel insurance market size is expected to increase from USD 711.64 million in 2026 to USD 875.67 million by 2031 at a 4.24% CAGR, supported by steady outbound travel and wider adoption of embedded and parametric products .

Which coverage types are leading and growing fastest in Germany?

Single-trip policies led with 59.18% share in 2025, while annual multi-trip policies are projected to grow at a 12.74% CAGR through 2031 as frequent travelers prioritize convenience .

Who are the notable players shaping the competitive landscape?

HanseMerkur, ERGO, Allianz Partners, Union Reiseversicherung, Würzburger TravelSecure, Zurich Cover-More, and Berlin Direkt are key players, with moves such as embedded telecom partnerships, parametric claims, and high consumer ratings influencing share in the Germany travel insurance market.

Why do German travelers still buy private travel health insurance in Europe?

Embedded partnerships with airlines, OTAs, and mobile providers will scale simple covers, while brokers remain central for multi-trip and complex itineraries under clear IDD disclosure norms in the Germany travel insurance market.

How are climate and disruption risks changing product design?

Carriers are adding parametric modules with predefined triggers for weather and flight delays to deliver instant payouts and reduce friction, a feature that is gaining momentum in the Germany travel insurance market.

Page last updated on: