Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

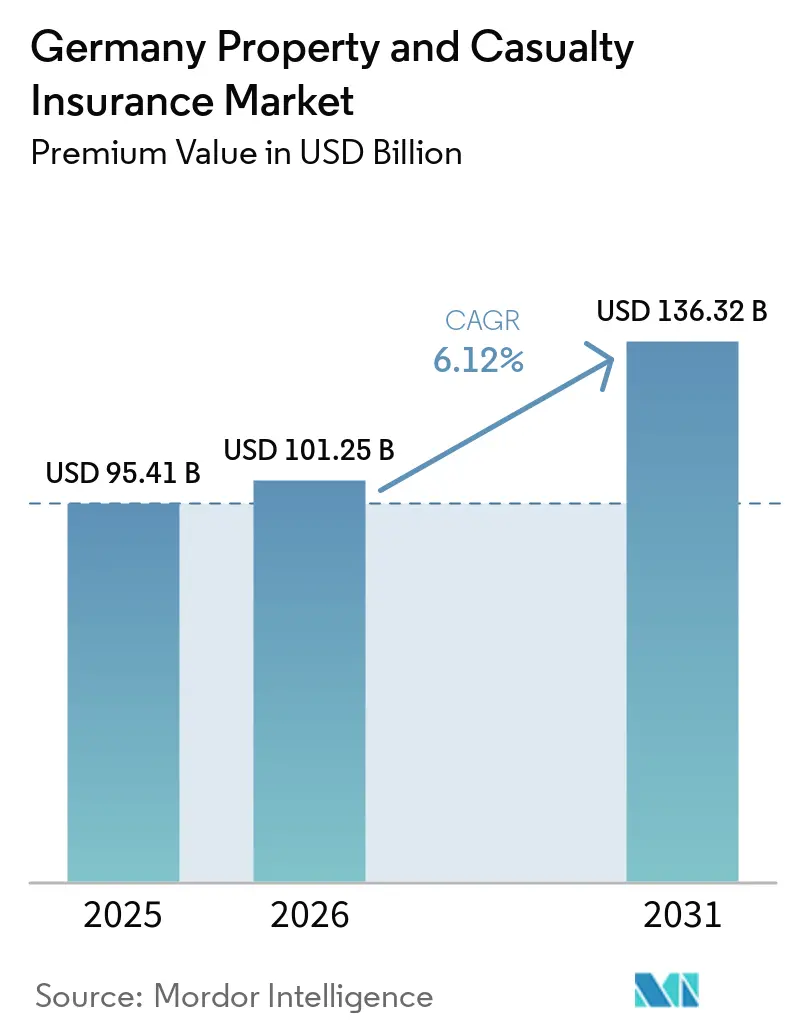

| Base Year Market Size (2025) | USD 95.41 Billion |

| Market Size (2026) | USD 101.25 Billion |

| Market Size (2031) | USD 136.32 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Property and Casualty Insurance Market Analysis by Mordor Intelligence

The Germany Property And Casualty Insurance Market size in terms of premium value is expected to increase from USD 95.41 billion in 2025 to USD 101.25 billion in 2026 and reach USD 136.32 billion by 2031, growing at a CAGR of 6.12% over 2026-2031.

The steady climb in the German property and casualty insurance market size mirrors the sector’s capacity to raise premiums and tighten underwriting standards amid heavier natural-catastrophe losses, stricter Solvency II capital rules, and new Digital Operational Resilience Act (DORA) mandates that took effect in January 2025. Heightened compliance spending on cybersecurity is pushing carriers to accelerate operating-model redesign, while embedded distribution and API-driven connectivity keep customer-acquisition costs in check. Pricing momentum in property lines continues as severe convective storms and flood events inflate reinsurance costs, yet the German property and casualty insurance market benefits from policy discussions on mandatory natural-hazard cover that could widen its premium base. Technology investments in straight-through underwriting, claims automation, and AI-enabled risk scoring underpin margin protection, allowing larger carriers to offset claims-cost inflation in motor insurance.

Key Report Takeaways

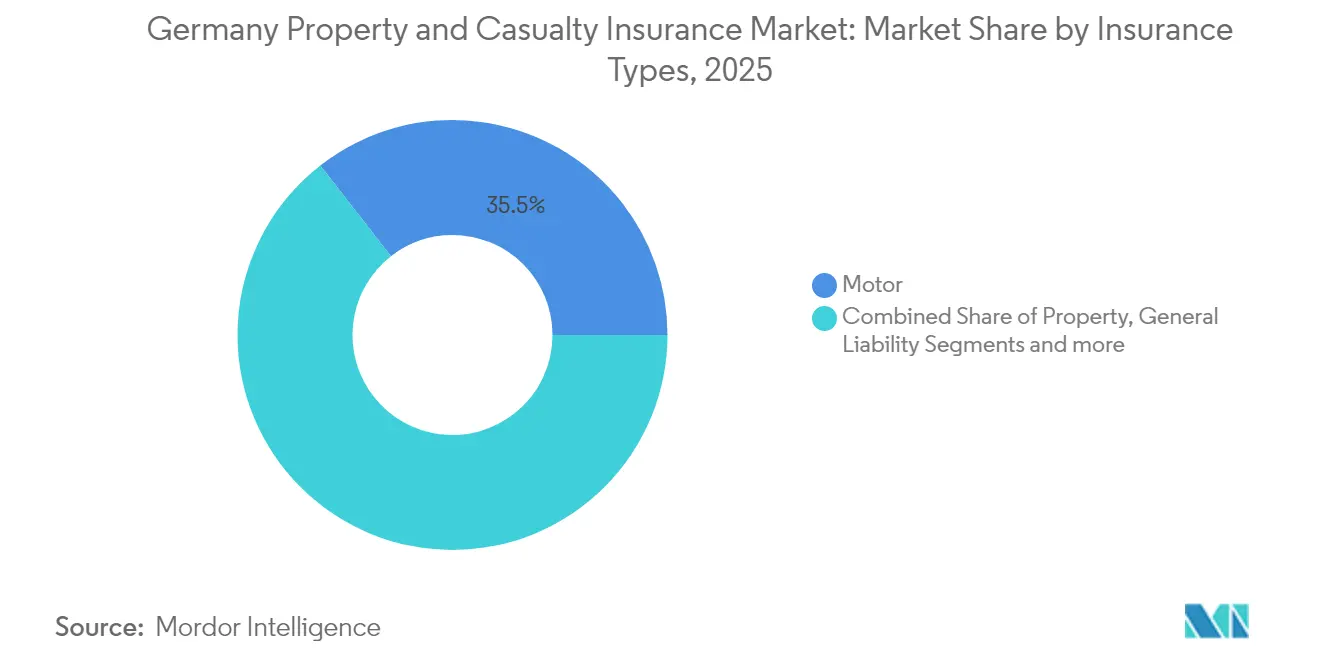

- By insurance type, motor insurance led with 35.54% of Germany property and casualty insurance market share in 2025; specialty lines are projected to expand at a 12.86% CAGR through 2031.

- By distribution channel, brokers and independent agents held 44.02% of the Germany property and casualty insurance market size in 2025, while direct & digital channels posted the fastest 10.88% CAGR to 2031.

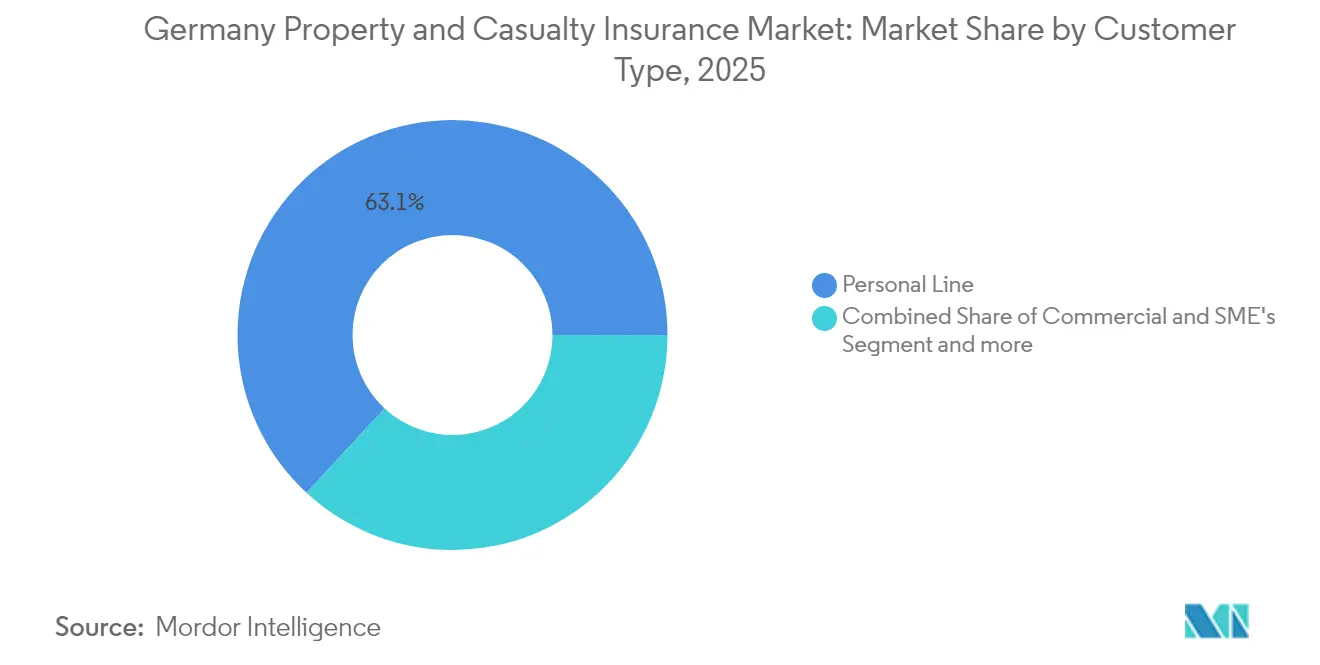

- By customer type, personal lines represented 63.12% of premiums in 2025, whereas corporate & industrial lines advanced at a 7.18% CAGR through 2031.

- By end-user industry, construction and real estate accounted for 55.06% of premiums and are advancing at 5.61% annually.

- By region, Westdeutschland captured 44.92% revenue share in 2025; Ostdeutschland delivers the highest 5.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Property and Casualty Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitalization & API-first insurance ecosystems | +1.2% | National, with early gains in Munich, Hamburg, Berlin | Medium term (2-4 years) |

| Regulatory reforms (IDD, Solvency II review, ESG disclosures) | +0.8% | National, aligned with EU framework | Long term (≥ 4 years) |

| Rise in NatCat losses driving premium growth | +1.5% | National, concentrated in Bavaria, Baden-Württemberg | Short term (≤ 2 years) |

| Embedded & usage-based coverages in mobility and retail | +0.9% | National, with urban concentration | Medium term (2-4 years) |

| AI-driven straight-through underwriting efficiencies | +0.7% | National, led by major insurers | Medium term (2-4 years) |

| Mandatory flood-cover debate & public–private pool design | +0.6% | National, priority in flood-prone regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digitalization and API-first insurance ecosystems driving market

API-first architecture is reshaping how players engage customers and partners. ERGO’s tie-up with O2 Telefónica rolled out “O2 Care” in August 2024, embedding device insurance directly in mobile bills and unlocking a demographic that prefers digital-native transactions. Allianz Direct’s single-platform model spans multiple EU markets, enabling real-time pricing, instant policy issuance, and low-touch claims flows. As the German property and casualty insurance market scales API connectivity, incumbents integrate motor telematics, travel, and gadget cover into fintech, mobility, and retail ecosystems, broadening reach without heavy fixed-cost sales networks. BaFin’s proportionality approach eases supervisory burdens for innovative pilots while keeping consumer protections intact [1]Bundesanstalt für Finanzdienstleistungsaufsicht, “BaFin Annual Report 2025,” bafin.de.

Regulatory reforms (IDD, Solvency II review, ESG disclosures) as driver

The 2024 Solvency II recalibration introduced capital-efficiency levers for long-term infrastructure assets and stricter climate-risk stress testing, steering investment toward renewable-energy projects and low-carbon portfolios. From 2025, the Corporate Sustainability Reporting Directive (CSRD) adds mandatory climate-risk disclosure for large insurers, nudging underwriters to integrate ESG metrics into pricing and reserving. IDD enhancements elevate product-suitability duties, favoring players with digital portals that offer real-time comparisons and personalised guidance. Collectively, these shifts strengthen policyholder protection and channel fresh capital into sustainable German infrastructure, enlarging the Germany property and casualty insurance market over the long term[2]Münchener Rückversicherungs-Gesellschaft AG, “REALYTIX ZERO Product Sheet,” munichre.com.

Rise in NatCat losses driving premium growth

Insured natural-catastrophe claims hit USD 6.21 billion in 2024, up USD 1.85 billion from 2023[3]Clean Energy Wire, “Germany Weighs Mandatory Natural-Hazard Insurance,” cleanenergywire.org. Severe convective storms eclipsed flood events as the top loss driver, compelling reinsurers to lift rates and lower catastrophe limits, which primary players pass on through higher household premiums. Only 54% of German homes carry NatCat coverage, sparking official debate over compulsory flood insurance. If enacted, the measure could enlarge the Germany property and casualty insurance market size materially during the forecast horizon. Munich Re data show improved warning systems kept September 2024 Central European flood losses to USD 1.74-2.29 billion, proving that mitigation investments restrain severity even as event frequency rises.

Embedded & usage-based coverages in mobility and retail

Telematics programs such as HUK-COBURG’s “Telematik Plus” cut premiums by up to 30%, rewarding safe driving and sharpening risk segmentation. Partnerships between mobility platforms and players embed trip-based cover into ride-hailing or car-sharing apps, widening reach among younger consumers. For retailers, warranty and device-protection add-ons bundled at checkout become incremental revenue streams. As data flows scale, the Germany property and casualty insurance market leverages behavioural analytics to refine rating factors, curbing anti-selection and improving combined ratios.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & GDPR compliance costs | -0.4% | National, aligned with EU framework | Long term (≥ 4 years) |

| Claims-cost inflation (auto-repair parts & labour) | -0.8% | National, acute in urban centers | Short term (≤ 2 years) |

| Thin investment yields pressuring combined ratios | -0.5% | National, affecting all insurers | Medium term (2-4 years) |

| Growing cyber-risk aggregation limits re/insurance appetite | -0.3% | National, concentrated in financial centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Claims-cost inflation (auto-repair parts & labor)

Motor insurers face a squeeze as complex sensors in advanced driver-assistance systems and battery-electric drivetrains lift parts prices and workshop times. The German Insurance Association estimates motor-line outgo could exceed USD 38.15 billion for 2024, eroding underwriting margins. Supply-chain bottlenecks and labour shortages add further strain, prompting mid-single-digit premium hikes across the Germany property and casualty insurance market in 2025. Players with direct-repair networks and AI-guided damage appraisal reduce leakage, cushioning profitability.

Data-privacy & GDPR compliance costs

Expanding data capture from telematics and IoT raises compliance risks. Fines for GDPR breaches rose in 2024, and DORA now obliges all insurers to report major incidents within tight timelines. Meeting encryption, audit, and resiliency benchmarks diverts budget from front-office innovation. Smaller mutual insurers—significant players in the Germany property and casualty insurance industry- bear a disproportionate cost burden, which could narrow product variety in certain sub-regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Specialty lines outpace motor dominance

Motor generated 35.54% of Germany property and casualty insurance market share in 2025, underpinned by mandatory third-party liability and the country’s 49 million-plus registered vehicles. Yet, claims inflation forces tariff increases, driving consumers to telematics-based products. Specialty Lines, marine, aviation, and engineering, post a 12.86% CAGR, elevating their contribution to the Germany property and casualty insurance market size through 2031 as Germany expands offshore wind, airport modernisation, and semiconductor-fab construction. Insurers with technical-underwriting depth leverage global facultative reinsurance to capture this growth.

Insured sums for homeowners and commercial property benefit from potential compulsory flood cover. General liability persists as a mid-scale segment but grapples with rising social inflation stemming from collective-redress mechanisms. Accident and supplementary health under P&C regulation see renewed demand as employers expand voluntary benefits. Overall, players that blend usage-based motor offers with engineering and cyber-risk packages balance their risk mix across the Germany property and casualty insurance market.

By Distribution Channel: Brokers anchor complex business while digital accelerates

Brokers and independent agents controlled 44.02% of premiums in 2025. Their advisory depth proves critical for industrial fire, construction all-risk, and multinational programs, sustaining relevance despite fee compression. Direct & digital channels expand 10.88% annually, powered by API gateways that embed household and mobility coverage in e-commerce journeys. The Germany property and casualty insurance market size for broker-sold products still rises, yet its share will dilute gradually as embedded and affinity partners unlock new micro-ticket volumes. These shifts are also influencing the broader Germany life and non-life insurance market, where insurers increasingly adopt unified digital platforms to cross-sell life, health, and property products through integrated customer ecosystems.

Multi-access strategies dominate players roadmaps: virtual video-advice blends with chatbot self-service, while in-branch agents focus on life-event reviews. Bancassurance retains steady household-insurance cross-sales via mortgage portfolios. Affinity schemes with utilities and mobility platforms illustrate how the Germany property and casualty insurance market adopts retail pricing disciplines to lower distribution cost ratios.

By Customer Type: Corporate demand gains pace

Personal lines remained 63.12% of the premium in 2025. However, corporates register 7.18% CAGR as supply-chain fragility and cyber threats push German Mittelstand firms to higher cover limits. Captive reinsurance frameworks proliferate among large exporters, yet primary players still write fronting layers, enhancing the Germany property and casualty insurance market. SMEs remain under-insured, offering white-space for tailored property-business-interruption bundles.

Personal customers migrate to digital claims journey touchpoints, raising expectations for 24/7 status tracking. Corporate risk managers prioritise engineering risk surveys and climate-scenario analytics. As data quality improves, the Germany property and casualty insurance market leverages parametric products for weather-triggered payouts, especially in renewable energy and agri-supply chains.

By End-user Industry: Construction fuels growth

Construction & real estate contributed 55.06% of the premium in 2025 and grew 5.61% per year as Germany retrofits housing for energy efficiency and upgrades flood defenses. The Germany property and casualty insurance market size tied to infrastructure projects expands further if mandatory NatCat cover becomes law. Manufacturing is the second pillar, undergirded by robotics investments that require equipment breakdown and cyber endorsements.

Transportation & logistics benefit from e-commerce parcel volumes, raising demand for players and warehouse legal liability covers. Professional & financial services confront data-breach exposures, adopting blended cyber-liability and crime-insurance solutions. Public utilities and renewable-energy operators stimulate engineering and delay-in-start-up covers, adding diversity to the Germany property and casualty insurance market.

Geography Analysis

Westdeutschland generated 44.92% of premiums in 2025, anchored by North Rhine-Westphalia’s dense industrial base and Frankfurt’s financial hub. High-value commercial property schedules and business-interruption endorsements sustain premium density. Motor penetration is near-saturation, but specialty and cyber lines still lift overall growth for the Germany property and casualty insurance market in the region.

Ostdeutschland posts the quickest 5.52% CAGR as infrastructure upgrades, EV-battery-plant projects, and EU structural funds catalyse economic momentum. Lower historical insurance penetration provides headroom, and property-modernisation grants stimulate demand for multi-risk household policies. Regional insurers invest in agent networks and digital kiosks to capture first-time buyers in the Germany property and casualty insurance market.

Süddeutschland combines Bavaria and Baden-Württemberg, where convective-storm and flood exposure inflates property rates yet also spurs adoption of risk-mitigation devices. Norddeutschland’s maritime industries and offshore wind farms call for high-limit marine and engineering covers, enlarging the Germany property and casualty insurance market through specialised syndication capacity and facultative placements.

Competitive Landscape

Ten insurance groups collect roughly two-thirds of total premiums, signalling moderate concentration. Allianz leverages global economies of scale to drive sub-20% expense ratios and an API-centric direct unit across Europe. Munich Re combines primary insurer ERGO with its reinsurance engine, offering integrated facultative and treaty solutions that smaller players cannot replicate. Talanx positions HDI as a specialist for industrial and mid-market clients, capturing growth in renewable-energy construction.

Regional mutuals such as Versicherungskammer Bayern defend personal-lines share through dense agency footprints, while insurtech entrants build cloud-native policy-admin stacks and white-label products. Embedded-insurance orchestrators partner with retailers and mobility platforms to bypass legacy distribution, reshaping acquisition economics for the Germany property and casualty insurance market. BaFin’s proportional-supervision stance enables innovation while safeguarding solvency, evident in its swift intervention in ELEMENT Insurance AG’s 2025 insolvency.

Investment in AI-enabled underwriting accelerates. Munich Re’s Realytix Zero auto-builds personal-accident products in minutes, trimming product-development cycles and enabling micro-cover launches in niche affinity programs. Players pursuing similar toolsets widen cost advantages, intensifying competition across the Germany property and casualty insurance market.

Germany Property and Casualty Insurance Industry Leaders

Allianz SE

Munich Re (ERGO, Great Lakes)

Talanx Group (HDI, Hannover Re)

AXA Konzern AG

Generali Deutschland

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Allianz, BlackRock and T&D Holdings agreed to acquire Viridium Group for around USD 3.82 billion, adding 3.4 million policies

- March 2025: Generali Deutschland’s property and casualty unit improved its combined ratio to 89.7%, with an operating profit of USD 1.12 billion

- February 2025: BaFin opened final insolvency proceedings for ELEMENT Insurance AG, affecting roughly 320,000 contracts.

- December 2024: Barmenia-Gothaer merger projected 2024 premium income of USD 9.27 billion, elevating the combined group into Germany’s top-10 insurers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

The Germany property & casualty (P & C) insurance market, as framed by Mordor Intelligence, totals all gross written premiums booked inside Germany for motor, property, general liability, and specialty commercial lines, reported on a direct basis in euros and converted to U.S. dollars at the prevailing annual average.

Scope exclusion: reinsurance cessions, insurance-linked securities, stand-alone life or health contracts, and overseas branches are not counted.

Segmentation Overview

- By Insurance Type

- Motor

- Homeowners / Residential Property

- Commercial Property (incl. Fire & Multi-risk)

- General Liability

- Specialty Lines (Marine, Aviation, Engineering)

- Legal Expense

- Accident & Health (P&C regulated)

- By Distribution Channel

- Direct & Digital

- Tied Agents

- Brokers & Independent Agents

- Banks & Bancassurance

- Affinity & Embedded Partners

- Customer Type

- Personal Lines

- Commercial & SME

- Corporate & Industrial

- By End-user Industry

- Manufacturing

- Construction & Real Estate

- Transportation & Logistics

- Retail & Wholesale

- Professional & Financial Services

- Public Sector & Utilities

- By Region

- Norddeutschland

- Ostdeutschland

- Westdeutschland

- Süddeutschland

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held interviews with underwriting managers, multiline brokers, and regulatory observers in Germany, the Netherlands, and Switzerland. These conversations clarified tariff repricing, digital-channel uptake, and expected claim-cost inflation, sharpening the assumptions fed into our model.

Desk Research

Our team first extracted multi-year premium and claims statistics from BaFin insurance statistics, the German Insurance Association, Eurostat, and OECD. We blended these with economic markers such as consumer-price inflation, new passenger-car registrations, dwelling permits, and catastrophe loss tallies that we accessed through Destatis, EIOPA dashboards, and the EM-DAT disaster database. Company annual reports, Solvency II filings, and proprietary feeds from D&B Hoovers plus Dow Jones Factiva then helped us benchmark carrier level movements and validate channel shares. The sources listed are illustrative; numerous additional publications informed data collection, cross-checks, and research clarification.

Market-Sizing & Forecasting

We anchor the headline value using a top-down build that starts with BaFin gross premiums, adjusts for euro-to-dollar conversion, and strips non-P & C classes. Sampled carrier roll-ups and broker channel checks supply a bottom-up reasonableness test. Key drivers include motor-park growth, average premium per policy, property rebuild-cost inflation, weather-loss frequency, and corporate liability exposure; these feed a multivariate-regression forecast. Scenario analysis captures potential swings from major regulatory shifts or severe catastrophes, while gaps in bottom-up rows are bridged with historic loss-ratio averages.

Data Validation & Update Cycle

Outputs pass variance checks against BaFin monthly flashes, exchange-rate sensitivity tables, and a two-layer analyst review. Reports refresh each year, with interim updates when material events occur, ensuring clients receive our latest view.

Why Mordor's Germany Property And Casualty Insurance Benchmark Deserves Trust

Published figures often diverge because each firm chooses its own class mix, currency moment, and refresh cadence.

Differences in including specialty lines, handling outward reinsurance, or projecting premium uplift can quickly widen gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 95.41 B (2025) | Mordor Intelligence | - |

| USD 70.50 B (2024) | Global Consultancy A | Excludes motor liability and freezes premiums at 2023 tariffs |

| USD 82.67 B (2025) | Industry Data Service B | Counts only direct channels and locks EUR/USD at January 2024 rate |

| USD 67.09 B (2025) | Trade Journal C | Applies conservative scenario with no climate-related premium growth |

The comparison shows that our disciplined scope choices, live exchange conversions, and annual review cadence give decision-makers a balanced baseline that is transparent, traceable, and repeatable.

Key Questions Answered in the Report

What is the current size of the Germany property and casualty insurance market?

The Germany property and casualty insurance market size stands at USD 101.25 billion in 2026.

How fast is the Germany property and casualty insurance market expected to grow?

It is projected to expand at a 6.12% CAGR, reaching USD 136.32 billion by 2031.

Which insurance segment is growing the fastest in Germany?

Speciality lines such as marine, aviation and engineering are forecast to grow at 12.86% CAGR through 2031.

Which distribution channel is expanding most quickly?

Direct and digital channels are advancing at an 10.88% CAGR as consumers embrace online purchasing.

Page last updated on: